Sample Category Title

Dollar Caps Losses, Gains Against Majors, Kiwi Tumbles To More Than 2-Month Lows

The dollar managed to recoup some of yesterday's losses against the yen, when the US currency tumbled on the President's remarks about a government shutdown. Other majors also weakened with the kiwi underperforming as it tumbled to more than a two-month lows against the greenback. Oil prices slipped after yesterday's surge.

During another relatively quiet trading day in Asia, the dollar managed to reverse its losses and post a moderate gain against the yen. Dollar/yen was last trading at 109.27, up a quarter of a percent on the day. President Trump rattled markets yet again with his speech about a possible government shutdown and exit from the NAFTA trade treaty on Tuesday night. The dollar took a breather today and gained against the yen, as the US Congress is in summer recess until September 5 and upon return, it will have about 12 working days to approve spending measures and prevent the government from shutting down. Traders will be focusing on the central bankers' meeting in Jackson Hole that starts today. They will be on the lookout for any clues about future monetary policy steps by either the European Central Bank or the Federal Reserves.

Internal political woes shook up the currencies down under. The kiwi lost ground and tumbled against its US counterpart, deepening yesterday's losses when it fell on curtailed economic growth outlook by the New Zealand government. Many investors have raised concerns over political instability and question the government's chance to be re-elected next month. Kiwi/dollar was last trading at 0.7197, hitting its lowest point since mid-June. Its cousin, the aussie also tumbled and was last trading at $0.7837. The aussie weakened on news that some high-profile politicians with dual citizenship may not be able to stand for Parliament unless they renounce their other citizenship.

Sterling was under pressure as the British currency dipped below the $1.28 level for the first time since June. Concerns over Britain's economic prospects and its exit from the EU are increasing and pushing the pound lower. Markets are unimpressed with the UK government's efforts to provide clarity and stability during this painful process. All eyes will be on the release of the second estimate of second-quarter GDP figure for the UK at 8:30 GMT, which will include details on business spending. Pound/dollar was last trading at $1.2790.

The euro faded against the greenback to trade at $1.1791 as traders await the Jackson Hole meeting with ECB President Draghi expected to speak tomorrow. The common currency also fell modestly against the pound to last trade at 0.9218, after four days of gains.

Oil prices fell slightly against yesterday's surge with Brent last trading at $52.48 a barrel and WTI at $48.29. Linked to the dollar strength, gold prices gave up most of yesterday's gains and fell to $1,286.32.

Euro Contained By 61.8 Fib

The EURUSD pair has again been contained by the 61.8 Fibonacci retracement level, at 1.1815, with price action continuing to print bearish lower daily high's, just below the current weekly price high.

Despite the euro's latest bullish move above the 1.1800 level, the pair still remains somewhat cautious ahead of the Jackson Hole symposium.

The EURUSD pair remains bullish in the short-term, while trading above the daily pivot point, found at the 1.1792 level.

Key technical support below the 1.1792 level is located at the 200-week MA, at 1.1783. Critical intraday support is found at 1.1769, with further support below, at 1.1731.

To the upside, 1.1818 is the current daily price high, with resistance found at 1.1847 and 1.1858. The 1.1900 level remains critical technical resistance above the 1.1858 level.

Pound Remains Soft Ahead Of Q2 GDP Data

The British pound remains soft on Thursday, with price continuing to trade below the 1.2800 technical level against the U.S dollar, ahead of the release of second quarter GDP data from the United Kingdom economy.

Later today the Jackson Hole symposium will get underway, although FED Chair Janet Yellen and ECB President Mario Draghi will be speaking on Friday.

The GBPUSD pair remains bearish on all time-frames, with price action creating bearish lower highs on shallow pullbacks, and lower price low's.

Key technical support below the 1.2777 level, is found at 1.2750 and 1.2716, with the key 200-day moving average approaching, at 1.2680.

Key short-term technical GBPUSD resistance is found at the 1.2819 and 1.2832 levels, with critical intraday resistance situated in the 1.2839 to 1.2850 zone.

Annual Jackson Hole Summit Set To Begin

The Jackson Hole Symposium is officially underway on Thursday. The annual event, which is hosted by the Kansas City Federal Reserve Bank, will attract central bankers from over 40 countries.

The theme of this year's event is 'Fostering a Dynamic Global Economy,' and will take place between 24-26 Aug. Among the attendees are Fed Chairwoman Janet Yellen and European Central Bank (ECB) President Mario Draghi.

Signs of shifting policy over the next three days could have ripple effects on the global economy. Analysts say they are not expecting any substantial signal from central bankers during the event. Reports circulated last week that Draghi could use Jackson Hole as an opportunity to deliver a big monetary policy speech. Those reports were later refuted by Reuters.

Investors can also expect a deluge of economic data from around the world. Action begins at 07:00 GMT with a report on Spanish gross domestic product (GDP). Spain's GDP is forecast to have grown 0.9% in the second quarter.

UK National Statistics will release revised second quarter GDP numbers on Thursday. Quarterly growth is expected at 0.3%, unchanged from the previous estimate.

In North America, the US Labor Department will issue its weekly jobless claims report, which provides an ongoing snapshot of the labor market. Claims are projected to rise by 6,000 in the week ended 18 August to reach 238,000.

The National Association of Realtors (NAR) will report on existing home sales at 14:00 GMT. The sale of pre-owned homes is forecast to rise 0.9% to a seasonally adjusted 5.57 million in July. On Wednesday, the Commerce Department said new home sales plunged last month.

The Kansas City Fed will also release its monthly manufacturing survey at 15:00 GMT, capping off a highly active session.

EUR/USD

The EUR/USD rebounded Wednesday as upbeat data boosted demand for the common currency. The pair broke above 1.1800, although gains stalled well below 1.1830 – a region that is likely to attract renewed selling interest. The pair faces immediate support at 1.1730.

GBP/USD

The British pound slipped to fresh two-month lows on Wednesday, as cable struggled to shake off bearish pressure. The GBP/USD was down 0.1% in Asian trade. Prices are testing an initial support level at 1.2780. A break below that level would expose 1.2750 followed by 1.2710.

GOLD

Gold prices rose on Wednesday, as risk aversion creeped back into the financial markets. Political risks were once again front and centre after US President Donald Trump said he would let the government shut down unless Congress provides funding for his planned border wall with Mexico. Bullion remains well supported in its current range, but will find it difficult to make a clean break above $1,300.00

USDJPY Intraday Analysis

USDJPY (109.18): The USDJPY continues to consolidate around the support level of 109.15. The currency pair fell back to this level after earlier attempts to bounce off this level faded. The support level at 109.08 thus continues to remain a strong level of support. To the upside, USDJPY will be looking towards targeting the resistance level at 110.72. However, the potential for a downside breakout in prices could formalize. Below 109.08, USDJPY could initially slip towards 109.00 followed by further declines depending on the daily close.

GBPUSD Intraday Analysis

GBPUSD (1.2786): The British pound extended the declines below 1.2847 support level, and further declines could be expected in the near term. The next main support level is at 1.2628. In the near term, any retracement could be limited to the support level of 1.2847 which could be tested in order for resistance to be established. In the event that GBPUSD posts a stronger retracement, we can expect the sideways pattern to play out within the ranges of 1.2908 and 1.2847.

EURUSD Intraday Analysis

EURUSD (1.1799): The EURUSD remains trading flat with price action posting some gains yesterday, reaching to 1.1815. The sideways range saw price briefly retesting the breakout level from the ascending triangle pattern. Resistance is seen at 1.1815 - 1.1820 with the potential for an upside breakout. This could send the common currency to test the previous resistance level of 1.1882 with further gains expected on a break above this resistance level. To the downside, a close below yesterday's low near of 1.1749 could keep EURUSD falling back to retest the support level at 1.1688.

Trump’s Remarks Keep The Greenback Subdued

The US dollar remained weak yesterday as investors digested the news about the latest threats from President Trump. Speaking at an event in Arizona the day before, Trump threatened to shut down the government if he did not receive funding to build the wall at the Mexican border. Further to this, the fact that the US debt ceiling will be hit by October further accentuated the remarks.

On the economic front, new home sales fell 9.4% more than the forecasts of a flat reading. However, the previous three month new home sales data was revised significantly higher offsetting the declines. Markit's flash manufacturing PMI for the US fell to 53.3 falling below the estimates of 52.5 but services PMI rose to 56.9.

In the Eurozone, flash composite PMI continued to rise, especially with the manufacturing PMI hitting a six and a half year high. Services PMI for August, however, slipped to a 7-month low.

Looking ahead, the annual Jackson Hole symposium starts today. On the economic front, the UK's second revised GDP estimate for the quarter ending June will be coming out. Estimates point to no change in the quarterly GDP, but business investment is expected to decline.

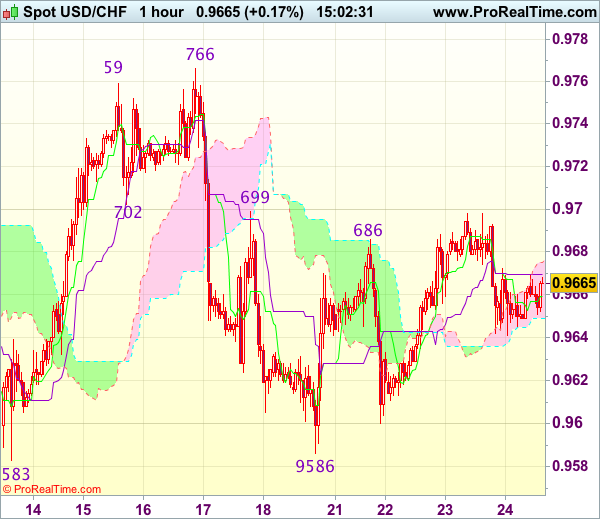

Trade Idea : USD/CHF – Buy at 0.9620

USD/CHF - 0.9656

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 0.9659

Kijun-Sen level : 0.9670

Ichimoku cloud top : 0.9675

Ichimoku cloud bottom : 0.9649

Original strategy :

Buy at 0.9620, Target: 0.9720, Stop: 0.9585

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9620, Target: 0.9720, Stop: 0.9585

Position : -

Target : -

Stop : -

Dollar’s retreat after faltering below resistance at 0.9699 suggests initial downside risk remains for weakness to 0.9620-30, however, as long as support at 0.9586 holds, prospect of another rebound remains, above indicated resistance at 0.9699 would signal the retreat from 0.9766 has ended at 0.9586 last week and mild upside bias is seen for gain to 0.9720, then 0.9740, having said that, reckon resistance at 0.9766-73 would cap upside and bring further consolidation. Only a break of 0.9773 would retain bullishness and signal early rise from 0.9438 has resumed and extend gain to 0.9800.

In view of this, we are looking to buy dollar on further pullback as 0.9620-30 should limit downside. Below 0.9600 would risk test of strong support at 0.9583-86 but only break there would signal a downside break of recent broad range has occurred, bring subsequent fall to 0.9550.

What Does A Government Shutdown Mean For The U.S. Markets?

'If we have to close down our government, we're building that wall' Donald Trump

After stocks and the dollar surged on Tuesday, following a Politico report that Trump's team have taken a significant step on tax reforms, the President's threatson Tuesday night to shut down the government and terminate the NAFTA agreement,were not well received by investors, who responded by dragging both equities and the dollar lower.

History reveals that markets tend to experience modest weakness during shutdowns, with the S&P 500 falling an average of 0.6% over the period of closure. However, markets don'talways drop. Equities gained eight times out of the 18 shutdowns from 1976 to 2013, and the largest recorded rally was during Obama's era in 2013, with gains exceeding 3%. However, when one party controlled the Presidency, Senate, and the House, it looked different. From 1977 until 1979, when Democrats lead by Jimmy Carter, controlled all three branches, the government was shut down five times,markets dropped on four of these occasions, with average losses of 2.7%. If a shutdown can'tbe avoided, investors hope it looks more like an Obama than a Carter era.

A shutdown isn't the biggest threat right now, the more pressing issue is the timing of the delivery of a detailed plan on tax reforms. The longer such reforms are delayed, the more anxiety will be felt in financial markets, thus expect to see further weakness in U.S. equities in September.

Investors in wait-and-see mode

Financial assets, whether it's equities, currencies, or fixed income,are trading in very tight ranges early Thursday, and I expect such moves to continue throughout the day. With the lack of tier one economic data, investors are bracing for some hints from the annual central bank gathering at Jackson Hole, which kicks off today.

ECB's Mario Draghi refrained from giving any indications on future policy,when he delivered a speech at a conference in Germany yesterday. It seems he is trying to avoid commenting on monetary policy, after the Euro surged by more than 12% on expectations of QE getting closer to an end. I believe Euro bulls will also be disappointed when Draghi speaks on Friday, as he'll continue to shy away from any specific timing on tapering bond purchases. However, given the strength in economic activity and diminishing outstanding bonds available to purchase, the ECB has no alternative but to begin the normalization process, and any pull back in the Euro will be seen as an opportunity to get in.

Fed Chair, Janet Yellen will also be speaking Friday on financial stability. Her speech is of great importance, given the recent warnings from the Fed on vulnerabilities associated with asset valuations. Few disagree that the global easy monetary policies have created overstretched valuations. Whether it's stocks, fixed income, real estate or bitcoins, there is a bubble somewhere. Sooner or later some sort of significant correction in prices should occur, but central bankers want to make sure that economic stability won'tbe impacted and this isn't an easy task.