Sample Category Title

Can’t Stop Canada – Another Solid Canadian GDP Report

- The Canadian economy notched up its seventh straight monthly expansion in May, growing an impressive 0.6% month-on-month.

- Growth was again broad based, with 14 of 20 major industries expanding on the month.

- The goods-producing side of the economy tore ahead, growing 1.6% month-on-month. Leading the way was mining and quarrying (+4.6%), as a major oil facility came back online following a shutdown earlier, and conventional extraction saw robust growth. Canadian manufacturing expanded 1.1% on broad-based sub-sector strength, more than offsetting last month's declines. The fly in the ointment was construction, which fell for a second month (-0.6%), attributed in part to a strike among Quebec workers.

- While less exciting, the services-producing industries remained reliable, notching up a 0.2% gain in its 21st straight monthly expansion. Leading the way were retail trade (+0.9%), finance and insurance (+0.9%), and wholesale trade (+0.7%). The impact of changes to real estate market regulations in Ontario could be seen in the real estate/rental and leasing sector , which declined 0.2% in May, the largest decline seen since mid-2010.

Key Implications

- There appears to be no holding back the Canadian economy, at least for now. Making a robust GDP print even more impressive was that those sectors that did decline did so either due to government policy (real estate), normalization after a robust April (arts and entertainment), or one-off factors (construction), suggesting an even healthier underlying signal.

- May's solid report continues a string of encouraging economic data, and suggests that the Canadian economy likely saw its strongest first half performance since at least 2004 (Current Q2 tracking: 3.8%).

- The near-term robustness of the Canadian economy will likely allow the Bank of Canada to carry through with another interest rate increase this fall, completing the removal of the 2015 emergency stimulus, and consistent with the rapid change in their communication tone.

- Beyond the near-term, a return to a more cautious communication strategy and pace of interest rate increases is expected in light of the headwinds facing Canada, and evidence suggesting that recent economic strength may not translate as meaningfully into inflationary pressures relative to historic experience.

Gold Shrugs Off Strong US GDP, Climbs to 6-Week Highs

Gold has posted considerable gains in the Friday session. In North American trade, spot gold is trading at $1264.43, up 0.42% on the day. On the release front, US Advance GDP posted a strong gain of 2.6%, above the forecast of 2.5%. UoM Consumer Sentiment will be released later in the day, with the key indicator expected to dip to 93.2 points.

There have been ominous warnings that the US economy is in trouble and that second quarter growth might follow a soft first quarter. However, the naysayers were nowhere to be found on Friday, as the economy expanded at an impressive clip of 2.6%. Consumer spending and business investment led the way with strong gains, as the economy recovered from a slow start to the quarter. Still, more data will be available for the next two GDP reports, which could show more restrained growth. Gold prices shrugged of the GDP numbers, as the metal has climbed to its highest level since mid-June.

It's become an all-too-familiar pattern out of Washington – trouble for the White House has translated into losses on global stock markets, as higher political risk has made investors jittery. It was déjà vu on Thursday, as President's struggling healthcare bill gasped its final breath as the bill was defeated in the Senate after three Republican lawmakers joined the Democrats and voted against the bill. This is another setback for President Trump, who has been unable to get Congress to pass any significant legislation, despite the Republicans controlling both the House and the Senate. Trump will now be able to focus on other issues such as tax reform, but investors are skeptical as to whether the President will have the support he needs in Congress to pass major legislation.

With the Federal Reserve holding rates at 1.25% at this week's policy meeting, the markets focused on the rate statement, as investors looked for clues about future rate moves. The statement was cautiously optimistic in tone, with policymakers saying that the economy was growing at a moderate pace and that the labor market remained strong. The statement made note of low inflation, but said that the Fed expected the economy to continue to expand. Another key issue on the Fed's plate is the $4.2 trillion balance sheet. The rate statement said that the Fed plans to taper asset purchases "relatively soon", which is a likely nod at September as the start date. This would involve the Fed tapering its purchases of Treasury bonds and mortgage securities, with an initial taper likely of $10 billion/month. Although the Fed continues to talk about another rate hike in 2017, investors remain skeptical. The rate statement did not change many minds, as the odds of rate increase in December stand at 47%, according to the CME Group.

EUR/USD Is Still Bullish But Watch Weekly H3 Camarilla Pivot

The EUR/USD has been in a steady uptrend as I also showed on Live trading webinar but now it is struggling to break W H3/D H4 camarilla pivot. The POC zone is 1.1700-1.1710( D H3, ATR pivot, 23.6, trend line) and if the pair get there it might spike again towards the 1.1730 and 1.1750. A strong momentum above 1.1750 should provide a continuation wave towards 1.1770 and 1.1800. However a break below 1.10695 could initiate a pullback towards 1.1660. Today is Friday, so pay attention to possible profit taking that could instill additional volatility during the EOD (End Of Day).

US GDP Report Confirms Q2 Acceleration as Domestic Demand Remained Strong

Highlights:

- US Q2 GDP growth matched consensus, picking up to an annualized 2.6% pace from Q1's 1.2% gain.

- Final domestic demand growth held steady at 2.4% in Q2.

- Consumer spending growth rebounded to 2.8% from 1.9%. The Q1 increase was revised up from 1.1%, which looked surprisingly weak given aggregate income gains and strong consumer sentiment.

- Nonresidential investment maintained momentum with a 5.2% gain in Q2 building on the previous quarter's 7.1% gain.

- Stronger business investment was broadly-based though the increase in structures was due to a further surge in mining exploration.

- Residential investment slipped back following a double-digit gain in Q1. Some housing activity may have been brought forward by unseasonably warm winter weather.

- Net exports added to growth for a second consecutive quarter, reflecting solid export gains year-to-date.

Our Take:

It would be easy to say the US economy got its groove back in Q2 with GDP growth jumping to 2.6% following Q1's sub-trend 1.2% gain. However, revisions show much of that slowing can be attributed to weaker inventory investment. Underlying demand never really lost its mojo with final sales to domestic purchasers rising 2.4% in each of the last two quarters. The previously-reported slowdown in Q1 consumer spending has been lessened to 1.9% through revisions with Q2's growth rate rebounding to 2.8% and thus more consistent with solid employment gains to date this year. Another solid increase in business investment was also encouraging, coming from both rebounding oil and gas capex and spending by non-energy firms. We don't think the Fed will be surprised by today's data; they've been anticipating a Q2 rebound for some time now and have consistently pointed to strength in consumer spending and business investment. But confirmation of a solid increase is heartening, particularly in the face of slowing inflation in recent months. The return to above-trend growth points to remaining economic slack being absorbed, which should begin to put upward pressure on prices and help return inflation to their 2% objective. As such, we continue to expect another rate increase before year end, to which markets are only attaching 50/50 odds at present.

Canada’s May GDP Soars Despite Quebec Construction Strike

Highlights:

- Canadian GDP rose an impressive 0.6% in May following a 0.2% gain in April.

- Market expectations had been for a much more moderate 0.2% increase with the upward surprise mainly concentrated in the mining sector soaring 4.6% in the month.

- Today's report is indicative of no slowing in Q2 from the Q1 annualized increase of 3.7%.

Our Take:

Canadian GDP jumped a much stronger than expected 0.6% in May marking the 7th consecutive month of increases. The upward surprise was mainly concentrated in the mining sector as it soared 4.6% in the month. There was an expected return of an oil sands upgrader after a temporary shutdown starting in March but the strength went well beyond this factor and occurred despite oil prices remaining moderately weaker than expected. A year ago this sector was hammered by the Alberta wildfires and widespread shutdowns of oil sands production facilities. Eliminating the upward impact of the mining sector GDP growth would still have increased a solid 0.2% despite a one-week construction strike in Quebec that subtracted about 0.1 percentage point from overall monthly growth. Thus today's report is indicative of solid growth persisting in the Canadian economy through the second quarter.

With today's report the annual year-over-year increase in GDP has jumped to 4.6% in May from 3.3% in April and an annual increase in 2016 of only 1 1/2% . In large part this rebound reflects a strong upward trend in mining output with today's report continuing this pattern of strong support. Additionally the manufacturing sector has been steadily, albeit more slowly, improving. Today's report showed that the annual increase in manufacturing activity jumped to an impressive 5.2%, teeing up for the second quarter to build on Q1's 2.1% rise. This improvement in part is due to increasing demand for manufactured goods from the energy sector but also likely reflects rising external demand with U.S. industrial production starting to trend higher. Our forecast assumes that these supportive factors will likely be sustained through the forecast allowing manufacturing to continue to provide support to overall growth in the economy.

Dollar Continues to Struggle on Soft US Price Data

- The wave of selling across the tech stocks has reached Europe. The Euro Stoxx 50 index currently hovers around intraday losses of -0.9%. The US stock indexes opened on the same negative sentiment with especially the highly tech-weighted Nasdaq underperforming (-0.36%).

- The first estimate of the American GDP for the second quarter was, with 2.6% Q/Q, lower than the expected 2.7% but significantly higher than the downwardly revised 1.2% in the first quarter. Both consumption (+2.8% Q/Q) and investments (+ 2.0%) contributed strongly. Today's numbers confirm that the Q1 slowdown was temporary.

- The price data were subdued in the US. The GDP price index declined from 2.0% Q/Q in Q1 to 1.0% in Q2. The consensus had expected a higher reading (1.3%). The same goes for the Employment Cost Index which was 0.5% in Q2, down from a 0.8% number in Q1 and a 0.6% consensus. The core PCE was the only number above expectations (0.9% Q/Q compared to the expected 0.7%).

- GDP readings for Q2 in France, Austria and Spain were all better than expected or they at least matched expectations. In Spain, GDP rose from 0.8% to 0.9% Q/Q and from 3.0% to 3.1% Y/Y (consensus 0.9% M/M and 3.0% Y/Y). France saw its GDP stabilise Q/Q at 0.5% while the Y/Y figure increased from 1.1% to 1.8%, more than the forecasted 1.6%.

- The German CPI surprised to the upside in July with a 0.4% M/M and a 1.5% Y/Y rise (consensus 0.3% M/M and 1.4% Y/Y). In France, the CPI declined an expected 0.4% M/M but stabilised Y/Y at 0.8%. The Spanish CPI declined from a positive 0.1% M/M to a negative 1.2% M/M (consensus -1.3%) but rose from 1.6% Y/Y to 1.7% Y/Y (consensus 1.6%).

- Sentiment among UK households dropped this month to match the weakest reading since just after the Brexit vote, led by a sharp drop in confidence in the economy. The Gfk consumer confidence reading of -12 in July is down two points compared to June and lower than the expected -11.

- The European Commission's monthly measure of economic confidence nudged up 0.1 points to 111.2 in July – its best level since before the financial crisis hit in 2007. The gauge was driven higher by a bump in confidence in Germany and the Netherlands, but fell back in Italy, France and Spain.

Rates

Core bonds show two faces

Global core bond showed two faces. During the European morning session, the Bund (and US Treasuries) were hard hit by an avalanche of strong activity data and higher than-expected German and Spanish inflation (for July). The Bund fell from about 162.20 to 161.40. Regarding the eco data, French and Spanish Q2 GDP were strong, as was the EC euro area economic sentiment (highest since June 2007). German inflation exceeded expectations and stabilized (HICP) instead of declining. The German curve bear steepened (0.5 to 3.2 bps higher). Intra-EMU 10-yr yield spreads versus Germany were little changed.

The US Treasury followed the Bund lower in sympathy, but limited the losses. During the US session, US Treasuries erased losses on the US economic data, before reverting again a bit lower. US Q2 GDP was near expectations at 2.6%. Q1 GDP was revised marginally lower (see headlines for details). The GDP price indicator, however, slowed sharply to 1% Q/Qa from 2% Q/Qq in Q1 and fell short to expectations (1.3% Q/Qa). Core PCE deflator slowed to 0.9% Q/Qa from 1.8% Q/Qa, beating consensus (0.7%) though. Markets are very sensitive for inflation indicators. After soft CPI inflation, the slowing of the deflators shouldn't have been a major surprise. However, the soft Employment Cost Index might have been of greater impact on US Treasuries. Wages rose a sluggish 0.5% Q/Q, underlining that the tight labour market isn't (yet?) triggering wage increases. Without higher wages, the Fed's hope on fulfilling its target may remain elusive. That also questions the Fed's gradual tightening campaign. So, US Treasuries erased the losses (bunds barely regained ground), before some selling re-occurred. At the time of writing, US yields are nearly unchanged compared to yesterday's closing levels.

Currencies

Dollar continues to struggle on soft US price data

The euro initially gained a few ticks on good EMU data today and a declining interest rate differential with the dollar. Euro strength was replaced by USD softness later in the session. US Q2 GDP growth was in line with expectations, but the price data (cost employment indices) were again soft. EUR/USD trades in the 1.1725 area. USD/JPY struggles not to fall below 111.

The decline in equities/rise in volatility in the US spilled over to Asian markets. Losses ranged from roughly 0.5% to about 2%. Japanese household spending was strong and the jobless rate (2.8%) matched the multi-year lows. Japanese inflation held at low levels, close to the 0% mark. There was again little direct impact on the yen. USD/JPY held up quite well given the pick-up in volatility. EUR/USD didn't show a clear trend and trades in the 1.1680 area.

European data (French and Spanish GDP, EC confidence data and German inflation) were mostly strong (or at least better than expected). There was no one-on-one relation between the data and EUR/USD. Short-term interest rate differentials were little changed. LT European yields rose throughout the session and differentials narrowed in favour of the euro. EUR/USD returned gradually north of 1.17. USD/JPY hovered in a tight range mostly in the 111 area (even as equities remained in the defensive). So, the intraday rise of EUR/USD was at least partially due to euro strength.

EUR/USD rose further ahead of the publication of the US Q1 GDP. However, looking at other USD cross rates, this was more USD softness. US Q2 GDP was very close to expectations (2.6% Q/Qa). The price data in the report were mixed, but a low employment cost index was another indication of slow wage growth. US yields and the dollar declined. EUR/USD reacted most. EUR/USD spiked to the mid 1.17 area, but trades again in the 1.1730/35 area. The test of the 1.1714/35 barrier continues. The loss of USD/JPY was more modest. The pair tries not to fall below 111.00. The conclusion from the previous days hasn't changed: sentiment on the dollar will probably remain fragile unless there comes good news from prices and even more from US wages.

Sterling rebound stalls as global uncertainty weighs

GFK consumer confidence was marginally softer than expected overnight. There were no other important eco data in the UK today. Of late, the UK currency tried to regain ground against the euro. EUR/GBP slipped temporary below 0.89. However, the move had no strong legs. The rise in overall volatility yesterday and this morning weighted on sterling. Good EMU data, rising EMU yields and a rebound in EUR/USD, pushed EUR/GBP higher. There were also some, albeit second tier, headlines confirming stubborn hurdles in the Brexit negotiations (UK exit bill, Irish border…). The 0.8995 correction top looms again on the horizon. EUR/GBP trades currently in the 0.8970 area. Cable trades near 1.3080.

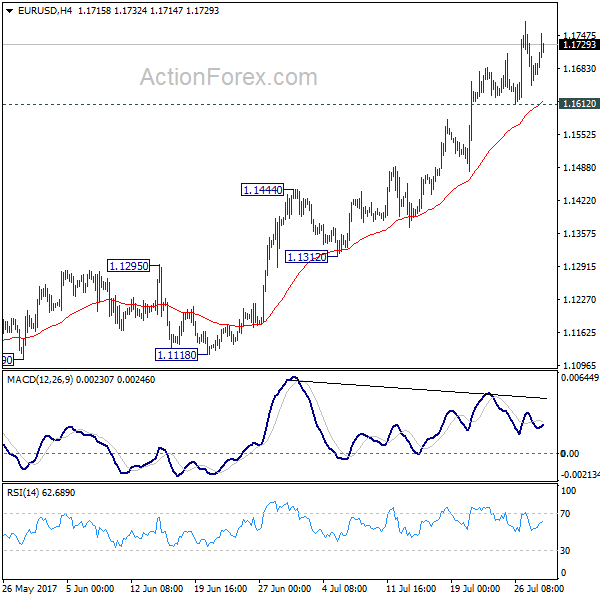

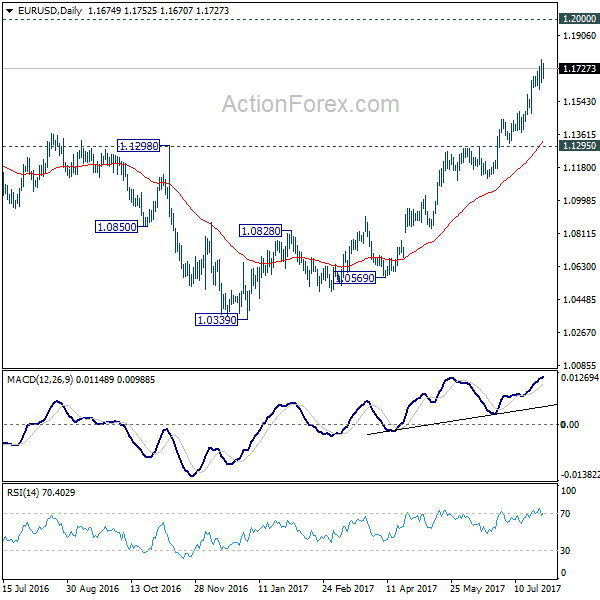

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1624; (P) 1.1700 (R1) 1.1751; More...

With 1.1612 minor support intact, intraday bias in EUR/USD remains on the upside. Current medium term rally is expected to target 1.2 handle next. Nonetheless, considering bearish divergence condition in 4 hour MACD, break of 1.1612 will indicate short term topping and bring lengthier consolidation first.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained break of 55 month EMA (now at 1.1760) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

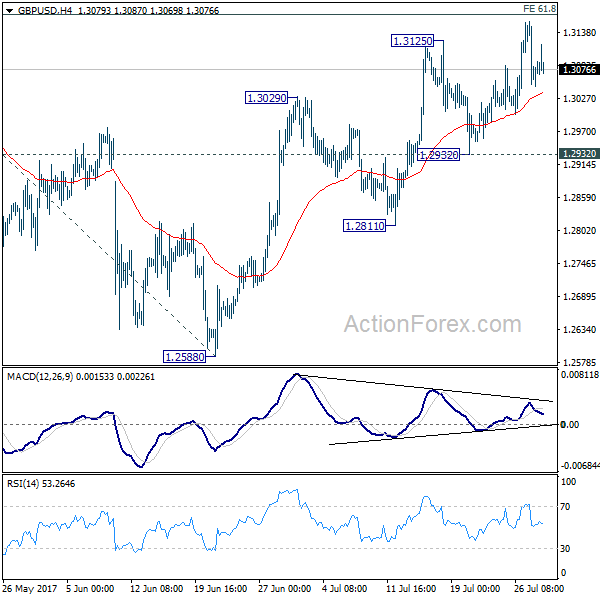

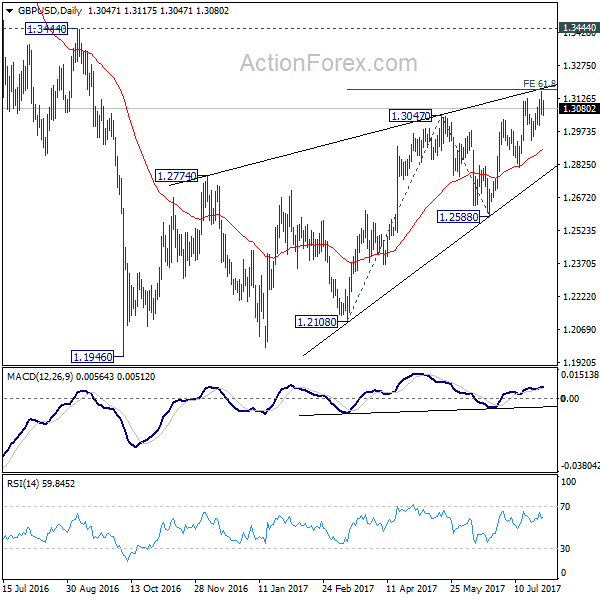

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3023; (P) 1.3091; (R1) 1.3131; More...

No change in GBP/USD's outlook. Price actions from 1.1946 is seen as a corrective pattern. Considering bearish divergence condition in 4 hour MACD, we'd stay cautious on strong resistance from 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 to limit upside. Break of 1.2932 support will be the first sign of reversal and will turn bias to the downside to target 1.2588 key support next. Though, sustained break of 1.3168 will bring further rise towards 1.3444 before completing the correction.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is expected, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

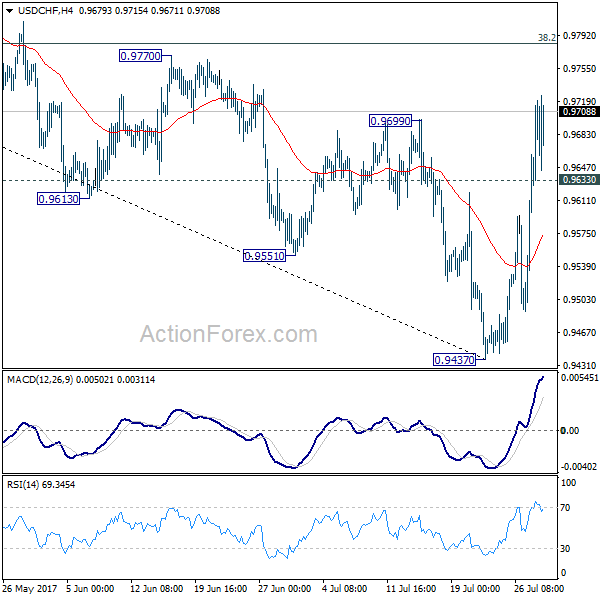

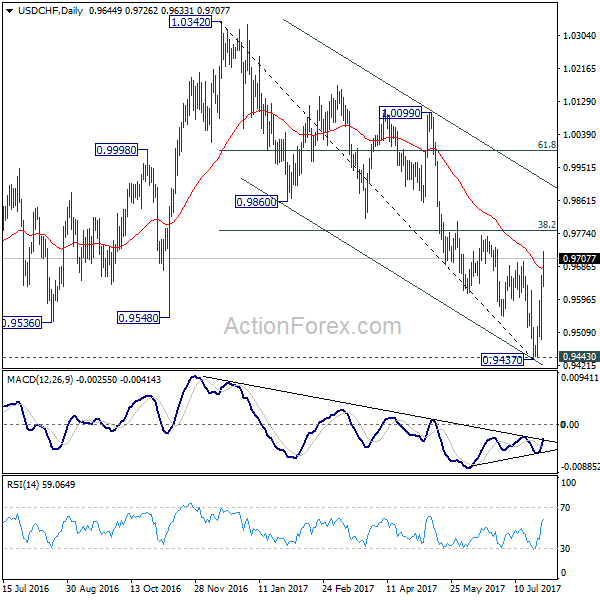

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9538; (P) 0.9600; (R1) 0.9709; More...

Intraday bias in USD/CHF remains on the upside for the moment. The pair should have bottomed at 0.9437 after defending 0.9443 key support level. This is also supported by bullish convergence condition in daily MACD. Further rise should be seen to 38.2% retracement of 1.0342 to 0.9437 at 0.9783 first. Break will target channel resistance (now at 0.9912). On the downside, below 0.9633 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, current development argues that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rising level. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996.

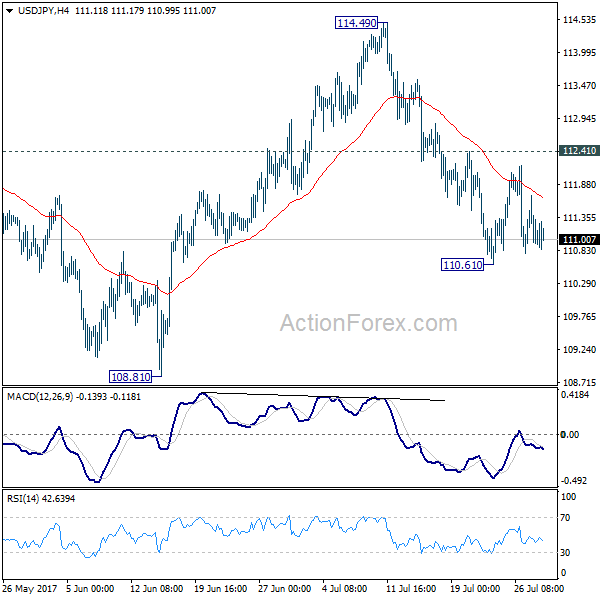

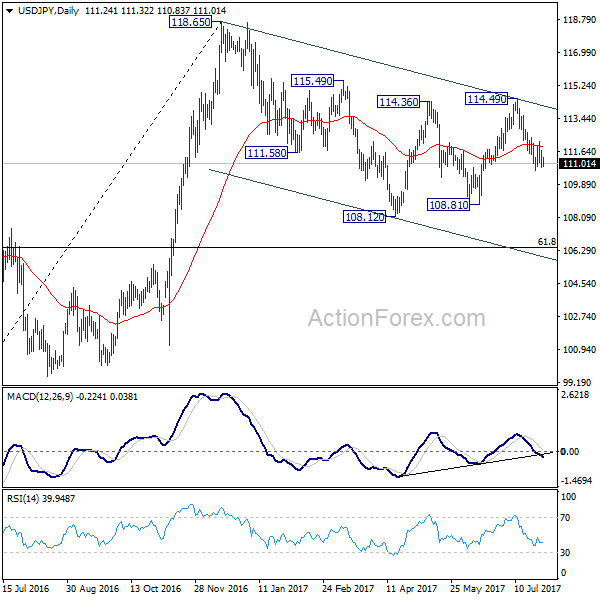

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.79; (P) 111.25; (R1) 111.72; More...

USD/JPY is still bounded in consolidation above 110.61 temporary low and intraday bias remains neutral. As long as 112.41 resistance holds, further decline is expected. Break of 110.61 will target 108.81. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, break of 112.41 will dampen this bearish view and turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.