Sample Category Title

USD/CHF Drops Like A Rock

Dropped sharply on Thursday and resumed the Wednesday's bearish candle as the USDX failed once again to close above the 93.81 static resistance. USDX stays also below a dynamic resistance, signaling a minor drop in the upcoming days. The index dropped despite the mixed US economic data and is located right above the 93.60 level.

I want to remind you that only a valid breakout above the 93.81 static resistance will confirm a further increase. Technically, the index was somehow expected to increase further as the behavior changed on the daily chart.

Unfortunately, the USD wasn't impressed by the Unemployment Claims amazing drop, the indicator was reported at 232K in the previous week, much below the 240K estimate and versus the 244K in the previous reporting period, the Philly Fed Manufacturing Index dropped from 19.5 to 18.9, has come in better versus the 18.3 estimate. Moreover, the Capacity Utilization Rate and the CB Leading Index have come in line with expectations, only the Industrial Production has disappointed because has increased only by 0.2%, less versus the 0.3% estimate.

Price decreased sharply since Wednesday and invalidated, for now, a further increase. Could drop much deeper after another false breakout above the median line (ml) of the minor descending pitchfork. A further drop will be confirmed if will make a valid breakdown below the second warning line (WL2) of the former ascending pitchfork.

Only a rejection from the WL2 and a valid breakout above the median line (ml) will signal a potential Inverse Head and Shoulders pattern.

West Wing Scandalmongering

West Wing Scandalmongering.

White House schmaltz continues to weigh negatively on investor sentiment.

The influence of gossip mongering was on full display as investors launched into full risk averse mode when chatter circulated that that White House Economic Advisor Gary Cohn is disconsolate with his White House role and on the verge of resigning. Despite Whitehouse denial, the market remained flustered into the NY close as the mear thought of more internal conflicts and or power struggles within the administration sends investors scurrying for cover. Cohn is one of the Trump’s key political/economic operators and is pivotal to getting President Donald Trump’s economic agenda of tax cuts, and infrastructure spending put through. The thought of this key backroom operator heading for the exit could sound the death knell for Trump fiscal agenda.

Diminishing West Wing support from both business and political allies will continue to abrade investors’ confidence in President Trump’s economic agenda.

The White House Drama shows little sign of easing and with US investors nerves fraying at the thought of a discombobulated Whitehouse as the face of the nation, investor risk appetite could remain fractured for some time

The dollar, for the most part, remains in a state of directionless confusion, supported on the one hand by resurgent US economic data yet burdened by the expanding rat’s nest in the West Wing.

Japanese Yen

The go to currency haven USDJPY continues to sag in early Asia trade as investor remain unnerved by the 24/7 US political melodrama that’s filling the airwaves. A very risk off scenario was evident overnight, and I suspect there could be more room for this move to play out as one should surmise we’ve only brushed the surface on the Cohn saga.

Euro

Not too surprising as the market chatter was suggesting that the ECB would lean against the speed of the EURO’s recent ascension The European Central Bank minutes showed concern over EURUSD “overshooting” providing a distinctly dovish flavour to the minutes.This should take a bit of wind out of the Euro sails over the short run until further clarity on the ECB tapering plans are cemented

Australian Dollar

Risk aversion weighing on the risk sensitive Aussie overnight

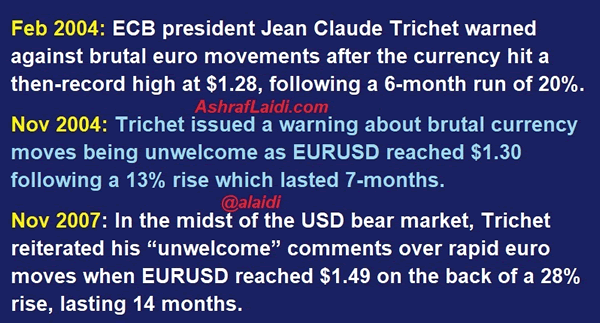

Euro Far From Brutal

The big moves today were undoubtedly in equities. But the euro suffered a minor bump on the release of the minutes from last month's ECB Governing Council policy meeting, which revealed growing concerns with a possible overshoot in the value of the euro. Before we start speculating over when ECB policy makers may start jawboning the currency lower, it's worth reminding the times when and why the ECB warned over excessive euro strength.

WTI Oil Price Rebounds from Fresh Three-Week Low

WTI oil price rebounds from fresh three-week low at $46.44 posted on Thursday but action remains capped by daily cloud top ($47.00) which was broken on Wednesday's strong fall and now acts as resistance.

Oil maintains bearish bias on persisting concerns about rising global production, as Wednesday's much stronger than expected draw in crude inventories showed no positive impact on oil price.

Repeated close within the cloud, following break and close below $47.21 (Fibo 38.2% of $42.04/$50.41 rally) will be another strong bearish signal for further extension of bear-leg from $50.41 peak.

Bears found footstep at $46.52 (55SMA) which was dented today, with sustained break lower to trigger further retracement of $42.04/$50.41 rally.

Above daily cloud top, next significant barrier lies at $47.69 (broken daily Kijun-sen).

Res: 47.00; 47.69; 48.00; 48.32

Sup: 46.44; 46.22; 45.50; 45.24

Greenback Holds Positions Despite Contradicationary Data

The euro price has fallen without substantial reasons today and despite negative news for the USD thanks to President Trump losing support from business circles that may lead to a deepening of the political crisis in the US. Traders mostly ignored the increase of the Eurozone's trade balance surplus to 22.3 billion euro in July versus the 19 billion euro in June. The consumer price index in July remained at 1.3% which met an average market forecast.

Some support for the greenback came from the report on initial unemployment claims that reduced to 232,000 but it was partly offset by industrial production growth in America of only 0.2% in the previous month which is 0.1% less than expected. The markets also noted the negative effect from the lack of unity between the FOMC members concerning the question of a third rate hike for this year. The quotes are consolidating in anticipation of new drivers.

The strong data on retail sales expansion in the UK during the previous month by 0.3% against the expected 0.2% was not able to change the bearish sentiment for the GBP/USD and this reaction may point to a high possibility of further GBP/USD decline.

The strong demand for the US dollar was also able to offset positive news from the Australian labour market in July. The the unemployment rate fell by 0.1% to 5.6% and employment increased by 27,900 against the forecasted 19,800.

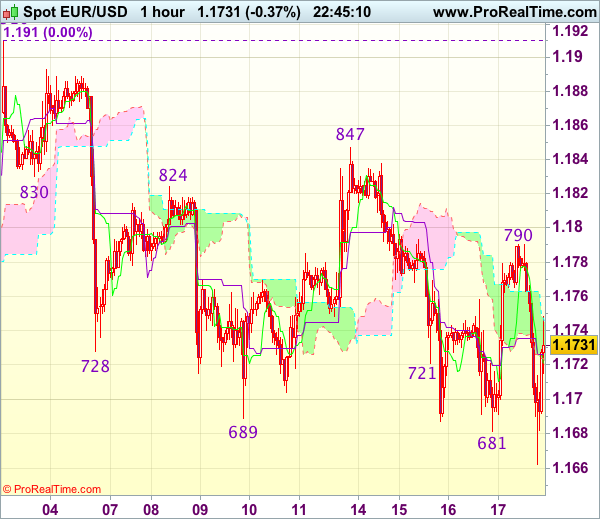

EUR/USD

The volatility of EUR/USD remains high. Currently the quotes are trying to fix below 1.1700 and in case of success we are likely to see the quotes hitting 1.1620 and 1.1500. The RSI on the 15-mitute chart just rebounded from the oversold zone that gives the bears a chance to resume pulling the price down. In case of an upward correction the potential target will be 1.1800.

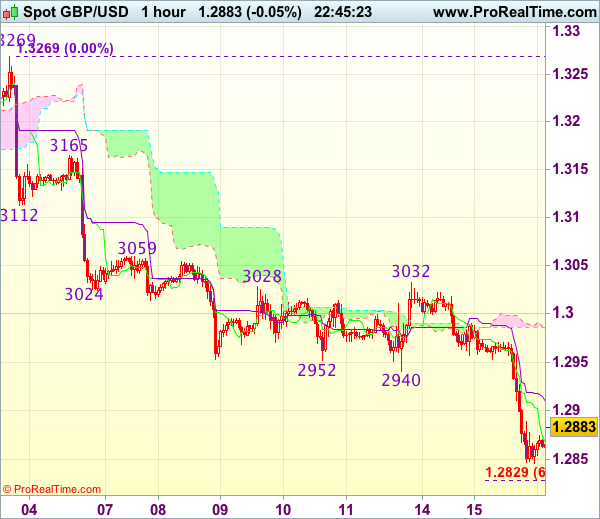

GBP/USD

The bulls in GBP/USD were not able to succeed in gaining a foothold above 1.2880 and breaking through the upper limit of the descending channel. In case of leaving the channel and fixing above 1.2900 the immediate objectives will be at 1.2950 and 1.3050. On the other side, there remains an increased probability of a continued decline within the channel to the closest targets at 1.2800 and 1.2740.

AUD/USD

The AUD/USD price rolled back to the SMA100 and is currently trying to resume growing. In this case the next targets will be at 0.8000 and 0.8050. The MACD signal line has crossed the zero level which is in favour of further decline to the closest support at 0.7900 or even below it.

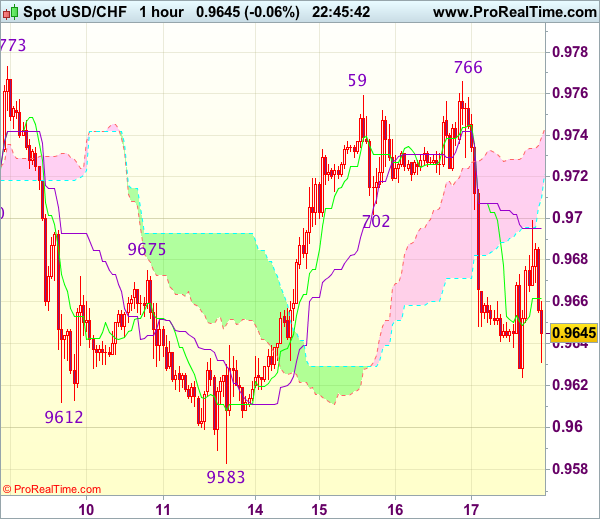

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9643

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9662

Kijun-Sen level : 0.9691

Ichimoku cloud top : 0.9743

Ichimoku cloud bottom : 0.9721

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s brief rise to 0.9766, the subsequent sharp retreat after faltering below resistance at 0.9773 dampened our bullishness and further choppy consolidation below said resistance would be seen, hence weakness to 0.9620 cannot be ruled out, however, reckon downside would be limited to 0.9600-05 and support at 0.9583 should remain intact, bring another rebound later.

On the upside, whilst recovery to 0.9695-00 cannot be ruled out, reckon upside would be limited to the upper Kumo (now at 0.9743) and price should falter well below resistance at 0.9766, bring another retreat later. As near term outlook is mixed, would be prudent to stand aside in the meantime.

Trade Idea Wrap-up: GBP/USD – Sell at 1.2920

GBP/USD - 1.2883

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2868

Kijun-Sen level : 1.2910

Ichimoku cloud top : 1.2986

Ichimoku cloud bottom : 1.2984

Original strategy :

Sell at 1.2920, Target: 1.2820, Stop: 1.2955

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2920, Target: 1.2820, Stop: 1.2955

Position : -

Target : -

Stop : -

As cable has remained under pressure after yesterday’s selloff, adding credence to our bearish view that the decline from 1.3269 top is still in progress for retracement of early upmove, hence downside bias remains for further weakness to 1.2825-30 (61.8% projection of 1.3269-1.2940 measuring from 1.3032), having said that, near term oversold condition should limit downside to 1.2800 and reckon 1.2770 would hold from here, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell sterling on recovery as said previous support at 1.2933 should turn into resistance and cap cable’s upside, bring another decline. Above 1.2950 would defer and risk a stronger rebound to 1.2990-00 before another decline.

Trade Idea Wrap-up: EUR/USD – Buy at 1.1715

EUR/USD - 1.1744

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.1714

Kijun-Sen level : 1.1726

Ichimoku cloud top : 1.1743

Ichimoku cloud bottom : 1.1720

New strategy :

Buy at 1.1715, Target: 1.1815, Stop: 1.1680

Position : -

Target : -

Stop : -

Although the single currency slipped again today, lack of follow through selling on break of support at 1.1681 and current rebound from1.1662 suggest an intra-day low is possibly formed and consolidation with mild upside bias is seen for another test of indicated resistance at 1.1790, however, break there is needed to add credence to this view, bring further gain to 1.1820 but resistance at 1.1847 should hold from here.

In view of this, we are looking to buy euro on dips as 1.1700-10 should limit downside. Below 1.1680-85 would risk retest of 1.1662, break there would extend the erratic decline from 1.1910 top to 1.1640-50 (50% Fibonacci retracement of 1.1370-1.1910 and previous support) but reckon 1.1600 would hold from here.

ECB Warned of Euro Appreciation, Asset Purchase Reference to be Changed Soon

ECB's July minutes voiced concerns over euro's strength. This is particularly important as the central bank is about to discuss tapering of the asset purchase program. Yet, the members generally agreed that "there was presently a continuing need for steady-handed and persistent monetary policy". The single currency instantly dropped to a 3-week low of 1.1661 against USD, 2-day low of 0.9061 against GBP and 4-day low of 1.1302 against CHF, before recovery.

The central bank expressed the concerns over euro's appreciation. Policymakers worried about "a possible overshooting in the repricing by financial markets, notably the foreign exchange markets, in the future". They emphasized that "the still favourable financing conditions could not be taken for granted and relied to a considerable extent on a continued high degree of monetary policy support".

On the asset purchase program, the minutes indicated that the members discussed making "incremental" changes to their forward guidance as they believed that "postponing an adjustment for too long could give rise to a misalignment between the Governing Council's communication and its assessment of the state of the economy". This could "trigger more pronounced volatility in financial markets when communication eventually had to shift". At the post meeting press conference, President Drahghi noted that the discussion of tapering might begin in the fall. In June, the members considered "revisiting the easing bias with respect to the APP purchases, whereby the Governing Council signaled its readiness to increase the pace and/or duration of the asset purchases if necessary". They eventually decided to remain cautious and prudent, and maintain the original language.

Persistently weak inflation remained a concern. Headline CPI stayed unchanged at +1.3% y/y, while core CPI improved for a second consecutive month to +1.27%, in July. However, inflation remained well below ECB's target of +2%.

We believe ECB would begin the discussion of tapering asset purchases in coming months. The actual timing would be somehow affected by euro's movement. EURUSD has rallied for 6 consecutive months since March, gaining +11.5%. The momentum has accelerated since June as ECB removed the reference that it would move the interest rates "lower" and Draghi suggested in late June that the Eurozone's "deflationary forces have been replaced by reflationary ones". During the period, weaker-than-expected inflation and the political drama in the White have also weighed on the greenback. A stronger currency is tightening in nature, making tapering less urgent.

Euro Slides to 3-Week Lows on ECB Overshoot Concerns; Dollar Weighed by Trump, Fed

The euro underperformed its peers in today's European session as a combination of option expiries and dovish ECB meeting minutes drove the single currency to three-week lows against the US dollar. The greenback managed to reverse around half of yesterday's losses brought on by the FOMC minutes that showed growing concern among some Fed policymakers that inflation might remain below 2% for longer than anticipated.

In other currencies, the pound was unable to get much of a lift from stronger-than-expected retail sales data out of the UK, but the aussie surged on the back of sharp gains in metal prices.

The euro fell to its lowest since late July, touching $1.1661 (down almost 1%), before rebounding to around the $1.17 level. It was also lower against the yen and sterling, falling to 128.83 yen (a one-week low) and 0.9079 pounds. The euro had come under pressure earlier in the day from large option expiries but its losses were exasperated by the release of the European Central Bank's accounts of the July policy meeting. The minutes lacked any hawkish tone and while the central bank signalled that a review of policy was forthcoming in the autumn, policymakers expressed concern about "the risk of the exchange rate overshooting in the future".

There was little support for the single currency from the final Eurozone CPI readings for July, despite an upward revision to the core rate. Headline inflation was confirmed at an annual rate of 1.3% in July, but core CPI was revised from 1.2% to 1.3% – the highest in four years.

UK retail sales were also released today, which came in above expectations. The month-on-month rate was up 0.3% in July, beating estimates of 0.2%, but the year-on-year rate moderated to 1.3% from 2.8% in June, missing forecasts of 1.4%. Reaction to the data was limited with the pound rising only briefly after the data as the stronger-than-expected figures for July were offset by downward revisions to the prior month's numbers.

The pound spiked to $1.2905 after the data before dipping to as low as $1.2852, only to head back up again in late European session to trade around $1.2880.

In US data, jobless claims and the Philly Fed beat expectations but industrial output disappointed. Weekly jobless claims fell to 232k in the week starting August 7 – the lowest in six months. This was better than the expected 240k and down from 244k in the prior week. The Philly Fed's manufacturing index fell to 18.9 in August from 19.5 in July, though this was above forecasts of 18.5. Finally, industrial output in the United States expanded by 0.2% m/m in July, slower than the prior 0.4% rate and below estimates of 0.3%.

The dollar firmed slightly after the robust jobless claims numbers but fell back following the soft industrial output numbers. However, the greenback held on to most of its gains posted after its Asian session lows when it had hit 109.64 yen. It was last trading slightly down on the day around 110.10 yen as political uncertainty surrounding President Trump weighed on the currency, in addition to yesterday's dovish FOMC minutes.

Gold benefited from the risk-off associated with Trump's decision yesterday to disband the White House business councils after several CEOs quit in protest to Trump's remarks over the violence in Virginia involving far-right groups. A less hawkish Fed also boosted gold, with the yellow metal coming close to breaking above last week's two-month high of just under $1292 an ounce.

Meanwhile, non-precious metals, specifically industrial metals, eased from their recent highs on profit taking. Expectations of rising demand from China, as well as from the Chinese government's efforts to reform the country's industrial sector by cutting overcapacity had driven copper and aluminium prices to three-year highs yesterday, while zinc had soared to a near 10-year high.

The metal rally has helped the Australian dollar to move away from one-month lows to climb to a two-week high of $0.7962 earlier today. The aussie eased to around $0.7920 in late session.

Oil prices continued to drift lower today, dropping to three-week lows. Another drawdown in US weekly crude stocks yesterday did little to boost prices as investors remained concerned about rising US output, which rose to the highest in two years last week. WTI crude was last trading slightly down on the day at $46.72 per barrel and Brent crude at $50.26 a barrel.

Looking ahead to the remainder of the day, speeches by Dallas Fed President, Robert Kaplan and Minneapolis Fed President, Neel Kashkari should attract some attention.