Sample Category Title

AI Rally Defies Gravity, Focus on EZ CPI, US Jobs Data

Early year worries that the AI rally would fizzle out were rapidly wiped out at the start of this week by Microsoft’s announcement to be willing to spend $80bn on data centers – which pushed the stock up to 1.4% yesterday, by Foxconn’s announcement of a 42% surge in its December sales thanks to AI-driven demand – which pushed Micron 10% higher in the US yesterday and Foxconn 3% higher in Taiwan today, and by news that Qualcomm is now introducing new chips that only cost $600 to power personal computers that are capable of running the latest AI software. Qualcomm gained 1.28% yesterday. And Nvidia – in all this – jumped 3.43% before Jensen Huang’s CES speech and hit a fresh record high yesterday. That doesn’t look like a rally that’s fizzling out just yet – although the AI discussions this year will shift from hype and hope to real-life applications and return on massive investments. Consequently, the data beyond the AI enablers (like chip and equipment makers) will likely command a larger share of investor attention in 2025. A concrete integration of AI to daily tools and increased revenues are essential.

For now though, the AI enablers continue to shoulder the rally. The S&P500 kicked off the week with a 0.55% gain, while its tech-heavy peer Nasdaq 100 gained more than 1%. Mood elsewhere was murkier however. The Dow Jones for example was slightly lower on Monday, as the 10-year yield spiked past 4.60% and the 30-year yield hit 4.86% - for the first time since November 2023 on expectation that the Federal Reserve (Fed) could make a long pause before its next rate cut due to worries of reviving inflation with Donald Trump’s pro-growth and tariff policies.

The US dollar couldn’t benefit from higher yields as Washington Post reported that Trump’s policies wouldn’t be as harsh as promised. But Trump rapidly denied the news and the dollar rebounded. The USDCAD sharply fell on Trudeau’s resignation – and probably on the back of a rally in US crude to $75pb. Note that US crude is now in the bullish consolidation zone and could extend gains toward its 200-DMA – that stands near $75.70pb level.

Coming back to FX, most major currencies spiked against a weaker US dollar yesterday. The EUR/USD – which tanked to 1.0224 in the early hours of the new year - rebounded past the 1.04 level, while Cable successfully threw itself back above the 1.25 mark.

Euro could extend rebound

The first day of 2025 marked the end of gas flows from Russia to Europe that flew through Ukraine. Winter temperatures are low and the European gas reserves are melting faster than average. And that’s pushing the nat gas prices higher. The European nat gas futures rallied up to 30% in the last two weeks of December. We are not close to the spike experienced at the beginning of the war but the outlook is positive, and price dips – like the one we saw yesterday – are interesting opportunities to strengthen long positions. The only thing that could reverse the gas rally right now is the hope that the expired contract will be renewed in the next few weeks, on hope that Trump will magically end the war in Ukraine, and/or weak demand from China – which, by the way, recorded its worst start to the year since 2016...

But coming back to Europe, the big problem with rising energy prices is that it starts to be reflected in inflation figures. Released yesterday, the German inflation spiked to 2.9% in December from 2.4% printed a month earlier, and the Eurozone’s aggregate CPI – due later this morning - will likely show a similar upside pressure, as well. And that’s not good news for the European Central Bank (ECB) that is supposed to give support to the weakened European economies by ample rate cuts this year. If inflation spikes, the ECB won’t be able to ease the financial conditions as much as desired. The latter reasoning is positive for the euro’s valuation, but negative for stock valuations. The Stoxx 600 rallied to its 200-DMA yesterday but a stronger-than-expected CPI number from the Eurozone this morning could spoil that optimism, while allowing the EURUSD to extend gains above the 1.04 mark and reclaim a rise toward the 1.05 psychological level.

Eyes on US jobs

The US will be releasing its latest jobs figures starting from today, and the numbers will matter fpr the Fed expectations. The US economic growth last year remained robust, the jobs market started cooling but the cool down was not as sharp as the Fed predicted; the US economy ended by adding close to 180K new nonfarm jobs on average every month during last year. As such, the potentially excessive Fed cuts of last year now fuel the expectation that the Fed will pause for a few months. Activity on Fed funds futures suggests that the next Fed cut will not arrive before May. A sufficiently soft figures this week could scale back a part of that hawkishness, pull the US dollar lower and allow the others to gain field.

Focus on Euro Area Inflation After Country Releases Surprise on the Upside

In focus today

The focus today is the euro area inflation print. Inflation was expected to be 2.4% y/y in December, up from 2.2% in November. But with Germany rising 50bp and both Spain and Portugal rising 40bp, inflation will most likely come in higher. We expect headline inflation at 2.6% y/y, while we expect core inflation at 2.8% y/y. In our view, an upside surprise in December inflation should not alter the near-term outlook for the ECB, as the focus remains on weak growth prospects. We also receive data on unemployment, which we expect to show a small uptick to 6.4% from 6.3%, as surveys have pointed to a softening in the labour market; overall, however, the unemployment rate remains historically low.

This morning, we receive Swiss inflation data for December. Headline and core inflation are expected to drop further and remain at the lower end of the SNB's target range of 0-2%. We expect the SNB policy rate to bottom at 0% this summer following two consecutive 25bp cuts.

In the afternoon, both the December ISM Services and November JOLTs Job Openings are due for release from the US. The latter is a key measure of labour demand for the Fed.

Economic and market news

What happened yesterday

In Germany, inflation rose to 2.9% y/y in December from 2.4% y/y, beating expectations of 2.6% y/y. The increase in German inflation was mainly due to energy base effects, as energy inflation rose to -1.7% y/y from -3.7% y/y. Core CPI inflation rose slightly to 3.1% y/y in December from 3.0% y/y. The monthly momentum in underlying inflation presents a somewhat softer picture of inflation in December than the increase in yearly headline inflation, but underlying inflation continued to rise at a pace faster than what is compatible with 2% annualised inflation.

In the euro area, we received the final release of the service PMIs for December. The PMIs for the whole euro area were revised upwards, signalling stronger activity in the euro area than initially thought. The French services PMI was revised up to 49.3 in the final print from 48.2 in the flash release. The services PMI is thus now back above the October level after the sharp decline in November. The quarterly average for Q4 is below the Q3 level, indicating lower activity even excluding the Olympics, but the upward revision does provide some relief.

USD broadly weakened after The Washington Post reported that US President-elect Trump's plans to impose tariffs on trade partners would be less comprehensive than initially presented. More specifically, the report stated that Trump was considering tariffs that would be applied only to critical imports. Previous comments from Trump suggested a 25% tariff on all imports from Canada and Mexico, and an additional 10% tariff on imports from China. Trump commented on the report and said that it is wrong that the tariffs will be pared back. Last night, the US Congress formally certified Donald Trump' election victory. The broad USD index began yesterday at 108.9 and ended in 108.2. Before Trump's comments it briefly fell below 108.

In Canada, Prime Minister Justin Trudeau resigned after nine years in power. An election was already scheduled for October but is now likely to happen sooner. The parliament is now set to resume work in late March, which means that a new election is unlikely to be held until May at the earliest. The Conservative Party leads Trudeau's Liberals by more than 20 points in the pre-election polls. Mark Carney, the former governor of the BoC and BoE, has said he is considering entering the race to replace Trudeau.

Equities: Global equities were higher yesterday on a day that reminded us of what the next four years will bring. Whether we like it or not, we must prepare to deal with a new and higher level of noise as the new US administration comes in. However, even before the Wall Street Journal article about the potential winding down of tariff plans, equities were already higher in Europe. Naturally, the story further boosted those moves. As Trump denied the story on Truth Social, some of this optimism faded. It brings back memories of Trump's first term as president and serves as a good reminder that we need to be extremely careful when interpreting political headlines over the next four years.

Beneath all the political noise, we had yet another day of significant cyclical outperformance, which brings us closer to the point where one should start considering reducing cyclical exposure as they have simply been running too far ahead of fundamentals.

In the US yesterday, Dow -0.1%, S&P 500 +0.6%, Nasdaq +1.2%, and Russell 2000 -0.1%. Asian markets are mixed this morning, illustrated by the Nikkei 225 being higher by 2% while the Hang Seng is down 2%. Futures on both sides of the Atlantic are lower this morning.

FI: The combination of supply as well as higher inflation pressure is putting pressure not only in Euroland but also in the US, where 30Y yields rose to 4.85%, which is close to the old top around 5% from back in 2023. Germany followed US Treasuries, and the Bund ASW-spread is still trading around 50bp.

FX: The broad USD softened across the G10 space following reports of more moderate tariff plans than initially anticipated. Although Trump later denied these reports, they nevertheless contributed to a wave of broad-based USD depreciation. EUR/USD edged higher toward 1.04, while USD/JPY approached the 158 level. EUR/CHF has remained range-bound between 0.93 and 0.94 over the past week. In the Scandies, NOK's recent outperformance has paused, with EUR/NOK stabilising just above the 11.70 level.

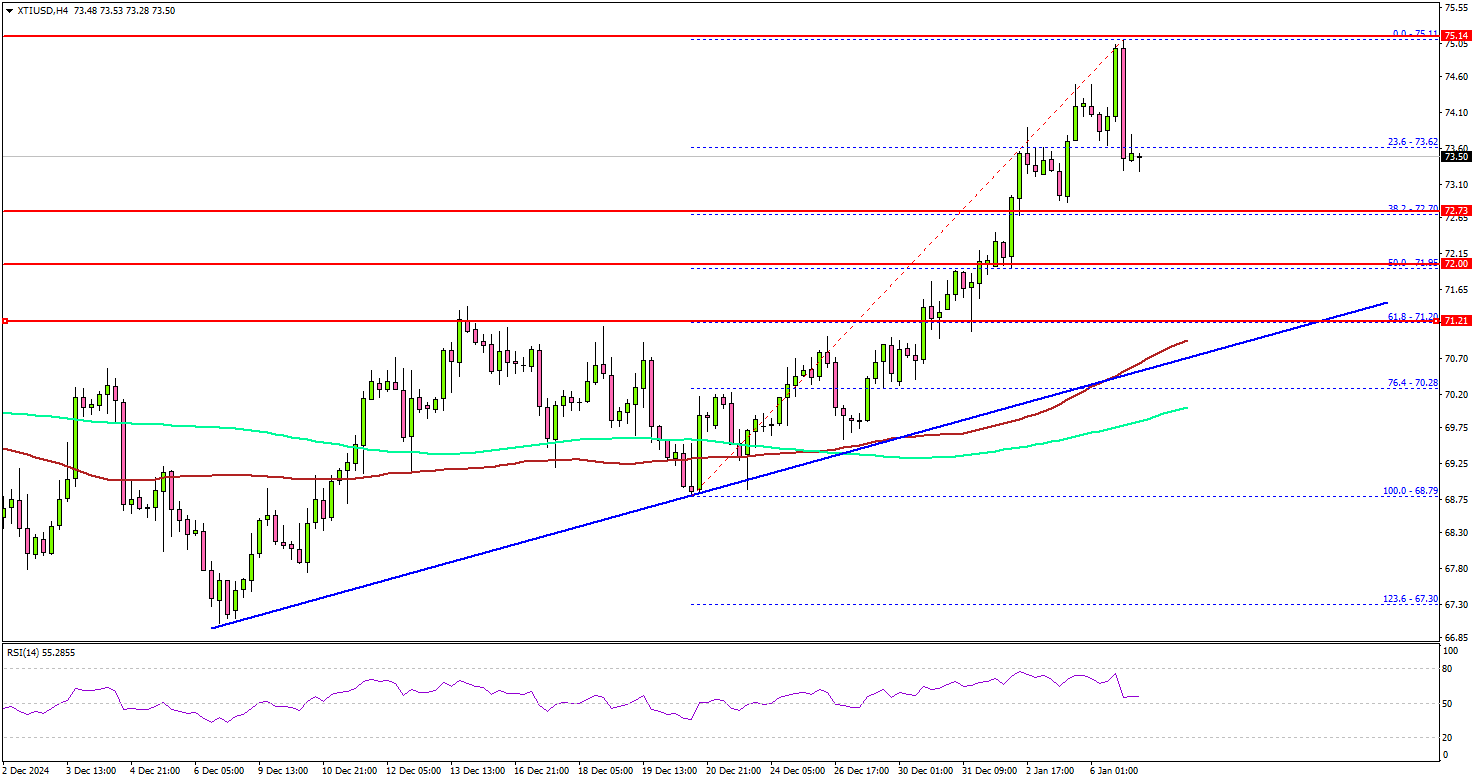

WTI Crude Oil Regains Strength: Can The Uptrend Continue?

Key Highlights

- WTI Crude Oil prices started a fresh increase above the $71.50 resistance zone.

- A connecting bullish trend line is forming with support at $71.20 on the 4-hour chart.

- Gold prices could advance if there is a clear move above $2,650.

- EUR/USD must surpass 1.0420 to start a decent recovery wave.

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price found support near the $68.80 zone. A base was formed and the price started a fresh increase above $70.00.

Looking at the 4-hour chart of XTI/USD, the price traded gained pace for a move above the $71.50 resistance zone, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The bulls even pushed prices above the $74.00 level. A high was formed at $75.11 and the price is now consolidating gains. There was a minor decline below the 23.6% Fib retracement level of the upward move from the $68.79 swing low to the $75.11 high.

There is also a connecting bullish trend line forming with support at $71.20 on the same chart. The trend line is close to the 61.8% Fib retracement level of the upward move from the $68.79 swing low to the $75.11 high.

On the upside, the price is facing hurdles near the $74.20 level. The main hurdle is still near the $75.00 zone, above which the price may perhaps accelerate higher.

In the stated case, it could even visit the $76.50 resistance. Any more gains might call for a test of the $78.00 resistance zone in the near term. On the downside, the first major support sits near the $72.70 zone.

A daily close below $72.70 could open the doors for a larger decline. The next major support is $71.20. Any more losses might send oil prices toward $70.00 in the coming days.

Looking at Gold, there was a steady increase above the $2,620 level and the bulls could now aim for a move above $2,650.

Economic Releases to Watch Today

- US ISM Services Index for Dec 2024 – Forecast 53.0, versus 52.1 previous.

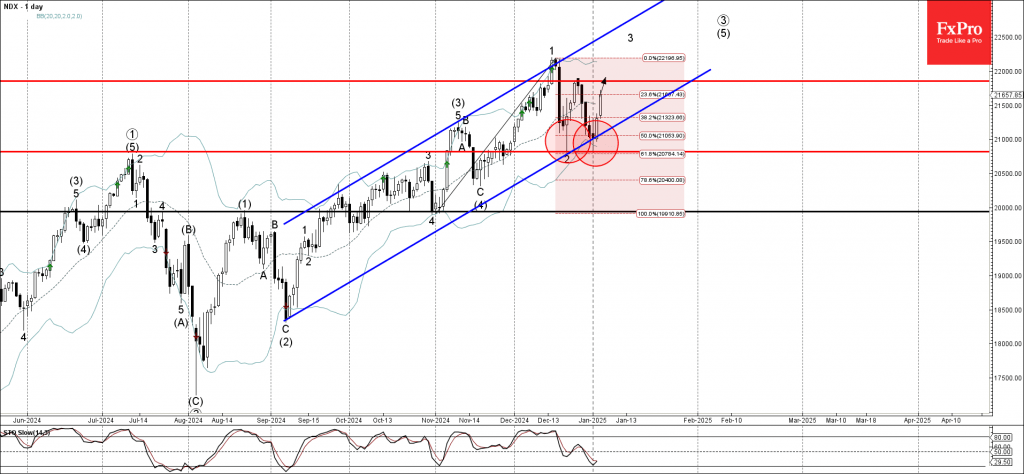

Nasdaq-100 Wave Analysis

- Nasdaq-100 reversed up from support zone

- Likely to rise to resistance level 21855.00

Nasdaq-100 index recently reversed up from the support zone located at the intersection of the support level 20820.00 (low of the previous minor correction 2), support trendline of the daily up channel from September, 61.8% Fibonacci correction of the upward impulse from October and the lower daily Bollinger Band.

The upward reversal from this support zone created the daily Japanese candlesticks reversal pattern Morning Star, which has the daily Hammer as its middle candle.

Given the clear daily uptrend, Nasdaq-100 index can be expected to rise to the next resistance level 21855.00 (which formed the daily Evening Star last month).

Sunset Market Commentary

Markets

US and EMU yields initially maintained the post-Fed upward bias that still reigned during the first 2025 trading sessions last week. However especially US LT yields are closing in on key technical resistance levels. The US 10-y yield is testing the end December top (4.64%), with the 2024 top (4.73%) also nearby. The 30-y yield briefly exceeded the 2024 4.84% top. However, with less than 50 bps of additional Fed cuts discounted by the end of this year, investors already loyally embrace the guidance from the December Fed dots plot. Really significant ‘new news’ is probably needed to extend the repositioning into a next technical era. US yields currently add 0.6 bps (2-y) to 2.5 bps (30-y), awaiting this week’s key US eco data (services ISM, labour market data). This week’s first round of US Treasury auctions, totaling $119bn, starts with today’s $58bn 3-y sale (10-y and 30-y to follow tomorrow and on Wednesday) and will also help to assess investor appetite at ‘repriced’ entry levels. The dynamics on EMU yield markets was slightly different. The ECB is largely expected to move its policy rate to a neutral level (2-2.5% area). However, after an upward surprise of the Spanish CPI last week, higher than expected preliminary German inflation data (HICP 0.7% M/M and 2.9% Y/Y from 2.4% vs 2.6% expected; services inflation 4.1% from 4%) illustrated that there is no reason to already preposition for a sub-2% depo rate. In a slight (re)flatting move, EMU swap yields currently add between 4.5 bps (2-y) and 1.5 bps (30-y).

On FX markets, the dollar showed wild intraday swings. Relative interest rate moves between the EMU and the US initially supported cautious EUR/USD gains. However, around noon European time, the Washington Post (WP) reported that the Trump administration was looking to only impose tariffs on sectors that are deemed critical to national or economic security. The headlines triggered a broad risk-on move with higher (European) equities and a USD correction. EUR/USD temporary jumped from the low 1.03 area to 1.04+ levels. DXY tumbled from the 108.70 area just before the WP headlines to ease below the 108 big figure. However, in the Trump era, news on the policy of the new administration is only viable until the next headlines from the President(-elect). That came only a few hours later as Trump said that his Tariffs Policy won’t be pared back. The dollar regained part of its losses but still trades negative on a daily basis (EUR/USD 1.0375, DXY 108.35). European equities are trading off the intraday highs, but mostly keep decent gains (Eurostoxx 50 +1.4%). US indices also remain well supported (S&P 500 + 1%, Nasdaq + 1.5%).

News & Views

The Kingdom of Belgium announced a new syndicated euro benchmark bond to be issued in the near future – most likely tomorrow. It’s the first of three new fixed-rate benchmarks with maturities of 5 year, 10 year and one in a unspecified long maturity (> 10 years). Tomorrow’s 10-yr OLO 103 will mature 22/06/2035 and will help fund a €44.65 bn gross borrowing requirement consisting largely of €22.62 bn of redemptions and €19.43 bn in net financing. The Belgian Debt Agency noted the latter assumes Belgian compliance with the new European fiscal framework. The Kingdom, however, has not yet submitted its Medium Term Fiscal and Structural Plan to the European Commission, making the estimate prone to revisions. OLOs make up the vast bulk of the provisional €44.65 bn funding needs with the BDA intending to issue €42 bn.

France’s new finance minister Eric Lombard lowered the end-of-2025 budget deficit reduction goal during a radio-interview this morning. The previous minority government imploded after its plans to cut the gap from 6.1% to 5% forced out a no-confidence motion from the opposition. Lombard said that the >1% reduction is too much, saying they also need to support the economy. He instead targets a deficit that would be between 5 and 5.5%, containing around €50bn of tax increases and spending cuts compared to the €60bn former PM Barnier proposed. The shallower fiscal consolidation path would not derail the longer term objective of bringing the deficit back to the 3% mark by 2029. OAT/swap spreads ease several basis points today in a move joined by most other European peers.

US PMI services finalized at 56.8, optimism with questions over Fed’s rate cuts

US economy concluded 2024 on a strong note, with PMI Services finalized at 56.8 in December, up from 56.1 in November and marking a 33-month high. Although below the preliminary estimate of 58.5, the services sector's robust performance overshadowed the ongoing weakness in manufacturing. PMI Composite also rose to 55.4 from 54.9 in the prior month, confirming solid growth momentum.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, highlighted that "Business activity in the vast services economy surged higher in the closing month of 2024 on fuller order books and rising optimism about prospects for the year ahead". The sector's strength has buoyed GDP growth, which is expected to remain "robust" after registering a 3.1% expansion in Q3 2024.

Optimism is partly tied to expectations of business-friendly policies under the incoming Trump administration, including potential tax reforms, deregulation, and selective tariffs aimed at supporting domestic industries. Such measures have bolstered sentiment among service providers, with many forecasting faster growth in 2025.

However, Williamson cautioned that the economy's current momentum might make Fed policymakers hesitant to aggressively lower interest rates. Financial services, in particular, have played a critical role in late 2024's economic performance, fueled by expectations of lower borrowing costs. The challenge in the months ahead will be balancing continued economic growth with the potential fallout from a changing interest rate outlook.

Fed’s Cook: Can afford to proceed more cautiously with further cuts

Fed Governor Lisa Cook highlighted in a speech today that Fed can "afford to proceed more cautiously with further cuts". She noted that risks to the dual mandate of price stability and maximum employment are now "roughly in balance". But since September, "The labor market has been somewhat more resilient, while inflation has been stickier than I assumed". Also, with the 100bps of rate cuts last year, Fed has already "notably reduced the restrictiveness of monetary policy. "

Elaborating on the outlook, Cook highlighted progress in core goods pricing, which has eased due to better supply-demand balance. She expects housing services inflation, a significant contributor to elevated prices, to cool further in 2025 as slower rent growth filters through the system. However, she remains watchful of uneven progress, maintaining confidence that inflation will "gradually—if unevenly—return over time to our goal of 2 percent."

Turning to the labor market, Cook described it as solid but moderating. High turnover and elevated job-switching seen earlier in the post-pandemic recovery have subsided, creating better balance between supply and demand for labor. "I do not see the labor market as a source of significant inflationary pressure," she added, noting that wage growth disparities between job switchers and stayers have largely diminished.

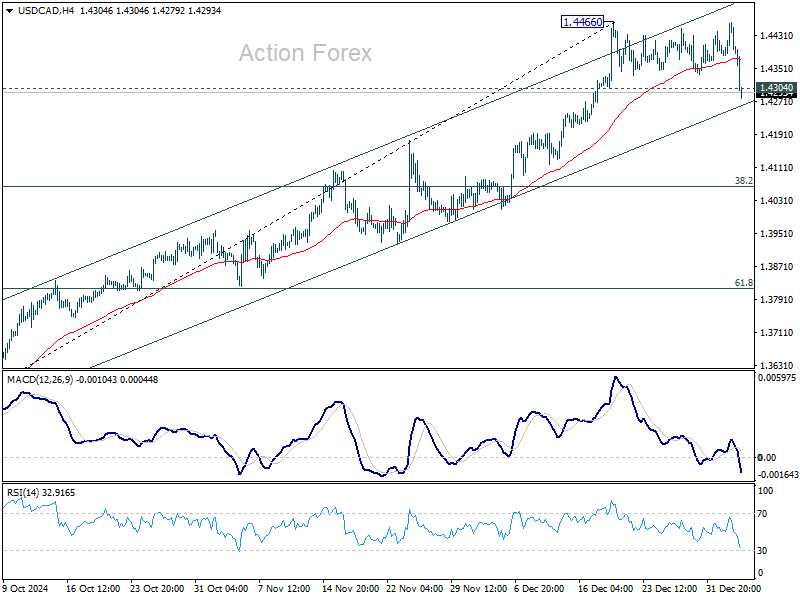

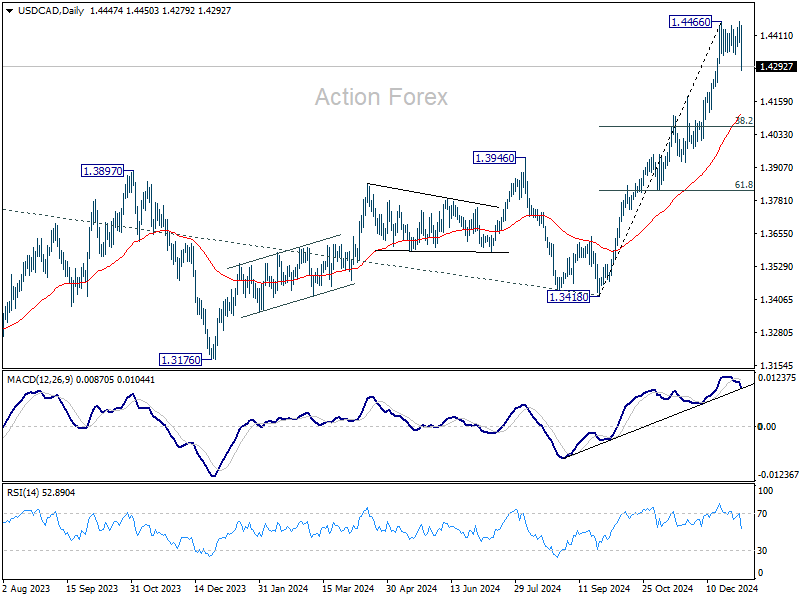

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4400; (P) 1.4432; (R1) 1.4481; More...

Break of 1.4304 support suggests short term topping at 1.4466 in USD/CAD. Intraday bias is back on the downside for pull back to 55 D EMA (now at 1.4112). But downside should be contained by 38.2% retracement of 1.3418 to 1.4466 at 1.4066 to bring rebound. For now, risk of more consolidations remains as long as 1.4466 holds, in case of recovery.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

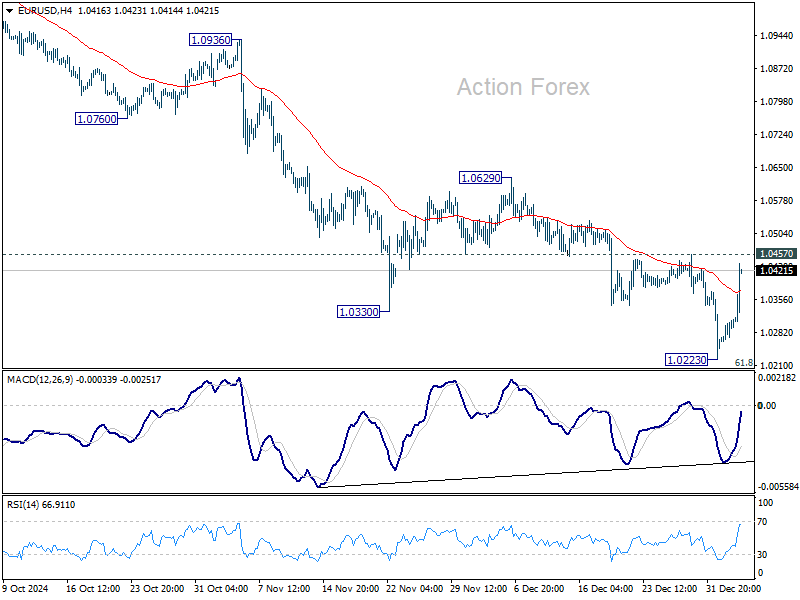

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0273; (P) 1.0291; (R1) 1.0328; More...

EUR/USD is still holding below 1.0457 resistance despite today's strong rebound and intraday bias stays neutral. Another fall remains in favor. Firm break of 1.0223 will resume the fall from 1.1213 to 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. However, sustained break of 1.0457 will confirm short term bottoming, and turn bias to the upside for 55 D EMA (now at 1.0569).

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.