Sample Category Title

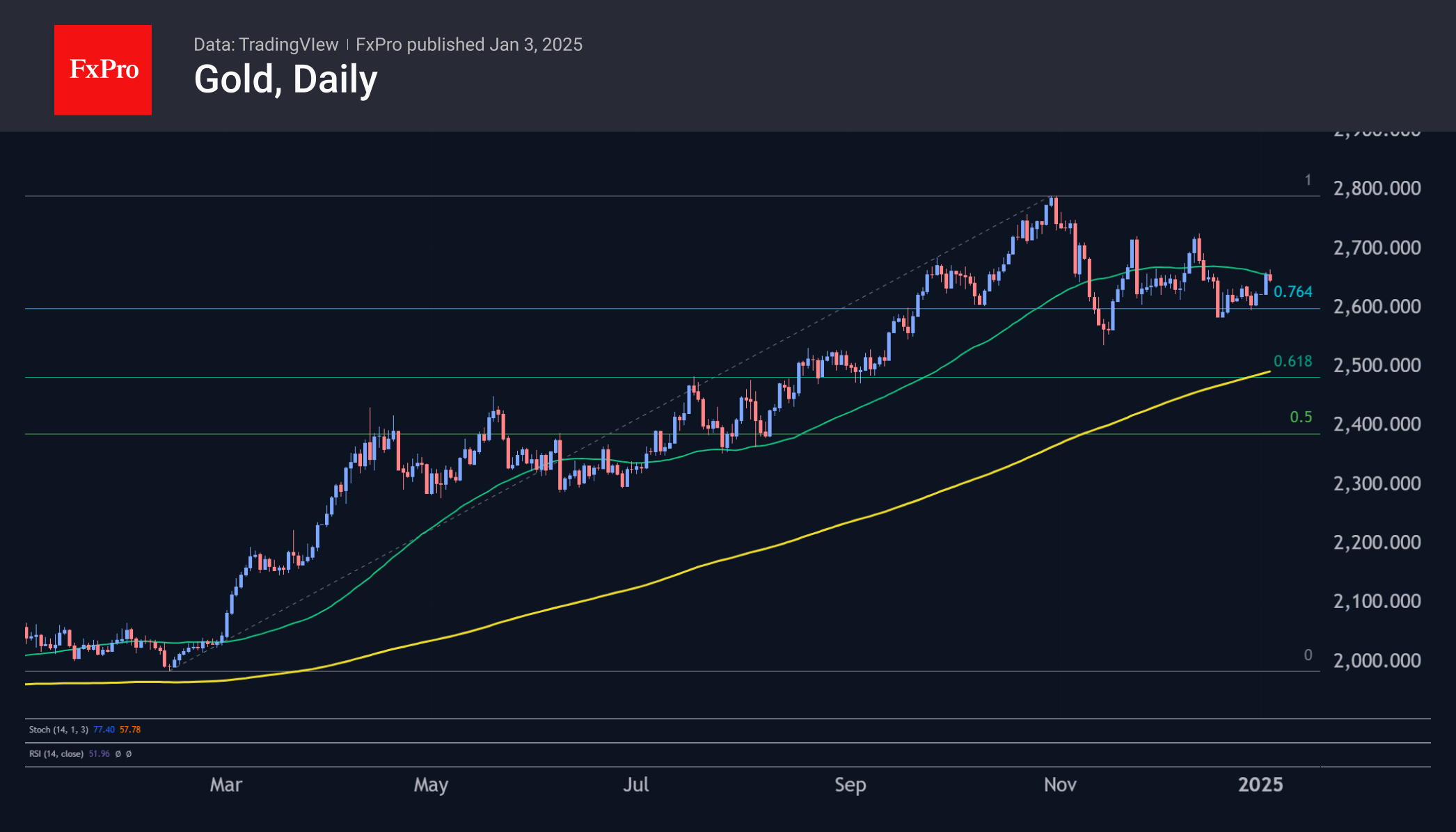

Gold Growth Halted But With Upside Risks

The pressure on risk assets on 31 December and 2 January, including a 1.5% rise in the dollar over the period, has not prevented Gold from strengthening. Although the market amplitude is still rather unimpressive, a simultaneous rise in the dollar and gold as equities fall is characteristic of periods of safe-haven traction.

If these sentiments find a solid footing, we could see the dollar’s bullish momentum develop. Much depends on the trade war situation. The further distancing of production chains is a signal for global speculators to step up their gold buying in anticipation of China and other emerging markets favouring gold over dollar-denominated bonds.

As with tariff uncertainty, the technical picture offers arguments for both bulls and bears.

Gold tested its 50-day moving average in the first trading session of the new year. A dip below it in November broke the uptrend and sent gold into a consolidation phase after a 12-month rally of more than 50%. Failure to stay above this curve for long in November, December and early January looks like a bearish signal: too many sellers looking to take profits.

However, the longer-term picture is bearish as the recent pullback looks like a shallow correction to the 76.4% level of the advance. Such shallow corrections are characteristic of strong bull markets. Breaking through the historic highs above $2800 in the next few months will signal the start of growth towards the $3400 area. The cancellation of this scenario will be a failure below $2550 ($100 below current prices), but even then, there is a chance that we will see a transition to a classic correction rather than a long-term reversal.

Fed Barkin sees upside growth potential

Richmond Fed President Thomas Barkin expressed a cautiously optimistic outlook during remarks today, highlighting economic growth upside while noting inflation risks tied to labor market strength.

"How economic policy uncertainty resolves will matter. But, with what we know today, I expect more upside than downside in terms of growth," he stated.

Barkin also flagged that hiring trends could add upward pressure on inflation if the job market strengthens further.

Barkin noted that financial markets appear more aligned with Fed's projected slower pace of interest rate cuts this year, adding that there seems to be broader acceptance of persistently higher long-term interest rates.

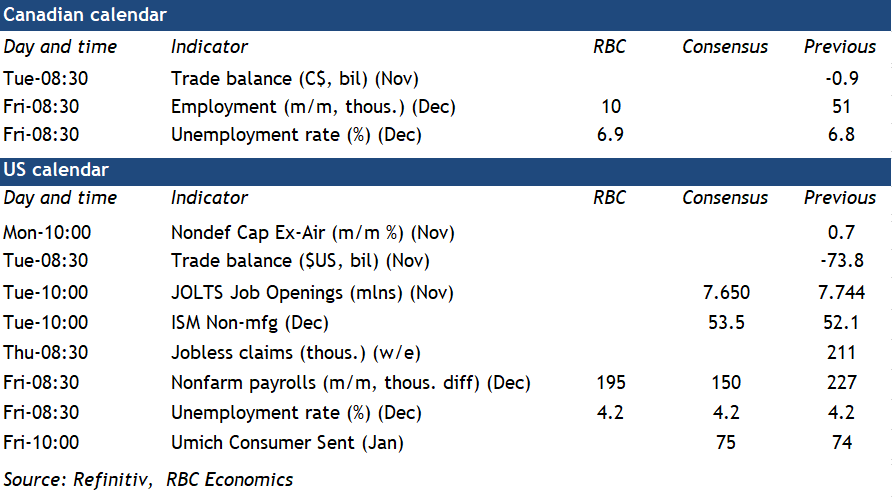

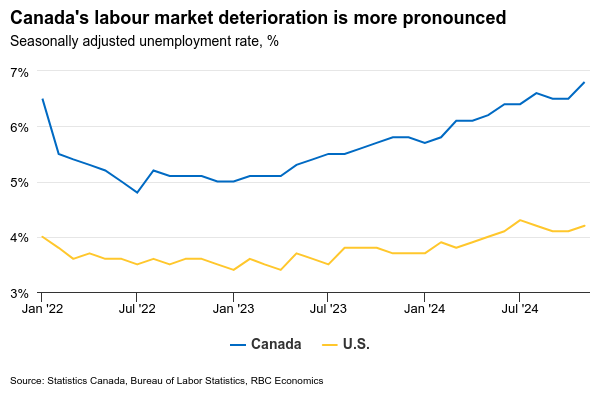

Canada’s Labour Market Likely Continued to Underperform at the End of 2024

Canadian and U.S. job market reports for December on Friday will mark the first major data releases of the year ahead of interest rate decisions later in the month for both the Bank of Canada and the U.S. Federal Reserve.

Canada’s labour market likely continued to underperform a resilient U.S. one. We look for the Canadian unemployment rate to edge up to 6.9% in December from 6.8% in November. Ahead of the December print, the unemployment rate has risen by 1 percentage point in one year (and 2 percentage points from cycle lows). We expect Canada added 10,000 jobs in December despite a rising unemployment rate. This has broadly been a story of the pace of job creation (329,000 over the last year) not keeping up with labour market growth (605,000 participants).

The lagged impact of earlier and more aggressive interest rate cuts from the BoC in 2024 compared to other parts of the world is expected to help stabilize the labour market early in 2025, and slower population growth will limit labour force increases. But for now, lower hiring demand means the unemployment rate is not likely at its peak yet. Wage growth has been resilient, but is expected to slow as job openings fall amid higher unemployment.

In the U.S., on the other hand, we’ve seen a more muted deterioration in the jobs market. The unemployment rate has risen by 0.5 percentage points over the past year, and by 0.8 percentage points from its lowest point in the cycle. But, it is still low by historical standards, and consistent with a labour market normalizing rather than faltering. We look for payroll employment to rise by 195,000 in December—above the 173,000 average over the previous three months, and for the unemployment rate to hold steady at 4.2%. Job openings have continued to decline, and the share of unemployment coming from layoffs has continued to gradually increase. But, we continue to expect labour markets to remain resilient in 2025, in a big part thanks to the positive impacts of an unusually large government budget deficit for this point in the economic cycle.

We continue to expect both the BoC and the Fed will cut interest rates by 25 basis points later this month, but the Fed will pause after that reduction, while the BoC continues cutting into mid-year to address an underperforming Canadian economy.

Week ahead data watch

US ISM Manufacturing Index Gains Again in December

The ISM Manufacturing Index firmed to 49.3 in December from 48.4 last month, and ahead of the step back to 48.2 expected. The deceleration in the manufacturing sector slowed again, as a broader segment of the industry reported growth.

Seven of 18 industries reported growth for the month – up from three in November. Despite none of the six largest industries reporting growth, 52% of manufacturing GDP reported a contraction, down from 66% in November.

Demand conditions showed another notable improvement, flipping back into growth territory. The new orders reported its second consecutive expansion (52.5), while new export orders (50.0) ended a months-long period of decline. Moreover, despite an improvement in production, backlogs of orders shrank at a slower pace than in November (45.9 vs. 41.8).

The production index gained again, reaching expansion territory (50.3) for the first time since May. Employment took a step back (45.3) to close out 2024 with it's 11th contraction of the year.

Price gains accelerated last month (52.5), as the price index reported rising prices for the eleventh time since the start of the year.

Key Implications

A good report for the manufacturing sector to close out 2024. New orders built on last month's momentum ending the year in positive territory, while export orders have also clawed their way back from a prolonged contraction. Although further interest rate cuts might come at a slower clip, any additional monetary easing will be welcome for the beleaguered sector.

Unfortunately for a manufacturing sector that is starting to show some verve, 2025 could be a rocky ride as uncertainty about the outlook could weigh on investment plans. On the downside, the risk that tariffs and trade restrictions impact supply chains and dent global growth persists, while the future of manufacturing subsidies related to the Inflation Reduction Act are in doubt. Conversely, any further tax cuts could help offset the deleterious effects from a ramp up in restrictive trade policies and higher interest rates.

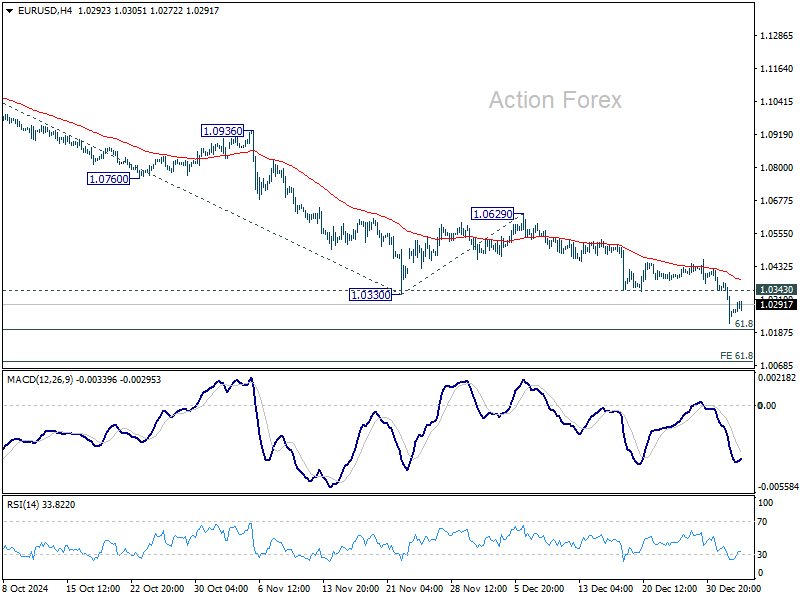

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0203; (P) 1.0289; (R1) 1.0353;More...

Intraday bias in EUR/USD remains neutral for the moment. Fall from 1.1213 is in progress to 1.0199 fibonacci level. Decisive break there will solidify the case of larger bearish trend reversal. Next target will be 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. On the upside, above 1.0343 support turned resistance will turn intraday bias neutral first. But outlook will now stay bearish as long as 1.0629 resistance holds, in case of recovery.

In the bigger picture, current development suggests that rebound from 0.9534 (2022 low) has already completed at 1.1274 after rejection by 55 M EMA. Deeper fall should be seen to 61.8 retracement of 0.9534 to 1.1274 at 1.0199. Sustained trading below there will pave way back to 0.9534 low. This will now remain the favored case as long as 1.0629 resistance holds.

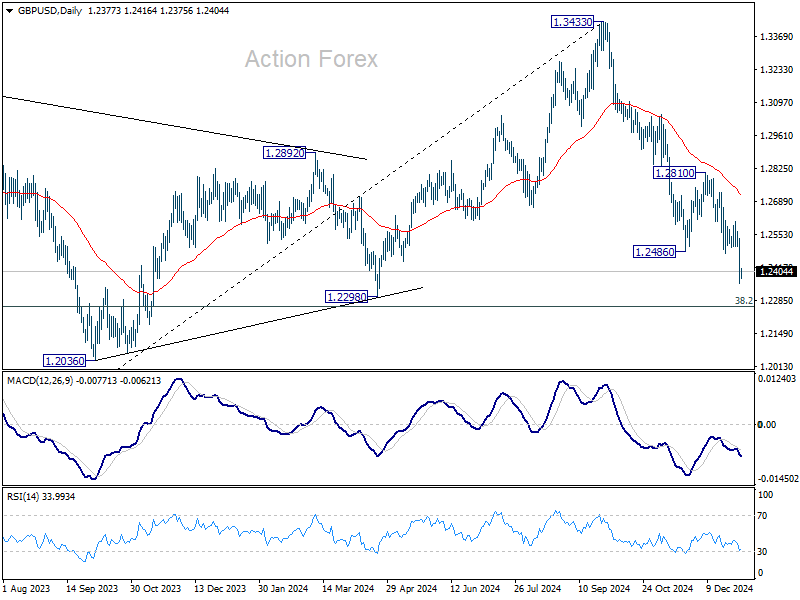

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2309; (P) 1.2425; (R1) 1.2497; More...

GBP/USD's fall is still in progress and intraday bias remains neutral. Decline from 1.3433 should target 1.2256/98 cluster support zone. Strong support is expected there to contain downside to bring rebound, at least on first attempt. On the upside, break of 1.2474 support turned resistance will turn intraday bias neutral first. However, decisive break of 1.2256/98 will carry larger bearish implications.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

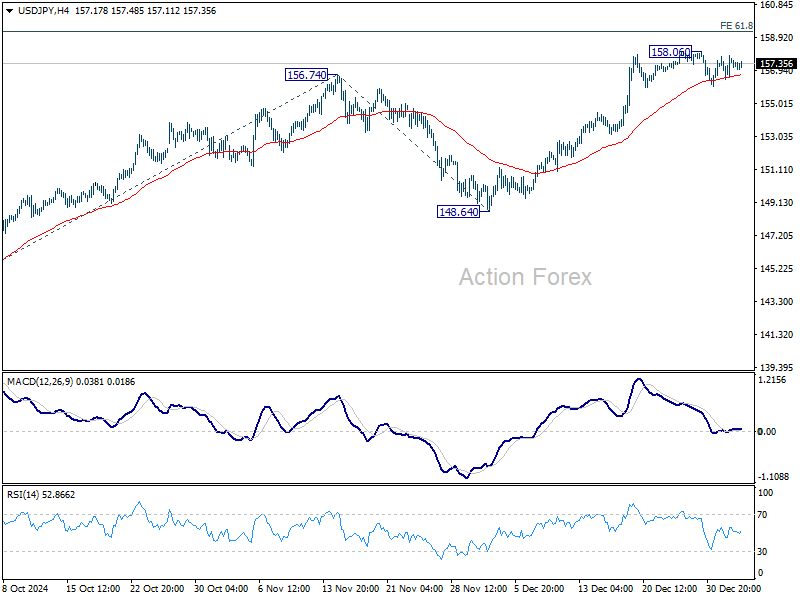

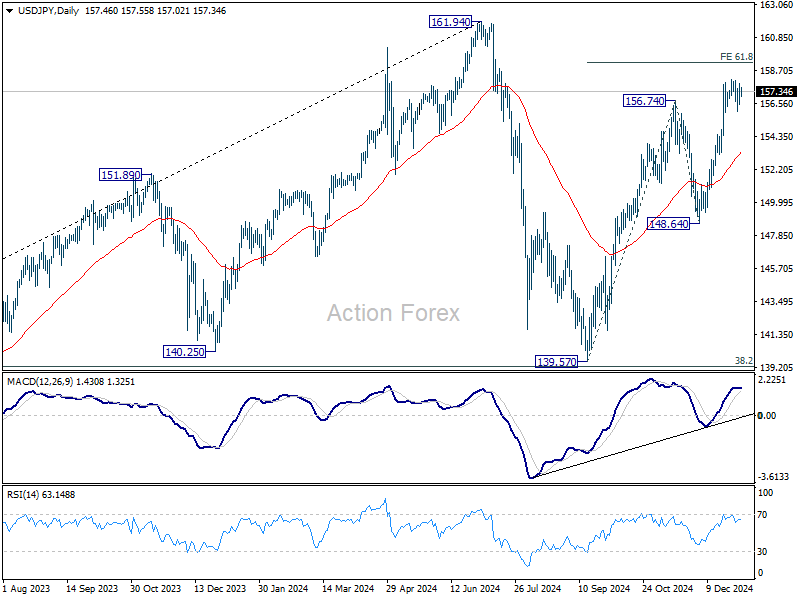

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.69; (P) 157.27; (R1) 158.10; More...

No change in USD/JPY's outlook as consolidation continues in tight range below 158.06. While another retreat cannot be ruled out, outlook will stay bullish as long as 55 D EMA (now at 153.34) holds. On the upside, above 158.06 will resume the rally from 139.57 to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will pave the way back to 161.94 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Manufacturing Stabilization Supports Dollar, European Struggle Continues

Dollar strengthened modestly following the latest ISM Manufacturing PMI, which indicated some stabilization in the US manufacturing sector toward the end of 2024. Despite the improvement, the sector continues to face challenges, with half of its industries still contracting.

The ISM report did little to shift expectations that Fed will pause its easing cycle at its next meeting on January 29, with fed fund futures pricing an 88% chance of a hold. Market attention now turns to next week’s ISM services data and the non-farm payroll report to further solidity this expectation.

For the holiday-shortened week, Yen is currently the best perform, in tight race with second-placed Dollar, while Canadian is the third. On the other hand European majors are clearly struggling with Sterling at the bottom, followed by Euro and then Swiss Franc. Aussie and Kiwi are positioning in the middle.

In Europe, at the time of writing, FTSE is down -0.38%. DAX is down -0.62%. CAC is down -1.49%. UK 10-year yield is down -0.0335 at 4.566. Germany 10-year yield is up 0.032 at 2.415. Earlier in Asia, Japan was still on holiday. Hong Kong HSI rose 0.70%. China Shanghai SSE fell -1.57%. Singapore Strait Times rose 0.03%.

US ISM manufacturing improves to 49.3, but remains in contraction territory

US ISM Manufacturing PMI edged up from 48.4 to 49.3 in December, exceeding market expectations of 48.3. Despite the improvement, the index remained below the 50.0 threshold, signaling contraction for the ninth consecutive month and for the 25th time in the past 26 months.

The ISM highlighted that the December reading corresponds to an annualized 1.9% growth in real GDP, indicating a modest contribution to the broader economy.

Delving into the subcomponents, new orders climbed from 50.4 to 52.5, while production improved notably, rising from 46.8 to 50.3. However, employment fell sharply from 48.1 to 45.3. Additionally, prices accelerated, increasing from 50.3 to 52.5, pointing to renewed input cost pressures.

Yuan Pressure Against Dollar, But Rises Against CFETS Basket

The Chinese Yuan presented an interesting paradox in today’s market action. Onshore Yuan sank below 7.3 mark against US Dollar, registering a 14-month low. This decline has intensified speculation that the People's Bank of China might be adopting a more lenient stance toward currency depreciation. Such a move could be part of broader efforts to bolster economic growth amid mounting headwinds. The downward bias has been further fueled by the possibility of a renewed “Trade War 2.0” under the incoming US administration.

Conversely, the CFETS RMB Index—a measure of the Yuan’s trade-weighted performance against a basket of currencies—surged to its highest level since October 2022. Although primarily driven by the relative weakness of major currencies versus the Dollar, this uptick hints at potential challenges for China’s export competitiveness to other key markets.

These moves also coincide with CFETS basket weighting adjustments for 2025, including reductions in the weightings of Dollar (from 19.46% to 18.903%), Euro (from 18.08% to 17.902%), and Yen (from 8.963% to 8.584%).

The larger question remains: How far is China willing to let Yuan depreciate? This is a mounting question given the uncertainty surrounding any trade measures the US might impose after Donald Trump’s January 20 inauguration. Beijing’s true intentions would become clearer after that.

Technically, it does look like that USD/CNH (Dollar vs offshore Yuan) is ready to resume it's long term up trend from 6.3057 (2022 low). Decisive break of 7.3745 (2022 high) will pave the way to 100% projection of 6.6971 to 7.3673 from 6.9709 at 7.6411.

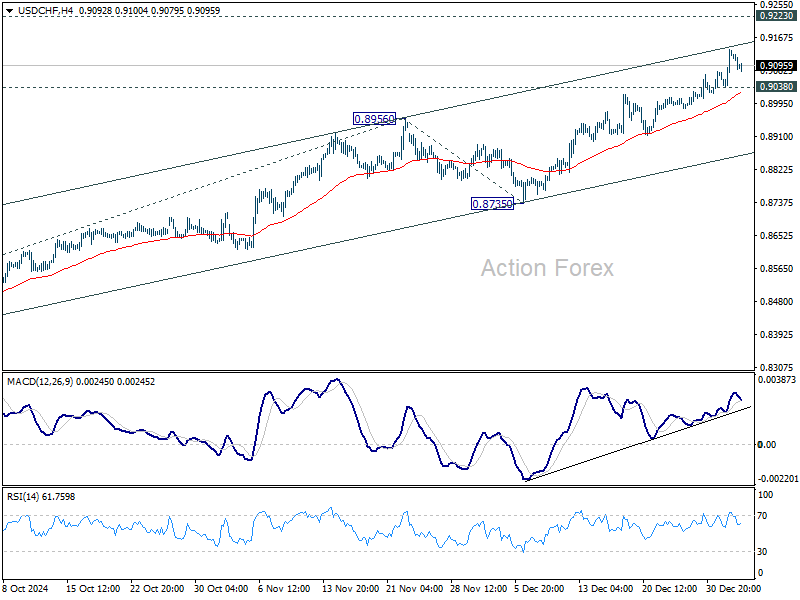

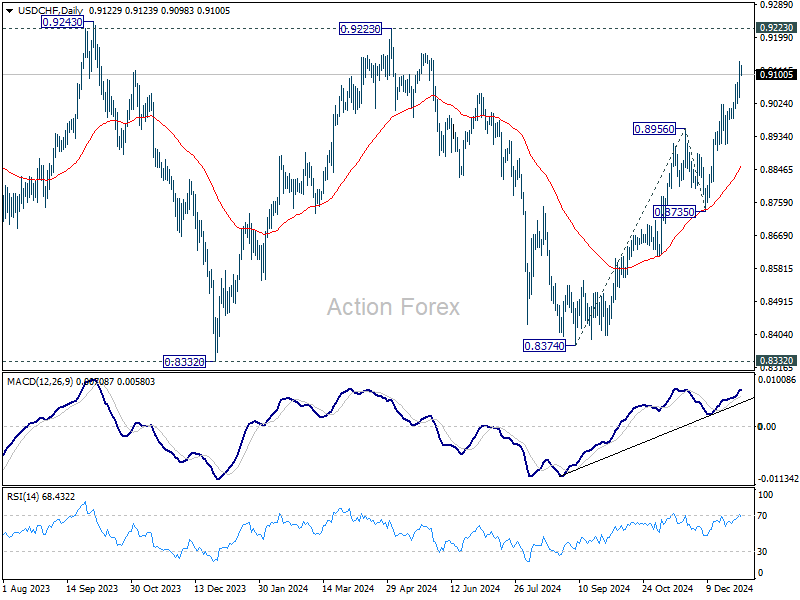

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9063; (P) 0.9100; (R1) 0.9161; More…

Intraday bias in USD/CHF stays on the upside for now despite current shallow retreat. Rally from 0.8374 is in progress for 0.9223 key resistance. Strong resistance is expected there to limit upside, at least on first attempt. On the downside, below 0.9038 minor support will turn intraday bias neutral first. Nevertheless, decisive break of 0.9223 will carry larger bullish implications.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9063; (P) 0.9100; (R1) 0.9161; More…

Intraday bias in USD/CHF stays on the upside for now despite current shallow retreat. Rally from 0.8374 is in progress for 0.9223 key resistance. Strong resistance is expected there to limit upside, at least on first attempt. On the downside, below 0.9038 minor support will turn intraday bias neutral first. Nevertheless, decisive break of 0.9223 will carry larger bullish implications.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

US ISM manufacturing improves to 49.3, but remains in contraction territory

US ISM Manufacturing PMI edged up from 48.4 to 49.3 in December, exceeding market expectations of 48.3. Despite the improvement, the index remained below the 50.0 threshold, signaling contraction for the ninth consecutive month and for the 25th time in the past 26 months.

The ISM highlighted that the December reading corresponds to an annualized 1.9% growth in real GDP, indicating a modest contribution to the broader economy.

Delving into the subcomponents, new orders climbed from 50.4 to 52.5, while production improved notably, rising from 46.8 to 50.3. However, employment fell sharply from 48.1 to 45.3. Additionally, prices accelerated, increasing from 50.3 to 52.5, pointing to renewed input cost pressures.