Sample Category Title

Elliott Wave View: XAUUSD (Gold) Has Ended Correction and Turned Higher

Short Term Elliott Wave view in Gold (XAUUSD) suggests rally from 11.14.2024 low is unfolding as a 5 waves impulse. Up from 11.14.2024 low, wave (1) ended at 2721.41 and pullback in wave (2) ended at 2583.21 as the 1 hour chart below shows. The metal has turned higher in wave (3). Up from wave (2), wave (i) ended at 2626.41 and pullback in wave (ii) ended at 2586.82. Index has resumed higher in wave (iii) towards 2633.29 and pullback in wave (iv) ended at 2608.05. Final leg wave (v) ended at 2639.14 which completed wave ((i)) in higher degree.

Pullback in wave ((ii)) unfolded as a double three where wave (w) ended at 2611.28. Wave (x) rally ended at 2628.12 and wave (y) lower ended at 2595.91. This completed wave ((ii)) in higher degree. The metal has resumed higher in wave ((iii)) towards 2665.33 and pullback in wave ((iv)) ended at 2614.36. Expect the metal to finish wave ((v)) higher soon and this should complete wave 1 of (3). It should then pullback in wave 2 to correct cycle from 12.19.2024 low (2581.9) before turning higher again. Near term, as far as pivot at 2581.92 low stays intact, expect dips to find support in 3, 7, or 11 swing for more upside.

XAUUSD (Gold) 60 Minutes Elliott Wave Chart

XAUUSD Elliott Wave Video

https://www.youtube.com/watch?v=u2aHJgixjik

Bitcoin (BTCUSD) Elliott Wave Forecasting the Decline After Expanded Flat Pattern

In this technical article we’re going to take a look at the Elliott Wave charts charts of Bitcoin BTCUSD published in members area of the website. As our members know, we generally favor the long side in BTCUSD, and it has recently offered good trading opportunities. However, BTCUSD is currently correcting the cycle from the August low and is not ready for buying at this stage. Recently, we observed a recovery against the 108364 high, which unfolded as an Irregular Flat pattern. Once this flat correction was completed, the crypto declined as anticipated.

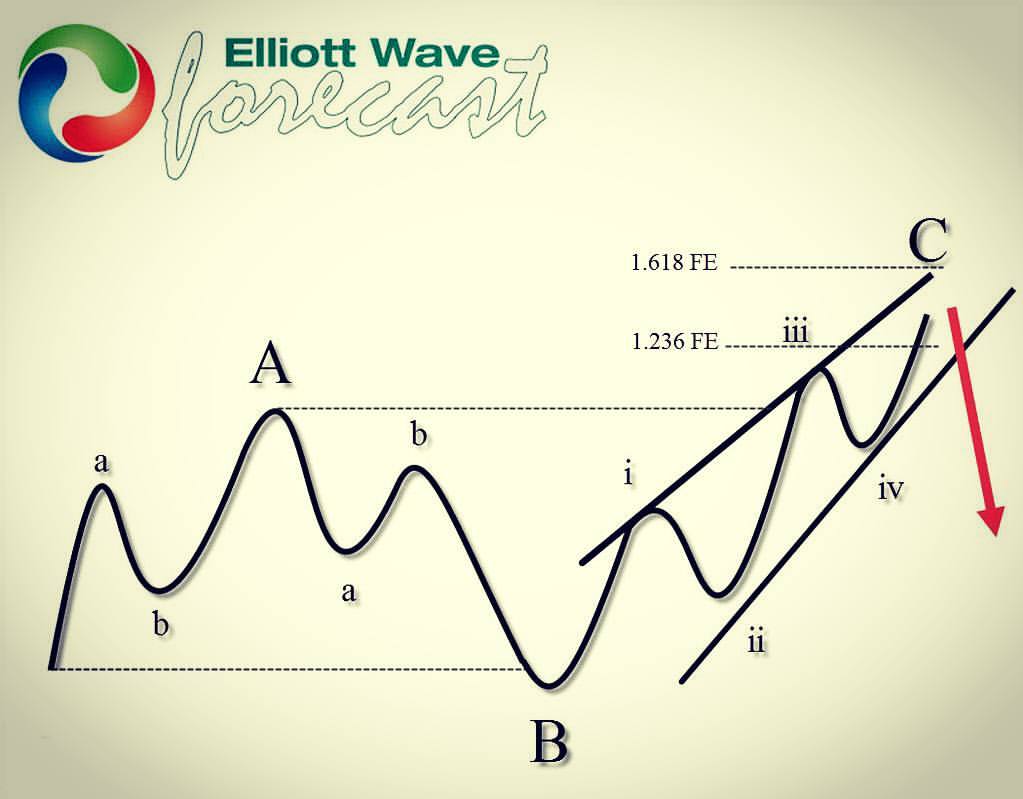

Before we take a look at the real market example of Expanded Flat, let’s explain the pattern in a few words.

Elliott Wave Expanded Flat Theory

Elliott Wave Flat is a 3 wave corrective pattern which could often be seen in the market nowadays. Inner subdivision is labeled as A,B,C , with inner 3,3,5 structure. Waves A and B have forms of corrective structures like zigzag, flat, double three or triple three. Third wave C is always 5 waves structure, either motive impulse or ending diagonal pattern. It’s important to notice that in Irregular Flat Pattern wave B completes below the starting point of wave A. Wave C ends above the ending point of wave A . Wave C of Flat completes usually between 1.00 to 1.236 Fibonacci extension of A related to B, but sometimes it could go up to 1.618 fibs ext.

At the graphic below, we can see what Expanded Flat structure looks like

Now, let’s take a look what Elliott Wave Flat Pattern looks like in the real market

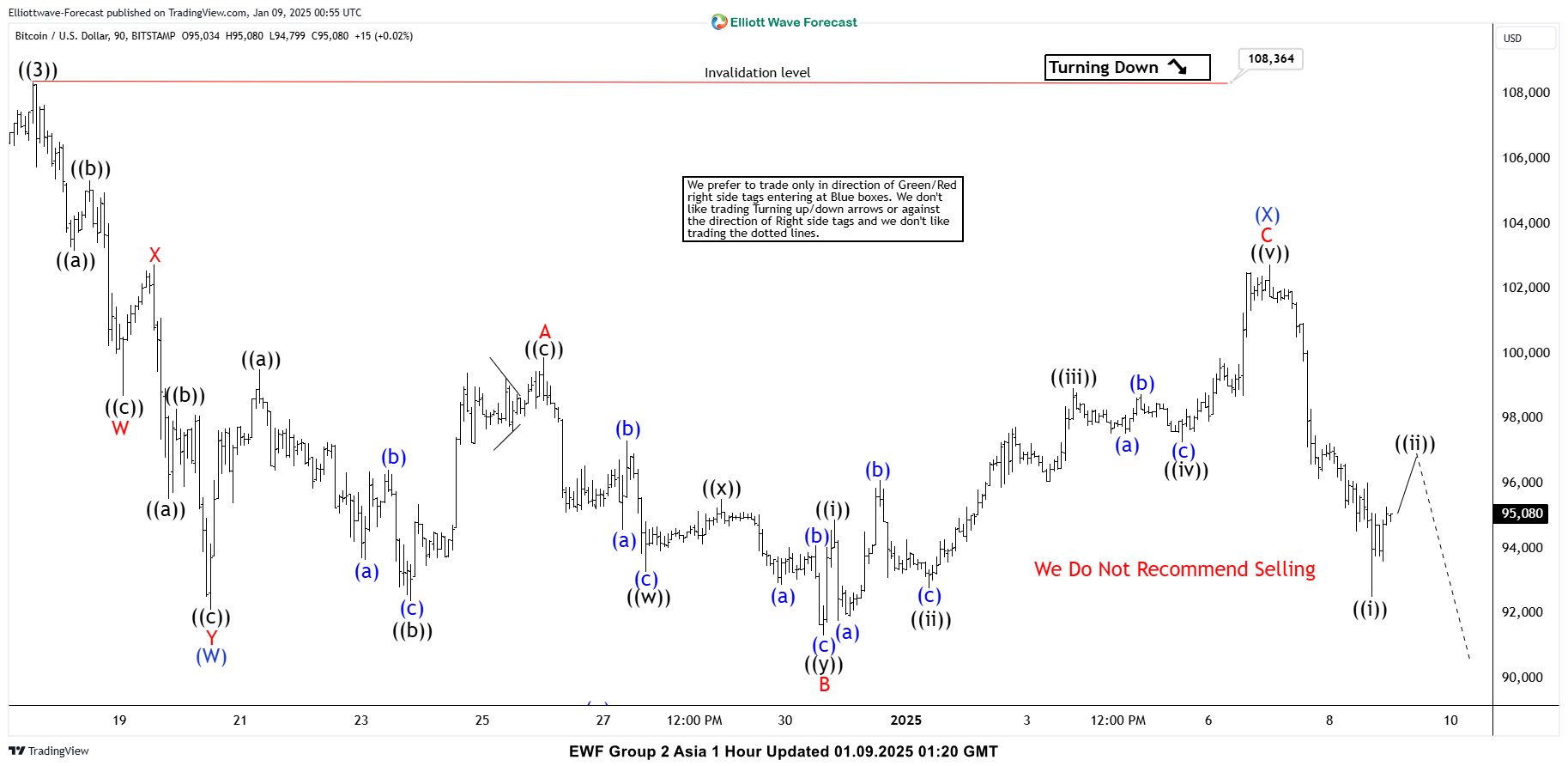

Bitcoin BTCUSD 1h Hour Elliott Wave Analysis 01.05.2025.

Currently, BTCUSD is correcting the cycle from the 108364 high. The Elliott Wave view suggests that the recovery is unfolding as an Irregular Flat Pattern. When we analyze the lower time frames, we can observe that the inner subdivisions of waves A and B (red) exhibit corrective sequences. Wave B has already broken below the starting point of wave A, while wave C is expected to break above the point of wave A, which is characteristic of an Irregular Flat pattern. At this stage, we see that the C leg is still missing another wave up to complete its structure as a 5-wave move. We recommend our members avoid buying at this stage.

Bitcoin BTCUSD 1h Hour Elliott Wave Analysis 01.09.2025.

Bitcoin made another leg up in wave ((v)) of C, completing the (X) blue recovery at the 102730 high. As anticipated, the crypto turned lower. We are now looking for a break below wave B (red) to confirm that the next leg down is in progress. At this stage, we do not favor selling and would prefer to wait for the (Y) leg to reach the extreme area before considering buying BTC again.

USD/CHF Technical Outlook: Bulls in Charge as Potential Double Top Pattern Forms

- USD/CHF has been in a strong uptrend since September 2024, largely mirroring the US Dollar Index (DXY).

- A potential double top pattern is forming around the 0.9137 resistance level.

- Key support levels to watch are 0.9087, 0.9040, and the psychological 0.9000 handle.

- A break above the 0.9137 resistance could lead to further gains.

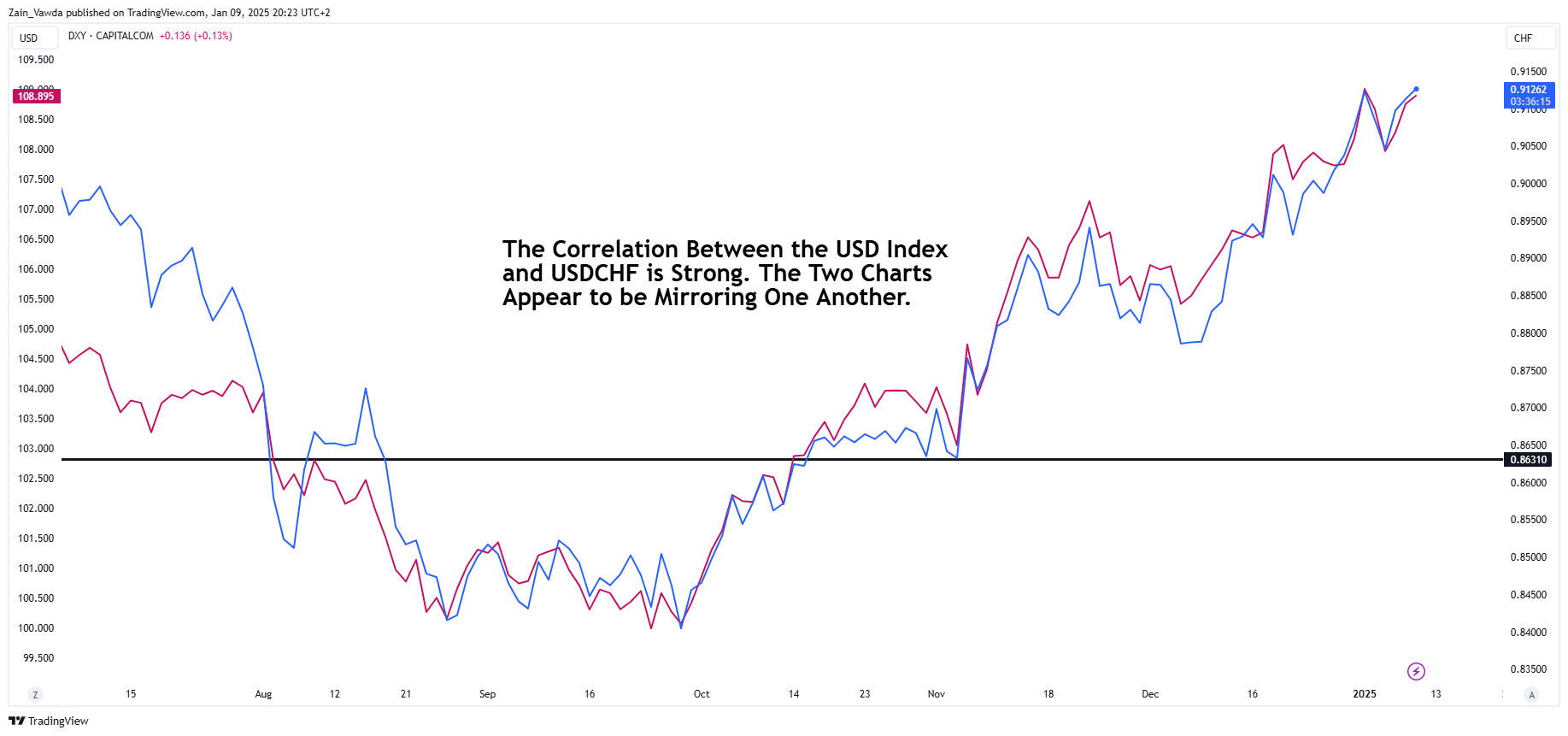

USD/CHF has been on an incredible run since bottoming out in September 2024. The rally which has been largely driven by the US Dollar Index has continued with brief pullbacks and pauses as it hovers comfortably above the psychological 0.9000 handle.

In reality if one looks at the US Dollar Index and USD/CHF daily charts they are mirror images of another. A sign of the US Dollars significance in the recent rally. As you can see the below just how correlated the two have been with the USD Index represented by the red/purple line and USD/CHF in the blue line.

US Dollar Index (DXY) vs USD/CHF Daily Line Chart

Source: TradingView (click to enlarge)

The Swiss economy has faced its fair share of challengers but the weakening currency is not one of them. Switzerland, which is viewed as somewhat of an export economy, had been under pressure by those in the export industry as the strengthening Franc left exporters unable to compete.

Markets are pricing in a rate cut from the SNB in March and if expectations around rate cuts from the Federal Reserve continue to be hawkishly repriced, this could leave USDCHF vulnerable to further upside.

US Jobs data due tomorrow could have a significant impact in this regard, as markets return from the US Holiday today.

Technical Analysis

From a technical standpoint, USD/CHF has been on a tear since the back end of September 2024.

More recently however, price has formed a base around the psychological 0.9000 level which is serving as strong support. The relationship with the DXY was shown above and underscores the importance of the index in USD/CHFs next move.

USD/CHF Daily Chart, January 9, 2025

Source: TradingView (click to enlarge)

Dropping down to a four-hour chart and it did appear that USD/CHF might be ready for a deeper retracement on January 6. USD/CHF broke structure by closing below the swing low of January 2, putting the bears in control.

However, instead of printing a lower high, USD/CHF went on to break the previous swing high and bring the bullish momentum back into play.

There is some light at the end of the tunnel for bears however. USD/CHF currently trades at 0.9128 with the most recent high just above at 0.9137.

A rejection of the previous high would lead to a double top pattern print, which is usually a sign that a reversal may be incoming.

A lot of this will depend on the US Dollars performance in the coming days but is worth watching.

A break of the resistance at 0.9137 brings resistance at 0.9157 and potentially 0.9224 into focus.

A rejection and double top print could open the door to a deeper retracement which may find support at 0.9087 before the 0.9040 and psychological 0.9000 come into focus.

USD/CHF Four-Hour Chart, January 9, 2025

Source: TradingView (click to enlarge)

Support

- 0.9087

- 0.9040

- 0.9000

Resistance

- 0.9137

- 0.9157

- 0.9224

WTI Crude Oil Wave Analysis

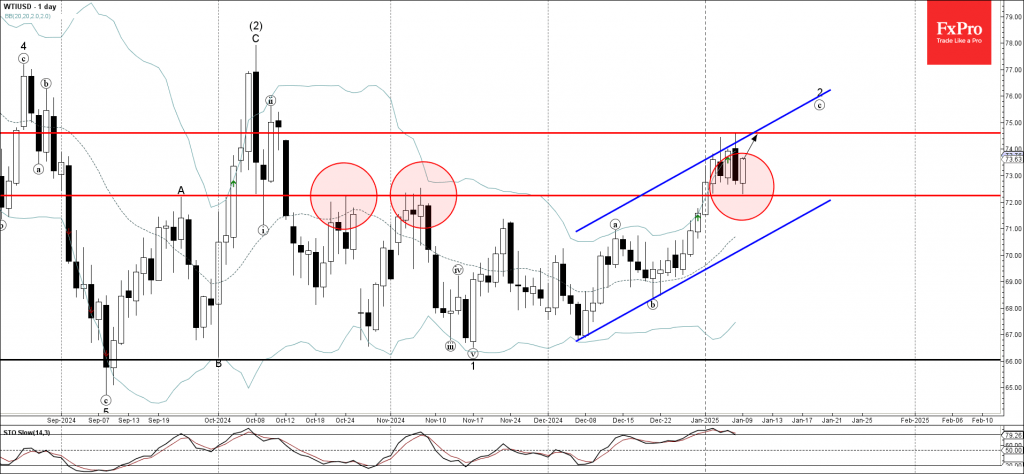

- WTI crude oil reversed from support level 72.25

- Likely to rise to resistance level 74.60

WTI crude oil recently reversed up from the key support level 72.25 (former resistance from October and November, as can be seen below).

The upward reversal from the support level 72.25 continues the c-wave of the active ABC correction 2 from the middle of November.

WTI crude oil can be expected to rise in the active minor c-wave to the next resistance level 74.60, coinciding with the resistance trendline of the narrow daily up channel from last month.

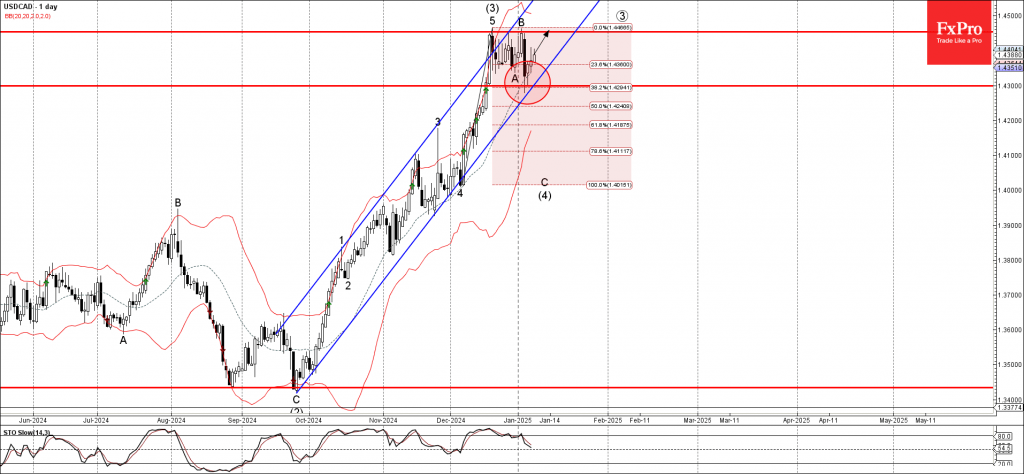

USDCAD Wave Analysis

- USDCAD reversed from support zone

- Likely to rise to resistance level 1.4450

USDCAD currency pair recently reversed up from the support zone located between the support level 1.43000, 20-day moving average and the support trendline of the sharp daily up channel from September.

This support zone was further strengthened by the 38.2% Fibonacci correction of the upward impulse from last month.

Given the clear daily uptrend, USDCAD currency pair can be expected to rise to the next resistance level 1.4450 (which stopped the previous waves (3) and B).

BoE’s Breeden: Pace of rate cut uncertain, gradual easing expected

BoE Deputy Governor Sarah Breeden today reinforced expectations for gradual easing of monetary policy, citing the abating effects of past economic shocks.

"I expect to continue to remove restrictiveness gradually over time," she added.

However, she cautioned against prescriptive timelines, remarking that it is "difficult to know" how quickly rates should fall.

Fed’s Harker: To maintain easing bias but pause briefly to assess impact

Philadelphia Fed President Patrick Harker reaffirmed his view today that Fed remains on a “downward policy rate path,” but emphasized flexibility based on future data.

“Looking at everything before me now, I am not about to walk off this path or turn around,” he stated at an event.

However, Harker suggested that the current stage of the policy cycle calls for some patience. “I think it’s appropriate for us to take a bit of a pause right now and see how things shake out,” he said, hinting at a temporary hold in rate adjustments to assess the economic impact of past cuts.

While advocating for a short pause, Harker added that Fed likely won’t remain in this holding pattern for long.

Fed’s Collins advocates gradual and patient approach on rate cuts

Boston Fed President Susan Collins noted in a speech today that the economy is overall in a "good place" and inflation steadily retreating from its 2022 peak. She added that current monetary policy is already closer to a neutral stance, allowing Fed to proceed with a "gradual and patient approach" as it evaluates further steps.

Collins acknowledged the significant progress in lowering inflation, describing it as moving "gradually, if unevenly," toward Fed’s 2% target. Importantly, this progress has been achieved alongside a "healthy overall" labor market that has shown signs of rebalancing from previously overheated conditions.

Reflecting on Fed’s decision to cut rates last month, Collins her support as a “close call,” as the move provided "some additional insurance" to support the labor market while maintaining a restrictive stance necessary to restore price stability.

Sunset Market Commentary

Markets

The spotlights remain squarely focused on the UK. Gilts yields gapped another 12 bps higher across the curve at the open this morning before calm returned somewhat. While net daily changes are close to zero today, the sharp uptick over the previous days and increased media attention did force the UK government to respond to urgent questions in parliament today. Treasury’s number two, Darren Jones, said the bond market is functioning in an orderly way and stressed that “There should be no doubt of the government’s commitment to economic stability and sound public finances. This is why meeting the fiscal rules is non-negotiable.” The material yield increase is eroding the limited fiscal headroom Chancellor Reeves has to comply with her self-imposed rule to fund day-to-day public spending with tax receipts by 2029-30. People familiar already told Bloomberg that if updated OBR forecasts end March would indeed show fiscal headroom has been absorbed by risen debt costs, Reeves would resort to spending cuts instead of higher taxes or even worse: change the rules of the game once again as she did back in October. Sterling is headed for back-to-back losses with EUR/GBP briefly topping the 0.84 big figure. The pair is currently trading around 0.838. Cable slipped to the lowest level since November 2023 to hit an intraday low around 1.224 but then paring losses to 1.23.

Moves in other core areas remain very limited. German rates barely budge and US yields ease a few basis points. Yesterday’s successful 30-yr auction underscored solid demand, especially at such attractive yields. That offered some respite for bonds on a day that had little to offer otherwise. The eco calendar is empty and US markets have either a shortened (bond markets) or no trading session at all (stocks) on this national day of mourning for ex-president Carter. USD changes are confined to tight ranges. JPY outperforms in one of the “bigger” moves today.

News & Views

UK CFOs in December assumed a slight rise in inflations expectations, the Bank of England Decision Maker Panel survey revealed. Year ahead own price inflation was expected to be 3.8% up from 3.7% in November. 3.8% was also the reported level of realized annual output price inflation in the three months to December of last year. A similar trend was seen in CFO’s CPI inflation expectations. Perceived CPI was 2.5% in the three months to December, down 0.1% from 2.6% but the one year ahead expectations rose from 2.7% to 2.8% in the three months to December. The corresponding measure for three-year ahead CPI inflation expectations was 2.7% from 2.6% in November. Reported annual wage growth eased 0.1% to 5.4%. Expected year-ahead wage growth remained unchanged at 4.0%. Asked about their reaction to the increase in employer national insurance contributions in the Autumn Budget, on average over the November and December surveys, 61% of firms expect to lower profit margins, 54% expect to raise prices, 53% expect lower employment and 39% expect to pay lower wages than they otherwise would have done.

Eco data in Hungary published today showed a mixed picture. Industrial production in November declined 1.9% M/M (SA) resulting in a 2.9% contraction compared to the same month last year. The statistical office reported falling production volumes in November 2024 in the great majority of the manufacturing subsections, with growth seen only in three subsections including the manufacture of coke and refined petroleum products. In the first 11 months of the year production was 3.9% lower than in the same period last year. Retail sales showed a slightly better picture rising 0.6% M/M and 4.1% Y/Y. YTD November sales growth was reported at 2.9%. The finance Ministry today also indicated that the 2024 budget shortfall probably came out at 4.8%, missing the deficit target of 4.5%. Despite the 2024 overshoot, the government still intends to reduce the budget deficit to 3.7% this year. This budget target however is based on an assumption of 3.4% 2025 GDP growth and 3.2% Inflation, which might be challenging to realize. After being under pressure due to global market sentiment, the forint regains modest ground trading near EUR/HUF 415 compared to reaching weakest levels since end 2022 (416.6 area) earlier this week.