Sample Category Title

AUD/USD Daily Report

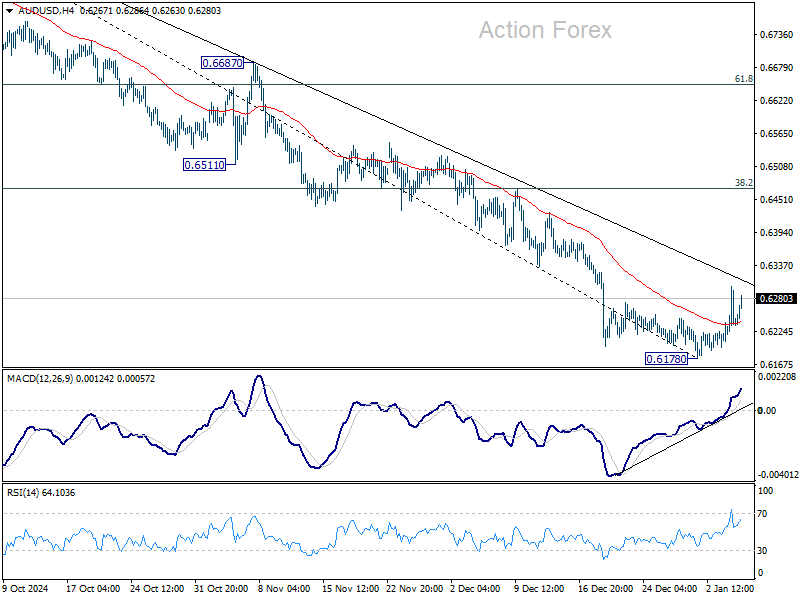

Daily Pivots: (S1) 0.6201; (P) 0.6251; (R1) 0.6296; More...

Intraday bias in AUD/USD stays mildly on the upside for the moment, and further rebound would be seen to 55 D EMA (now at 0.6418). But near term outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6178 at 0.6469. For now, more consolidation is in favor in the near term as long as 0.6178 holds, in case of retreat.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006, and could have completed at 0.6941 already. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.

GBP/USD Recovers as EUR/GBP Starts Consolidation

GBP/USD is attempting a recovery wave above the 1.2500 resistance. EUR/GBP is consolidating and might aim for a fresh increase above 0.8320.

Important Takeaways for GBP/USD and EUR/GBP Analysis Today

- The British Pound is attempting a fresh increase above 1.2420.

- There was a break above a key bearish trend line with resistance at 1.2455 on the hourly chart of GBP/USD at FXOpen.

- EUR/GBP is trading in a bearish zone below the 0.8330 pivot level.

- There is a short-term contracting triangle forming with resistance near 0.8305 on the hourly chart at FXOpen.

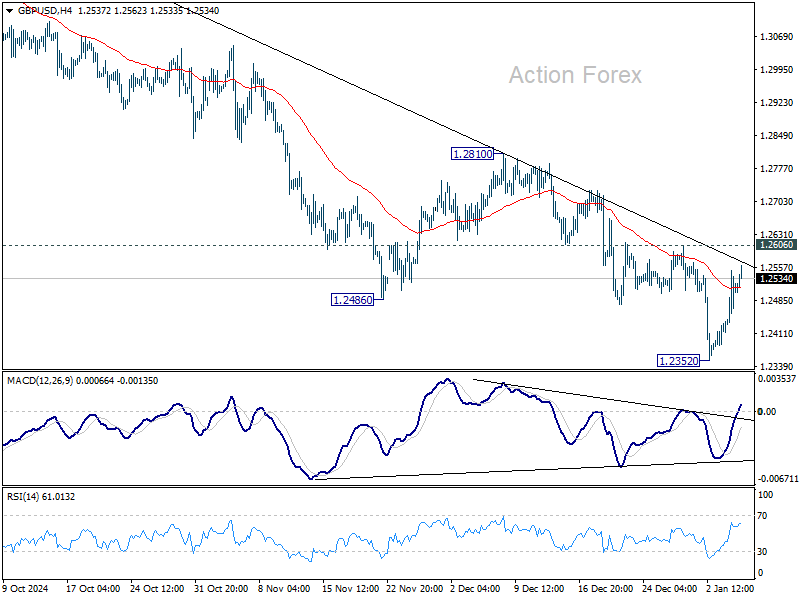

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair declined after it failed to clear the 1.2600 resistance. As mentioned in the previous analysis, the British Pound even traded below the 1.2500 support against the US Dollar.

Finally, the pair tested the 1.2350 zone and is currently attempting a fresh increase. The bulls were able to push the pair above the 50-hour simple moving average and 1.2450. The pair even climbed above the 1.2500 level.

There was a break above a key bearish trend line with resistance at 1.2455. The pair climbed above the 50% Fib retracement level of the downward move from the 1.2607 swing high to the 1.2352 low.

On the upside, the GBP/USD chart indicates that the pair is facing resistance near 1.2545 or the 76.4% Fib retracement level of the downward move from the 1.2607 swing high to the 1.2352 low. The next major resistance is near 1.2605.

A close above the 1.2605 resistance zone could open the doors for a move toward 1.2650. Any more gains might send GBP/USD toward 1.2750.

On the downside, there is decent support forming at 1.2480. If there is a downside break below 1.2480, the pair could accelerate lower. The first major support is near the 1.2455 level. The next key support is seen near 1.2410, below which the pair could test 1.2350. Any more losses could lead the pair toward the 1.2220 support.

EUR/GBP Technical Analysis

On the hourly chart of EUR/GBP at FXOpen, the pair started a consolidation phase after it failed to surpass 0.8330. The Euro traded below the 0.8320 and 0.8300 support levels against the British Pound.

The EUR/GBP chart suggests that the pair even declined below the 50% Fib retracement level of the upward move from the 0.8275 swing low to the 0.8317 high. It is now consolidating losses and trading below the 50-hour simple moving average.

The pair is now facing resistance near the 0.8305 level. There is also a short-term contracting triangle forming with resistance near 0.8305.

The next major resistance could be 0.8320. The main resistance is near the 0.8330 zone. A close above the 0.8330 level might accelerate gains. In the stated case, the bulls may perhaps aim for a test of 0.8380. Any more gains might send the pair toward the 0.8400 level.

Immediate support sits near 0.8290. The next major support is near 0.8285 or the 76.4% Fib retracement level of the upward move from the 0.8275 swing low to the 0.8317 high.

A downside break below the 0.8285 support might call for more downsides. In the stated case, the pair could drop toward the 0.8265 support level.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Crypto Climbing

Market Picture

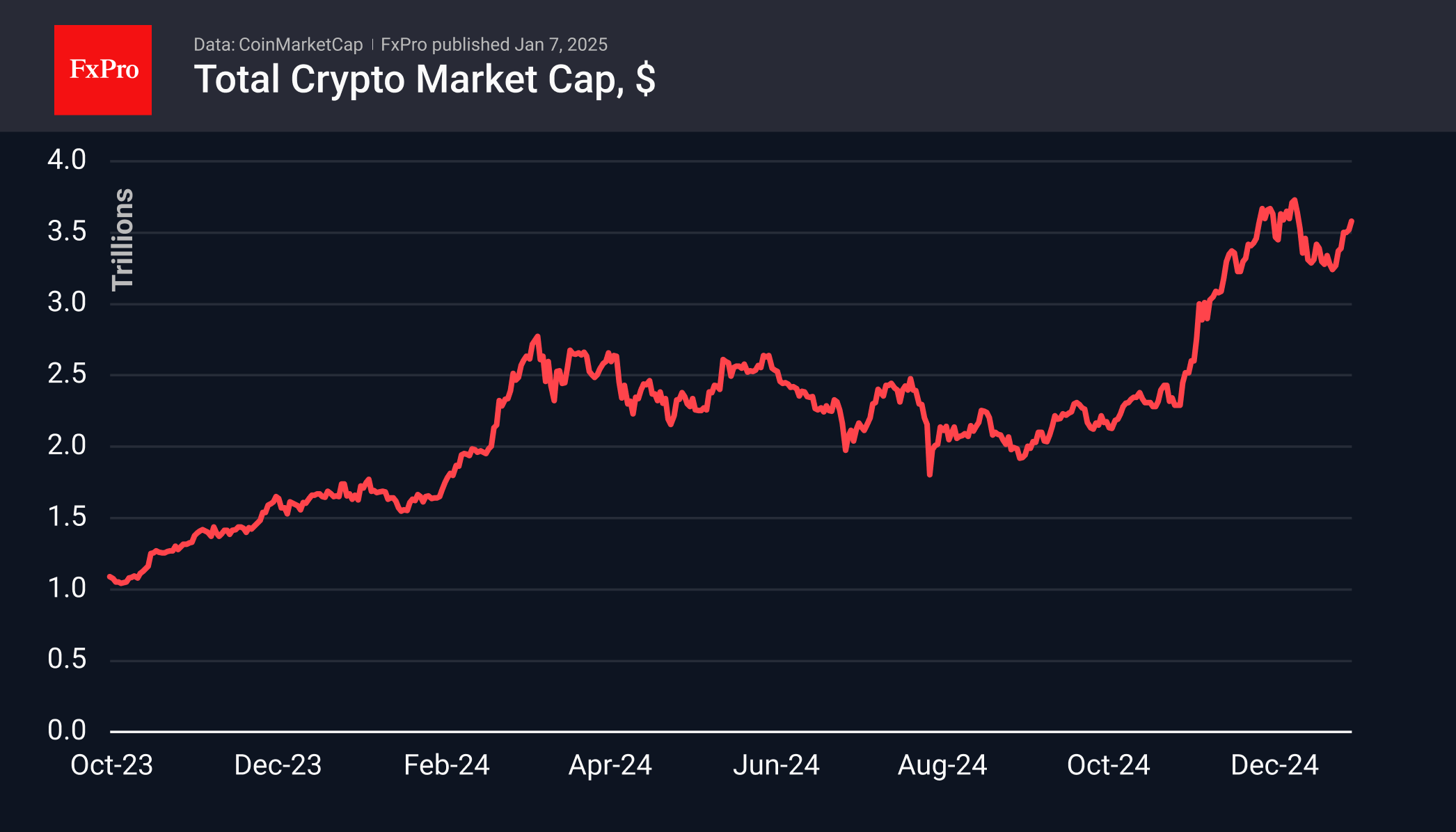

The crypto market has been on the rise since the beginning of the year. The 1.25% gain on the last day brought the gain since the beginning of January to 10%. At the current level of $3.58 trillion, the market has recovered around two-thirds of the losses since peaking at around $3.80 in mid-December. Interestingly, the market is not currently being held back by growing expectations of tighter monetary policy from the Fed.

The cryptocurrency Fear and Greed Index is back in extreme greed territory at 78. That’s high enough to indicate active buying interest but not too hot, leaving room for upside.

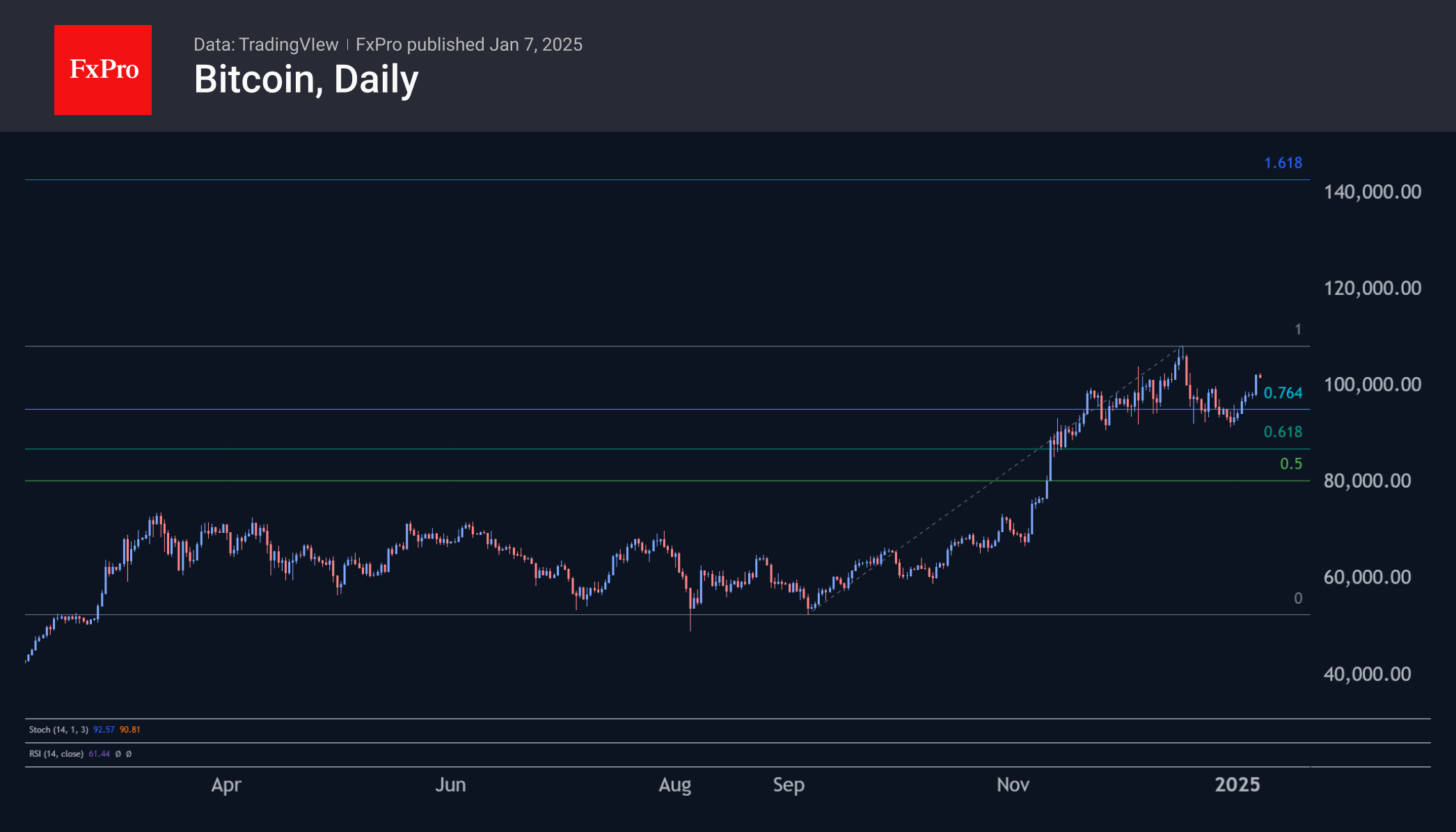

Bitcoin passed the $100K mark and climbed above $102K late on Monday. After rallying since early November, the first cryptocurrency completed a classic Fibonacci retracement and returned to growth. A break above the $110K level will initiate an expansion pattern with an upside potential of $134K.

News Background

According to CoinShares, global investment in crypto funds reached a record $44.2 billion in 2024, almost four times the previous record set in 2021. Bitcoin investment grew by $38 billion over the year and Ethereum by $4.9 billion.

Among other altcoins, $438 million went into XRP funds, $69 million into Solana and $53 million into Litecoin.

MicroStrategy bought 2,138 BTC for $209 million last week at an average price of around $97,837 per coin. The company holds 446,400 BTC on its balance sheet at an average price of $62,428.

Traders are focusing on call options with a strike price of $120,000. Key market catalysts are Trump’s inauguration on the 20th and the Fed’s rate decision on the 29th.

Miner MARA directed 7,377 BTC, or 16.4% of its bitcoin reserves, to cryptocurrency lending services to generate ‘modest’ additional income. The expected return on the contracts does not exceed 10% per year.

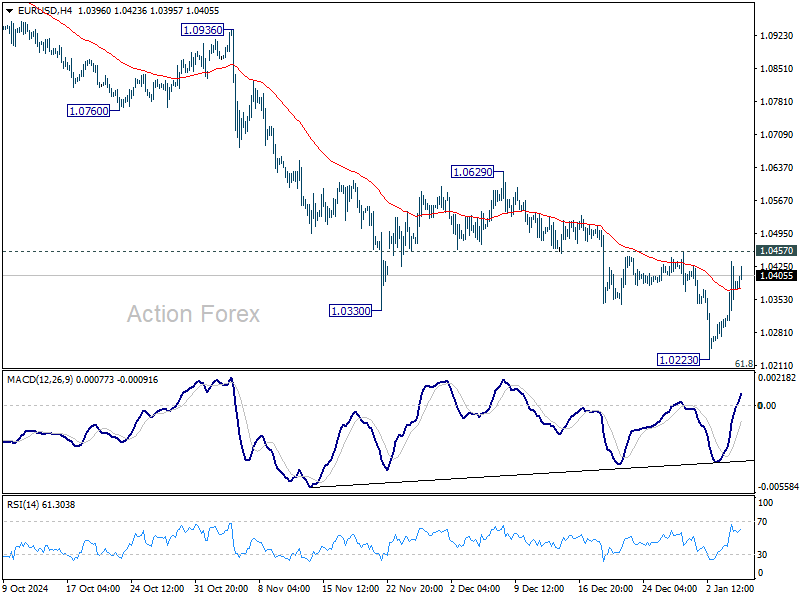

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0312; (P) 1.0374; (R1) 1.0453; More...

Intraday bias in EUR/USD remains neutral and some more consolidations could be seen above 1.0223. But further decline remains in favor as long as 1.0457 resistance holds. Firm break of 1.0223 will resume the fall from 1.1213 to 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. However, sustained break of 1.0457 will confirm short term bottoming, and turn bias to the upside for 55 D EMA (now at 1.0562).

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

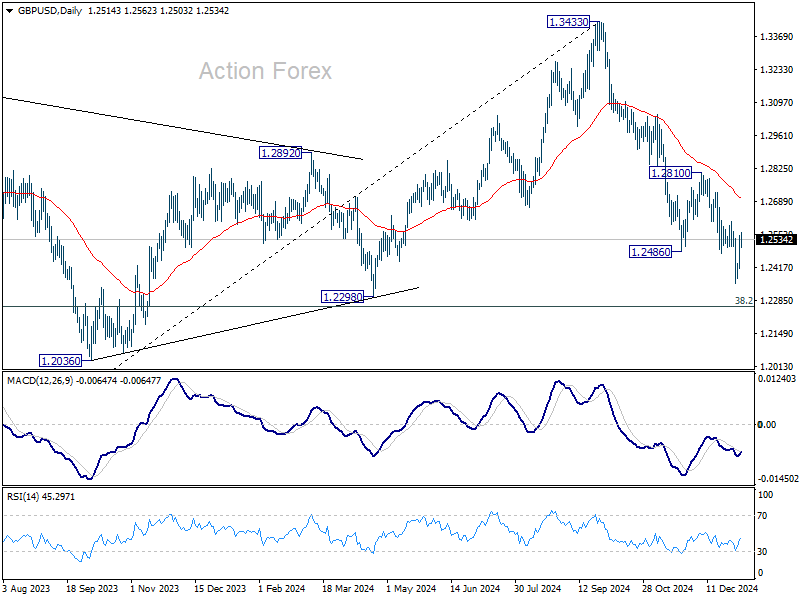

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2440; (P) 1.2495; (R1) 1.2576; More...

Intraday bias in GBP/USD remains neutral and more consolidations could be seen above 1.2352. But further decline remains in favor as long as 1.2606 resistance holds. Break of 1.2352 will resume the fall from 1.3433 to 1.2256/98 cluster support zone. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 1.2606 will confirm short term bottoming, and turn bias back to the upside to 55 D EMA (now at 1.2701).

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

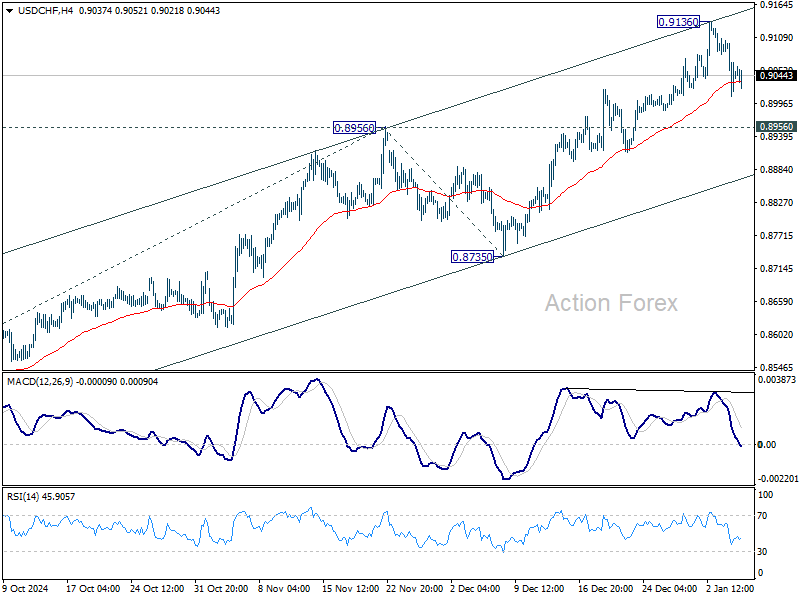

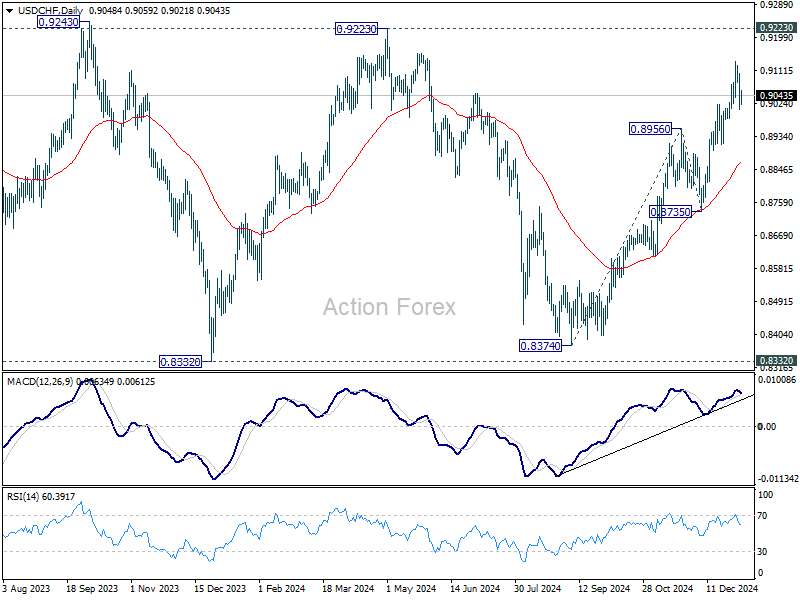

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9001; (P) 0.9053; (R1) 0.9097; More…

Intraday bias in USD/CHF remains neutral and more consolidations could be seen below 0.9136. But further rally is expected as long as 0.8956 resistance turned support holds. Above 0.9136 will resume the rally from 0.8374 to 0.9223 key resistance next. However, firm break of 0.8956 will turn bias back to the downside for 55 D EMA (now at 0.8869).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

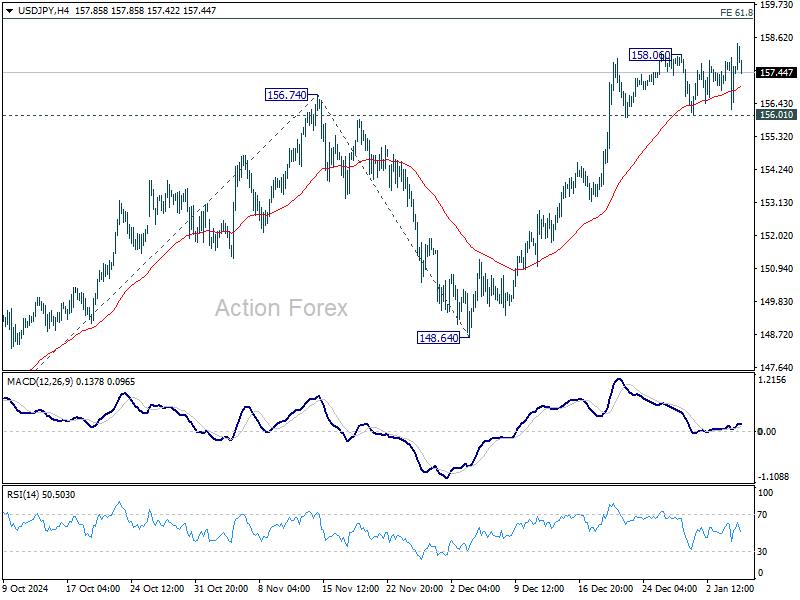

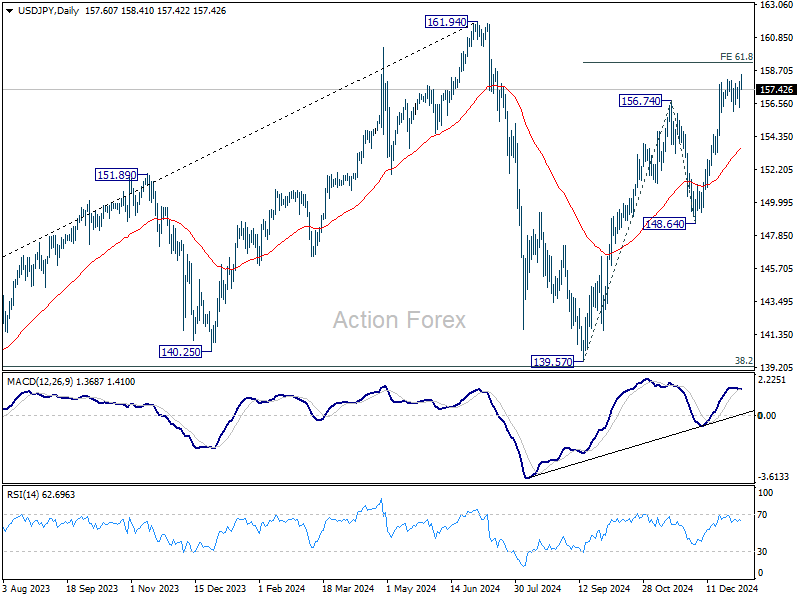

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.61; (P) 157.28; (R1) 158.33; More...

Intraday bias in USD/JPY is back on the upside with breach of 158.06. Current rally from 139.57 is resuming to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will target 161.94 high. However, break of 156.01 support will indicate short term topping, likely with bearish divergence condition. Intraday bias will then be back on the downside for 55 D EMA (now at 153.64) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Dollar Struggles on Trade Policy Ambiguity, Yen on Watch as USD/JPY Approaches 160

Dollar remains under some pressure as markets digest conflicting signals about the trade policy direction of the incoming Trump administration. President-elect Donald Trump dismissed media reports suggesting a sector-specific tariff plan as "fake news" but provided no further clarification. The lack of concrete details leaves markets grappling with uncertainty, unable to assess the economic impact of the administration’s trade strategies.

Despite the unease, the greenback's pullback has been contained, with market participants turning their attention back to critical economic data and events. Key releases this week include the ISM Services PMI later today, FOMC minutes on Wednesday, and Friday's non-farm payroll report. These events are expected to offer clarity on the Fed’s policy direction and provide a counterbalance to the prevailing trade-related uncertainties.

Meanwhile, Dollar’s earlier gains against Yen in Asian session prompted a swift reaction from Japan. Finance Minister Katsunobu Kato issued a stern warning against "one-sided, sharp moves" in the foreign exchange market. Kato emphasized that the Japanese government is closely monitoring developments and is prepared to take "appropriate action" to address excessive currency fluctuations. As the comments triggered a modest recovery in Yen, speculation is mounting that Japan could intensify its vigilance if USD/JPY approaches the psychologically significant 160 level.

In the broader currency market, New Zealand Dollar has emerged as the top performer so far this week. Sterling and Euro are also posting gains. Yen lags behind as the weakest currency, followed by Dollar and Swiss Franc. Canadian Dollar and Australian Dollar are trading in a middle range, with the Loonie showing limited reaction to Canadian Prime Minister Justin Trudeau's resignation.

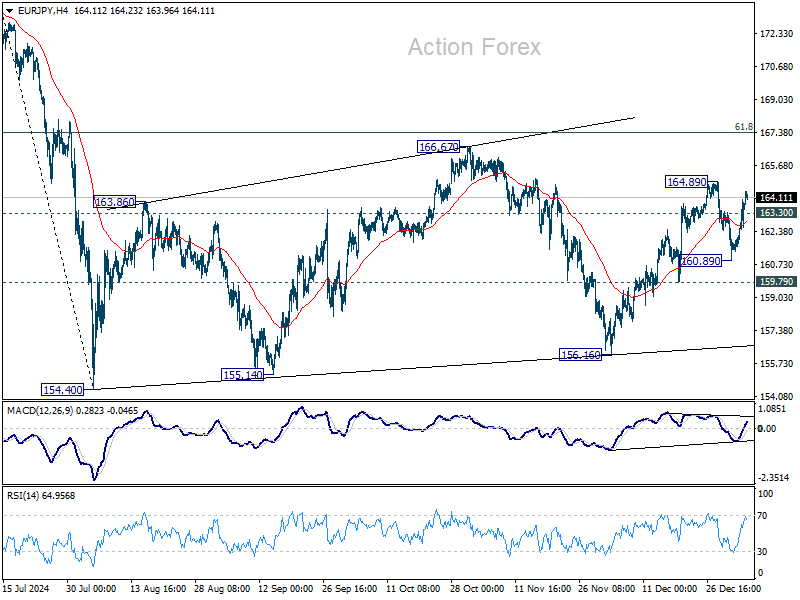

Technically, EUR/JPY's retreat from 164.89 appeared to be completed at 160.89 with current extended rebound. Rise from 156.16, as another leg of the corrective pattern from 154.40, could be ready to resume to 166.67 and possibly above. But strong resistance might be seen from 61.8% retracement of 175.41 to 154.40 at 167.38 to limit upside.

Swiss CPI falls back to 0.6% yoy in Dec

Swiss CPI fell -0.1% mom in December, matched expectations. Core CPI (excluding fresh and seasonal products, energy and fuel) was unchanged for the month. Domestic products prices rose 0.1% mom while imported products prices fell -0.5% mom.

Comparing with the same month a year ago, headline CPI slowed from 0.7% yoy to 0.6% yoy, matched expectations. Core CPI slowed from 0.9% yoy to 0.7% yoy. Domestic products prices slowed from 1.7% yoy to 1.5% yoy. Imported products prices ticked up from -2.3% yoy to -2.2% yoy.

Looking ahead

Eurozone CPI flash is the main focus in European session, while unemployment rate will also be released. Later in the day, both Canada and US will release trade balance. But attention will mainly be on US ISM services PMI.

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.61; (P) 157.28; (R1) 158.33; More...

Intraday bias in USD/JPY is back on the upside with breach of 158.06. Current rally from 139.57 is resuming to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will target 161.94 high. However, break of 156.01 support will indicate short term topping, likely with bearish divergence condition. Intraday bias will then be back on the downside for 55 D EMA (now at 153.64) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Swiss CPI falls back to 0.6% yoy in Dec

Swiss CPI fell -0.1% mom in December, matched expectations. Core CPI (excluding fresh and seasonal products, energy and fuel) was unchanged for the month. Domestic products prices rose 0.1% mom while imported products prices fell -0.5% mom.

Comparing with the same month a year ago, headline CPI slowed from 0.7% yoy to 0.6% yoy, matched expectations. Core CPI slowed from 0.9% yoy to 0.7% yoy. Domestic products prices slowed from 1.7% yoy to 1.5% yoy. Imported products prices ticked up from -2.3% yoy to -2.2% yoy.

Trump’s (Trade) Policy Ruffled Markets

Markets

Trump’s (trade) policy ruffled markets yesterday, underscoring the importance of politics under a second term of the former POTUS. The Washington Post citing three people familiar with the matter ran an article saying Trump’s aides are exploring tariff plans that would be applied to every country but only cover critical imports. It’s a major change from the president-elect’s campaign rhetoric, where he promised to slap duties on everything imported into the US. Trump later denied the report but that didn’t stop the risk-on train. It’s a potential sign markets priced in much (if not all) of the bad (tariff) news. European stocks excelled with the EuroStoxx50 rising 2.36%. Tech stocks on Wall Street took the lead (Nasdaq +1.24%). The dollar lost against all major peers except JPY. DXY eased from 108.97 to 108.25 and EUR/USD rebounded towards 1.04. USD/JPY eked out a small gain towards a former (JPY) intervention level of 158. The pair briefly jumped north of that in Asian dealings this morning before paring gains. Export-reliant currencies rose as well. The Aussie dollar tested AUD/USD 0.63 but eventually settled for less at 0.6246. Core bond yields rose but Europe showed a bear flattener compared to the US steepener. European swap yields added between 2.4 and 4.2 bps with front end underperformance following slightly better than expected final PMI’s and a big beat in German CPI figures (0.7% m/m and 2.9% y/y vs 0.5% and 2.6% expected). The latter together with other national readings (eg. Spain) point to upside risks of the European number later today. A 0.4% m/m pace is expected to lift the yearly reading from 2.2% to 2.4%. The acceleration is driven by energy base effects and has been anticipated by the ECB for some time now, meaning it shouldn’t derail easing intentions later this month. Core inflation is expected to match November’s 2.7%. US rates were more or less flat at the front and rose 3.8 bps in the 30-yr sector. The first auction of the year - a $58bn 3-year note sale - tailed >1 bps, putting the spotlights on tonight’s $39bn 10-yr one. The US economic calendar also features the November JOLTS report and the December services ISM. The latter is expected to undo some of the four-point November setback by rising from 52.1 to 53.5. Today’s data is one of the first reality checks to the strong December core bond sell-off. As long as they do not disappoint, we think yield momentum could hold. Resistance in the US 10-yr is located between 4.68 and 4.73%. Yesterday’s FX/dollar price action in our view suggests EUR/USD’s bottom has become a bit better protected, regardless of the ISM outcome.

News & Views

The British Retail Consortium BRC reported UK retail sales rising 3.2% Y/Y in December of last year, rebounding from a 3.3% decline in the previous month. Same some store sales showed a similar picture (3.1% Y/Y VS -3.4%). The sharp swings in the monthly measure were due to a statistical distortion as 2024 Back Friday sales were reported in the December figure compared to November for 2023. Sales for Q4 as a whole showed only very modest growth of 0.4% in nominal terms, de facto resulting in negative volume growth compared to the same period last year. "Following a challenging year marked by weak consumer confidence and difficult economic conditions, the crucial 'golden quarter' failed to give 2024 the send-off retailers were hoping for," BRC chief executive Helen Dickinson was quoted. Total 2024 retail sales rose 0.7% while like-for-like sales rose 0.5%. The Q4 sales at least suggest that the new UK budget including higher taxes, didn’t help to support fragile domestic demand. This will remain a element in the BoE assessment when it reassess monetary policy early February.

The Czech Republic over 2024 realized a CZK 271.4 bln budget deficit, down CZK 17.1 bln from the previous year, its Finance Ministry reported. The year-on-year improvement in the balance reflects an increase in tax and insurance collections on the revenue side and moderate growth in total expenditures. The Czech Republic's state debt grew to CZK 3 365 bln at the end of 2024 from CZK 3 111 bln the year before. The debt ratio rose to 42.8% of GDP from 40.8% in 2023. The Fin Min yesterday also published the funding and Debt management strategy for 2025. For 2025, the total state financing needs amount to CZK 563.5 bln, i.e. approximately 6.7% of GDP. In the medium-term outlook, the total financing needs will be stabilised at 5.9% and 5.4% of GDP for 2026 and 2027, respectively, which is caused by decreasing state budget deficits and stabilized state debt redemptions in these years.