Sample Category Title

Trade Idea : GBP/USD – Buy at 1.2770

GBP/USD - 1.2800

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2790

Kijun-Sen level : 1.2804

Ichimoku cloud top : 1.2862

Ichimoku cloud bottom : 1.2833

New strategy :

Buy at 1.2770, Target: 1.2870, Stop: 1.2735

Position : -

Target : -

Stop : -

Although cable has remained under pressure and near term downside risk remains for recent selloff to extend one more fall, loss of downward momentum should prevent sharp fall below 1.2750-55, risk from there has increased for a rebound to take place soon, above 1.2845-50 would suggest a temporary low is possibly formed, bring a stronger rebound to 1.2870, break there would add credence to this view, then retracement of recent decline would commence for further gain to 1.2900.

In view of this, we are inclined to turn long on next decline. Below 1.2740-50 would risk weakness to 1.2720-25, however, still reckon downside would be limited to 1.2700-05 (100% projection of 1.3269-1.2940 measuring from 1.3032) and risk from there remains for another rebound to take place later.

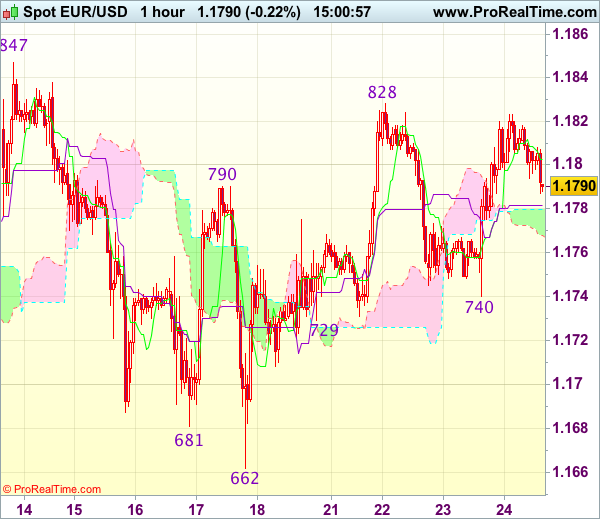

Trade Idea : EUR/USD – Hold long entered at 1.1765

EUR/USD - 1.1791

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.1803

Kijun-Sen level : 1.1782

Ichimoku cloud top : 1.1780

Ichimoku cloud bottom : 1.1768

Original strategy :

Bought at 1.1765, Target: 1.1865, Stop: 1.1770

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1770

New strategy :

Hold long entered at 1.1765, Target: 1.1865, Stop: 1.1770

Position : - Long at 1.1765

Target : - 1.1865

Stop : - 1.1770

As the single currency has retreated after faltering below resistance at 1.1828, suggesting minor consolidation would be seen, however, as long as 1.1765-70 holds, mild upside bias remains for another rebound, above said resistance at 1.1828 would extend the rise from 1.1662 low to resistance at 1.1847, break there would provide confirmation that the pullback from 1.1910 has ended and encourage for headway to 1.1870-80 but reckon said resistance at 1.1910 would hold from here.

In view of this, we are holding on to our long position entered at 1.1765. Only below 1.1740 support would abort and suggest the rebound from 1.1662 has ended instead, risk weakness to 1.1695-00 first.

Trade Idea : USD/JPY – Stand aside

USD/JPY - 109.35

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 109.11

Kijun-Sen level : 109.21

Ichimoku cloud top : 109.54

Ichimoku cloud bottom : 109.23

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling initially to 108.84 earlier today, the subsequent rebound suggests decline is not ready to resume yet and further consolidation is in store, hence risk of another bounce to 109.55-60 is seen, however, reckon resistance at 109.83 (yesterday’s high) would hold and bring retreat later. Only a break of 109.83 would signal low has been formed at 108.60 earlier, bring further gain to 110.00 and later towards previous resistance at 110.37.

On the downside, below 109.00 would bring test of 108.84 but only break of said support at 108.60 would revive bearishness and confirm recent decline has resumed for further weakness to 108.30 (1.618 times projection of 110.95-109.67 measuring from 110.37), then towards 108.00. As near term outlook is still mixed, would be prudent to stand aside in the meantime.

Aussie Dollar At Risk Of Breakdown Vs Japanese Yen

Key Highlights

- The Aussie Dollar is struggling against the Japanese Yen and just holding the 86.00 support.

- There is a steep bearish trend line with resistance at 86.20 forming on the 4-hours chart of AUD/JPY.

- Japan’s Leading Economic Index for June 2017 posted an increase from the last revised reading of 104.7 to 105.9.

- Japan’s Coincident Index for June 2017 posted an increase from the last revised reading of 115.8 to 117.1.

AUD/JPY Technical Analysis

The Aussie Dollar after a close below 86.60 struggled a lot against the Japanese Yen. The AUD/JPY pair is trading above a crucial 86.00 support, but remains at a risk of a breakdown.

The pair has almost breached the 86.00 support area and poised to extend declines. On the upside, there is a steep bearish trend line with resistance at 86.20 forming on the 4-hours chart.

The pair recently failed to break the 38.2% Fib retracement level of the last decline from the 86.86 high to 86.06 low. Therefore, there are high chances of it breaking 86.00 and declining further.

The pair is also well below the 100 and 200 simple moving average (positioned near 86.50-60). Overall, as long as the pair does not overtake the 86.50 resistance, it remains at a risk of a downside break below 86.00.

Japan’s Leading Economic and Coincident Index

Today, Japan saw releases of the Leading Economic and the Coincident index for June 2017 by the Cabinet Office.

The Leading Economic index was forecasted to remain unchanged from the last reading of 106.3. However, the end result was mixed, as the Leading Economic index came in at 105.9, and the last reading was revised down from 106.3 to 104.7. So, there was a net increase of 1.2 points.

Similarly, the Coincident index was forecasted to remain unchanged from the last reading of 117.2. However, the end result was neutral, as the Coincident index came in at 117.1, and the last reading was revised down from 117.2 to 115.8. So, there was a net increase of 1.3 points.

The Coincident index is stable around the BMA (3), which is 3 months backward moving average. And, the index is now well above BMA (7), which is 7 months backward moving average.

Currencies: Dollar Resists Trump’s Comments Rather Well

Sunrise Market Commentary

- Rates: More neutral positioning into Jackson Hole speeches?

Core bond markets are rather dovish positioned. More subdued inflation readings questioned central banks' urge to complete a near term tightening push. Expectations of pre-announced policy changes by Draghi and/or Yellen tomorrow are (too) low. Therefore, some investors might be willing to take some chips off the table, resulting in more neutral positioning. - Currencies: Dollar resists Trump's comments rather well

Yesterday, USD soon found a bottom after a series of unconventional comments from US president Trump. Today, more wait-and-see trading can be expected going into the Jackson Hole symposium. Draghi needs to convince investors that the ECB will go very slowly to trigger a meaningful correction of EUR/USD. EUR/GBP extends its impressive ascent.

The Sunrise Headlines

- US equities managed to limit losses to 0.4% yesterday, despite US President Trump's latest controversial comments on NAFTA and a government shutdown. Asian stock markets are mixed with China and Japan underperforming.

- ECB policy maker Hansson said he isn't currently concerned about the strength of the euro as officials prepare to discuss how to wind down their bondpurchase program.

- The ECB should quickly end asset buys next year as the outlook does not warrant the extension of its €2.3 trillion scheme, Bundesbank President Weidmann said, weighing in on the biggest issue facing the ECB this autumn.

- Fitch Ratings said that it could put the US's top-notch 'AAA' sovereign rating on review for a possible downgrade if lawmakers fail to raise the country's debt limit in a timely manner.

- Dallas Fed President Kaplan reiterated that he wants to be patient on raising interest rates, adding that he's not saying it should happen again this year. The central bank should start soon in paring its balance sheet, he said.

- The UK's financial sector is seeking an 'ambitious' trade pact between Britain and the EU to try to prevent a costly shift of jobs and business to the continent once the country leaves the bloc, according to a draft report seen by Reuters.

- Today's eco calendar contains the second reading of UK Q2 GDP, US weekly jobless claims and US existing home sales. The annual Jackson Hole Economic Symposium starts.

Currencies: Dollar Resists Trump's Comments Rather Well

Modest USD damage after Trump comments

A new wave of unconventional comments of US president Trump on NAFTA and on a government shutdown aborted Tuesday's USD rebound. Poor US housing data were also a slight additional USD negative. At the same time, the euro was supported by strong EMU PMI's. EUR/USD returned north of 1.18 and closed the session at 1.1807. USD/JPY drifted to the 109 barrier, but the pace of the decline slowed during US session as the damage from the Trump comments on equities remained modest.

Overnight, Asian equities mostly show modest gains with Japan and China underperforming. Volumes remain thin as investors look forward to the Jackson Hole symposium. ECB's Hansen, a hawk, isn't overly worried about recent euro strength. At the same time, he left plenty of options open on the degree of monetary policy stimulation. At least for now, his comments don't cause any further euro gains. EUR/USD stabilizes in the 1.18 area. USD/JPY holds in the low 109 area. So, for now, the 108.60 ST correction low 'survived' the unconventional trump comments.

The EMU calendar contains only second tier national data which are unlikely to affect EUR/USD trading in a profound way. Also the US initial claims, Existing Home sales and the Kansas Fed manufacturing survey will at best only have intraday significance as traders are focused on Jackson Hole. The meeting starts today, but key speeches of Yellen and Draghi are only scheduled for tomorrow . Regarding the Fed: the timing of the start of the tapering but also the Fed's views on the missing link between buoyant employment, wages and ultimately inflation are important. Regarding the ECB, the outlook for the tapering of the APP programme matters most. Inflation, the ECB target, and the strength of the euro are crucial variables. Today, we expect more wait-and-see trading in EUR/USD. The market needs a 'reassurance' from Draghi that the ECB will move extremely slowly to trigger a meaningful correction of the EUR/USD. The modest reaction of USD/JPY (and of equities) on Tuesday's Trump comments suggest that the decline of USD/JPY is taking a pause, awaiting more clear guidance from central bankers and the Trump administration

Broader context and technical picture. Late June, EUR/USD started a new upleg as investors anticipated a reduction of ECB bond buying to be announced in autumn. The Fed was expected to remove policy stimulation only in a very gradual way as US inflation remains soft. Uncertainty on the policy of the Trump administration was an secondary negative factor for the dollar. EUR/USD set a new correction top north of 1.19 before consolidating in a narrow 1.1662/1.1910 range. We expect this range to hold going into the Jackson Hole symposium. If US data remain ok (as most were this month) and if Draghi gives little information on next ECB steps, there might be room for a modest USD comeback. A return of EUR/USD to the 1.15/16 area is possible. Pockets of US political risk are a (negative) wildcard for the dollar. A downward correction in core (US and European) yields supported the yen in August. USD/JPY declined from mid 114 mid-July to 108.60. The April correction low (108.13) remains the line in the sand. For now, this level won't be easy to break as quite some USD bad news is discounted after the recent protracted setback. A cautious buy-on-dips approach (with stop-loss protection below 108) may be considered.

EUR/US: awaiting clearer CB guidance

EUR/GBP

EUR/GBP: another day, another new ST top

Yesterday, sterling selling persisted. There were plenty of press articles on the role of the ECJ (Court of Justice) and on how the UK and the EMU will handle juridical disputes post-Brexit. Some comments considered the British language that it will accept no 'DIRECT' jurisdiction of the court as an easing on earlier tough separation rhetoric, but it didn't help sterling. EUR/GBP jumped north of 0,92, admittedly in the first place due to strong EMU PMI's. Cable also dropped below 1.28. The lack of progress in the Brexit talk still makes selling sterling the way of least resistance. EUR/GBP closed the session at 0.9224. Cable finished the day at 1.2800.

Today, the details of the UK Q2 GDP and the CBI August retail data will be published. UK growth is expected to be confirmed at a soft 0.3% Q/Q and 1.7% Y/Y. The details (e.g. on private consumption) are interesting, but the report is a bit outdated to have a lasting impact on sterling. CBI retail sales data are expected to have eased in August. However, we expect a slight positive surprise, as UK activity data weren't too bad of late. Still, it won't be a sterling game-changer. The focus for trading remains the Brexit negotiations and to a lesser extent inflation. Sterling's decline can't however continue till eternity without a pause or a temporary correction on which we put our money.

From a technical point of view, EUR/GBP cleared the 0.8854/80 resistance (top end June), opening the way for further gains. The move was the result of euro strength (strong EMU data and expectations of the ECB QE reduction). At the same time, UK price data rare soft enough to keep the BoE side-lined as the Brexit negotiations continue. MT, we maintain a buy EUR/GBP on dips approach as we expect the combination of relative euro strength and sterling softness to persist. The 0.9415 'flash-crash spike' is the next target on the charts. However, we don't jump on the up-trend and wait for a correction, e.g. to the technical support in the 0.88/89 area

EUR/GBP: uptrend continues unabatedly. Is the sky the limit?

Trump’s Threats Unnerve Markets

Concerns have risen that the US housing market recovery is stalling, as the US Commerce Department data on US new home sales dropped 9.4% last month to the lowest level since December 2016. The drop confounded many market analysts, who were expecting a 0.3% gain. A separate report on Wednesday from the US Mortgage Bankers Association indicated mortgage applications also decreased. A lethargic housing market weighs on US GDP.

Markets got more rhetoric from President Trump on Wednesday, with him warning that he might terminate the NAFTA trade treaty with Mexico and Canada after 3-way talks failed to bridge deep differences. At a political rally in Phoenix, Arizona Trump stated; “Personally, I don't think we can make a deal. I think we'll probably end up terminating NAFTA at some point”. Such comments again raise concerns that his administration is unable to deliver on fiscal plans and caused USD to give back recent gains.

Latest government data showed that, whilst US crude stockpiles slid last week with a drawdown of -3.327 (expected -3.450M) production was steady. The latest EIA report marks the 8th straight week of crude oil inventory declines. Production remained flat on the week at 9.5 million bpd giving further, albeit temporary, cause for optimism.

Today starts the Jackson Hole Symposium. Speeches from Fed chair Janet Yellen and ECB President Mario Draghi are not expected until Friday, however, it is not uncommon for potentially policy-relevant remarks to be made by attendees on the sidelines of the event.

EURUSD improved 0.5% on Wednesday, reaching a high of 1.18195. Currently, EURUSD is trading around 1.1800.

USDJPY rose to 109.821 on Wednesday, before USD bears pushed the pair lower. Currently, USDJPY is trading around 109.15.

GBPUSD traded in a narrow range on Wednesday and is currently trading around 1.2785.

Gold appears to be stuck in a narrow trading range of less than $10, with it currently trading around $1,289.

WTI reacted favourably to the latest EIA report, seeing it gain >1.5% on Wednesday. Currently, WTI is trading around $48.40pb.

At 09:30 BST, National Statistics will release UK Gross Domestic Product YoY and QoQ for Q2. Market expectations are for both releases to be unchanged at 1.7% & 0.3% respectively. Any deviation from the consensus will have an impact on GBP.

At 13:30 BST, the US Department of Labor will release Initial Jobless Claims for the week ending August 18th. Consensus is calling for an increase to 238K from the previous 232K. At the same time, Continuing Jobless Claims for the week ending August 11th will be released. Consensus is calling for a slight reduction of 1.950M from the previous release of 1.953M. Whilst a reduction is expected the markets are unlikely to buy USD unless it is significantly lower than expected.

USD/CHF Needs A Bullish Spark

The USD/CHF is trading in the green and is setting up for the next move. Is narrowing and should give birth to a significant move very soon. Price is located above the 0.9634 static support and above the second warning line (WL2) of the major ascending pitchfork, but needs a bullish spark to be able to breakout above the median line (ml) of the minor descending pitchfork. A valid breakout will almost confirm the Inverse Head and Shoulders pattern.

Gold Consolidating The Latest Gains

Price moves in range right above the 38.2% retracement level and tries to recapture more directional energy before will try to breakout from the extended sideways movement. You can see that we had a false breakout on Friday, that’s why the rate has come back to confirm the major static support (resistance turned into support).

Technically should climb towards new highs as long as is located above the mentioned support level, only a valid breakdown will open the door for a broader drop.

GBP/USD Throwback?

Price shown little movement in the early morning, but we may have a some action later, after the United Kingdom will release the high impact data. Price hovers right above a major dynamic support, we'll see how will react in the upcoming days, a breakdown is still favored as the Nikkei stock index is located in the seller's territory.

The JP225 posted little gains and tries to recover after the yesterday's drop. Continues to stay above the 19309 low. I've said in a former article that the index has signaled an oversold on the short term, remains to see if this will be an accumulation or a distribution movement.

The UK's Second Estimate GDP should bring life on the GBP/JPY, it is expected to increase by 0.3% in the Q2, matching the 0.3% growth in the first quarter. You should keep an eye on the economic calendar because more UK's data will be released.

Price is into a corrective phase and is almost to reach the next major downside target from the first warning line (WL1) of the major ascending pitchfork. A rebound will appear if the Nikkei will stay above the 19309 level. Could increase also because the GBP/JPY failed to reach the lower median line (lml) once again, signaling that is losing the bearish momentum.

However, I want to remind you that the pair remains under massive selling pressure on the short term after the breakdown from the chart pattern. Only a valid breakdown will confirm a further drop.

Trading Tentative Ahead Of Jackson Hole Central Bankers Meeting

Dollar Pressured By Trump Comments On Government Shutdown. The dollar slid down as investors began to take seriously threats of Trump's government shutdown over funding for a wall on the Mexican border. The dollar fell 0.55 percent to 108.96 yen, with the dollar index slipping 0.4 percent to 93.167.

Euro Gains On Positive Eurozone Data. The euro recouped some of its losses from the earlier trading session as traders kept their hopes up for tapering remarks in Draghi's Jackson Hole speech. The upbeat survey was the latest sign of economic recovery in the single currency bloc, which may lead the European Central Bank to start scaling back its stimulus program. The euro was propped up by strong German and French PMI survey readings (both countries registering strong private-sector growth in August), although analysts warned its gains could be short-lived due to concerns about heavy one-sided bets. The euro rose 0.5 percent to $1.1818.

New Zealand Posts First July Trade Surplus Since 2012. The New Zealand Dollar appreciated against its major counterparts after July's merchandise trade balance crossed the wires. New Zealand's monthly trade surplus came in at 85m as opposed to a forecasted deficit of 200m.

British Pound Is Subject To A Negative Bias At Present. Sterling fell below $1.28 for the first time since late June. Concerns about Britain's economic prospects and the Brexit process encouraged investors to push the pound lower.

Oil Steady On Falling Crude Inventories. Oil prices were little changed in early trade on Thursday, holding most of their gains from the previous session after another fall in U.S. crude inventories which is seen as a sign of a tighter market.

Gold Eases Ahead Of Central Bankers Meeting. Gold edged lower early Thursday, giving up some of its gains made after U.S. President Donald Trump's threat of a government shutdown, while investors began to focus on a major central bankers' conference in Jackson Hole.