Sample Category Title

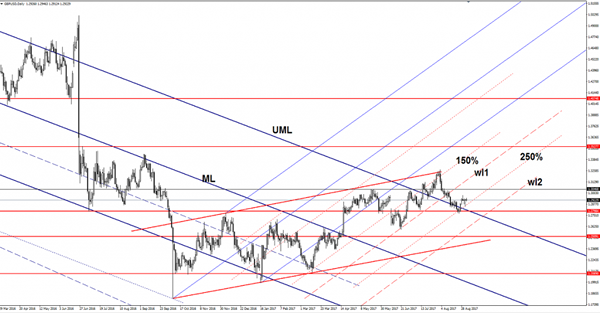

GBP/USD Bloodless

Price posted humble gains today and looks undecided on the short term. Is narrowing and waits for a bullish spark to be able to climb much higher in the upcoming period. GBP/USD maintains a bullish perspective on the daily chart as the uptrend is unharmed.

It could climb much higher in the upcoming days if the dollar index will slide further, the USDX hovers above the 92.49 static support, only an accumulation will signal another rebound.

Is premature to talk about a broader rebound on the dollar index because it's still trapped under a very strong dynamic resistance.

Technically, the GBP/USD is expected to climb much higher on the short term, but you should be careful because the fundamental factors will take the lead today. The United States will release high impact data in the afternoon, so a high volatility is expected.

GBP/USD is trading near the half of the ascending channel maintaining a bullish perspective on the daily chart after the false breakdown below the upper median line (UML) of the major descending pitchfork. Could retest the 250% Fibonacci line (ascending dotted line) before will climb much higher.

It's moving sideways, but I hope that we'll have a clear direction after the afternoon storm. This is a crucial day for the US dollar, the economic data could ruin or lift it. The economic calendar is filled with high impact data, so you should be careful not to suffer a heavy loss.

Price stands above the Monday's gap up, maintaining a bullish bias, a retest of the 250% Fibonacci line could bring more buyers. The next upside target will be at the 1.3046 static resistance, only a drop under the, mentioned dynamic support will signal a drop towards the 1.2798 critical support.

CAD And Oil Rebound In Tandem, Commodities Ended August On A Positive Note

Greenback Rallied Then Reversed. The U.S. currency was off to a good start as headlines contained several positive updates for the economy, but end-of-the-month profit-taking eventually took hold after US Treasury Secretary Mnuchin tried to talk the dollar down noting that a lower US Dollar is good for US trade.

CAD Takes A New Run. The Loonie was the big winner for the day as monthly GDP release came out stronger-than-expected, getting an extra boost from higher oil and lower USD. Market watchers seem to be buzzing about another Bank of Canada interest rate hike.

Gold Rallied Up Off Of $1,300. US Treasury Secretary Mnuchin speech sparked a rebound in gold up off of $1,300 back toward $1,320 and enabled EUR and GBP to cut early losses.

Oil Turning Sharply Upward. Crude oil ticked higher on reports of lower natural gas storage levels and an expected surge in gasoline demand during the U.S. Labor Day long weekend.

Watch Out Today For:

12:30 pm GMT: USD Nonfarm Payrolls

14:00 pm GMT: USD ISM Manufacturing PMI

European Open Briefing: Asian Markets Got Off To A Slow Start On September Ahead Of The NFP

Global Markets:

- Asian stock markets: Nikkei up 0.02 %, Shanghai Composite rose 0.48 %, Hang Seng climbed 0.25 %, ASX 200 rose 0.19 %

- Commodities: Gold at $1324.62 (+0.18 %), Silver at $17.50 (+0.18 %), WTI Oil at $46.92 (-0.68 %), Brent Oil at $52.72 (-0.25%)

- Rates: US 10-year yield at 2.12, UK 10-year yield at 1.03, German 10-year yield at 0.35

News & Data:

- EUR German Retail Sales m/m -1.2 % vs -0.5 % expected

- EUR CPI Flash Estimate y/y 1.5 % vs 1.4 % expected

- EUR Core CPI Flash Estimate y/y 1.2 % vs 1.2 % expected

- CAD GDP m/m 0.3 % vs 0.1 % expected

- USD Unemployment Claims 236 K vs 237 K expected

- USD Personal Spending m/m 0.3 % vs 0.4 % expected

- USD Chicago PMI 58.9 vs 58.7 expected

- USD Pending Home Sales m/m -0.8 % vs 0.4% expected

- CNY Caixin Manufacturing PMI 51.6 vs 50.9 expected

- JPY Final Manufacturing PMI 52.2 vs 52.8 expected

- Crude falls as flooding from Harvey roils U.S. oil industry- RTRS

- U.S. job growth likely slowed in August; wages seen tepid- RTRS

Markets Update:

Asian markets got off to a slow start on September ahead of the NFP. After gains on Wall Street to end August, moves were widely muted early on Friday. Equities fluctuated in Tokyo, Seoul and Sydney after the MSCI Asia Pacific Index completed its eighth straight month of gains and nudged closer to its highest in almost a decade.

USDJPY is currently seen trading around 110.03, The dollar's recent advance slowed as rate hike expectations were dented. Overall The yen fell less than 0.1 percent against the US dollar after rising 0.2 percent in the previous session. Data from Japan today was disappointing for capex, and the final reading for Nikkei manufacturing PMI slipped back from its preliminary reading.

EUR/USD is little changed on the session, with the EURO currently seen trading at 1.1895 against the US Dollar after falling to a one-week low of $1.1823 overnight. The dollar index against a basket of six major currencies is currently unchanged 92.69. The index has managed to bounce back yesterday without hitting it’s 2-1/2-year low of 91.621.

AUDUSD is currently seen trading at 0.7940, Price had managed to climb up to high of 0.7955 early on Friday from the initial lows of 0.7940 before falling back again and currently remains net unchanged for the session. NZD/USD is currently seen trading near it’s opening price at 0.7170 after falling from session highs of 0.7190. Most of the Currencies had similar small ranges, which is hardly surprising for the Asian day ahead of the US NFP.

Upcoming Events:

- 07:15 GMT – (EUR) Spanish Manufacturing PMI

- 08:30 GMT – (GBP) Manufacturing PMI

- 12:30 GMT – (USD) Average Hourly Earnings m/m

- 12:30 GMT – (USD) Non-Farm Employment Change

- 12:30 GMT – (USD) Unemployment Rate

- 14:00 GMT – (USD) ISM Manufacturing PMI

- 14:00 GMT – (USD) Revised UoM Consumer Sentiment

Elliott Wave View: GBPJPY Turning Lower

GBPJPY Short Term Elliott Wave suggests that the decline to 8/23 low at 139.27 ended Minor wave W. Minor wave X bounce is proposed complete at 142.93 as a double three Elliott Wave Structure. Minute wave ((w)) of X ended at 141.47, Minute wave ((x)) of X ended at 139.98, and Minute wave ((y)) of X is proposed complete at 142.93. Near term, while bounces stay below 142.93, expect pair to turn lower again. If pair breaks above 142.93 from here, the move higher from Minor W can be counted as a triple three. In this case, it will open extension higher to 143.75 – 144.27 area before pair turns lower.

GBPJPY 1 Hour Elliott Wave View

Double Three is the most important pattern in Elliott wave’s new theory. It’s probably the most common pattern in the market these days. Double three is also known as a 7-swing structure. It is a very reliable pattern that gives traders a good opportunity to trade with a well-defined level of risk and target areas. The image below shows what Elliott Wave Double Three looks like. It has labels (W), (X), (Y) and an internal structure of 3-3-3. This means that all 3 legs has corrective sequences. Each (W) and (Y) is formed by 3 waves oscillation and has a structure of A, B, C or W, X, Y of smaller degrees.

With Inflation Soft, How Important Is US Jobs Data?

- US jobs report today's main event;

- Eurozone PMIs could provide a further headache for the ECB.

- Friday is likely to cap off what has already been another eventful week for the markets.

The week started with a missile launch from North Korea and tropical storm in the US but attention has gradually been diverted to the fundamentals, with numerous pieces of data being released over the last couple of days. Risk appetite has gradually improved throughout the week following a rather shaky start, which is normal during periods of heightened geopolitical risk, but the data we've seen has been a bit of a mixed bag.

The US jobs report headlines today's releases but with yesterday's inflation numbers once again highlighting the subdued price pressures in the country, you wonder how great an impact today's numbers will have on the Federal Reserve. The central bank has already achieved its target of maximum employment, at least as far as the headline figures suggest, and yet inflation has been gradually declining this year – as per the core PCE price index. This is also happening despite the dollar index having fallen almost 10% since the start of the year to hit its lowest since the start of 2015.

Still, the jobs data does tend to generate a lot of hype and therefore volatility and I expect the same will be the case today. While the most important release at the moment is the average earnings number – as without improvements here, the Fed's 2% target will be difficult to achieve – it's the NFP and unemployment figures that tend to grab traders attention initially. Market expectations are for 180,000 jobs to have been created last month leaving unemployment at 4.3%, although it should be noted that ADP reported 237,000 on Wednesday. While not always accurate, the number may suggest expectations are far too low.

Prior to this, we'll get manufacturing PMIs from across the eurozone this morning. While these are revised figures, which typically means the market impact is lessened, the improvement in the economy and confidence in the recovery has been impressive. With the euro trading around its highest levels in more than two and a half years against the dollar, inflation building – albeit from low levels – and the ECB considering tapering, traders may be watching today's figures quite closely. The euro is potentially looking a little overbought at the moment and responses to the data can often provide a signal of this.

Ahead of the European open, markets are trading relatively flat and equity markets are expected to open in much the same way. It will be interesting to see whether weekend risk is seen as we head into the close today, given the heightened geopolitical risk environment.

Market Update – Asian Session: FX And Equity Markets Generally Quiet Ahead Of US Payrolls

Asia Summary

With the US payrolls report due later today, Asian equity markets have generally seen little volatility. The S&P ASX 200 conducted its quarterly rebalancing (Charter Hall Long Wale Reit, NIB Holdings, Washington H Soul Pattinson added; Isentia, Sky Network TV and Virtus Health removed).

On data front, Japan’s Q2 CAPEX missed expectations and this has led to speculation that Q2 GDP could be revised lower from the preliminary annualized reading of 4.0%. South Korea’s Aug CPI rose at the fastest pace in over 5-years and the government attributed the increase to temporary factors. China’s Aug Caixin Manufacturing PMI, which hit the highest level since Feb, had little noticeable impact on markets, as it followed Thursday’s release of the official PMI figures.

(CN) PBoC reiterates 'prudent and neutral' monetary policy; Property market has become major source of financial risk; Cannot expect use of ‘pure’ monetary policies to address problems in the property market; China should keep tight property curbs in main cities; mulling measures related to home mortgage loan growth to reduce volatility related to property market prices; Reiterates property market tax reform should be included in broader tax reform considerations – Publication

Key economic data

(AU) Australia AiG Perf of Mfg Index: 59.8 v 56.0 prior

(AU) Australia Aug CBA Australia PMI Mfg: 53.5 v 54.4 prior

(CN) CHINA AUG CAIXIN PMI MFG: 51.6 V 51.0E (Highest since Feb)

(KR) SOUTH KOREA AUG TRADE BALANCE: $7.01B V $6.24BE; Exports Y/Y: 17.4% v 15.8%e (10th straight rise)

(JP) JAPAN Q2 CAPITAL SPENDING Y/Y: 1.5% (3RD CONSECUTIVE RISE) V 7.9%E; EX-SOFTWARE Y/Y: 0.6% V 8.2%E

(KR) SOUTH KOREA AUG CPI M/M: 0.6% V 0.2%E; Y/Y: 2.6% V 2.2%E (fastest rate in over 5-years)

(KR) SOUTH KOREA Q2 FINAL GDP Q/Q: 0.6% V 0.6%E; Y/Y: 2.7% V 2.7%E

(NZ) NEW ZEALAND Q2 TERMS OF TRADE INDEX Q/Q: 1.5% V 3.0%E

Speakers and Press

China

(CN) China Communist Party expected to convene National Congress on Oct 18th - Xinhua

Other

(JP) Japan Fin Min Aso: Will not travel to the US on Sept 4 due to North Korea risk; Says his comments on Hitler were unrelated to cancellation of US trip.

(US) US President Trump to propose initial $5.9B in Harvey aid; said to consider linking debt limit increase to Harvey aid - US financial press

(US) US Transportation Sec: Signed executive order allowing expedited fuel deliveries to Texas from 25 other states

(US) Pemex: Due to port closures in Houston, importing fuel shipments from Bermuda, US East Coast and Alabama

(US) Houston Port: Heavy current into Houston Ship Channel making it unsafe to bring in vessels

(US) Explorer Pipeline planning to start lines on Saturday and Sunday - US financial press

(US) EIA: In June, US gasoline consumption 9.77M bpd, +1.1% y/y (record)

Asian Equity Indices/Futures (00:30ET)

Nikkei flat, Hang Seng +0.4%, Shanghai Composite +0.6%, ASX200 +0.2%, Kospi flat

Equity Futures: S&P500 flat ; Nasdaq +0.1% , Dax +0.1% , FTSE100 flat

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1186-1.1923; JPY 109.93-110.15; AUD 0.7937-0.7957; NZD 0.7169-0.7189

Aug Gold +0.2% at1,324 /oz; Aug Crude Oil -0.6% at $46.95/brl; Sept Copper flat at $3.10/lb, Gasoline Futures -0.1%

GLD SPDR Gold Trust ETF daily holdings flat at 816.4 metric tons

(CN) PBOC SETS YUAN REFERENCE RATE AT: 6.5909 V 6.6010 PRIOR (yuan set stronger for 5 straight sessions, today's fix strongest since June 24, 2016)

(CN) PBoC skips OMO v skipped 7 and 14-day prior; Drains net CNY50B v CNY40B prior

(JP) Bank of Japan (BoJ) announces amounts to buy in QE operation: Cuts 3-5 yr JGB purchases to ¥300B from ¥330B prior

(AU) Australia sells A$500M in 2.00% Dec 2021 Bonds, avg yield 2.1575%, bid to cover 7.82x; Says one buyer purchased all of the 2021 notes at the auction.

Equities notable movers

Australia

Virtus Health, VRT.AU Removed from S&P ASX 200 Index; -2.4%

Sky Network TV, SKT.AU Removed from S&P ASX 200 Index; -3.5%

Hong Kong/China

Sunac China, 1918.HK Reversed opening gains seen after earnings, commented on its exposure to Wanda;-2.5%

GD Power Development Co, 600795.CN Higher on M&A; +10%

US markets on close: Dow +0.3%, S&P500 +0.6%, Nasdaq +1.0%, Russell +1.0%

Best Sector in S&P500: Health Care +1.7%

Worst Sector in S&P500: Financials flat

At the close: VIX 10.59 ( -0.63 pts); Treasuries: 2-yr 1.33% (flat), 10-yr 2.119% (-2.5bps), 30-yr 2.725% (-2bps)

US Market Summary

Stocks rose again today, helped by strong jobless data and low CPE data. Mnuchin's comments on tax reform and the aim to pass a bill by year end gave investors hope. Crude turned the recent sell-off around, rising 2.5%, with CLV7 trading above $47 at close. Treasury yields declined after weak inflation data seemed to confirm inaction from Fed for the rest of year; the 10-year yield was down 2 bps from yesterday at 2.12%, 10s30s curve spread unchanged from yesterday at 60 bps. Weak inflation data also saw gold continue its bullish trend, as the Fed seems even less likely to raise rates before year end.

US Afterhours Movers

LULU Reports Q2 $0.39 v $0.35e, Rev $581.1M v $568Me; Guides Q3 $0.50-0.52 v $0.52e, Rev $605-615M v $601Me; SSS mid single digits increase; +7.1% afterhours

PANW Reports Q4 $0.92 v $0.79e, Rev $509.1M v $487Me; Guides Q1 $0.67-0.69 v $0.69e, Rev $482-492M v $487Me; +6.8% afterhours

TECD Reports Q2 $1.74 v $2.06e, Rev $8.88B v $8.71Be; Guides Q3 $1.84-2.04 v $2.20e, Rev $9.0-9.35B v $8.6Be; -19.4% afterhours

Today All Eyes Will Be On The US Labour Market Report

Market movers today

Today all eyes will be on the US labour market report. Focus remains on the unemployment rate and wage growth as these remain crucial for the Fed's decisions on quantitative tightening. In line with the continued growth in employment , we expect further declines in the unemployment rate over time. However, we expect wage growth to remain around current levels for some time and to fail to show a significant pickup as the second round effects of several years with low inflation are dragging wage growth (see Flash Comment US: Fed likely to continue tightening on strong jobs report, 7 August ).

Focus will also be on global PMI manufacturing figures with the release of the US, euro area, Swedish and Norwegian figures. For the euro area, the most interesting numbers are the first releases in Italy and Spain. In Italy, the composite PMI new orders index is around the level in Germany, although the two economies are doing very differently. In our view, there are still significant challenges for Italy including some political risks. In Germany, in cont rast , the upcoming election should not change much (see German Election Monitor No. 1: Next euro area election unlikely to rock the boat, 29 August ). For more about the Scandi PMIs, see page 2.

In the US, ISM manufacturing is also due for release. The gap between the ISM and PMI manufacturing figures is the biggest in 10 years, implying the two figures are sending mixed signals about the US economy currently. For the August print , we expect ISM manufacturing to stay around its existing high level and therefore not close in on the gap to PMI manufacturing. Note the preliminary PMI manufacturing figure has already been published and the final print should stay around the level seen in the preliminary report .

Selected market news

Yesterday, US Treasury Secretary Steven Mnuchin told CNBC that the debt limit deadline has been pushed forward a ‘couple of days' due to additional spending since Hurricane Harvey. It remains our base case that the debt limit will be raised or suspended eventually but we have to get closer to the deadline before a deal will be reached.

Also the Harvey storm has hit the supply of gasoline in the US, which has led to a surge in US gasoline future prices. In a very short period of time the gasoline future price for September has increased from USD1.60/gallon to now USD2.14/gallon. Higher fuel prices may affect US inflation in coming months, although it is difficult to say how much yet , as it also depends on how quickly refineries are up and running again (24% of US refining capacity remains shut ). That said, the PCE inflation data for July, which were released yesterday, showed a fall in the PCE core inflation rate to 1.4% from 1.5%, so it is unlikely to really put pressure on the Fed.

In China, state media reports the Chinese Communist Party Congress will begin on 18 October, where President Xi Jinping will out line his political programme for the coming five years and needs to fill important posit ions in the Politburo Standing Commit tee, which is the most important decision body in China.

Canadian GDP Rockets Ahead For Another Quarter

Defying expectations for a slower pace of growth, the Canadian economy accelerated in the second quarter to grow at an annualized rate of 4.5 percent and, in so doing, it retains the title of fastest growing G-7 economy

Sorry Japan, Canada Just Stole the Spotlight

Canada's economy expanded at an annualized rate of 4.5 percent in the second quarter, besting market expectations of a 3.7 percent gain. Before all of the results were in, it looked like Japan with its 4.0 percent growth in the second quarter would hold the distinction of fastest growing G-7 economy. In recent months, the year-over-year GDP growth numbers have crested above 4.0 percent. As the middle chart shows, that is the fastest annual growth Canada has seen in roughly a decade. The faster growth is catching forecasters and financial markets somewhat by surprise. Even the Bank of Canada (BoC), which has been known to overshoot its growth estimates from time-to-time, is forecasting only 2.8 percent GDP growth for 2017 as a whole, according to projections in its July Monetary Policy Report. Growth would have to slow meaningfully in the second half of the year to come in with anything below 3.0 percent.

Canada's households continue to boost the economy, with spending growing at an annualized rate of more than 4.5 percent each of the first two quarters of the year. We were already concerned about high consumer debt levels in Canada, and today's report increases that concern. Consumer spending was so strong in Q2 that the personal savings rate slipped below 5.0 percent in the first half of the year, after having remained above 5.0 percent in 2016.

Business investment, which had been under pressure in 2015 and 2016 due to depressed commodity and oil prices, has rebounded in recent quarters, although admittedly the 1.9 percent growth rate for business investment in the second quarter marks a significant slowdown relative to the 10.5 percent surge in the first three months of the year.

Business inventories ratcheted up another $14 billion after a $10.3 billion increase in the prior quarter. While the quickening demand environment in Canada may justify the stockpiling, we suspect a slower pace of inventory accumulation in the second half may be a drag on GDP growth. After being a drag on overall growth in Q1, net exports boosted growth in the second quarter, adding seven-tenths of a percentage point to the overall top-line growth rate for the period.

Bank of Canada Meeting Next Week Is Live

The BoC lifted its overnight rate to 0.75 percent at its July meeting and has since maintained a tightening bias. Prior to today's report, we would have said that the next hike could come as soon as the October meeting. While that is still our base case scenario, we would be remiss not to acknowledge there is some risk policy-makers could act at their scheduled meeting this coming Wednesday. CPI inflation at 1.2 percent is still near the low end of the target range, meaning they are not compelled to act now.

Australia’s Manufacturing Sector Expanded At Its Fastest Pace In 15 Years In August

For the 24 hours to 23:00 GMT, the AUD rose 0.48% against the USD and closed at 0.7943.

LME Copper prices rose 0.6% or $37.0/MT to $6792.0/MT. Aluminium prices rose 2.3% or $47.0/MT to $2113.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7951, with the AUD trading 0.1% higher against the USD from yesterday's close, on the back of robust manufacturing report from Australia.

Data revealed that Australia's AiG performance of manufacturing index advanced to a level of 59.8 in August, expanding at its quickest pace since May 2002 and suggesting that manufacturing sector will propel third quarter economic growth in the resource-rich economy. The PMI had recorded a reading of 56.0 in the prior month.

Elsewhere in China, Australia's largest trading partner, the Caixin manufacturing PMI recorded an unexpected rise to a level of 51.6 in August, notching a six-month high level. Markets had envisaged the PMI to drop to a level of 51.0, after registering a level of 51.1 in the previous month.

The pair is expected to find support at 0.7896, and a fall through could take it to the next support level of 0.7840. The pair is expected to find its first resistance at 0.7982, and a rise through could take it to the next resistance level of 0.8012.

Moving ahead, investors will closely monitor the Reserve Bank of Australia's (RBA) interest rate decision, due next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Annual Inflation Jumped To A 4-Month High In August, Unemployment Rate Remained Steady At An 8-Yyear Low In...

For the 24 hours to 23:00 GMT, the EUR rose 0.14% against the USD and closed at 1.1913, following robust economic data in the Euro-zone.

Data indicated that the Euro-zone's preliminary consumer price index (CPI) climbed more-than-expected by 1.5% on an annual basis in August, hitting its highest since April 2017, suggesting that price pressures in the common currency region are regaining some momentum. In the prior month, the CPI had gained 1.3%, while markets were expecting it to rise by 1.4%. Additionally, the region's unemployment rate remained unchanged at an eight-year low level of 9.1% in July, meeting market consensus.

Separately, Germany's seasonally adjusted unemployment rate remained steady at a record low level of 5.7% in August, in line with market expectations. On the contrary, the nation's retail sales fell more-than-anticipated by 1.2% on a monthly basis in July, stoking fears that private consumption in the Euro-bloc's biggest economy may have lost momentum at the start of the third quarter.

The greenback lost ground against a basket of currencies, after pending home sales in the US unexpectedly dropped 0.8% on a monthly basis in July, confounding market anticipations for a rise of 0.3% and following a revised gain of 1.3% in the previous month. Meanwhile, the nation's initial jobless claims rose to a level of 236.0K in the week ended 26 August 2017, lower than market expectations for a rise to a level of 238.0K. In the previous week, initial jobless claims had recorded a revised level of 235.0K.

Another data indicated that personal spending in the US climbed 0.3% MoM in July, undershooting market expectations for a rise of 0.4%. In the prior month, personal spending had risen by a revised 0.2%. Further, the nation's personal income recorded a more-than-expected rise of 0.4% on a monthly basis in July, while markets anticipated for an advance of 0.3%. In the prior month, personal income had registered a flat reading. Also, the nation's Chicago Fed purchasing managers index remained steady at a level of 58.9 in August, while investors had envisaged the index to ease to a level of 58.5.

In the Asian session, at GMT0300, the pair is trading at 1.1905, with the EUR trading 0.07% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1844, and a fall through could take it to the next support level of 1.1784. The pair is expected to find its first resistance at 1.1944, and a rise through could take it to the next resistance level of 1.1984.

Moving ahead, investors will keep a close watch on the final Markit manufacturing PMI for August across the Euro-zone, slated to release in a few hours. Moreover, traders anxiously awaited the US non-farm payrolls, unemployment rate and average hourly earnings data, all for August, scheduled to release later in the day. Moreover, the nation's construction spending for July, ISM manufacturing PMI as well as final Michigan consumer confidence index, both for August, will also be eyed by traders.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.