Sample Category Title

Sentiment In The US Dollar Improves. US Final GDP Awaited

The greenback managed to post some gains on the back of a better than expected durable goods orders report. Data showed that headline durable goods orders rose 1.7% on a month over month basis in August, beating expectations of a 0.9% increase. Investors were also positive on the U.S. dollar on the proposed tax overhaul which is expected to offer lower tax on corporate businesses and tax cuts on small businesses.

The RBNZ's meeting held yesterday saw the OCR being unchanged at 1.75% as widely expected. The RBNZ was seen lowering its GDP forecasts for the year ahead with the central bank likely preparing for a dovish forward guidance.

Looking ahead, the economic calendar today will focus on the final GDP revisions for the second quarter. According to the median estimates, the U.S. final GDP is expected to remain steady at 3.0%. The BoE Governor Carney is also expected to speak later today.

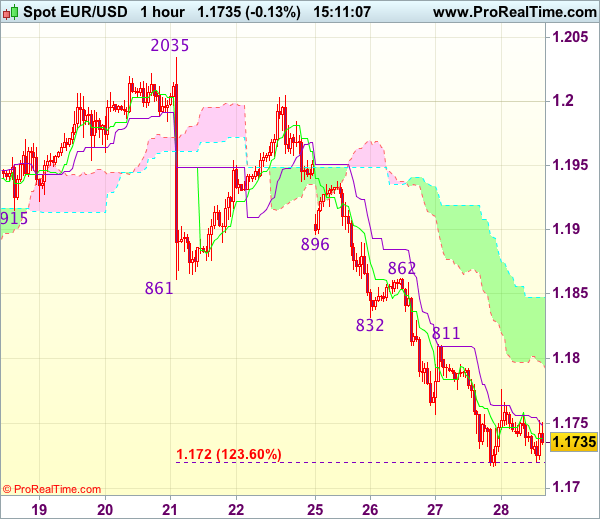

Trade Idea : EUR/USD – Sell at 1.1810

EUR/USD - 1.1756

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1739

Kijun-Sen level : 1.1749

Ichimoku cloud top : 1.1847

Ichimoku cloud bottom : 1.1796

Original strategy :

Sell at 1.1830, Target: 1.1720, Stop: 1.1865

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1810, Target: 1.1710, Stop: 1.1845

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after recent selloff, adding credence to our bearish view that the decline from 1.2093 top is still in progress and downside bias remains for further weakness to 1.1700, however, loss of downward momentum should prevent sharp fall below previous support at 1.1662 and reckon 1.1625-30 would hold, bring rebound later.

In view of this, we are looking to sell euro on recovery as resistance at 1.1811 should limit upside and bring another decline. Above previous support at 1.1832-38 (now resistance) should hold and bring another decline later. Above resistance at 1.1862 would abort and signal low is formed instead, bring a stronger rebound to 1.1896 (another previous support).

USDJPY Holding Onto Gains

The USDJPY pair continues to trade at an 11-week high around the 113 level, as Japanese politics and a stronger U.S dollar help to lift the pair. Japanese parliament was earlier dissolved in time for a snap election, which is widely speculated to be held on October 22nd.

Given the recent strength in the U.S dollar and the uncertainty surrounding the Japanese election, the expectation is for the USDJPY pair to remain bullish in intraday trading.

From a technical perspective, the USDJPY pair will remain strongly bullish, while trading above the former weekly price high, at 112.71.

A clear break above the current monthly high, at 113.25 should encourage USDJPY buying interest towards the July 14th swing high, at 113.57.

Key USDJPY technical support is currently located at 112.89 and the 112.71. Below 112.71 the pair risks further intraday losses towards 112.57 and 112.23.

To the upside, key intraday resistance above the current monthly price-high is found at 113.57 and 113.80. Above 113.80, price further resistance is found at 114.10 and 114.49.

.

GBPUSD Pair Remains Weak

The GBPUSD trades under the 1.3400 level, as Brexit negotiations with the EU remain deadlocked and the U.S dollar index continues to strengthen, after President Donald Trump proposed the biggest U.S. tax overhaul in three decades.

Sterling is expected to remain under further selling pressure while U.S fundamentals outweigh the United Kingdom's, while trading sentiment surrounding the greenback support further U.S dollar gains.

The GBPUSD pair has struggled to advance past the 1.3400 technical level during the Asian session, with price-action slipping further towards the currently weekly price-low.

Going forward, the GBPUSD pairs key 200-week moving average remains key, a move below the 200-week MA would signal further bearish losses for sterling

Key intraday support for the GBPUSD pair is found at 1.3360, 1.3340 and the key 1.3300 level. Below the 1.3300 level, the former yearly price high at 1.3268 acts as the foremost support.

To the upside, key GBPUSD technical resistance is found at the pairs daily pivot point, at 1.3400 and the 50-hour moving average at 1.3430. Above 1.3430, buying interest should accelerate towards 1.3444 and 1.3461.

.

Data-Dependent Traders Will Have Plenty To Talk About On Thursday

A deluge of economic data will make the rounds on Thursday, giving investors the latest insight into the Eurozone and US economies.

Market participants will be up bright and early for the release of the German consumer confidence survey, courtesy of GfK. The 06:00 GMT release is expected to show a slight increase in the confidence level of German consumers.

The European Commission's statistical agency will release a spate of sentiment indicators at 09:00 GMT, including services sentiment, consumer confidence, economic sentiment, business climate and industrial confidence. The September data sets are expected to confirm steady progress in the 19-member euro area.

Three hours later, Germany will release preliminary CPI data for the month of September. The consumer price index is forecast to rise 1.8% in the 12 months through September, unchanged from August.

Shifting gears to North America, the Labor Department kicks off Thursday trading with a weekly report on jobless claims. At the same time, the Department of Commerce will issue reports on the goods trade balance and second quarter GDP. The third and final estimate of gross domestic product is expected to show 3% annual growth between April and June, unchanged from the previous estimate.

Investors will also be busy keeping track of central bank speeches on Thursday. A pair of European Central Bank (ECB) policymakers are scheduled to speak, followed by Federal Reserve Governors Esther George and Stanley Fischer.

Fed officials are becoming increasingly hawkish on the prospect of a December interest rate increase. The hawkish posture has driven sharp gains in the US dollar, which once again proves the bizarre concept of “buying and rumour and selling the fact.” Between mid-2014 and January 2017, the US dollar index posted monstrous gains on the mere expectation that rates might rise one day. Now that rates have been hiked four times, it's no longer seen as a big deal.

EUR/USD

The euro got whacked again on Wednesday, falling to its lowest level in over a month. The EUR/USD exchange rate is trading around 1.1740, Prices are now eyeing the August low of 1.1661. Losing this level could prove catastrophic for the euro's bullish run.

GBP/USD

The British pound suffered another setback Wednesday, with prices falling below 1.34 US. Cable is currently in a four-day slump even as markets continue to price in a 2017 rate hike by the Bank of England. The GBP/USD faces immediate support at 1.3364. On the upside, immediate resistance is likely found at 1.3490.

USD/CAD

A dovish Stephen Poloz on Wednesday triggered another slide in the Canadian dollar, with the USD/CAD climbing to one-month highs. The pair has gained another 0.1% on Thursday and is up a whopping 400 pips since 8 September. The next major resistance is 1.2464, which is the 50-day moving average.

Euro At Risk Of Further Declines Vs British Pound

Key Highlights

- The Euro started a downside move from the 0.9280 swing high and now trading below 0.8800 against the British Pound.

- There is a key bearish trend line forming with resistance at 0.8780 on the 4-hours chart of EUR/GBP.

- Germany’s GfK Consumer Confidence in Oct 2017 is forecasted to decline from 10.9 to 10.8.

- The US Gross Domestic Product report will be released for Q2 2017, and the GDP is forecasted to rise 3% (Annualized).

EURGBP Technical Analysis

The Euro started a major downside move from the 0.9280-90 levels against the British Pound. The EUR/GBP pair is already down more than 400 pips and looks set to break 0.8740.

The 4-hours chart of EUR/GBP clearly points a downtrend from well above 0.9250. The pair broke many support levels recently, including 0.9000, 0.8900 and 0.8850. There was even a close below 0.8800 and the 100 simple moving average (H4).

The pair recently traded as low as 0.8746 and is currently correcting higher. On the upside, there is a key bearish trend line forming with resistance at 0.8780 on the 4-hours chart.

An initial resistance is around the 23.6% Fib retracement level of the last decline from the 0.8885 high to 0.8746 low. As long as the pair is below 0.8800, it might decline further. Alternatively, a close above 0.8800 could push the pair towards 0.8850-60.

Germany’s GfK Consumer Confidence

Today in the Euro Zone, the German GfK Consumer Confidence for Oct 2017 was released. The forecast was slated for a minor rise from the last reading of 10.9 to 11.0.

The actual result was below the forecast, as there was a decline from 10.9 to 10.8. According to the report, both income expectations and propensity to buy decreased in September and thus GfK forecasts a decline in the consumer climate index from 10.9 to 10.8.

The report added that:

After the setback of the preceding month, income expectations in September stabilized and increased moderately. With an increase of 3 points, the indicator compensates for part of the decrease from August. It currently stands at 33.4 points. The indicator’s clear increase of 26.6 points in comparison with the preceding year can also be viewed as a clear indicator for the continuing positive economic sentiment.

The result is slightly negative and brings no hope for EUR/GBP, and that’s why any major recoveries remain capped near 0.8780-0.8800.

Economic Releases to Watch Today

US Initial Jobless Claims – Forecast 270K, versus 259K previous.

US Core Personal Consumption Expenditure for Q2 2017 (QoQ) – Forecast +0.9%, versus +0.9% previous.

US Wholesale Inventories for August 2017 (preliminary) – Forecast +0.4%, versus +0.6% previous.

US Gross Domestic Product Q2 2017 (Annualized) – Forecast 3% versus previous 3%.

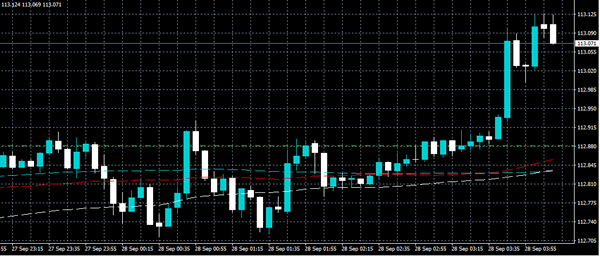

Trade Idea : USD/JPY – Stand aside

USD/JPY - 113.05

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 112.96

Kijun-Sen level : 112.82

Ichimoku cloud top : 112.20

Ichimoku cloud bottom : 112.01

Original strategy :

Exit long entered at 112.65,

Position : - Long at 112.65

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback has staged a strong rebound after yesterday’s retreat to 112.38, break of this week’s high at 113.26 is needed to revive bullishness and signal recent upmove has resumed, then further gain to previous resistance at 113.58 would follow but loss of upward momentum should prevent sharp move beyond 113.75-80 and reckon 114.00-10 would remain intact, bring correction later.

In view of this, would not chase this rise here and would be prudent to stand aside. Below 112.70 would prolong consolidation and bring another retreat to 112.38, however, only a drop below this support would signal top has been formed, bring retracement of recent rise to the lower Kumo (now at 112.01) and then towards 111.75-80 but support at 111.47 should remain intact.

Forex: US & UK Rate Hikes Likely

The US economy's strength was underlined on Thursday with the release of US Durable Goods Orders for August that beat all estimates coming in at 1.7%. Markets had been expecting an improvement from the previous release of -6.8% to 1%. The strong release also negated the effects of the recent Hurricanes, which were expected to drag on Q2 growth. In addition, Core capital goods orders surged 3.3% year-on-year. With signs of increased business spending, the likelihood of a December rate hike looks ever more certain. The latest CME FedWatch tool rose to 83% from 72% on Monday on the likelihood of a December hike in rates.

The Trump Administration, and Republicans, unveiled their Tax Reform Plan to Congress. Changes in personal taxation and, more importantly, a huge reduction in corporation tax from 35% to 20% will help speed along US economic growth through capital & consumer spending. A repatriation of overseas assets is also part of the reform. This would allow US companies that hold in excess of $2.5 Trillion in profits overseas to repatriate this money back to the US at a significantly reduced tax rate – and not the current 35% corporate tax on earnings. Bear in mind, this is a “blueprint” that appears to leave out many details and will require a large amount of new legislation if, indeed, it gets passed. Trump is desperate for a “win”, as all of his previous plans have failed to be enacted, although many believe enacting this plan will face many hurdles.

The Bank of England's Chief Economist, Andy Holdane, commented on Wednesday that he saw encouraging signs of pay growth in the UK and that any increase in UK interest rates should be seen as a “good news story” for Britain's economy. He also stated, “In the September minutes in particular, a majority of the committee – of which I am one – said we could be nearing the point where a reduction in some degree of monetary stimulus might be warranted in the coming months”. The markets believe a hike in UK rates could come after the Bank of England November 2nd meeting, with suggestions of a 0.25% hike to 0.5%.

EURUSD remains weak but is holding above 1.1700 to currently trade around 1.1740.

USDJPY improve 0.2% in early Thursday trading to currently trade around 113.00.

GBPUSD is little changed overnight, currently trading around 1.3390.

Gold continues to suffer from overall USD strength. Currently, Gold is down 0.2% in early Thursday trading at $1280.

WTI has declined 0.3% overnight to currently trade around $52.00pb.

Major economic data releases for today:

At 07:35 BST, Bank of Japan Governor Haruhiko Kuroda will hold a press conference about monetary policies in Tokyo.

At 09:15 BST, Bank of England Governor Carney speaks. The markets will be scrutinizing his speech for clues regarding future monetary policy. His comments have been known to initiate GBP volatility.

At 13:30 BST, the US Bureau of Economic Analysis, Department of Commerce will release Core Personal Consumption Expenditures (QoQ) (Q2). Consensus is suggesting an unchanged release of 0.9%. Any release that is substantially different will result in USD volatility.

At 14:30 BST, the US Bureau of Economic Analysis will release Gross Domestic Product Annualized (Q2). Consensus forecasts suggest an unchanged rate of 3%.

Market Update – Asian Session: Equities Follow US Lead, USD Strengthens Asia Summary

Asia Summary

Asian equity markets opened mixed, generally following the lead of US markets. Hong Kong property names were weaker on another Chinese city adding property curves. Financial names gained on US yields rose overnight. Analysts note that Q4 volatility in China is likely to be subdued with efforts to keep markets stable ahead of Communist Party gathering on Oct 8th. RBNZ left rates unchanged as expected, noting that weaker currency is best for dealing with tradables inflation. Japan PM Abe dissolved lower house to make way for snap elections.

USD strength in the session attributed to Trump’s confirmation of proposed tax plan. USD/JPY rose giving some support to the Nikkei which opened +0.7%. The USD/KRW fell for a 3rd consecutive day, with North Korea continuing to weigh. In Japan weekly portfolio data, foreign investors sold a record amount of Japan assets, ¥3.41T, the most since mid-June. In Hong Kong, the 1-week HK$ HIBOR rose 15bps to 0.57786%, a fresh 2017 high.

Key economic data

(NZ) NEW ZEALAND CENTRAL BANK (RBNZ) LEAVES OFFICIAL CASH RATE (OCR) UNCHANGED AT 1.75%; AS EXPECTED

(CN) CHINA AUG SWIFT GLOBAL PAYMENTS (CNY): 1.94% V 2.00% PRIOR

(KR) South Korea Sept CPI m/m: 0.1% v 0.2%e; y/y: 2.1% v 2.2%e; Core y/y: 1.6% v 1.7%e

(AU) Australia Jun- Aug Job Vacancies: 6.0% v 3.3% prior (highest on record for quarter)

Speakers and Press

China/Hong Kong

(CN) China State Council chaired by Premier Li: Will further bolster its small and micro businesses with more financial measures to increase vitality of the economy – Xinhua

(CN) China State-owned Assets Supervision and Administration Commission (SASAC) Planning 3rd phase of SOE mixed-ownership pilot

Korea

(KR) North Korea (DPRK): joint declaration issued a decade ago with South Korea on realizing peaceful national reunification "clarified the practical ways for building trust between the north and the south

(KR) South Korea to allow tax deferment to companies impacted by Thaad; to offer cheap loans to car component markers impacted by China measures

(KR) South Korea Fin Min Kim: Growth is firm despite North Korea risk

Japan

(JP) Japan considering lowering leverage limit for FX trades on grounds that both retail and institutional investors are facing greater risks should the market face sudden fluctuations – Nikkei

(JP) S&P Analyst: Japan PM Abe's announcement to defer the FY20 primary budget balance goal will not affect S&P's credit rating for Japan

(JP) Japan PM Abe: Election will be a fight over developing Japan's future

US/Europe

(US) Fed's Rosengren (moderate, non-voter): Does not offer clue on rate hike timing

(UK) BOE's Haldane (chief economist): Was part of MPC majority that felt a reduction in monetary stimulus may be warranted in the coming months - UK press

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.5%, Hang Seng -0.4%; Shanghai Composite -0.1%, ASX200 +0.1%, Kospi -0.1%

Equity Futures: S&P500 -0.0%; Nasdaq100 +0.0%, Dax +0.0%, FTSE100 -0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1756-1.1727; JPY 113.09-112.71; AUD 0.7856-0.7816;NZD 0.7233-0.7187

Dec Gold -0.3% at $1,284/oz; Nov Crude Oil -0.3% at $51.97/brl; Dec Copper -0.3% at $2.92/lb

GLD SPDR Gold Trust ETF daily holdings +0.3% to 864.7 metric tonnes

(CN) PBOC OMO: injects CNY70B in 14 and 28-day reverse repos v skips prior; drains net CNY0B v CNY40B prior

USD/CNY (CN) China PBOC sets yuan reference rate at 6.6825 v 6.6192 prior

(JP) Bank of Japan (BOJ) to accommodate T+2 JGB settlement for foreign central banks

(JP) Japan MoF sells ¥816.9B in 3-month bills; avg yield -0.1652%; bid-to-cover 4.46x\

(JP) Japan MoF sells ¥1.80T v ¥2.2T indicated in 0.1% 2-yr JGBs; avg yield -0.1190%; bid-to-cover 4.11x v 4.97x prior (lowest bid-to-cover since March)

Equities notable movers

Australia/New Zealand

OEL.AU Gives independent reserves report for the SM 71 project; +17.5%

SHJ.AU Receives statement of claim for class action; -13.5%

Japan

9064.JP Amazon has agreed to pay Yamato at least 40% more for shipping services in Japan – Nikkei; +4%

8028.JP Raises H1 guidance Net ¥23B from ¥14B; Op ¥33.5B from ¥24.6B; Rev ¥633B from ¥628.1B, +8.8%

Hong Kong/China

Hong Kong property sector weaker on additional city adding cooling measures: 884.HK -3.8%, 1030.HK -3.3%

Currencies: Higher US Yields Support USD Comeback

Sunrise Market Commentary

- Rates: Reflation trade back in the driver's seat

Investors fell back under the spell of reflationary spirits after US President Trump announced details of his tax reform proposal. Core bond yield curves bear steepened and the US Note future loses more ground overnight. We expect more bond losses today, especially in case of higher than expected German inflation data. - Currencies: Higher US yields support USD comeback

The reflation trade supported the dollar yesterday. There are plenty of eco data today, but they probably won't change the broader picture. The USD rebound might take a breather, but higher US yields should provide a solid floor for the US currency.

The Sunrise Headlines

- US stock markets gained around 0.4% yesterday with Nasdaq outperforming (+1.15%). Equities benefit together with the dollar from revived reflationary bets. Overnight, Asian risk sentiment is more mixed.

- US President Trump presented Republican's proposition for tax reforms including lower taxes on corporate profits, incentives for business investment, fewer and lower individual income tax brackets and the end of estate taxes.

- Bank of England Chief Economist Haldane said he saw encouraging signs of pay growth and any increase in interest rates should be seen as a "good news story" for Britain's economy.

- St. Louis Fed Bullard said "the current level of the policy rate is appropriate" given the economy and the fact that inflation "has surprised to the downside." But Boston's Fed Rosengren said the central bank should raise rates in a "regular and gradual" way despite low inflation.

- New Zealand's central bank kept its policy rate at 1.75% and hinted at a lower growth outlook as a long construction boom loses momentum and against the backdrop of political uncertainty from an inconclusive national election.

- The Canadian loonie extended its losses against the US dollar after Bank of Canada governor Poloz said the central bank that will proceed “cautiously” with any additional rate rises.

- The eco calendar contains EMU EC confidence data, German inflation, US weekly claims and the final US Q2 GDP reading. Several central bankers speak and Italy & the US tap the bond market.

Currencies: Higher US Yields Support USD Comeback

Dollar rebound gains momentum

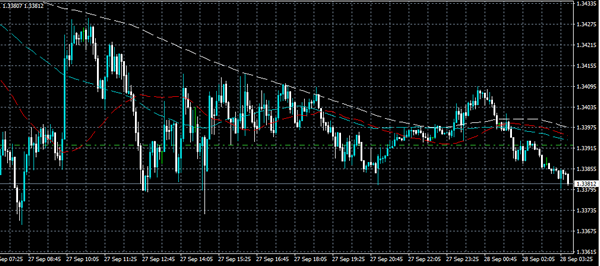

European investors kick-started an new phase in the reflation trade yesterday. Yellen's confirming the Fed's intention to normalize policy, the prospect of a US tax reform and good eco data added to the overall positive sentiment. The dollar also profited. The break of EUR/USD below 1.1823 is confirmed. EUR/USD finished the session at 1.1745. USD/JPY temporary regained the 113 big figure, but closed at 112.84.

Asian equities show again a mixed picture. Japanese equities profit from the rise of the dollar/decline of the yen. USD/JPY trades again in the 113 area. A further rise of US bond yields overnight suggests that the dollar might continue to enjoy interest rate support. The impact of a rising dollar and higher US yields on other Asian/EM markets is mixed. EUR/USD (1.1735 area) holds within reach of yesterday's correction low. The rise of the oil price has halted, but with no direct impact on the dollar.

Today, the EC economic confidence survey is expected to show minor gains (112 versus 111.9). We put the risks to the downside, but the decline shouldn't be dramatized. The German September HICP inflation is probably more important for markets. The consensus expects a 0.1% M/M rise. The Y/Y reading is expected at 1.9% from 1.8%. We join the consensus, but any deviation, especially on the upside, might affect core bonds. The US eco data are less in interesting. The final Q2 GDP is expected unrevised at 3%, jobless claims might still be distorted by the hurricanes. The trade deficit is expected to have widened, but Q3 trade is still likely to add positively to Q3 GDP. There are lots of ECB and Fed speakers, but we don't expect them to rock the boat. Recent Fed talk indicated that the Fed wants to hike rates again in December en in 2018, unless data surprise.

Yesterday, the dollar rebound continued, making the overall picture for the US currency more solid. The Trump administration indeed announced a ‘bold' tax plan, but plenty of details (including the financing) have still to be worked out. So, the positive impact from this theme might gradually fade. Today's US data won't be than important, but a further trend-rise in US yields might keep the downside of the dollar protected. Higher German inflation might support the overall reflation trade and shouldn't be that negative for the overall USD performance. The dollar rebound might slow/take a breather today, but we expect the trend to persist.

From a technical point of view EUR/USD hovered in a consolidation pattern between 1.1823 and 1.2070. It took time for the pair to break below the 1.1823 range bottom, but the break occurred earlier this week yesterday. The rise in US yields looks more solid and so does the rebound of the dollar. This week's price action is growing more encouraging for USD bulls. Next support in EUR/USD comes in 1.1662.

The day-to-day momentum in USD/JPY was constructive recently, but it was primarily due to yen weakness. USD/JPY regained the 110.67/95 previous resistance, a short-term positive. The 114.49 correction top is the next important reference. The cross rate remains sensitive to changes in overall risk sentiment.

EUR/USD correction continues as break below 1.1823 is confirmed

EUR/GBP

Sterling rebound against the euro slows.

There are tentative signs that the sterling rebound is losing momentum. EUR/GBP yesterday still touched a minor new correction low in the mid 0.87 area, but this move was due to the EUR/USD decline. The overall rise of the dollar also kept cable under pressure. The sterling support from very strong CBI retail data proved temporary. EUR/GBP closed at 08774, off the intraday lows. Cable closed the session at 1.3387. In an interview, BoE's Haldane said that a rate hike would be good news as it shows that the economy is healing.

There are no important eco data on the UK agenda today. Markets will keep an eye on the BoE Independence conference in London. On Brexit, there are rumours that the EU is considering small concessions and start talking on the transition period. This might be slightly sterling supportive, but we don't expect a big impact on sterling. It already made a nice rebound of late. We have to impression that the decline of EUR/GBP is losing momentum. The rise of the dollar sent cable in downward correction.

EUR/GBP made an impressive uptrend from April to set a MT top at 0.9307 late August. UK price data amended the dynamics and hawkish BoE comments reinforced a sterling rebound. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of euro strength and sterling softness to persist. However, the prospect of (limited) withdrawal of BOE stimulus put a solid floor for sterling ST term. We look how far the current correction goes. EUR/GBP is nearing support at 0.8743 and 0.8652, which we consider difficult to break. We gradually look to by EUR/GBP on dips.

EUR/GBP: downtrend show tentative signs of slowing.