Sample Category Title

AUD/USD Weekly Report

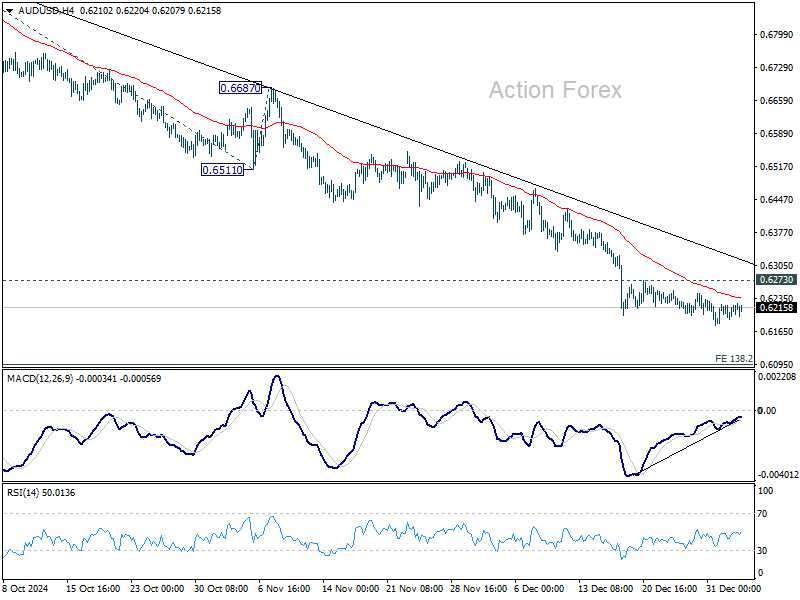

AUD/USD edged lower last week but lost momentum just ahead of 0.6169 key support. Further decline remains in favor as long as 0.6273 resistance holds. Decisive break of 0.6169 will target 138.2% projection of 0.6941 to 0.6511 from 0.6687 at 0.6074. However, considering bullish convergence condition in 4H MACD, break of 0.6273 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

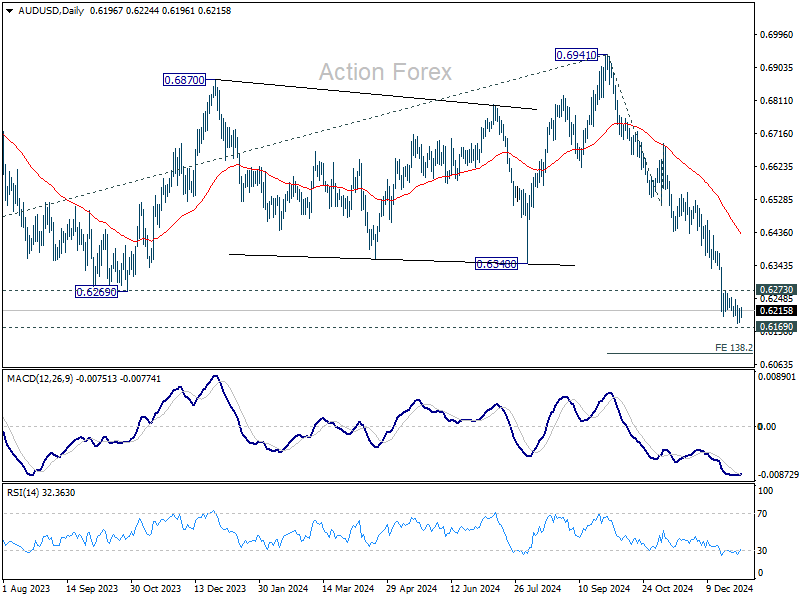

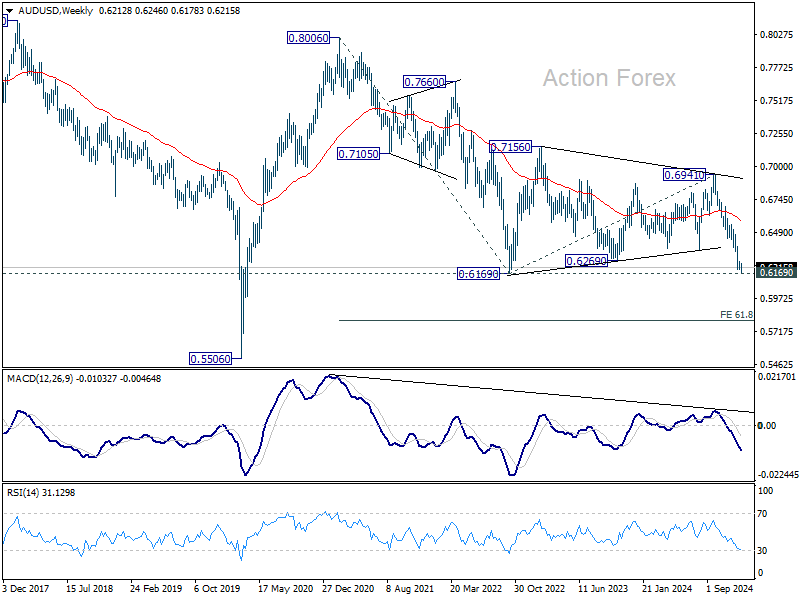

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006, and could have completed at 0.6941 already. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It's unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen as the second leg of the pattern. Hence, even in case of deeper fall, strong support should emerge above 0.5506 to contain downside to bring reversal.

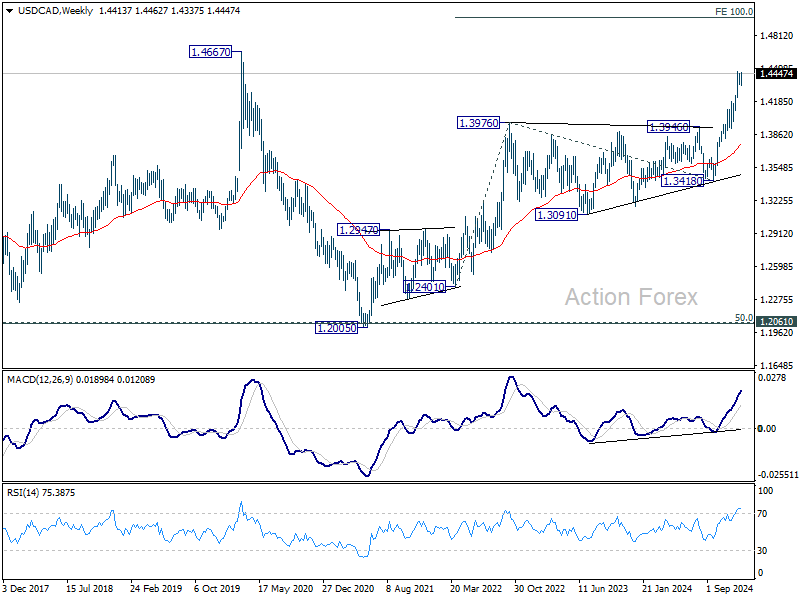

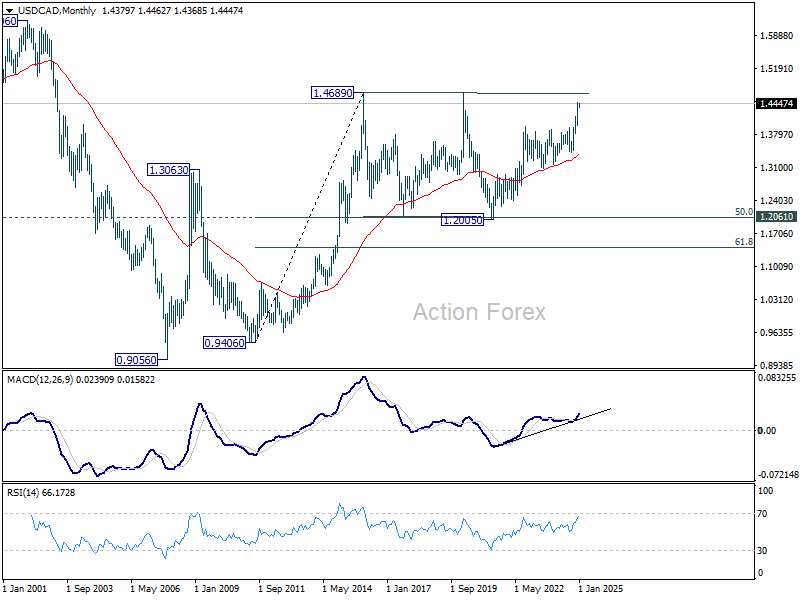

USD/CAD Weekly Outlook

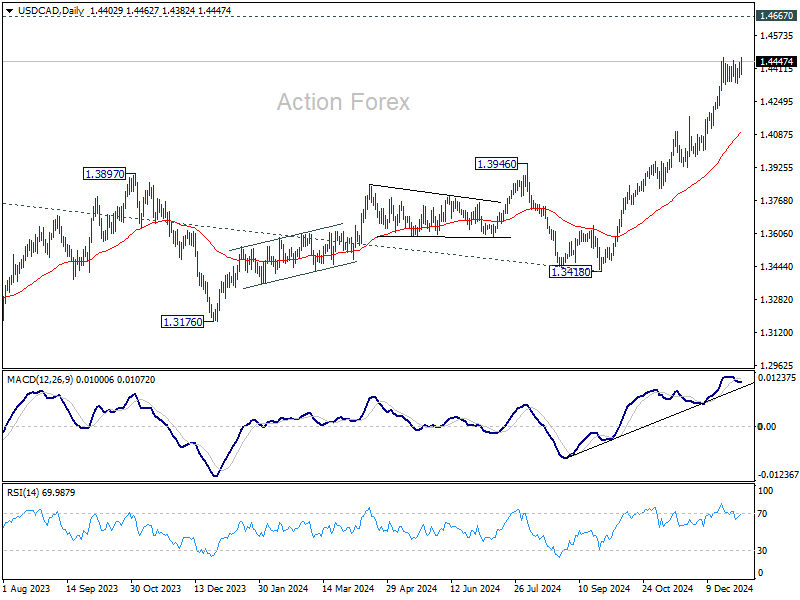

USD/CAD stayed in consolidation below 1.4466 last week. Initial bias stays neutral this week first. Outlook will stay bullish as long as 1.4304 support holds. Break of 1.4466 will resume larger up trend to 1.4667/89 long term resistance zone. However, firm break of 1.4304 will turn bias to the downside for deeper pull back.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.3418 support holds.

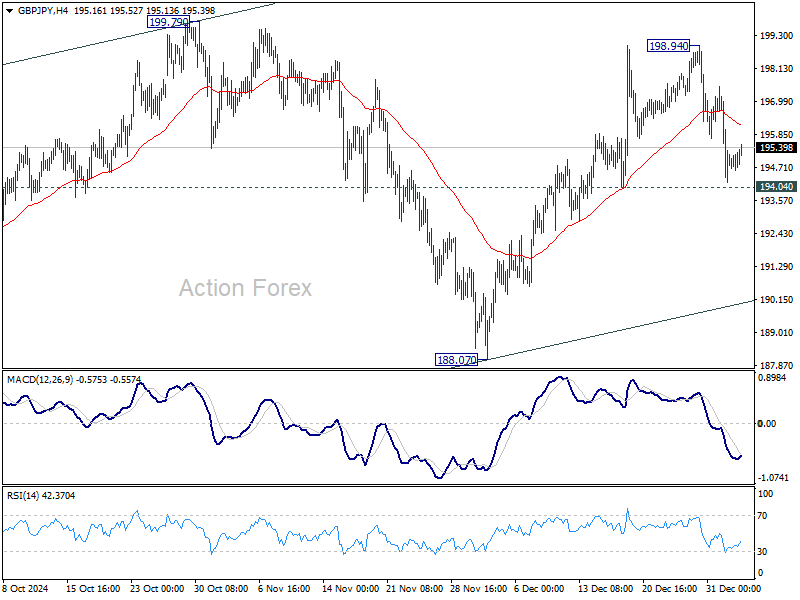

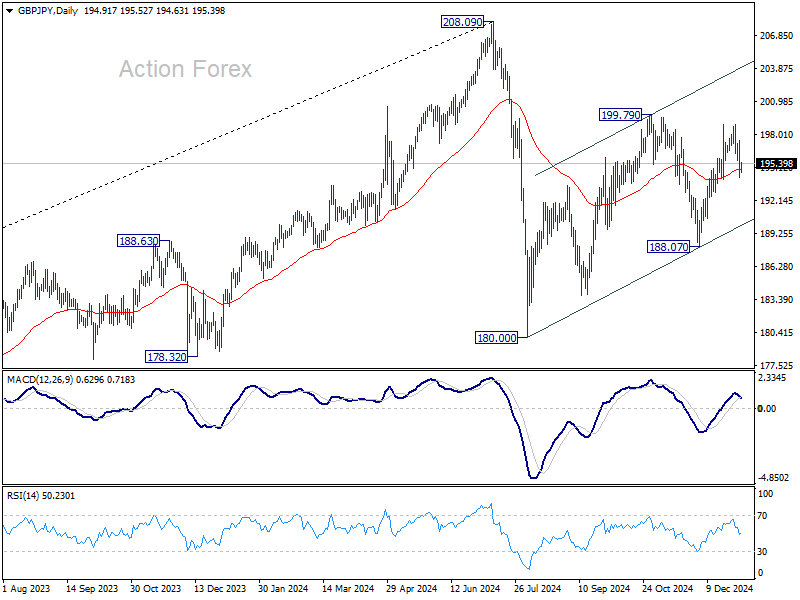

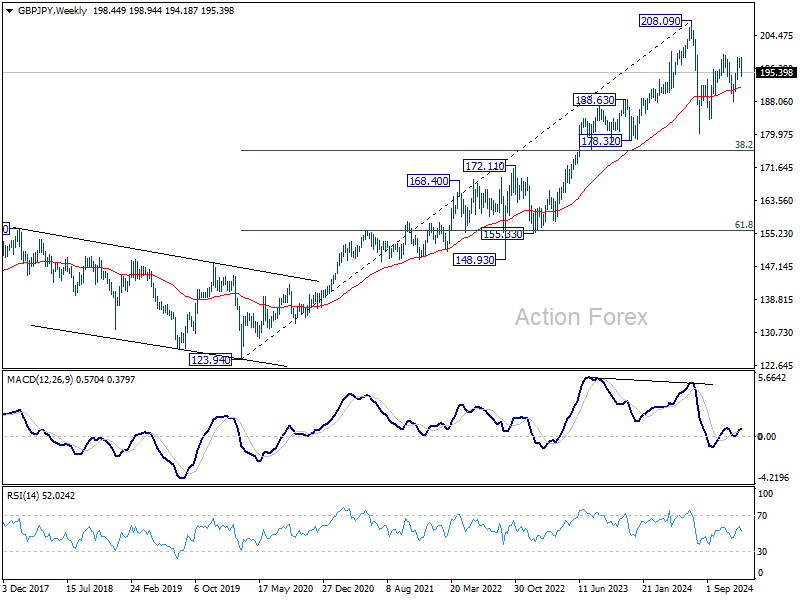

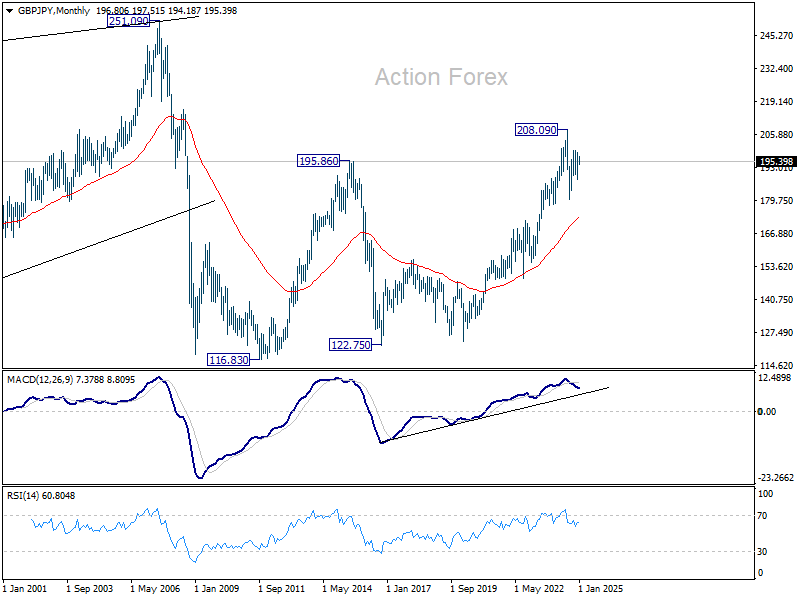

GBP/JPY Weekly Outlook

GBP/JPY retreated sharply after edging higher to 198.94 last week but stays above 194.04 support. Initial bias stays neutral this week first and outlook is unchanged. Corrective pattern from 180.00 is still extending. On the upside, above 199.79 will will target channel resistance (now at 203.90). However, firm break of 194.04 will turn bias to the downside for 188.07 support instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

In the longer term picture, while a medium term top was formed at 208.09 (2024 high), it's still early to conclude that the up trend from 122.75 (2016 low) has completed. But GBP/JPY is at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 173.52).

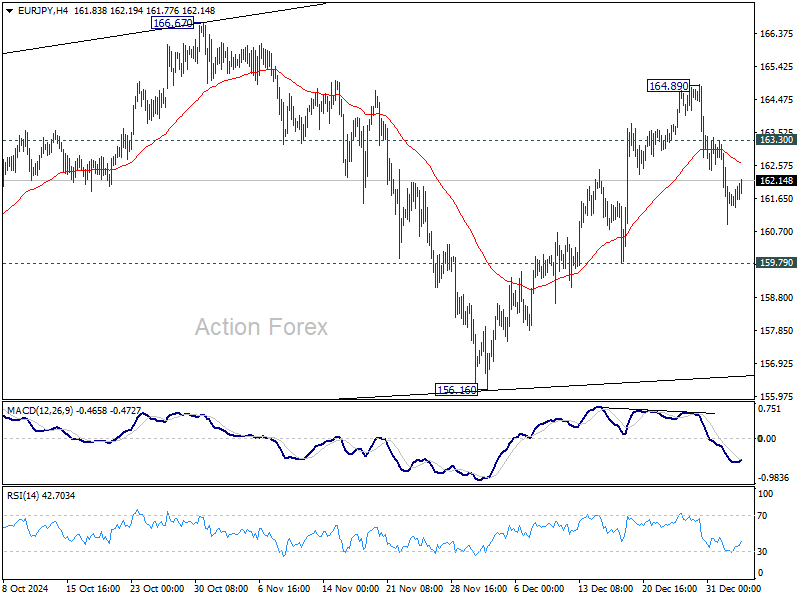

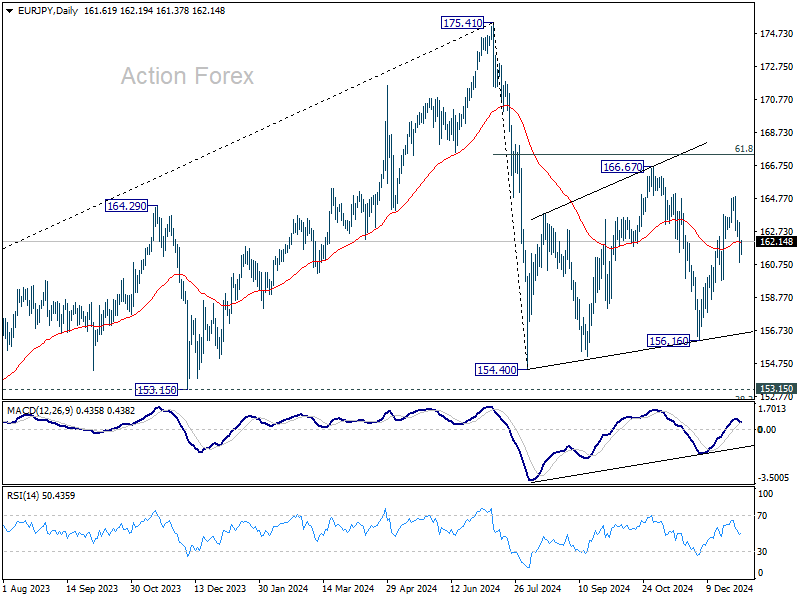

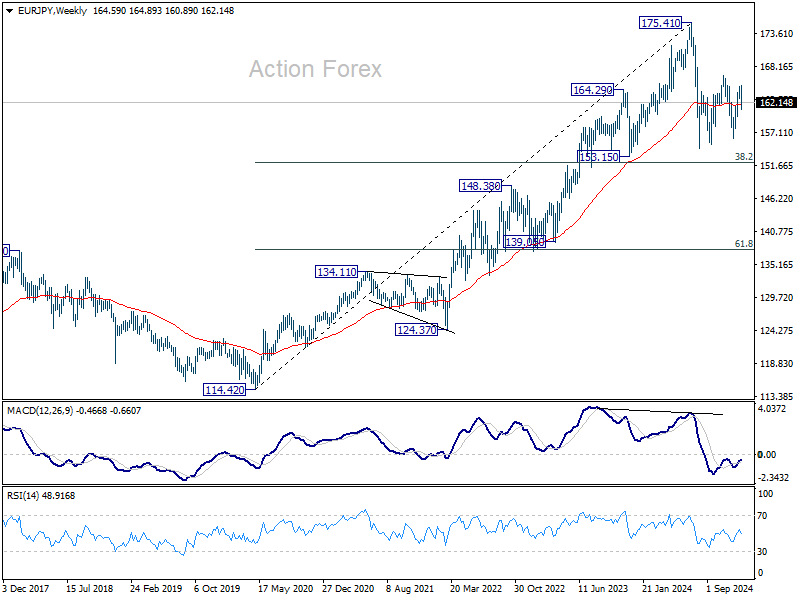

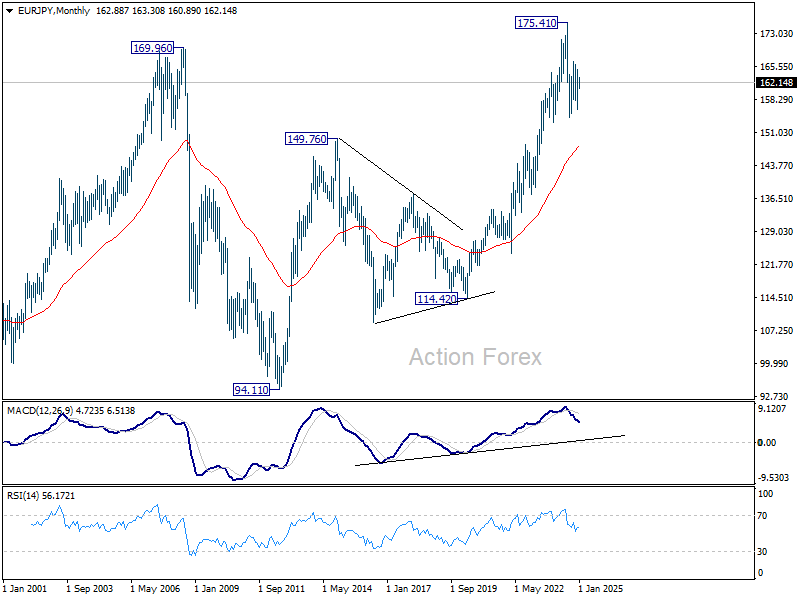

EUR/JPY Weekly Outlook

EUR/JPY edged higher to 164.89 last week but retreated sharply from there. But overall outlook is unchanged that corrective pattern from 154.40 is still extending. Initial bias remains neutral this week first. Above 163.30 minor resistance will bring retest of 164.89 first. Break there will target 166.67 resistance next.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

In the long term picture, while 175.41 is at least a medium term top, it's still early to conclude that up trend from 94.11 (2012 low) has completed. A medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 148.21).

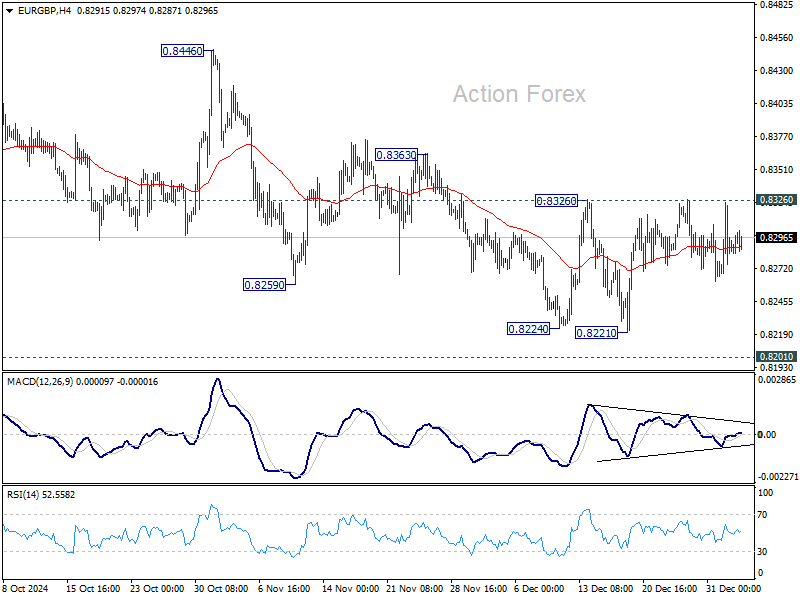

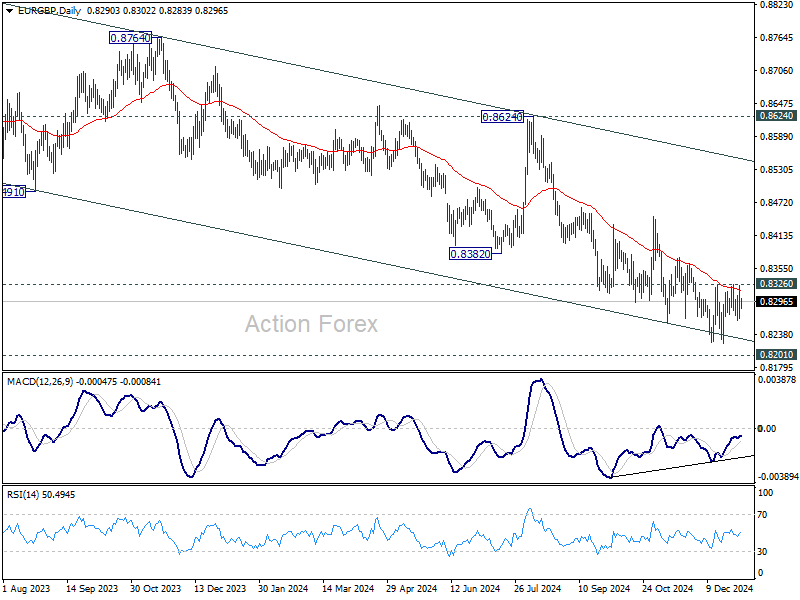

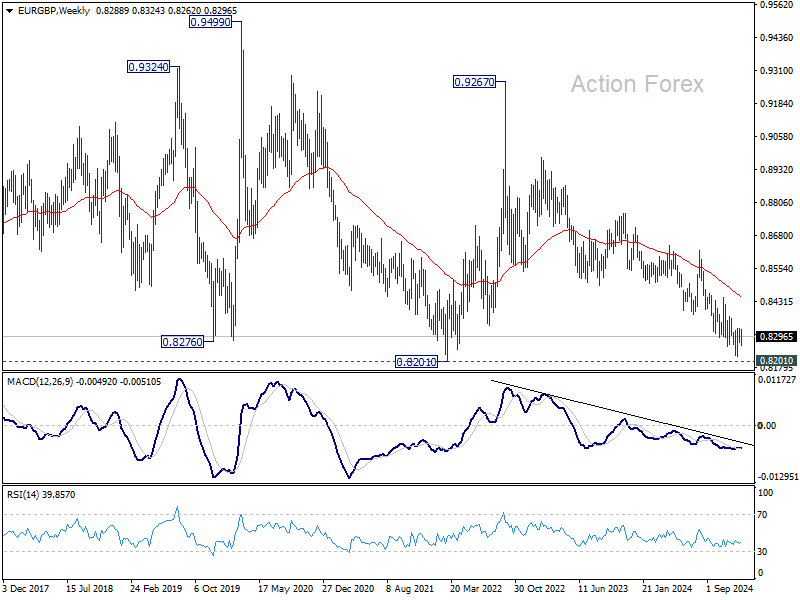

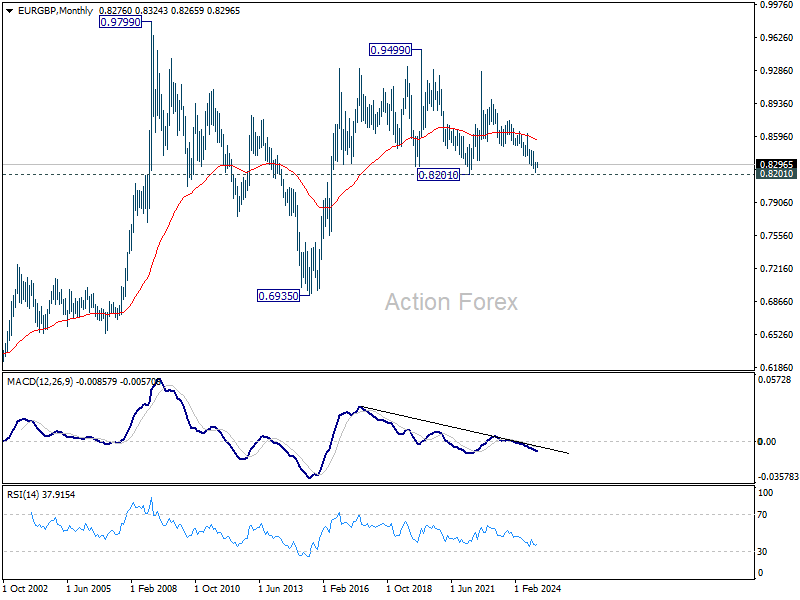

EUR/GBP Weekly Outlook

EUR/GBP stayed in sideway trading in range of 0.8221/8326 last week and outlook is unchanged. Initial bias remains neutral this week first. On the upside, firm break of 0.8326 resistance will confirm short term bottoming at 0.8221, ahead of 0.8201 key support. Intraday bias will be turned back to the upside for 0.8446 structural resistance next.

In the bigger picture, focus remains on whether 0.8201 key support (2022 low) is strong enough to complete the whole down trend from 0.9267 (2022 high). In any case, medium term outlook will be neutral at best until decisive break of 0.8624 key resistance. Risk will stay on the downside even in case of strong rebound.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

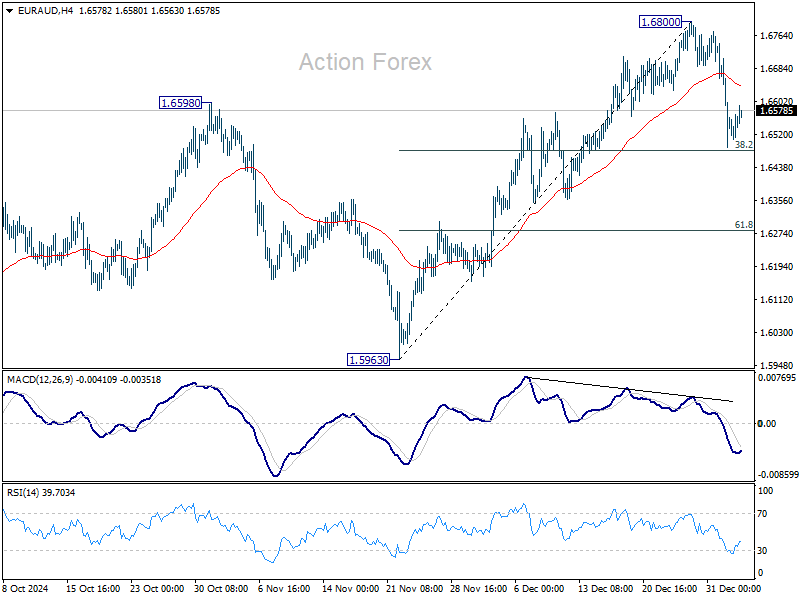

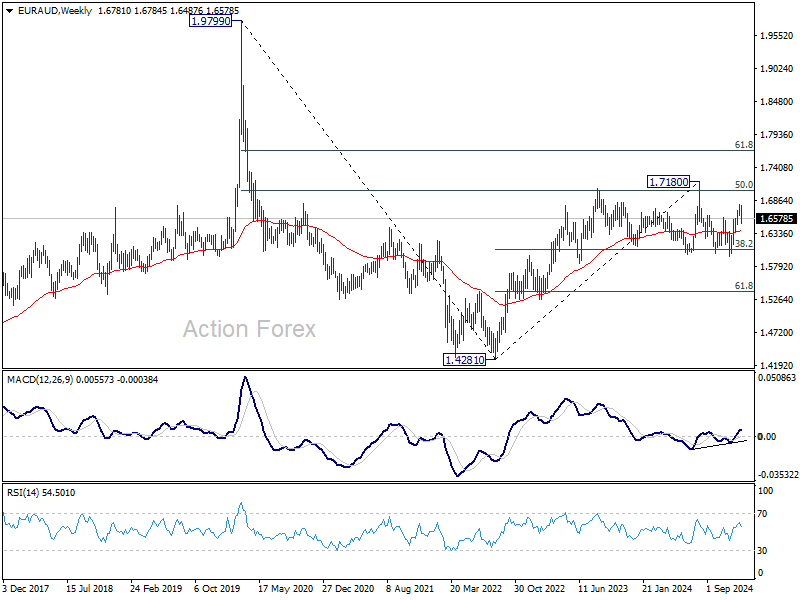

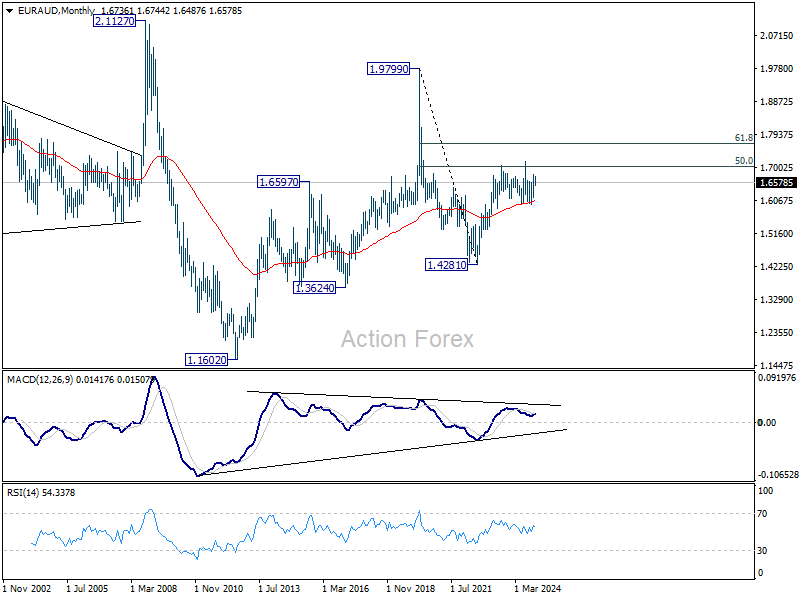

EUR/AUD Weekly Outlook

EUR/AUD's deep retreat last week confirmed short term topping at 1.6800. Yet, it recovered just ahead of 38.2% retracement of 1.5963 to 1.6800 at 1.6480. Initial bias is turned neutral this week first. Risk is now mildly on the downside as long as 1.6800 resistance holds, in case of extended recovery. Firm break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed and deeper decline would be seen.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6073) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

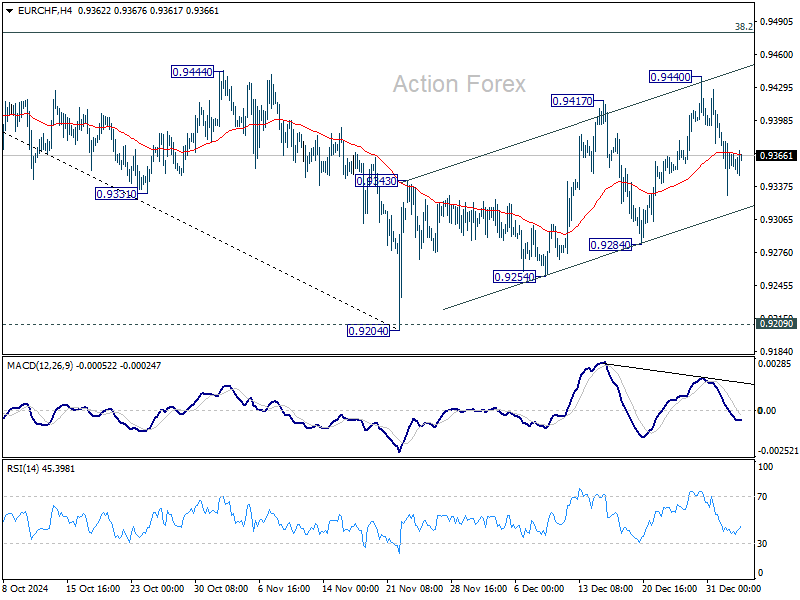

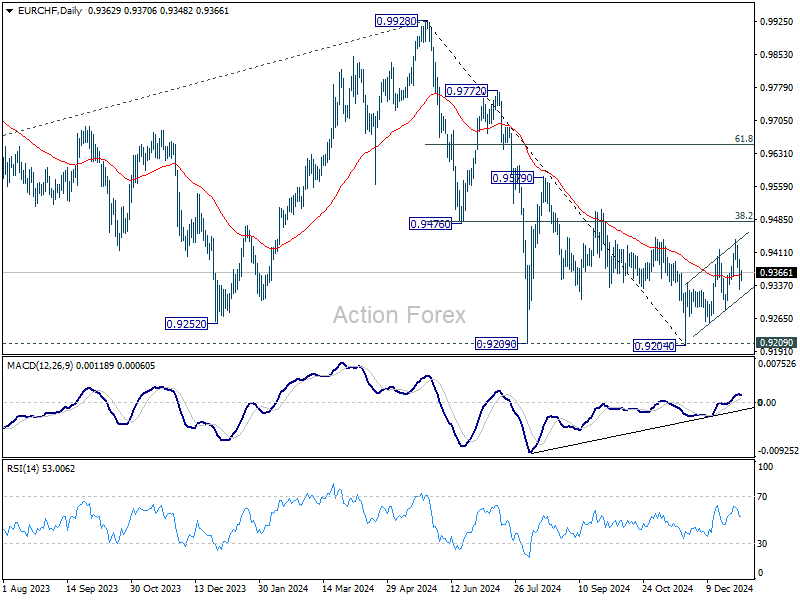

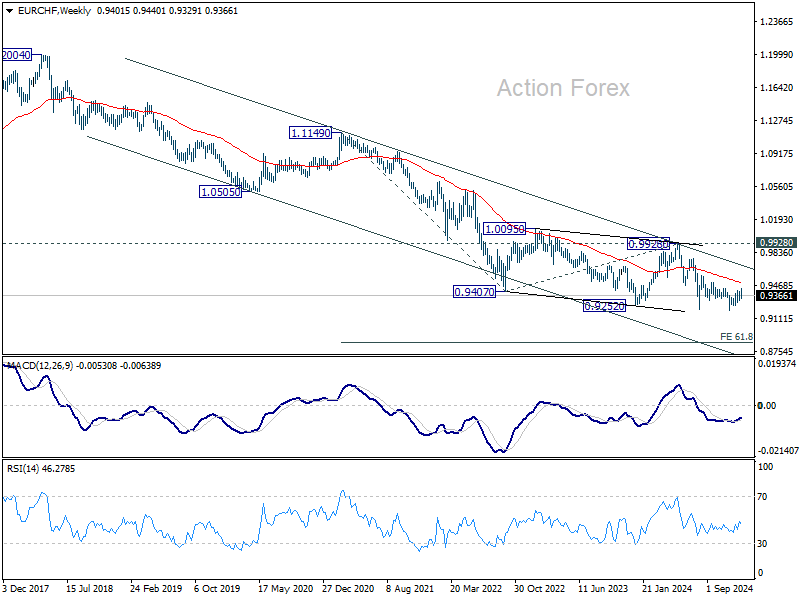

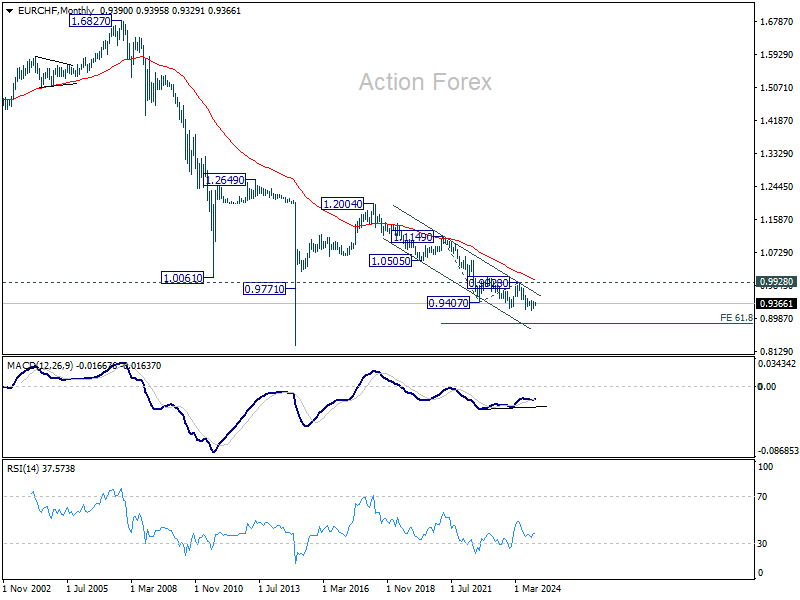

EUR/CHF Weekly Outlook

EUR/CHF reversed after edging higher to 0.9440 last week but stayed in near term rising channel. Corrective rebound from 0.9204 could still extend higher. But upside should be limited by 0.9481 fibonacci resistance. On the downside, firm break of 0.9284 support will argue that the correction has completed, and bring retest of 0.9204 low.

In the bigger picture, while rebound from 0.9204 might extend higher, strong resistance could be seen from 38.2% retracement of 0.9928 to 0.9204 at 0.9481 to limit upside. Down trend from 0.9928 (2024 high) is still in favor to resume through 0.9204/9 support zone at a later stage.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption to 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

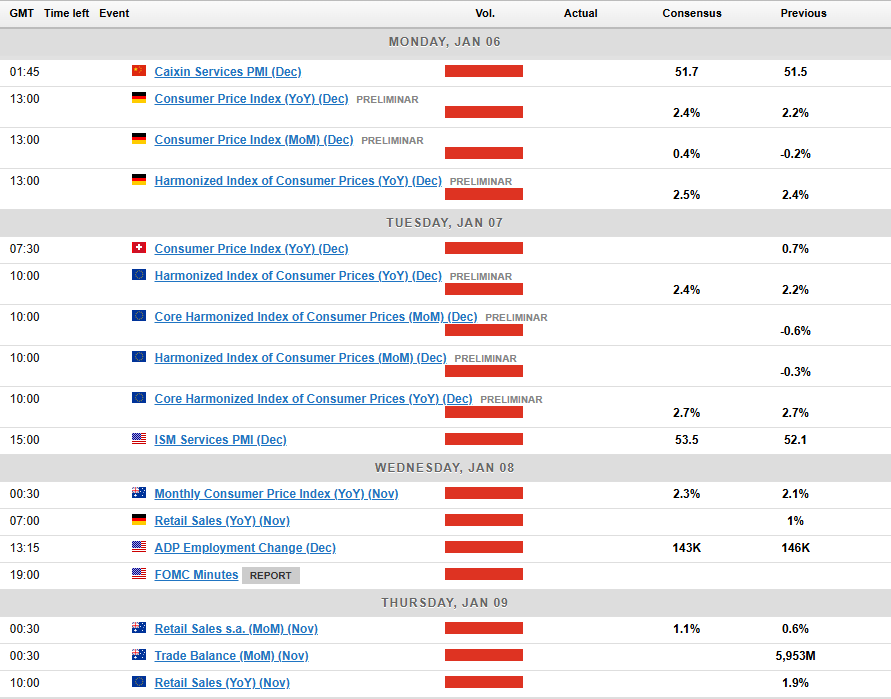

Summary 1/6 – 1/10

Monday, Jan 6, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Services PMI Dec F | 51.4 | 51.4 |

| 01:45 | CNY | Caixin Services PMI Dec | 51.7 | 51.5 |

| 07:30 | CHF | Real Retail Sales Y/Y Nov | 1.20% | 1.40% |

| 08:50 | EUR | France Services PMI Dec F | 48.2 | 48.2 |

| 08:55 | EUR | Germany Services PMI Dec F | 51 | 51 |

| 09:00 | EUR | Eurozone Services PMI Dec F | 51.4 | 51.4 |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | -17.1 | -17.5 |

| 09:30 | GBP | Services PMI Dec F | 51.4 | 51.4 |

| 13:00 | EUR | Germany CPI M/M Dec P | 0.40% | -0.20% |

| 13:00 | EUR | Germany CPI Y/Y Dec P | 2.40% | 2.20% |

| 14:45 | USD | Services PMI Dec F | 58.5 | 58.5 |

| 15:00 | USD | Factory Orders M/M Nov | -0.30% | 0.20% |

| 23:50 | JPY | Monetary Base Y/Y Dec | -0.20% | -0.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Services PMI Dec F | |

| Forecast: 51.4 | Previous: 51.4 | ||

| 01:45 | CNY | Caixin Services PMI Dec | |

| Forecast: 51.7 | Previous: 51.5 | ||

| 07:30 | CHF | Real Retail Sales Y/Y Nov | |

| Forecast: 1.20% | Previous: 1.40% | ||

| 08:50 | EUR | France Services PMI Dec F | |

| Forecast: 48.2 | Previous: 48.2 | ||

| 08:55 | EUR | Germany Services PMI Dec F | |

| Forecast: 51 | Previous: 51 | ||

| 09:00 | EUR | Eurozone Services PMI Dec F | |

| Forecast: 51.4 | Previous: 51.4 | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | |

| Forecast: -17.1 | Previous: -17.5 | ||

| 09:30 | GBP | Services PMI Dec F | |

| Forecast: 51.4 | Previous: 51.4 | ||

| 13:00 | EUR | Germany CPI M/M Dec P | |

| Forecast: 0.40% | Previous: -0.20% | ||

| 13:00 | EUR | Germany CPI Y/Y Dec P | |

| Forecast: 2.40% | Previous: 2.20% | ||

| 14:45 | USD | Services PMI Dec F | |

| Forecast: 58.5 | Previous: 58.5 | ||

| 15:00 | USD | Factory Orders M/M Nov | |

| Forecast: -0.30% | Previous: 0.20% | ||

| 23:50 | JPY | Monetary Base Y/Y Dec | |

| Forecast: -0.20% | Previous: -0.30% | ||

Tuesday, Jan 7, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Building Permits M/M Nov | -1.00% | 4.20% |

| 07:30 | CHF | CPI M/M Dec | 0.00% | -0.10% |

| 07:30 | CHF | CPI Y/Y Dec | 0.70% | |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Dec | 725B | |

| 09:30 | GBP | Construction PMI Dec | 54.5 | 55.2 |

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 6.40% | 6.30% |

| 10:00 | EUR | Eurozone CPI Y/Y Dec P | 2.40% | 2.20% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec P | 2.70% | 2.70% |

| 13:30 | USD | Trade Balance (USD) Nov | -78.4B | -73.8B |

| 13:30 | CAD | Trade Balance (CAD) Nov | 0.8B | -0.9B |

| 15:00 | USD | ISM Services PMI Dec | 53.5 | 52.1 |

| 15:00 | CAD | Ivey PMI Dec | 55.4 | 52.3 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Building Permits M/M Nov | |

| Forecast: -1.00% | Previous: 4.20% | ||

| 07:30 | CHF | CPI M/M Dec | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 07:30 | CHF | CPI Y/Y Dec | |

| Forecast: | Previous: 0.70% | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Dec | |

| Forecast: | Previous: 725B | ||

| 09:30 | GBP | Construction PMI Dec | |

| Forecast: 54.5 | Previous: 55.2 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Nov | |

| Forecast: 6.40% | Previous: 6.30% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Dec P | |

| Forecast: 2.40% | Previous: 2.20% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec P | |

| Forecast: 2.70% | Previous: 2.70% | ||

| 13:30 | USD | Trade Balance (USD) Nov | |

| Forecast: -78.4B | Previous: -73.8B | ||

| 13:30 | CAD | Trade Balance (CAD) Nov | |

| Forecast: 0.8B | Previous: -0.9B | ||

| 15:00 | USD | ISM Services PMI Dec | |

| Forecast: 53.5 | Previous: 52.1 | ||

| 15:00 | CAD | Ivey PMI Dec | |

| Forecast: 55.4 | Previous: 52.3 | ||

Wednesday, Jan 8, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Nov | 2.20% | 2.10% |

| 05:00 | JPY | Consumer Confidence Index Dec | 36.6 | 36.4 |

| 07:00 | EUR | Germany Factory Orders M/M Nov | -0.10% | -1.50% |

| 07:00 | EUR | Germany Retail Sales M/M Nov | 0.40% | -1.50% |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Dec | 95.6 | 95.8 |

| 10:00 | EUR | Eurozone Industrial Confidence Dec | -11.4 | -11.1 |

| 10:00 | EUR | Eurozone Services Sentiment Dec | 5.3 | |

| 10:00 | EUR | Eurozone Consumer Confidence Dec F | -14.5 | -14.5 |

| 10:00 | EUR | Eurozone PPI M/M Nov | 0.40% | |

| 10:00 | EUR | Eurozone PPI Y/Y Nov | -3.20% | |

| 13:15 | USD | ADP Employment Change Dec | 143K | 146K |

| 15:30 | USD | Crude Oil Inventories | -1.2M | |

| 19:00 | USD | FOMC Minutes | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Nov | 2.70% | 2.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Nov | |

| Forecast: 2.20% | Previous: 2.10% | ||

| 05:00 | JPY | Consumer Confidence Index Dec | |

| Forecast: 36.6 | Previous: 36.4 | ||

| 07:00 | EUR | Germany Factory Orders M/M Nov | |

| Forecast: -0.10% | Previous: -1.50% | ||

| 07:00 | EUR | Germany Retail Sales M/M Nov | |

| Forecast: 0.40% | Previous: -1.50% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Dec | |

| Forecast: 95.6 | Previous: 95.8 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Dec | |

| Forecast: -11.4 | Previous: -11.1 | ||

| 10:00 | EUR | Eurozone Services Sentiment Dec | |

| Forecast: | Previous: 5.3 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Dec F | |

| Forecast: -14.5 | Previous: -14.5 | ||

| 10:00 | EUR | Eurozone PPI M/M Nov | |

| Forecast: | Previous: 0.40% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Nov | |

| Forecast: | Previous: -3.20% | ||

| 13:15 | USD | ADP Employment Change Dec | |

| Forecast: 143K | Previous: 146K | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -1.2M | ||

| 19:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Nov | |

| Forecast: 2.70% | Previous: 2.60% | ||

Thursday, Jan 9, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Nov | 1.10% | 0.60% |

| 00:30 | AUD | Trade Balance (AUD) Nov | 5.62B | 5.95B |

| 01:30 | CNY | CPI Y/Y Dec | 0.10% | 0.20% |

| 01:30 | CNY | PPI Y/Y Dec | -2.40% | -2.50% |

| 07:00 | EUR | Germany Industrial Production M/M Nov | 0.50% | -1.00% |

| 07:00 | EUR | Germany Trade Balance (EUR) Nov | 14.4B | 13.4B |

| 09:00 | EUR | ECB Economic Bulletin | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Nov | 0.50% | -0.50% |

| 13:30 | USD | Initial Jobless Claims (Jan 3) | 210K | 211K |

| 15:00 | USD | Wholesale Inventories Nov F | -0.20% | -0.20% |

| 15:30 | USD | Natural Gas Storage | -116B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Nov | |

| Forecast: 1.10% | Previous: 0.60% | ||

| 00:30 | AUD | Trade Balance (AUD) Nov | |

| Forecast: 5.62B | Previous: 5.95B | ||

| 01:30 | CNY | CPI Y/Y Dec | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 01:30 | CNY | PPI Y/Y Dec | |

| Forecast: -2.40% | Previous: -2.50% | ||

| 07:00 | EUR | Germany Industrial Production M/M Nov | |

| Forecast: 0.50% | Previous: -1.00% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Nov | |

| Forecast: 14.4B | Previous: 13.4B | ||

| 09:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Nov | |

| Forecast: 0.50% | Previous: -0.50% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 3) | |

| Forecast: 210K | Previous: 211K | ||

| 15:00 | USD | Wholesale Inventories Nov F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -116B | ||

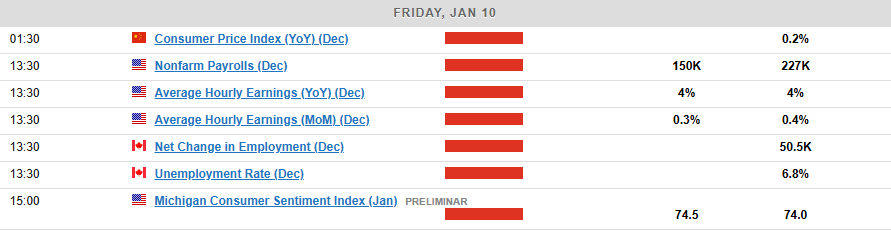

Friday, Jan 10, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Nov P | 107.2 | 109.1 |

| 06:45 | CHF | Unemployment Rate Dec | 2.60% | 2.60% |

| 07:45 | EUR | France Consumer Spending M/M Nov | 0.10% | -0.40% |

| 07:45 | EUR | France Industrial Output M/M Nov | 0.10% | -0.10% |

| 13:30 | USD | Nonfarm Payrolls Dec | 150K | 227K |

| 13:30 | USD | Unemployment Rate Dec | 4.20% | 4.20% |

| 13:30 | CAD | Building Permits M/M Nov | -3.10% | |

| 13:30 | CAD | Net Change in Employment Dec | 50.5K | |

| 13:30 | CAD | Unemployment Rate Dec | 6.80% | |

| 15:00 | USD | Michigan Consumer Sentiment Jan P | 74.5 | 74 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Nov P | |

| Forecast: 107.2 | Previous: 109.1 | ||

| 06:45 | CHF | Unemployment Rate Dec | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 07:45 | EUR | France Consumer Spending M/M Nov | |

| Forecast: 0.10% | Previous: -0.40% | ||

| 07:45 | EUR | France Industrial Output M/M Nov | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 13:30 | USD | Nonfarm Payrolls Dec | |

| Forecast: 150K | Previous: 227K | ||

| 13:30 | USD | Unemployment Rate Dec | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 13:30 | CAD | Building Permits M/M Nov | |

| Forecast: | Previous: -3.10% | ||

| 13:30 | CAD | Net Change in Employment Dec | |

| Forecast: | Previous: 50.5K | ||

| 13:30 | CAD | Unemployment Rate Dec | |

| Forecast: | Previous: 6.80% | ||

| 15:00 | USD | Michigan Consumer Sentiment Jan P | |

| Forecast: 74.5 | Previous: 74 | ||

Markets Weekly Outlook – US Jobs Data in Focus as King Dollar Eyes Further Gains

- The US dollar started 2025 strong, reaching a two-year high, while US equities were disappointing due to a lackluster Santa Rally.

- Global equity funds saw an 86% drop in inflows compared to the previous week, attributed to rising bond yields and potential portfolio rebalancing.

- The week ahead focuses on the US NFP jobs report and its potential impact on USD dominance.

- Australia’s CPI, retail sales, and trade balance data will provide insights into its economy.

Week in Review: King Dollar Starts 2025 on the Offensive… More to Come?

A week that started in 2024 and ended in 2025 showed glimpses of what many had been expecting from the year ahead.

The main one being that the US Dollar is set to remain king in 2025 as the Dollar Index started 2025 on the front foot. The DXY has hit a two year high above the 109.50 handle. A sign of things to come?

US Equities disappointed with regards to the Santa Rally this year. The S&P 500 index suffered 5 successive days of losses beginning on December 26. However, as discussed in my Thursday article titled (S&P 500, Nasdaq 100 Update – Are Wall Street Indexes Set for a January Jump?), January or at least the first half of January has historically been a positive month for US stocks.

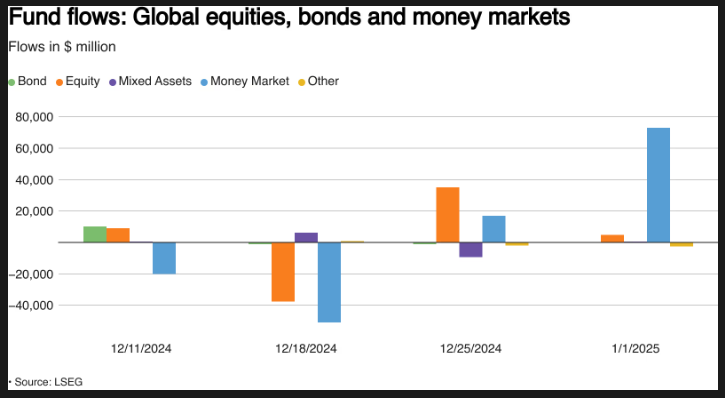

Looking at fund flows, data from LSEG Lipper showed that investors added a net $4.93 billion worth of global equity funds, an 86% drop in inflows compared with about $35.1 billion worth of net purchases in the prior week. This has been attributed to rising bond yields as the US 10Y yield rose to 4.64%, the highest since May 2, but it could be down to portfolio rebalancing as well.

Source: LSEG

Gold prices edged higher this week but remain largely rangebound. The reason for Gold’s malaise can be summed up by looking at all the competing narratives at play. Donald Trump’s proposed tariffs are likely to lead to a stronger US Dollar but the uncertainty surrounding the global economy, geopolitics and the impact of tariffs are likely to keep safe haven demand in play.

This makes the precious metal an intriguing proposition in 2025 and it will be interesting to see how prices and policy from the incoming US administration develops.

Brent crude oil enjoyed an excellent week following 7 or 8 weeks of consolidation. Brent is up around 4% for the week as US stockpiles continue to decline. The 2025 Oil outlook is not positive however as a recent Reuters poll indicated. Analysts are eyeing around $70 a barrel for Brent in 2025 after losses of around 3% in 2024 and a closing price of $ 75.19 a barrel.

The Week Ahead: NFP to Pose a Test for USD Dominance

Asia Pacific Markets

The week ahead in the Asia Pacific region still remains light on the data front.

The highlights include the Caixin Service PMI due on Monday from China. Markets will be keeping a close watch on China and developments this past week around the Yuan and Chinese Bonds are echoing Japan in the 90s.

Deflationary worries have risen while the Yuan hit fresh lows to the US Dollar. However, it may not be all doom and gloom as this past week’s manufacturing data remained on the positive end with a slight improvement. While a weaker Yuan might be a play by Chinese authorities in anticipation of proposed trade tariffs led by incoming US President Donald Trump

Such weakness in the Yuan is usually met by intervention of some sort, however the lack of action may suggest that this is a ploy in anticipation of tariffs.

Wednesday and Thursday the focus will shift to Australia where we have three high impact data releases this week. Monthly CPI data will be joined by retail sales and trade balance data. The data should provide further insights into the Australian economy which has been on a rollercoaster in 2024. This was largely down to the Australian Dollars commodity currency tag as well as concerns around China, a major trading partner.

Europe + UK + US

In developed markets, the US will steal the headlines next week with the NFP jobs report due. Given the US Dollars rocking start to 2025 markets will be paying close attention to the data as well as any adjustments to prior prints.

The initial prediction is that December’s non-farm payrolls will increase by 153,000, with estimates ranging from 125,000 to 200,000. These expectations will be updated throughout the week as more data, like job openings, ADP private payrolls, and ISM employment figures, are released.

The unemployment rate is expected to stay at 4.2%, and wage growth is anticipated to remain at 4% compared to last year. This aligns with a general slowdown in the job market. After the Fed cut rates by 100 basis points in 2024, market participants are pricing in around 50 bps of cuts for the year ahead.

In Europe, Inflation data will be due as the Euro reached two-year lows against the greenback. Market participants have been looking at the possibility of parity for EUR/USD. A drop in inflation could ramp up rate cut bets as the ECB continues to struggle from lackluster growth. Such a move could lead to further divergence in policy with the US Federal Reserve and thus drag EUR/USD closer to parity.

Chart of the Week

This week’s focus is back to the US Dollar index (DXY).

The DXY broke out of consolidation on January 2 to start the New Year with a bang. The Index rose toward the 109.50 resistance level which was also a two-year high.

However Fridays daily candle close is set to close as an inside bar bearish candle which would hint at a pullback in the week ahead. However, looking at recent history and pullback have tnded to be short-lived since the DXY rally began around the back end of September.

There is an ascending trendline which may come into play if we do get a deeper pullback. As things stand, immediate support rests at 108.50 before the 108.00 and 107.50 handles come into focus.

A push higher from current price will first need to break this weeks highs at 109.53 before the 110.00 and 110.50 handles come into focus.

US Dollar Index (DXY) Daily Chart – January 3, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 108.50

- 108.01

- 107.50

Resistance

- 109.52

- 110.00

- 110.50

The Weekly Bottom Line: Awaiting the Changing of the Guard

Canadian Highlights

- Canada’s economy gained momentum in the latter half of 2024, providing a decent hand-off into the current year. We expect real GDP growth to move closer to a trend-like pace in 2025.

- The Bank of Canada has more rate cuts in the tank. Lower borrowing costs should continue to support household consumption and the housing market, though rate spreads to the U.S. will likely pressure the Loonie lower.

- The Canadian federal election comes into focus this year, but Canadian financial markets will likely continue to be heavily influenced by stateside political developments.

U.S. Highlights

- The 119th session of Congress commenced this week, with the House of Representatives beginning the process of electing a Speaker of the House.

- The debt ceiling suspension that had been in place since June 2023 expired this week, with the U.S. Treasury expected to begin implementing extraordinary measures in the coming weeks to avert a potential default.

- Pending home sales improved in November, but elevated mortgage rates continue to restrain the housing sector.

Canada – Staying Alive in 2025

Happy new year to all! To commemorate the transition into the fifth year of the decade, we highlight five key themes for Canada’s economy in 2025.

Tariffs

Incoming president Trump has promised to levy tariffs on trading partners across the globe, with Canada currently under the threat of a 25% tariff on all exported goods. Our recent research (here and here) highlight why we think Canada will avoid the full tariff and what the most likely outcomes are for Canada’s economy. Tariff threats alone are enough to weigh on sentiment and negatively impact business investment. Meanwhile, the global trade picture sits on shaky ground.

More Interest Rate Cuts

The Bank of Canada (BoC) kicked off their easing cycle in June 2023, delivering a cumulative 175 basis point (bps) of cuts to date, bringing the policy rate to 3.25% which is the upper end of its neutral target range. With inflation having settled at around 2%, the BoC has signaled a more gradual pace of easing in 2025. At present, we expect the BoC to continue lowering the policy rate, to the tune of 25 bps per quarter, landing at 2.25% by end-2025 (Chart 1). The goal for the BoC now is to follow a rate path supportive enough to balance downside risks to growth while keeping inflation at bay.

Consumer & Housing Bright Spots

Our forecast for Canadian growth to step up to 1.7% in 2025 (from 1.3% in 2024) is driven by year-end momentum in the country’s traditional growth drivers—consumption and housing. 2025 should be a firm year for both categories, supported by falling borrowing costs, federal measures, and continued economic growth. A key risk to the spending outlook is the sharp planned slowdown in population growth, which could stifle aggregate demand if population growth slows too rapidly and without an offsetting bump in per-capita spending.

Shifting Political Landscape

The election spotlight shifts from the U.S. to Canada in 2025. As it stands, the Canadian federal election will take place on October 20, 2025. It is too early to know if Canada will see an earlier election, but PM Trudeau has been facing pressure to resign, which escalated after finance minister Chrystia Freeland stepped down in the hours before delivering the Fall Economic Statement. All told, we don’t think Canada’s political backdrop will have a big impact on Canadian financial markets. Instead, U.S. fiscal policy and the Trump trade will continue to drive spillover into Canadian yields.

Loonie Weakness

Widening interest rate spreads to the U.S. has put downward pressure on the Canadian dollar over the last several months. Our forecast for a weak 70 cent dollar in 2025 would be the lowest since 2002 (Chart 2). The depreciating dollar has offsetting effects on our outlook. Aside from the damaging effect to purchasing power and the ability of businesses to invest, it imparts a secondary path for inflation. At the same time, a weaker dollar could buffer export declines in the event that the incoming U.S. administration does follow through on its tariff threats.

U.S. – Awaiting the Changing of the Guard

Turning the page on 2024, we eased into the new year this week with limited updates on the state of the economy. For that reason, the attention of financial markets was more attuned to developments in Washington as the 119th session of Congress kicked off. However, the holiday period continued to weigh on trading volumes overall, with the S&P falling 1.1% on the week, while U.S. Treasury yields declined modestly.

Economic data releases this week showed that housing market activity continued to gradually recover from its current subdued state. Pending home sales improved for a fourth consecutive month in November, although gains have moderated recently as rates ticked higher through the fourth quarter. With mortgage rates remaining near 7% (Chart 1) and the Federal Reserve shifting into a more cautionary stance in 2025, the housing market’s recovery is expected to remain gradual this year (see report). As of the time of writing, market pricing implies a nearly 90% probability of the Fed pausing at their next meeting at the end of the month, but the ultimate trajectory of monetary policy this year will likely depend on the fiscal policies implemented by the incoming administration and the impact they have on the economy.

Shifting over to D.C., the federal government continues to be funded by the continuing resolution passed by Congress on December 20th, which will remain in effect until March 14th. This means the twelve appropriation bills for the current fiscal year will be one of the first priorities of the new session of Congress which commenced this week. In addition, the debt ceiling suspension that had been in place since June 2023 expired with the start of the new year. The U.S. Treasury put out a statement last week stating that they anticipated that the debt ceiling would become binding in the next 2-3 weeks, at which time they would begin taking extraordinary measures to avoid defaulting on their fiscal obligations. These measures would likely last until the summer (as they did when the debt ceiling was last hit in early 2023 – Chart 2), but the timely implementation of measures to suspend, raise, or eliminate the debt ceiling will be of paramount importance in the first half of 2025.

With a full legislative agenda already taking form, the first order of business for the new Congressional session this week was electing a new Speaker of the House, with a vote expected Friday afternoon. Looking ahead, Senate confirmation hearings for President-elect Trump’s cabinet nominees are likely to begin in the coming weeks, with the much-anticipated presidential inauguration day set for two weeks from Monday.

On the economic front, we’ll return to a more normal schedule of data releases next week, with the December employment report expected to show 153k new jobs added for the month – down from 227k in November. FOMC December meeting minutes will also be released next Wednesday, which will provide further insights on the Fed’s updated projections. All-in-all, 2025 already looks set to be an eventful year.