Sample Category Title

Soft Producer Price Inflation Extends in July

On broad-based weakness, the PPI for final demand unexpectedly fell 0.1 percent in July - extending the recent decline in the year-over-year rate. This only heightens anticipation for tomorrow's CPI update.

Alert: Chemical Spill

Marking the first monthly decline since August 2016, the PPI for final demand unexpectedly contracted in July. Price declines were broad-based with lower readings in energy and services, while wholesale food prices remained flat.

Services accounted for over 80 percent of the headline's decline, with about 60 percent attributable to a 5.8 percent drop in margins for chemicals and allied products wholesaling.

Outlook Remains Tame

Our favorite measure of core producer prices, ex-energy, food and trade services, was flat on the month, taking the year-overyear rate down modestly to 1.9 percent. It is important to remember the PPI data can be volatile on a monthly basis. That said, today's miss heightens the focus on the July CPI report. From our view, the health of economic fundamentals continues to point to a firming inflation environment in H2.

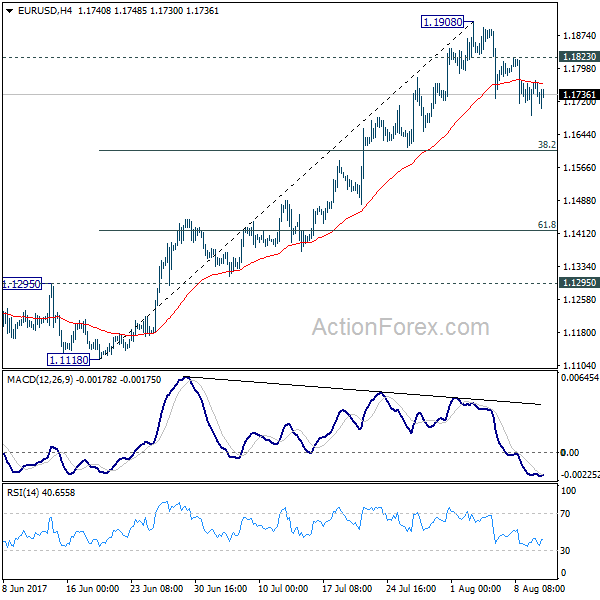

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1710; (P) 1.1736 (R1) 1.1784; More...

Intraday bias in EUR/USD remains on the downside as the pull back from 1.1908 is still in progress. At this point, we'd expect strong support from 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring rebound. But break of 1.1908 is needed to confirm up trend resumption. Otherwise, more consolidation would be seen in near term. Meanwhile, sustained break of 1.1606 would bring deeper pull back to 61.8% retracement at 1.1420.

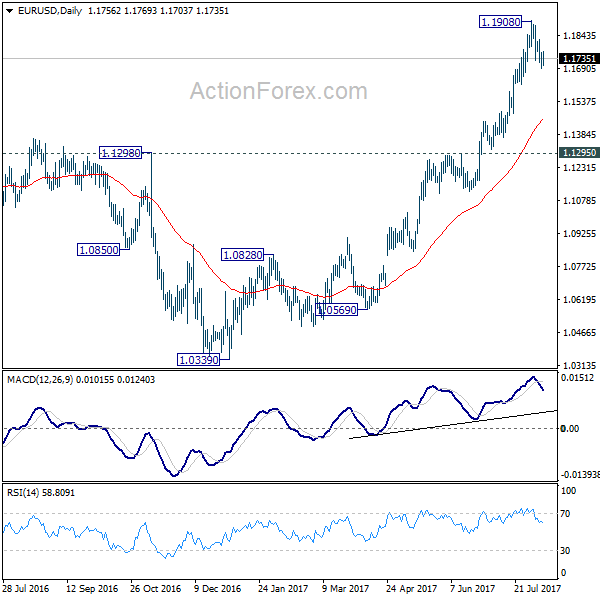

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained break of 55 month EMA (now at 1.1760) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

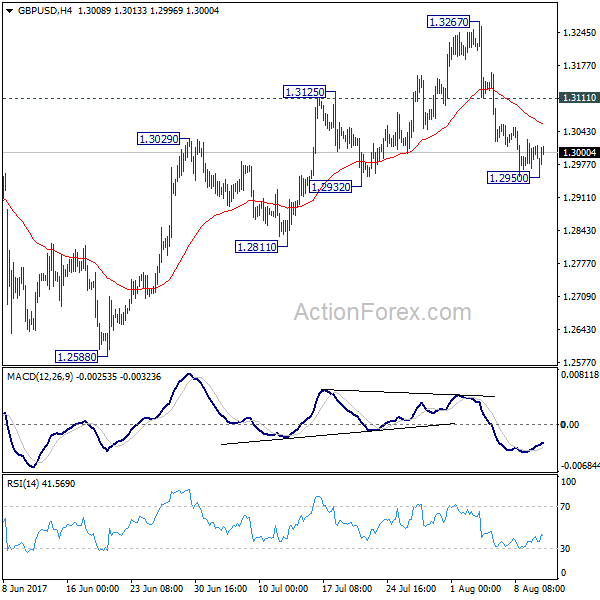

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2970; (P) 1.2998; (R1) 1.3030; More...

A temporary low is in place at 1.2950 with 4 hour MACD crossed above signal line and intraday bias is turned neutral first. Deeper decline will be expected as long as 1.3111 resistance holds. As noted before, price actions from 1.1946 are seen as a corrective pattern and could have completed at 1.3267. Break of 1.2932 will affirm this bearish case and target 1.2588 key near term support for confirmation. However, break of 1.3111 resistance will turn bias back to the upside for retesting 1.3267 high.

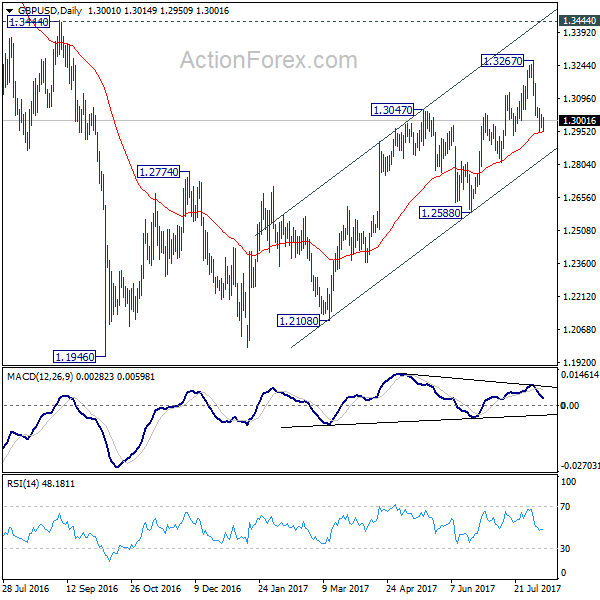

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

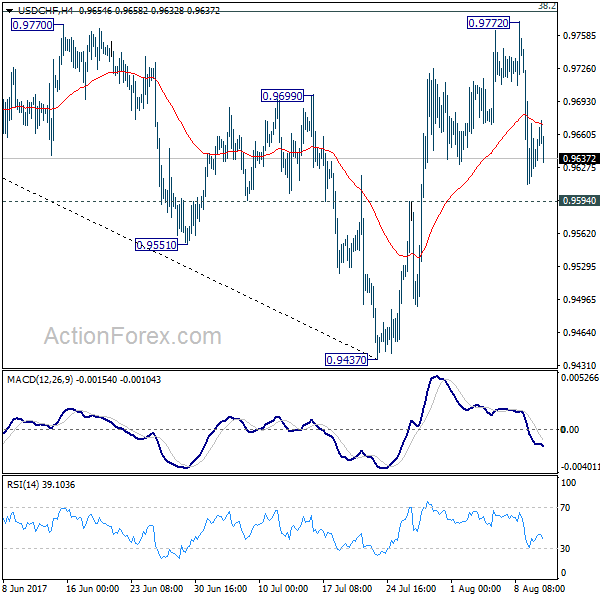

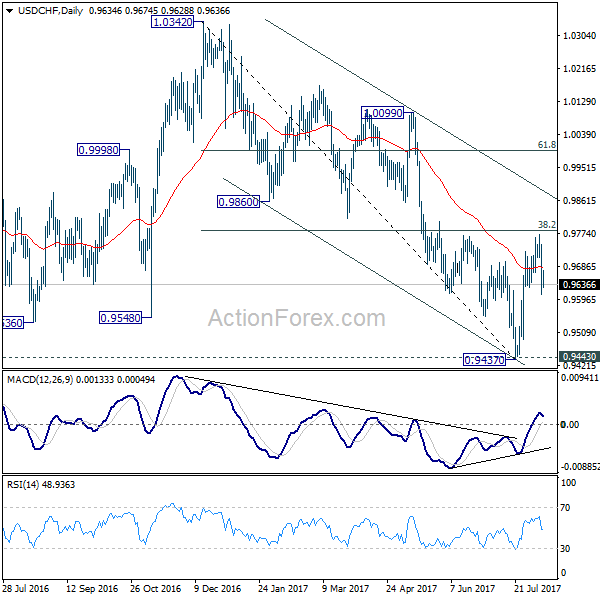

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9583; (P) 0.9663; (R1) 0.9716; More...

USD/CHF is staying in range of 0.9594/9772 and intraday bias remains neutral for the moment. Outlook is a bit mixed as the pair is bounded inside medium term falling channel. The pair was also limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783. Firm break of 0.9594 will dampen our bullish view and turn bias back to the downside for 0.9437. This could also extend the fall through 1.0342 through 0.9437/43 key support level. On the upside, above 0.9772 will revive the bullish case of reversal and turn bias back to the upside.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996.

Sterling Gains as British Iindustrial Production Rises, but Trade Balance Disappoints

While the BOE is hoping for exports and investments to rebalance the slowdown in consumption, as MPC member Michael Sanders expressed a month ago, data released on Thursday showed the goods trade deficit widening and reaching the highest level since September. On the other hand, industrial output showed improvement, but the improvement was seen as temporary. As a response, sterling picked up from a three-week low it touched prior the data.

According to the Office for National Statistics, British industrial output expanded unexpectedly in June as oil companies postponed seasonal maintenance. Industrial production recovered from a 0.1% contraction in May, expanding by 0.5% month-on-month and exceeding the forecast of 0.1% growth. Year-on-year the change was positive at 0.3%, while analysts expected the figure to rise from a negative 0.2% to a negative 0.1%. However, the improvement in the data was mainly due to a postponing in oilfield maintenance which is likely to take place later in the year.

Looking at the industrial sectors, the output in the manufacturing sector showed no growth in June as expected, following a decline of 0.1% in May (upwardly revised from 0.2%). A reason for this was attributed to a sharp fall in car production which amounted to 3.6% (steepest fall since December 2013) versus a drop of 2.3% in May. On a yearly basis manufacturing output growth doubled in June, in line with forecasts, from 0.3% to 0.6%.

Construction activities, which represent 6% of the economy, also contracted during the month, falling surprisingly by 0.1% compared to a 0.4% downturn in the previous month. Analysts anticipated instead a 1.5% improvement in construction output. The yearly equivalent increased from 0.5% to 0.9%, missing the forecast of 1.9%.

In the other important report of the day, trade data came in worse than expected. Goods trade deficit widened from £11.31 billion to £12.72 billion, whilst analysts expected the trade deficit to narrow to £11 billion. This was the biggest trade deficit since September. Regarding Non-EU trade balance, the deficit rose by almost £1 billion to £4.47 billion, above the £3 billion expected.

Including exports in services, the trade deficit rose to £4.6 billion, the highest record since September. This brought doubts on whether British exporters have really benefitted since the Brexit vote from the depreciated pound (18%).

In the forex markets, sterling reacted positively after the release of the data with sterling/dollar finding support from better- than- expected industrial output growth. Sterling/dollar jumped by 0.30% slightly above the 1.30 handle before it slipped back to 1.2992. Before the data, the pound was hovering around a three-week low of 1.2950 reached today.

Canadian Dollar Yawns as US Inflation Data Disappoints

The Canadian dollar is unchanged in Thursday trade. In the North American session, USD/CAD is trading at the 1.2701, up 0.03% on the day. On the release front, Canadian NHPI posted a gain of 0.2%, short of the forecast of 0.5%. In the US, inflation releases missed expectations, as PPI and Core PPI both posted declines of 0.1%. Unemployment claims rose to 244 thousand, higher than the estimate of 240 thousand.

Global markets remain uneasy, as tensions continue to ratchet higher between North Korea and the US. With the war of words escalating between the two countries, global markets are down, as investors have dumped shares in favor of safe-haven assets, such as gold. North Korea has vowed to retaliate over new sanctions imposed by Washington and has threatened to attack Guam, which is a major US military base. President Trump and North Korean President Kim Jong-un are on a possible collision course, which has caused alarm in South Korea and Japan, strong allies of the US.

In contrast to the uncertainty over the Fed's monetary plans, the Bank of Canada is leaning towards further tightening, possibly before the end of 2017. The bank raised interest rates in July and the odds of a rate increase in October are at 78 percent. In May, annualized GDP was up 4.6%, and the labor market continues to produce jobs. The increase in oil prices has revived the economy has also pushed the Canadian dollar higher. At the same time, similar to the situation in the US, inflation remains subdued, despite a stronger economy and an improving labor market. The lack of inflation could cause the Federal Reserve to abandon plans for another rate hike this year, and this could also lead to the BoC deciding to delay a rate hike until inflation moves higher.

The markets are looking for some clarity from the Federal Reserve, which is showing signs of backtracking on another rate hike in 2017. Earlier this year, the Fed strongly hinted that it planned to raise rates three times in this year, but so far only pressed the rate trigger twice, in March and June. After the June hike, Fed Chair Janet Yellen shrugged off concerns over low inflation, saying that it was due to "transient" factors. However, inflation has not improved and the Fed has changed its tune. Last week, St. Louis Federal Reserve President James Bullard said he opposed further Fed hikes, warning that another hike would actually delay inflation from hitting the Fed's target of 2%. The Fed appears uncertain about when to raise rates, and predictably, this hesitancy is making investors skeptical that the Fed will act. There is little chance that the Fed will make any moves at the September and November meetings, and the odds of a rate hike in December are currently at 42%. Analysts are hoping for some insight into the Fed's thinking when the Fed Reserve Dallas President Robert Kaplan and Minneapolis President Neel Kashkari deliver speeches on Friday.

Sterling Mixed as UK Data Conflicts

Market players are unsure whether to throw Sterling a lifeline, or to punish the currency further on Thursday, following the mixed bag of different economic releases from the United Kingdom.

Total industrial production exceeded expectations by rising 0.5% in June but manufacturing remained flat. The trade deficit unexpectedly widened, which weighed on sentiment.

With the UK economy ending the second quarter on a soft note, and with disappointing manufacturing data, speculation around the Bank of England raising UK interest rates this year is likely to weaken even further. Although it has been over one year since Britain voted to leave the European Union, it's remarkable how the deteriorating economic fundamentals are now starting to shine through, and continue to suggest that the nation is struggling to shake off the Brexit blues.

The British Pound is still struggling to nurse its wounds, following the sharp sell-off in Sterling last week, after the Bank of England (BoE) doves crashed the party, in August's monetary policy meeting. The economic data from the UK is not complimenting prior hints from the BoE, that UK interest rates could be raised, which is seen as a threat that may limit buying sentiment.

Sterling bears still seem to be in control of the Pound, following the inspiration they received after the downgrade in economic forecasts from the BoE. This coupled with the weakening optimism of a UK interest rate rise seems to indicate that the Pound could still drop lower. From a technical standpoint, the GBPUSD remains under pressure on the daily charts. A weekly close below 1.3000 should encourage a further depreciation towards 1.2850.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.62; (P) 109.98; (R1) 110.42; More...

Intraday bias in USD/JPY remains on the downside as the decline from 114.49 is still in progress. Further fall should be seen to 108.81 support. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. On the upside, break of 111.04 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

Dollar Mildly Lower after PPI Miss, Gold Heading to 1300, WTI Oil Breaches 50

There is no change in the general risk-aversion mode in the financial markets today. Investors continue to watch the development of US-North Korea tension with much caution. Yen remains the strongest one but Aussie and Canadian Dollar are catching up. Gold extends recent rally and breaches 1290, setting to take on 1300 handle. WTI crude oil was lifted by news that OPEC raised demand forecast and breaches 50 handle finally. Dollar trades lower in early US session, in particular against Japanese Yen after disappointing PPI. New Zealand Dollar remains the weakest one after dovish RBNZ comments.

US PPI missed expectations, jobless claims steady

US headline PPI dropped -0.1% mom in July, missing expectation of 0.1% mom. PPI annual rate slowed to 1.9% yoy, down from 2.0% yoy, missing expectation of 2.2% yoy. Core PPI dropped -0.1% mom, below expectation of 0.2%. Core PPI annual rate slowed to 1.8% yoy, down from 1.9% yoy and missed expectation of 2.1% yoy. While Fed is generally expected to start unwinding the balance sheet in September, question remains on whether it will hike again in December. Slowdown in inflation will more likely keep Fed on hold throughout the year.

Initial jobless claims rose 3k to 244k in the week ended August 5, slightly above expectation of 240k. Initial claims have now stayed at or below 250k level for 10 straight weeks already. Continuing claims dropped 16k to 1.95m in the week ended July 29. From Canada, new housing price index rose 0.2% mom in June.

Oil breaches 50 as OPEC raised demand forecasts

WTI crude oil is gathering some upside momentum and breaches 50 handle today. OPEC raised forecast of demand by 100k barrels a day for both 2017 and 2018. That is, demand will reach 1.37m barrels a day this year. OPEC also lowered estimated supply of non-OPEC countries by 50k barrels a day in 2017 and 90k barrels a day in 2018. That offset the impact of rise in production in July due to Libya, Nigeria and Saudi Arabia.

Reuters poll: Half of economists expect ECB tapering in September

According to a Reuters poll, 25 of 50 economists surveyed expected ECB to make an announcement in September on tapering the EUR 60b asset purchase program. 15 expected the announcement to happen in October. Most of the others expected it to start in early 2018. Economists consensus for growth in Eurozone is 2% this year. They expect inflation to hit 1.5% this year, and 1.4% in 2018, both well below target of 2%. 43 respondents answered an extra question and believed that rising Euro will not threaten Eurozone's recovery.

Sterling steady after mixed data

Sterling is staying in tight range against Euro after mixed economic data. Industrial production rose 0.5% mom, 0.3% yoy in June, above expectation of 0.1% mom, -0.1% yoy. Manufacturing rose 0.0% mom, 0.6% yoy, versus consensus of 0.0% mom, 0.7% yoy. Construction output dropped -0.1% mom in June. Trade deficit widened to GBP -12.7b in June. NIESR GDP estimate rose 0.2% in July. RICS house price balance dropped to 1 in July.

RBNZ left OCR unchanged at 1.75% as widely expected

As expected, the RBNZ left the OCR unchanged at 1.75%. Governor Wheeler reiterated that the monetary policy would remain accommodative for some time. The staff projection continued to forecast the first rate hike to come in 2H19. They also revised lower the short term inflation outlook and intensified the warning that a lower currency is needed for growth. NZD/USD jumped to a 3-day high of 0.7371 after the announcement, but gains were erased afterwards. At the time of writing NZD/USD has already resumed recent fall from 0.7553 and reaches as low as 0.7298. More in RBNZ Left Policy Stance Unchanged, Heightened Warning Over NZD Strength.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.62; (P) 109.98; (R1) 110.42; More...

Intraday bias in USD/JPY remains on the downside as the decline from 114.49 is still in progress. Further fall should be seen to 108.81 support. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. On the upside, break of 111.04 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 23:01 | GBP | RICS House Price Balance Jul | 1% | 9% | 7% | |

| 23:50 | JPY | Machine Orders M/M Jun | -1.90% | 3.70% | -3.60% | |

| 23:50 | JPY | Domestic CGPI Y/Y Jul | 2.60% | 2.30% | 2.10% | 2.20% |

| 01:00 | AUD | Consumer Inflation Expectation Aug | 4.20% | 4.40% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Jun | 0.00% | 0.20% | -0.10% | |

| 08:30 | GBP | Industrial Production M/M Jun | 0.50% | 0.10% | -0.10% | |

| 08:30 | GBP | Industrial Production Y/Y Jun | 0.30% | -0.10% | -0.20% | |

| 08:30 | GBP | Manufacturing Production M/M Jun | 0.00% | 0.00% | -0.20% | -0.10% |

| 08:30 | GBP | Manufacturing Production Y/Y Jun | 0.60% | 0.70% | 0.40% | 0.30% |

| 08:30 | GBP | Construction Output M/M Jun | -0.10% | 1.20% | -1.20% | -0.40% |

| 08:30 | GBP | Visible Trade Balance (GBP) Jun | -12.7B | -11.0B | -11.9B | -11.3B |

| 12:00 | GBP | NIESR GDP Estimate Jul | 0.20% | 0.30% | 0.30% | |

| 12:30 | CAD | New Housing Price Index M/M Jun | 0.20% | 0.50% | 0.70% | |

| 12:30 | USD | Initial Jobless Claims (AUG 05) | 244K | 240K | 240K | 241K |

| 12:30 | USD | PPI M/M Jul | -0.10% | 0.10% | 0.10% | |

| 12:30 | USD | PPI Y/Y Jul | 1.90% | 2.20% | 2.00% | |

| 12:30 | USD | PPI Core M/M Jul | -0.10% | 0.20% | 0.10% | |

| 12:30 | USD | PPI Core Y/Y Jul | 1.80% | 2.10% | 1.90% | |

| 14:30 | USD | Natural Gas Storage | 38B | 20B | ||

| 18:00 | USD | Monthly Budget Statement Jul | -55.5B | -90.2B |

Trade Idea: EUR/GBP – Hold short entered at 0.9080

EUR/GBP - 0.9025

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Sold at 0.9080, Target: 0.8980, Stop: 0.9080

Position : - Short at 0.9080

Target : - 0.8980

Stop : - 0.9080

New strategy :

Hold short entered at 0.9080, Target: 0.8980, Stop: 0.9080

Position : - Short at 0.9080

Target : - 0.8980

Stop : - 0.9080

Euro’s retreat after this week’s brief rise to 0.9088 has retained our view that consolidation below this level would be seen and mild downside bias remains for test of indicated support at 0.8995, break there would suggest top is possibly formed there, then weakness to 0.8965-70 would follow but below 0.8945-50 is needed to add credence to this view, bring retracement of recent upmove towards support at 0.8922.

In view of this, we are holding on to our short position entered at 0.9080. Above said resistance at 0.9088 would risk gain to 0.9145-50, however, still reckon sharp move beyond there should not be repeated and upside should be limited to 0.9175-80, price should falter below 0.9100, bring correction later.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.