Sample Category Title

Cable Probed Below Strong 100SMA

Cable fell on Thursday and probed below strong 100SMA / daily cloud top supports (1.2861/64) following repeated failure above 1.2900 barrier. Negative tone continues to dominate despite better than expected release of UK Retail Sales, as overall structure is bearish on daily chart.

Repeated attack at daily cloud top which was cracked in past two days but without close in the cloud, could result in firm break this time, as fresh bears eye another strong support at 1.2840 (Tue / Wed lows) to open daily cloud base (1.2818) and generate firm signal of bearish continuation.

Such scenario could result in extension towards weekly Kijun-sen (1.2688) and may expose 1.2588 (21 June low).

We will look for today's close for further negative signals on close within the cloud. Conversely, prolonged consolidation could be expected if the pair repeatedly closes above daily cloud.

Daily 55SMA marks strong resistance and first upper pivot at 1.2929.

Res: 1.2908; 1.2929; 1.2950; 1.2965

Sup: 1.2840; 1.2811; 1.2749; 1.2688

GBP/USD Needs A Spark

Price decreased today and tries to resume the downside movement. Technically was somehow expected to decrease in the upcoming period, but the fundamental factors have taken the lead in the yesterday's session. Stays much below the 1.3000 psychological level, signaling that the bears are still in the game.

GBP/USD decreased today as the USDX has managed to delete the morning losses and to climb above 93.81 static resistance. I'll repeat myself, but only a valid breakout above the 93.81 level will confirm a larger rebound on the USDX.

You should be careful later as the United States data may bring a high volatility, the figures will shake the markets. The Unemployment Claims are expected to drop from 244K to 240K in the previous week, while the Capacity Utilization Rate could be reported at 76.7%, above the 76.6% in the previous reporting period. The Industrial Production could increase as well, by 0.3%, the greenback will be boosted by better economic numbers.

Price is challenging the upper median line (UML) of the major descending pitchfork. We had only a false breakdown on Tuesday because it is located above this major dynamic support. Was expected to drop after the breakdown below the warning line (wl1) of the minor ascending pitchfork.

I've said in the previous analysis that only a valid breakdown below the UML and below the 1.2798 static support will confirm a larger drop in the upcoming weeks. Price could increase again if the mentioned support levels will hold and will reject it.

EUR/JPY Melting Down

Price goes down as expected, I've said that we may have another leg lower after the minor rebound. Has come to retest the upper median line (UML) and the red uptrend line, but failed to retest the median line (ml) of the black ascending pitchfork and the upper median line of the minor descending pitchfork, signaling a decrease.

However, we need a confirmation that we'll have a broader drop in the upcoming weeks, only a valid breakdown below the 38.2% retracement level will validate it.

USD/JPY Undecided

USD/JPY dropped in the morning and retested the red uptrend line and now has squeezed again. Needs a bullish spark to be able to increase further. We may have a bullish momentum if the US data will impress later. Hovers above the 110.00 psychological level, the next upside targets will be at the 38.2% retracement level and higher at the third warning line (WL3).

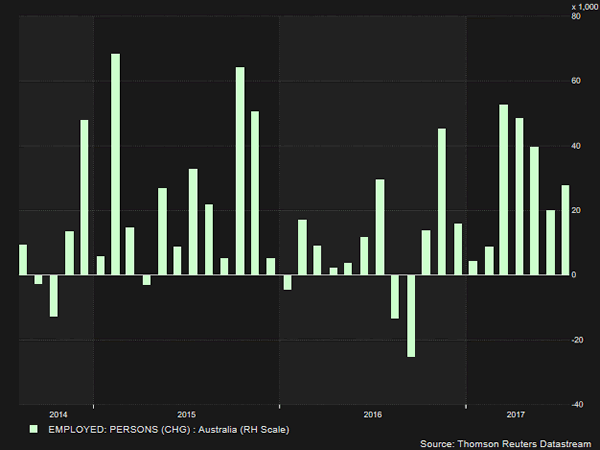

Aussie Extends Gains As Australian Employment Climbs, But Number Of Full-Timers Decreases

In July, employment in Australia rose more than expected. However, full-time jobs decreased while the number of part-timers increased. The RBA projects labor conditions improving in the upcoming years and hence boosting the overall economy by driving consumption higher. After the data release, the Australian dollar experienced volatility relative to its US counterpart, rising to a near two-week high later during early European trading hours.

On Thursday, the Australian Bureau of Statistics published labor data for the month of July. The figures showed that the Australian economy created 27,900 new job positions (seasonally adjusted), exceeding the number of 20,000 expected by analysts, which was also June’s reading (upwardly revised from 14,000).

Overall, the participation rate ticked up by 0.1 percentage points to 65.1% while expectations were for the rate to remain unchanged at 65.0%. Turning to the unemployment rate, it slipped as expected to 5.6%, below the 5.7% seen in June and which was the result of an upward revision from 5.6%.

Breaking down the figures, full-time positions fell for the first time since April, posting the largest decline in six months, while part-time positions rose. Particularly, 20,300 full-time positions were lost compared to an expansion of 69,300 observed in the previous month. In contrast, 48,200 part-time jobs were added during July. On a yearly basis though, full-time and part-time employment were up by 197,700 and 41,600 positions respectively.

On Tuesday, the RBA minutes for the latest meeting revealed the confidence the Bank’s policymakers had on the labor market outlook, urging for a switch in focus towards the housing market, where debt levels are extremely high. In general, July’s labor data justify the RBA’s optimism about labor conditions strengthening in the future. However, with full-time positions decreasing, wages are likely to grow slowly instead as full-time payments are those which contribute the most to wage growth. Slowly growing wages are expected to restrict consumption from rising faster.

Concluding with the reaction in the forex markets, the Australian dollar had a mixed response versus the greenback upon immediate release of the numbers but later on built on yesterday’s strength (it finished the day 1.3% higher in yesterday’s trading) to rise to a near two-week high of $0.7962. The pair was last up on the day, though it gave up on a significant portion of the gains it made earlier on the day.

Market Update – European Session: ECB Minutes Eyed For Clues Of QE Exit

Notes/Observations

FOMC minutes highlight the most divided Board since the central bank began normalizing policy

ECB July Minutes likely to paint a likely dovish spin ahead of any clue of when policy would begin to start normalizing

Overnight

Asia:

Australia July Employment Change: +27.9K v +20.0Ke (5th straight increase); Unemployment Rate: 5.6% v 5.6%e

Japan's exports and imports rose at a fast clip in July aided by a recovery in global demand (exports to China +18% y/y)

Europe:

Next phase of Brexit talks said to be anticipated to be delayed until Dec as London awaits new German govt

Americas:

FOMC Jun 14th Minutes: Several participants ready to move on balance sheet in July; others sought confirmation that weak inflation was transitory before next hike. Officials split over whether inflation expectations are well anchored

Fed's Mester (hawk, non-voter): do not feel soft inflation readings should delay rate hike

President Trump tweets: "Rather than putting pressure on the businesspeople of the Manufacturing Council & Strategy & Policy Forum, I am ending both. Thank you all!"

Energy:

Saudi Arabia Jun production at 10.07M v 9.88M bpd prior; exports drop to 6.89M bpd in Jun from 6.92M in May - JODI

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.2% at 378.2, FTSE -0.3% at 7411, DAX -0.3% at 12223, CAC-40 -0.4% at 5156, IBEX-35 -0.8% at 10468, FTSE MIB -0.3% at 21924, SMI -0.8% at 8973, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

European Indices trade slightly lower this morning following a pullback on Wall Street overnight. Earnings remain the focus as we enter the back end of earnings with notable upside moves for Straumann and Oriflame following results, while Kingfisher lags on the FTSE following weakler LFL sales. Other downside movers include Hikma Pharma after cutting FY forecasts, while Vestas Wind and Geberit trading sharply lower after missing estimates.

Looking ahead notable earners include Walmart and Alibaba.

Equities

Consumer discretionary [ Kingfisher [KGF.UK] -3.6% (Earnings), Rank Group [RNK.UK] -4.3% (Earnings), Sixt SE [SIX2.DE] +2.5% (Earnings), Straumann [STMN.CH] +7.6% (Earnings), Oriflame [ORI.SE] +13.5% (Earnings)]

Industrials: [Geberit [GEBN.CH] -6.8% (Earnings)]

Healthcare: [Hikma Pharma [HIK.UK] -8.1% (Earnings), Novo Nordisk [NOVOB.DK] +1.9% (Novo's Semaglutide superior to Lilly's dulaglutide on glucose control and weight loss in people with type 2 diabetes in SUSTAIN 7)]

Energy: [Vestas Wind Sys [VWS.DE] -7.5% (Earnings)]

Speakers

Thailand Central Bank Gov Veerathai reiterated view that would closely monitor the THB currency (Baht); have not seen any unusual speculation at this time

Currencies

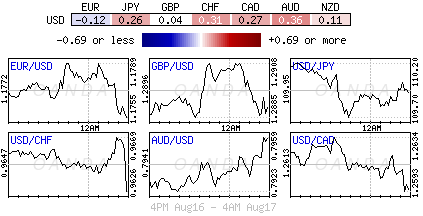

The GBP was trying to halt a 5-day decline against the USD and EUR pairs after retail sales data came in better-than-expected (back-months revised lower). GBP/USD hovering around the 1.29 level

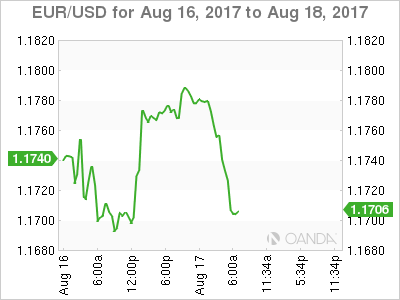

EUR/USD was lower by 0.3% ahead of the ECB release of its July minutes. Markets looking for more clarity in the ECB's account later today. Overall the view that ECB would not unveil any strategy for tapering of its bond purchases or when it is likely to make an announcement on its plan. For the time being dealers noted that the recent Euro bull run could subside with EUR/USD possible testing 1.15 if the ECB showed signs of caution

Fixed Income

Bund futures trades at 163.94 down 5 ticks as thin summer trading continues. Downside targets 163.50 followed by 162.56. To the upside the 164.50 to 165.20 remains key resistance.

Gilt futures trades at 127.57 down 1 tick after Retail Sales in UK grew modestly. A resumption to the upside could eye 128.25 then 128.75. A move back below 126.51 targets 125.97

Thursday’s liquidity report showed Wednesday's excess liquidity in the Euro Zone fell to €1.722T from €1.742T and use of the marginal lending facility rose to €174M from €94M prior.

Corporate issuance saw $5.75B come to market via 3 issuers headlined by VMWare Inc $4B 3 part offering, and Bank of New York Mellon $750M 12-year subordinated notes

Looking Ahead

(BR) Brazil Aug CNI Industrial Confidence: No est v 50.6 prior

(EG) Egypt Central Bank Interest Rate Decision: Deposit Rate currently at 18.75%; Lending Rate currently at 19.75%

05:30 (HU) Hungary Debt Agency (AKK) to sell bonds (3 tranches)

05:30 (PL) Poland to sell Bonds

06:00 (IL) Israel Jun Manufacturing Production M/M: No est v -4.1% prior

06:45 (US) Daily Libor Fixing

07:30 (EU) ECB account of the monetary policy meeting (July Minutes)

07:30 (BR) Brazil Jun Economic Activity Index (Monthly GDP) M/M: +0.7%e v -0.5% prior; Y/Y: -0.5%e v +1.4% prior

08:00 (PL) Poland July Employment M/M: 0.1%e v 0.2% prior; Y/Y: 4.3%e v 4.3% prior

08:00 (PL) Poland July Average Gross Wages M/M: 0.4%e v 2.7% prior; Y/Y: 5.4%e v 6.0% prior

08:00 (UK) Baltic Dry Bulk Index

08:30 (US) Initial Jobless Claims: 240Ke v 244K prior; Continuing Claims: 1.96Me v 1.951M prior

08:30 (US) Aug Philadelphia Fed Business Outlook: 18.0e v 19.5 prior

08:30 (CA) Canada Jun Manufacturing Sales M/M: -1.0%e v +1.1% prior

08:30 (UK) Weekly USDA Net Export Sales

09:00 (RU) Russia Gold and Forex Reserve w/e Aug 11th: No est v $420.1B prior

09:00 (RU) Russia July Unemployment Rate: 5.1%e v 5.1% prior

09:00 (RU) Russia July Real Disposable Income: 0.4%e v 0.0% prior; Real Wages Y/Y: 3.1%e v 2.9% prior

09:00 (RU) Russia July Real Retail Sales M/M: 3.5%e v 1.1% prior; Y/Y: 1.0%e v 1.2% prior

09:00 (RU) Russia July PPI M/M: +0.3%e v -0.3% prior; Y/Y: 3.0%e v 2.9% prior

09:15 (US) July Industrial Production M/M: 0.3%e v 0.4% prior; Capacity Utilization: 76.7%e v 76.6% prior; Manufacturing Production: 0.2%e v 0.2% prior

10:00 (US) July Leading Index: 0.3%e v 0.6% prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN bills

11:00 (BR) Brazil to sell 2023 and 2027 bonds

17:00 (CH) Chile Central Bank (BCCh) Interest Rate Decision; Expected to leave Overnight Rate Target unchanged at 2.50%

U.S Dollar’s Glass Chin

Thursday August 17: Five things the markets are talking about

Yesterday's FOMC meeting minutes showed that U.S policy makers are somewhat split over whether inflation expectations are well “anchored.”

Some members continue to require confirmation that a drop in the inflation rate is only ‘transitional' before there is another rate hike stateside.

Members agreed that the economic activity had risen and that the U.S labor market had continued to strengthen on average since the beginning of the year, but are stymied on why inflation remains subdued or benign.

In truth, yesterday's minutes did not seem to offer anything much different than what the market already knew. Regardless of when the Fed next raises rates, it is widely expected to tighten monetary policy very “gradually” over the longer-term, and reason enough for investors to interpret the minutes as being a tad “dovish.”

European stocks slipped after a mixed Asian session while sovereign bonds have followed U.S Treasuries higher as the market digests the reduced odds of another rate hike this year.

Note: This morning's ECB minutes (07:30 am EDT) will be eyed for clues of QE exit.

1. Stocks mixed results

In Japan, stocks felt the weight of a rebounding yen (¥110.00) and edged down overnight in thin trade. The Nikkei share average ended -0.1% lower while the broader Topix shed -0.2%. Turnover was only ¥1.806T, below the average daily ¥2T.

In Hong Kong, shares closed slightly down as profit-taking outweighed solid gains by the gaming and social media sector. The Hang Seng index fell -0.2%while the China Enterprises Index also lost -0.2%.

In China, industrial and materials stocks helped lift regional bourses higher as well as investor hopes that there will be significant changes to open up the economy more widely to foreign investors. The blue-chip CSI300 index rallied +0.5%, while the Shanghai Composite Index gained +0.7%.

In Europe, regional indices trade slightly lower following yesterday's pullback on Wall Street, with corporate earnings remaining the focus.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx600 -0.2% at 378.2, FTSE -0.3% at 7411, DAX -0.3% at 12223, CAC-40 -0.4% at 5156, IBEX-35 -0.8% at 10468, FTSE MIB -0.3% at 21924, SMI -0.8% at 8973, S&P 500 Futures -0.1%

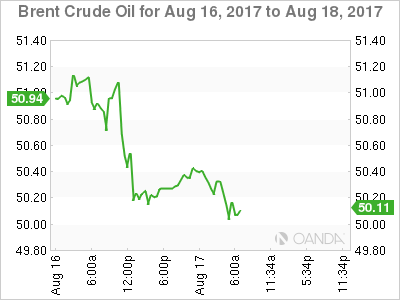

2. Oil steadies as high U.S output balances crude stock draw, gold higher

Ahead of the U.S open, oil prices trade steady after yesterday's U.S data showed a big fall in crude stockpiles, but also an increase in production to its highest in more than two-years.

Brent crude is unchanged at +$50.27 a barrel, while U.S light crude (WTI) is -5c lower at +$46.73. Both benchmarks fell more than -1% Wednesday.

Yesterday's EIA data showed commercial U.S. crude stocks had fallen by almost -13% from their peaks in March to +466.5m barrels. Stocks are now lower than in 2016.

But U.S oil output is rising fast as shale producers take advantage of a recent increase in prices – production jumped by +79k bpd to over +9.5m bpd last week, its highest level in two-years.

Note: Rising U.S output continues to undermine efforts by OPEC and non-OPEC producers to drain a global fuel glut.

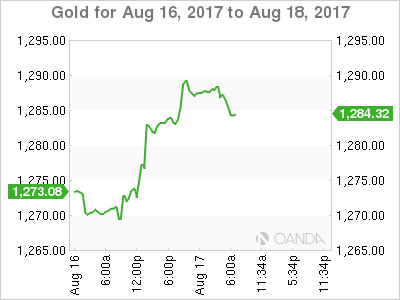

Gold has edged up on softer dollar. Spot gold is up +0.4% at +$1,287.90 per ounce, after gaining nearly +1% Wednesday.

3. Sovereign yields fall

U.S fed fund futures are now pricing in about a +40% chance that the Fed will raise rates by December, compared with just under +50% before release of yesterday's Fed's minutes.

The prospect of slower removal of stimulus is giving support to fixed income assets with Euro government bond and U.S Treasury yields heading lower.

The yield on U.S 10-year Treasuries fell -1 bps to +2.23%, while U.K 10-year Gilt yields dipped -2 bps to +1.087%. German 10-year Bund yields decreased -1 bps to +0.43%.

Note: The ECB may require more time and data before hinting at tapering its asset purchase program; therefore anyone who is hoping for more clarity in this morning's ECB's minutes (07:30 am EDT) could be disappointed.

4. Dollar takes it on the chin

Along with yesterday's Fed minutes, the ‘mighty' dollar has also come under domestic political pressure when President Trump decided to disband two business councils after a number of members quit in protest over his comments on white nationalists.

Sterling (£1.2887) is trying to halt a five-day decline outright and against the EUR (€0.9100) after retail sales data (see below) beat expectations.

The EUR (€1.1721) is a tad lower, -0.45% ahead of the ECB release of its July minutes. The market is looking for more clarity, however, smart money would suggest that the ECB would not unveil any strategy for tapering, or when it is likely to make an announcement on its plan. EUR bears believe the single unit could possible test the €1.15 region if the ECB shows any signs of caution.

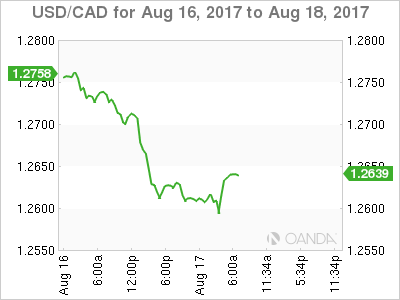

The loonie (C$1.2641) ended a brief losing streak outright yesterday as traders interpreted the latest minutes from the Fed's July meeting as ‘dovish.' The CAD is likely to see some volatility following the release of domestic manufacturing data this morning (08:30 am EDT) and any Nafta headlines.

5. U.K retail sales up modestly in July, Eurozone's trade surplus widens

U.K retail sales rose modestly last month, with sales at food stores and household goods stores offsetting weakness elsewhere.

Sales rose +0.3% m/m and matched the monthly increase in sales seen in June. Sales were +1.3% higher on the year.

The figures point to continued spending by U.K consumers, albeit subdued, t the start of Q3 despite weak wage growth and rising prices.

Note: The U.K consumer requires some help and reason why business investment and exports will need to pick up to sustain growth this year and next.

Other data showed the eurozone's trade surplus widened to a seasonally adjusted +€22.3B in June from €19B in May as exports fell less sharply than imports.

That suggests that while the EUR's recent appreciation may be making life more difficult for eurozone's exporters, the weakness of imports means that has not yet lowered economic growth.

Fed Comment Eyed In Light Of FOMC Minutes

- Dovish Fed minutes halt equity rally;

- USD and Treasury yields slip after minutes;

- ECB accounts could offer taper clues as core inflation rises.

US equity markets are poised to open a little lower on Thursday, tracking similar moves in Europe earlier in the day as traders absorb Wednesday's FOMC minutes and await more data from the world's largest economy.

The minutes highlighted the growing divide that is appearing within the Federal Reserve with respect to interest rates. There appears to be a united front when it comes to reducing the balance sheet – which now looks increasingly likely to start in September – but traders currently appear unconcerned by this. The debate on the third interest rate of the year has been happening for some time outside of the Fed, which is why markets have never priced it in as much as the other two. The fact that it's now happening within the Fed won't improve those odds.

The US dollar felt the brunt of it initially, with the yield on US Treasuries also coming under pressure as markets continue to price in a slower pace of tightening going forward. With markets being relatively unresponsive to reductions to the balance sheet, policy makers may see this as the preferred method of “tightening” for now until inflation returns to a more acceptable level and shows signs of rising towards target.

It will be interesting to hear the views of Neel Kashkari and Robert Kaplan later in the session, with both FOMC voters scheduled to appear. While Kashkari is arguably the most dovish on the committee, Kaplan is one of those that have shown a willingness to wait for more inflation data before raising rates again so his views will be particularly interest. There's also a number of pieces of data being released on Thursday, including jobless claims, Philly Fed manufacturing index, capacity utilization and industrial production.

Another central bank looking to carefully reduce accommodation is the ECB, which is due to release accounts from its July meeting today. Traders will be looking for clues regarding its bond buying, with the current program due to expire at the end of the year. The ECB is widely expected to announce another reduction and extension to the program, possibly at the September meeting, but along with its peers, it faces difficulties due to inflation running well below target.

Today's numbers did little to ease the burden, with the final figures for July showing prices rising only 1.3%, both on an overall and core basis. The core number represented a slight upward revision from the preliminary number but this failed to lift the euro, with traders seemingly viewing it as not being enough to guarantee another taper. Still, while overall inflation has fallen since the start of the year, core inflation has been on a gradual upward trajectory, which will be encouraging to policy makers and may give them the green light to taper.

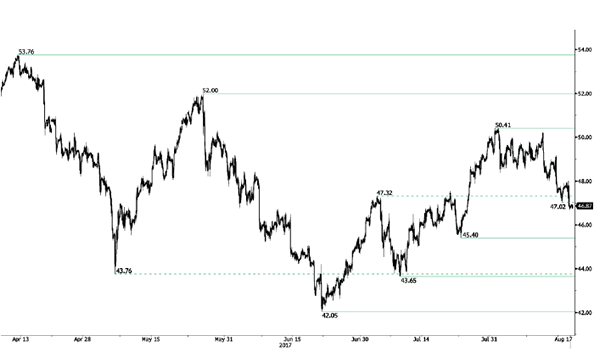

CRUDE OIL Wide-Open For Further Weakness

Crude Oil is trading lower. Hourly support is given at a distance at 45.40 (24/07/2017 low). Strong resistance can be found at 50.41 (31/07/2017). Expected to show short-term weakness.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

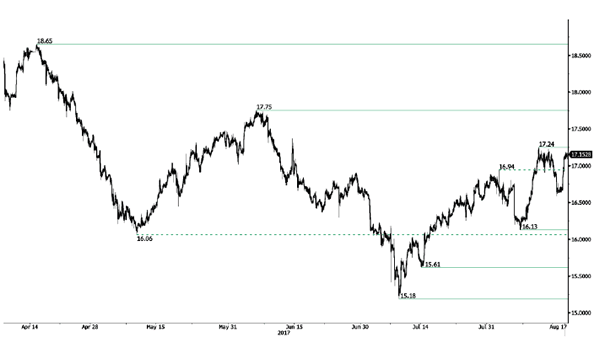

SILVER Bullish Pressures

Silver's bullish pressures are on. Hourly resistance lies at 17.24 (10/08/2017 high) while support can be found at 16.13 (07/08/2017 high). The commodity lies in a short-term uptrend channel. Expected to show continued current bullish momentum.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).