Sample Category Title

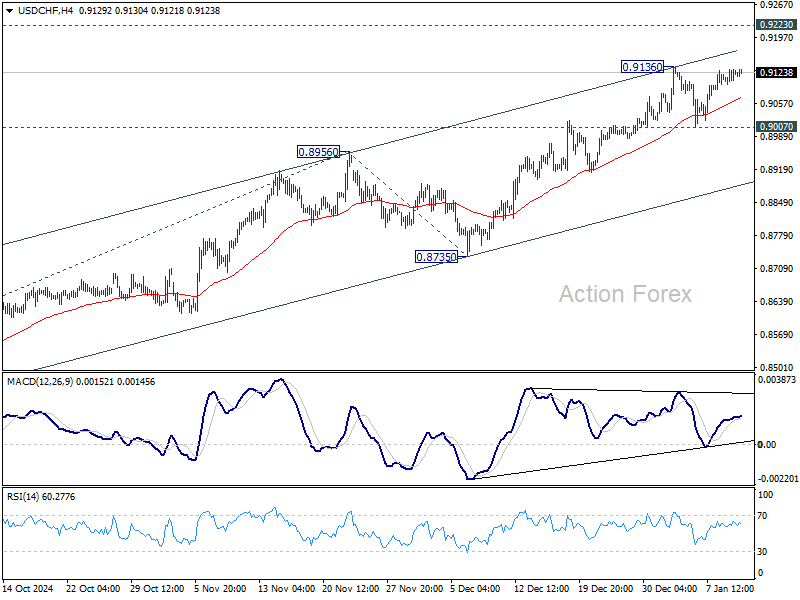

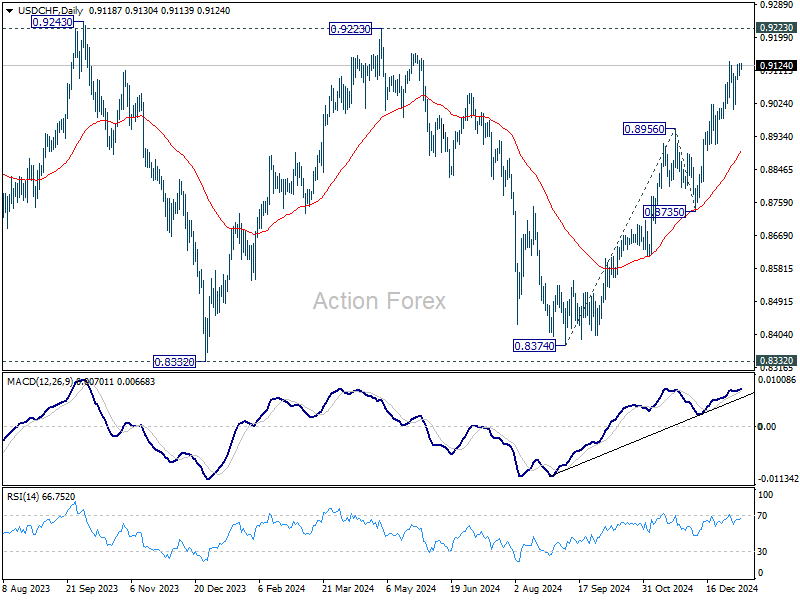

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9101; (P) 0.9117; (R1) 0.9137; More…

USD/CHF is still bounded in range below 0.9136 and intraday bias remains neutral. With 0.9007 support intact, further rally is expected. On the upside, break of 0.9136 will resume the rally from 0.8374 to 0.9223 key resistance next. However, firm break of 0.8956 will turn bias back to the downside for 55 D EMA (now at 0.8896).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

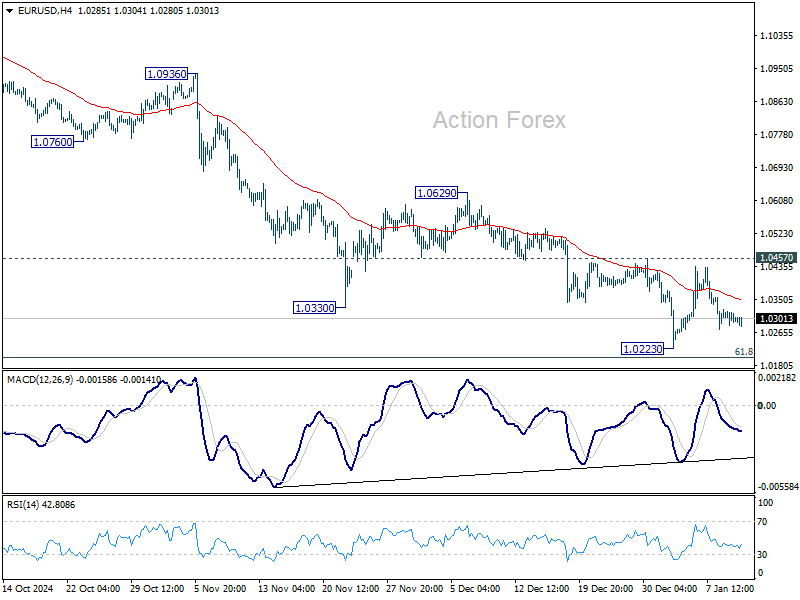

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0281; (P) 1.0302; (R1) 1.0321; More...

EUR/USD is still bounded in range of 1.0223/0457 and intraday bias stays neutral for the moment. With 1.0457 resistance intact, outlook stay bearish. On the downside, firm break of 1.0223 will resume the fall from 1.1213. However, sustained break of 1.0457 will confirm short term bottoming, and turn bias to the upside for 55 D EMA (now at 1.0533).

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

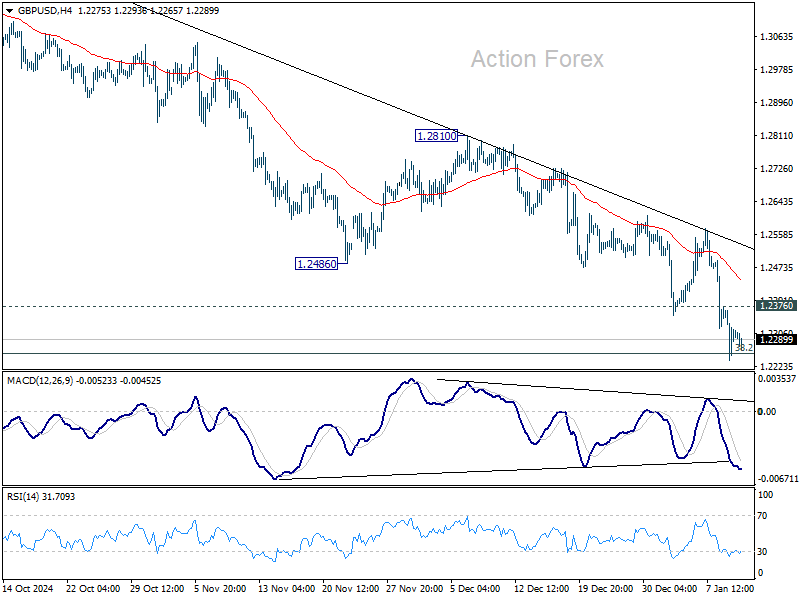

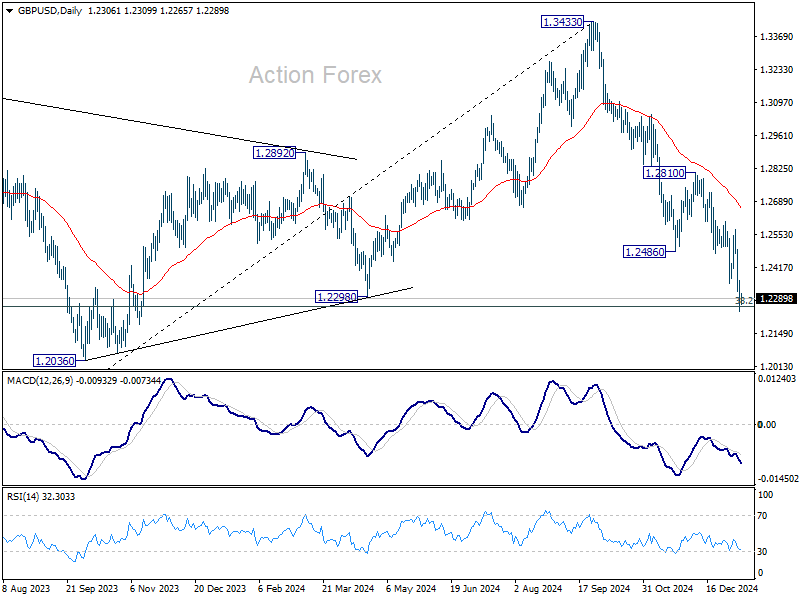

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2240; (P) 1.2306; (R1) 1.2375; More...

There is no clear sign of bottoming yet in GBP/USD and intraday bias remains on the downside. Sustained trading below 1.2256 fibonacci level will carry larger bearish implications. On the upside, break of 1.2376 will turn intraday bias neutral first. Further break of 1.2486 support turned resistance should confirm short term bottoming.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Strong support is still expected from 38.2% retracement of 1.0351 to 1.3433 at 1.2256 to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

NFP Set to Boost Dollar, But Trump Inauguration Risks May Limit Sustained Gains

Dollar holds onto its leadership position as markets await the US non-farm payroll report. Investors expect the data to reinforce Fed’s decision to pause rate cuts this month, particularly if the report confirms continued labor market strength. In such a scenario, rising US Treasury yields could further bolster the greenback.

However, any post-NFP rally might be short-lived, given the looming inauguration of President-elect Donald Trump on January 20. Trade policy rumors have already spurred market volatility, with conflicting reports about sector-specific tariffs and the possible use of emergency powers. Traders may be quick to take profits after NFP-driven moves, wary of sudden developments in Washington.

For the week, Canadian Dollar remains the top performer, consolidating gains against the second-ranked Dollar. Euro occupies third place, while Sterling languishes at the bottom, pressured by concerns over UK fiscal stability. Swiss Franc and Yen are next weakest, as Euro and Australian Dollar sit at middle positions.

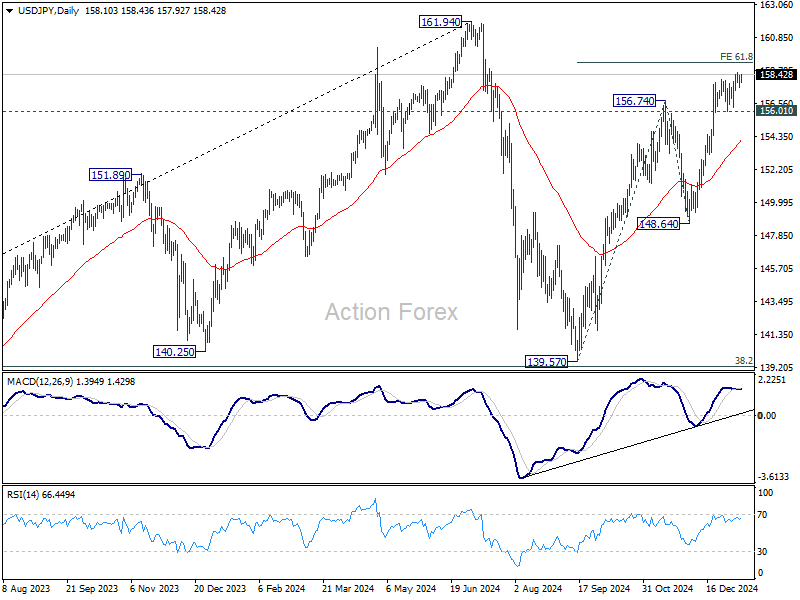

Technically, USD/JPY has seen its rally slow just shy of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Caution is rising as the pair approaches 160 psychological level, where intervention risk from Japan looms. Nonetheless, further upside is favored as long as 156.01 support holds, pointing to a test of the 161.94 high once 159.25 is cleared. That zone represents significant resistance and could cap any near-term gains.

NFP to anchor Fed pause, 10-year yield eyes higher level

US non-farm payroll report is taking center stage today as markets look for confirmation of Fed’s anticipated decision to pause rate cuts this month. Recent comments from multiple Fed officials have highlighted a cautious approach to further monetary easing, with a consensus forming that the central bank is nearing a pause in its rate-cutting cycle.

Fed fund futures currently price 93% likelihood of a hold at the meeting, and an in-line or stronger-than-expected jobs report could push this probability closer to certainty.

The broader debate now shifts to two key questions: how long the Fed’s pause might last and how much more easing, if any, will occur this year. Current market pricing indicates a 60% chance of another hold in March, followed by a 53% probability of a rate cut in May. For the rest of 2025, markets see over an 85% chance that rates will remain steady at 4.00%-4.25%.

Following today’s data, the immediate focus is whether the odds of a March hold increase, reflecting an extended pause.

Regarding expectations on the data, for December, headline job growth is forecasted to slow to 150k, with the unemployment rate expected to hold steady at 4.2%. Average hourly earnings are anticipated to rise by 0.3% month-over-month.

While some signals, such as the ISM Manufacturing PMI Employment component falling to 45.3 and ADP private employment growth decelerating to 122k, point to a cooling labor market, others remain robust. ISM Services PMI Employment component held steady at 51.4, and the 4-week moving average of initial jobless claims fell to a historically strong 213k, suggesting resilience and leaving room for an upside surprise in today’s report.

In terms of market reactions, a major focus is on treasury yields. Technically, 10-year yield breached 61.8% projection of 3.603 to 4.505 from 4.126 at 4.683 this week, as rally from 3.603 resumed.

Strong NFP number could push TNX higher, and sustained trading above 4.683 should pave the way towards 100% projection at 5.028, which is close to 4.997 high, and 5% psychological level. Any upside acceleration could realize this target at around the end of Q1.

In any case, outlook in TNX will stay bullish as long as 4.517 support holds, in case of retreat.

Japan’s household spending falls for fourth month, minister flags critical economic transition

Japan’s household spending declined for the fourth consecutive month in November, falling -0.4% yoy. While this was an improvement from October's -1.3% drop and surpassed expectations of -0.8%, it still reflects ongoing consumer caution.

The decline was driven by significant cuts in expenditures on home appliances and food, highlighting weak domestic demand.

Spending on furniture and electric appliances plummeted by -13.8%, marking the third straight month of decline, while clothing and footwear saw a similar drop -of 13.7%, down for the second consecutive month. Food purchases also contracted slightly, falling by-0.6%.

Separately, Economy Minister Ryosei Akazawa acknowledged the challenges, stating that Japan's economy is at a "critical stage" in shifting public sentiment away from deflation and toward sustainable growth driven by higher wages and investment.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2240; (P) 1.2306; (R1) 1.2375; More...

There is no clear sign of bottoming yet in GBP/USD and intraday bias remains on the downside. Sustained trading below 1.2256 fibonacci level will carry larger bearish implications. On the upside, break of 1.2376 will turn intraday bias neutral first. Further break of 1.2486 support turned resistance should confirm short term bottoming.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Strong support is still expected from 38.2% retracement of 1.0351 to 1.3433 at 1.2256 to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

Asian-Pacific Dealings Lacking Much Other News Revolve Mostly Around PBOC

Markets

The partial absence of US investors due to a national day of mourning for ex-president Carter and the empty economic calendar kept markets squarely focused on the UK. Gilt yields gapped another 12 bps higher at the open before paring most of those gains into the close. The earlier surge nevertheless means multi-year or even -decade highs. Breeden from the Bank of England was the first to comment but wouldn’t go much further than saying they are monitoring what is happening and that the moves reflect a lot of “global factors”. The genie appears to be out of the bottle for sterling. EUR/GBP tested the 0.84 big figure. The pound has the easing of the gilt sell-off to thank for avoiding the technical break (EUR/GBP 0.8368). Cable’s picture looks much more dire. The 2024 GBP/USD low of 1.23 was cracking and succumbs in Asian trading this morning. GBP/USD 1.228 trades at the weakest level since November 2023 and marches closer to an important support area around 1.225 (38.2% retracement on the 2022-2024 ascent). Rates in Europe added a few basis points in a bear flattening move (up to 3 bps in Germany) compared to a liquidity-thinned bull steepening in the US with moves from -2 bps to flat. Currency markets ex GBP were a sea of calm.

Asian-Pacific dealings lacking much other news revolve mostly around the PBOC announcement (see News & Views) to suspend bond buying. All eyes are on US economic agenda for today. The University of Michigan’s consumer confidence indicator (January) is scheduled but it’s the December payrolls report that’ll get most of the market attention. We think risks to the 165k consensus are skewed to the upside. The front end of the US curve is at a stalemate with markets already positioned more hawkish than the Fed (40 bps of cuts priced in compared to 50 bps in the dot plot). Similarly we do not think that a downside surprise would suddenly prompt a material dovish rebalancing. Recent Fed speak was clearly in favour of a prolonged pause at the current level of rates. The long end is most vulnerable for further losses in case of a topside surprise. Important resistance in the 10-yr yield is located at 4.73%. A break implies a return towards the 2023 high of 5.02%. Dollar strength remains our base case. With the euro not yet ripe for a rebound from its own making, south is the past of least resistance in EUR/USD. 1.0226 is the reference to watch.

News & Views

The People’s Bank of China (PBOC) this morning announced that it suspends its Treasury Bond purchases. In explaining the move, the PBOC said that supply of bonds has fallen compared to demand, triggering a shortage in the market. Bond purchases since last year gained in significance as a tool to manage market liquidity as the central bank tried to ease monetary conditions to support the ailing economy. However, the subsequent sharp decline in yields is seen as a factor putting additional pressure on the currency. The run on (long-dated) bonds can also be seen as a sign of investor doubts on the ability of authorities to address current deflationary trends. Chinese authorities showed unease with the financial stability risks related to a stretched bond positioning in the market (risk for a crash). The central bank left the timing open of a resumption of its program which. It will take place at a proper time depending on supply and demand in the government bond market. In a first reaction, the 10-y Chinese government bond yield jumped 4 bps to 1.68%, but the gain dwindled as trading continued. The yuan trades little changed near recent lows at USD/CNY 7.332.

Inflation in Mexico declined eased further in December printing at 0.38% M/M and 4.21% Y/Y. The latter marked the lowest level since February 2021. Core inflation reaccelerated to 0.51% M/M and 3.65% Y/Y. The central bank of Mexico aims to keep inflation at 3.0% with a 1.0% tolerance band. The data most likely will allow the bank to continue its easing cycle. The central bank cut its policy rate in December by 25 bps to 10%. It started its easing cycle in March of last year at 11.25%. The Minutes of the December policy meeting yesterday showed that a majority of the board members leaned to considering larger rate cuts. "In view of the progress on disinflation, larger downward adjustments could be considered in some meetings, albeit maintaining a restrictive stance," the minutes said. The Mexican peso, which suffered from overall USD strength in the second half of last year, remains in the defensive. At USD/MXN, the local currency holds within reach of the weakest levels since mid-2022 reached at the end of last year.

Jobs Day

In the absence of the US, the UK sat on the headlines yesterday, with its debt drama. Everyone threw in what he or she thought about what today’s situation reminded them. The discussions went from the latest aggressive selloff triggered by Liz Truss to 1976 debt crisis when the UK had to ask IMF help to get its head above water. I don’t think that the UK is there just yet, and yesterday’s retreat in yields (after reaching fresh highs) *without the Bank of England’s (BoE) intervention* was more than welcome. But the fact is, Rachel Reeves is losing her fiscal headroom and her manoeuvre margin with every basis point rise in borrowing costs, and that muddies the UK’s growth outlook. In numbers, the 10-year gilt yield has risen around 60bp since Rachel Reeves announced her latest budget. Note that the yields didn’t rise as spectacularly and immediately as in reaction to Liz Truss’ mini budget disaster, but the yields are now above Liz levels – and that leaves the UK government with three choices: either they will announce more tax rises, or lower spending, or both. According to people who are familiar with the matter, it would be the second option: lowering spending plans in the first instance. Maybe that’s what brings some relief to investors. But in all cases, the UK’s drama in not over. Cable has now slipped below the 1.23 mark and is set for a deeper selloff. Price rebounds could be interesting opportunities to strengthen short positions and target the 1.20 support. On the euro front, we should see consolidation and extension of the latest gains in favour of the euro.

Fun fact before we move on. The UK – which has a huge debt, dismal productivity and growth and a thick layer of unnecessary regulation like continental Europe – still has a debt-to-GDP level lower than other developed economies like France, Italy, Spain and Japan! But the country faces relatively tougher market reaction to its political decisions. I have the feeling that investors somehow continue to blame the UK for its decision to quit the EU. But anyway, the selloff in gilts and the pound may have cooled down yesterday, but cost of boosting growth has become significantly more expensive for the UK government, meaning that we may not see the UK perform as well as it did last year. And that sets the pound outlook negative at the early weeks of the new year.

Moving on, the EURUSD continued to be sold in the absence of Americans yesterday and is trading below the 1.03 mark this morning. The selling pressure is backed by strong dovish expectations from the European Central Bank (ECB) that were – in return – backed by the French central bank head Francois Villeroy’s view that the ECB should cut its rates at every policy meeting into summer to reach a neutral rate. I doubt that his German equivalent shares the same opinion after inflation in Germany jumped to 2.9% last month...

In all cases, the EURUSD’s – and other major pairs’ – short-term direction will likely be set by the US dollar. The US will release its latest jobs data today, and the numbers could help slowing the fast progress of the Federal Reserve (Fed) hawks that resulted – along with US debt worries – in rapidly rising yields.

Before the announcement of the US official jobs data, activity on Fed funds futures suggests that the Fed’s next rate cut should arrive in May – with around a 53% chance. A set of stronger-than-expected data could flip this expectation to the ‘no cut until June’ side very rapidly and enhance the selloff in the US dollar and support a further appreciation of the US dollar, while a set of softer-than-expected jobs data could strengthen the hope of a May cut. Given how quickly the Fed hawks have gained ground in recent weeks—and how much more investors are excited by dovish signals—the market’s reaction to soft data could outweigh its response to strong figures. The expectation is that the US economy may have added 164K new nonfarm jobs in December – well below the 227K added a month ago, but that number was boosted by the strikes and hurricanes of the month before (so the fall won’t be as bad as it first looks). Then, the average earnings is expected to remain highly sticky near the 4% on an annual basis – which is a problem for the Fed because people who earn more tend to spend more. And finally, the unemployment rate is seen steady near 4.2%. Again, strong NFP and wages growth would be supportive of the dollar, while soft NFP and wages growth should lead to a pullback in both. But if we see mixed figures, wages data could overweigh – unless we see an alarmingly high or low NFP figure.

Meanwhile in China

On the flip side of the world, the Chinese struggle with a completely different problem. Despite the announcement of multitude stimulus measures, yields there continue to dive, and the gap between the US and Chinese yields are widening *alarmingly*. We hear the phrase ‘Japanification of China’ pronounced very often since last year - the Japanification referring to inability to boost spending and investment despite lower rates. This – formally the liquidity trap – is probably the worse disease for an economy and takes very longtime to heal. The CSI 300 experienced its worst start to a year since 2016 and is finding difficult to rebound on low rates. The yuan is weak and the Chinese are expected to let it weaken further as an additional tool in the trade war against Trump. But low yields and prospects of a weaker yuan make it harder to convince foreign investors to bring on money, as the economic growth remains lacklustre. China will release its latest inflation report this weekend, and everyone prays for deflation to slow.

Time for NFP, Buckle Up

In focus today

The most important data release of the day will be the US December Jobs Report. We expect nonfarm payrolls growth to slow down to +170k (from +227k), see unemployment rate steady at 4.2% and average hourly earnings growth at +0.3% m/m SA. University of Michigan's preliminary consumer sentiment survey for January is also due for release later in the afternoon.

In Denmark, we get December inflation data. We expect an increase to 1.9% from 1.6% in November. Much of the increase is driven by a base effect from falling energy prices in December 2023. The scale of the food sale (not least on butter) is always a joker in December.

In Norway, inflation data for December is released. There are always significant effects on the inflation figures in December amid the effects of Christmas shopping. Card data suggests that consumption in December was moderate, at least until the last weekend before Christmas. In addition, we saw less price reductions than usual during Black Week. Overall, we therefore believe that core inflation slowed to 2.8 % y/y in December.

In Sweden, November's batch of Swedish macro data is on the agenda, including the GDP-indicator, Production Value Index (PVI) and household consumption. The two prior GDP-readings have signaled negative monthly growth and was further corroborated by negative readings for both PVI and the consumption indicator in October. As the weak Swedish growth, and repeatedly postponed recovery, have been a key reason behind the Riksbank's previous monetary policy stance, today's numbers are likely to carry some weight for the January meeting. Especially if they continue to disappoint given the Riksbank's recent hawkish shift in communication. However, the GDP-indicator is notably unstable and subject to heavy revisions, so interpret with caution. The Nation Debt Office will also release their latest, and 2024's last, monthly report on the net borrowing requirement. Up until and including November, the budget surplus sums up to SEK 22.9bn. However, with a forecasted deficit (and hence borrowing requirement) of SEK 108bn for December, Sweden is heading for a deficit for the full year 2024, following three years of budget surpluses.

Economic and market news

What happened overnight

In China, PBOC said that it has halted its buying of treasury bonds until an "appropriate time" due to supply shortage on the market. The decision follows months after the announcement from PBOC that they would start purchasing bonds as part of measures to improve liquidity management. Chinese yields jumped somewhat on the message.

What happened yesterday

In the euro area, retail sales rose 0.1% m/m SA in November following a decline of 0.3% m/m SA in October. The positive rebound trajectory that retail sales have been on since H2 2023 has thus faded recently like the development in consumer confidence. This is a concerning sign for the GDP outlook since consumption is expected to be the key driver of the recovery in 2025.

In Germany, industrial production rebounded in November with production rising 1.5% m/m SA following a decline of -0.4% m/m SA in October. The increase was broad-based across manufacturing, construction, and energy production. The negative trend in industrial production has become less severe in H2 2024. The same picture is shared when looking at "truck toll mileage" which has stabilised at a low level. These hard data points contrast somewhat with the continued weak PMIs. Overall, we expect the negative trend in industrial production to continue, likely resulting in a small decline in GDP in both Q4 and Q1 2025 before lower policy rates and rising real wages should give temporary boost to growth in the second half of this year and in 2026.

In the UK, GBP FX and Gilts remained under pressure with the 30Y Gilt yield trading at its highest level since 1998 above the 5.35% mark. Amid a backdrop of global financial conditions tightening and rates ticking higher, the UK is left vulnerable given its fragile fiscal position due to its large public debt and deficits. The Labour government's expansionary budget from the end of October has come under pressure with funding costs soaring together with weaker than expected growth since the announcement of the budget. As we have previously argued, we think the government is set to either roll back some of its measures or hike tax further at the next fiscal event in March. We remain cautiously optimistic that the move in UK space is overdone, but stress that if risk appetite continues to sour the moves could continue.

On the geopolitical front, we published our revamped Geopolitical Radar yesterday. The key things to look out for in January are Trump's inauguration, the expiry date of Hezbollah-Israel ceasefire a few days later and whether the EU and China can make any progress in tariff talks. Please see the revamped edition here Geopolitical Radar, 9 January.

Equities: Global equities were flat yesterday, with Europe higher, Asia lower, and the US closed. In Europe, we observed some improvement in sentiment during the day. However, it was not an outstanding day on the European macro front. Nevertheless, European equities have been performing well lately, outperforming their US counterparts. This indicates how low the consensus expectations for Europe currently are.

In Europe yesterday, the STOXX 600 rose by 0.4%, the FTSE 100 increased by 0.8%, the DAX remained unchanged, and the CAC gained 0.5%. Asian markets are lower again this morning, and the same applies to US futures, while European markets are marginally higher.

FI: The upward pressure on EGB yields continued throughout Thursday's session, with market attention focused on the substantial supply entering the market. Debt sustainability is currently the key theme in the UK market. Yesterday, the 30Y Gilt yield reached its highest level since 1998. As global financial conditions tighten due to higher real yields, the question arises whether and how central banks should respond. For now, members of both the Fed and ECB seem hesitant, likely because they are waiting to see how persistent the recent move will be. However, the UK Treasury issued a public statement yesterday asserting that a repeat of the 2022 Gilt crisis is unlikely, as institutional investors currently have significantly higher levels of liquidity and collateral.

FX: Lower trading volume and more consolidation yesterday as the US markets observed the National Day of Mourning. EUR/USD consolidates around 1.03 and GBP/USD around 1.23. GBP has been the last couple of days' focal point within G10 FX but for today we look towards NFP and the dollar. Scandies found some modest support and NOK/SEK consolidates just shy of 0.98.

NFP to anchor Fed pause, 10-year yield eyes higher level

US non-farm payroll report is taking center stage today as markets look for confirmation of Fed’s anticipated decision to pause rate cuts this month. Recent comments from multiple Fed officials have highlighted a cautious approach to further monetary easing, with a consensus forming that the central bank is nearing a pause in its rate-cutting cycle.

Fed fund futures currently price 93% likelihood of a hold at the meeting, and an in-line or stronger-than-expected jobs report could push this probability closer to certainty.

The broader debate now shifts to two key questions: how long the Fed’s pause might last and how much more easing, if any, will occur this year. Current market pricing indicates a 60% chance of another hold in March, followed by a 53% probability of a rate cut in May. For the rest of 2025, markets see over an 85% chance that rates will remain steady at 4.00%-4.25%.

Following today’s data, the immediate focus is whether the odds of a March hold increase, reflecting an extended pause.

Regarding expectations on the data, for December, headline job growth is forecasted to slow to 150k, with the unemployment rate expected to hold steady at 4.2%. Average hourly earnings are anticipated to rise by 0.3% month-over-month.

While some signals, such as the ISM Manufacturing PMI Employment component falling to 45.3 and ADP private employment growth decelerating to 122k, point to a cooling labor market, others remain robust. ISM Services PMI Employment component held steady at 51.4, and the 4-week moving average of initial jobless claims fell to a historically strong 213k, suggesting resilience and leaving room for an upside surprise in today’s report.

In terms of market reactions, a major focus is on treasury yields. Technically, 10-year yield breached 61.8% projection of 3.603 to 4.505 from 4.126 at 4.683 this week, as rally from 3.603 resumed.

Strong NFP number could push TNX higher, and sustained trading above 4.683 should pave the way towards 100% projection at 5.028, which is close to 4.997 high, and 5% psychological level. Any upside acceleration could realize this target at around the end of Q1.

In any case, outlook in TNX will stay bullish as long as 4.517 support holds, in case of retreat.

Japan’s household spending falls for fourth month, minister flags critical economic transition

Japan’s household spending declined for the fourth consecutive month in November, falling -0.4% yoy. While this was an improvement from October's -1.3% drop and surpassed expectations of -0.8%, it still reflects ongoing consumer caution.

The decline was driven by significant cuts in expenditures on home appliances and food, highlighting weak domestic demand.

Spending on furniture and electric appliances plummeted by -13.8%, marking the third straight month of decline, while clothing and footwear saw a similar drop -of 13.7%, down for the second consecutive month. Food purchases also contracted slightly, falling by-0.6%.

Separately, Economy Minister Ryosei Akazawa acknowledged the challenges, stating that Japan's economy is at a "critical stage" in shifting public sentiment away from deflation and toward sustainable growth driven by higher wages and investment.

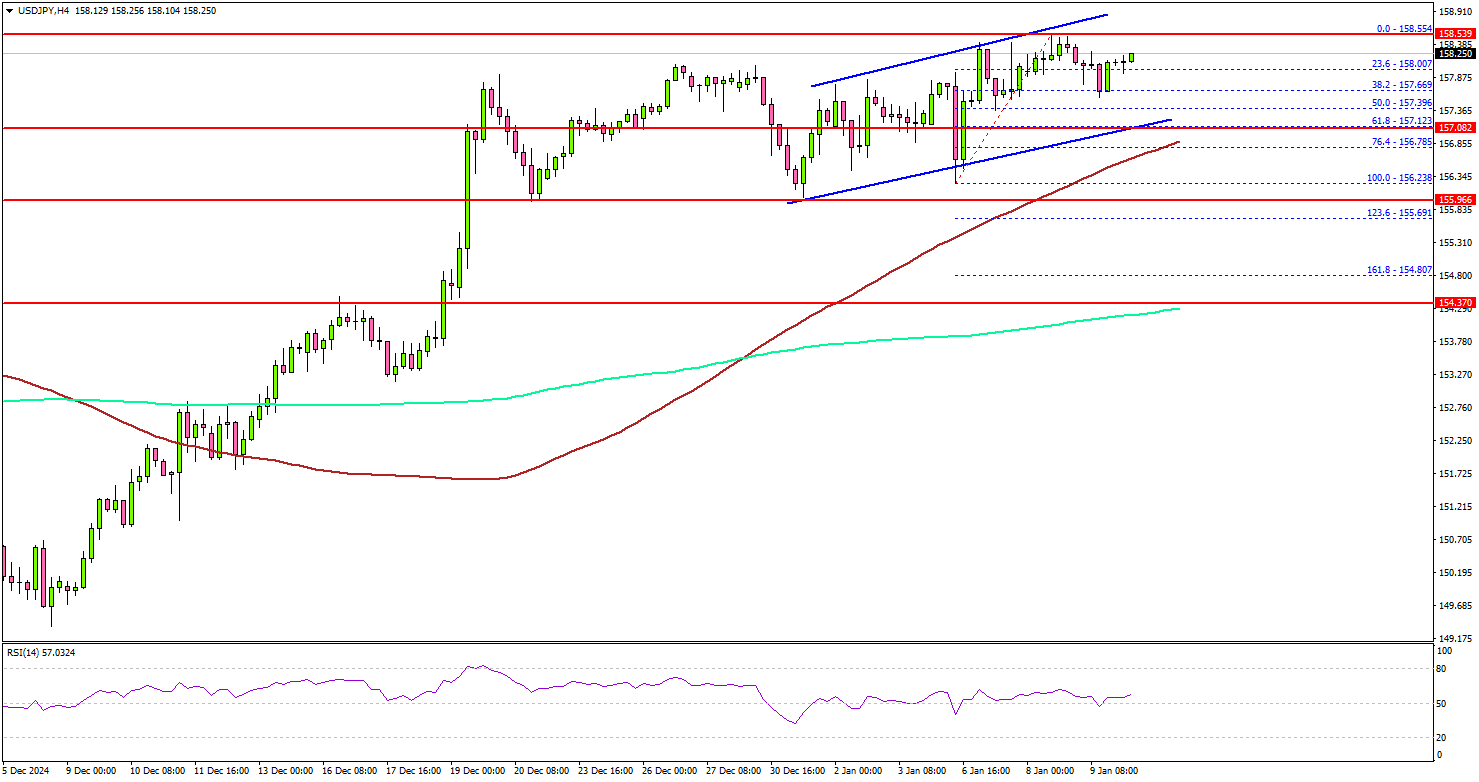

USD/JPY Poised for Action: Will NFP Drive More Upside?

Key Highlights

- USD/JPY started a consolidation phase above the 156.20 support.

- A short-term rising channel is forming with support at 157.10 on the 4-hour chart.

- GBP/USD accelerated losses below the 1.2350 support.

- AUD/USD and NZD/USD trade heavily in the bearish zone.

USD/JPY Technical Analysis

The US Dollar remained in a positive zone above 155.00 against the Japanese Yen. USD/JPY climbed above the 156.50 and 157.00 levels before the bears appeared.

Looking at the 4-hour chart, the pair settled above the 157.00 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair tested the 158.50 zone and traded as high as 158.55.

It is now consolidating gains below the 158.50 zone. There is also a short-term rising channel forming with support at 157.10. On the upside, the pair is facing hurdles near the 158.50 level. The first major resistance is near the 159.20 level.

The next major resistance is near the 160.00 level. A close above the 160.00 level could set the tone for another increase. In the stated case, the pair could rise toward the 162.00 resistance.

On the downside, immediate support sits near the 157.10 level and the trend line. The next key support sits near the 156.50 level. Any more losses could send the pair toward the 155.50 level.

Looking at GBP/USD, the pair started another decline and the bears were able to push the pair below the 1.2350 support.

Upcoming Economic Events:

- US nonfarm payrolls for Dec 2024 – Forecast 160K, versus 227K previous.

- US unemployment Rate for Dec 2024 - Forecast 4.2%, versus 4.2% previous.