Sample Category Title

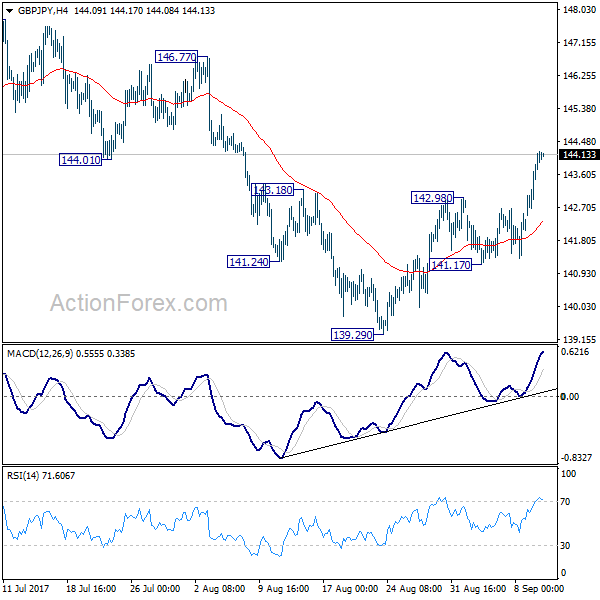

GBP/JPY Daily Outlook

Daily Pivots: (S1) 142.90; (P) 143.53; (R1) 144.60; More

Intraday bias in GBP/JPY remains on the upside for as rebound from 139.29 continues. As noted before, fall from 147.76 has completed at 139.29 already, on bullish convergence condition in 4 hour MACD. Further rise should be seen for 147.76/148.42 resistance zone. Overall, price actions from 148.42 are seen as a sideway consolidation pattern. Break of 141.17 support will turn bias to the downside and bring another fall. But downside should be contained by 135.58 cluster support to bring rebound.

In the bigger picture, the sideway pattern from 148.42 is still unfolding. In case of deeper fall, we'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

UNSC Passed New North Korea Sanctions after US Conceded, Markets Cheered With Returning Risk Appetite

Risk appetite staged a strong strong return as DOW closed up 259.58 pts, or 1.19%, to close at 22057.37 overnight. S&P 500 also gained 26.68 pts, or 1.08%, to 2488.11, a record close. 10 year yield also responded positively, gaining 0.064 to 2.125. Gold, on the other hand, extended this week's sharp pull back and is back below 1330. Asian markets followed with MSCI Asian Pacific ex Japan hitting the highest level since 2007. Sentiments were given a boost after United Nation Security Council passed fresh sanctions against North Korea. It may be a slap in the face to the US as it can only get a much watered down version of the sanctions approved. But the fact that there is no outright ban on oil supplies to North Korea means the threat of an immediate military confrontation should have eased. And that was cheered by investors. IN the currency markets, Canadian Dollar and US Dollar remain the strongest ones for the week while Yen and Swiss Franc are the weakest.

UNSC passed fresh sanctions on North Korea, without oil embargo

The United Nations Security Council passed tougher sanctions on North Korea yesterday. All 15 council members backed the resolution unanimously, including Russia and China. This came after the US compromised and tabled a much watered down version of the original draft of sanctions. The resolution imposes a ban on the pariah regime's textile exports, such as fabrics and apparel products, and a ban its import of natural gas liquids. Textile is North Korea's second-biggest export after coal and other minerals in 2016, totaling USD 752m.

On imports, the UNSC decided that all member states would "prohibit the direct or indirect supply, sale or transfer" to North Korea "of all refined petroleum products beyond 500K barrels during an initial period of three months (Oct 1 2107 to Dec 31, 2017) and exceeding 2M bpd per year during a period of 12 months beginning on Jan 1, 2018 and annually thereafter. Meanwhile, the members would "not supply, sell or transfer crude oil" to North Korea "in excess of the amount supplied, sold or transferred by that State in the 12-month period prior to the adoption of today's resolution".

The US initially proposed to include an oil embargo, but this was objected by Russia and China, the two permanent UNSC members possessing veto power to reject the entire resolution.

Brexit Repeal Bill won first Commons vote

In UK, the House of Commons approved the European Union (Withdrawal) Bill by a vote of 326 to 290, passing the first hurdle in Parliament. The bill is now approved in principle, but there will be challenges from lawmakers on the details and requests for amendments before a final vote later this year. There will be 64 hours of debate over eight days as lawmakers scrutinize the bill line-by-line. In short, the so called Repeal Bill aims at converting EU laws and regulations into UK legislations on the day on Brexit in March 2019.

Prime Minster Theresa May hailed that "Parliament took a historic decision to back the will of the British people and vote for a bill which gives certainty and clarity ahead of our withdrawal from the European Union" And, "this decision means we can move on with negotiations with solid foundations and we continue to encourage MPs from all parts of the UK to work together in support of this vital piece of legislation."

ECB officials pave the way for gradual stimulus removal

A number of ECB officials spoke yesterday. The general tone is that while remaining cautious, it's about time to make the decision to scale back stimulus in gradual manner. Executive Board member Sabine Lautenschlaeger said that "the economy in the euro area is doing better and the conditions are in place for inflation to pick up and move steadily toward our goal." And, "we have to be prepared to take tough decisions in good time. We also have to adapt our communications accordingly." Another Executive Board member Yves Mersch said that "over the course of autumn we will see how far our instruments should or have to be adapted on the basis of new insights and how confident we are that we can withdraw the support to the economy through our monetary policy."

Also an Executive Board member, Benoit Coeure, sounded more cautious and said that "compared with past demand shocks, policy will remain more accommodative for longer, thereby likely muting further the pass-through of any growth-driven exchange rate appreciation."

Governing Council member Ardo Hansson wrote in an article that "too much emphasis has been put on the fears of policy normalization." And he emphasized that "the process of normalization of policy stance is very gradual, and in fact it has been already started." Another Governing Council member Ewald Nowotny also said that the plan to scale back stimulus must be "well designed, it has to be gradual, clear and consistent with our reaction function and our forward guidance."

ECB President Mario Draghi said last week that the "bulk" of decisions on recalibration of the stimulus will be made at the October meeting.

Australia business confidence dropped below long term average

Australia NAB business condition rose to 15 in August up from 14, and hit the highest level since 2008. However, business confidence tumbled notably to 5, down from 12. It's also the first time it dropped below its long-term average since mid-2016. NAB chief economist Alan Oster noted that "for those indicating deterioration in confidence, the biggest concerns appear to be customer demand, government policy, as well as cost pressures - both energy and wages." But, it's "it is probably too early to read much into the drop in confidence this month." And, "household consumption is a notable point of difference between our relatively subdued growth outlook and the RBA's more sanguine forecasts, and will be key to the economy's sustained return to trend growth."

Looking ahead

UK inflation data will be the main focus of the day. In particular, headline CPI is expected to climb back to 2.8% yoy in August. RPI and PPI will also be released.

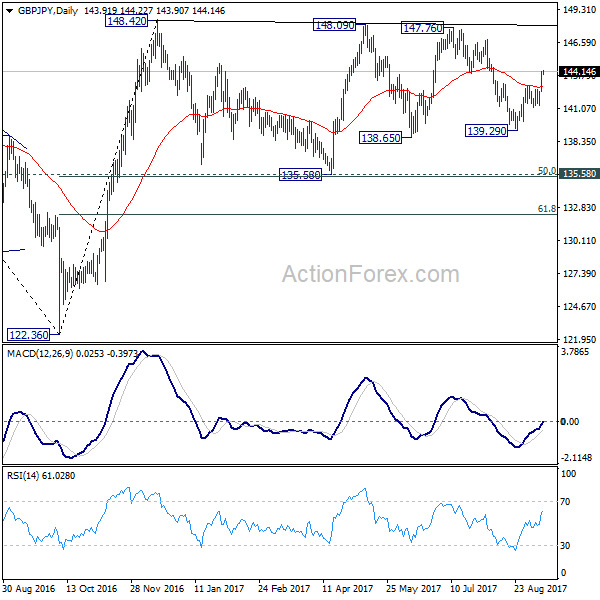

GBP/JPY Daily Outlook

Daily Pivots: (S1) 142.90; (P) 143.53; (R1) 144.60; More

Intraday bias in GBP/JPY remains on the upside for as rebound from 139.29 continues. As noted before, fall from 147.76 has completed at 139.29 already, on bullish convergence condition in 4 hour MACD. Further rise should be seen for 147.76/148.42 resistance zone. Overall, price actions from 148.42 are seen as a sideway consolidation pattern. Break of 141.17 support will turn bias to the downside and bring another fall. But downside should be contained by 135.58 cluster support to bring rebound.

In the bigger picture, the sideway pattern from 148.42 is still unfolding. In case of deeper fall, we'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | NAB Business Confidence Aug | 5 | 12 | ||

| 8:30 | GBP | CPI M/M Aug | 0.50% | -0.10% | ||

| 8:30 | GBP | CPI Y/Y Aug | 2.80% | 2.60% | ||

| 8:30 | GBP | Core CPI Y/Y Aug | 2.50% | 2.40% | ||

| 8:30 | GBP | RPI M/M Aug | 0.60% | 0.20% | ||

| 8:30 | GBP | RPI Y/Y Aug | 3.80% | 3.60% | ||

| 8:30 | GBP | PPI Input M/M Aug | 1.30% | 0.00% | ||

| 8:30 | GBP | PPI Input Y/Y Aug | 7.30% | 6.50% | ||

| 8:30 | GBP | PPI Output M/M Aug | 0.10% | 0.10% | ||

| 8:30 | GBP | PPI Output Y/Y Aug | 3.10% | 3.20% | ||

| 8:30 | GBP | PPI Output Core M/M Aug | 0.10% | 0.10% | ||

| 8:30 | GBP | PPI Output Core Y/Y Aug | 2.30% | 2.40% | ||

| 8:30 | GBP | House Price Index Y/Y Jul | 4.80% | 4.90% | ||

| 14:00 | USD | JOLTS Job Openings Jul | 5950 | 6163 |

Elliott Wave View: DXY Dollar Index Bearish Below 93.36

DXY Dollar Index Short Term Elliott Wave view suggests that the decline from 8/16 peak is unfolding as an Ending Diagonal Elliott Wave structure. Down from 8/16 high, Minor wave 1 ended at 91.62 and Minor wave 2 ended at 93.347. Minor wave 3 is unfolding as a double three Elliottwave structure. Minute wave ((w)) of 3 ended at 91.01 and Minute wave ((x)) of 3 is in progress. The internal subdivision of Minute wave ((x)) shows a zigzag Elliottwave structure. Minutte wave (a) of ((x)) ended at 91.62 and Minutte wave (b) of ((x)) ended at 91.41.

The Index has reached an inflection area where Minutte wave (c) = Minutte wave (a) and thus cycle from 9/8 low is mature. Expect Minute wave ((x)) of 3 to end at 92.02 – 92.4. While bounces stay below 93.36, Index should resume lower or at least pullback in 3 waves. We don’t like buying the Dollar Index.

DXY 1 Hour Elliott Wave Chart

Ending Diagonal typically happens inside wave 5 of an impulse Elliottwave structure or inside wave C of a zigzag. Ending Diagonal has 5 waves subdivision and each wave is further subdivided into 3 waves. Thus Ending Diagonal has the structure of 3-3-3-3-3.

Gold Closes The Gap

Gold continues to drop on the short term and could close the gap up. Is trading right above the $1325 per ounce and could drop much deeper if the USD will resume the yesterday’s rebound. The next major downside target will be at the first warning line (WL1) of the major descending pitchfork. The retreat is natural after the false breakout above the lower median line (LML) and after the failure to close near it.

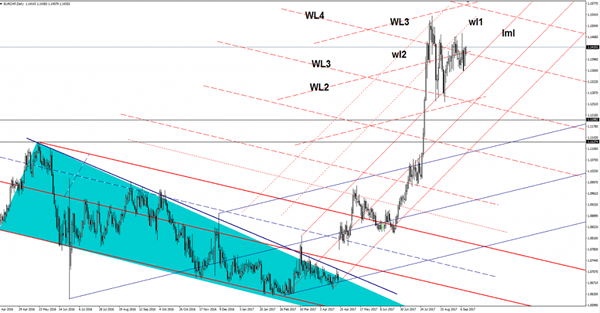

EUR/CHF Breakout Underway

Price resumes the yesterday's bullish candle and is approaching the 1.1450 psychological level. Is trading in the green after the rejection from the upper median line (uml) of the minor ascending pitchfork. I've said in the previous reports that a valid breakout above the WL4 will confirm a further increase.

The failure to stay near the upper median line is signaling that the bulls are very strong on the short term.

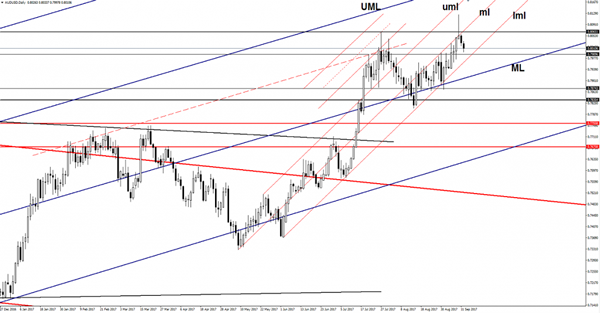

AUD/USD Turned To The Downside

AUD/USD dropped further after the yesterday's bearish candle and should hit fresh new lows very soon. Price has found strong resistance, so the current drop is natural. The USD has taken the lead again as the USDX has rallied in the yesterday's session.

We'll see what will happen on the dollar index because the rebound could be only temporary. As you already know, the USDX remains under massive selling pressure despite the current bounce back. Only an accumulation could signal a reversal on the USDX.

The Aussie goes down also because the NAB Business Confidence was reported at 5 points in August, much below 12 points in the previous reading period. The economic indicator has reached the lowest level since December 2016. We'll see how the pair will react after the release of the US data, the JOLTS Job Openings are expected to drop from 6.16M to 5.96M, while the NFIB Small Business Index decreased from 105.2 to 104.8 points.

The pair has turned to the downside after the false breakout above the 0.8065 horizontal resistance and above the median line (ml) of the minor ascending pitchfork. The next downside target will be at the lower median line (lml) of the minor ascending pitchfork. A breakdown from the pitchfork's body will send the rate towards the median line (ML) of the major ascending pitchfork, where he could find support again.

Market Morning Briefing: The Aussie Is Testing The Support At 0.8000

STOCKS

Major stock indices have shot up yesterday. Dow and Dax have rallied up and Nikkei has opened at higher levels. Shanghai may be in a pause mode for some time. Nifty looks bullish for the week.

Dow (22057.37, +1.19%) has been trading sideways since mid-Aug only to build base and gather more momentum for a sharp surge as seen yesterday. Immediate resistance is seen near 22100 which is likely to break on the upside targeting 22400 soon.

Dax (12475.24, +1.39%) also opened with a gap up and rose higher. The bullish momentum looks strong just now and could take the index to levels near 12750-12800 again in few sessions.

Nikkei (19742.20, +1.00%) opened today with a sharp gap up above our immediate resistance near 19600. A test of 19900-20200 levels is on the cards for the near term.

3400 could act out as a decent resistance for Shanghai (3375.37, -0.03%) in the next few sessions. A slight fall in the near term could be helpful to gain some more momentum to resume the longer term uptrend. If not an immediate fall, we could see some sideways consolidation between 3400-3300 zone.

Nifty (10006.05, +0.72%) could re-test 10100 or higher in the coming sessions while immediate support near 9900 holds. Thereafter a slight corrective dip is possible.

COMMODITIES

Gold (1329) moved lower in line with our short term bearish view due to overbought condition and renewed strength in Dollar Index. Immediate trading range for Gold is now 1327-1363 and a close below 1327 could open up 1303 levels as well. Similarly Silver (17.75) has also moved lower and trading within the range of 17.40-18.01.

Copper (3.03) has also come down in line with our expectation and trading within the range of 3.00-3.16 and a daily close below 3.00 could open up 2.90 levels as well.

No directional move had been seen in Brent (53.80) as it is hovering around the support of its near term trading range of 53.30-55.60.Only a close below 53.30 could open up 51 regions, otherwise it might move up towards 55. WTI (48.06) is also trading at yesterday's level, within its narrow range of 47.22-50-48.70. Only above 48.70, the higher resistance of 50.20 can come into consideration.

FOREX

As it turns out, Dollar-Yen (109.36) has broken above the 108.70-90 region, bringing it back into the earlier 108-111 range. However, the market may stall for a while between 109.00-110.00 for a couple of days. A break above 110 is needed to propel the market to higher levels.

The Euro-Yen (130.74) has risen along with Dollar-Yen, within an overall uptrend that can target 132+. This might also help Euro-Dollar (1.1960) to maintain its overall uptrend by remaining above trend Support at 1.1900.

The Pound (1.3177) has done well for itself by rising from 1.28 since 23rd August. We have been looking for further upside to 1.3270 as well. But, it could run into profit-taking soon if it is unable to move up to 1.3270 immediately, say today itself.

The Aussie (0.8011) is testing the Support at 0.8000. Deeper Support seen near 0.7965 as well. While these hold, we continue to be bullish overall, targeting 0.82. At the same time, we acknowledge the chances of a near term dip to 0.7965 as well.

Further short-covering being seen in the Dollar-Yuan (USDCNY = 6.5439). Chances of seeing 6.5750 now.

Dollar-Rupee closed at 63.86 yesterday, but trades near 63.99/64.03 on the NDF market, following the rise in the Dollar Index (91.875), which might move up to 92.00-20 this week. If so, Dollar-Rupee could see 64.20.

INTEREST RATES

The benchmark US 10Yr yield (2.12%) moved higher as it is trading above 2.08% regions. It is trading within a bearish channel since 10th of July 2017 and only a daily close above 2.16-18% regions could help to get out of the same.

EUR/USD moved lower due to lack of upside momentum in both German-US 2 Yr Spread (-2.03%) and the German-US 10Yr Spread (-1.73%).

Muted price action has been seen in across all the Japanese Bond yields. Japan 10Yr yield hovering around at 0.00% levels while the 30Yr (0.81%) and the 5Yr (-0.14%) are almost unchanged.

UK Gilts yields has rebound marginally as UK 5Yr and 30Yr Gilt Yields (5Yr 0.45% and 20Yr 1.55%) are up by 2-3 pips. The UK 10Yr (1.02%)is also moved higher with an immediate resistance at 1.07% regions.

USD/JPY Breaks Support But Is Immediately Bought With Vigour

I'm back in the office after a long weekend and just want to take my time today easing myself back into the price action that I missed.

Take a look at the unfolding USD/JPY price narrative that we've been following on the blog with price lunging below the major daily support level that we've been talking about…

USD/JPY Daily:

…but nope, that certainly didn't last long. The buyers stepped in and price immediately reversed with some serious vigour.

The momentum in the bounce back is highlighted by the fact that price didn't even pause at the retest of short term support. It's all about that higher time frame support level right now.

Now take a step into the intraday chart and take a look at how price actually reacted to the level…

USD/JPY Hourly:

So here we can see that price actually gapped back through the level on Monday's open. From there, momentum has taken hold and we can see why the cliche of not stepping in front of a moving train to pick a top is said so often.

USD & Indices Rally After Hurricanes

US and global indices rallied across the board as fears of widespread damage from Hurricanes Harvey and Irma have ebbed slightly. Lack testing activity from Pyongyang also helped appease markets. The Hurricanes will weigh on Q3 GDP by 0.3%-0.4%, while the rebuilding boost may lift Q4 to as high as 3.5% from an expeccted 2.0% in Q3. Our DAX short was stopped out. A new Premium trade has been issued with detailed charts highlighting a crucial analog.

USD/JPY soared 150 pips to 109.50 from a Friday's low of 107.36 on Friday. The bounce brings the pair back above a few critical support levels, including the April low of 108.13. That one will be critical in the day ahead.

Estimates to the Hurricanes damage range from as high as $200 billion to $50 billion but in order for both storms to surpass the magnitude as a percentage of GDP as that reached in 2005, their combined damage would have to exceed $220 billion.

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

EUR +96K vs +87K prior GBP -54K vs -52K prior JPY -74K vs -69K prior CHF -2K vs -2K prior CAD +54K vs +53K prior AUD +65K vs +67K prior NZD +15K vs +19K prior

The overall moves were modest, likely as the market hunkered down ahead of the BOC and ECB, but the increase in the euro net long was enough to push it to the highest since May 2011.

A Big Sigh Of Relief

A Big Sigh of Relief

New York traders breathed a huge sigh of relief after the Dollar deftly sidestepped a gaping chasm when North Korea didn’t test H-bombs or launch ICBM’s and the devastation from hurricane Irma was not of the Apocalyptic scale some had anticipated

On cue, the US equity markets rocketed higher with the S&P closing in record territory while the US 10y yields pumped four bp’s higher to close at 2.13 Now that the ” storm has passed” and North Korea played the good man over their 69th anniversary, the question now is whats next for the beleaguered dollar as some key themes are developing in the background beyond the current NK risk play and dovish Fed narrative.

A relief rally or not the Green back has dodged the bullet once again.

Japanese Yen

Predictably USDJPY was the biggest beneficiary, rising from 108. 25 at yesterday’s Singapore open to 109.49 taking out last Wednesday high due to the unwinding of risk-aversion trades. It’s safe to say that haven trades were a bit stretched as traders could not get enough yen to whet their appetite last week when aversion trades were the rage so the unwind is not too surprising given the lack of Geo escalation over the weekend.

Investors in the JPY space will likely look favourably on the fact the UN Security Council has voted unanimously to step up sanctions against North Korea even if it’s watered down version of the US proposal but it does have the decisive support from both Russia and China.

However, the fate of USDJPY extension will be Thursdays US CPI and given we may have seen our high water mark for US inflation; a tepid CPI print will pressure USDJPY lower

Euro

After opening in Singapore yesterday at 1.2025 and flirting with 1.2035 in London, the Euro prices headed straight down as traders started fretting about the lack of top side follow through as arguably stretched USD dollar short position made trader nervous. Also and the fact that USDCNH found a base after rallying hard on Friday when the Pboc reduced forward hedging margins cooled the greenback sell off. But traders started trimming Euro longs aggressively when a Reuters article surfaced that a report, written by six European Central Bank members, supported a very very gradual roll back of the QE program. The Dovish ECB narrative has always been an impediment to gains above the 1.200 level as the Doves are not happy with the rapid appreciation of the Euro more so given that the EU is still in recovery mode and a strong Euro hurts productivity

Australian Dollar

The Aussie is slipping lower on the back of the USD recovery overnight. As for the regional sentiment, the Greenback was also buttressed by a rebound in USDCNH after the pair rallied from a multi year low when PBoC reduced the onshore FX risk reserve requirement from 20% to 0%. While this does not signal or is intended to curb the RMB appreciation, it gave rise to consolidation and traders were more apt to book profits amid crowded positions. Similarly, extended long Aussie positioning also turned for the exits