Sample Category Title

SPX & Nasdaq 100 React to Strong US Data: Rate Cut Outlook Shifts

- Stronger-than-expected US economic data (JOLTs job openings and ISM Services Index) weigh on US Indices.

- Markets exhibited sensitivity to monetary policy expectations and potential volatility, with sector performance varying.

- Technical analysis of the S&P 500 suggests a range-bound market with key support and resistance levels identified.

- Upcoming non-farm payrolls and Fed meeting minutes releases are expected to further influence market volatility.

US Indices and stocks are on course to end two consecutive days of gains following a batch of strong US data. The data fueled speculation that any potential rate cuts in 2025 would come later in the year, evidenced by the fact that traders no longer fully price in a Fed rate cut before July.

US ISM Services and JOLTs Data Smash Estimates

The US Labor Department reported 8.098 million job openings in November, higher than the 7.7 million economists surveyed by Reuters had expected.

Additionally, an ISM survey showed that services activity in December remained strong with a reading of 54.1, beating the expected 53.3 and improving from the previous month.

The robust data has added to expectations around rate cuts from the Federal Reserve this year.

Markets Remain Sensitive to Monetary Policy Expectations

If today’s data confirmed anything it is that markets will remain sensitive to changes in monetary policy expectations moving forward. There is also the belief that extremely high valuations have left markets and US stocks more sensitive to volatility shocks.

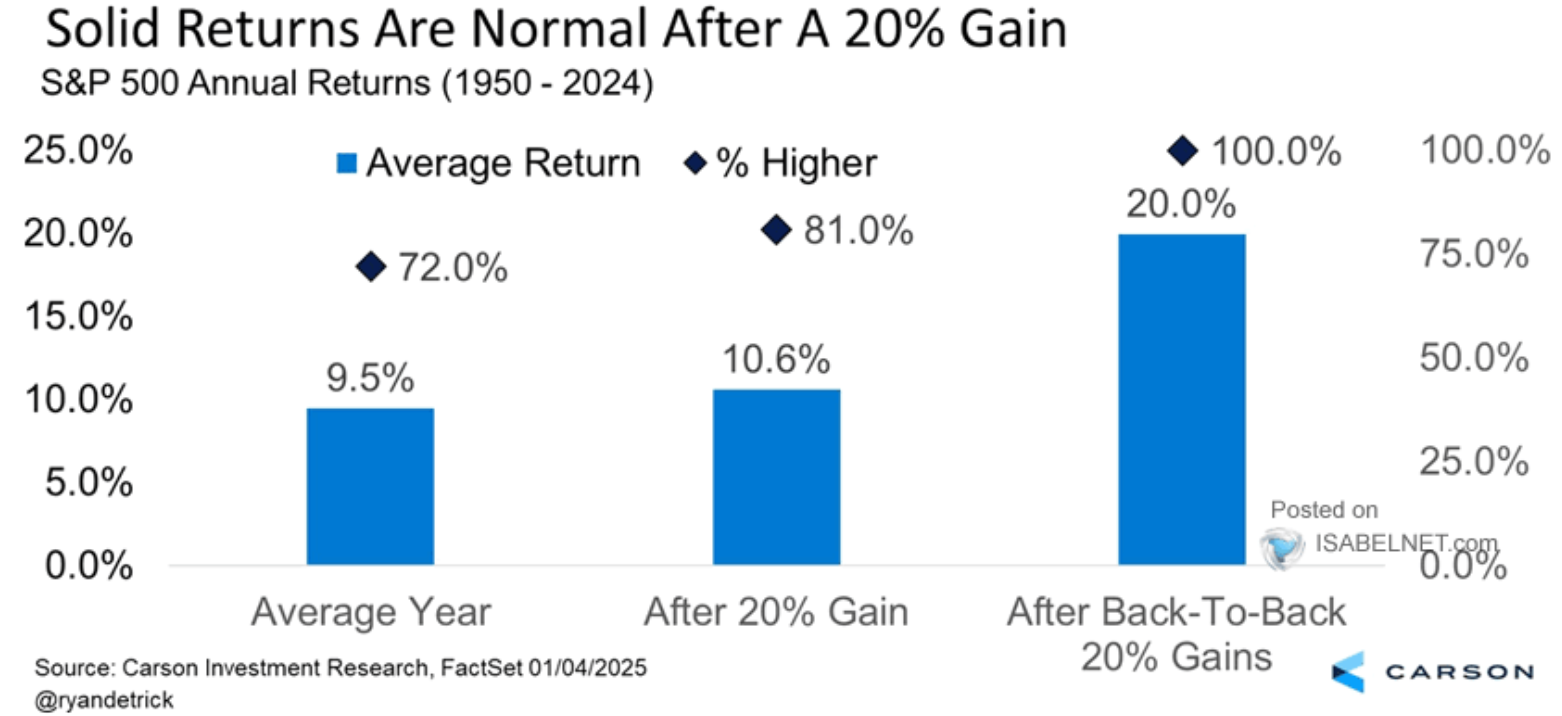

However despite these high valuations and a stellar 2024, the election of Donald Trump as well as historical data appear to support further gains.

Bulls rejoice when the S&P 500 posts a 20% annual return. Historically, the following year has seen positive returns 81% of the time, with an average gain of 10.6% since 1950.

Source: Isabelnet, Carson Research (click to enlarge)

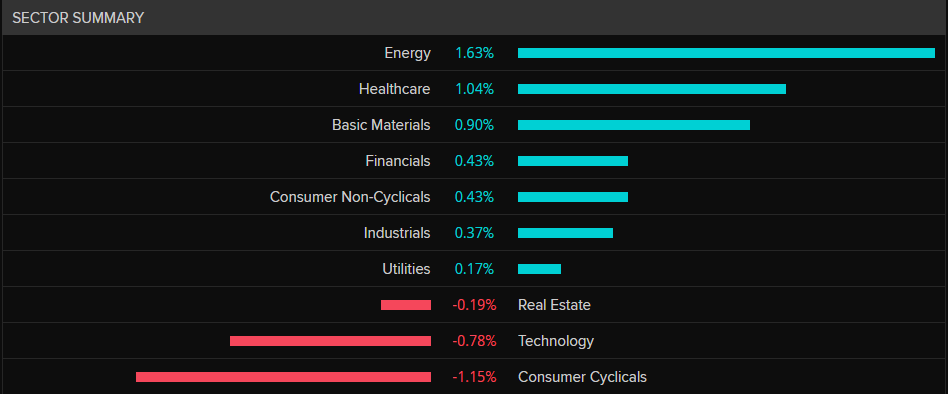

Winners and Losers

Looking at the sector performance today as well as individual winners and losers thus far, healthcare stocks saw a 1% rise, leading gains in the S&P 500 sectors. Vaccine makers like Moderna, Novavax, and Pfizer jumped due to rising worries about bird flu.

Tesla shares fell 2.9% after BofA Global Research downgraded the stock from “buy” to “neutral,” which also impacted the consumer discretionary sector.

Micron Technology rose 5% following comments from Nvidia’s CEO, Jensen Huang, that the company is supplying memory for Nvidia’s new GeForce RTX 50 Blackwell gaming chips.

Big banks performed well, with Citigroup increasing by 0.3% after positive coverage from Truist Securities, and Bank of America gaining 0.6% thanks to favorable ratings from several analysts.

Source: LSEG (click to enlarge)

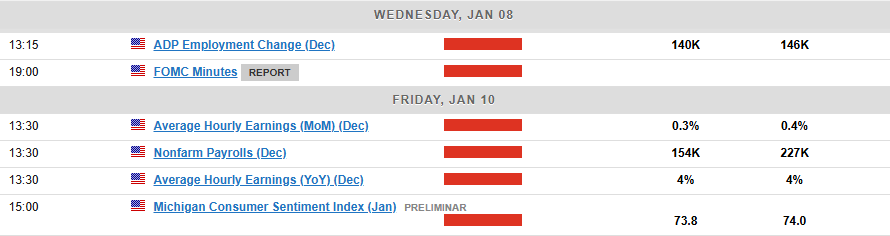

The Week Ahead

This week, the main highlights are the important non-farm payrolls report and the release of the Fed’s December meeting minutes due on Wednesday and Friday respectively.

Judging by today’s reaction, volatility seems to be a given. The bigger question right now is whether any moves to the downside remain sustainable or are they just opportunities for potential longs to get involved?

Technical Analysis

S&P 500

From a technical standpoint, the S&P 500 remains in somewhat of a range having broken the previous bullish structure that was in play.

The overall price action picture does remain bearish following the daily candle close on December 18, 2024. Since then the Index has printed a lower high but failed to print a lower low.

This could be seen as a sign of the bullish pressure and overall buoyant mood toward US stocks in general.

More recently the index has failed to break the 6025 swing high or the 5828 swing low, keeping it confined in a +- 100 point range.

A break of the swing high at 6025 could facilitate a move toward the all time just above and potentially the next key area on the upside around 6170. (based on a triangle pattern breakout yet to be fulfilled).

A continuation of today’s bearish move may find support at 5910 and 5828 which rests just above the 100-day MA, making this a key area of support.

A break of this key support level could pave the way for a deeper retracement toward the 5700 swing low from October 31, 2024.

S&P 500 Daily Chart, January 7, 2025

Source: TradingView (click to enlarge)

Support

- 5910

- 5828

- 5700

Resistance

- 6000

- 6025

- 6090

Euro Rally Fizzles, Eurozone CPI Climbs to 2.2%

The euro is slightly lower on Tuesday after rallying 1.2% over the past two trading sessions. In the North American session, EUR/USD is currently trading at 1.0363, down 0.25% on the day.

Eurozone, German CPI rises in December

Eurozone inflation accelerated for a third successive month, climbing to 2.4% y/y in December, up from 2.2% in November and in line with the market estimate. Energy prices increased for the first time since July and services inflation rose to 4% from 3.9%, double the European Central Bank’s target of 2%. The core rate remained unchanged at 2.7%, matching the market estimate.

In Germany, the eurozone’s largest economy, inflation jumped in December and was higher than expected. Annual inflation hit 2.6%, up from 2.2% in November and above the market estimate of 2.4%. Monthly, CPI rose to 0.4%, up sharply from -0.2% in November and above the market estimate of 0.3%. With inflation rising and economic activity struggling, there is a significant possibility of stagflation, which is a combination of slow economic growth and high inflation.

How will the ECB react to the latest inflation data? The ECB lowered rates by 25 basis points in December and is likely to continue trimming rates in early 2025. The deposit interest rate of 3% is still restrictive for the weak eurozone economy. The ECB could cut rates by 25-basis points at the next meeting on January 30.

The US economy is in good shape, buoyed by a robust services sector. The S&P Global Services PMI eased in December to 56.8, down from 58.5 in November. This was followed by the ISM Services PMI rose to 54.1 in December, up from 52.1 and above the market estimate of 53.3. This points to solid expansion in the services industry.

EUR/USD Technical

- EUR/USD is testing resistance at 1.0374. Above, there is resistance at 1.0453

- There is support at 1.0312 and 1.0233

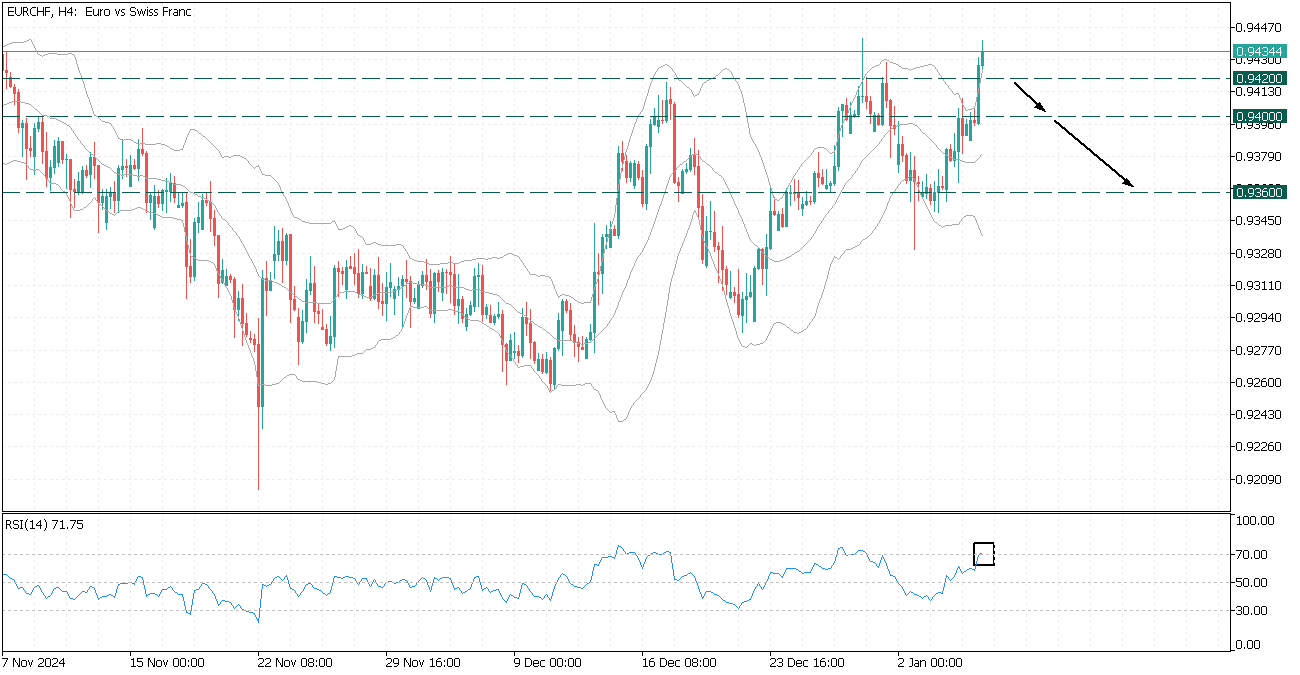

EURCHF: Counter-Trend Strategy

EURCHF, H4

EURCHF is rising and breaching above the upper Bollinger Band.

The RSI oscillator is in the oversold zone, giving a Counter-trend strategy set up on the chart, with a good opportunity to short the asset!

Consider a short trade on EURCHF on a consolidation below 0.9420 with the target at 0.9400 and 0.9360.

How Far Will They Go? China’s Outlook for 2025

Highlights

- At the Central Economic Work Conference, authorities said all the right things, pledging to deploy fiscal and monetary stimulus to boost domestic demand and create the conditions to develop a consumer-driven economy.

- However, the strategy behind fiscal stimulus thus far bears an eerie resemblance to Japan’s in the 1990s after the bursting of the asset bubble.

- Structurally stronger consumer demand in China would help rebalance the growth model and take pressure off authorities to provide repeated rounds of stimulus.

- To the extent Chinese authorities fall short, it would entrench excess capacity that would be a disinflationary force globally, while also weighing on sales and margins of multinationals operating in China. However, tit-for-tat escalation of tariffs and export restrictions risks creating a whipsaw effect on global prices.

China’s economy continues to contend with the ramifications of a housing market meltdown, decades of investment-driven growth, and a trade war with the U.S. that is set to re-accelerate. Faced with these headwinds, policymakers have recommitted to monetary and fiscal stimulus to boost domestic demand. This is critical for durable growth, but how the money is spent is almost as important as how much. To date, the strategies deployed by policymakers harken back to those in post-asset bubble Japan rather than the reforms and spending that have been called for. An extension of the approach employed thus far risks proving inadequate to materially lift China’s soft inflation or help reset the country on a sustainable growth trajectory.

For North American firms and households, the implications are two-fold; (1) the absence of domestic pricing power will likely imply margin compression and reduced profitability for foreign firms operating in China, and (2) the course of the trade war will determine if, and when, the global disinflationary force from China’s excess supply manifests.

The Base Case

We expect China’s growth to clock in at 4.8% in 2024, in line with the 5%-ish target set out by policymakers. Next year, authorities are likely to set a growth target of around 5%, along with an expansion in the fiscal deficit1. However, risks are tilted to the downside and our forecast is for a 4.7% expansion, a virtual repeat of this year’s performance, as the trade war with the U.S. gains steam. There is ample uncertainty around this forecast as the scale and scope of tariffs, along with the size of the policy response from China’s authorities, remains unknown.

Consumer spending has expanded well below its pre-pandemic pace (Chart 1). October’s retail spending figures were a welcome uptick as the latest round of stimulus measures (in part the cash-for-clunkers program for household appliances) helped lift spending, but November saw a give-back of some of the gains. Ample capacity remains, and with home prices continuing to correct (albeit at a slower pace2), consumer confidence is likely to be locked in the doldrums, resulting in a protracted recovery.

A soft outlook for household demand is the driving force behind our expectation for a near-absence of inflation in 2025. Weakness in indicators of consumers’ assessment of prospects add conviction to this view. Loan demand remains tepid, with new loan growth failing to gain traction in the months after interest rate cuts. This signals a preference towards paying down balances and rebuilding balance sheets (Chart 2). The upshot is that incremental increases in incomes would be diverted to balance sheet repair rather than capacity absorbing net-new demand.

Thus far, price growth has continued to cool with both economy-wide measures (the GDP deflator) and consumer prices in, or near, deflationary territory. The weak pricing environment is bleeding through to inflation expectations, measures of which have been on a downward trajectory for months (Chart 3).

The risk is that this spirals into a deflationary trap, where falling prices create a self-reinforcing loop of delayed demand, increased savings, and further economic weakness. This would add further global disinflationary pressure, while also weighing on foreign firms’ investment returns in China.

The Trade War is About to Flare Up

The trade war between the U.S. and China never went away when the Biden administration took over in 2021. While rhetoric cooled, and U.S. allies were no longer overtly threatened with tariffs, restrictions on China’s access to critical U.S. components were ramped up and tariffs were kept in place.

We have already gotten a hint of how China will respond to additional tariffs. Using a set of new laws and regulations, authorities are now willing and able to target individual firms and limit supplies of key products to other countries. Authorities have used these powers to target companies with ties to the U.S. national security establishment3 and limit the availability of three critical minerals – germanium, gallium and antimony – driving up their prices. Moreover, straightforward tariffs on U.S. agricultural exports are now more feasible than in the past as China has diversified its import sources away from the U.S. in recent years. This allows for retaliatory tariffs while limiting damage to domestic consumers.

However, these present the worst-case scenario for the trade war. Chinese authorities will likely look to strike a delicate balance between trade retaliation to stand up for their interests and alienating foreign firms through actions perceived as unfriendly to businesses. The tradeoff is important as avoiding disorderly capital flight remains top-of-mind amid a tapering-off of foreign direct investment flows into the country (Chart 4) and the prospect of further yuan devaluation to combat tariff hikes4.

Worrisome Policy Parallels with Japan’s Fiscal Strategy from the 1990s

More fiscal and monetary stimulus is on the way5, but how it is implemented matters greatly for the economy. For this reason, Japan’s experience after the bursting of the asset bubble in the late 1980s is an interesting case study. The focus below is on the ineffectiveness of Japan’s fiscal policy, even though a multitude of factors weighed on growth over the following decade (including a liquidity trap, a credit crunch, and the Asian Financial crisis6).

First, and foremost, Japan’s policymakers remained committed to fiscal discipline7 at a time that growth slowed rapidly. Initial budgets were often not expansionary – and sometimes outright contractionary – only further loosening when the hoped-for growth failed to materialize8. This stop-start dynamic was found to increase uncertainty, undermining the hoped-for growth lift9. This bears an eerie similarity to China’s recent strategy of targeting a 3% deficit, and then making up ground later in the year by allowing it to increase (as in 2023), or through the ad-hoc issuance of special purpose bonds10.

Importantly, this incremental strategy looks set to extend into next year. The IMF’s projection for the Augmented Cyclically Adjusted Primary Balance (a measure of the deficit that includes borrowing from local government funds and strips out the effects of automatic stabilizers) showed that a remarkable degree of restraint was expected around mid-year when the Article IV consultation was done (Chart 5). Even with the new announcements at the Central Economic Work Conference, the official deficit target for 2025 is rumored to be roughly 4%, only moderately higher than the 3% target this year11. It was only later in the month that rumors of a 3 trillion yuan (2.4% of 2023 GDP) special bond issuance to fund consumption support, infrastructure, and bank recapitalization emerged12.

Secondly, Japan relied on local governments to deliver public investment projects, but cash-strapped and highly indebted localities chronically underspent, opting to not to invest in low-return public projects to deliver central government spending promises13. This mirrors the current situation in China where local level governments are operating under large debt burdens with limited revenues. Faced with fewer projects that can meet investment criteria14, and wary to add more debt amid falling land sales, they have not been fully using up their budgeted allotment of special purpose bonds.

The problem is that public investment forms an important avenue for the kind of “Real Water” measures that lift GDP. So, despite years of investment-driven growth eroding the marginal returns on new initiatives15,16, it still forms an important part of the policy prescription. For China, an opportunity exists to use the funds to facilitate the transition to a consumer-driven economy through investments to expand the social safety net.

Lastly, Japan’s announced stimulus was often not allocated to GDP boosting ventures (“Real Water” initiatives). Asset reshuffles to restore balance sheets were often lumped in with headline stimulus figures that, while serving a purpose, were not effective in creating net-new domestic demand and absorbing excess capacity. China faces a similar situation. For instance, the 10 trillion-yuan ($1.4 trillion) announcement for local government debt swaps is an important (and expensive) measure to bring relief to local level balance sheets17, and likely a necessary condition to get increased compliance with the aforementioned additional borrowing, but not stimulating net-new demand on its own.

The Good News

Policymakers continue to say all the right things. Monetary policy is going to be “moderately loose”, and authorities stressed the importance of spurring consumer demand at December’s Central Economic Work Conference (CEWC)18. An expansion of the evidently effective cash-for-clunkers program for consumer goods is in the cards. Rumors of a large special bond issuance (2.4% of 2023 GDP) to bankroll the scheme and fund strategic investments have also emerged in the past weeks19. Optimistically, reporting from the CEWC, contained language on solidifying the social safety net20. The effective expansion of social supports would help create room for the persistently high household savings rate to fall, a necessary condition for the sustainable rotation to a consumption led growth model.

All the focus on the consumer will be needed as the effectiveness of additional monetary stimulus is highly uncertain. Sinking credit demand suggests that looser monetary policy may have a small impact on growth as, even at lower rates, borrowers don’t see much upside to increasing leverage. That said, supporting asset prices to prevent a steep correction21 (likely in the hopes of propping up consumer sentiment and stimulating a wealth effect) is part of the stimulus playbook.

To avoid a credit crunch, capital buffers at major banks were proactively increased in September22, helping absorb some of the ongoing margin compression from a cut to existing mortgage rates and lower long-term rates. As major banks are relied upon to implement credit expansions23, preemptively shoring up balance sheets should help ease the burden of lending in a more challenging environment.

Lastly, at its Third Plenum in the summer, authorities began reforms to add more revenue levers for local governments. In particular, the gradual move to “pass collection power to local government”24 of excise taxes is an important transition to provide local government an alternative to land sales as a revenue source.

Bottom Line

At the CEWC, authorities said all the right things, pledging to deploy fiscal and monetary stimulus to boost domestic demand and create the conditions to develop a consumer driven economy. That’s all well and good, but now we need to see it in practice. The rumored expansion of the deficit to 4%, along with a 5% growth target for 2025 suggest that the piecemeal approach to policy will continue, with comprehensive reforms to bolster the social safety net and wean off the investment driven growth model being kicked further down the road.

Absent a coordinated fiscal and monetary impulse, domestic demand is likely to be insufficient to absorb the economy’s productive capacity. This means ongoing downward pressure on prices. This also implies exports will continue to be a key source of real growth, raising the risk of drawing the ire of trade partners that could be inundated with relatively inexpensive products. A tail risk is that severe trade retaliation from the U.S. and others results in a whipsaw effect on prices as tit-for-tat escalations results in China implementing severe export restrictions on critical components.

For the global outlook the implications are twofold. First, with or without new U.S. tariffs, the absence of a large stimulus effort means demand for commodity inputs is unlikely to surge. For global consumers of commodities, this provides an element of stability to the price outlook and thus global producer prices. Moreover, a steep devaluation of the yuan could make Chinese exports relatively cheaper, adding another disinflationary force on input prices.

Secondly, for North American firms with substantial investments in China, the downbeat domestic situation could weigh on sales activity and investment returns. For some perspective, Canadian multinational enterprises reported sales equivalent to almost 0.7% of GDP in China in 2023. U.S. data are slightly more lagged, but majority owned affiliates reported sales equivalent to 1.9% of GDP in 2022. Moreover, with trade tensions escalating, uncertainty about the prospective returns on hundreds of billions of dollars of assets in China increases.

So, now we wait. A concerted and coordinated approach to stimulus could lift China’s prospects for 2025 and beyond, facilitating the rotation to a consumer driven economy. Much like in the U.S., the decisions by key policymakers in the coming months could have widespread ramifications.

End Notes

- Reuters (Dec. 17, 2024) “Exclusive: China Plans Record Budget Deficit of 4% of GDP in 2025, Say Sources” https://www.reuters.com/markets/asia/china-plans-record-budget-deficit-4-gdp-2025-say-sources-2024-12-17/

- Reuters (Dec. 16, 2024) “China Sees Slowest Home Price Decline in 17 Months Amid Signs of Stabilisation” https://www.reuters.com/markets/asia/china-new-home-prices-fall-slowest-pace-17-months-nov-2024-12-16/

- Bergen, M., M. Hawkins, G. Volpicelli (Dec. 9, 2024) “China is Cutting Off Drone Supplies Critical to Ukraine War Effort” Bloomberg News, https://www.bloomberg.com/news/articles/2024-12-09/china-is-cutting-off-drone-supplies-critical-to-ukraine-war-effort

- Reuters (Dec. 11, 2024) “Exclusive: Chinese Authorities Are Considering a Weaker Yuan as Trump Trade Risk Looms” https://www.reuters.com/markets/currencies/chinese-authorities-are-considering-weaker-yuan-trump-trade-risks-loom-sources-2024-12-11/

- Xinhua (Dec. 12, 2024) “China Holds Central Economic Work Conference to Make Plans for 2025”, State Council of The People’s Republic of China, https://english.www.gov.cn/news/202412/12/content_WS675ae633c6d0868f4e8ede69.html,

Reuters (Dec. 24, 2024) “Exclusive: China Plans Record $411 Billion Special Treasury Bond Issuance Next Year” Reuters News: https://www.reuters.com/world/china/china-plans-411-bln-special-treasury-bond-issuance-next-year-sources-say-2024-12-24/ - See. Kuttner, K., A. Posen, (2001) “The Great Recession: Lessons for Macroeconomic Policy from Japan” Brookings Papers on Economic Activity, Vol. 2001, No.2 (2001), pp. 93-160; Bayoumi., T. (2000) “The Morning After: Explaining the Slowdown in Japanese Growth” Post-Bubble Blues: How Japan Responded to Asset Price Collapse, Ch. 2, IMF; Ramaswamy, R., C. Rendu (2000) “Identifying the Shocks: Japan’s Economic Performance in the 1990s” Post-Bubble Blues: How Japan Responded to Asset Price Collapse, Ch. 3., IMF; Wilson, B.A. (2008) “Japanese Fiscal Policy: A Bridge to Nowhere” FOMC https://www.semanticscholar.org/paper/8.-Japanese-Fiscal-Policy%3A-A-Bridge-to-Nowhere-Wilson/913f5677e0125ce0fb8c6931271f984eb59e72b0

- Mulhleisen, M., (2000) “Too Much of a Good Thing? The Effectiveness of Fiscal Stimulus” Post-Bubble Blues: How Japan Responded to Asset Price Collapse, Ch. 6, IMF

- Mulhleisen, M., (2000) “Too Much of a Good Thing? The Effectiveness of Fiscal Stimulus” Post-Bubble Blues: How Japan Responded to Asset Price Collapse, Ch. 6, IMF

- Wilson, B.A., (Dec. 5, 2000) “Japanese Fiscal Policy – A Bridge to Nowhere” FOMC

- Posen, A. (1998) “Fiscal Policy Works When It Is Tried” Restoring Japan’s Economic Growth, Ch. 2, Institute for International Economics

- Reuters (Dec. 15, 2023) “China to Run Budget Gap of 3% of GDP in 2024, Issue Special Debt” https://www.reuters.com/world/china/china-run-budget-gap-3-gdp-2024-issue-special-debt-sources-2023-12-15/

- Reuters (Dec. 24, 2024) “Exclusive: China Plans Record $411 Billion Special Treasury Bond Issuance Next Year” Reuters News: https://www.reuters.com/world/china/china-plans-411-bln-special-treasury-bond-issuance-next-year-sources-say-2024-12-24/

- Ishii, H., E. Wada, (1998) “Local Government Spending: Solving the Mystery of Japanese Fiscal Packages” Peterson Institute for International Economics, Working Paper 98-5, https://www.piie.com/publications/working-papers/local-government-spending-solving-mystery-japanese-fiscal-packages

- Huang, T., (2024) “Lessons from China’s Fiscal Policy During the COVID-19 Pandemic” Peterson Institute for International Economics.

- Bloomberg News (Jul. 13, 2023) “Next China: Road to Nowhere” https://www.bloomberg.com/news/newsletters/2023-07-14/roads-to-nowhere-highlight-xi-s-stimulus-conundrum-next-china

- Ishii, H., E. Wada, (1998) “Local Government Spending: Solving the Mystery of Japanese Fiscal Packages” Peterson Institute for International Economics, Working Paper 98-5, https://www.piie.com/publications/working-papers/local-government-spending-solving-mystery-japanese-fiscal-packages

- Bloomberg News (Nov. 8, 2024) “China Unveils $1.4 Trillion Debt Swap, Saves Stimulus for Trump” https://www.bloomberg.com/news/articles/2024-11-08/china-unveils-839-billion-debt-swap-to-rescue-local-governments?srnd=homepage-asia

- Xinhua (Dec. 12, 2024) “China Holds Central Economic Work Conference to Make Plans for 2025”, The State Council of The People’s Republic of China, https://english.www.gov.cn/news/202412/12/content_WS675ae633c6d0868f4e8ede69.html

- Reuters (Dec. 24, 2024) “Exclusive: China Plans Record $411 Billion Special Treasury Bond Issuance Next Year” https://www.reuters.com/world/china/china-plans-411-bln-special-treasury-bond-issuance-next-year-sources-say-2024-12-24/

- Xinhua News Agency (Dec. 12, 2024) The Central Economic Work Conference was held in Beijing, and Xi Jinping delivered an important speech-Xinhuanet

- Reuters (Oct. 18, 2024) “China Rolls Out $112 Bln Funding Schemes to Bolster Stock Market” https://www.reuters.com/world/china/china-kicks-off-112-billion-funding-schemes-support-stock-market-2024-10-18/#:~:text=BEIJING%2FSHANGHAI%2C%20Oct%2018%20(,newly%2Dcreated%20monetary%20policy%20tools

- Bloomberg News (Sep. 23, 2024) “China to Add Capital at Big Banks for First Time in a Decade” https://www.bloomberg.com/news/articles/2024-09-24/china-to-boost-capital-at-mega-banks-for-first-time-in-a-decade

- Mak, R. (Nov. 11, 2024) “China Hands Banks Poor Stimulus Consolation Prize” Reuters, https://www.reuters.com/breakingviews/china-hands-banks-poor-stimulus-consolation-prize-2024-11-11/

- Xinhua (Jul. 26, 2024) “China to Accelerate Building a Fiscal System Compatible with Chinese Modernization” The State Council of The People’s Republic of China https://english.www.gov.cn/news/202407/26/content_WS66a389eec6d0868f4e8e97b2.html

US: ISM Services Index Shows Solid Growth to Close Out 2024, But Details Muddy

The ISM Services index rose 2.0 points to 54.1 in December, slightly ahead of the 53.5 consensus was expecting. However, only nine industries out of eighteen reported growth, five fewer than in October and November.

Business activity recovered last month, rising 4.5 points to 58.2, more than offsetting last month's pullback. Conversely, new order growth firmed only slightly (54.2 vs 53.7 last month) and was unable to match October's 57.4 reading.

The employment sub-index was virtually unchanged (51.4, -0.1 points) suggesting a modest expansion of payrolls. December was the third consecutive month of payrolls growth and the sixth of the year.

The prices paid sub-component jumped sharply (+6.2 points to 64.4) indicating that prices rose at their fastest pace since February of 2023.

Key Implications

A bit of a mixed bag to end the year from the ISM services index. The top line figure showed a healthy services sector with business activity posting a solid expansion and payrolls continuing to expand. However, the breadth of the expansion narrowed as only half of the industries reported growth for the month. It will also be worth keeping an eye on whether the jump in the prices paid component is a temporary blip like last January or the start of another march higher on input costs.

This report was better than expected, but heading into 2025 uncertainty is the name of the game. The prospect of port disruptions, new tariffs and possible changes to tax policy are all clouding the outlook. For policymakers, monitoring whether any of these factors are leading to sustained inflationary cost pressures will be top of mind.

Markets Reduce Rate Cut Expectations for 2025

- Central banks, especially the Fed, have toned down expectations of rate cuts, it seems at least partly reflecting concerns that the Trump administration will pursue more inflationary policies.

- Economic surprises have generally been to the positive side in the US and the negative side in the euro area, with concerns remaining elevated over the German economy and public finances in several countries, not least France.

- There are indications that consumer spending in Denmark might finally be increasing somewhat, and we also see more rays of light in other Nordic economies.

For anyone hoping for steep interest rate cuts, December’s central bank meetings were a disappointment. First, the ECB cut its policy rates by 25bp as largely expected, although some market participants had bet on a 50bp cut. A week later, the Federal Reserve cut the policy target range by 25bp accompanied by a clearly hawkish message. Apparently, policymakers put a lot of emphasis on the upside inflation risks stemming from the incoming US administration and their planned economic policies. Moreover, as market-based short-term inflation expectations have increased since the US election both in the US and in the euro area, it is clear investors consider the risks global, not only local.

The change in monetary policy outlook led to a repricing in the rate markets. Before the FOMC meeting, markets were pricing in almost three rate cuts by the Fed for 2025. Currently, it expects less than two. Similarly, before the ECB meeting, the central bank was priced to cut rates at least five times in 2025. Now, markets lean towards four cuts only. We think markets overestimate inflation risks, and underestimate risks to growth. The renewed market focus on inflationary risks largely builds on investor speculations around Trump’s future economic policies. But even if campaign promises are held, implementation of e.g. tariffs may not be as easy nor as fast as many expect, or their inflationary impact may not be significant.

Hence, we are still less concerned of a prolonged period of elevated inflation, and more concerned about growth continuing to surprise to the downside. The German economy remains in dire straits, a persistent headwind for euro area. European recovery would also benefit from a pickup in Chinese demand, but that in turn hinges on further fiscal stimulus by local authorities. The US economy remains relatively robust, and surprises have been on the positive side lately, but growth is likely to slow. For one thing, slowing immigration flow is one more negative risk to growth. We keep our call that the ECB will cut rates in every meeting until September, bringing the deposit rate to 1.5%. We revised our Fed call to reflect the hawkish views of the Committee members, and now expect quarterly cuts instead of cuts in every meeting, but we still expect them to land at 3.00% by March 2026.

The reduction in rate cut expectations has eroded stock market optimism lately. In Denmark, Novo Nordisk share price fell sharply as it occurred that its weight-loss pill may not be as effective as previously thought. The US dollar has remained bid and EUR/USD has declined to a two year-low below 1.03 level. While the weaker euro versus the dollar is a reflection of the diverging growth stories, it also compensates the European exporters for a large part for the negative impact from the potential US import tariffs.

As we enter 2025, we expect another eventful and potentially turbulent year. Economies continue to normalise, but growth might disappoint, and geopolitical risks remain. The incoming US administration has signalled they would continue to arm Ukraine, which is positive from Europe’s perspective, but momentum for ceasefire is also building both in Ukraine, and in Middle East. Alternative scenarios could be more upsetting for markets, for example if Israel is allowed to go “all in” after Iranian regime, all while the US support for Ukraine falters.

US ISM services rises to 54.1, robust activity and rising price pressures

US ISM Services PMI rose to 54.1 in December, beating expectations of 53.5 and marking a robust rebound from November’s 52.1. The strong performance signals continued resilience in the services sector, which has now expanded in 22 of the past 24 months. The December reading, the third-highest of 2024, suggests solid momentum heading into the new year.

Breaking down the components, business activity and production surged to 58.2, up significantly from 53.7, while new orders ticked higher from 53.7 to 54.2. Employment showed marginal softness, edging down from 51.5 to 51.4. The standout figure was in prices, which jumped sharply from 58.2 to 64.4, raising fresh concerns over inflationary pressures in the sector.

The overall services reading suggests a positive contribution to the economy, aligning with projected 1.7% annualized GDP growth rate.

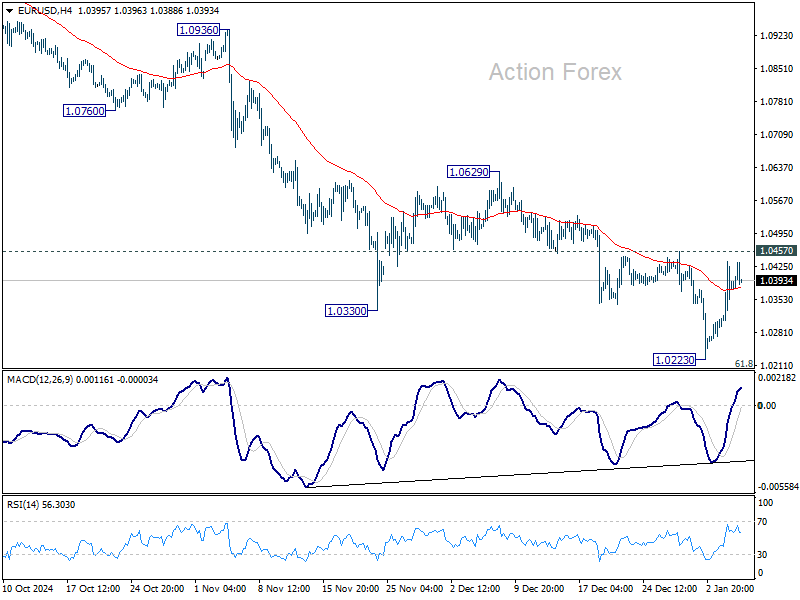

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0312; (P) 1.0374; (R1) 1.0453; More...

Intraday bias in EUR/USD stays neutral at this point, and more consolidations could be seen above 1.0223. But further decline remains in favor as long as 1.0457 resistance holds. Firm break of 1.0223 will resume the fall from 1.1213. However, sustained break of 1.0457 will confirm short term bottoming, and turn bias to the upside for 55 D EMA (now at 1.0562).

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

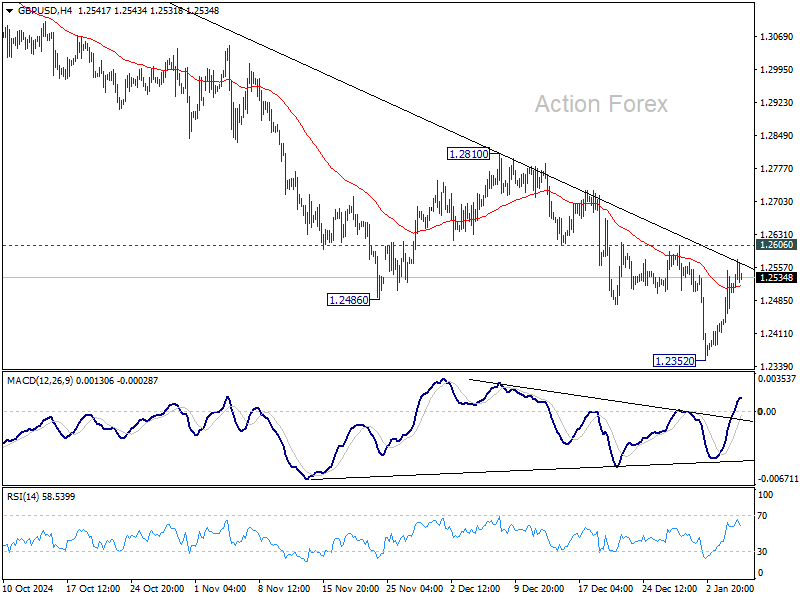

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2440; (P) 1.2495; (R1) 1.2576; More...

Intraday bias in GBP/USD stays neutral for now, and more consolidations could be seen above 1.2352. But further decline remains in favor as long as 1.2606 resistance holds. Break of 1.2352 will resume the fall from 1.3433 to 1.2256/98 cluster support zone. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 1.2606 will confirm short term bottoming, and turn bias back to the upside to 55 D EMA (now at 1.2701).

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

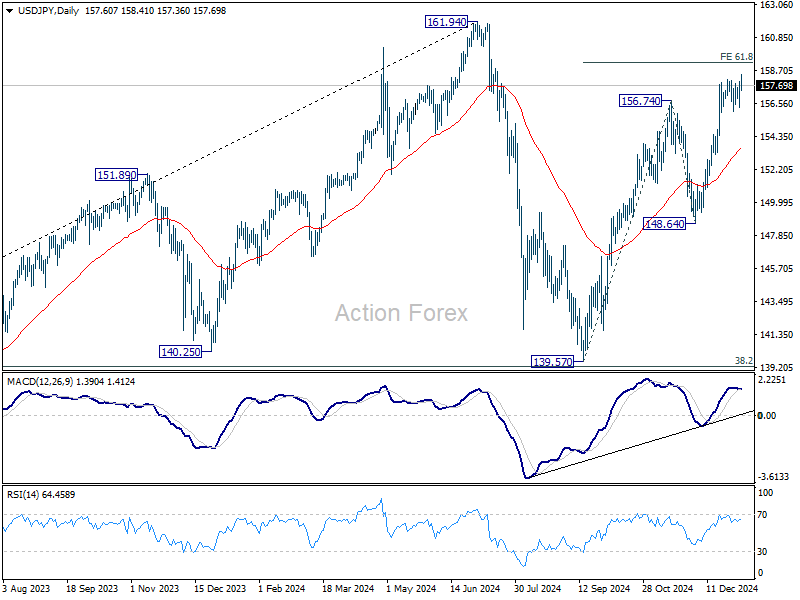

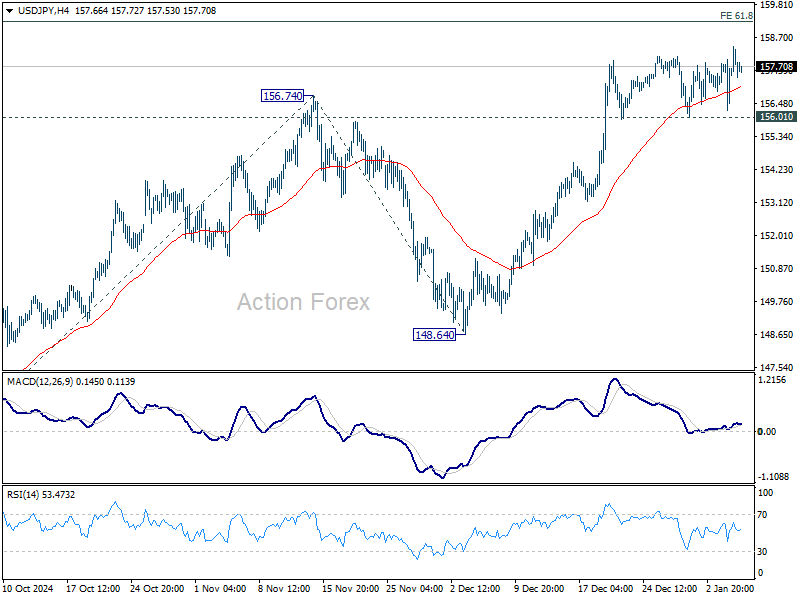

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.61; (P) 157.28; (R1) 158.33; More...

Intraday bias in USD/JPY stays on the upside at this point. Current rally from 139.57 is in progress to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will target 161.94 high. However, break of 156.01 support will indicate short term topping, likely with bearish divergence condition. Intraday bias will then be back on the downside for 55 D EMA (now at 153.64) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.