Sample Category Title

Trade Idea Update: EUR/USD – Stand aside

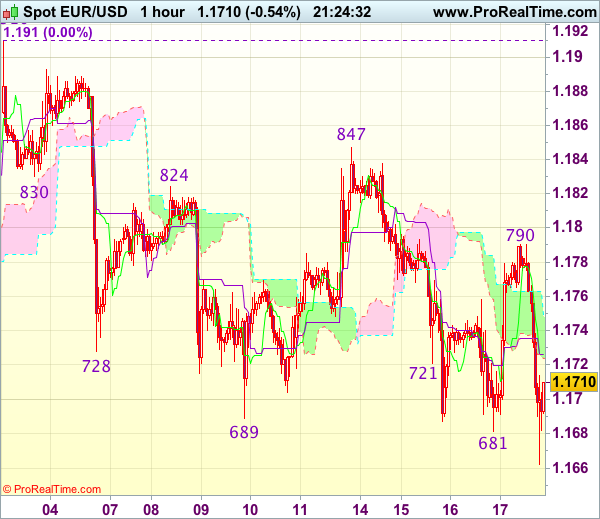

EUR/USD - 1.1716

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the single currency met renewed selling interest at 1.1790 and has dropped again, lack of follow through selling on break of previous support at 1.1681 (yesterday’s low) suggests consolidation would be seen and recovery to 1.1745-50 cannot be ruled out, however, said resistance at 1.1790 should hold and bring another decline later. Below 1.1660 would extend the erratic decline from 1.1910 top to 1.1640-50 (50% Fibonacci retracement of 1.1370-1.1910 and previous support) but reckon 1.1600 would hold from here.

On the upside, only break of said resistance at 1.1790 would suggest low is formed instead, bring a stronger rebound to 1.1820-25 but resistance at 1.1847 should hold on first testing. As near term outlook is still mixed, would be prudent to stand aside for now.

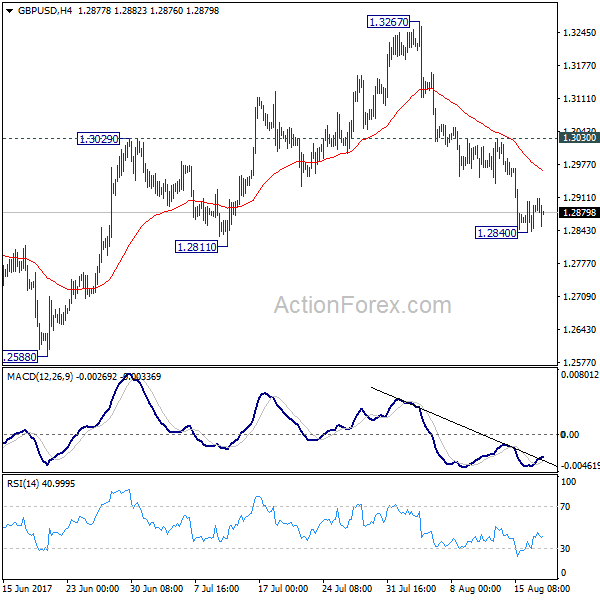

Sterling Again Rejected From 1.2900 Level

The GBPUSD pair has come under further selling pressure, despite better than expected monthly United Kingdom retail sales data. Retail sales increased by 0.3 percent in July, with the year on year comparison figure growing by 1.3 percent.

Sterling has again moved below the 1.2900 level, with price dropping sharply towards trendline support, and the pairs 100-day moving average, at 1.2858, as the U.S dollar moves higher across the board.

The GBPUSD pair has now turned bearish on all-time frames, and trades below the daily, weekly and monthly calculated pivot points.

Key technical support is found at the 100-day moving average, at 1.2858, the current weekly price low, at 1.2841. The June monthly price low offers further support for sterling, at 1.2810.

To the upside, the daily pivot point is found at 1.2879, with the daily price high offering further resistance, at 1.2911. Above the daily price high, GBPUSD buyers will look to target the key 1.2932 and1.2951 levels.

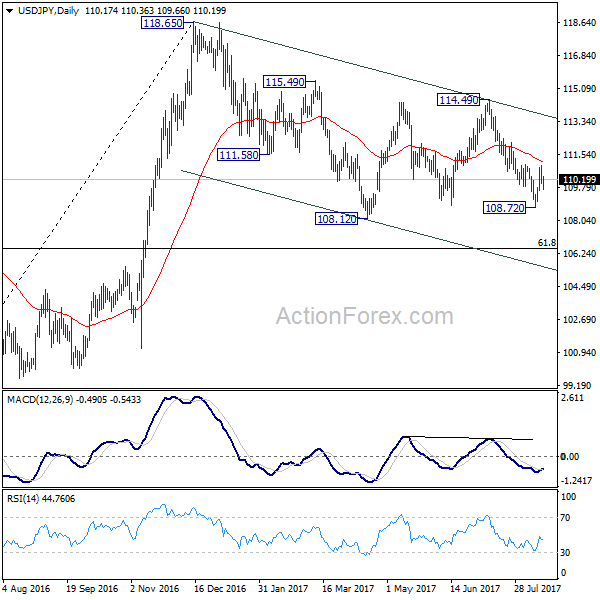

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 110.09

Original strategy :

Exit long entered at 110.00

Position : - Long at 110.00

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s marginal rise to 110.95, the subsequent selloff on dollar’s broad-based weakness, dampening our bullishness and suggesting the rebound from 108.73 has ended at 110.95, hence downside risk is seen for weakness to 109.60, then test of support at 109.42, however, as broad outlook remains consolidative, reckon downside would be limited to 109.00-05 and said support at 108.73 should remain intact.

In view of this, would be prudent to stand aside for now. Above 110.40 would bring recovery to the upper Kumo (now at 110.72), however, price should falter below said resistance at 110.95, bring another retreat later.

Euro Weakens as ECB Shows Concerns Over its Strength, Dollar Recovers as Markets Reassess Fed Minutes

Euro trades broadly lower today as ECB monetary policy meeting accounts show that policy makers are concerned with the currency's strength. Meanwhile, Dollar regains much ground against most currencies. Markets reassessed FOMC minutes released yesterday as saw them not as dovish as initially perceive. Overall, the forex markets are mixed with Aussie and Yen trading as the strongest ones at the same time. In other markets, Gold is staying firm above 1290 but lacks follow through buying for a take on 1300 handle yet. WTI crude oil is extending recent decline to as low as 46.46 so far.

ECB accounts show concerns on Euro strength

The accounts of July 19-20 ECB policy meeting showed that officials are concerned with Euro's strength. ECB noted that "while it was remarked that the appreciation of the euro to date could be seen in part as reflecting changes in relative fundamentals in the euro area vis-a-vis the rest of the world, concerns were expressed about the risk of the exchange-rate overshooting in the future." Meanwhile, the account also showed that "the point was made that, looking ahead, the Governing Council needed to gain more policy space and flexibility to to adjust policy and the degree of monetary policy accommodation, if and when needed, in either direction."

At the same time, policy makers also discussed making "incremental" changes to the central bank's forward guidance. And the account noted that "postponing an adjustment for too long could give rise to a misalignment between the Governing Council's communication and its assessment of the state of the economy, which could trigger more pronounced volatility in financial markets when communication eventually had to shift." Besides, the accounts noted the removal of political uncertainly in Eurozone and markets expectations over US interest rates. And, "these two factors were now largely priced out, leaving the euro back around the levels prevailing before the UK referendum."

Released in Eurozone, CPI was finalized at 1.3% yoy in July, core CPI at 1.2% yoy. Eurozone trade surplus widened to EUR 22.3b in June. Also from Europe, UK retail sales rose less than expected by 0.3% mom in July.

FOMC minutes show worries on inflation

The price actions in US dollar and Treasuries suggested that the market views the July FOMC minutes as a dovish one. The minutes revealed that policymakers were concerned that US inflation might stay below 2% longer than previously anticipated. However, the minutes were not as dovish as anticipated. Despite the disappointment in June inflation, most members continued to maintain the view that the current weak price levels were transitory, although some were worried that inflation might take longer than previously expected to reach the 2% target. Indeed, headline inflation improved modestly, while core inflation steadied, in July. These should be a relief for the members. Barring any dramatic deterioration the economic outlook, we continue to expect one more rate hike in December and a formal announcement of balance sheet reduction to come in September. More in FOMC Minutes Not As Dovish As Seen By The Market

US initial jobless claims dropped -12k to 232k in the week ended August 12, below expectation of 240k. That's the lowest level since February and second lowest since 2009. Continuing claims dropped -3k to 1.95m in the week ended August 5. Industrial production rose 0.2% in July while capacity utilization was unchanged at 76.7%.

Elsewhere

Japan trade surplus widened to JPY 0.34T in July. Australia employment grew 27.9k in July, above expectation of 20.0k. Australia unemployment rate was unchanged at 5.6%. New Zealand PPI inputs rose 1.4% qoq in Q2 while PPI outputs rose 1.3% qoq.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1705; (P) 1.1741 (R1) 1.1803; More...

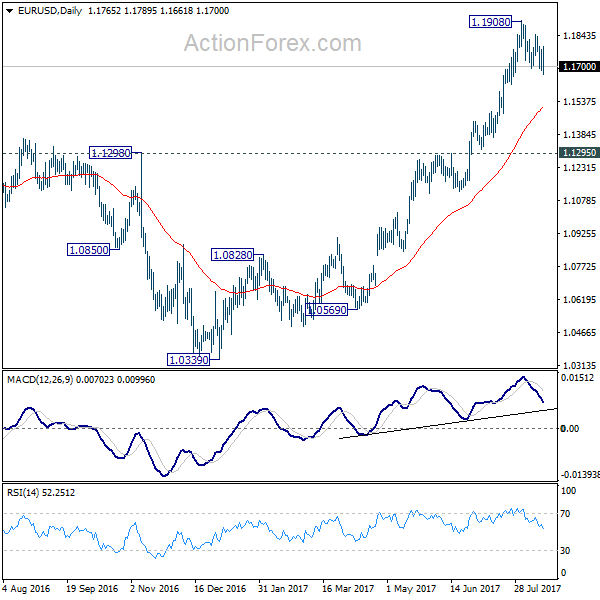

EUR/USD's correction fall from 1.1908 resumed after brief recovery. But intraday bias stays neutral for the moment. While deeper pull back could be seen, downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring rebound. On the upside, break of 1.1908 will extend recent up trend to 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Inputs Q/Q Q2 | 1.40% | 0.90% | 0.80% | |

| 22:45 | NZD | PPI Outputs Q/Q Q2 | 1.30% | 0.70% | 1.40% | |

| 23:50 | JPY | Trade Balance (JPY) Jul | 0.34T | 0.20T | 0.08T | 0.09T |

| 23:50 | JPY | Merchandise Trade Exports Y/Y Jul | 13.40% | 13.40% | 9.70% | |

| 01:30 | AUD | Employment Change Jul | 27.9K | 20.0K | 14.0K | |

| 01:30 | AUD | Unemployment Rate Jul | 5.60% | 5.60% | 5.60% | 5.70% |

| 08:30 | GBP | Retail Sales M/M Jul | 0.30% | 0.60% | 0.60% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | 22.3B | 20.3B | 19.7B | 19.0B |

| 09:00 | EUR | Eurozone CPI M/M Jul | -0.60% | -0.50% | 0.00% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jul F | 1.30% | 1.30% | 1.30% | |

| 09:00 | EUR | Eurozone CPI - Core Y/Y Jul F | 1.20% | 1.20% | 1.20% | |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | CAD | Manufacturing Shipments M/M Jun | -1.80% | -1.00% | 1.10% | |

| 12:30 | USD | Initial Jobless Claims (AUG 12) | 232K | 240k | 244k | |

| 12:30 | USD | Philadelphia Fed Business Outlook Aug | 18.9 | 18.8 | 19.5 | |

| 13:15 | USD | Industrial Production Jul | 0.20% | 0.30% | 0.40% | |

| 13:15 | USD | Capacity Utilization Jul | 76.70% | 76.70% | 76.60% | 76.70% |

| 14:00 | USD | Leading Indicators Jul | 0.30% | 0.60% | ||

| 14:30 | USD | Natural Gas Storage | 28B |

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1705; (P) 1.1741 (R1) 1.1803; More...

EUR/USD's correction fall from 1.1908 resumed after brief recovery. But intraday bias stays neutral for the moment. While deeper pull back could be seen, downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring rebound. On the upside, break of 1.1908 will extend recent up trend to 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

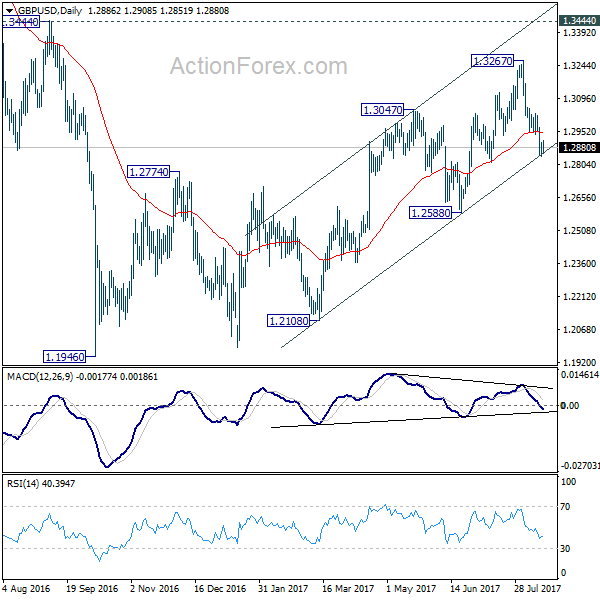

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2853; (P) 1.2877; (R1) 1.2915; More...

Intraday bias in GBP/USD stays neutral for consolidation above 1.2840 temporary low. Outlook will stay bearish as long as 1.3030 resistance holds. We're preferring the case that correction from 1.1946 is completed at 1.3267. Below 1.2840 will target 1.2588 key support to confirm our bearish view. Nonetheless, break of 1.3030 will dampen our view and turn bias back to the upside for retesting 1.3267.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

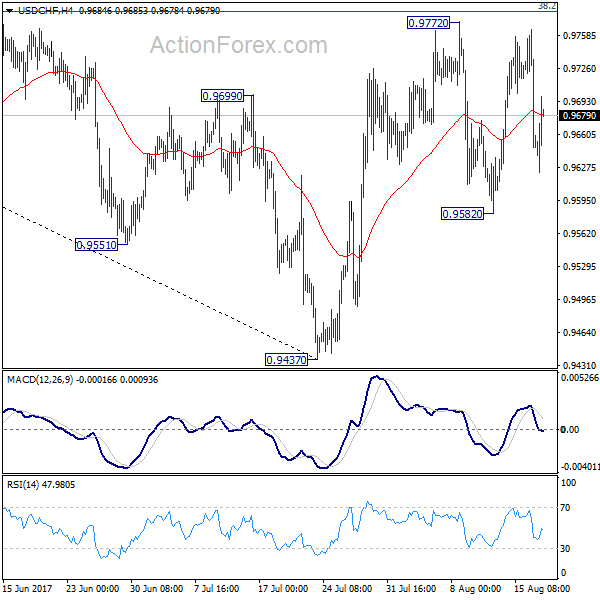

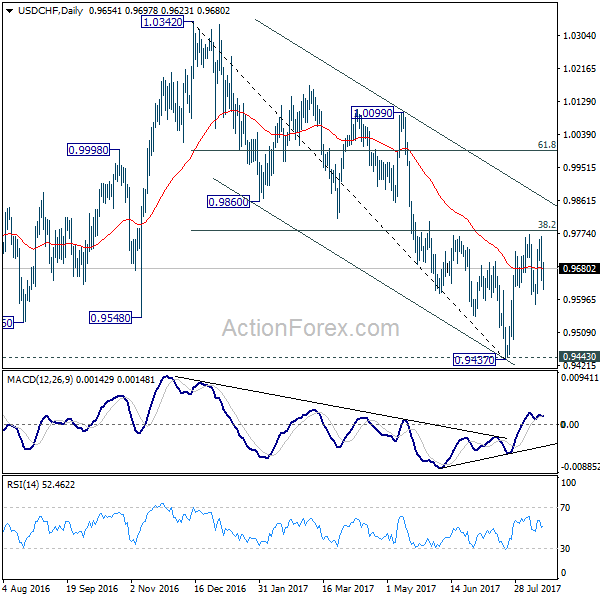

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9614; (P) 0.9690; (R1) 0.9731; More...

Intraday bias in USD/CHF remains neutral for the moment. On the upside, decisive break of 0.9772 resistance will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. USD/CHF should then target channel resistance (now at 0.9862) next. Meanwhile, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.82; (P) 110.38; (R1) 110.74; More...

USD/JPY recovery after dipping to 109.56 earlier and intraday bias is turned neutral first. Overall, price actions from 118.65 are seen as a correction pattern. There is clear indication that it's completed yet. On the downside, break of 108.72 will likely resume the whole decline from 118.65 through 108.12 to next medium term fibonacci level at 106.48. On the upside, above 110.94 will extend the rebound to 112.18 resistance next. Break there will turn focus back to 114.49 key near term resistance.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

UK Retail Sales Data Fails to Pack the Punch

Sterling bulls were hesitant to make an appearance during Thursday's trading session, despite U.K. retail sales exceeding market estimates by rising 0.3% in July.

July sales were largely driven by the biggest increase in food buying in almost two years, which offset a decline in the purchase of other goods. However, in annual terms, sales disappointed by growing just 1.3%, which was below the 1.6% expectations. What took the punch out of the report and repelled bulls further, was the fact that June's retail sales were also revised down from 0.6% to 0.3%. Although the volume of goods sold in July printed above expectations, the total growth was relatively soft and highlighted how the gap between inflation and wages continues to squeeze household finances.

It has certainly been another interesting trading week for Sterling, with bear's bent on winning the tug of war around 1.2850. The GBPUSD is under pressure on the daily charts with traders eyeing 1.2850. A breakdown and daily close below this level should encourage a further decline towards 1.2775.

Euro pressured following ECB minutes

The mighty Euro lost ground against a stronger Dollar on Thursday, after the European Central Bank minutes from July's meeting revealed concerns over the strength of the Euro.

A stronger Euro poses a headache for European policy makers and dilutes the ECB's efforts to hit the golden 2% inflation target by making exports less attractive and imports cheaper. The absence of a hawkish presence in the minutes, also compounded the downside, with the EURUSD trading around 1.1670 at the time of writing.

Although encouraging macro-fundamentals from the European economy have supported the Euro, speculation around the central bank tapering QE, remains one of the key culprits behind the Euro's resurgence. With the Euro becoming sensitive to monetary policy speculation, the currency is at risk of depreciating further against the Dollar if expectations of the central bank tapering QE, start to fade amid the inflation concerns.

Commodity Spotlight – Gold

Gold bulls received a shot in the arm on Wednesday after July's dovish Federal Reserve minutes weighed on the prospects of higher US interest rates this year.

The yellow metal was granted further support from the ongoing uncertainty revolving around President Donald Trump which bolstered its allure. With fading rate hike expectations punishing the Dollar and political drama in Washington stimulating risk aversion, Gold is likely to remain supported moving forward. From a technical standpoint, the yellow metal is bullish on the daily timeframe as there have been consistently higher highs and higher lows. The breakout above $1283 should encourage a further appreciation towards $1300.

German, Italian Exports Most Exposed to Strengthening Euro, Netherlands Cushioned

In times of a strengthening euro, the region's exporters could be hurt as sales generated outside of the eurozone may translate poorly back into earnings reports denoted in euros. The biggest export countries with the least exposure to the single currency zone could be dented the most. Germany and Italy are some of the world's largest exporters, yet they have the smallest amount of exports delivered within the eurozone. By contrast, the Netherlands outperforms them with more than 50% of revenues generated within the region.

With about $1.3 trillion in exports, Germany ranks third among the world's largest export countries, behind China and the US. That translates to almost half of its annual GDP. The US is its largest single country-market as 9% of its products get delivered there. While Germany's exposure to the eurozone is high, standing at about a third of its total exports, the share is still among the lowest compared to its large peers. Germany delivers about 6% of its exports to China.

The recent strengthening of the euro against the currencies of the US and China could harm some of the large exporters that report in the single currency. The euro rose 12% against the dollar this year while it is 8% higher versus the yuan. More importantly for exporters, looking at the average value of quarterly periods we can note that the average value of the euro thus far in the third quarter is 4% higher against the dollar and 5% higher against the yuan when compared to the average value of the third quarter of 2016. Due to the rally in the greenback following last year's November presidential elections, the fourth quarter could be especially arduous for euro-reporting exporters even if the common currency stays at the current levels. Comparing the average exchange rate thus far in the second half of the year versus the whole of the second half of 2016, we can note that the average euro/dollar pair and the euro/yuan is 6% higher.

Looking at individual German companies, Volkswagen Group, Daimler, BMW, Siemens and Bayer are the largest exporters. Daimler reported a 3% boost to its top-line during 2016 on the back of the weaker euro against some currencies the company exports to. Its largest markets comprise of the US (26% of group revenues is generated in the US) and China (10% of group revenues). BMW had around a 2% translation boost to its 2016 revenue. The group generates 17% of its total revenues from the US and 18% from China.

Luxottica is one of Italy's largest export companies with only about a quarter of its revenues coming from Europe. North America is its largest market with almost two-thirds of group revenues generated there. During the first half of the year, the company had around a 2.5% revenue lift from the translation effect when the average value of the euro/dollar pair was 3% down. However, with the euro strengthening, especially against the dollar towards the end of the year, the company could face strong headwinds.

Looking at countries that have the largest eurozone exposure, the Netherlands comes first. This provides a cushion for the country and its exporters in times of an appreciating exchange rate. The Netherlands also has the highest share of its exports delivered to the UK compared to its peers. While this was bad in the first six months of the year, the second half could improve due to the annualization of the weakness in sterling following the plunge last June after the Brexit referendum.

Spain ranks second and France third in their export exposure to the eurozone, among analyzed countries.

Apart from exporters, all tourism dependent businesses within the eurozone could feel a pinch. Chinese tourists, the world's largest outbound nation, tend to use the strength of the yuan against the currency of a potential destination as one of the criteria when choosing their next travel location. During the summer of 2015, many tourism dependent businesses saw a revenue lift due to a surge of Chinese visitors. During 2015, the average value of the euro/yuan pair fell 15% versus the average value of 2014, luring mainland visitors.

Should the European Central Bank give a sign it will start tightening monetary policy within the eurozone at its next meeting, the euro could strengthen further. Many economists are predicting that the euro could easily hit the level of 1.20 by year end. However, recent economic data out of the US has instilled confidence that the Federal Reserve will hike interest rates once again this year that boosted the dollar. Even if the euro doesn't strengthen further, the current levels against major peers are still significant enough to dent sales via negative translation effect.