Sample Category Title

GST Break Pushes Canadian Inflation Down a Tick in December

Headline CPI inflation fell a tenth to 1.8% year-on-year (y/y) in December, pushed lower by the temporary GST/HST break that went into effect mid-month.

Approximately 10% of the All-items CPI basket was affected by the tax exemption. Main price impacts were seen in food purchased from restaurants (-1.6% y/y), booze (-1.3% y/y), toys, games, and hobby supplies (-7.2% y/y) and children's clothing (-10.6% y/y).

Shelter inflation has been a key challenge for Canadians for some time now and cooled further in December to 4.5% y/y. Rent inflation cooled slightly to 7.1% y/y from 7.7% y/y in November, and the lift from higher mortgage interest costs continued to wane (to 11.7% y/y).

For Canadians looking to escape the cold, inflation for travel-related items rose in December. Travel services prices were up 7.9% y/y, and tours rose 5.7% y/y. Even gassing up for a road trip would cost you 3.5% more relative to a year ago. The impact of Taylor Swift's Eras Tour could be seen in accommodation prices in B.C., which were up 13.6% y/y, driven by the largest month-on-month increase in the series ever (+62% m/m).

The Bank of Canada's preferred "core" inflation measures were down slightly at 2.5% y/y on average, down from 2.6% in November.

Key Implications

December's inflation data came in line with the Bank of Canada's expectations for inflation to average close to 2%. Despite the tax cut driven dip in headline inflation, core inflation pressures have picked up over the past three months, suggesting that inflation readings are likely to move up a bit in the months ahead. This will give the Bank of Canada reason to adopt a more gradual pace of interest rate cuts this year. We expect a quarter point cut at every other decision in 2025.

Tariffs on Canadian exports didn't come on day one of the new administration, but President Trump does plan to establish an "External Revenue Agency" largely to collect tariffs, and Trump reiterated threats of a 25% tariff on Canada and Mexico, now due on Feb 1st. This creates a very challenging backdrop for Canada's economy, and we expect the BoC to cut rates a quarter point next week, which would put interest rates further into "neutral" territory – a stance we think is warranted given relatively soft demand backdrop for Canada's economy.

Sunset Market Commentary

Markets

All eyes are on the US dollar today. Yesterday’s sigh of relief by currencies ex-USD already went in reverse. President Trump didn’t go full-on tariff mode on day 1 in office and stopped short of announcing any. But mere hours later he very much kept the possibility afloat of levies on Canada and Mexico as soon as February 1. The USD bounced back in early Asian dealings and held on throughout the day. The trade-weighted index rose from 108 to 108.4 while EUR/USD’s adventure north of 1.04 looks to be a very short one (1.038). The Canadian Loonie and Mexican peso for obvious reasons underperformed. USD/CAD hovers near the recent highs of 1.445. USD/MXN is similarly circulating in the 20.75 area, the highest levels since mid-2022. Cyclical currencies have a tough time too. Lingering trade tensions combined with weaker commodity prices (eg. Brent below $80/barrel) pressure the likes of AUD & NZD with both reversing (part of) yesterday’s gains. The NOK suffers from lower oil prices and perhaps as well from the risk of losing the EU partially as a major customer. Trump suggested yesterday the EU could escape from tariffs if it buys more American energy. The NOK decline in any case may complicate the central bank’s upcoming monetary easing plans, with a first rate reduction up until now expected in March. The Japanese yen is the only currency able to fend off USD strength. Trump-related market volatility remains confined (so far, we should add) and that cleared the last obstacle for the Bank of Japan to raise rates a third time this Friday. Sterling loses out against both USD and EUR. The labour market report was close to expectations and as such not enough to offset last week’s set of disappointing data. Friday’s PMIs are the final chance for the pound to prevent a break above the EUR/GBP 0.845 resistance. GBP/USD sticks near 1.22. Global yields ease a few bps. It’s been a bond-friendly trading session with amongst others record bids for UK’s £8.5bn Jan2040 syndicated tap (books above £119bn) and a €134bn record demand for France’s May2042 €10bn syndicated deal. US Treasuries outperform in a first response to president Trump’s slew of executive orders yesterday. Net daily changes vary between -3 bps (2-yr) and -6.5 bps (10-yr). UK gilt yields drop 3-4 bps across the curve. German rates decline up to 2 bps. Several ECB members hit the wires before they no longer can from Thursday on. Villeroy (France) was no longer worried about inflation and expects more cuts going forward. He favours going at a steady 25 bps at every meeting so that they hit 2% by summer. This level is what Villeroy considers to be neutral. He doesn’t see the need to go below that at this stage. Slovakia’s Kazimir issued similar comments. He added that the January 30 rate cut is a done deal.

News & Views

December inflation data published by statistics Canada today were close to expectations. Headline inflation declined 0.4% compared to November causing the Y/Y measure to ease further from 1.9% to 1.8%. The monthly decline for an important part was driven by a temporary brake in the sales tax on goods such as food from restaurants and alcoholic beverages. The break applies from December 14 to February 15. Prices ex food and energy decline 0.1% M/M with the Y/Y index printing at 2.1%. Prices of clothing and footwear declined 3.0% M/M to be 4.5% lower on the same month last year. Among the factors keeping upward pressure on the global price level, shelter price inflation was 0.3%, but this only caused the Y/Y measure to decline from 4.6% to 4.5%. The core inflation measures that are closely monitored by the Bank of Canada when assessing its monetary policy slow further within the BOC inflation target band of 1%-3% to 2.4% for the core median measure and 2.5% for the trimmed mean measure. The Bank of Canada will hold its next policy meeting on January 29. At that meeting it will have new economic forecasts at its disposal. At its December meeting, the BoC for the second consecutive meeting cut its policy rate by 50 bps to 3.25%. The BoC indicated then that the ’Governing Council has reduced the policy rate substantially since June. Going forward, we will be evaluating the need for further reductions in the policy rate one decision at a time’. This suggest that the BoC might slow the pace of easing to 25 bps steps. The Canadian dollar recently suffered from the risk of tariffs potentially to be implement by the new US government. At USD/CAD 1.445, the loonie is trading within reach of the weakest levels against the US dollar since the start of the corona crisis early 2020.

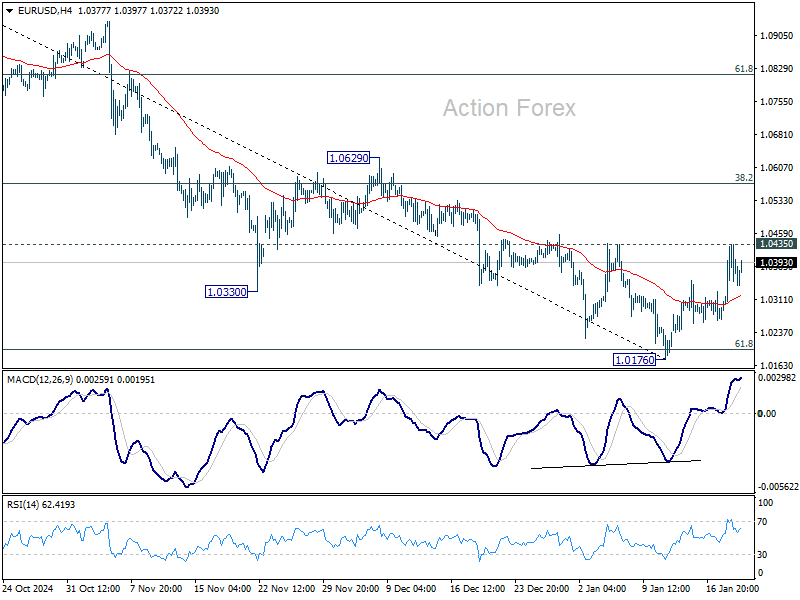

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0311; (P) 1.0373; (R1) 1.0478; More...

Intraday bias in EUR/USD remains neutral for the moment. With 1.0435 resistance intact, another decline is in favor. On the downside, firm break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound to 38.2% retracement of 1.1213 to 1.0176 at 1.0572.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

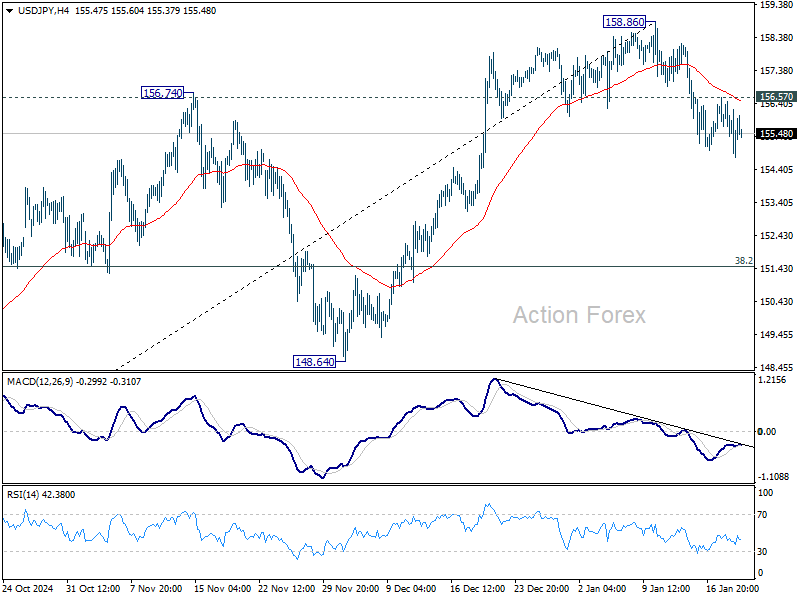

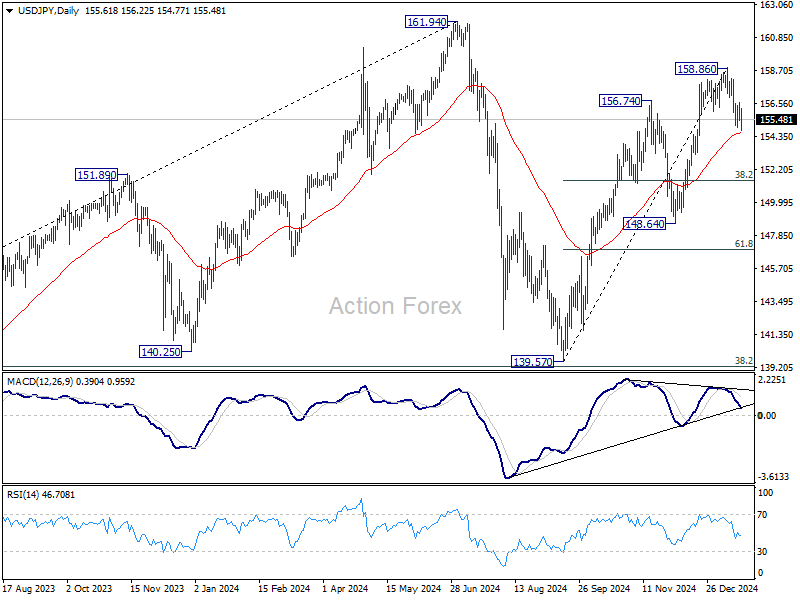

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.17; (P) 155.88; (R1) 156.33; More...

Intraday bias in USD/JPY remains mildly on the downside as fall from 158.86 short term top is in progress. Sustained break of 55 D EMA (now at 154.61) will target 8.2% retracement of 139.57 to 158.86 at 151.49 next. Nevertheless, firm break of 156.67 resistance will argue that the pull back has completed, and turn bias back to the upside for retesting 158.86 high instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

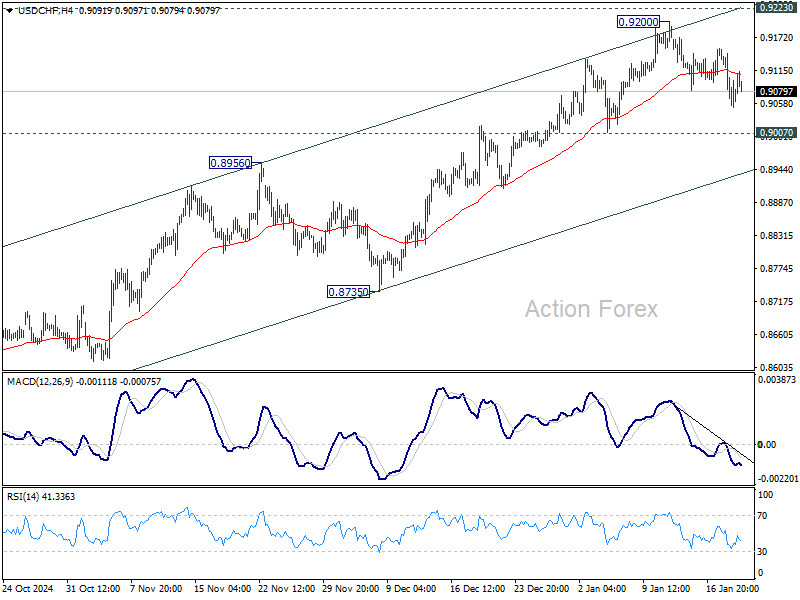

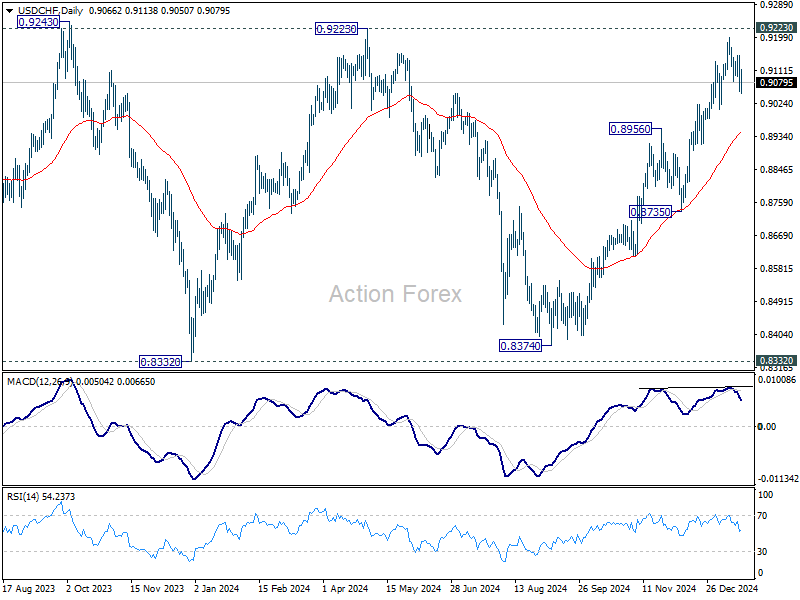

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9031; (P) 0.9092; (R1) 0.9128; More…

Intraday bias in USD/CHF remains neutral for the moment, as consolidation continues below 0.9200. Further rally is expected with 0.9007 support intact. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will turn bias back to the downside for deeper pull back to 55 D EMA (now at 0.8948).

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

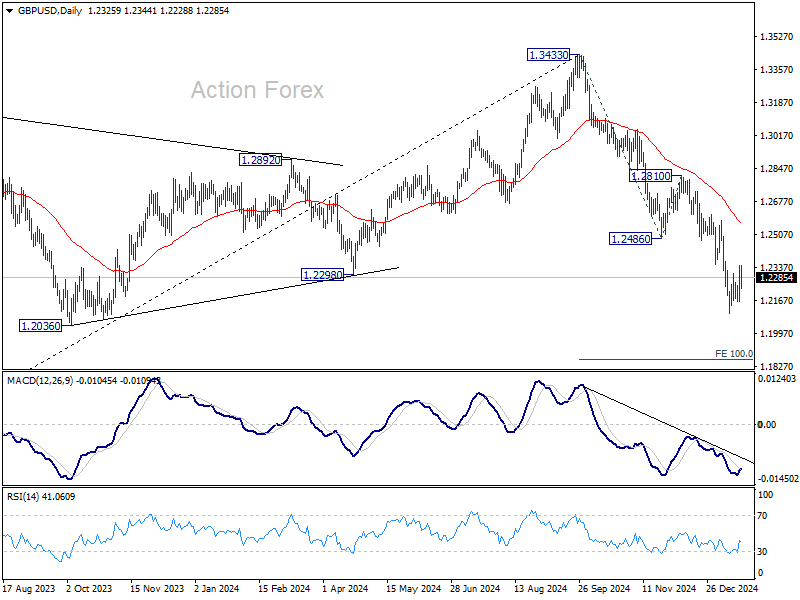

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2211; (P) 1.2278; (R1) 1.2395; More...

Intraday bias in GBP/USD remains neutral for the moment. Consolidations from 1.2099 could extend with stronger recovery But outlook will remain bearish as long as 12486 support turned resistance holds. On the downside, break of 1.2099 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

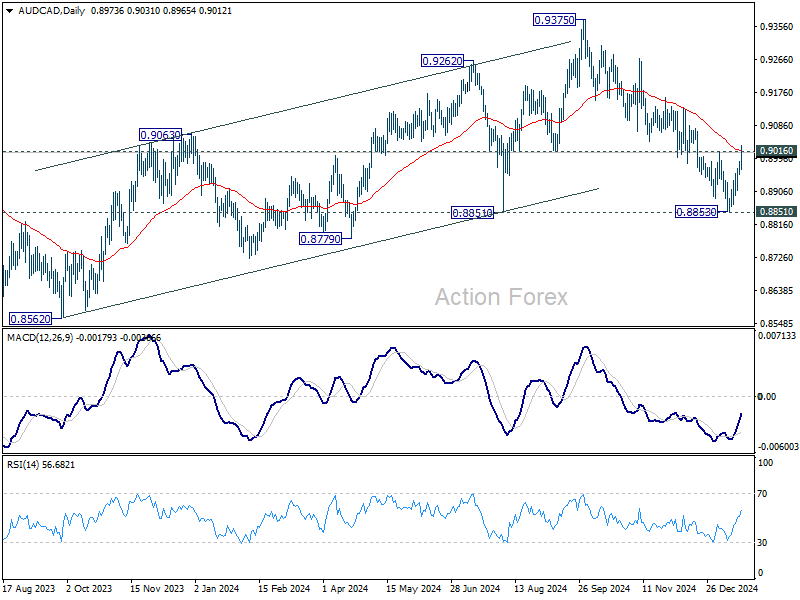

Loonie Weakness Persists in Calmer Markets, AUD/CAD Challenges Key Resistance

Forex markets have settled into quieter trading as the immediate impact of US President Donald Trump’s inauguration and initial executive orders fades. While Trump’s proposed tariffs remain a significant concern, their delayed implementation suggests a more calculated and strategic approach, tied to future negotiations. This tempered stance has brought a sense of cautious optimism to the markets, as the eventual impact may not be as severe as initially feared—especially if major agreements are reached with key allies like the EU.

Despite this relative calm, Canadian Dollar remains under significant pressure. As the most immediate target of Trump’s tariff agenda, with measures likely set to take effect on February 1. Loonie's recovery struggled to gain traction. This weakness has been compounded by softer-than-expected Canadian CPI data for December. While energy prices saw a boost due to base effects, other areas of the economy, such as food and restaurant pricing, contributed to the overall deceleration in inflation. With inflation hovering near the 2% target, BoC is expected to continue easing monetary policy, albeit at a slower pace.

So far this week, Dollar has been the weakest performer, followed by Loonie and Yen. On the other side of the spectrum, Kiwi leads the gainers, followed by Euro and Sterling. Swiss Franc and Australian Dollar are positioned more neutrally, sitting in the middle of the performance table.

Technically, AUD/CAD's rebound extended this week on Loonie's weakness. It's now pressing 0.9016 resistance and 55 D EMA. Sustained break there would argue that 0.8851 support was successfully defended, and corrective rally from 0.8562 (2023 low) remains intact. Further rise should then be seen back to retest 0.9375 high.

In Europe, at the time of writing, FTSE is up 0.09%. DAX is down -0.09%. CAC is up 0.18%. UK 10-year yield is down -0.053 at 4.610. Germany 10-year yield is down -0.011 at 2.518. Earlier in Asia, Nikkei rose 0.32%. Hong Kong HSI rose 0.91%. China Shanghai SSE fell -0.05%. Singapore Strait Times fell -0.33%. Japan 10-year JGB yield fell -0.0073 to 1.190.

Canada’s Inflation Slows to 1.8% in Dec Amid Food Price Decline

Canada’s annual inflation rate eased to 1.8% yoy in December, down from 1.9% yoy in November and slightly below expectations of 1.9% yoy. The deceleration was largely driven by declines in food prices and alcohol-related expenses.

Canadians paid 1.6% less for food purchased from restaurants on a year-over-year basis, marking the first annual decline in this index. Excluding food, CPI rose by 2.1% yoy.

Gasoline prices, for example, rose 3.5% yoy in December, reversing a -0.5% yoy decline in November. The increase was attributed to a base-year effect, as December 2023 saw a sharp -4.4% monthly decline due to concerns about oil demand amid high supply levels. However, on a month-over-month basis, gasoline prices edged down by -0.6% mom.

Looking at the core measures, CPI median slowed from 2.6% yoy to 2.4% yoy versus expectation of 2.5% yoy. CPI trimmed slowed from 2.6% yoy to 2.5% yoy, matched expectations. CPI common was unchanged at 2.0% yoy, above expectation 1.9% yoy.

German ZEW falls to 10.3 as Eurozone shows relative resilience

German ZEW Economic Sentiment fell sharply in January, dropping from 15.7 to 10.3 and missing market expectations of 15.1. In contrast, Current Situation Index showed slight improvement, rising from -93.1 to -90.4, slightly better than forecasts of -93.0.

Meanwhile, Eurozone ZEW Economic Sentiment painted a more optimistic picture, climbing from 17.0 to 18.0, exceeding expectations of 16.9. Current Situation Index for the Eurozone also rose, gaining 1.2 points to -53.8.

ZEW President Achim Wambach attributed the decline in Germany’s sentiment to persistent economic headwinds. He noted, “The second consecutive year of recession caused economic expectations in Germany to fall.”

Key factors include weak private household spending and low demand in the construction sector. Wambach warned that if these trends persist, “Germany will fall further behind the other countries of the Eurozone.”

Adding to the challenges, Wambach highlighted growing political uncertainty in Germany due to the complexities of coalition-building and the unpredictability of economic policies under the new Trump administration in the US.

UK payrolled employment falls -47k in Dec, unemployment rate rises to 4.4% in Nov

UK payrolled employment fell -47k or -0.2% mom in December. Median monthly pay rose 5.6% yoy, down from 6.4% yoy in November and 7.9% yoy in October. Claimant count rose 0.7k, below expectation of 10.3k.

In the three months to November, unemployment rate ticked up to 4.4%, above expectation of 4.3%. Average earnings excluding bonus rose 5.6% yoy, up from 5.2% yoy, and above expectation of 5.5% yoy. Average earnings including bonus rose 5.6% yoy, up from 5.2% yoy, matched expectations.

NZ BNZ services fall to 47.9, contracts for 10th month

New Zealand’s BNZ Performance of Services Index declined from 49.1 to 47.9 in December, well below historical average of 53.1. This also marks the 10th consecutive month of contraction.

The breakdown of the data highlights broad weakness: activity/sales fell from 48.3 to 46.2, and supplier deliveries dropped sharply from 52.5 to 47.7. New orders/business remained stagnant at 49.5, just below the threshold for expansion, while employment showed a marginal improvement, rising from 46.7 to 47.4. Stocks/inventories also slipped into contraction territory, falling from 52.0 to 48.8.

Negative sentiment among respondents increased to 57.5% in December, up from 53.6% in November, with cost-of-living pressures and concerns about the general economic climate dominating feedback.

BNZ’s Senior Economist Doug Steel remarked, “Comparing across our key trading partners, New Zealand has the only PSI in contraction. Our neighbour Australia is the closest comparison, but their equivalent PSI is sitting more comfortably at 50.8.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2211; (P) 1.2278; (R1) 1.2395; More...

Intraday bias in GBP/USD remains neutral for the moment. Consolidations from 1.2099 could extend with stronger recovery But outlook will remain bearish as long as 12486 support turned resistance holds. On the downside, break of 1.2099 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

Canada’s Inflation Slows to 1.8% in Dec Amid Food Price Decline

Canada’s annual inflation rate eased to 1.8% yoy in December, down from 1.9% yoy in November and slightly below expectations of 1.9% yoy. The deceleration was largely driven by declines in food prices and alcohol-related expenses.

Canadians paid 1.6% less for food purchased from restaurants on a year-over-year basis, marking the first annual decline in this index. Excluding food, CPI rose by 2.1% yoy.

Gasoline prices, for example, rose 3.5% yoy in December, reversing a -0.5% yoy decline in November. The increase was attributed to a base-year effect, as December 2023 saw a sharp -4.4% monthly decline due to concerns about oil demand amid high supply levels. However, on a month-over-month basis, gasoline prices edged down by -0.6% mom.

Looking at the core measures, CPI median slowed from 2.6% yoy to 2.4% yoy versus expectation of 2.5% yoy. CPI trimmed slowed from 2.6% yoy to 2.5% yoy, matched expectations. CPI common was unchanged at 2.0% yoy, above expectation 1.9% yoy.

NASDAQ (NQ): Two Scenarios That Show Perfect Setup For Traders

NASDAQ E-Mini Futures (NQ) appears to be extending the bullish sequence from October 2022. Will the sequence finish soon and lead to a big sell-off across the US indices? While the sequence persists, where should traders eye the next opportunity?

The NQ chart is very clear. After the markets recovered from Covid in March/April 2020, a massive bullish cycle followed. This rally continued until November 2021 and was identified as wave (I). From November 2021, a sell-off began to correct the Covid recovery cycle. The sell-off ended in November 2022 and was identified as wave (II). Wave (III) then started in October 2022 and has continued to rise since. The bullish cycle from October 2022 has gained over 105% from its low and lasted nearly 28 months. Further analysis shows this rally as wave I of (III). Therefore, wave (III) still has a long way to go.

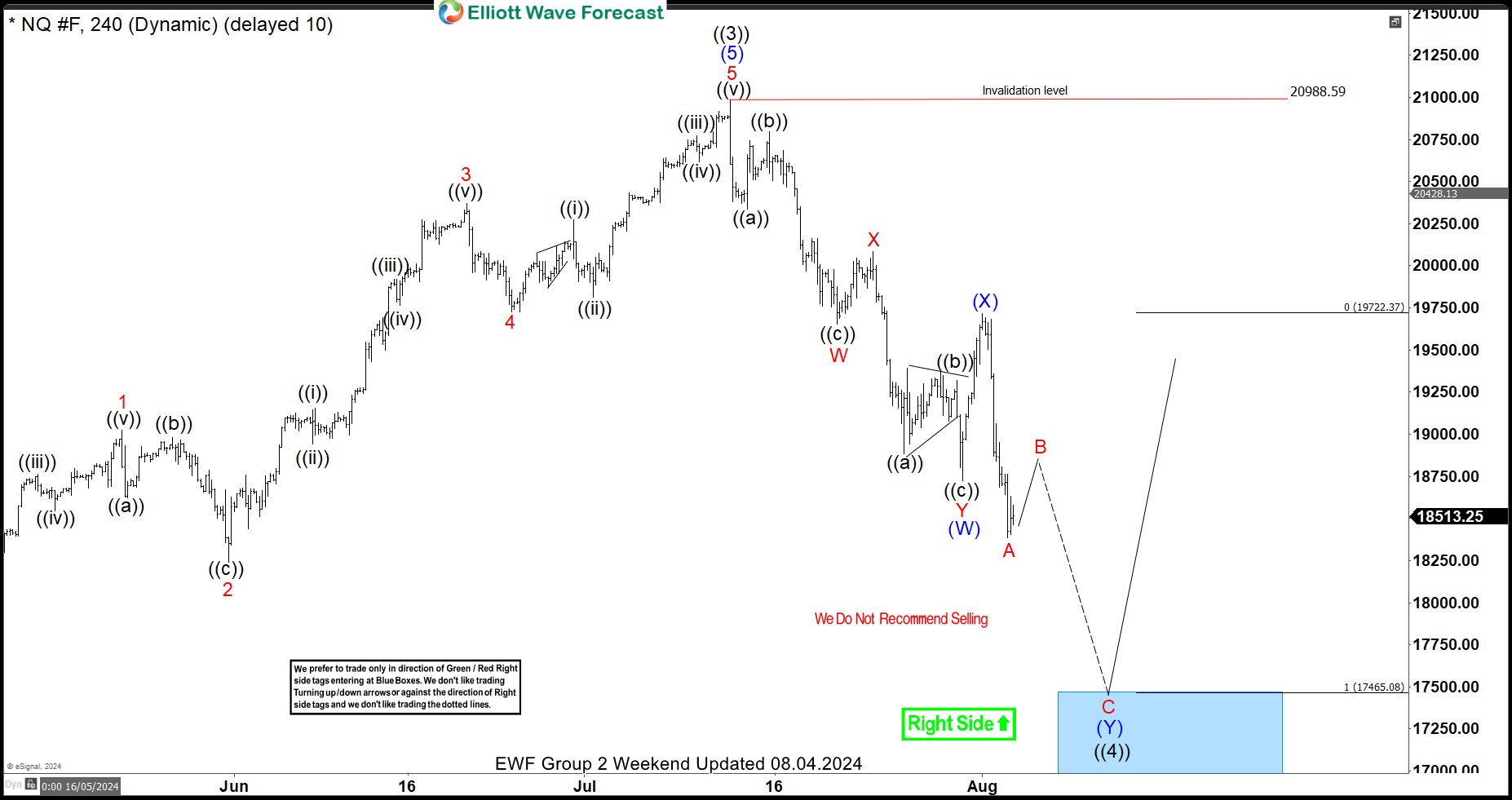

When such a bullish sequence emerges, we prefer buying pullbacks in 3, 7, or 11 swings from the blue box. These blue boxes are shown on the chart for Elliottwave-Forecast members. Within the bullish sequence from October 2022, there have been multiple pullbacks. Members have profited from these. The most recent pullback occurred on August 5, 2024. As shown on the 8.4.2024 chart below, we bought at the extreme of this pullback.

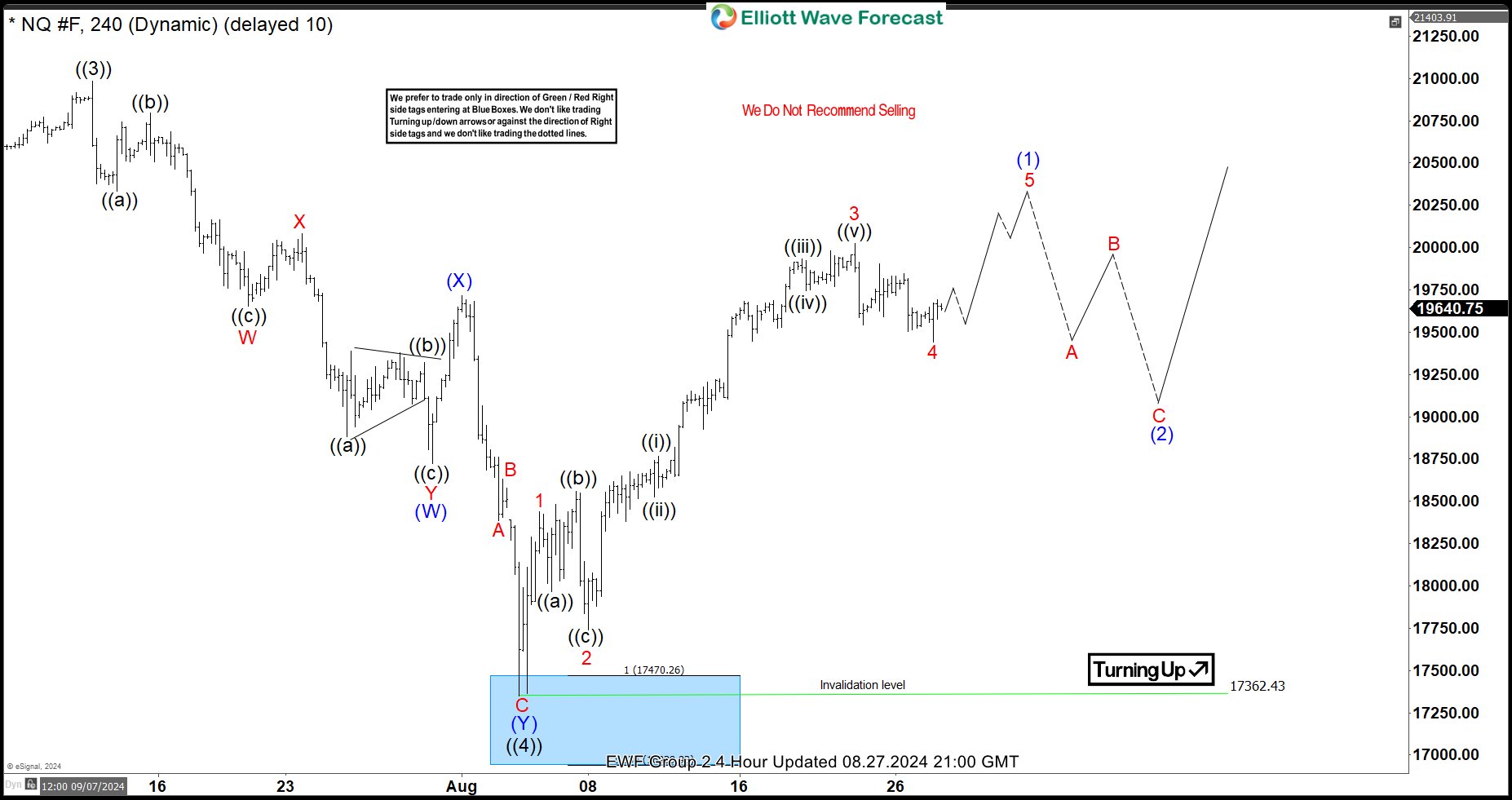

Price reached the blue box to conclude a 7-swing structure and then rallied from there. The 8.27.2024 chart below shows a later update we shared with members as we continue to provide update from this extreme area.

From the blue box, NQ gained about 29% until the recent pullback from December 2024 started. Again, pullbacks within a bullish sequence should be a perfect opportunity for buyers to go again. What are the likely scenarios buyers should look forward to, for the next perfect blue box opportunity? This post will provide two best buying scenarios for traders.

From the blue box, NQ gained about 29% until the recent pullback from December 2024 started. Again, pullbacks within a bullish sequence should be a perfect opportunity for buyers to go again. What are the likely scenarios buyers should look forward to, for the next perfect blue box opportunity? This post will provide two best buying scenarios for traders.

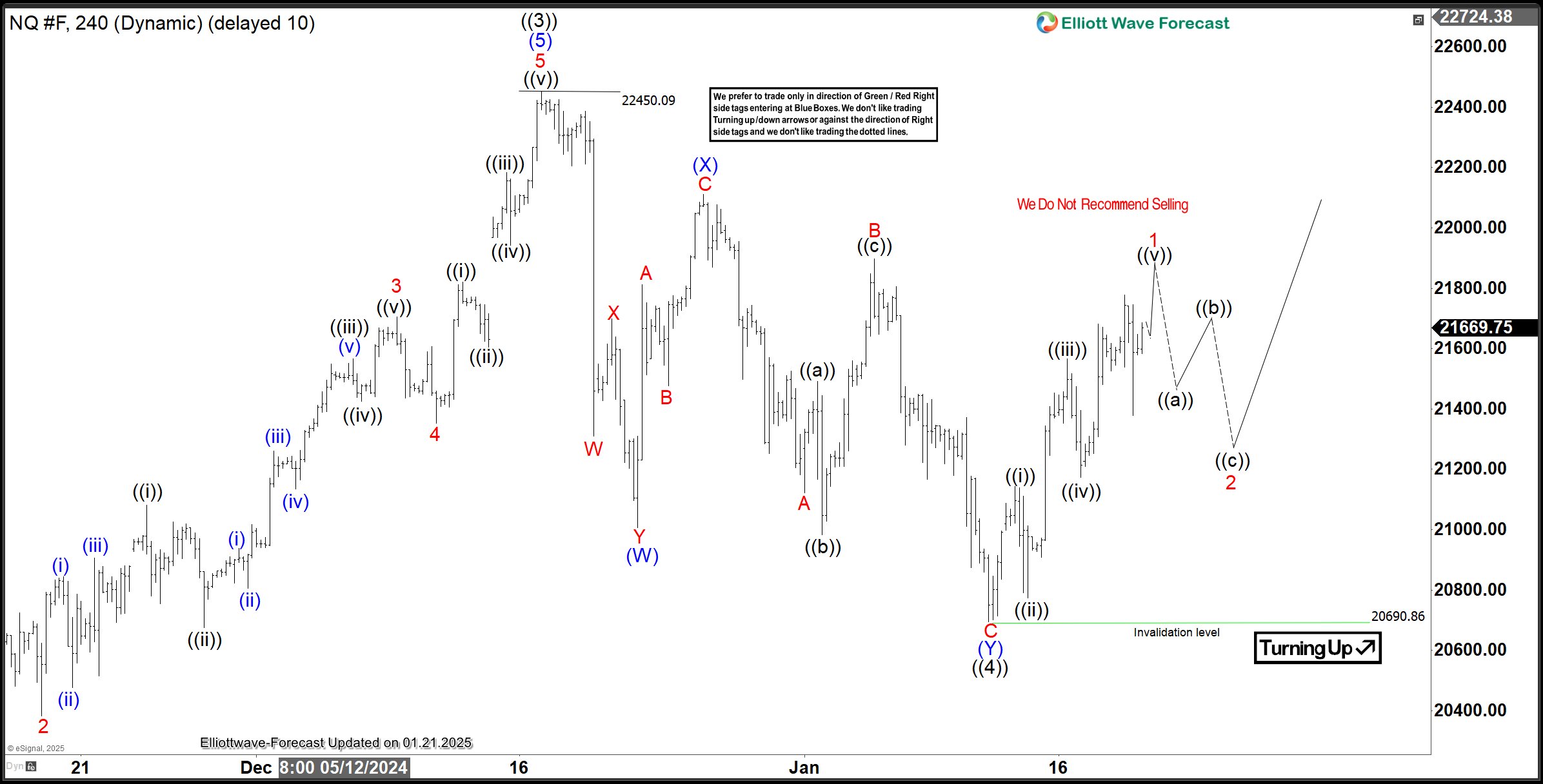

NQ Elliott Wave Analysis – 1st Scenario. 01.21.2025 Update

The NQ chart above shows that wave ((4)) of I ended on January 13, 2025, at 20,690. From this pullback low, wave ((5)) began to emerge. The price is now close to completing wave 1 of (1) of ((5)). A pullback for wave 2 should follow. The best entry was at the extreme of wave ((4)), but it was barely missed. The next opportunity will come after the price breaks above the December 2024 peak at 22,450 with wave 3. After this, buyers can wait for the next pullback. It could be for wave 4, wave ((ii)) of 3, or wave ((iv)) of 3 within the bullish sequence from January 13, 2025. This bullish setup depends on the price breaching the December 2024 high. But what if the price turns lower instead of breaking this high?

NQ Elliott Wave Analysis – 2nd Scenario. 01.21.2025 Update

If the price doesn’t breach 22,450 to confirm the first scenario, it could fall further for a deeper wave ((4)). As the chart above shows, wave ((4)) could develop into a larger 7-swing structure. Wave (W) ended on January 13, 2025, where the current bounce for wave (X) began. Wave (X) may extend to 22,044.07–22,250.96. If the price turns lower from this zone or below it, buyers can watch for the next extreme of wave ((4)) for a perfect long entry. However, if the bounce breaches 22,450, this scenario becomes invalid, and the first scenario becomes valid. In either case, we have prepared our members to act. The strategy is simple: just buy from the blue box! You can also learn to trade from our blue box for just $0.99 for the next 14 days.

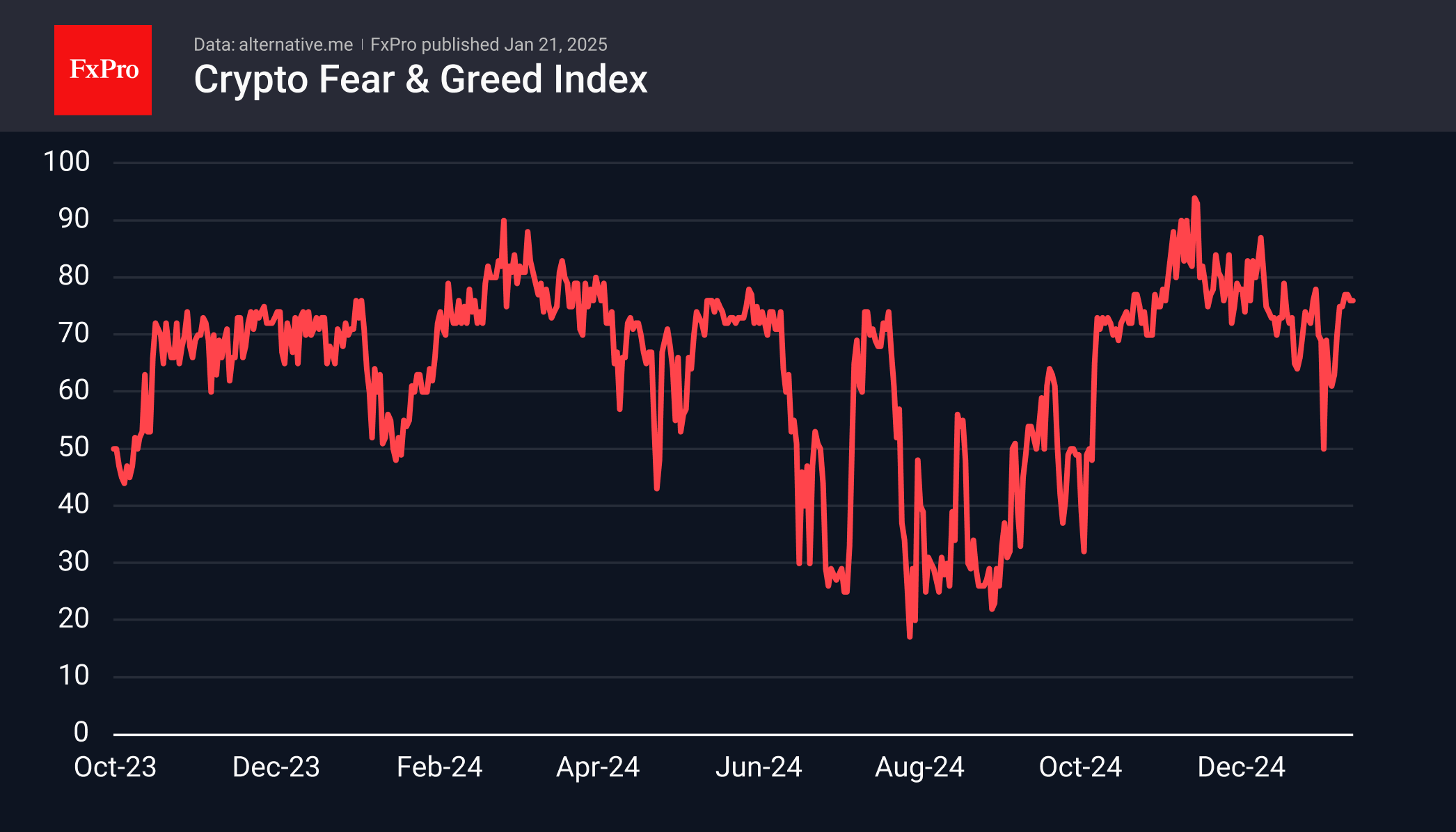

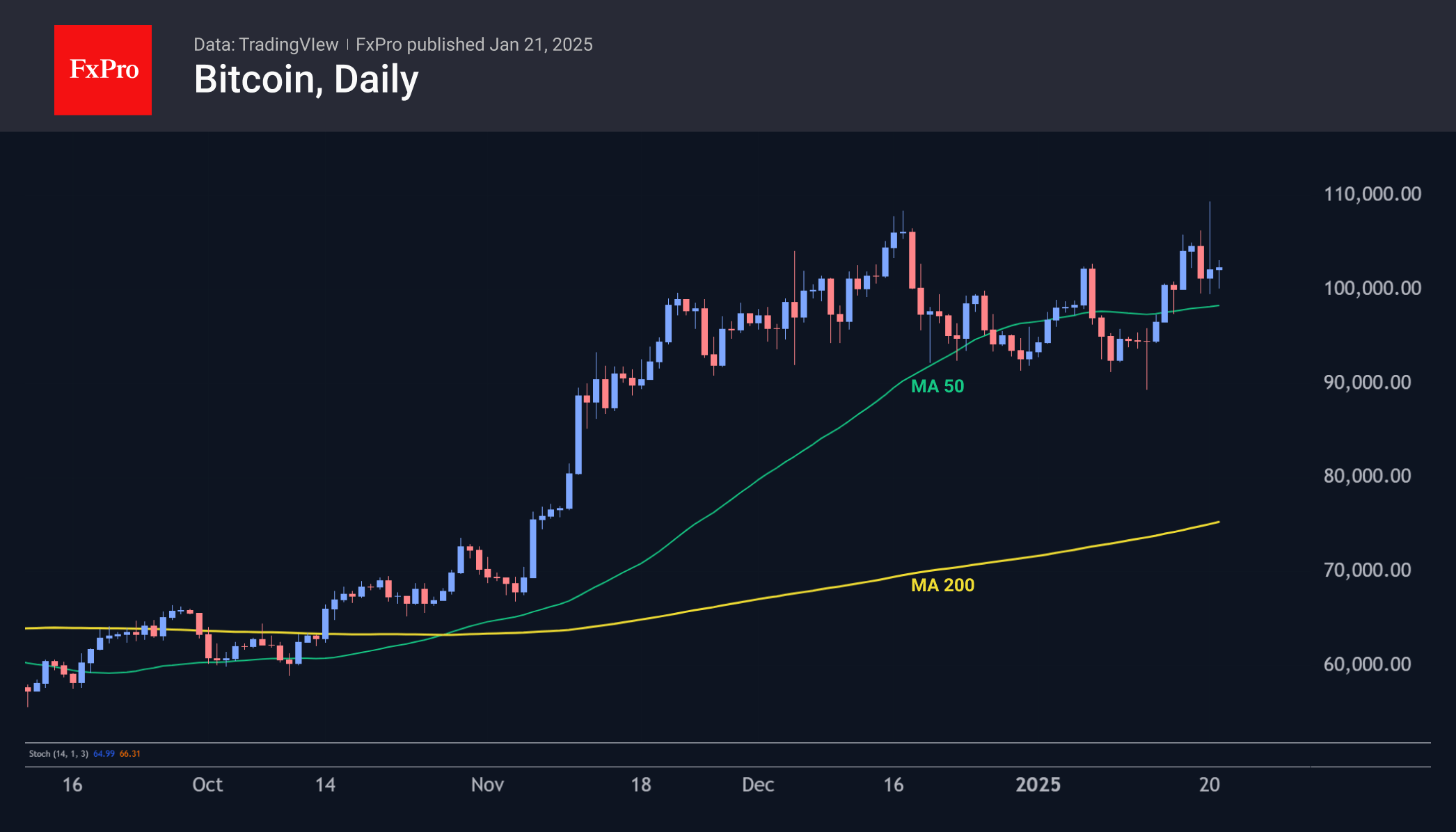

Crypto Market Took a Step Back But Unlikely to Turn Around

Market Picture

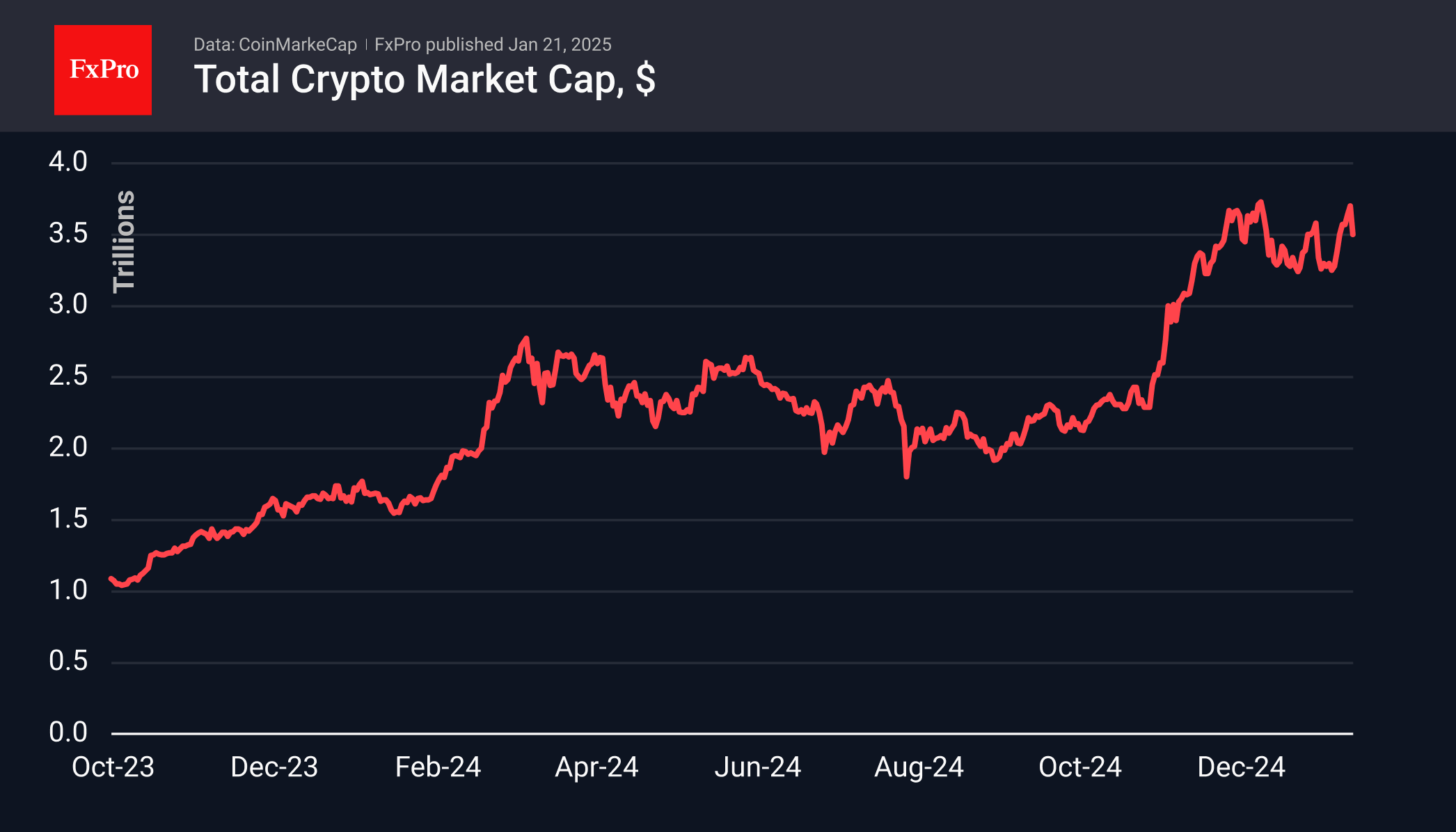

The cryptocurrency market experienced a decline, with a reduction of approximately 5.3% compared to the previous day. This downturn was attributed to high expectations surrounding Trump’s inauguration speech, which did not mention cryptocurrencies. Consequently, the total capitalisation of cryptocurrencies decreased to $3.5 trillion, reverting to the level observed at the end of the previous week. While this indicates a reduction in optimism, it does not suggest a market reversal.

The Cryptocurrency Fear and Greed Index stands at 76, having ranged between 75 and 77 for six consecutive days. This is considered the initial stage of ‘extreme greed’. Observations indicate that during a bull market phase, values exceeding 80 increase the risk of a corrective pullback, whereas current values may coexist with further movement towards historical highs.

Bitcoin reached a new all-time high on Monday, approaching the $110k level. However, significant selling followed, resulting in a 9% pullback from the peak. By the start of trading in Europe, Bitcoin was trading near $102k. The resistance level observed on January 7th temporarily became support. It is anticipated that the market will progress gradually, overcoming one level after another.

Corrective pullbacks also impacted other major altcoins. Over the past 24 hours, Ethereum decreased by 4.3%, XRP fell by 5.8%, and Solana declined by 9.6%.

News Background

According to CoinShares, global investment in crypto funds increased 46 times last week to $2.195 billion, the highest in five weeks. Investments in Bitcoin rose by $1.903 billion, Ethereum by $246 million, XRP by $31 million, and Solana by $2.5 million.

The SEC reported a surge in applications to launch cryptocurrency ETFs in the US, with more than a dozen applications submitted by major management companies in recent days.

Following the change of administration in the US, MN Consultancy founder Michael van de Poppe highlighted significant growth potential in three categories of crypto assets: cryptocurrencies previously classified as securities by the SEC, including XRP, Matic, and Algorand; coins from World Liberty Financial’s portfolio, such as Chainlink and Aave; and Ethereum ecosystem projects.

On Polymarket, a prediction platform, voting on creating the Bitcoin reserve within the first 100 days of Trump’s presidency indicated a shift in sentiment. The odds of a favourable outcome decreased from 48% to 29% in less than 24 hours.