Sample Category Title

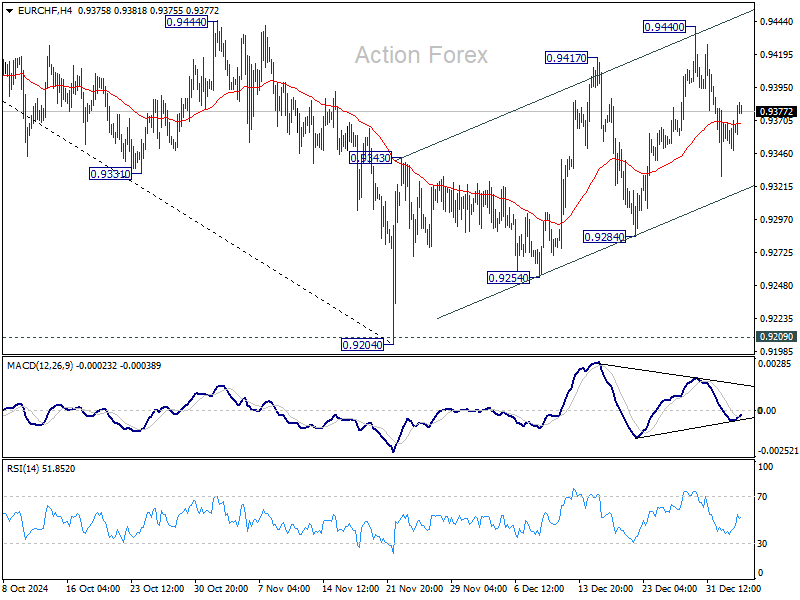

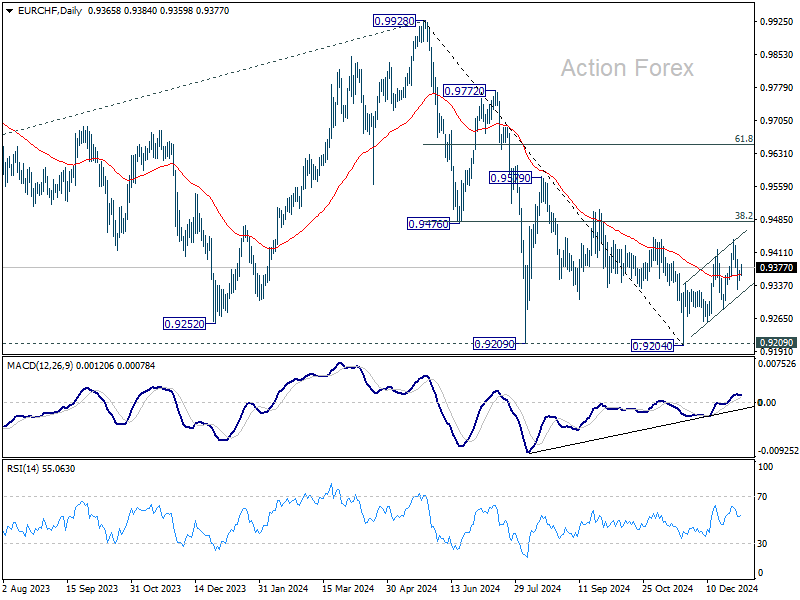

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9341; (P) 0.9357; (R1) 0.9380; More....

Intraday bias in EUR/CHF remains neutral for the moment. Corrective rebound from 0.9204 could still extend higher. But upside should be limited by 0.9481 fibonacci resistance. On the downside, firm break of 0.9284 support will argue that the correction has completed, and bring retest of 0.9204 low.

In the bigger picture, while rebound from 0.9204 might extend higher, strong resistance could be seen from 38.2% retracement of 0.9928 to 0.9204 at 0.9481 to limit upside. Down trend from 0.9928 (2024 high) is still in favor to resume through 0.9204/9 support zone at a later stage.

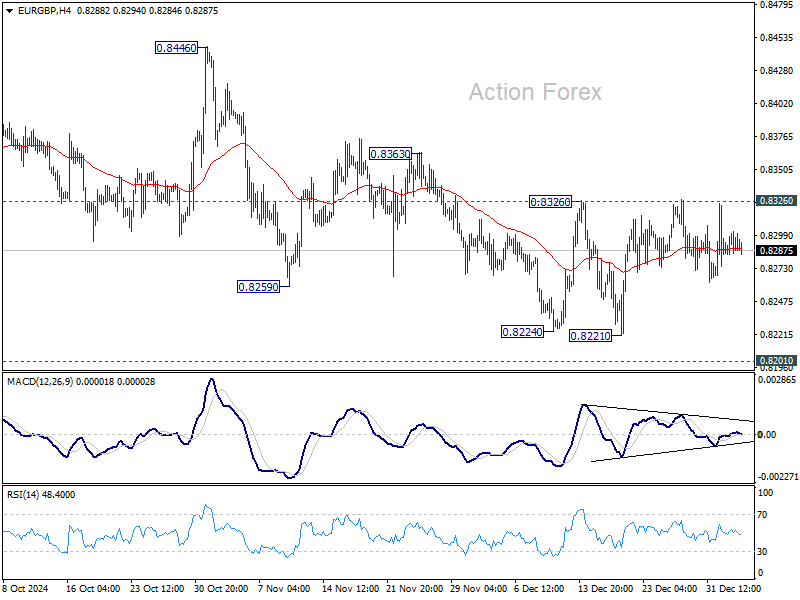

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8288; (P) 0.8296; (R1) 0.8306; More...

Intraday bias in EUR/GBP remains neutral for the moment as range trading continues inside 0.8221/8326. On the upside, firm break of 0.8326 resistance will confirm short term bottoming at 0.8221, ahead of 0.8201 key support. Intraday bias will be turned back to the upside for 0.8446 structural resistance next.

In the bigger picture, focus remains on whether 0.8201 key support (2022 low) is strong enough to complete the whole down trend from 0.9267 (2022 high). In any case, medium term outlook will be neutral at best until decisive break of 0.8624 key resistance. Risk will stay on the downside even in case of strong rebound.

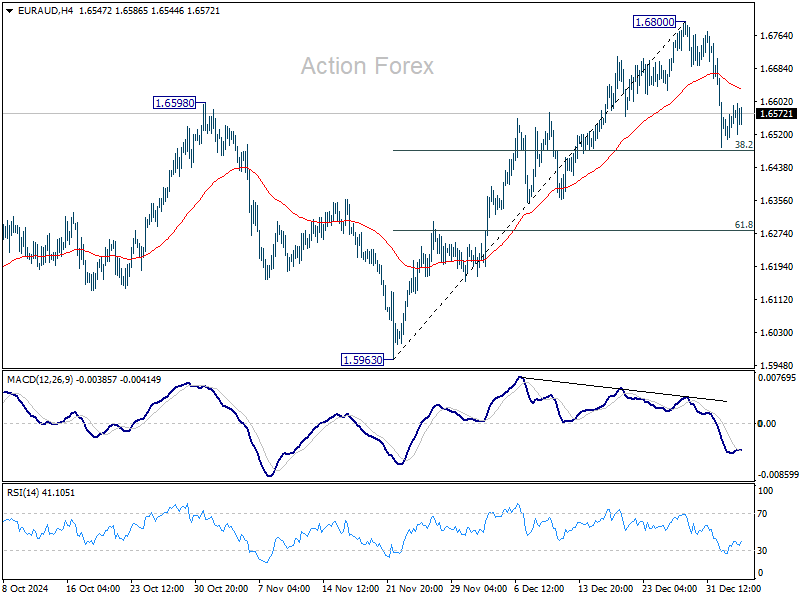

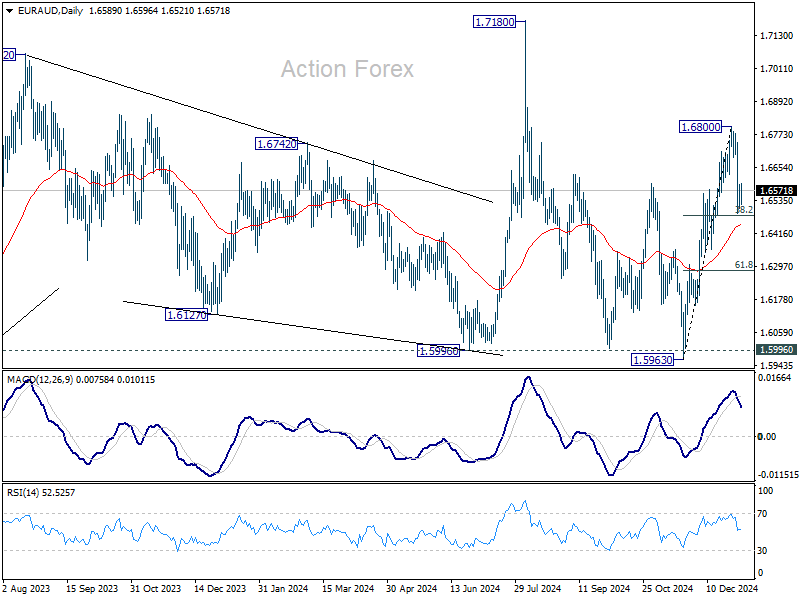

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6529; (P) 1.6562; (R1) 1.6614; More...

Intraday bias in EUR/AUD remains neutral for the moment. Strong support could be seen from 38.2% retracement of 1.5963 to 1.6800 at 1.6480 to bring rebound. But near term risk will stay mildly on the downside as long as 1.6800 resistance holds, in case of extended recovery. Firm break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed and deeper decline would be seen.

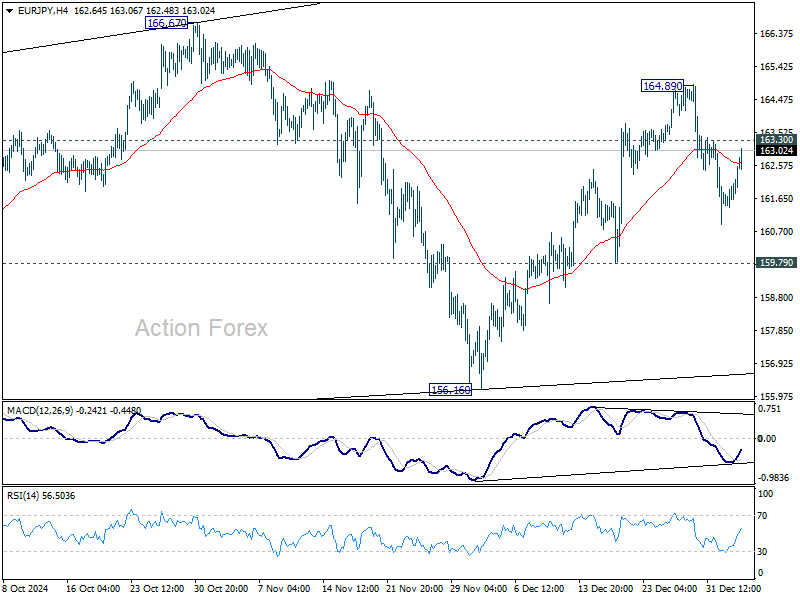

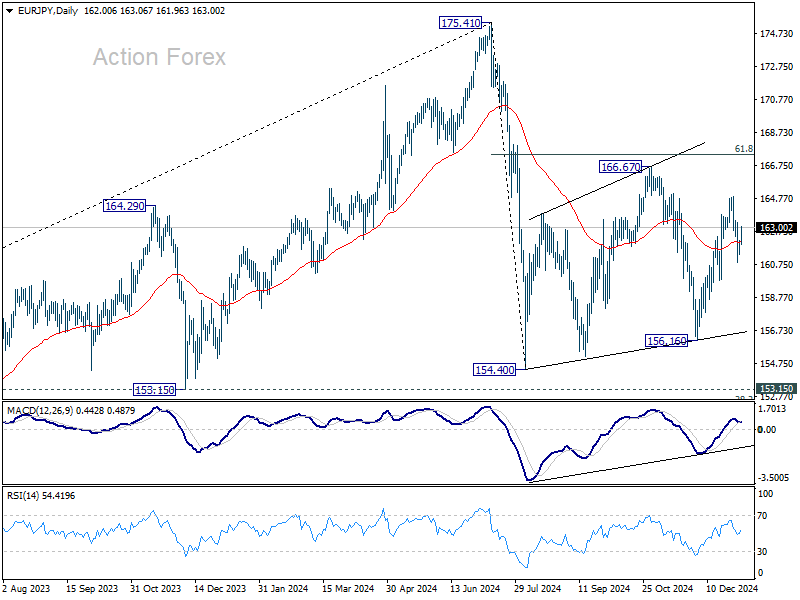

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.58; (P) 161.90; (R1) 162.49; More...

EUR/JPY recovered further today but stays below 163.30 minor resistance and intraday bias stays neutral. Outlook is unchanged that t corrective pattern from 154.40 is still extending. Above 163.30 minor resistance will bring retest of 164.89 first. Break there will target 166.67 resistance next.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

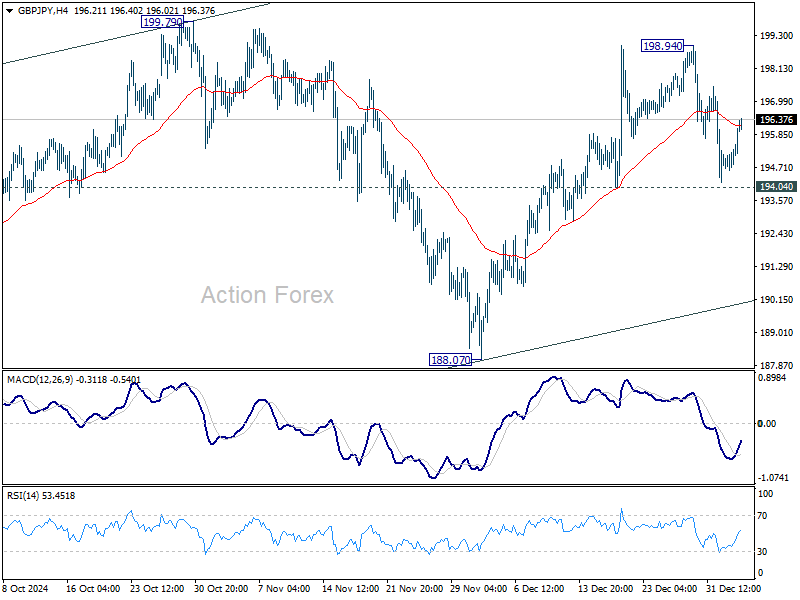

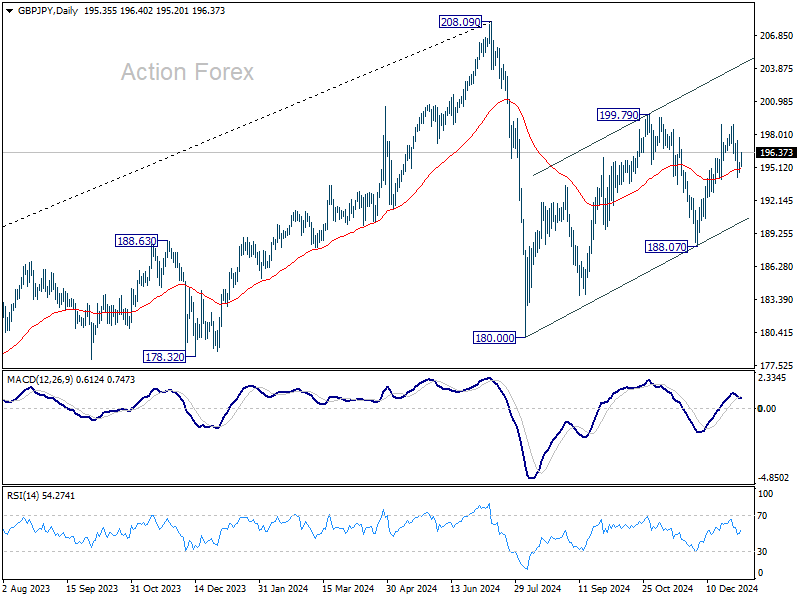

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.83; (P) 195.19; (R1) 195.74; More...

GBP/JPY recovers notably today but stays in range below 198.94 and intraday bias remains neutral. Outlook is unchanged that corrective pattern from 180.00 is still extending. Further rise is in favor with 194.04 minor support intact. On the upside, above 199.79 will will target channel resistance (now at 203.90). However, firm break of 194.04 will turn bias to the downside for 188.07 support instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

Yen Weakens Despite Risk-Off Sentiment,Jobs and Inflation Data to Drive Markets Ahead

Yen struggles today even as risk aversion set the tone across Asian markets. Nikkei extended its retreat after briefly breaching 40k psychological level last week, as the rally proved unsustainable for investors. Adding to Yen's woes, December PMI Services data highlighted only marginal growth, failing to provide a meaningful lift to the broader economy. Meanwhile, BoJ Governor Kazuo Ueda reiterated a cautious stance, offering no concrete hints about a rate hike this month. Last week’s recovery in Yen may turn out to be fleeting.

Elsewhere, commodity currencies emerge as the strongest performers today so far, extending their resilience from last week. However, their gains lack significant momentum, reflecting market caution. Meanwhile, Euro and Sterling are trading in a mixed manner, stabilizing after last week’s sharp losses. Dollar, Yen, and Swiss Franc are lagging behind, with Yen as the weakest performer.

Markets are bracing for a critical week ahead, with a slew of high-impact economic data on the docket. US Non-Farm payrolls and ISM services data will likely set the tone for the Dollar, particularly as markets remain firmly priced for Fed to pause its easing cycle this month. Inflation data from the Eurozone, Switzerland, and Australia will also attract attention, shaping the narrative around ECB, SNB, and RBA policies. Additionally, Canadian employment data will test the resilience of Loonie, which outperformed other commodity currencies last month but has recently shown signs of waning momentum.

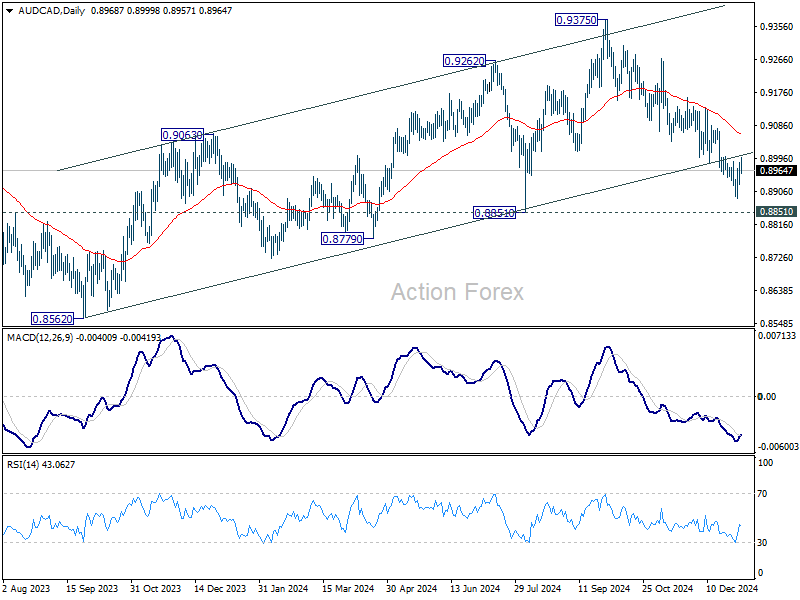

Technically, AUD/CAD's break of the medium term rising channel is a sign that whole corrective rally from 0.8562 has completed at 0.9375. Firm break of 0.8851 support will solidify this bearish case. However, strong bounce from current level, followed by sustained break of 55 D EMA (now at 0.9060) will keep this up trend intact. The outcome of Australia’s CPI and Canada’s employment data later this week will likely play a crucial role in determining the pair’s next significant move.

In Asia, Nikkei fell -1.47%. Hong Kong HSI is down -0.46%. China Shanghai SSE is down -0.14%. Singapore Strait Times is up 0.27%. Japan 10-year JGB yield rose 0.0357 to 1.129.

BoJ Ueda stresses caution on policy adjustments

BoJ Governor Kazuo Ueda reiterated the cautious stance on monetary policy adjustments at a Japanese Bankers Association event today. He emphasized that any interest rate hikes would depend on sustained improvements in economic and price conditions.

“Our stance is that we will raise the policy interest rate to adjust the degree of monetary easing if economic and price conditions keep improving,” Ueda stated.

However, he highlighted the need for vigilance regarding various risks, signaling that the timing of such adjustments would be carefully assessed. The governor also expressed his hopes for balanced growth in wages and prices in the coming year.

Japan's PMI services finalized at 50.9, optimism eases

Japan's service sector showed slight improvement in December, with final PMI Services index rising to 50.9 from 50.5 in November, indicating marginal growth. PMI Composite also increased to 50.5 from 50.1, reflecting modest stabilization in the broader economy.

Usamah Bhatti, Economist at S&P Global Market Intelligence, noted, "December data revealed sustained rises in both business activity and new business," with new orders growing at the fastest pace in four months. Employment in the service sector rose for the fifteenth consecutive month, signaling steady labor market gains. Despite these improvements, business optimism softened slightly.

The overall economic expansion was underpinned by softer contraction in manufacturing output and ongoing growth in the service sector. New orders across sectors expanded at their fastest rate since August, supported by the completion of outstanding work, particularly in manufacturing. However, optimism regarding future output declined, falling below the 2024 average.

China's services sector gains momentum, but Composite PMI signals broader economic strain

China’s services sector gained pace in December, with Caixin PMI Services rising to 52.2 from 51.5 in November, marking its highest level since May. However, the overall economic picture remains mixed as PMI Composite slipped to 51.4, its lowest since September. This divergence highlights that faster services growth was insufficient to offset the slowdown in manufacturing output expansion.

Wang Zhe, Senior Economist at Caixin Insight Group, remarked, “Prominent downward pressures remain, with tepid domestic demand and mounting unfavorable external factors.”

He added that sluggish employment and squeezed profit margins are weighing on market optimism. Declines in some gauges from the manufacturing PMI survey indicate that more time is needed to evaluate the consistency and effectiveness of recent policy stimulus.

Jobs and inflation: Critical data to drive first full week of 2025

As global markets enter the first full trading week of 2025, the economic calendar is packed with high-stakes events. US data, particularly Non-Farm Payrolls and ISM Services, will take center stage. Fed expectations for a pause in its easing cycle this month are solidifying, and the data is unlikely to disrupt this view unless prints are unexpectedly catastrophic. Fed minutes from December, also due this week, could offer additional context on policymakers’ risk assessments and rationales for the expected policy path.

Inflation will also be in the spotlight, with CPI releases from Eurozone, Switzerland, and Australia. Eurozone inflation is expected to rise modestly as energy base effects diminish, but this is unlikely to derail ECB’s measured pace of easing. ECB is still projected to cut rates again in January. In Switzerland, inflation should continue to hold steady stabilized at sub-1% levels, maintaining the case for SNB to proceed with further rate reductions later this year.

In Australia, the inflation picture is less clear. While the base case is still for RBA to commence rate cuts by May, steady monthly CPI readings at around 2% could bolster arguments for an earlier move in February. However, the broader outlook hinges on the upcoming quarterly inflation report due later this month.

Elsewhere, Japan’s cash earnings and household spending reports will offer insights into the domestic economy, but global uncertainties—particularly regarding US economic conditions—could push BoJ to maintain its cautious wait-and-see approach, even in the face of robust data.

Canada’s employment report will be a critical barometer for BoC’s monetary stance. BoC has signaled a slowdown in its easing pace this year, but labor market resilience—or lack thereof—will significantly influence the depth of its ongoing rate-cutting cycle.

Here are some highlights for the week:

- Monday: China Caixin PMI services; Swiss retail sales; Eurozone PMI services final, Sentix investor confidence; UK PMI services final; US PMI services final, factory orders.

- Tuesday: Japan monetary base; Australia building permits; Swiss CPI, foreign currency reserves; UK PMI construction; Eurozone CPI flash, unemployment rate; Canada trade balance, Ivey PMI; US trade balance, ISM services.

- Wednesday: Australia monthly CPI; Japan consumer confidence; Germany factory orders, retail sales; Eurozone PPI; US ADP employment, jobless claims, FOMC minutes.

- Thursday: Japan average cash earnings; Australia retail sales, goods trade balance; China CPI, PPI; Germany industrial production, trade balance; Eurozone retail sales.

- Friday: Japan household spending; Swiss unemployment rate; France consumer spending, industrial production; Canada employment; US non-farm payrolls, U of Michigan consumer sentiment.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.83; (P) 195.19; (R1) 195.74; More...

GBP/JPY recovers notably today but stays in range below 198.94 and intraday bias remains neutral. Outlook is unchanged that corrective pattern from 180.00 is still extending. Further rise is in favor with 194.04 minor support intact. On the upside, above 199.79 will will target channel resistance (now at 203.90). However, firm break of 194.04 will turn bias to the downside for 188.07 support instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

Greenback to Remain in Center of Attention in Run-up to Trump’s Inauguration

Markets

The dollar was talk of the town during the holiday period. We expect the greenback to remain in the center of attention in the run-up to president-elect Trump’s inauguration January 20. The US currency appreciated since the hawkish Fed policy meeting, resulting in a mere 40 bps of cuts expected in 2025, and got another boost at the start of the new year. Economic data remains solid with last week’s jobless claims and manufacturing ISM (new orders) case in point. EUR/USD end last week came close to the critical 1.0201 support zone. This 61.8% dollar recovery on the September 2022 – July 2023 decline is the final hurdle towards parity. EUR/USD recouped some of the losses over the last two trading sessions, including this morning’s, but that doesn’t change the technical picture. The trade-weighted dollar index hovers around 109, its best level since November 2022. USD/JPY has been trading just shy of 158 since the December 18 Fed meeting. JPY investors, fearing FX interventions, are wary to push it even further. It could be just a matter of time though. Other Asian currencies have suffered more, China’s yuan in particular. CNY broke above the USD/CNY 7.3 last Friday to 7.3288 this morning after state banks briefly stopped defending this psychologically important level. It may be a sign that China allows a weaker currency to support the ailing economy. The PBOC’s strong fixing rate this morning – from which CNY may deviate 2% in a daily perspective – does suggest that it won’t stand rapid, disorderly depreciation. In any case, the 16-year low of 7.3499 seen in August 2023 is just an inch away now. Core bonds have remained under pressure since yields started bottoming out around the start of December to either hit (Germany) or move beyond (US) the late 2024-highs. Friday’s (mostly European) bear flattening was an exception to the broader steepening trend. US yields rose between 3.3 and 4.4 bps across the curve. German rates added 3.2 (30-yr) to 6.1 bps (2-yr). We wouldn’t row against the tide, both for the dollar and for (long-term) rates, from a momentum perspective. The eco calendar this week does offer some important input for markets going forward. The US kicks off its first auction of the year with a $58bn 3-yr one tonight, followed by a 10-yr sale tomorrow and a 30-yr one on Wednesday. US November job openings & the December services ISM are scheduled for release tomorrow, along with European inflation data. Wednesday’s Fed meeting minutes and ADP job report are followed by the December payrolls on Friday.

News & Views

In an interview with CNN Prima news channel this weekend, Czech central bank (CNB) governor Ales Michl kept a (guarded) hawkish tone. He continues advocating a restrictive bias for both monetary and fiscal policy as inflation continues running somewhat above the 2.0% inflation target (2.8% in December). Michl in particular mentioned the fiscal gap as a source of persistent price pressures even as economic growth was subdued of late. As the Czech economy is currently not in a crisis modus, the CNB governor indicated that a balanced budget is the best way to fight inflation. Aside from the impact of fiscal policy, the CNB governor also mentioned ongoing services inflation and a potential recovery in the housing market as risks to containing inflation. CNB at the December meeting paused its easing cycle leaving the policy rate unchanged at 4.0% as it assessed the recent disinflation process as being incomplete. The Czech koruna recently found a new short-term equilibrium in the EUR/CZK 25.10/25 area.

China’s services activity in December expanded at the quickest pace since May of last year with the Caixin PMI rebounding from 51.1 to 52.2. According to the Caixin press release, the acceleration in business activity growth was supported by greater new business inflows. Quicker new business growth resulted in another accumulation of backlogged work. On the other hand, export business declined and services firms also lowered employment levels amid a reduction in business optimism. Finally, selling prices rose for the first time in six months as cost pressures intensified. The China composite index slowed from 52.3 to 51.4. Last week, the manufacturing gauge was reported at 50.5 (from 51.5 in November). The rise in services activity might be a first indication that domestic demand is improving after plenty of stimulus measures announced by the government at the end of last year, but more convincing confirmation is needed. The release at least didn’t prevent a further weaking of the yuan to USD/CNY 7.328, even as the PBOC kept the daily fixing at a stronger than expected level below USD/CNY 7.20 (7.1876).

BoJ Ueda stresses caution on policy adjustments

BoJ Governor Kazuo Ueda reiterated the cautious stance on monetary policy adjustments at a Japanese Bankers Association event today. He emphasized that any interest rate hikes would depend on sustained improvements in economic and price conditions.

“Our stance is that we will raise the policy interest rate to adjust the degree of monetary easing if economic and price conditions keep improving,” Ueda stated.

However, he highlighted the need for vigilance regarding various risks, signaling that the timing of such adjustments would be carefully assessed. The governor also expressed his hopes for balanced growth in wages and prices in the coming year.

China’s services sector gains momentum, but Composite PMI signals broader economic strain

China’s services sector gained pace in December, with Caixin PMI Services rising to 52.2 from 51.5 in November, marking its highest level since May. However, the overall economic picture remains mixed as PMI Composite slipped to 51.4, its lowest since September. This divergence highlights that faster services growth was insufficient to offset the slowdown in manufacturing output expansion.

Wang Zhe, Senior Economist at Caixin Insight Group, remarked, “Prominent downward pressures remain, with tepid domestic demand and mounting unfavorable external factors.”

He added that sluggish employment and squeezed profit margins are weighing on market optimism. Declines in some gauges from the manufacturing PMI survey indicate that more time is needed to evaluate the consistency and effectiveness of recent policy stimulus.

Japan’s PMI services finalized at 50.9, optimism eases

Japan's service sector showed slight improvement in December, with final PMI Services index rising to 50.9 from 50.5 in November, indicating marginal growth. PMI Composite also increased to 50.5 from 50.1, reflecting modest stabilization in the broader economy.

Usamah Bhatti, Economist at S&P Global Market Intelligence, noted, "December data revealed sustained rises in both business activity and new business," with new orders growing at the fastest pace in four months. Employment in the service sector rose for the fifteenth consecutive month, signaling steady labor market gains. Despite these improvements, business optimism softened slightly.

The overall economic expansion was underpinned by softer contraction in manufacturing output and ongoing growth in the service sector. New orders across sectors expanded at their fastest rate since August, supported by the completion of outstanding work, particularly in manufacturing. However, optimism regarding future output declined, falling below the 2024 average.