Sample Category Title

US Backs Down on Tough North Korea Sanctions, Sterling Jumps on BoE Talk

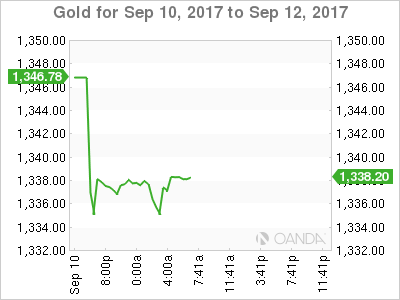

Dollar recovers mildly today as risk aversion eased slightly. Hurricane Irma is weakening as it moved past Tampa, Florida. Some analysts pointed out that damage of Irma is not as catastrophic as feared, even though it's still devastating. Meanwhile, North Korea risk is temporarily eased after the weekend. The US has backed down on pushing toughest sanctions on North Korea. A watered down version will be tabled for vote in UNSC today. While the greenback trades mildly higher, it's clearly outshone by Canadian Dollar and Sterling. Meanwhile, Yen and Swiss Franc are trading as the weakest ones. Gold is also notably weaker, hitting as low as 1335.2, comparing to Friday's high at 1362.4. WTI crude oil is hovering tight range below 48 handle.

US watered down its proposal on North Korea sanction, UNSC to vote

A major focus today will be on United Nation Security Councils' vote on fresh sanctions on North Korea. The US originally wanted to propose tougher measures that include bans on oil imports, textile exports and employment of works from North Korea. However, it's reported that the US has backed down and scaled back the proposal before the vote. Now, the revised draft dropped the proposed complete oil ban. It's changed to a cap on shipments of refined petroleum products at 2m barrels a year. Crude oil exports to North Korea would be maintained at current level. Workers ban was also diluted while freeze of leader Kim Jong-Un's assets and national airline Koryo is dropped too. But even after that, it's uncertain whether the proposal would be passed in UNSC. Two veto-holding members, Russia and China, are known to be against fresh sanctions on North Korea.

Meanwhile, geopolitical tension between the US and North Korea seemed to have eased moderately. North Korea did nothing provocative on the foundation day during the week end. However, North Korea did warned that "in case the U.S. eventually does rig up the illegal and unlawful 'resolution' on harsher sanctions, the DPRK shall make absolutely sure that the U.S. pays a due price.." And, "the forthcoming measures to be taken by the DPRK will cause the U.S. the greatest pain and suffering it had ever gone through in its entire history."

Sterling jumps on BoE talks, but it will face CPI test first

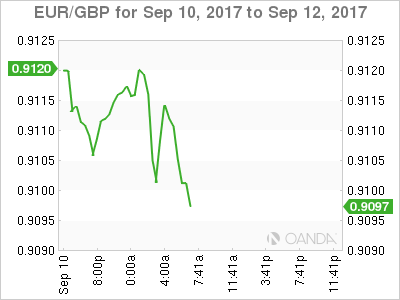

Sterling jumps broadly today on talk that BoE would step up its warning on interest rate later in the week. The central bank is widely expected to keep bank rate and asset purchase target unchanged. Based on current inflation outlook, there is also no imminent need for a hike. But BoE may reiterate that markets are under-estimating the scale of interest rate hikes in the coming years. And it may want households, business and investors to be well prepared. However, it should be noted that policy makers will have to look into inflation data to be released tomorrow. In particular, CPI is expected to climb back to 2.8% yoy in August. Any downside surprise there would intensify expectation that inflation won't hit 3% handle as BoE projected. And that would knock Sterling back down. Of course, focus will also be on whether hawks Michael Saunders and Ian McCafferty would change their mind on voting for rate hike too.

Before that, eyes will be on a parliamentary vote of the so called Brexit "Repeal Bill" today. In short, the bill seeks to copy and paste EU laws into UK legislation so that UK will have the same functioning laws and regulatory framework at the time of Brexit. Brexit Secretary David Davis warned that a vote against the bill is "a vote for chaotic exit from the European Union". And he emphasized that "businesses and individuals need reassurance that there will be no unexpected changes to our laws after exit day and that is exactly what the repeal bill provides. Without it, we would be approaching a cliff edge of uncertainty which is not in the interest of anyone." The government will need to secure the votes today to move on to the next phase of the legislation process. Opposition Labour Party has already indicated that they will vote against unless there are concessions.

ECB Coeure warned of exogenous shocks to the exchange rate

ECB Executive Board member Benoit Coeure said today "compared with past demand shocks, policy will remain more accommodative for longer, thereby likely muting further the pass-through of any growth-driven exchange rate appreciation." He noted that current recovery in Eurozone is "driven by domestic demand". Therefore, Euro strength might "have less of an impact on growth than, for example, after the Great Financial Crisis." Stronger than expected growth this is has prompted ECB policy makers to consider scaling back the quantitative easing program. Coeur noted that "at the current juncture, however, the policy-relevant horizon – the 'medium term' concept in our monetary policy strategy – is likely to be longer given the persistence of subdued inflationary pressures." And he warned that "exogenous shocks to the exchange rate, if persistent, can lead to an unwarranted tightening of financial conditions with undesirable consequences for the inflation outlook."

BoJ's ultra loose policy will destabilize the banking sector

A Japan Financial Services Agency adviser Naoki Ohgo warned that BoJ's stimulus program is severely cutting into bank profits. "Only a handful of regional banks successfully making money in niche areas." Others are struggling to find new business models. And, unless regional banks boost profitability it "might not take long" for BoJ's policies to finally destabilize the banking sector. Ohgo warned that "consolidation is inevitable". Meanwhile, Ohgo also pointed out that "despite abundant supply of cash in the economy, inflation did not reach 2 percent." Hence, "it's clear that monetary easing wasn't enough to generate inflation."

Released from Japan, machine orders rose 8.0% mom in July, M2 rose 4.0% yoy, tertiary industry index rose 0.1% mom in July. Machine tool orders rose 36.3% yoy in August.

China cut forex reserve requirement from 20% to 0%.

In China, the PBoC will unwind the rules on forex exchange forward reserve requirements that were implemented back in 2015. Back then the Renminbi exchange rate suffered prolonged depreciation after the devaluation in August 2015. The implementation of 20% reserve requirement was a move to halt the unwanted speculation in the exchanged rate. Effective today, the requirement is cut down to 0%. The move is seen by the markets as the government is adopting a more liberalized approach to Yuan trading. And it's also an act to soften restriction on capital outflow. Released over the weekend, China CPI accelerated to 1.6% yoy in August, up from 1.4% yoy. PPI slowed to 5.4% yoy, below 5.5% yoy.

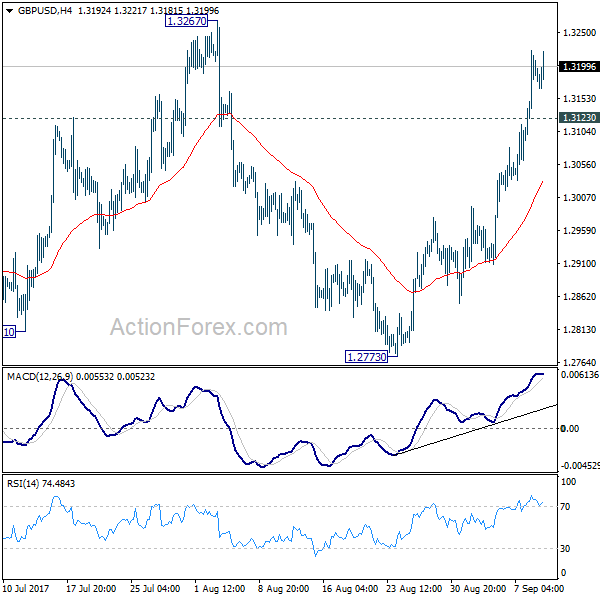

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3113; (P) 1.3168; (R1) 1.3245; More...

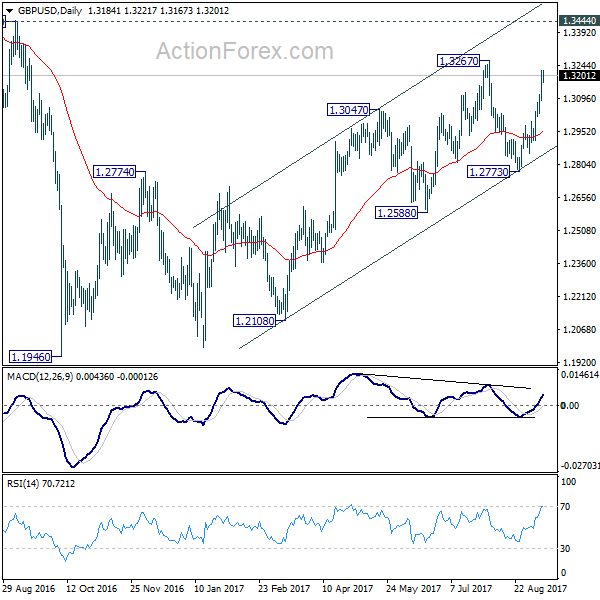

Intraday bias in GBP/USD remains on the upside and rise from 1.2773 should target 1.3267 resistance first. Break there will resume whole rise from 1.1946 and target 1.3444 key resistance next. But again, price actions from 1.1946 are still seen as a corrective pattern. Hence, we'd expect strong resistance from 1.3444 to limit upside to bring larger down trend reversal eventually. On the downside, below 1.3123 minor support will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2773 support will be the first sign that such down trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M Jul | 8.00% | 4.10% | -1.90% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Aug | 4.00% | 4.10% | 4.00% | |

| 4:30 | JPY | Tertiary Industry Index M/M Jul | 0.10% | 0.10% | 0.00% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Aug P | 36.30% | 28.00% | ||

| 12:15 | CAD | Housing Starts Aug | 223K | 220.0K | 222.3K |

Gold Retreats As Risk Appetite Returns

Gold gapped down on Monday, but with the Dollar vulnerable to further losses, the yellow metal will likely remain supported in the long-term.

Gold lost some of its sparkle on Monday, having hit its highest level in over a year in the previous session, as risk appetite flickered back to life.

The market players who were bracing for North Korea to conduct another missile launch over the weekend to mark their foundation day, were relieved when Pyongyang decided to host a celebration instead. This reprieve has rekindled appetite for riskier assets, and supported the Greenback while punishing safehavens such as Gold. While the yellow metal may continue to edge lower amid the risk-on trading environment, the lingering air of caution is likely to limit downside losses.

The Dollar is still vulnerable to further losses, as expectations rapidly fade over the Federal Reserve raising US interest rates in December, so Gold is likely to remain supported moving forward. Further upside is still on the cards, especially when considering how heightened political uncertainty in Washington, geopolitical tensions and Brexit concerns continue to stimulate the flight to safety.

From a technical standpoint, Gold bulls are still in the game, despite the nasty drop from over the weekend. A breakout above $1340 should encourage a further appreciation higher towards $1350. In an alternative scenario, a breakdown and repeated weakness under $1325 is likely to encourage a decline towards $1315 and $1300, respectively.

Dollar Gains Tentative Traction

Global equities and the U.S dollar are edging a tad higher this Monday morning, while haven assets retreat, as capital market fears ease about a standoff with North Korea and the impact of Hurricane Irma on the U.S economy.

Nonetheless, North Korea has warned of retaliation if the UN Security Council approves harsher sanctions in a vote later today.

The week ahead will feature an early look at how the eurozone's economic momentum is holding up in Q3, while consumer price data from the U.K and U.S. will show if those countries' central banks are getting any closer to their inflation targets.

The Bank of England (BoE) will hold its monetary policy meeting Thursday, the same day as the Swiss National Bank (SNB) will give its quarterly monetary policy assessment.

The volatile U.S retail sales date will close out the week on Friday giving the market a birds eye view on U.S consuming spending, while in Asia, the market will continue to monitor data from China with key industrial production and retail sales data scheduled. Down-under, Australia will release its jobs data on Thursday.

1. Global stocks edge higher

A weaker yen (¥108.40) boosted Japanese blue-chip stocks. Overnight, the Nikkei rallied +1.4%, after setting fresh four-month lows on Friday and logging its worst week in seven months. The broader Topix gained +1.2% on the lowest volume in a fortnight.

In South Korea, the Kospi was up +0.7%, while down-under, Australia's S&P/200 rose +0.7%.

In Hong Kong, stocks rallied the most in a week, encouraged by another case of Chinese state enterprise reforms and Beijing's loosening of controls to curb outflows that underlined rising confidence over the Yuan's value. The Hang Seng index rose +1.0%, while the China Enterprises Index gained +0.6%.

Note: The People's Bank of China (PBoC) scrapped two rules intended to support the yuan, showing that authorities are less worried about yuan depreciation after the currency's recent surge against the dollar.

In China, stocks were slightly higher, led by gains in shares of electric vehicle makers. The blue-chip CSI300 index was unchanged, while the Shanghai Composite Index added +0.3%.

In Europe, regional indices trade sharply higher across the board, led by Re-Insurers, as the impact from Hurricane Irma was less than feared.

In the U.S stocks are set to open in the black (+0.5%).

Indices: Stoxx600 +0.9% at 378, FTSE +0.6% at 7424, DAX +1.1% at 12432, CAC-40 +1.1% at 5170, IBEX-35 +1.4% at 10276, FTSE MIB +1.2% at 22026, SMI +0.6% at 8968, S&P 500 Futures +0.5%.

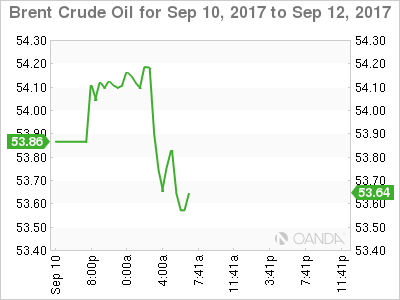

2. Oil weaker on U.S demand fears, gold lower

Ahead of the U.S open, oil prices are a tad lower on concerns that Hurricane Irma's pounding of Florida could dent oil demand. However, losses are being capped by weekend talks between the Saudi's and other OPEC members to possibly extend a pact to cut global oil supplies beyond next March.

Brent crude oil futures for November are down -5c at $53.73 a barrel, while benchmark U.S West Texas Intermediate crude (WTI) fell by -4c to $47.80.

Note: The market believes that Irma will have a negative impact on demand, but not on processing. Hurricane Harvey and Irma are expected to inflict a bearish shock on oil demand this month of about -600k bpd.

Gold prices are under pressure after hitting it's highest in over a year in Friday's session, as the dollar recovers from last week's lows and as the lack of geopolitical developments dented safe-haven appeal.

Spot gold is down -0.8% at +$1,335.10 an ounce – it rallied to +$1,357.54 on Sept. 8.

3. Sovereign yields back up

U.S yields are backing up a tad as market concerns about the impact of Hurricane Irma on the U.S economy is decreasing after it hit Florida yesterday with the strength of a Cat 4 storm, rather than a Cat 5 hurricane.

The 10-year U.S Treasury bond yield has edged up +3 bps to +2.09%.

In Germany, Bund yields briefly dipped this morning after comments from ECB board member Benoit Coeure that monetary policy is likely to remain more accommodative for longer. 10-year yields are trading at +0.33%.

Note: ECB President Draghi may have appeared ‘dovish' in his press conference last week, but German Bunds also have to deal with domestic ‘hawkish' unofficial guidance.

In the U.K, 10-year Gilt yields increased +2 bps to +1.01%.

Note: There's a Bank of England (BoE) monetary policy meeting Thursday, and inflation and employment data before that. Governor Carney is expected to hold rates steady despite a potential uptick in in inflation before the meet.

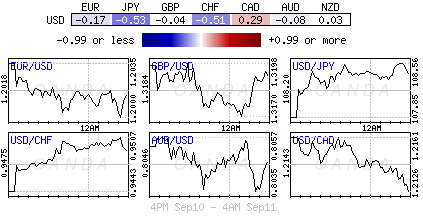

4. Dollar gains tentative traction

With North Korea not deploying any missiles and Hurricane Irma landing as a Cat 4 storm has had a negative impact on the risk aversion trade.

The EUR/USD continues to hover just north of the psychological €1.2000 handle. The single unit's soft tone has been aided by this morning ‘dovish' comments from ECB's Coeure who reiterated that the Council view that monetary policy would likely remain more accommodative for longer.

USD/JPY (¥108.50) is higher as the North Korean missile test failed to materialize for the time being. Reports are also circulating that a UN draft on North Korea dropped its call for an oil embargo of the country.

GBP/USD (£1.3135) is a tad higher ahead of the U.S open. Focus is on U.K's Parliament vote on Brexit repeal bill later today. Brexit Minister Davis warned of chaotic Brexit if Parliament blocked the repeal bill.

5. Norway goes to the polls

Norway goes to the polls today to decide whether the Conservative Prime Minister, Erna Solberg, or her Labour rival, Jonas Gahr Store, will lead the country for the next four years.

The contest looks too close to call, with Solberg's right wing bloc of parties and Store's left wing opposition group neck-and-neck.

The results for a half dozen smaller parties will be critical.

Note: Voting ends at 3:00 pm EDT with exit polls expected immediately after.

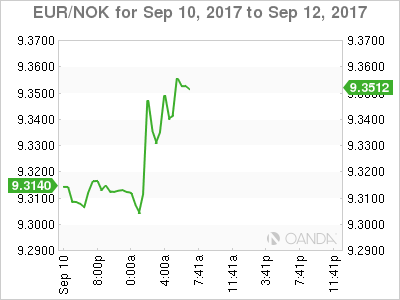

The NOK ($7.7800) is a tad softer after Norway's August CPI data came in lower-than-expected – m/m -0.8% vs. -0.4%e, y/y +1.3% vs. +1.7%e. Today's inflation data is unlikely to alter the Norges Bank's outlook.

Market Update – European Session: Risk Appetite Finds Fresh Legs After The Most Severe Scenarios Of Weekend Events Failed...

Notes/Observations

Risk appetite finds some room as threats of North Korea escalation and the most severe US hurricane scenarios have been temporarily avoided

Inflation in Norway slipped unexpectedly in August.

Focus was on UK Parliament vote on Brexit repeal bill later today. Brexit Min Davis warned of chaotic Brexit if Parliament blocked the bill

Overnight/weekend

Asia:

No North Korea missile test/launch detected on the 69th anniversary of NK National Founding Day

North Korea reiterated view that closely following US' moves with 'vigilance'; ready and willing to use 'any form of ultimate means'. Warned of retaliation if UN Security Council approved US request for further sanctions - KCNA

US called for a vote on Monday, Sept 11th concerning Draft UN Security Council resolution on additional sanctions on North Korea

China Aug CPI Y/Y: 1.8% v 1.6%e; PPI Y/Y: 6.3% v 5.7%e

China PBOC said to have removed reserve request for offshore bank yuan accounts (reflect major changes of market environment currently)

Europe:

UK Brexit Min Davis said to warn of chaotic Brexit if Parliament block bill. Without repeal bill we would be approaching a cliff edge of uncertainty

UK Aug Visa Consumer Spending y/y: +0.3% v -0.8% prior (1st increase since Apr)

Greece PM Tsipras: Determined to speed up conclusion of 3rd bailout review. Wants IMF to decide if it will join 3rd bailout by end-2017

Americas:

Hurricane Irma made landfall in Florida as a category 4 storm

Energy:

Saudi Arabia Energy Ministry stated that Al-Falih discussed with his Venezuelan and Kazakh counterparts the possible extension of the global oil supply cut pact beyond March 2018

Economic data

(NO) Norway Aug CPI M/M: -0.8% v -0.4%e; Y/Y: 1.3% v 1.7%e

(NO) Norway Aug CPI Underlying M/M: -0.9% v -0.4%e; Y/Y: 0.9% v 1.4%e

(SE) Sweden Aug PES Unemployment Rate: 4.1% v 4.0% prior

(FR) Bank of France Aug Business Sentiment: 104 v 106e

(CZ) Czech Aug CPI M/M: -0.1% v -0.1%e; Y/Y: 2.5% v 2.6%e

(TR) Turkey Q2 GDP Q/Q: 2.1% v 1.8%e; Y/Y: 5.1% v 5.3%e; GDP (unadj): 6.5% v 5.2%e

(DK) Denmark Aug CPI M/M: -0.3% v -0.5%e; Y/Y: 1.5% v 1.3%e

(DK) Denmark Aug CPI EU Harmonized M/M: -0.4% v +1.0% prior; Y/Y: 1.5% 1.5% prior

(IT) Italy July Industrial Production M/M: +0.1% v -0.4%e; Y/Y: 4.4% v 5.3% prior; Industrial Production WDA Y/Y: 4.4% v 3.7%e

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.9% at 378, FTSE +0.6% at 7424, DAX +1.1% at 12432, CAC-40 +1.1% at 5170, IBEX-35 +1.4% at 10276, FTSE MIB +1.2% at 22026, SMI +0.6% at 8968, S&P 500 Futures +0.5%]

Market Focal Points/Key Themes:

European Indices trade sharply higher across the board being led by Re-Insurers as the impact from Hurricane Irma was less than feared. Hannover Re, Swiss Re and Munich Re are all outperforming in Europe.In the UK Associated British Foods trades lower after there Full year Trading update, reporting strong sales especially from Primark, which reported sales up 13% (cc). Meanwhile Roche trades lower weighing on the Swiss SMI after its BRIM8 phase 3 study failed to meet primary endpoint.

Equities

Consumer discretionary [Air Berlin [AB1.DE] +13% (Hans Rudolf Wohrl offers up to €500M), Associated British Foods [ABF.UK] -2.2% (Trading update)]

Financials: [Beazly [BEZ.UK] +6%, Munich Re [MUV2.DE] +4.2%, Hannover Re [HNR1.DE] +4.4%, Swiss Re [SREN.CH] +4.5% (Hurricane Irma initial loss estimates less then originally forecast)]

Healthcare: [Roche [ROG.CH] -1.1% (Zelboraf (vemurafenib) failed to reduce the risk of melanoma recurring, compared with the placebo), Pharming Group [PHARM.NL] +5.6% (Concludes interactions with FDA)]

Speakers

ECB's Coeure (France): Exogenous shocks to exchange rate if persistent can lead to unwarranted tightening of financial conditions. Policy to remain more accommodative for longer, thereby muting further the pass-through of any growth-driven exchange rate appreciation. Transmission of monetary policy that the policy-relevant horizon likely to be longer given the persistence of subdued inflationary pressures

German govt said to seek Weidmann as next ECB chief when Draghi terms ends in 2019

Poland Central Bank's Lon: Saw need for 50bps cut in Base Rate

South Africa Fin Min Gigaba: Cautious on recovery in consumer spending

Thailand Central Bank reiterated view that current monetary stance is appropriate

Thailand Finance Ministry said to propose that central bank cut interest rates to boost investment

Currencies

The week began with a decrease in decline in risk aversion sentiment as North Korea held off any additional missile tests while Hurricane Irma’s wrath did not cause the extensive damage in Florida

North Korea marked the 69th anniversary of its founding on Saturday without resorting to any further missile or nuclear tests, fuelling some unwinding of safe-haven bets such as gold and government debt

EUR/USD hovering around the 1.20 level. The soft tone for Euro aided by dovish commentary from ECB’s Coeure who reiterated Council view that monetary policy would likely to remain more accommodative for longer.

USD/JPY was higher as the North Korean missile test failed to materialize for the time being. Reports also circulated that UN draft on North Korea dropped its call for an oil embargo of the country

GBP/USD was fractionally lower in the session. Focus was on UK Parliament vote on Brexit repeal bill later today. Brexit Min Davis warned of chaotic Brexit if Parliament blocked the repeal bill.

The NOK was softer after Norway Aug CPI data came in lower-than-expected. EUR/NOK higher by 0.3% to test above 9,35 level. The NOK was off its worst levels of the session as dealers believed the data Inflation unlikely to alter the Norges Bank's outlook

Fixed Income

Bund futures trade at 162.84 down 12 ticks trading lower on rising equities as the absence of activity from North Korea as well as Hurricane Irma damages being less than feared helped prop markets. Continued downside targets 162.53 while upside resistance stands initially at 163.22.

Gilt futures trade at 127.49 down 22 ticks with continued downside eyeing 127.25, then 126.88. A reversal targets 127.90 then 128.24.

Monday's liquidity report showed Friday’s excess liquidity rose to €1.778T from €1.775T and use of the marginal lending facility fell to €142M from €1.01B.

Corporate issuance saw $46.2B last week via 63 tranches, bringing YTD issuance to above $980B. For the week ahead analysts forecast around $25B to come to market.

In Euro denominated issuance ~€35B came to market via 41 issuers and 46 tranches marking the busiest day in Q3. Thursday saw the bulk of the issuance with just shy of €20B coming to market.

Looking Ahead

(UK) Parliament vote on Brexit repeal bill

05:30 (DE) Germany to sell €2.0B in 6-month BuBills

06:00 (IL) Israel Aug Consumer Confidence: No est v 116 prior

06:45 (US) Daily Libor Fixing

07:00 (IN) India announces details of upcoming bond sale (held on Fridays)

07:00 (BR) Brazil Sept IGP-M Inflation (1st Preview): 0.3%e v 0.0% prior

07:00 (CZ) Czech Central Bank to comment on CPI data

07:25 (BR) Brazil Central Bank Weekly Economists Survey

07:30 (TR) Turkey TCMB Survey of Expectations

08:00 (PL) Poland Aug Final CPI M/M: No est v -0.2% prelim; Y/Y: No est v 1.8% prelim

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

08:05 (UK) Baltic Dry Bulk Index

08:15 (CA) Canada Aug Annualized Housing Starts: 216.0Ke v 222.3K prior

09:00 (MX) Mexico July Industrial Production M/M: -0.1%e v +0.1% prior; Y/Y: -0.2%e v -0.3% prior; Manufacturing Production Y/Y: 2.4%e v 2.3% prior

09:00 (RU) Russia July Trade Balance: $6.5Be v $8.7B prior; Exports: $27.4Be v $29.5B prior; Imports: $21.0Be v $20.8B prior

09:00 (FR) France Debt Agency (AFT) to sell combined €4.0-5.2B in 3-month, 6-month and 12-month Bills

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

09:50 (UK) BOE to buy £1.125B in in APF Gilt purchase operation (3-7 years)

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

13:00 (US) Treasury to sell 3-Year Notes

14:15 (DE) German Chancellor Merkel takes questions at Televised Town-Hall Event in Luebeck

16:00 (US) Weekly Crop Progress Report

(MX) Mexico Aug ANTAD Same-Store Sales Y/Y: No est v 4.0% prior

USD/CAD – Canadian Dollar Rally Continues, Canadian Housing Report Next

The Canadian dollar has started the week with gains. Currently, USD/CAD is trading at 1.2107, down 0.43% on the day. On the release front, it’s a quiet day, with only one Canadian release, Housing Starts. The indicator is expected to slow to 216 thousand in August. There are no US releases on the schedule. On Tuesday, the US releases JOLTS Job Openings, with a forecast of 5.96 million.

Aside for a housing report later on Monday, there is only one other Canadian event this week – the New Housing Price Index. This means that much of this week’s movement of USD/CAD will be due to readings from US indicators, notably inflation and retail sales data. Will the Canadian dollar rally continue? The currency has now put together 4 consecutive winning weeks, and was boosted last week by the Bank of Canada, which caught markets by surprise when it raised the benchmark rate 25 basis points to 1.00%, up from 0.75%. Last week, USD/CAD dropped to a low of 1.2060, its lowest level since May 2015. Will the pair fall below the symbolic 1.20 level this week?

The week has started with 'R&R' – Relief and Risk, as global stock markets are responding positively to the lack of any hostile moves by North Korea over the weekend. With North Korea celebrating its 69th anniversary of independence, there were concerns that Pyongyang would use the occasion to flex some muscle and test a nuclear bomb or missile. North Korea marked last year’s anniversary by exploding its fifth nuclear test. This occasion passed without incident, although the US, along with its allies Japan and South Korea, remain on alert for further provocations from the north. Asian and European stock markets have started the week with solid gains, as investors are displaying a greater appetite for risk. This could translate into gains for risk currencies such as the Canadian dollar.

The US economy has been performing well, as underscored by an excellent second quarter GDP and a labor market which remains close to capacity. Still, inflation levels remain stubbornly low. Wage pressure has been limited, despite the fact that many businesses cannot fill job openings. Weak inflation has hampered the Fed’s plans to raise interest rates a third time this year, and the odds of a December hike have dipped to just 31%, as the markets are increasingly doubtful that the Fed will make a move before next year.

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

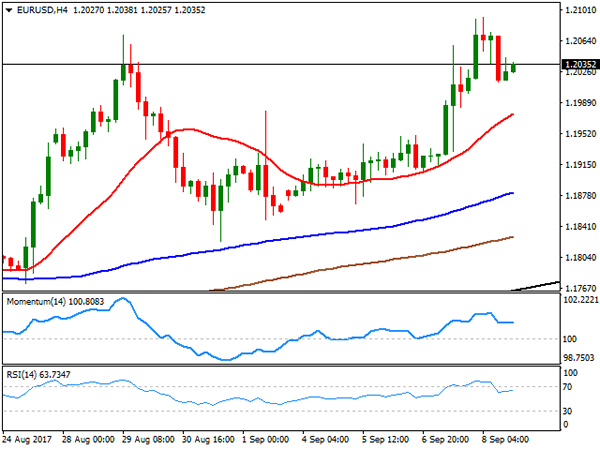

EUR/USD

The EUR/USD pair posted its best weekly close for the year, ending at 1.2035, after the ECB' monetary policy announcement on Thursday fueled demand for the common currency. The Central Bank left rates and the QE program unchanged, but in the press conference, head's Draghi reckon that they will discuss how to unwind facilities next October. Even if policy makers decide to maintain QE in place until December, a couple of months´ delay doesn't affect market's mood towards the EUR, moreover as the greenback was unable to find its footing for one more week. Escalating tensions between the US and North Korea kept it subdued at the beginning of the week, falling further later on the back of soft macroeconomic data exacerbated by the damages produced by Hurricane Harvey last week. Hurricanes and tropical storms hit the US this weekend, and fears on how it would affect the real economy, also weighed on the greenback.

The pair topped at 1.2092 on Friday, retreating in the US afternoon on profit taking ahead of the weekend, but ending up with gains for the day. The bullish potential remains intact for the upcoming days, with investors now eyeing the upcoming Fed´s monetary policy meeting next September 19-20th. In the meantime, the daily chart shows that the 20 DMA has gained upward strength below the current level, whilst technical indicators have eased modestly from overbought readings, far from suggesting upward exhaustion. The long term daily ascendant trend line coming from 1.0603, comes around 1.1780, the level to break to talk about an interim top and a possible trend reversal. Shorter term, and according to the 4 hours chart, the risk is towards the upside, as the price settled well above all of its moving averages, with the shortest currently around 1.1975, and technical indicators having stabilized well into positive territory after correcting overbought conditions.

Support levels: 1.2010 1.1975 1.1940

Resistance levels: 1.2070 1.2105 1.2150

USD/JPY

The USD/JPY pair plunged to a fresh 2017 low of 107.31 early Friday, as investors kept dumping the greenback following Thursday's ECB announcement and rushed towards safety ahead of the storms that hit the US this weekend, and on dovish Fed speakers´ comments. US Treasury yields fell to their lowest since the November election, with the 10-year note benchmark touching 2.02% before ending the week at 2.06%. The yield for the 30-year note ended the week at 2.68%. This week will start with Japan releasing July trade balance and Machinery Orders figures, alongside with industrial data for August. From a technical point of view, the pair has room to extend its decline, having settled below the previous yearly low, and with the daily chart showing that the RSI indicator keeps heading south, around 36, as the 100 and 200 SMAs gain downward strength far above the current level. For the shorter term, the 4 hours chart shows that the price is also well below bearish moving averages, whilst technical indicators settled well into the red, after correcting extreme oversold conditions reached at the beginning of the day, also supporting a new leg lower ahead.

Support levels: 107.65 107.30 106.90

Resistance levels: 108.10 108.45 108.90

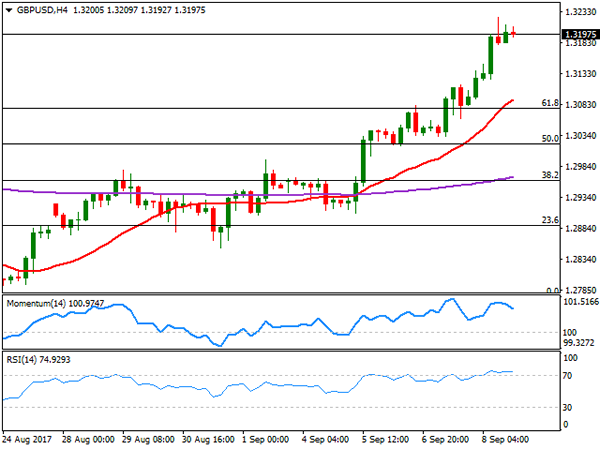

GBP/USD

The Pound had its best week in over two months against the greenback, rising up to 1.3223 on Friday to settle around the 1.3200 mark. The UK currency got help from encouraging local data, as industrial production rose by 0.2% in July, while on yearly basis output rose 0.4%. Manufacturing production increased by 0.5% in the month, and by 1.9% when compared to a year earlier, a significant improve for the beginning of the third quarter. Also, the UK's July goods trade deficit stood at £11.58 billion slightly below the £11.95 deficit expected. Anyway, market's choice to dump the dollar was the main driver for the GBP/USD pair's rally. Brexit headlines and the subsequent concerns have been left aside lately, but the lack of progress in negotiations hang over the Pound as a Damocles´ sword, and negative news could see the pair falling as quick as it rose these last few days. For now, the technical picture favors additional advances, as in the daily chart, technical indicators maintain their strong upward momentum, despite being in overbought territory, with a logical bullish target being 1.3266, August monthly high. In the 4 hours chart, the 20 SMA heads north below the current level, having surpassed the 61.8% retracement of the August decline around 1.3080, while technical indicators have lost upward strength, but remain within overbought territory, all of which maintains the risk towards the upside.

Support levels: 1.3180 1.3130 1.3090

Resistance levels: 1.3225 1.3665 1.3300

GOLD

Spot gold closed Friday at $1,346.63 a troy ounce, up for the week, but flat on the day. The bright metal surged to 1,357.49, its highest since July 2017 on dollar's sell-off, but corrected lower ahead of the close on profit taking. The metal is up for third consecutive week, as geopolitical jitters coupled with US Fed´s speakers dovish comments about the economy and possible upcoming rate hikes. The commodity may be traded with a cautious stance these upcoming days and ahead of Fed's announcement, but the upside remains favored, as despite some possible relief upward corrections, there are no bases for a dollar's appreciation. From a technical point of view, the daily chart shows that technical indicators keep hovering within overbought territory, whilst the price is far above a firmly bullish 20 SMA, this last around 1,310.00, all of which supports the ongoing bullish trend. In the 4 hours chart, the price settled above a bullish 20 SMA, this last around 1,342.70, providing an immediate support, while technical indicators stand directionless within positive territory.

Support levels: 1,342.70 1,331.60 1,325.00

Resistance levels: 1,352.55 1,363.40 1,372,90

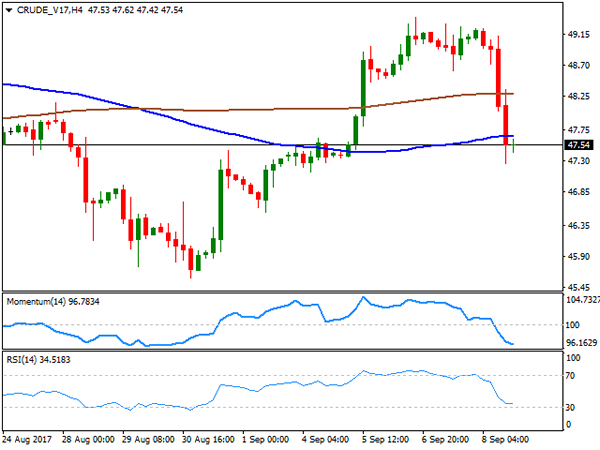

WTI CRUDE OIL

Crude oil prices plummeted on Friday to trim most of their weekly gains, amid news indicating that US refineries are recovering slowly from the destruction caused by Hurricane Harvey. Over 10% of US refinery capacity remained down, ahead of another batch of tropical storms hitting the country this weekend. West Texas Intermediate crude futures ended at $47.54 a barrel, after trading as highs as 49.40 mid-week. Additionally, the Baker Hughes report released on Friday shows that the number of active rigs drilling for oil fell just by 3, down to 756 for the week, somehow indicating that strong pumping will keep the market oversupplied. The daily chart shows that, after repeatedly failing to surpass its 200 DMA, the price plunged straight down to its 100 DMA, whilst technical indicators turned south, entering bearish territory, indicating that further declines are likely on a break below 47.20. In the 4 hours chart the price settled below its 100 and 200 SMAs, whist technical indicators stand near oversold readings, having barely lost their bearish strength, also supporting additional declines ahead.

Support levels: 47.20 46.60 36.10

Resistance levels: 48.10 48.70 49.40

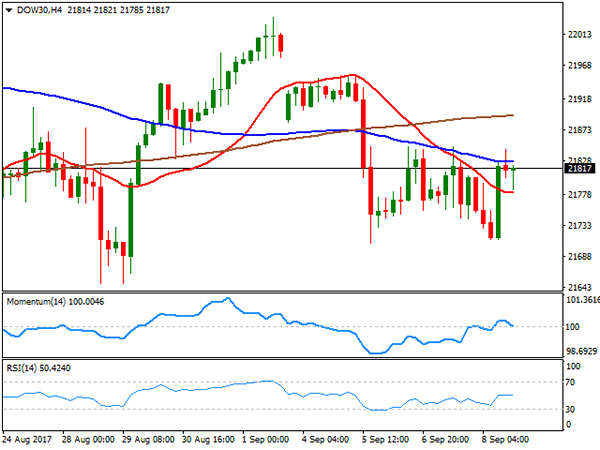

DJIA

The Dow Jones Industrial Average managed to add 13 points on Friday to settle at 21,797.79, but the Nasdaq Composite and the S&P closed in the red, down to 6,360.19 and 2,461.43 respectively. Appetite for riskier assets among stocks traders was subdued ahead of the upcoming hurricanes that hit the US during the weekend, and fears of another missile test in North Korea. The weekend passed with the first having produced less damage that initially expected and with N. Korea quiet, which could lift market's sentiment at the beginning of the week. Within the Dow, Travelers led, up 3.98%, followed by Home Depot that added 1.10%. The technology sector was the worst performer, with Apple leading losers , down 1.63%, followed by Wal-Mart that shed 1.55%. The daily chart shows that the index closed right below its 20 DMA for a third consecutive day, while technical indicators aim marginally higher within neutral territory, not enough to confirm further advances but limiting chances of a steeper decline. In the 4 hours chart, the index settled between its 20 and 100 SMAs, while technical indicators turned modestly lower within neutral territory, in line with a longer term perspective.

Support levels: 21,785 21,740 21,707

Resistance levels: 21,845 21,891 21,932

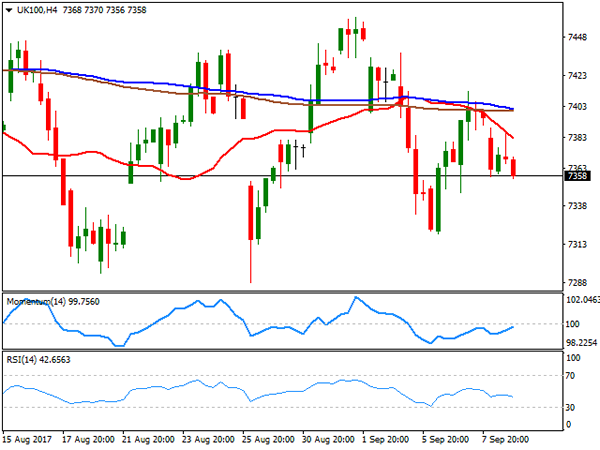

FTSE100

The FTSE 100 closed the week at 7,377.60, down on Friday by 19 points, and almost 1.0% for the week, with plummeting metals' prices pressuring the mining-related sector. A stronger Pound, which surged to its highest in over a month, added pressure to the Footsie. BHP Billiton led decliners, as oil prices fell sharply, losing 3.77%, followed by Antofagasta that shed 3.72%. Anglo American, Rio Tinto and Fresnillo lost over 3% each. St. James's Place was the best performer, adding 2.15%, while banks enjoyed a quiet data, with Barclay's following, up 1.96%. The daily chart shows that the index remains lacking clear directional strength, still hovering around its 20 and 100 DMAs, having settled for the week below them, as technical indicators lost upward strength around their mid-lines. Shorter term, and according to the 4 hours chart, the risk is towards the downside, as the index settled below all of its moving averages, with the 20 SMA accelerating south and currently at offering a dynamic resistance at 7,382, as technical indicators hover within negative territory, with the RSI turning south around 42, anticipating some further slides for this Monday.

Support levels: 7,333 7,288 7,261

Resistance levels: 7,382 7,413 7,444

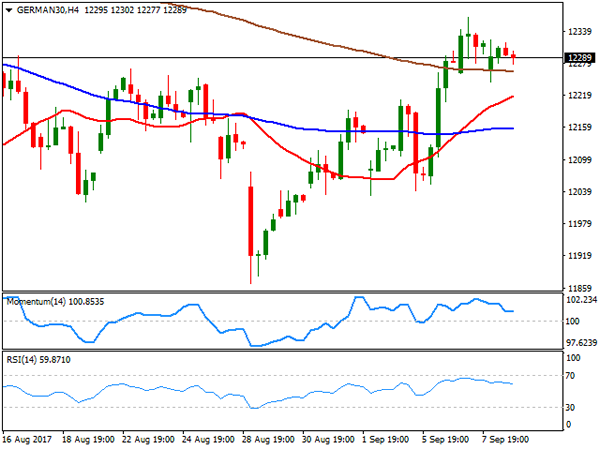

DAX

European equities closed little changed on Friday, easing at the end of the session amid fears over another missile test coming from North Korea and the hurricanes affecting the US Atlantic coast. The German DAX closed 7 points higher at 12,304.00, up anyway for the week, compliments to ECB's positive outlook of the local economy. ThyssenKrupp was the best performer, up 1.67% for the week, followed by Commerzbank, which added 1.04%. ProSiebenSat.1 on the other hand, led decliners, down 1.27%, followed by Bayer that shed 0.90%. From a technical point of view, the daily chart shows that the index maintains a modestly positive stance, trading above its 20 and 200 DMAs, but lacking momentum, as technical indicators head nowhere within positive territory. In the 4 hours chart, the index settled above all of its moving averages, despite having retreated from its weekly high, whilst technical indicators also consolidate within positive territory.

Support levels: 12,241 12,207 12,166

Resistance levels: 12,301 12,342 12,383

Technical Outlook: Gasoline Remains Firmly In Red, Bears Eye Daily Cloud Top At $1.6046

Gasoline future contract remains firmly in red for the seventh straight day and probes below support at $1.6274 (Fibo 76.4% of 1.5364/1.9221 upleg).

Bears eye strong support at $1.6046, provided by the top of thick daily cloud (cloud is spanned between $1.6046/1.5394) and reinforced by daily MA’s (55SMA at 1.6033, 200SMA at $1.5874 and 100SMA at $1.5743) where near-term bears from $1.9221 (30 Aug peak) would face strong headwinds.

Oversold slow stochastic on daily chart also supports scenario.

Overall bulls have been dented by recent fall but will remain in play if abovementioned supports contain recent bearish acceleration.

Otherwise, further retracement of larger 1.3953/1.9221 (21 June / 30 Aug rally) could be expected on break lower.

Res: 1.6570, 1.6725, 1.6935, 1.7026

Sup: 1.6200, 1.6046, 1.5874, 1.5743

Technical Outlook: WTI OIL – Downside Risk Will Remain In Play While $48.00 Zone Caps

WTI oil price edged higher on Monday but upside attempts were so far capped under $48.00 barrier. Consolidation is holding between daily Tenkan-sen ($47.48) and daily Kijun-sen ($47.92) with limited upside action as Friday's long bearish candle that completed reversal pattern, weighs. The oil price fell sharply on Friday on concerns of stronger impact from Hurricane Irma on refining infrastructure that would lower demand for crude oil. On the other side, the price failed to extended deeper into thickening daily cloud and stayed above plethora of daily MA supports (10/20 and 55/100SMA bull-crosses are forming) that may offer an additional support and limit losses. Bullish scenario requires close above daily cloud and lift above $48.08 (Fibo 38.2% of $49.40/$47.26 downleg) to generate bullish signal, as daily studies are mixed. Otherwise, downside is expected to remain at risk while $48.00 resistance zone caps. Extension and close below Friday's low at $47.26 will be bearish signal for fresh weakness towards next pivot at $47.03 (Fibo 61.8% of $45.57/$49.40 upleg).

Res: 47.92, 48.08, 48.33, 48.58

Sup: 47.56, 47.34, 47.26, 47.03

CRUDE OIL Sharp Decline

Crude oil has strongly declined after the commodity monitored the $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance can be found at 50.43 (31/07/2017). Expected to show continued short-term bearish move.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Pushing Higher

Silver has broken its key resistance at 17.75 opening the way for a test of the strong resistance at 18.65 (17/04/2017 high) while support can be found at 16.58 (15/08/2017 high). The commodity lies in an uptrend channel. Expected to show another leg higher.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).