Sample Category Title

US December CPI Preview: Concerns About Sticky Inflation to Linger

Summary

The December CPI report should indicate that the underlying trend in inflation is not re-accelerating, but it is unlikely to allay the FOMC's increased concerns that inflation has become stuck uncomfortably above its target. We look for the headline CPI to rise 0.4% on the back of a strong gain in energy prices, which would push the year-over-year rate up to a five-month high of 2.9%. Excluding food and energy, price growth looks to have been more moderate in December. After advancing 0.3% for four consecutive months, we look for the core index to increase 0.2%. If realized, that would leave the year-over-year rate at 3.3% for a fourth straight month. While we do not believe progress in the fight against inflation is going into reverse, we do see it stalling this year as earlier tailwinds to disinflation from supply chain improvements and lower commodity prices have faded and as fresh headwinds from trade policy are likely to emerge.

Headline Inflation Firming as Energy Prices Rebound

The lack of additional progress recently in the fight against inflation has tilted the Fed's focus back toward the price stability side of its mandate. The core Consumer Price Index has increased an average of 0.30% the past three months, or at an annualized rate of 3.7%. The Fed's preferred measure of inflation has fared a little better; over the past three months, the core PCE price index has increased an average of 0.21%, or an annualized rate of 2.5%. But that still leaves price growth running above the Fed's 2% target, with the more limited pace of improvement in 2024 evident in the year-over-year rate ticking up to 2.8% in November from 2.6% in June.

With the jobs market looking steadier since late last summer, we believe the FOMC will need to see progress on inflation resume as soon as this month in order to keep another rate cut in Q1 on the table. The December CPI report is likely to provide a half-hearted step to that end. We look for the core CPI to advance a more palatable 0.2% in November (0.22% unrounded). That said, with the increase in headline CPI looking likely to round up to 0.4% (0.36% unrounded), concerns about inflation becoming stuck above target are likely to linger. We estimate the 12-month change in CPI to rise to a five-month high of 2.9% in December.

Solid increases in energy and food prices in December look set to bolster the headline's gain. Gasoline prices fell less than usual this December and point to energy goods rising 3.7% over the month on a seasonally adjusted basis. Energy services inflation also looks likely to have firmed, with a further pickup in store in early 2025 after the recent spike in natural gas prices.

We suspect the late timing of Thanksgiving and the typical discounting that goes on at grocers around the holiday contributed to November's pop in prices for food at home. However, payback in December is likely to be minimal, with promotional activity at supermarkets down relative to last December and food-related commodity prices moving up since the fall.

Softer Core Unlikely to Be a Game-changer for Sticky Outlook

While the December CPI report is likely to show a more challenging price environment for necessities such as food and energy, a more tepid gain in the core index should suggest that the underlying trend in inflation is at least not re-accelerating. We look for the easing in monthly core CPI inflation to 0.2% from 0.3% in November to keep the year-over-year rate at 3.3% and within the narrow range of 3.2%-3.3% for a seventh straight month.

The moderation in the monthly pace of core CPI increases in December is likely to be primarily driven by core goods. New and used vehicles provided a sizable lift to core goods prices the past few months, fueled by replacement demand following Hurricanes Helene and Milton and lower financing costs. Yet with the CPI for used autos vehicles largely realigned with wholesale auction prices, we look for more modest gains in vehicle prices in December (Figure 3). Other core goods prices are likely to be unchanged and continue to firm on a year-over-year basis as the deflationary impulse from un-kinked supply chains has faded.

We expect core services to advance 0.3% again in December, but for the drivers to look a little different from November. While the deceleration in primary shelter in November was a welcome sign that housing disinflation has further room to run, last month's move likely overstated the pace at which the trend is slowing. As a result, we look for the monthly change in primary shelter to edge back up to 0.3% in December from 0.2% in November (Figure 4). The pickup should be offset, however, by a partial reversal of last month's 3.2% jump in hotel prices. Among all non-housing core services, we look for the monthly change in inflation to ease from 0.3% in November to 0.2% in December, which would push the year-over-year change in the CPI "super core" down to a 12-month low of 4.2%.

Our estimates point to the core PCE deflator advancing 0.2% in December, which would leave the year-over-year rate, at 2.8%, above its summer level. Yet Fed Chair Powell and other officials have been emphasizing that, excluding categories where prices are imputed rather than directly observed, progress on inflation has not gone into reverse (Figure 5). We estimate that the market-based core PCE, the Fed's inflation measure du jour, rose 0.2% in December to remain closer than the traditional core to the FOMC's target at 2.5% year-over-year.

While Fed officials have not completely lost faith in further disinflation ahead, the slow progress over the past year has underscored that the last leg of inflation's journey back to target will be the most arduous. The path ahead looks even more challenging now with economic policies under the incoming administration likely to be inflationary. While downward forces remain in place from stronger productivity growth, the cooler labor market and more price-conscious consumers, business remain more willing to raise prices than before the pandemic as consumers have not fully gone into hiding and increases in tariffs are likely to leave them little choice (Figure 6). As a result, we look for the pace of inflation to be little changed this year, leaving it stuck above the FOMC's target for a fifth consecutive year (Table).

Weekly Focus – Bracing for Trump 2.0

A new year is upon us and for sure it shapes up to be another interesting year. A key question from the start is how much of his policies US President-elect Donald Trump will actually pursue on issues such as tariffs, immigration, fiscal policy and Ukraine peace talks? We are yet to find out how much is rhetoric and what he will actually go for. And there is also a question of what he will be able to implement. On trade and foreign policy issues he has a lot of power, though. This week we introduced a revamp of our Geopolitical Radar, 9 January, where we take stock of geopolitical developments and outline scenarios. As we wrote in Nordic Outlook in December 2024, despite the uncertainties our baseline is still that it will be a year of normalisation in growth and inflation - and a further removal of tightness in monetary policy in most countries. Our baseline is a soft landing in the US, moderate growth improvement in the eurozone and continued muddling through in China. Often, we tend to overestimate the impact of politics on growth compared to other key drivers of the economies, such as the development in labour markets.

Speaking of labour markets, we see signs of cooling in the euro area after a long period of resilience: Consumers' unemployment expectations have shot higher lately and now point to rising unemployment and the PMI employment index has fallen below 50 indicating a decline in employment. At the same time, though, unemployment data this week showed another low reading at 6.3% so we have yet to see the cooling in the hard data. Focus in the euro area is predominantly on growth risks with clear structural concerns over too much regulation, high energy costs and rising competition from China coming on top of the weak cyclical indicators. We look for ECB to cut rates all the way to 1.5% by late summer (from 3% currently), which is around 50bp more than what markets price. Inflation data this week for December was in line with expectations showing an unchanged reading of 2.7% y/y for core inflation with a continued disinflationary trend in underlying momentum.

In the US, focus has instead shifted back on inflation risks, as the labour market has stopped cooling and consumer demand continues to look robust. This week JOLTS data showed an increase in job openings and a further decline in initial jobless claims (non-farm payrolls was released after deadline). Bond yields have shot higher lately due to the change in focus back on inflation as well as higher term premia related to debt concerns. We believe the optimism about the US economy is a bit overdone as we still look for moderation, not least due to much slower growth in the labour force. We believe the Fed has room to continue to cut rates on a quarterly basis in 2025 vs. market pricing of less than two cuts.

China has shown some rays of light in the housing market lately and policy makers have sharply increased focus on lifting home sales and private consumption (see China Headlines, 8 January). However, a trade war with the US is looming later this year and China is likely to face another bumpy year when it comes to growth.

Focus in the coming week will be on US CPI where consensus looks for 0.2% m/m in core CPI. An upward surprise could be challenging for bonds that are under pressure at the moment. Other market movers will be US retail sales, UK CPI, Chinese data for GDP, housing and retail sales.

Sunset Market Commentary

Markets

The week ended with a bang. December US payrolls beat consensus by a wide margin (256k vs 165k) while October and November data barely faced a revision (-8k combined). Big contributors were health care (+46k), leisure & hospitality (+43k) and government (+33k). Today’s numbers strongly add to the feeling that the Fed’s momentum to lower policy rates is rapidly fading. US money markets barely take into account one additional 25 bps rate cut by the end of 2025. The best payrolls report since March was accompanied by a good household survey (+478k), resulting in an unexpected tick lower in the unemployment rate (4.1% from 4.2%). Average hourly earnings increased by 0.3% M/M (& 3.9% Y/Y), in line with consensus. Markets reacted strongly to the US labour market figures. US Treasuries extend their sell-off with US yields rising by 5.9 bps (30-yr) to 8.5 bps (5-yr). The US 30-yr yield temporarily breached 5%. Together with a brief spell in the second half of October 2022, that’s the only the second time since July 2007. The US 10-yr yield took out the 2024 top at 4.73%, paving the way to test the 2023 top at the similar 5% mark. Imagine next week’s US December CPI numbers (release on Wednesday) beating consensus expectations… Markets are currently looking at 0.3% M/M rise for headline inflation (2.9% Y/Y from 2.7%) and 0.2% M/M pace for underlying core inflation (steady at 3.3% Y/Y). Global bonds follow US Treasuries lower with German yields adding 2.6 bps (30-yr) to 4.3 bps (5-yr) and UK yields rising another 3.1 bps to 4.9 bps. The dollar strengthened with EUR/USD testing the sell-off low at 1.0226. The trade-weighted dollar touched 110 for the first time since November 2022. Cable (GBP/USD) touched 1.22 for the first time since November 2023. USD/JPY set a minor new short term high around 158.85, erasing earlier JPY-gains following rumours that the BoJ could raise its inflation outlook at the policy meeting later this month, bringing it closer to a next rate hike. The BoJ currently sees underlying inflation rising by 2% this fiscal year, 1.9% next year, and 2.1% the year after. Upgrades would bring the forecasts consistently at or above the 2% inflation target. US stock markets took the higher for longer perspective badly with the S&P and Nasdaq opening respectively 0.75% and 1% lower. Brent crude prices hit $80/b (from $77/b) after Reuters reported that the US would impose sanctions on Russian’s oil fleet.

News & Views

Norwegian inflation in December came in on the softer side of expectations. Headline prices fell by 0.1% m/m to be at 2.2% on a yearly basis. That’s an unexpected deceleration from the 2.4% in November. A core gauge (excluding taxes and energy) dropped a monthly 0.1% too, allowing the y/y reading to wipe out November’s uptick to 3% back to 2.7% again. The inflation numbers strengthen the central bank’s case to finally start its easing cycle after having kept rates steady at 4.5% since December 2023. It clearly hinted at a pivot to come in early 2025. While the central bank meets later this month, we think it’ll wait until the March meeting when it has updated forecasts at its disposal to substantiate the decision. The Norwegian krone barely budged on the eco news, hovering around EUR/NOK 11.76. The currency has been trading relatively weak in a broader perspective though for the last two years. It was (and still is) one of the major reasons the Norges Bank resisted rate cuts for so long.

Canadian payrolls growth in December picked up sharply from the 50.5k in November. Employment grew by 90.9k, the quickest pace since January 2023, well beyond the 25k consensus estimate. Full-time jobs increased by 57.5k, part-times by 33.5k. It made the employment rate rise for the first time since January 2023 by 0.2 ppt to 60.8%. The unemployment rate ticked lower to 6.7% as did average hourly wages, from 4.1% to 3.8% y/y. The overall stronger-than-expected labour market report helps the Canadian Loonie fend off outright payroll-driven USD strength. USD/CAD trades little changed around 1.441. The Bank of Canada since its last meeting of 2024 is eying more gradual rate cuts after slashing them by 50 bps back to back. Money markets pared easing bets in the wake of the release but still assume two 25 bps reductions throughout 2025 (to 2.75%).

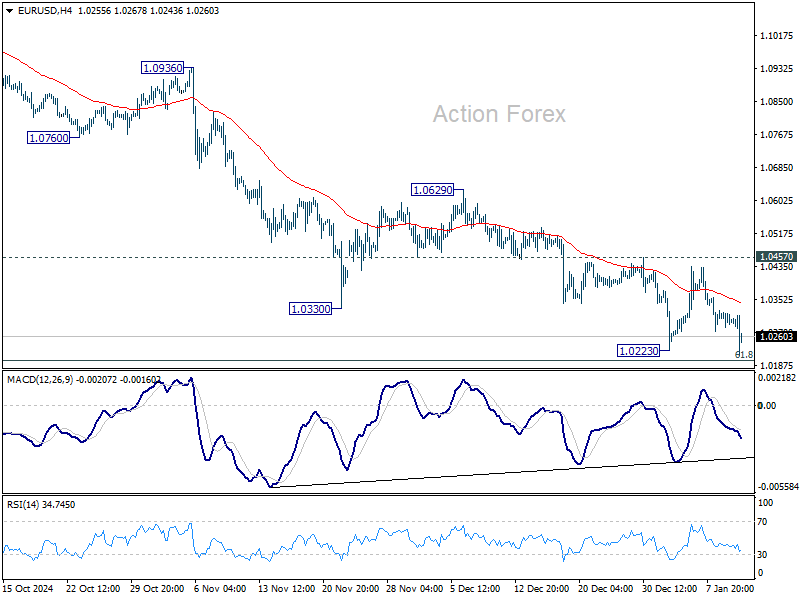

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0281; (P) 1.0302; (R1) 1.0321; More...

EUR/USD recovered after brief breach of 1.0223 support and intraday bias remains neutral. With 1.0457 resistance intact, outlook stay bearish. On the downside, firm break of 1.0223 will resume the fall from 1.1213. However, sustained break of 1.0457 will confirm short term bottoming, and turn bias to the upside for 55 D EMA (now at 1.0533).

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2240; (P) 1.2306; (R1) 1.2375; More...

GBP/USD's decline continues today and intraday bias stays on the downside. Sustained trading below 1.2256 fibonacci level will carry larger bearish implications. Next target is 61.8% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863. On the upside, break of 1.2532 minor resistance will turn intraday bias neutral first. Further break of 1.2486 support turned resistance should confirm short term bottoming.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Strong support is still expected from 38.2% retracement of 1.0351 to 1.3433 at 1.2256 to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

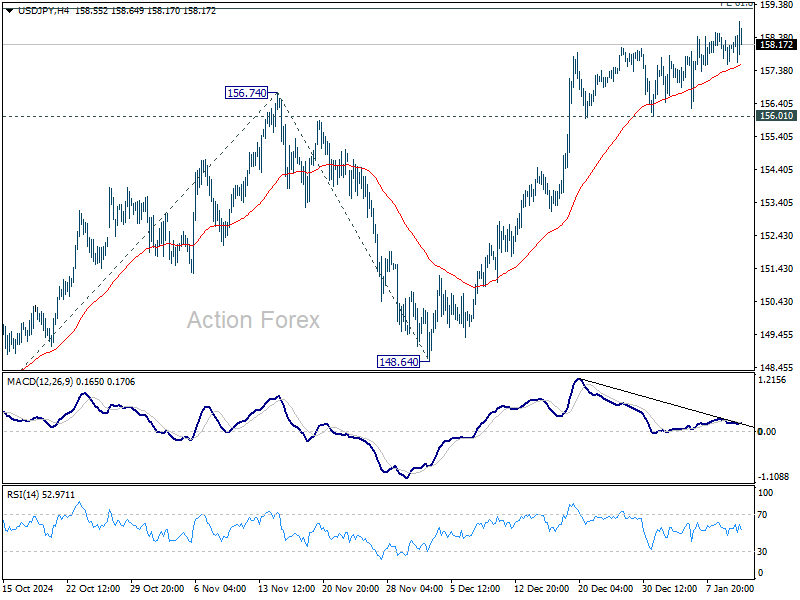

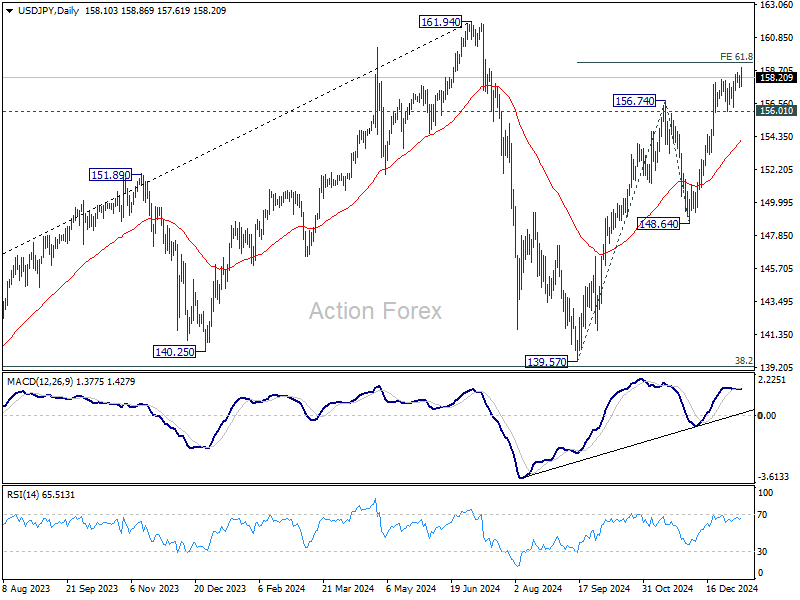

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.69; (P) 158.04; (R1) 158.51; More...

USD/JPY's rally continues today and intraday bias stays on the upside for 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will extend the rise from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 156.01 support will indicate short term topping. Intraday bias will then be back on the downside for 55 D EMA (now at 154.13) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Canada’s Jobs Market Surged in December

The Canadian labour market ended 2024 on a very strong note, adding 90.9k positions in December, primarily in full-time positions (+57.5k).

The healthy job gain pushed the unemployment rate down 0.1 percentage point to 6.7%. The labour force participation rate was unchanged at 65.1%.

Employment by sector showed widespread gains, led by educational services (+17k), transportation and warehousing (+17k), finance, insurance, real estate, rental and leasing (+16k), and health care and social assistance (+16k).

Lastly, total hours worked jumped a massive 0.5% month-on-month, pointing to solid economic growth on the month. Meanwhile wages were up a more palatable 3.8% year-on-year (from 4.1% in November).

Key Implications

This was as positive a labour market report as we could expect. Despite all the negative talk on Canada's economy, the country keeps adding jobs. Importantly, these jobs were largely full-time, and in cyclically sensitive industries. The growth in hours worked was also encouraging, as this will help support the continued resurgence in consumer spending. Wage growth has also been moving towards the level that is consistent with inflation stabilizing around the Bank of Canada's 2% target.

Today's report puts a January rate cut into question. Despite fears related to U.S. action against Canada, the BoC doesn't make political calls on the outlook. However, post inauguration on January 20th, they may have sufficient information on whether lower interest rates are necessary to shore up the economy. This will need to be balanced against any reaction on the Canadian dollar, that might also be providing a buffer on trade at that time.

US Payrolls Surge in December and Unemployment Rate Ticks Down to 4.1%

The U.S. economy added 256k jobs in December, well above the consensus forecast calling for a gain of 165k. Payroll figures for October were revised up by 7k (to 43k), while November was revised lower by 15k (to 212k), resulting in a total net revision of -8k over the two prior months.

- For the year, job growth totaled 2.2 million, down from 2023's 3.0 million, but a still solid year of hiring.

Private payrolls rose 223k – up from November's 182k – with the largest gains seen in health care & social assistance (+69.5k), leisure & hospitality (+43k), and professional & business services (+28k). The public sector added 33k new positions last month.

In the household survey, civilian employment surged by 478k – more than reversing November's sharp pullback – while the labor force grew by a smaller 243k, pushing the unemployment rate 0.1 percentage points lower to 4.1%. The labor force participation rate held steady at 62.5%.

- The household survey figures for December also included the usual updated seasonal adjustment factors. However, there was no discernable impact on monthly unemployment rate readings for 2024.

Average hourly earnings (AHE) rose 0.3% month-on-month (m/m), a tick lower than November's gain. On a twelve-month basis, AHE were up 3.9% (also a tick lower than November). Aggregate weekly hours rose 0.2% m/m, up from November's downwardly revised reading of 0.1% m/m (previously 0.4% m/m).

Key Implications

Non-farm payrolls end 2024 on a solid footing, coming in well above nearly all surveyed economist forecasts in Bloomberg. Smoothing through the recent volatility, job growth averaged 170k per-month in the fourth quarter, down from Q4-2023's monthly average of 212k. Meanwhile, the unemployment rose by 0.3 percentage points last year, but remains low at 4.1%.

There were virtually no signs underlying weakness in the labor market in this morning's employment report. And with progress on the inflation front showing signs of stalling in recent months, Fed officials have all the evidence they need to slow the pace of rate cuts. We still a view a March cut as likely (Fed futures are currently pricing a less than 25% probability for a March cut), though the next few months of data will be critical in shaping the final decision.

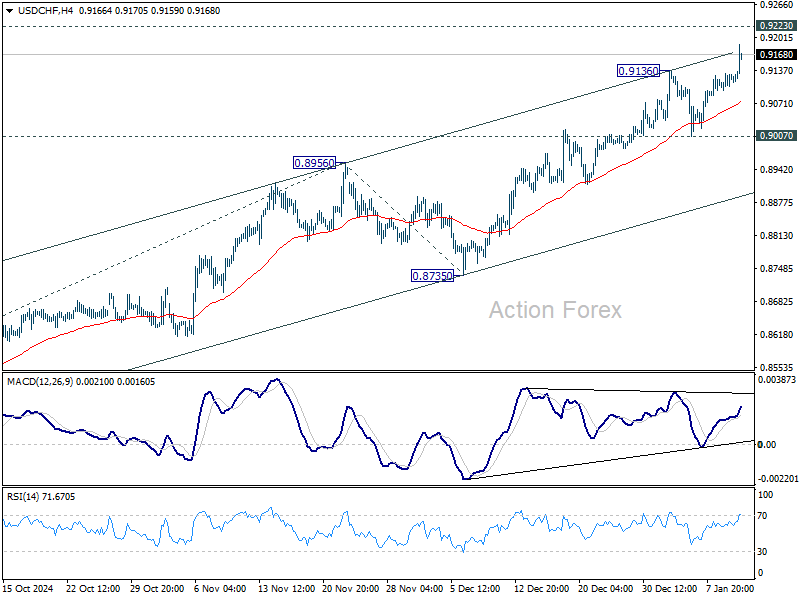

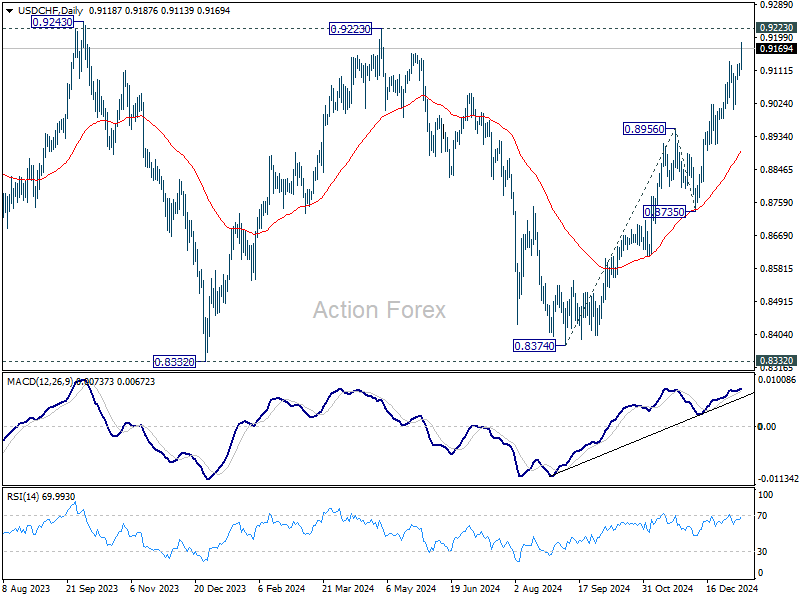

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9101; (P) 0.9117; (R1) 0.9137; More…

USD/CHF's rally resumed by breaking through 0.9136 and intraday bias back on the upside. Current rise from 0.8374 will now target 0.9223 key resistance next. Decisive break there will carry larger bullish implications. For now, near term outlook will stay bullish as long as 0.9007 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

Strong NFP Boosts Dollar Amid Rising Bets on Extended Fed Pause

Dollar is charging higher in early US session, buoyed by a strong set of employment data. Non-farm payrolls surged well above expectations in December, while the unemployment rate unexpectedly ticked lower. This set of data solidified the market's belief that Fed will pause rate cuts at its upcoming meeting later this moth, with the probability now exceeding 97%. Adding to the hawkish sentiment, odds for a rate hold in March have also risen sharply, now exceeding 70%, signaling that Fed may extend its pause in easing longer than previously anticipated.

The robust jobs data weighed heavily on equity and bond markets. DOW futures plunged more than -300 points in early trading, while NASDAQ futures shed over -1%. Treasury yields have also surged, with the 10-year yield setting its sights on the critical 4.8% level. Both these movements are unequivocally supportive for Dollar.

While Dollar's momentum appears solid, market participants might turn cautious ahead of the weekend. With President-elect Donald Trump's inauguration just days away, traders are wary of surprises or new trade policy developments that could inject volatility into the markets. Profit-taking may emerge before the weekly close.

Overall, despite Dollar's strong showing, Loonie remains the week's best performer, with Canada’s robust labor market report is flooring its selloff. Meanwhile, Euro continues to hold its ground as the third-strongest currency, benefitting from sterling's continued weakness.

At the bottom of the leaderboard, the Pound is staying as the weakest amid concerns over the UK government's fiscal challenges. At the same time, Aussie and Kiwi are the next worst. With equity markets under strain, further declines in risk-sensitive assets could deepen the antipodeans' losses. Swiss Franc and Japanese Yen are holding the middle positions.

US NFP grows 256k, unemployment rate ticks down to 4.1%

US labor market showcased its resilience in December, with non-farm payrolls surging by 256k, significantly outpacing expectations of 150k. This impressive figure also surpassed the average monthly gain of 186k for 2024.

Unemployment rate edged down to 4.1%, beating forecasts of remaining steady at 4.2%. This marks the seventh consecutive month where the unemployment rate has hovered within a tight range of 4.1% to 4.2%, reflecting a steady labor market. Meanwhile, the labor force participation rate held steady at 62.5%, a level consistent with its range since late 2023.

Wage growth showed a measured pace, with average hourly earnings rising by 0.3% mom, in line with market expectations. On a yearly basis, wage growth softened slightly to 3.9% from 4.0% yoy previously.

Canada's employment rises 91k in Dec, unemployment rate down to 6.7%

Canada's labor market closed 2024 on a strong note, with employment soaring by 91k in December, far exceeding expectations of 24.9k. Full-time positions accounted for a significant portion of the gains, with 56k new roles added.

Unemployment rate fell to 6.7%, defying expectations of an increase to 6.9%, and marked an improvement from the previous month's 6.8%. Employment rate also increased by 0.2 percentage points to 60.8%, marking the first uptick since January 2023.

Total hours worked rose 0.5% mom and were 2.1% higher than a year earlier. Meanwhile, average hourly wages grew 3.8% yoy, a deceleration from November’s 4.1% yoy.

Japan’s household spending falls for fourth month, minister flags critical economic transition

Japan’s household spending declined for the fourth consecutive month in November, falling -0.4% yoy. While this was an improvement from October's -1.3% drop and surpassed expectations of -0.8%, it still reflects ongoing consumer caution.

The decline was driven by significant cuts in expenditures on home appliances and food, highlighting weak domestic demand.

Spending on furniture and electric appliances plummeted by -13.8%, marking the third straight month of decline, while clothing and footwear saw a similar drop -of 13.7%, down for the second consecutive month. Food purchases also contracted slightly, falling by-0.6%.

Separately, Economy Minister Ryosei Akazawa acknowledged the challenges, stating that Japan's economy is at a "critical stage" in shifting public sentiment away from deflation and toward sustainable growth driven by higher wages and investment.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9101; (P) 0.9117; (R1) 0.9137; More…

USD/CHF's rally resumed by breaking through 0.9136 and intraday bias back on the upside. Current rise from 0.8374 will now target 0.9223 key resistance next. Decisive break there will carry larger bullish implications. For now, near term outlook will stay bullish as long as 0.9007 support holds, in case of retreat.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.