Sample Category Title

GBPUSD Intraday Analysis

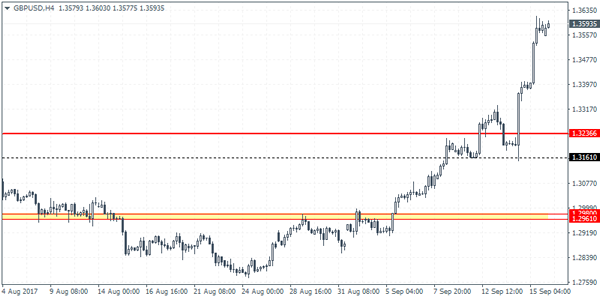

GBPUSD (1.3593): The British pound rallied strongly after rate hike expectations from the BoE found renewed optimism. GBPUSD close at 1.3588 by Friday's close. The cable now remains within a few pips short of filling the gap at 1.3677 from the June 2016 Brexit event that saw prices gapping lower. We do expect this rally to 1.3677 to be a touch and go event as the GBP is likely to take a breather in the short term. Support is now seen at 1.3236, exposing a large downside risk to the currency pair. Economic data from the UK this week is limited to only the retail sales numbers on Wednesday and of course the FOMC meeting later in the day.

EURUSD Intraday Analysis

The US dollar was seen giving up some of the gains by Friday's close, but the US dollar index was seen supported above the multi-year support level of 91.44. As a new trading week unfolds, all eyes are on the FOMC meeting due this Wednesday. Last week saw the British pound emerging on the top logging over 3% gains against the US dollar. This came as the Bank of England signaled that interest rates could rise in the coming months.

The Japanese yen was, of course, the weakest, as the currency declined 2.5% on the week by Friday's close. This made GBPJPY the currency pair logging the biggest gains as a result.

The economic calendar today is relatively light. Scheduled for 0900 GMT, the Eurostat will be releasing the final inflation figures for August. Based on the flash inflation estimates, consumer prices in the eurozone are forecast to rise 1.5% on the headline and 1.2% on the core. While headline CPI is accelerating, core CPI continues to remain sluggish in comparison. Still, the inflation data is unlikely to dent the sentiment in the euro currency.

Eurozone CPI To Confirm Consumer Prices Are Rising

The US dollar was seen giving up some of the gains by Friday's close, but the US dollar index was seen supported above the multi-year support level of 91.44. As a new trading week unfolds, all eyes are on the FOMC meeting due this Wednesday. Last week saw the British pound emerging on the top logging over 3% gains against the US dollar. This came as the Bank of England signaled that interest rates could rise in the coming months.

The Japanese yen was, of course, the weakest, as the currency declined 2.5% on the week by Friday's close. This made GBPJPY the currency pair logging the biggest gains as a result.

The economic calendar today is relatively light. Scheduled for 0900 GMT, the Eurostat will be releasing the final inflation figures for August. Based on the flash inflation estimates, consumer prices in the eurozone are forecast to rise 1.5% on the headline and 1.2% on the core. While headline CPI is accelerating, core CPI continues to remain sluggish in comparison. Still, the inflation data is unlikely to dent the sentiment in the euro currency.

Bank of Japan Meeting Concluding On Thursday

Market movers today

Today we have a very light data calendar with the final euro area inflat ion prints for August due out , although we do not estimate any significant changes.

Later in the week the focus will be on the FOMC meet ing on Wednesday, where we expect the Fed to announce that it will begin shrinking its balance sheet in October, the Bank of Japan meeting concluding on Thursday as well as PM T heresa May’s speech on Brexit in Florence on Friday.

In Scandinavia, the week peaks on Thursday with the Norges Bank monetary policy meeting and minutes from the Riksbank's September monetary policy meeting. We share the consensus view that Norges Bank will not touch interest rates.

Selected market news

Risk appetite improved in the US session on Friday as concerns about the worst-case scenarios for North Korea and hurricanes in the US eased. The large US equity indices ended the day higher after the negat ive close in Europe on Friday and in Asia this morning, regional indices trade higher while the yen has weakened versus all other G10 currencies. Japanese markets are closed for a holiday.

The series of US data released on Friday was a relatively mixed bag: while both US indust rial product ion and US retail sales for August came out weaker than expected, the empire manufacturing index surprised on the upside. It was widely expected that the August print s were distorted due to Hurricane Harvey, and in isolat ion this is not be a concern as such. ISM and regional surveys for manufacturing are quite robust , so manufacturing is likely to be doing fine. However, the down-revision to both June and July retail sales were a surprise indicat ing that momentum in US consumpt ion might have been over a longer period of t ime. We should expect more data for August and September to be distorted as Hurricane Irma is also affect ing numbers.

In Japan, speculat ion that Prime Minister Shinzo Abe is considering calling for a snap general elect ion is growing as Abe’s support has increased following the cabinet reshuffle in August and not least due to his handling of the North Korea crisis. According to the broadcaster NHK, Abe is likely to dissolve the Lower House in late September and call for a general election in late October. The political calendar in Japan is packed with important events in the coming years. Besides the possibility of an early elect ion, focus in coming months will also be on who will be appointed to lead the BoJ once Haruhiko Kuroda’s five-year term ends in April 2018. Increased polit ics in Japan may lead to more volatility on Japanese markets and induce some JPY appreciat ion.

On Friday, we published our new FX Forecast Update: A tale of three central-bank camps and Yield Outlook - Central banks gradually turning more hawkish. The most significant change in our new forecast is that we now expect the Bank of England to hike the Bank Rate by 25bp in November.

Market Update – Asian Session: Equities Markets Rally While China Housing Prices Gradually Slow

Asia Summary

Asian equity markets opened higher (Japan closed) taking its cue from a strong US session Friday. Hong Kong Hang Seng tested levels not seen since Dec 2007. The PBOC injected CNY300B in OMO, the most since January. NZD rose 0.5% against the US dollar after opening slightly weaker on New Zealand Refining disclosing a leak in a pipeline. So far the company is unsure how long it will take to repair and as a result the Govt is support supplies to Air New Zealand and Auckland airport. Both the Kospi and the won failed to react to North Korea activity and rhetoric. Trump spoke with S. Korea President Moon over the weekend and a US aircraft carrier is expected in South Korea in October. China released its August property price data, showing a modest slowdown, property names in China and Hong Kong took some strength on the news. Markets to remain focused on Fed meeting later this week and Bank of Japan.

Key economic data

(SG) SINGAPORE AUG NON-OIL DOMESTIC EXPORTS M/M: 4.5% V 3.1%E; Y/Y: 17.0% V 11.8%E; ELECTRONIC EXPORTS Y/Y: 21.7% V 15.0%E

(AU) AUSTRALIA AUG MOTOR VEHICLE SALES M/M: 0.0% V -2.4% PRIOR; Y/Y: 1.7% V 1.7% PRIOR

(CN) CHINA AUG PROPERTY PRICES M/M: RISE IN 46 OUT OF 70 CITES VS 56 PRIOR; Y/Y RISE IN 68 OUT OF 70 CITIES VS 70 PRIOR

Speakers and Press

China/Hong Kong

(CN) China economic growth may slow down in Q4, sees 2017 GDP at 6.8% - Chinese press

(CN) China Banking Regulatory Commission (CBRC) reports Aug Bank Bad Loan Ratio 1.86% - Xinhua

(CN) China Insurance Regulator (CIRC) to strengthen risk prevention by preventing risks stemming from excessive rapid growth in overseas investments - financial press

(HK) HKMA Chief Chan: Have confidence in HK$, no plans to change the peg; HK needs to diversify in terms of IPOs

Korea

(KR) According to KCNA, Kim Jong Un guided Hwasong-12 launching drill; Drill conducted to calm down “belligerence of the US"

(CN) South Korea investment into China for July YTD $1.75B v $3.1B y/y, -43.7% y/y - Korean press

(KR) South Korea defense ministry official: There is possibility of North Korean provocation, including additional ballistic missile launches and 7th nuclear test

Australia/New Zealand

(AU) Moody's: Australia residential mortgage arrears are at a 5-yr high and expected to increase

(AU) S&P: Australia July delinquent home loans underlying prime RMBS 1.17% v 1.15% m/m

Japan

(JP) Japan PM Abe said to be considering snap election as soon as Oct - financial press

Asian Equity Indices/Futures (00:00ET)

Nikkei closed, Hang Seng +1.1%; Shanghai Composite +0.2%, ASX200 +0.5%, Kospi +1.1%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.2%, Dax +0.4%, FTSE100 +0.3%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1955-1.1920; JPY 111.25-110.81; AUD 0.8035-0.7995;NZD 0.7343-0.7277

Dec Gold -0.3% at $1,321/oz; Nov Crude Oil 0.0% at $50.45/brl; Sept Copper +0.9% at $2.98/lb

(AU) Australia repurchases A$700M in 2018 and 2019 bonds, bid to cover 4.22x

(AU) Australia sells A$700M in 3.75% 2029 bonds; avg yield 2.8842%; bid-to-cover 3.39x

USD/CNY (CN) China PBOC sets yuan reference rate at 6.5419 v 6.5423 prior

(CN) PBoC OMO: injects CNY300B in 7 and 28-day (largest injection since January) vs injected combined CNY200B in 7,14 and 28 day reverse repos prior

(KR) Bank of Korea (BOK) sells KRW480B in 6-month bonds at 1.33%

(KR) South Korea Govt sells KRW629B 20-yr bond 2.28% v 2.38% prior

Equities notable movers

Australia/New Zealand

NZO.AU Confirms O.G Oil's partial takeover offer to acquire 67.6% stake; to create independent committee to respond; +3.5%

EVN.AU To sell Edna May mine to Ramelius for up to A$90M; Cuts FY18 production guidance following deal to 750-805K ozs (820-880K prior) at AISC of A$820-A$870/oz (prior A$850-900/oz)

NZR.NZ Reports leak at pipeline from refinery to Wiri; to impact revenues by NZ$10-15M, sees negative impact on income for pipeline and refining businesses; -3.2%

Hong Kong/China

2196.HK Updates offer for Gland Pharma: to acquire 74% stake for $1.09B; +2.6%; 656.HK Fosun International Ltd, +9.3%

US

OA Northrop Grumman said to be near deal to acquire Orbital ATK for over $7.5B in cash; deal could be announced as early as Monday - US financial press

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Dark cloud cover

• Time of formation: 10 Jul 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Evening doji

• Time of formation: 7 Aug 2017

• Trend bias: Down

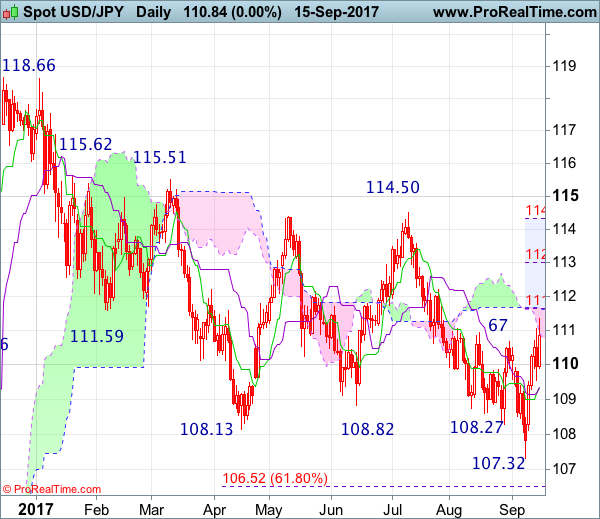

USD/JPY – 111.30

Despite falling to 107.32, the subsequent much stronger-than-expected rebound suggests a temporary low has been formed there and consolidation with upside bias is seen for test of 111.62-65 (current level of the upper Kumo and 38.2% Fibonacci retracement of 118.66-107.32), then towards previous resistance at 112.20, however, a sustained breach above there is needed to add credence to this view, bring retracement of recent entire decline from 118.66 to 112.99-00 (50% Fibonacci retracement) but reckon upside would be limited to 113.50-60, price should falter below 114.00.

On the downside, whilst pullback to 110.45-50 cannot be ruled out, reckon support at 109.90 would limit downside and bring another rise later. Below support at 109.55 would abort and suggest the rebound from 107.32 has ended instead, bring weakness to 109.00, however, still reckon downside would be limited to 108.45-50 and this week’s low at 108.12 should remain intact, price should stay well above recent low at 107.32, brig another rebound later.

Recommendation : Buy at 110.00 for 112.00 with stop below 109.00

On the weekly chart, the greenback opened higher last week and staged a stronger-than-expected rebound, a long white candlestick was formed, suggesting a temporary low has been made at 107.32, hence consolidation with mild upside bias is seen for gain to 112.20 resistance, however, above 112.99-00 (50% Fibonacci retracement of 118.66-107.32) is needed to signal recent entire decline from 118.66 has ended, bring further rise to 113.50-60, then towards 114.00 but price should falter well below chart resistance at 114.50 (July high) and bring retreat later.

On the downside, although initial pullback to 110.40-50 is likely, reckon the Tenkan-Sen (now at 109.76) would limit downside and the lower Kumo (now at 108.84) should hold, bring another rebound later. A drop below last week’s low at 108.12 would abort and suggest the rebound from 107.32 hs ended instead, bring retest of this level. Looking ahead, only a drop below 107.32 would signal the decline from 118.66 top has resume,ed and extend weakness to 107.00, then 106.50-55 (61.8% Fibonacci retracement of 99.01-118.66), however, previous resistance at 105.53 (now support) should remain intact.

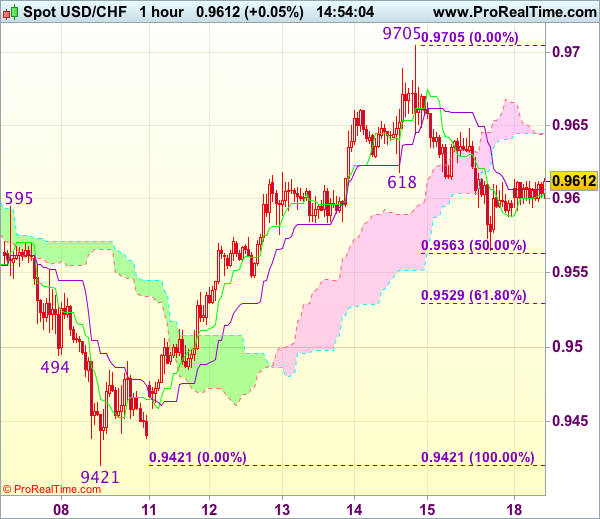

Trade Idea : USD/CHF – Sell at 0.9645

USD/CHF - 0.9612

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9605

Kijun-Sen level : 0.9602

Ichimoku cloud top : 0.9645

Ichimoku cloud bottom : 0.9645

New strategy :

Sell at 0.9645, Target: 0.9545, Stop: 0.9680

Position : -

Target : -

Stop : -

Although the greenback has recovered after finding support at 0.9565 on Friday and consolidation above this level would be seen, if our view that top has been made at 0.9705 last week is correct, reckon upside would be limited to minor resistance at 0.9648 and bring another decline later, below 0.9563-65 (50% Fibonacci retracement of 0.9421-0.9705 and said support) would extend weakness to 0.9525-30 (61.8% Fibonacci retracement), however, downside should be limited to 0.9500 and 0.9480-85 should hold.

In view of this, would not chase this fall here and would be prudent to sell dollar again on further recovery as 0.9648 should limit upside. Above 0.9680 would risk retest of said last week’s high at 0.9705, break there would extend recent rise from 0.9421 to 0.9740-50 later.

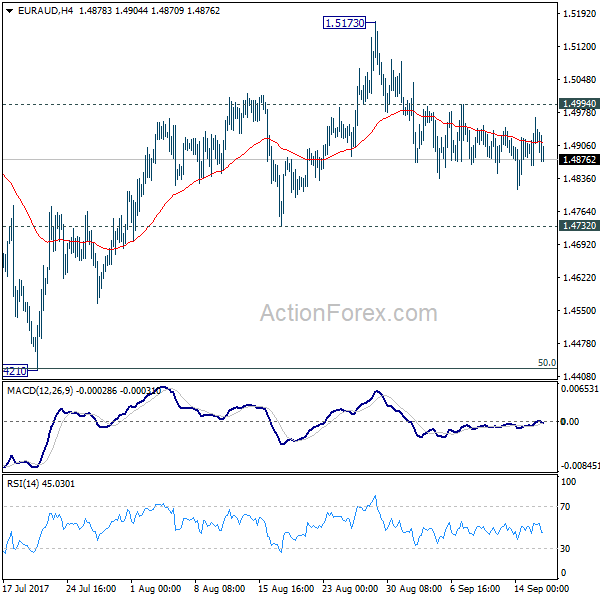

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4865; (P) 1.4916; (R1) 1.4968; More....

Intraday bias in EUR/AUD remains neutral for the moment. Another fall is mildly in favor as long as 1.4994 minor resistance holds. Break of 1.4732 will confirm that fall from 1.5173 is the third leg of consolidation pattern from 1.5226. In that case, further fall should be seen to 1.4421 again. But we'd expect strong support from there to contain downside and bring rebound. On the upside, above 1.4994 minor resistance will turn bias back to the upside for 1.5173/5226 resistance zone instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

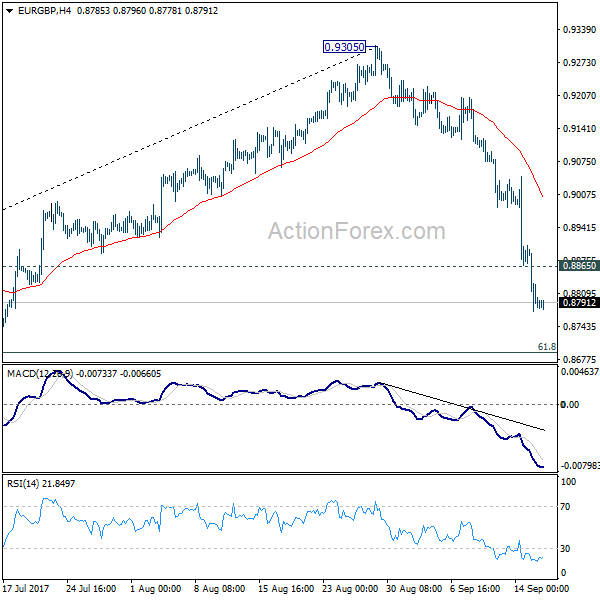

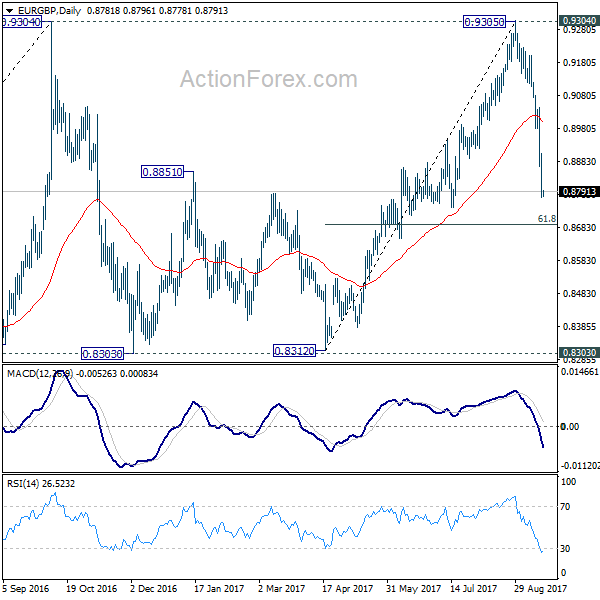

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8740; (P) 0.8822; (R1) 0.8872; More

Intraday bias in EUR/GBP remains on the downside for 61.8% retracement of 0.8312 to 0.9305 at 0.8691 and below. Fall from 0.9305 is seen as the third leg of the consolidation pattern from 0.9304. We'll look for bottoming signal again at it approaches 0.8303 support. On the upside, above 0.8865 minor resistance will turn intraday bias neutral and bring recovery, before staging another fall.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's still in progress with fall from 0.9305 as the third leg. Break of 0.8303 could be seen. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

Aussie Dollar Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.8006 on Friday.

LME Copper prices rose 0.6% or $38.5/MT to $6457.0/MT. Aluminium prices rose 0.2% or $3.0/MT to $2068.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.8027, with the AUD trading 0.26% higher against the USD from Friday's close.

Earlier today, in China, Australia's largest trading partner, the house price index climbed 8.3% on a yearly basis in August. The index had risen 9.7% in the previous month.

The pair is expected to find support at 0.7998, and a fall through could take it to the next support level of 0.7968. The pair is expected to find its first resistance at 0.8046, and a rise through could take it to the next resistance level of 0.8064.

Looking forward, minutes of the Reserve Bank of Australia's (RBA) latest meeting, scheduled to release in the early hours of tomorrow, will garner a lot of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.