Sample Category Title

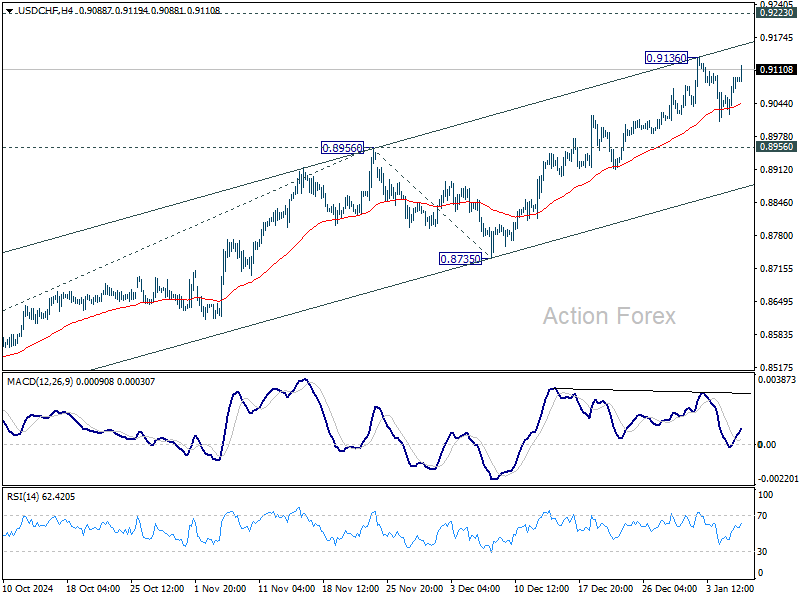

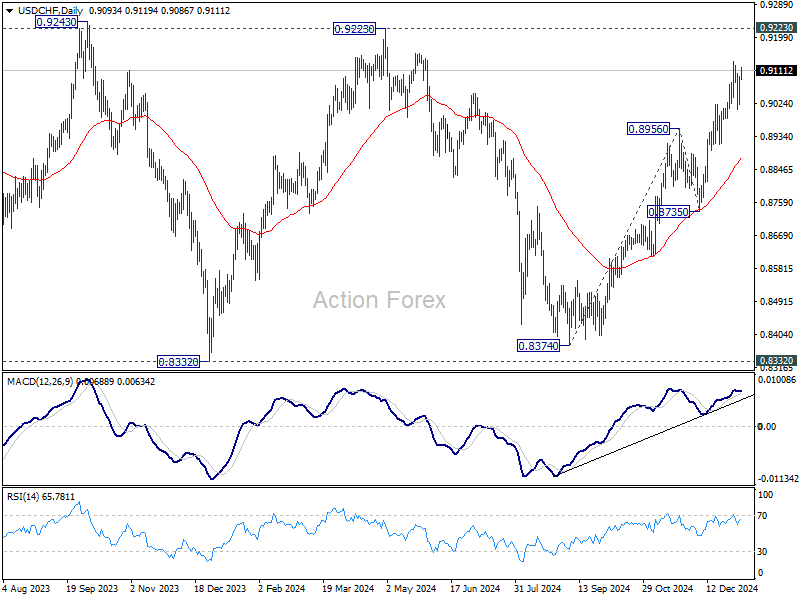

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9047; (P) 0.9073; (R1) 0.9122; More…

Intraday bias in USD/CHF stays neutral for the moment, and more consolidations could be seen below 0.9136 resistance. But further rally is expected as long as 0.8956 resistance turned support holds. Above 0.9136 will resume the rally from 0.8374 to 0.9223 key resistance next. However, firm break of 0.8956 will turn bias back to the downside for 55 D EMA (now at 0.8879).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

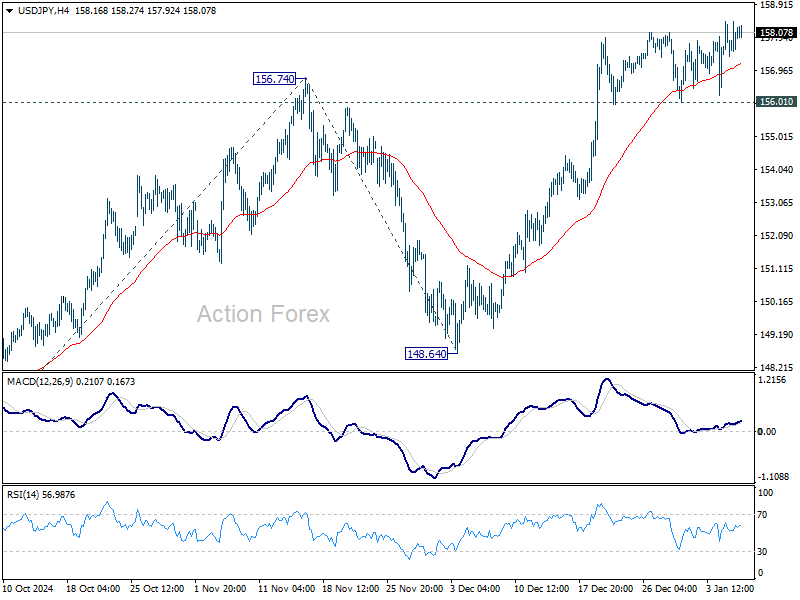

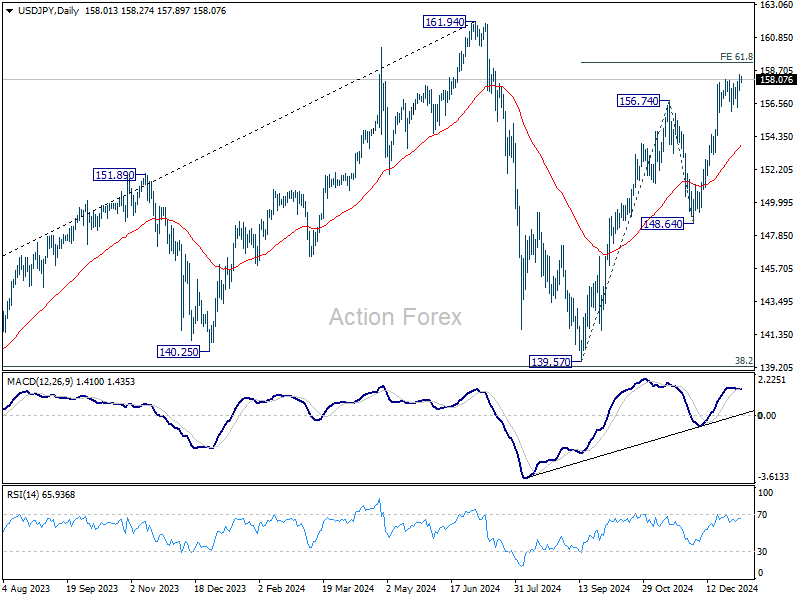

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.49; (P) 157.96; (R1) 158.54; More...

No change in USD/JPY's outlook and intraday bias stays on the upside for 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will extend the rally from 139.57 to target 161.94 high. However, break of 156.01 support will indicate short term topping, likely with bearish divergence condition. Intraday bias will then be back on the downside for 55 D EMA (now at 153.82) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

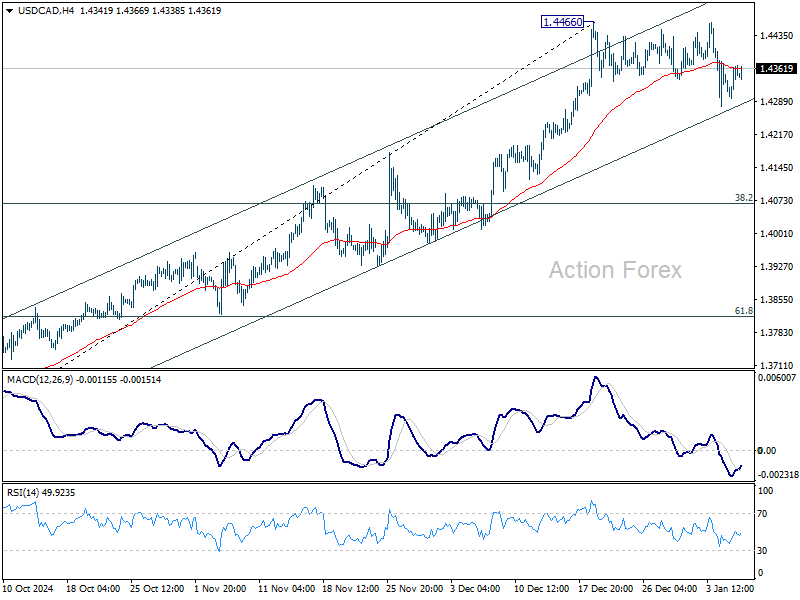

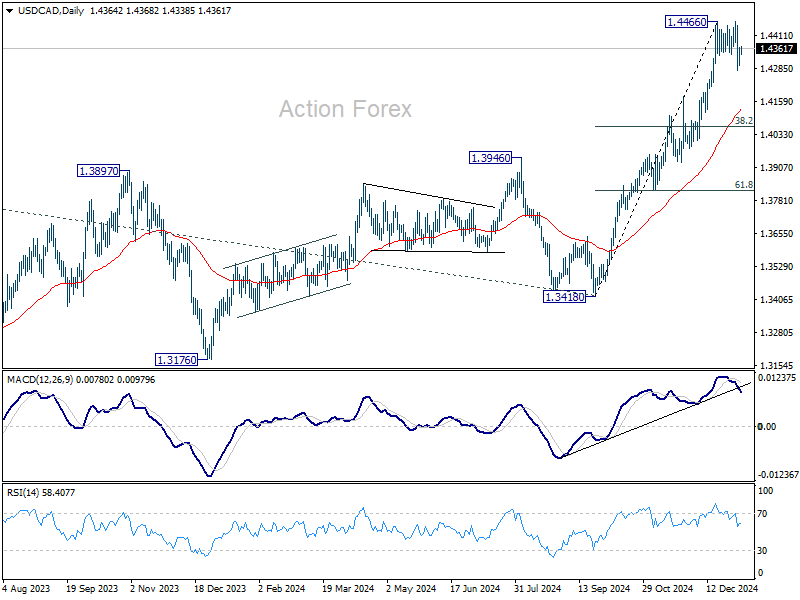

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4322; (P) 1.4347; (R1) 1.4397; More...

Intraday bias in USD/CAD stays mildly on the downside, as pull back from 1.4466 support might still extend. Deeper fall could be seen to 55 D EMA (now at 1.4130). But downside should be contained by 38.2% retracement of 1.3418 to 1.4466 at 1.4066 to bring rebound. For now, risk of more consolidations remains as long as 1.4466 holds, in case of recovery.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

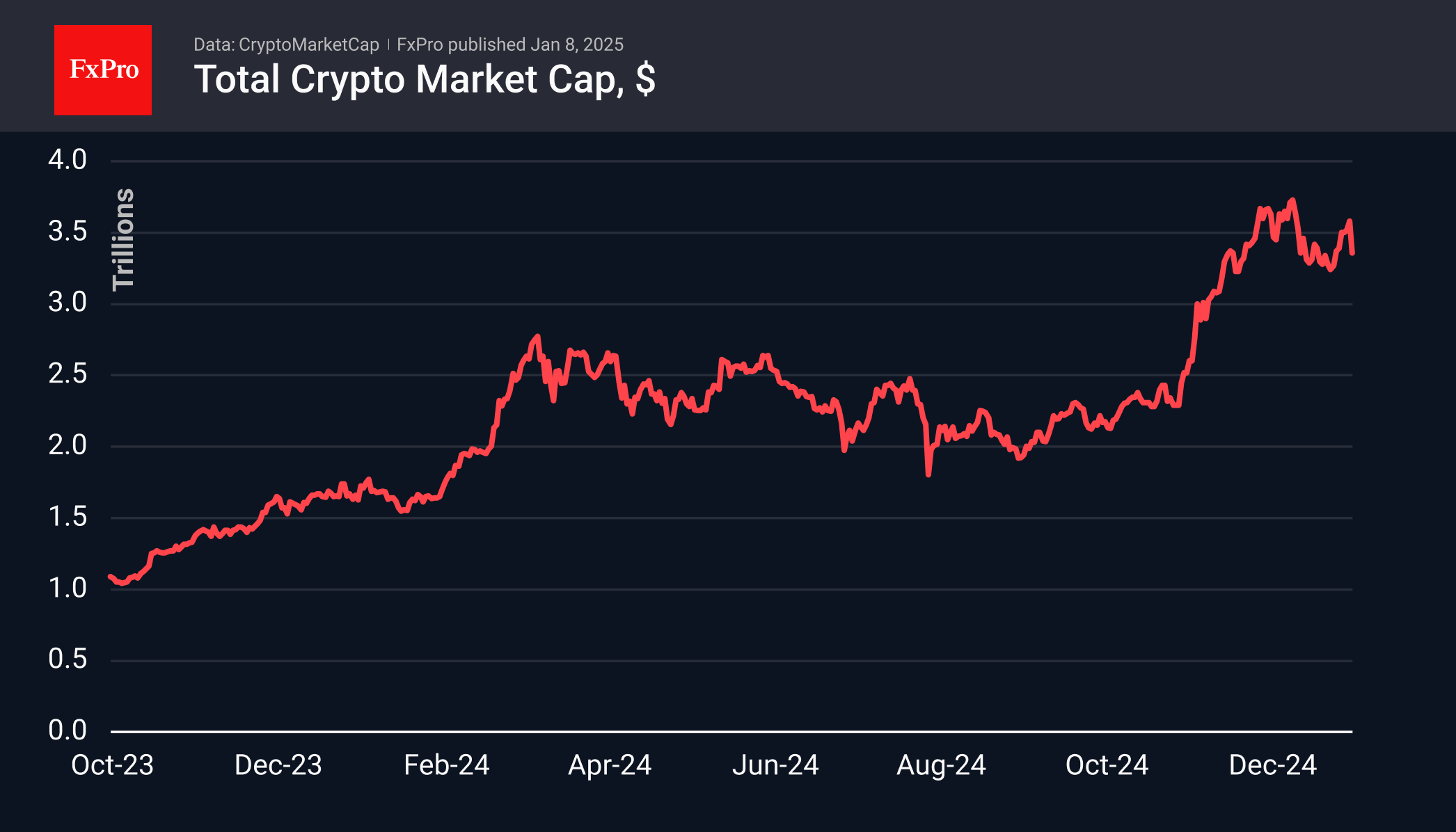

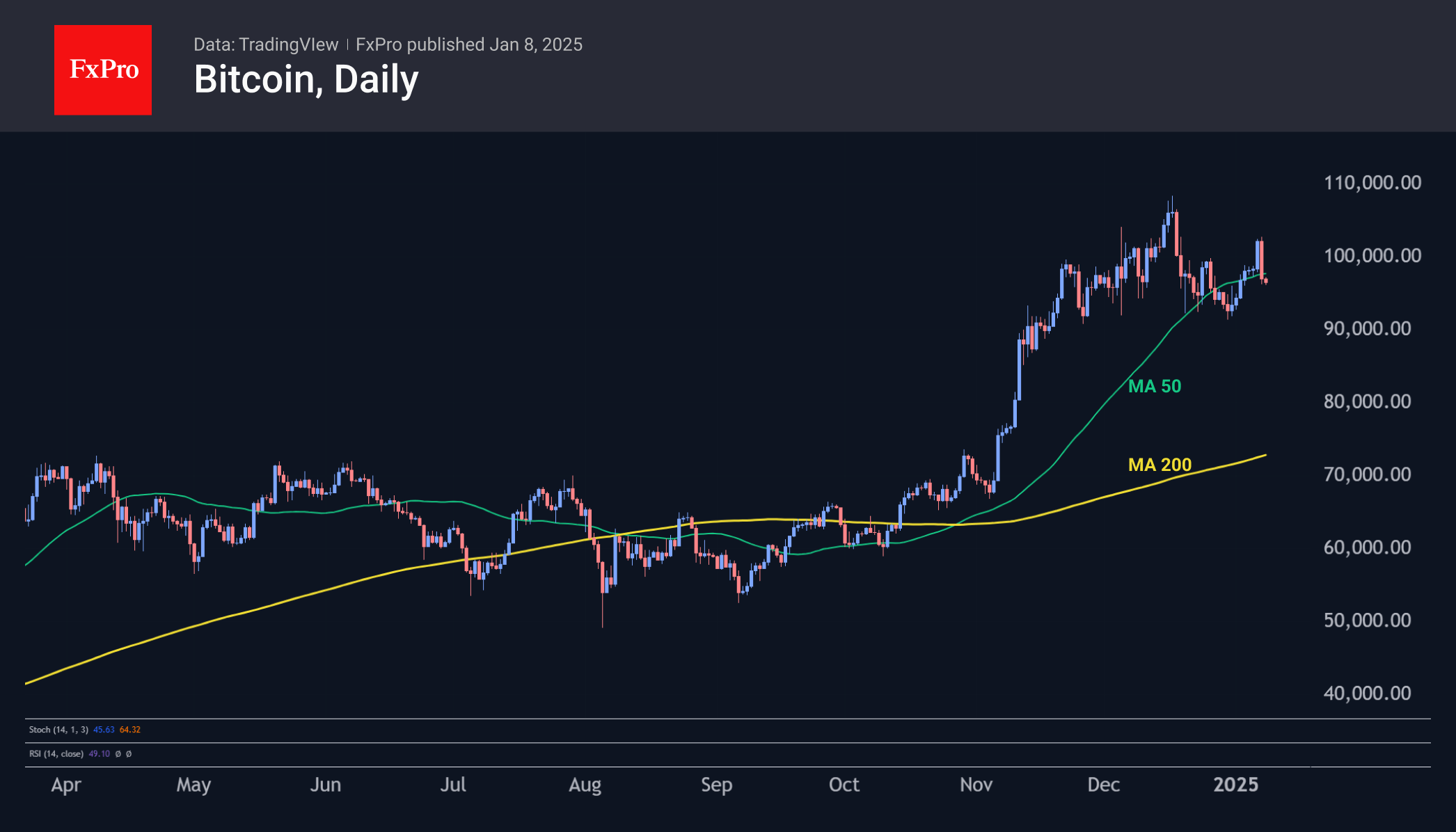

Crypto Stumbles on the Upswing

Market Picture

The cryptocurrency market took a hit on Tuesday as strong US data brought speculation of tighter monetary policy back into play. As a result, crypto market capitalisation lost over 6.2% in 24 hours by the start of active trading in Europe on Wednesday. US President-elect Trump continues with his passages about Canada as the 51st state, buying Greenland, and regaining control over the Panama Canal, which increases the pull from risk assets, hurting Bitcoin, among others.

The market is still bullish, but temporarily, investors have become more cautious, preferring to lock in profits quickly.

Bitcoin has lost about 7%, coming close to $96,000. This is a desperate attempt to bring the price back below its 50-day moving average. Failure to consolidate above $102,000 had short-term speculators looking for a reason to sell, and they quickly found one. That said, the positivity of the data and Trump’s outbursts are not news and do not drastically change expectations.

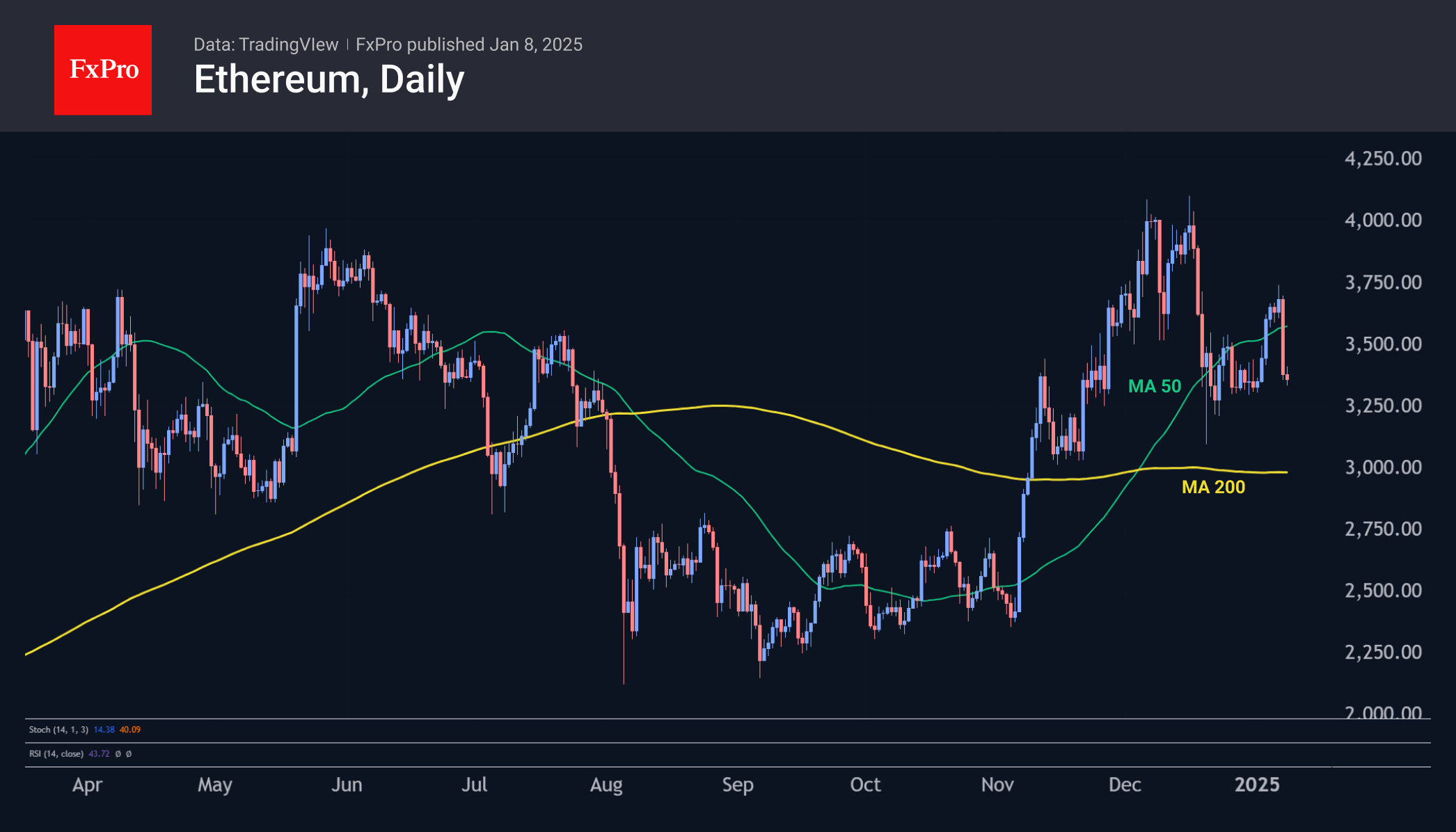

Ethereum erased all of its gains since the start of the year, pulling back to $3,360 during Tuesday’s sell-off. The sharp decline has brought the price back deep under its 50-day moving average, raising concerns about the near-term outlook.

News Background

Tech analyst Ali Martinez notes that Bitcoin’s important support zone is in the $95,400 to $98,400 range, where 1.77 million addresses have purchased more than 1.53 million BTC.

Glassnode draws attention to the decline in the funding rate to neutral levels below 0.01%. This suggests cautious positioning as speculators show limited willingness to pay premiums for long positions.

Ex-BitMEX CEO Arthur Hayes expects the bull rally in the crypto market to end in mid-March, after which the market will firmly correct. In his opinion, dollar liquidity will begin to decline in March and will resume growth no earlier than the third quarter.

The head of the Czech Central Bank suggested considering the possibility of using Bitcoin as part of a strategy to diversify the bank’s reserves. Still, it explained that there are no plans to acquire any cryptocurrency yet. In December, the country passed a law that exempts hodlers from capital gains tax when holding BTC for more than three years.

Pierre Poilievre, a Bitcoin supporter who has openly declared his support for BTC and blockchain technology, may become Canada’s new prime minister.

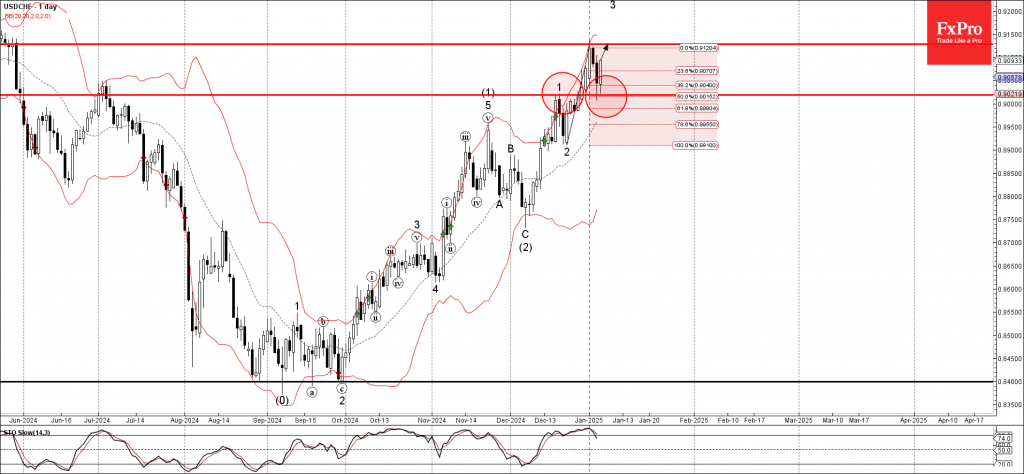

USDCHF Wave Analysis

- USDCHF reversed from support zone

- Likely to rise to support level 0.9130

USDCHF currency pair recently reversed up from the support zone located between the support level 0.9020 (former top of the impulse wave 1 from December) and the 50% Fibonacci correction of the upward impulse from last month.

The upward reversal from this support zone continues the active minor impulse wave 3 of the intermediate impulse wave (3) from December.

Given the persistent daily uptrend and the bullish US dollar sentiment, USDCHF currency pair can be expected to rise to the next resistance level 0.9130 (which reversed the earlier upward impulse).

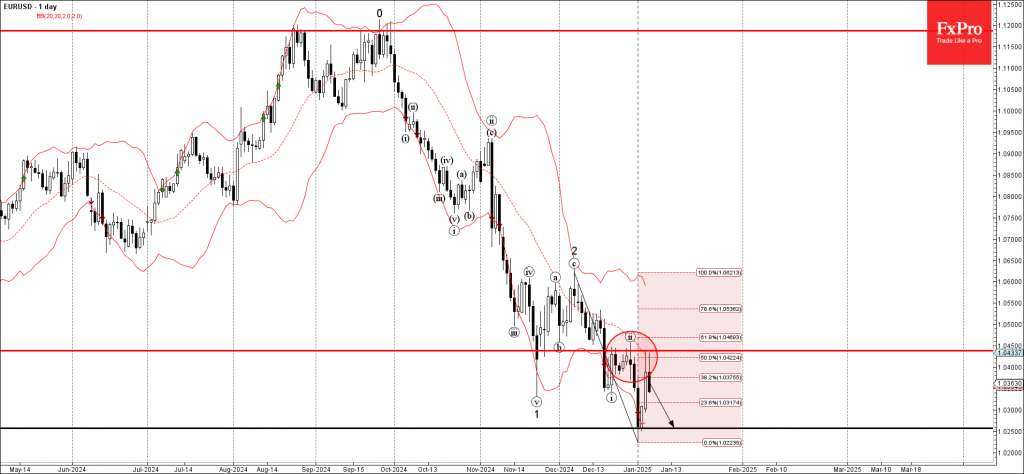

EURUSD Wave Analysis

- EURUSD reversed up from resistance zone

- Likely to fall to support level 1.0255

EURUSD currency pair recently reversed down from the resistance zone set between the resistance level 1.0435 (which has been steadily reversing the price from the end of December), 20-day moving average, 50% Fibonacci correction of the downward impulse from December.

The downward reversal from this resistance zone continues the active minor impulse wave 3 from the start of last month.

Given the clear daily downtrend, EURUSD currency pair can be expected to fall to the next support level 1.0255 (which reversed the price sharply at the start of January).

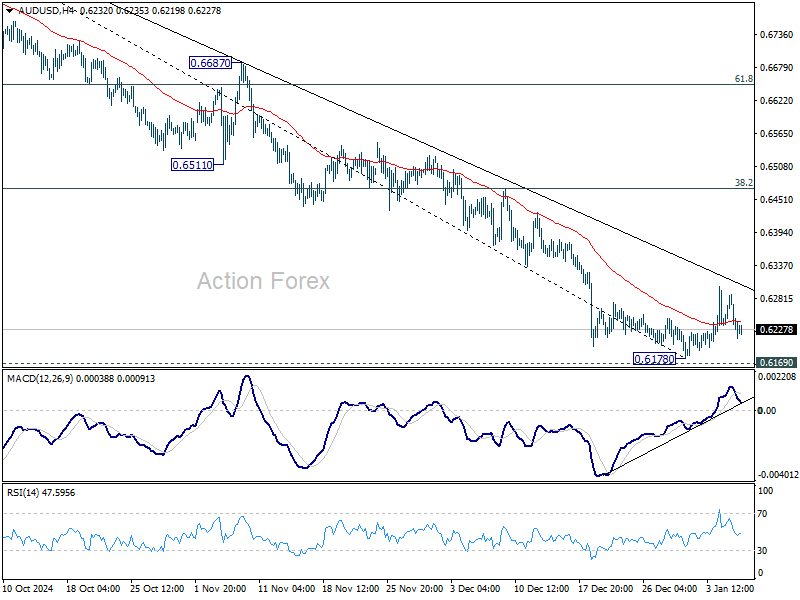

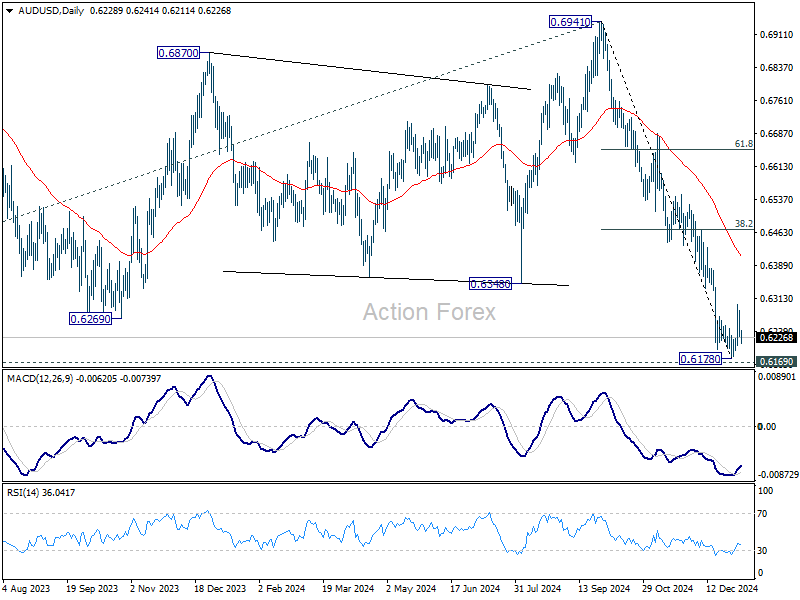

AUD/USD Daily Report

Daily Pivots: (S1) 0.6210; (P) 0.6249; (R1) 0.6270; More...

Intraday bias in AUD/USD is turned neutral with current retreat. Consolidation from 0.6178 could still extend with another rise to 55 D EMA (now at 0.6416). But near term outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6178 at 0.6469. Nevertheless, firm break of 0.6169 key support will confirm larger down trend resumption.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006, and could have completed at 0.6941 already. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.

Dollar Regains Ground Ahead of FOMC Minutes, Aussie Weakens on RBA Cut Prospects

Dollar regained some traction overnight, supported by strong services sector data that bolstered expectations for Fed to hold interest rates steady this month. Fed fund futures now imply a 95% probability of no rate cut in January, up from 90% last week. The upbeat economic performance placed moderate downward pressure on both equities and bonds, as markets reassess the Fed's path. Attention now turns to Friday’s non-farm payroll report, which could finalize the case for the Fed’s January decision and shift market focus toward policy moves for the remainder of the year.

The upcoming release of FOMC December meeting minutes today is another critical event for traders. At the meeting, policymakers projected a median year-end federal funds rate target of 3.75%–4.00%, reflecting a 50bps reduction from current levels. The minutes are expected to provide valuable insight into Fed’s internal deliberations, shedding light on whether risks favor a steeper or shallower easing path in 2025. This will be key in shaping market expectations for monetary policy throughout the year.

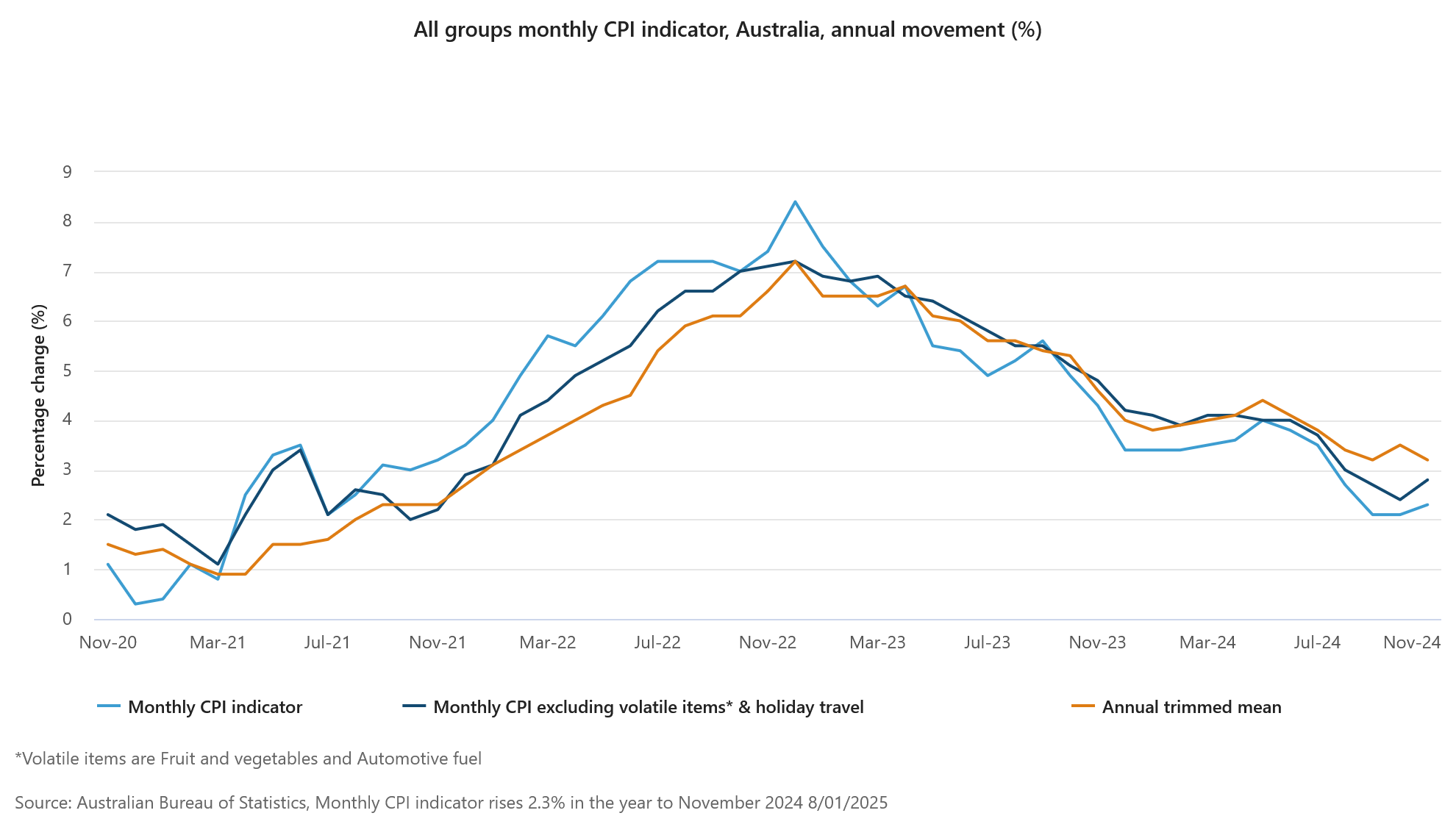

Elsewhere, Australian Dollar is under pressure today following release of November monthly CPI data. While headline inflation ticked higher due to the fading impact of energy rebates, the slowdown in trimmed mean CPI—a key measure of core inflation—provided welcome evidence of disinflation. Australian Treasurer Jim Chalmers highlighted the notable improvement in services inflation, which fell from 4.8% to 4.2%. Market expectations for an RBA rate cut in February have now increased to 60%-75%, with traders leaning toward an earlier start to the central bank’s easing cycle, rather than the May timeline initially anticipated.

For the week so far, most major currency pairs remain confined within last week's ranges. Yen, Swiss Franc, and Dollar are the weakest performers, while Canadian Dollar, British Pound, and New Zealand Dollar are showing relative strength. Euro and Australian Dollar are trading in the middle of the pack.

Technically, overall risk sentiment is a major focus for the rest of the week, for their reactions to FOMC minutes and NFP. NASDAQ is currently extending the consolidation pattern from 20204.58. Deeper retreat cannot be ruled out, but outlook will stay bullish as long as 18671.06 resistance turned support holds. The record-run up trend is expected to resume at a later stage.

Australian monthly CPI rises to 2.3%, but easing core pressures offer RBA relief

Australia's monthly CPI rose from 2.1% yoy to 2.3% yoy in November, slightly above market expectations of 2.2%. Inflation excluding volatile items and holiday travel jumped from 2.4% yoy to 2.8% yoy. However, trimmed mean CPI, a measure closely watched by RBA, declined from 3.5% to 3.2%, signaling some relief in underlying inflationary pressures.

The rise in CPI was influenced by the reduced impact of government electricity rebates compared to previous months. According to Michelle Marquardt, head of prices statistics at ABS, Electricity prices were -21.5% lower in November, compared to a -35.6% annual fall in October." Excluding government rebates, electricity prices would have declined by only -1.7% over the same period.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6210; (P) 0.6249; (R1) 0.6270; More...

Intraday bias in AUD/USD is turned neutral with current retreat. Consolidation from 0.6178 could still extend with another rise to 55 D EMA (now at 0.6416). But near term outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6178 at 0.6469. Nevertheless, firm break of 0.6169 key support will confirm larger down trend resumption.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006, and could have completed at 0.6941 already. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.

Australian monthly CPI rises to 2.3%, but easing core pressures offer RBA relief

Australia's monthly CPI rose from 2.1% yoy to 2.3% yoy in November, slightly above market expectations of 2.2%. Inflation excluding volatile items and holiday travel jumped from 2.4% yoy to 2.8% yoy. However, trimmed mean CPI, a measure closely watched by RBA, declined from 3.5% to 3.2%, signaling some relief in underlying inflationary pressures.

The rise in CPI was influenced by the reduced impact of government electricity rebates compared to previous months. According to Michelle Marquardt, head of prices statistics at ABS, Electricity prices were -21.5% lower in November, compared to a -35.6% annual fall in October." Excluding government rebates, electricity prices would have declined by only -1.7% over the same period.

USD Against G10 Peers Driven by Risk-Off More Than Anything Else

Markets

Core bond yields extended their December surge with the long end once again taking the lead. A strong first batch of US economic data did the trick. November JOLTS job openings snapped back to above 8 million and a strong headline services ISM for December was coupled with a sharp rise in the prices paid subseries to the highest since March 2023. The US 2-yr yield added 1.7 bps with money markets gently pushing the next Fed cut further out in time to 2025H2. Yields in the 10-30-yr bucket rose 5.5-6.4 bps. The 10-yr tenor attacked the lower bound of the 4.68-4.73% resistance band. The $39 bln 10-yr auction yesterday produced a minimal tail with a lower bid-cover than the previous ones. European rates joined the bear steepening move with changes between +0.2 (2-yr) to +5.4 bps (30-yr) in Germany. European CPI printed bang in line with expectations, 2.4% y/y and 2.7% y/y for headline and core respectively, and final December PMIs enjoyed some marginal upward revisions compared to the flash release. UK gilts underperformed strongly. Net daily changes varied between 3.8 (2-yr) and 7.3 (10-yr) bps. The 30-yr year added 6.7 bps to hit a new 27-yr high. The same-dated auction yesterday tailed slightly and drew the lowest demand since December 2023. It suggests investor caution for upcoming bond supply after the Labour government’s “one of the largest fiscal loosenings in recent decades” (dixit OBR) presented in October resulted in a near-record £297 bn of planned government bond sales this year. The UK serves as a reminder to other governments in Europe, the US and elsewhere of a fundamentally changed interest rate environment that isn’t as forgiving for huge deficits and massive borrowing as the ZIRP/NIRP one. It’s central in our view for structurally higher long-term bond yields. From a shorter-term point of view, today’s economic calendar may further support the case as well with the ADP job report and jobless claims scheduled for release in the US. They come ahead of Friday’s more important officials payrolls report. Assuming markets this early in the year are not eager to fully let go on some additional Fed easing in 2025 it is the long end that remains the most vulnerable. The modest dollar appreciation yesterday (EUR/USD 1.034, DXY 108.54) reveals that this does not necessarily supports the US currency. We think USD against G10 peers was in fact driven by the risk-off more than anything else. Additionally, the battered euro’s downside is finally looking better protected. We feel a lot of negatives have been priced in by now. The bar for euro area money markets to price in more ECB easing (100 bps this year) is rising. EUR/USD is technically still in danger though with the recent low around 1.0226 acting as key support.

News & Views

Real Indian GDP growth for FY 2024-25 is estimated at 6.4% compared to the 8.2% provisional estimate in FY 2023-24, the statistics ministry reported. The growth deceleration in the 2024-25 FY is mainly due to a developing decline in government capital investments. At the same time private consumption expenditure is expected accelerate from 4.0% to 7.3%. Government consumption also is seen rising from 2.5% to 4.1%. Real GVA of agriculture and allied sector has been estimated to grow by 3.8% during 2024-25 as compared to the growth of 1.4% witnessed in FY 2023-24. Real GVA of ‘construction’ and ‘financial, real estate & professional services’ has been estimated to observe good growth rates of 8.6% and 7.3%, respectively during the FY2024-25, the ministry Statement reported. The Indian rupee this morning is setting an all time record low against the dollar in the USD/INR 85.84 area.

The Australian Bureau of statistics reported monthly CPI for November to have risen to 2.3% from 2.1% in October. However, the head of ABS price statistics in a comment indicated that the rise was in part due to timing of electricity rebates. The underlying inflation figure showed a mixed picture. The CPI excluding volatile items and holiday travel rose 2.8% in the 12 months to November, compared to a 2.4% rise in the 12 months to October. This rise was also mainly driven by changes in electricity prices. Annual trimmed mean inflation was 3.2% in November, down from 3.5% in October. The latter is an important pointer in the RBA’s inflation assessment and as such is moving closer to the RBA’s 2-3% inflation target. The RBA has its first policy meeting on February 17-18. After holding its policy rate unchanged at 4.35% since November 2023, markets now see a chance of about 75% of an inaugural 25 bps rate cut in February. The Ausie dollar, which has been under pressure from a strong US dollar of late, only showed a limited reaction to the data. At AUD/USD 0.6235, it trades close to recent lows (0.6180 area).