Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.15; (P) 111.40; (R1) 111.82; More...

Intraday bias in USD/JPY remains on the upside and rise from 107.31 is still in progress. Further rally would be seen to medium term channel resistance (now at 112.91). Sustained break there will argue that whole correction from 118.65 has completed too. In that case, further rise should be seen to 114.49 resistance for confirmation. On the downside, break of 109.54 support is needed to indicate completion of the rebound. Otherwise, outlook will stay cautiously bullish in case of retreat.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

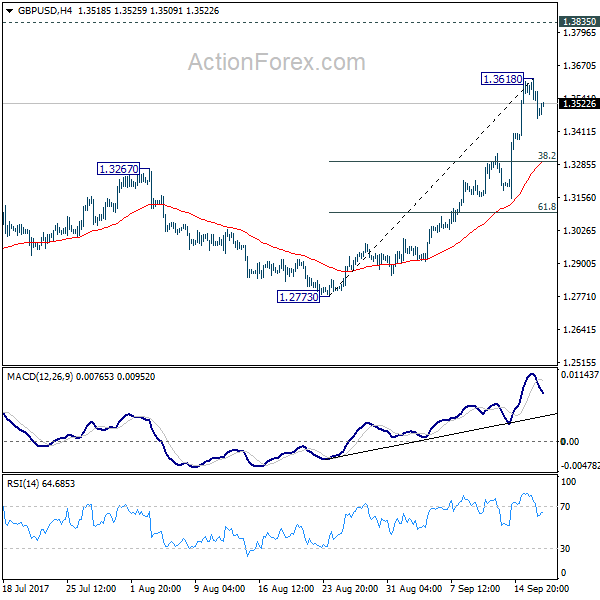

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3435; (P) 1.3526; (R1) 1.3589; More....

A temporary top is formed at 1.3618 in GBP/USD. Intraday bias is turned neutral for some consolidation first. Downside of retreat should be contained by 38.2% retracement of 1.2773 to 1.3618 at 1.3295 and bring rise resumption. Above 1.3618 will turn bias back to the upside for 1.3835 support turned resistance next. Break there will target 55 month EMA (now at 1.4405).

In the bigger picture, the strong break of 1.3444 key resistance now argues that the long term trend in GBP/USD has reversed. That is a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.

BoE Carney Tamed Rate Speculations, So Did BoC Lane

Risk appetite continued to drive US indices to new records higher overnight. DOW gained 63.01 points, or 0.28% to close at 22331.35. S&P 500 rose 3.64 points or 0.15% to 2503.87. Both were at new records. 10 year yield also gained 0.027 to 2.229. Traders continue to raise their bet on a December Fed hike, with over 57% chance as indicated by fed fund futures. But the Dollar is not getting much support yet. Markets will have their eyes on tomorrow's FOMC decision on balance sheet normalization, and the post meeting press conference first. Meanwhile, Sterling and Canadian Dollar are both talked down mildly by respective central bank officials. Yen and also stays weak in risk seeking environment. In other markets, Gold is extending recent pull back and is pressing 1310. WTI crude oil continues to struggle around 50.

Sterling retreats mildly as BoE Carney sounded cautious

Sterling retreats mildly and continues to digest recent sharp gain. BoE Governor Mark Carney sounded cautious in his speech at the IMF overnight. He reiterated that interest rates may rise "within months" in reaction to surging prices. But he emphasized that "any prospective increases in Bank Rate would be expected to be at a gradual pace and to a limited extent". Meanwhile, Carney described Brexit as an example of "deglobalization". And "the de-integration effects of Brexit can be expected... to be inflationary." He pointed out that lower immigration to the UK may boost domestic wage growth. Also, new trade barriers would lead to higher prices for goods and services. Meanwhile, the economic impacts of Brexit are subject to "tremendous uncertainty" in terms of scale and timing.

BoC Lane warned protectionists not to "turn back the clock"

Speaking to a business audience, BoC Deputy Governor Timothy Lane warned that rising protectionism is clouding the outlook of the Canadian economy. He pointed out that "the possibility of a material protectionist shift -- particularly regarding the outcome of negotiations on possible changes to NAFTA -- is a key source of uncertainty for Canada's economic outlook." He admitted that some workers were "left behind" because of trade and innovations. But policy makers should help workers in the transitions rather than seeking to "turn back the clock". Regarding recent rate hikes and appreciation of exchange rate, Lane said BoC will be "paying close attention to how the economy responds to both higher interest rates and the stronger Canadian dollar." And, going ahead, "each decision is a live decision". What Lane suggested was not to take a hike at every BoC meeting for granted.

RBA talked jobs, Aussie, iron and household debt in minutes

The RBA minutes for the September meeting contained little news. Four main areas of discussions include employment situation, Australian dollar, iron prices and the balance of household debt and low inflation. Policymakers acknowledged the improvement in the employment market, noting higher participation rate and steady unemployment rate. RBA appeared less worrisome about Aussie's strength. By attributing the appreciation of the Australian dollar to USD's weakness, it appears less likely that RBA would take actions to curb its strength. RBA expected iron ore prices to fall amidst new supply. As the biggest exporter of iron ores, Australian dollar has been affected by the movement in iron ore prices. More in RBA Minutes: More Confident Over Job Market, Less Action Against Rising Aussie.

On the data front

New Zealand Westpac consumer confidence dropped to 112.4 in Q3. Australia house price index rose 1.9% qoq in Q2. German ZEW economic sentiment is the main feature in European session. Eurozone will also release current account. Later in the day, US will release housing starts and building permits, current account and import price. Canada will release manufacturing shipments.

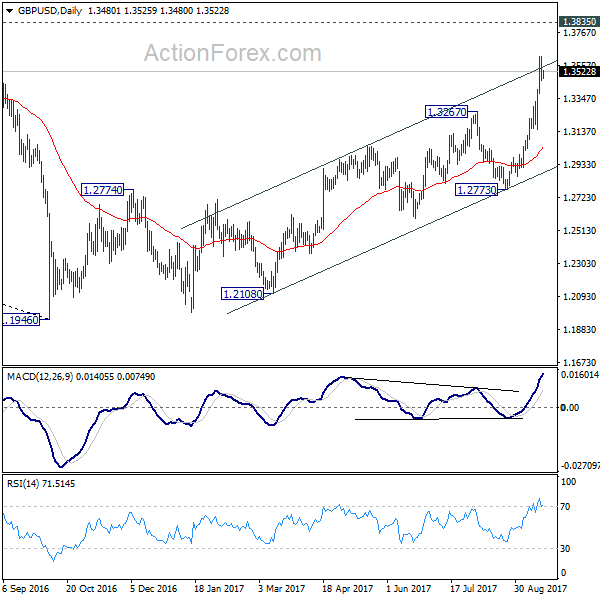

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3435; (P) 1.3526; (R1) 1.3589; More....

A temporary top is formed at 1.3618 in GBP/USD. Intraday bias is turned neutral for some consolidation first. Downside of retreat should be contained by 38.2% retracement of 1.2773 to 1.3618 at 1.3295 and bring rise resumption. Above 1.3618 will turn bias back to the upside for 1.3835 support turned resistance next. Break there will target 55 month EMA (now at 1.4405).

In the bigger picture, the strong break of 1.3444 key resistance now argues that the long term trend in GBP/USD has reversed. That is a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | NZD | Westpac Consumer Confidence Q3 | 112.4 | 113.4 | ||

| 1:30 | AUD | House Price Index Q/Q Q2 | 1.90% | 1.30% | 2.20% | |

| 1:30 | AUD | RBA Meeting Minutes Sep | ||||

| 8:00 | EUR | Eurozone Current Account (EUR) Jul | 22.3B | 21.2B | ||

| 9:00 | EUR | German ZEW (Economic Sentiment) Sep | 12 | 10 | ||

| 9:00 | EUR | German ZEW (Current Situation) Sep | 86.3 | 86.7 | ||

| 9:00 | EUR | Eurozone ZEW (Economic Sentiment) Sep | 32.4 | 29.3 | ||

| 12:30 | CAD | Manufacturing Shipments M/M Jul | -0.70% | -1.80% | ||

| 12:30 | USD | Current Account Balance (USD) Q2 | -113B | -117B | ||

| 12:30 | USD | Housing Starts Aug | 1.18M | 1.16M | ||

| 12:30 | USD | Building Permits Aug | 1.22M | 1.23M | ||

| 12:30 | USD | Import Price Index M/M Aug | 0.40% | 0.10% |

RBA Minutes: More Confident Over Job Market, Less Action Against Rising Aussie

The RBA minutes for the September meeting contained little news. Four main areas of discussions include employment situation, Australian dollar, iron ore prices and the balance of household debt and low inflation. Policymakers acknowledged the improvement in the employment market, noting higher participation rate and steady unemployment rate. RBA appeared less worrisome about Aussie's strength. By attributing the appreciation of the Australian dollar to USD's weakness, it appears less likely that RBA would take actions to curb its strength. RBA expected iron ore prices to fall amidst new supply. As the biggest exporter of iron ores, Australian dollar has been affected by the movement in iron ore prices.

Employment

RBA acknowledged the broad-based improvement in the employment market. The members also noted that full-time employment had 'risen strongly over the preceding year (even though it had declined in July) and had outpaced the growth in part-time employment over that period'. The members believed that trend of solid growth should continue. The central bank was also aware of the slow increase in wages, suggesting that low growth in wages and inflation should stay 'for some time'. Yet, they believed there would be 'a gradual increase' in wage and inflation as 'the spare capacity in the labour market was reduced and the economy continued to strengthen'.

Household Debt vs Low Inflation.

Low wage growth in light of a prosperous housing market has, however, posed the risks of 'growth in housing debt having outpaced the slow growth in household incomes'. RBA's monetary policy strategy should focus on balancing such risk.

Australian Dollar

The central bank softened its tone over Aussie's strength. As noted in the minutes, the members suggested that 'the appreciation of the Australian dollar over the course of 2017 had, in large part, reflected a broadly based depreciation of the US dollar'. This implies a shift of focus to Fed's monetary policy stance and the US economic growth outlook. The Fed is widely expected to make formal announcement of the balance sheet normalization plan at this week's meeting.

Iron Ores

Iron ores prices have rallied more than +30% over the past three months. Most the strength is driven by front-loaded demand for steel production as China is about to curtail the steel capacity in winter. As RBA noted in the minutes, iron ore prices should decline in the period ahead due to rising supply and peaking of Chinese steel production.

Market Morning Briefing: A Bit Of Profit-Taking In The Pound

STOCKS

Almost all indices look positive and bullish for the week except Shanghai which could possibly remain stable.

Dow (22331.35, +0.28%) could test 22400-22600 levels in the near term and Dax (12559.39, +0.32%) looks potentially bullish on the 3-day candle chart having a fair chance of moving up towards 12800 while above 12400. Thereafter a corrective fall from 12800 could be expected. Also note some rejection could come from levels near 12650 which is a decent resistance below 12800.

Nikkei (20197.56, +1.45%) also looks bullish just now and could test 20500-20800 before coming off from there. Note that for the long term 21000 is a crucial resistance and we do not expect a break above that in the coming weeks. Rejection from 20800-20700 looks more likely.

Shanghai (3357.05, -0.17%) is also potentially bullish to stable while above 3350. Only on a break below 3350, we may look at lower levels of 3325-3300. For now, while 3350 holds, the index could move up towards 3375-3390 again. has bounced back from levels near 3350 and while that holds, we may see a rise towards 3400 in the near term. A break below 3350, if seen could take the index lower towards 3325. Need to watch price action at current levels.

Nifty (10153.10, +0.67%) is all set to hit new highs near 10200-10300 levels in the coming sessions. But note on a longer term there could be a sharp fall on the index from levels below 10400-10300. For the near term, the index has some more room on the upside.

COMMODITIES

Commodities are all mixed. Precious metals look bearish over the next couple of sessions while Crude prices may remain stable. Copper looks bullish for the coming sessions.

Brent (55.39) has immediate resistance near 56-57 region and could come off from these levels in the near term, again targeting levels near 55-54 in the coming sessions. A break above 56 could take it higher towards 56.65 but chances seem less just now.

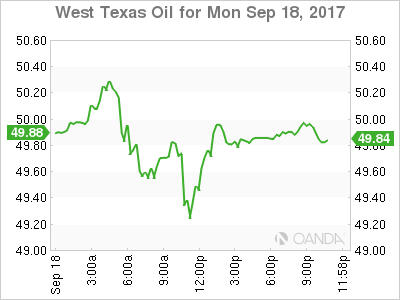

WTI (49.87) is likely to consolidate sideways within 50.50 and 49.10 for a few sessions. Support near 49 is holding well for now.

Gold (1308.29) and Silver (17.18) are down as expected. Gold could test 1296 over today and tomorrow before again attempting a bounce above 1300. Silver could come off towards 17.00 in the near term.

Copper (2.9680) has bounced a bit from support near 2.95 and while that holds, the price could rally towards 3.05 in the near term.

FOREX

Although the Euro (1.1965) and Aussie (0.7965) retain their uptrend, we need to watch their Supports. This is the inverse of the Dollar Index (91.96) which remains in a downtrend, but we need to watch the Resistance at 92.50.

Yesterday's reading remains valid on the Euro (1.1965) that "Two possibilities from here - either further sustained rise past 1.2035-50, or range trade between 1.2000 and 1.1850. The first three days may be quiet, waiting for the FOMC on Wednesday." Note though, that the overall uptrend remains in force while above 1.1850.

A bit of profit-taking in the Pound (1.3515) after a new high of 1.3619 was seen yesterday. Slightly greater chances now of a further dip towards 1.3450. Importantly, there are some chances of long-term Resistance at 1.38.

Increasing chances that Dollar-Yen (111.55) may rise further towards 113.50 over the next couple of weeks. The way to the upside is being cleared by the rise in Euro-Yen (133.45) well above 133.

Need to watch Support at 0.7960-50 on the Aussie (0.7965) which has not been able to build on its rise above 0.80 so far. Still, the uptrend remains valid while the Support holds. But needs to be watched carefully.

Dollar-Yuan (6.5917) has risen past 6.5750 and is within kissing distance of 6.60. Dollar-Rupee (64.13/14) might test 64.20 again. Need to see if that holds or not. Be careful there, the tide could just be turning.

INTEREST RATES

Minor uptick in German yields (10Yr 0.45%, up from 0.44% and 30Yr 1.25%, up from 1.23%). This is counterbalanced by the rise in the US 10Yr (2.22%, up from 2.20%), keeping the 10Yr German-US Spread (-1.77%) steady. This is the crucial variable to watch. A fall below -1.79% could weaken the Euro.

The US Yield Curve has been flattening over the last one week. However, we note a crucial Support near the current level (0.98%) on the 30-5 Yr Spread.. A bounce from here would lead to Curve steepening, suggesting chances of an interest rate hike ahead.

Resistance are holding on UK Gilts, at 1.30% on the 10Yr (1.30%) and 0.75% on the 5 Yr (0.73%). If the FOMC hints at a rate hike, the Pound could see profit-taking. A hint on the other side (delay in rate hike) could push the Pound up towards 1.38.

The Japanese 10Yr (0.03%) is dipping again within its overall downtrend, suggesting decent chances of further rise in the Dollar-Yen towards 113.50.

Over to the FOMC tomorrow and the BOJ on Thursday.

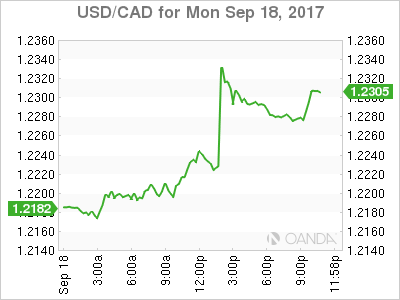

USD/CAD Canadian Dollar Lower As Fed Week Begins

The Canadian dollar fell on Monday after the US dollar is trading near the 1.23 price level. The September Federal Open Market Committee (FOMC) meeting kicks off on Tuesday and the market expects that when it ends on Wednesday the US central bank will have officially launched its balance sheet reduction initiative. The fixed income market is also eyeing a higher than 50 percent chance of a US rate hike in December.

Bank of Canada (BoC) Deputy Governor Timothy Lane was the first official to speak after the surprise rate hike in September. The Canadian central bank pivoted from a slightly dovish rhetoric until another Deputy Governor, Carolyn Wilkins spoke about the need to remove some stimulus. The comments were followed by Governor Stephen Poloz and the market got onboard with the rate hike announced in July. Policy makers were quiet since then and while the decision to raise interest rates were not a shock, specially considering the rapid pace of growth of the Canadian economy, the lack of warning from the central bank was an issue with market analyst.

Deputy Governor Lane said that the BoC will monitor how the economy responds to a higher interest rate and a stronger loonie. NAFTA was also addressed by the policymaker on the same day that US Trade envoy Robert Lighthizer said negotiations were moving quickly. Both Mexico and the United States want a fast resolution to the trade deal renegotiation to avoid it creating a political quagmire with upcoming 2018 elections in both countries.

Mexico’s Economy Minister expects the future of the agreement to hinge on trade deficits and rules of origin which will be discussed on the third round of negotiations to take place in Canada at the end of September.

The USD/CAD rose 0.876 percent on Monday. The currency pair is trading at 1.2298 as the USD recovered ahead of the end of the September Federal Open Market Committee (FOMC) on Wednesday. The Fed funds rate futures trading prices are pointing to a rising probability of a rate hike in December, but the move will be dependant on economic indicators release between now and then. The September monetary policy meeting was earmarked by the market early on as the one where the Fed would announce the start of its balance sheet reduction. With so much room to operate given the massive amount of funds accumulated during its QE program, the Fed has wiggle room and both hawks and doves within the FOMC welcome the initiative.

A rate hike in the United States is not as clear cut. Minnesota Fed President Neil Kashkari has become the major dove talking against another rate hike citing weak inflation. GDP growth has surprised to the upside, but inflation and retail sales remain soft and could push the December rate hike into next year, and probably into the mandate of a yet to be named Fed Chair after Fed Chair Janet Yellen’s term expires in February.

The September rate hike in Canada leaves the interest rate back to 1.00 percent, the same level it had in 2015 before the BoC had to proactively cut its rate twice to shield the economy from falling oil prices. The central bank is convinced the economy is strong enough to remove that stimulus, but the strong growth and comments on the strong currency being a reflection of the economy could lead to another rate hike this year

US energy prices are flat at 0.024 percent in the last 24 hours. The price of West Texas Intermediate is trading at 49.81 as energy is trading at a tight range at the top of the week. Seasonal maintenance has reduced demand for crude and stopped the oil rally in its tracks following the impacts of Hurricane Harvey and Irma.

While the Organization of the Petroleum Exporting Countries (OPEC) production cut agreement has managed to stabilize the price of oil, it has failed to spark a sustained recovery of prices. The $50 price level has been a hard one to crack and trade above consistently. US crude inventory reports will continue to show the impact of natural storms, but those effects should be worked out sooner rather than later. Energy markets will continue to trade on the assumption of a larger supply despite disruptions still creating a glut as demand grows at a slower pace.

Market events to watch this week:

Monday, September 18

9:30pm AUD Monetary Policy Meeting Minutes

Tuesday, September 19

8:30am USD Building Permits

Wednesday, September 20

4:30am GBP Retail Sales m/m

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Economic Projections

2:00pm USD FOMC Statement

2:00pm USD Federal Funds Rate

2:30pm USD FOMC Press Conference

6:45pm NZD GDP q/q

11:50pm JPY Monetary Policy Statement

Thursday, September 21

Tentative JPY BOJ Policy Rate

2:30am JPY BOJ Press Conference

8:30am USD Unemployment Claims

Friday, September 22

8:30am CAD CPI m/m

8:30am CAD Core Retail Sales m/m

8:30am All Day NZD Parliamentary Elections

The Reluctant Hawk

Mark Carney cast himself as a less-enthusiastic hawk on Monday while the BoC flexed its jaw muscle. The US dollar was the top performer while the Canadian dollar lagged. The RBA meeting minutes are due out later.

BoE Governor Carney had a chance to fine-tune his comments Monday, reiterateing that some tightening might be needed in the coming months. However, he also said that monetary policy may have to 'move in order to stand still' because rates are rising elsewhere.

In headline-driven markets, that's what stood out but a closer inspection showed that was just a small part of his overall justification for hiking. A bigger reason – and one that will last longer – is that he believes Brexit will be inflationary. Others may differ but the market voted for lower GBP on the overall message, perhaps more in a nod to the outsized recent gains than a genuine re-think on the path of rates. Cable fell a cent on the day.

In the bigger picture, a shakeout is emerging in markets trying to make sense of central bank policy. The BoC showed that the shift from dovish, to neutral to two rates hikes can take place in six months and we are all on the lookout for the next target. There are also signs the BOC is having second thoughts. Deputy Governor Lane said Monday that they will be “strongly” taking into account the CAD leap in upcoming decisions. That spooked loonie traders and sent USD/CAD nearly a full-cent higher.

Maybe the more-interesting comment in his speech was that rates are still relatively low compared to what they believe is the neutral level. It's another sign of how jumpy markets are right now. That means opportunities will abound in the weeks ahead.

Or even the day ahead. The RBA Minutes are up next as the market tries to sort out which way Lowe will tilt. The headlines are due at 0130 GMT.

Pound Loses Ground, Markets Eye Carney Speech

The British pound has posted losses at the start of the week, after posting strong gains in Thursday and Friday sessions. In North American trade, GBP/USD is trading at 1.3485, down 0.72% on the day. On the release front, British Rightmove HPI declined 1.2%, its second decline in three months. Bank of England Governor Mark Carney will deliver a lecture at the International Monetary Fund in Washington, D.C. In the US, there are no major releases on the schedule.

The pound enjoyed an excellent week, as GBP/USD jumped 3.0% percent. The pound climbed on Thursday and Friday, following surprisingly hawkish minutes from the BoE's policy meeting. As expected, the BoE opted to hold interest rates at 0.25%, where they have been pegged since August 2016. There have been calls for the BoE to raise rates in order to fend off high inflation levels, but most policymakers are of the opinion that current economic conditions do not warrant a rate hike. However, the minutes were surprisingly hawkish, stating that if current economic conditions continue, then "withdrawal of monetary stimulus is likely to be appropriate over the coming months in order to return inflation sustainably to target". The strong guidance from the BoE was unusual, and sets the stage for a likely rate hike in November, when the BoE holds its next policy meeting. Investors reacted positively to the hawkish message from the bank, sending the pound sharply higher, with the pound breaking the 1.36 level on Thursday, for the first time since June 2016.

US consumer spending has been a sore spot in a generally strong economy, and there was more disappointing news on Friday, as August retail sales reports missed expectations. Core Retail Sales slowed to 0.2%, missing the forecast of 0.5%. Retail Sales was even worse, posting a decline of 0.2%, compared to the estimate of +0.1%. Much of the slowdown in the August numbers are attributable to lower automobile sales, which have been slowing in recent months, and was likely made worse by Hurricane Harvey. These numbers underscore continuing weakness in consumer spending, despite a strong labor market. The Federal Reserve remains concerned about weak consumer spending, a key driver of economic growth, and could make reference to the lack of spending in its rate statement, which will be released later this week.

Dollar Resumes Gains, Pushes Above 111 Yen

USD/JPY has posted gains in the Monday session, continuing the upward movement which marked Friday trade. In the North American session, the pair is trading at 111.50, up 0.58%. On the release front, it is a quiet start to the week, with Japanese banks closed for a holiday. In the US, there are no major events on the schedule. On Tuesday, the US releases Building Permits and Housing Starts.

US releases wrapped up the week on a sour note, as retail sales reports missed expectations. Core Retail Sales slowed to 0.2%, missing the forecast of 0.5%. Retail Sales was even worse, posting a decline of 0.2%, compared to the estimate of +0.1%. Much of the slowdown in the August numbers are attributable to lower automobile sales, which have been slowing in recent months, and was likely made worse by Hurricane Harvey. These numbers underscore continuing weakness in consumer spending, despite a strong labor market. The Federal Reserve remains concerned about weak consumer spending, a key driver of economic growth, and could make reference to the lack of spending in its rate statement, which will be released later this week.

It was a rough week for the Japanese yen, as USD/JPY surged 2.4 percent. The yen pushed above the 111 level on Thursday, for the first time since August. Recent tensions between North Korea and its neighbors had boosted the yen, traditionally a safe-haven currency. North Korea had alarmed South Korea and Japan by firing missiles over Japan and testing a hydrogen bomb. However, the crisis has eased in the past week, reviving risk appetite. North Korea sent another missile over Japan last week, but this failed to put a dent in investor confidence. It's becoming increasing doubtful that last week's uneasy calm will continue, and that could mean more volatility from the yen. On Sunday, the US ambassador to the United Nations, Nikki Haley, warned that the UN Security Council had exhausted its options, and the US might have to refer the matter to the Pentagon. This was followed by a US-South Korean air drill on Monday.

Homebuilder Confidence Slips in September

The NAHB/Wells Fargo Housing Market Index (HMI) fell 3 points to 64 in September, reversing August's gain. Both present and future sales fell by 4 points. The Midwest and South accounted for the bulk of the drop.

Homebuilder Confidence Declines Slightly

- Homebuilder confidence fell slightly in September, as Hurricanes Harvey and Irma impacted the two largest states for new single-family homebuilding. Damages from the hurricanes introduce an element of uncertainty into the housing outlook and will likely bolster labor and material costs.

- The drop in the HMI may signal some moderation in new home sales and homebuilding during the latter part of 2017.

Hurricane Damages May Have Dampened Confidence

- Harvey and Irma caused widespread damage in Texas and Florida, which may interrupt activity in states that combined to account for 25 percent of the nation's single-family permits.

- Prospective buyers' traffic fell just 1 point to 47, which is the lowest since November 2016. Buyer traffic continues to be limited by low levels of completed homes but remains close to its recent range and is consistent with continued sales growth.