Sample Category Title

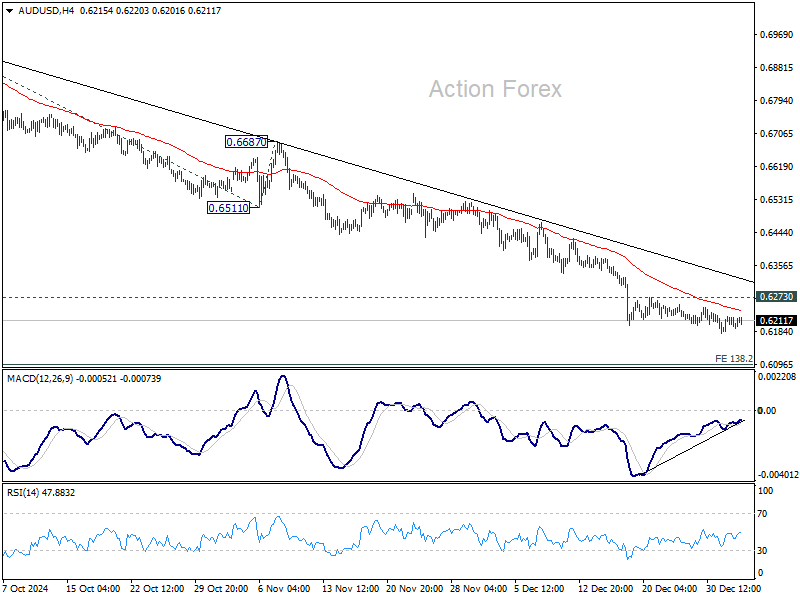

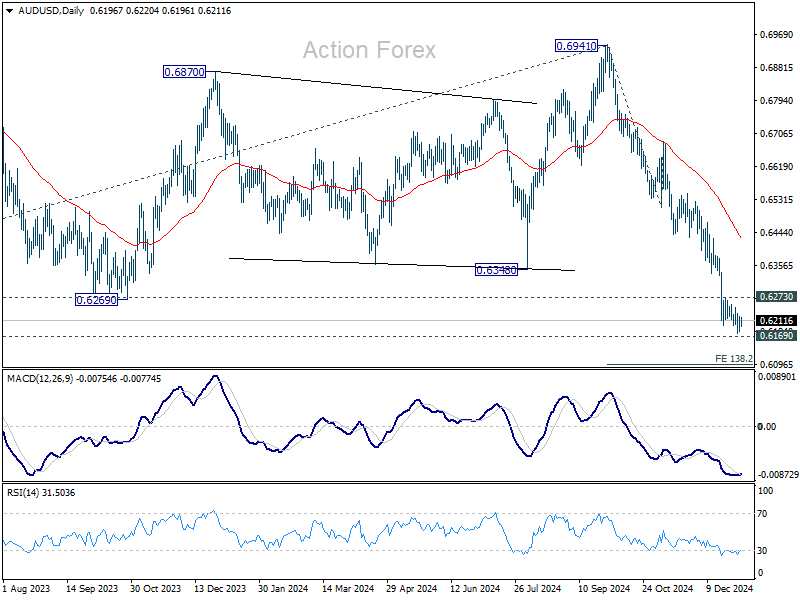

AUD/USD Daily Report

Daily Pivots: (S1) 0.6183; (P) 0.6203; (R1) 0.6224; More...

Intraday bias in AUD/USD remains mildly on the downside despite loss of momentum as see in 4H MACD. Current fall from 0.6941 should target .6169 long term support, and then 138.2% projection of 0.6941 to 0.6511 from 0.6687 at 0.6074. However, considering bullish convergence condition in 4H MACD, break of 0.6273 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6573) holds.

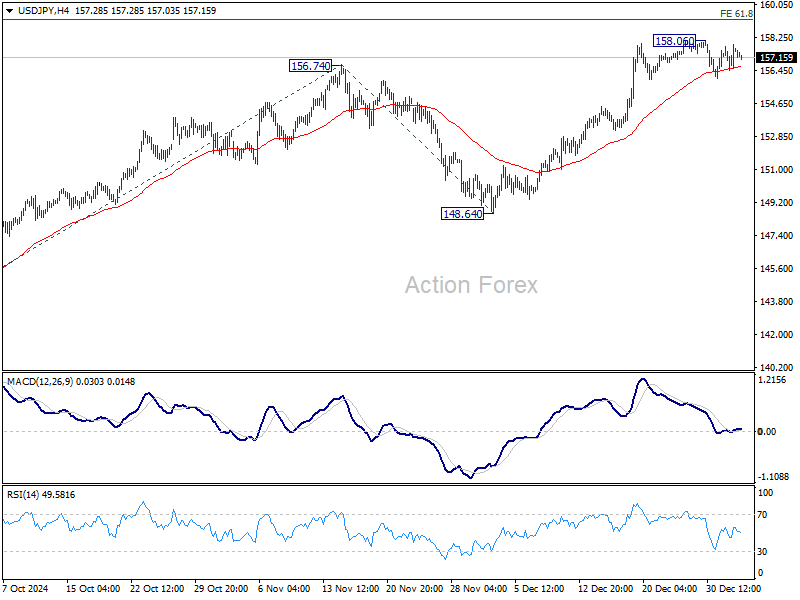

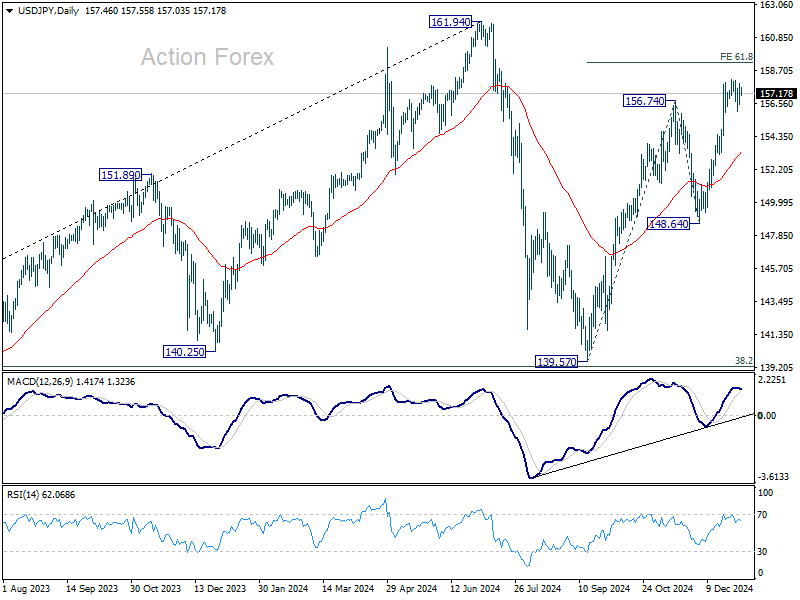

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.69; (P) 157.27; (R1) 158.10; More...

Intraday bias in USD/JPY stays neutral as consolidations continue below 158.06. While another retreat cannot be ruled out, outlook will stay bullish as long as 55 D EMA (now at 153.34) holds. On the upside, above 158.06 will resume the rally from 139.57 to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will pave the way back to 161.94 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

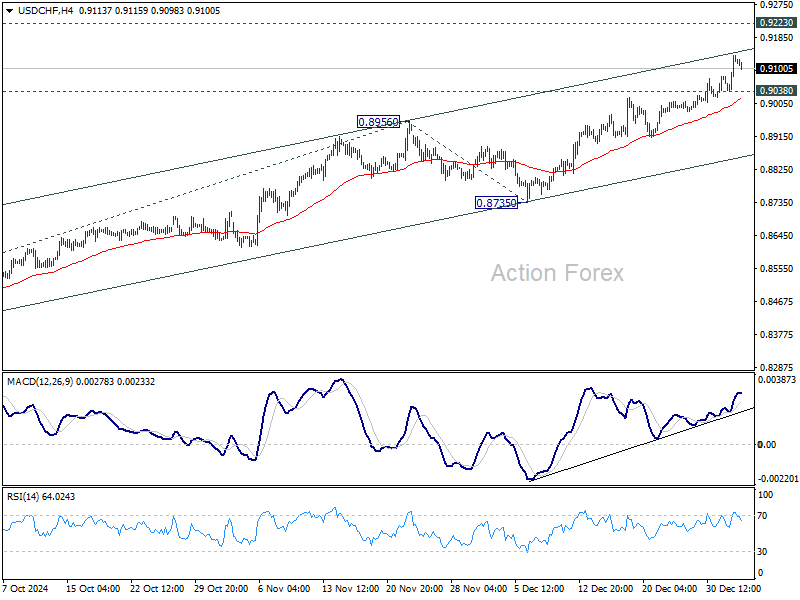

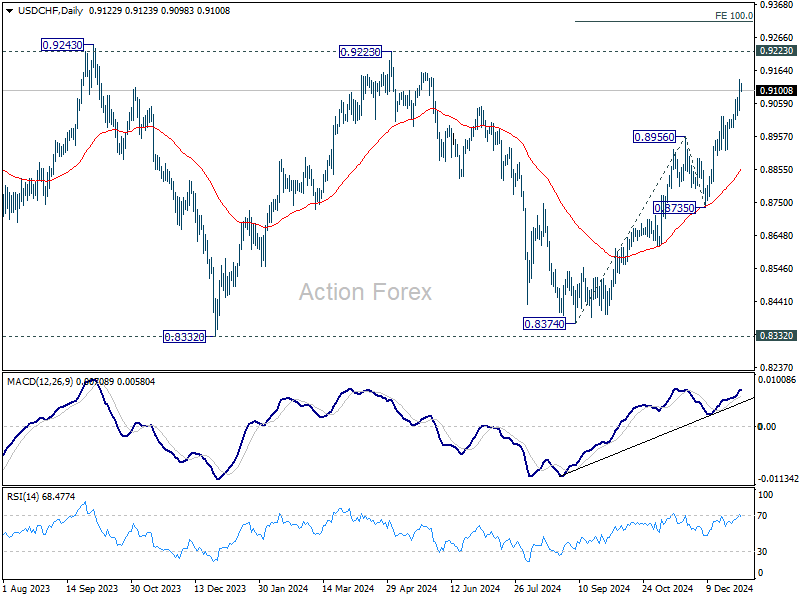

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9063; (P) 0.9100; (R1) 0.9161; More…

Intraday bias in USD/CHF remains on the upside as rally from 0.8374 is in progress. Next target is 0.9223 key resistance. Strong resistance is expected there to limit upside, at least on first attempt. On the downside, below 0.9038 minor support will turn intraday bias neutral first. Nevertheless, decisive break of 0.9223 will carry larger bullish implications.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

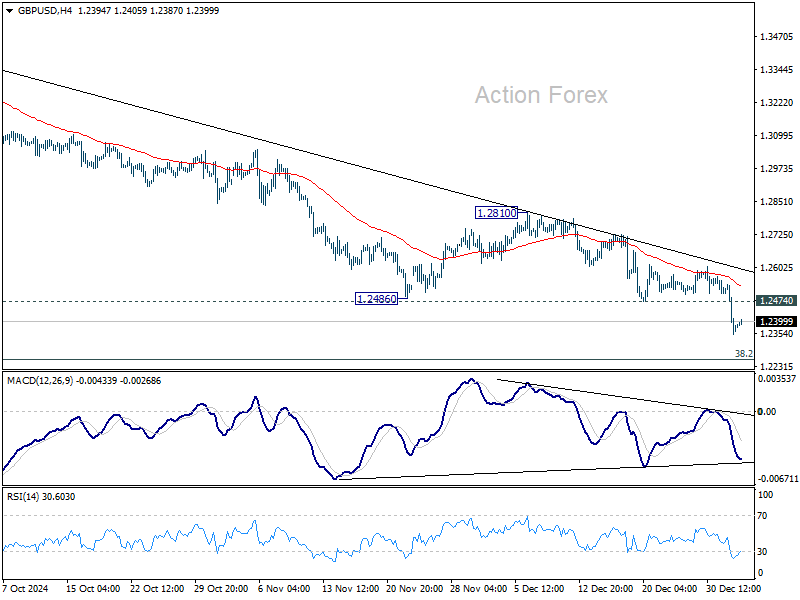

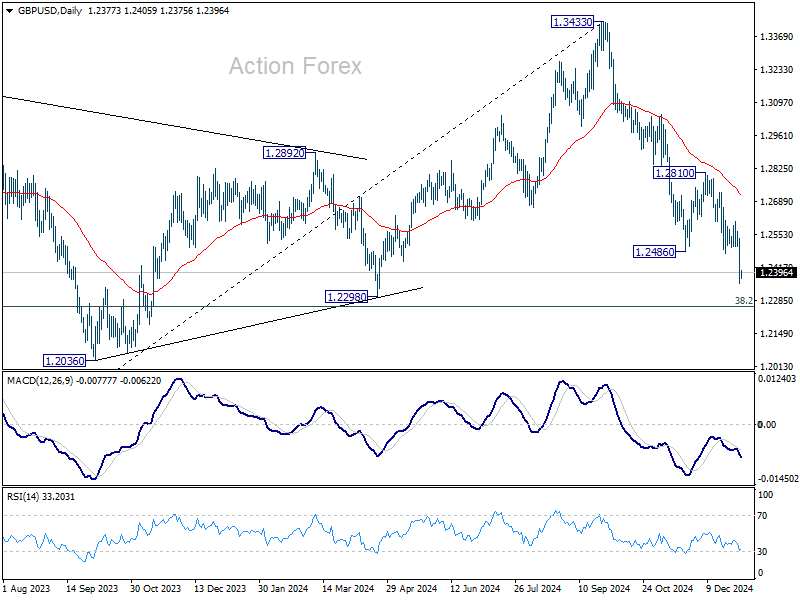

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2309; (P) 1.2425; (R1) 1.2497; More...

Intraday bias in GBP/USD remains on the downside as fall from 1.3433 is in progress for 1.2256/98 cluster support zone. Strong support is expected there to contain downside to bring rebound, at least on first attempt. On the upside, break of 1.2474 support turned resistance will turn intraday bias neutral first. However, decisive break of 1.2256/98 will carry larger bearish implications.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

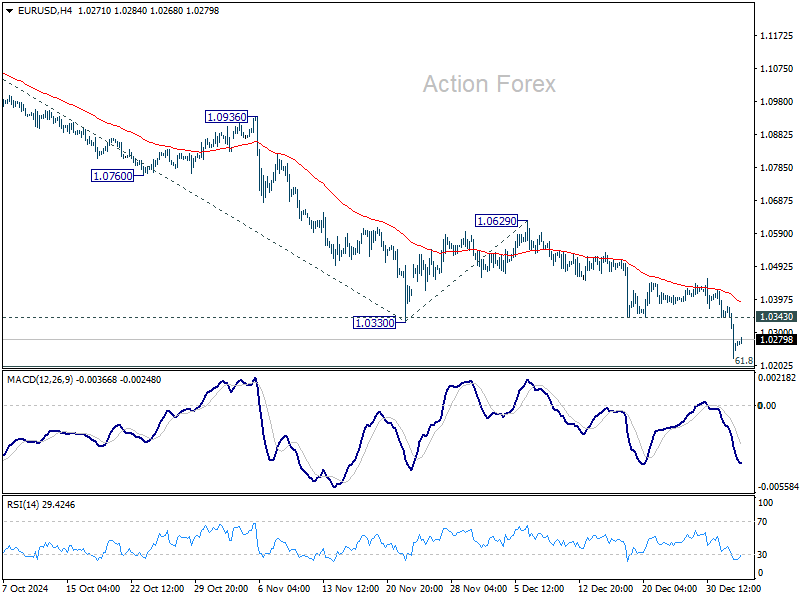

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0203; (P) 1.0289; (R1) 1.0353; More...

Intraday bias in EUR/USD remains on the downside at this point, as fall from 1.1213 is in progress to 1.0199 fibonacci level. Decisive break there will solidify the case of larger bearish trend reversal. Next target will be 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. On the upside, above 1.0343 support turned resistance will turn intraday bias neutral first. But outlook will now stay bearish as long as 1.0629 resistance holds, in case of recovery.

In the bigger picture, current development suggests that rebound from 0.9534 (2022 low) has already completed at 1.1274 after rejection by 55 M EMA. Deeper fall should be seen to 61.8 retracement of 0.9534 to 1.1274 at 1.0199. Sustained trading below there will pave way back to 0.9534 low. This will now remain the favored case as long as 1.0629 resistance holds.

Euro and Pound Struggle Amid Energy Price Shock and US Trade Threats

European currencies remain on the defensive as the new trading year unfolds, with Euro struggling near its lowest level against Dollar since 2022 and Sterling hovering close to a nine-month low. Dollar, while firm, is holding steady in narrow ranges against Yen and commodity-linked currencies, with traders awaiting fresh signals from today’s ISM Manufacturing PMI.

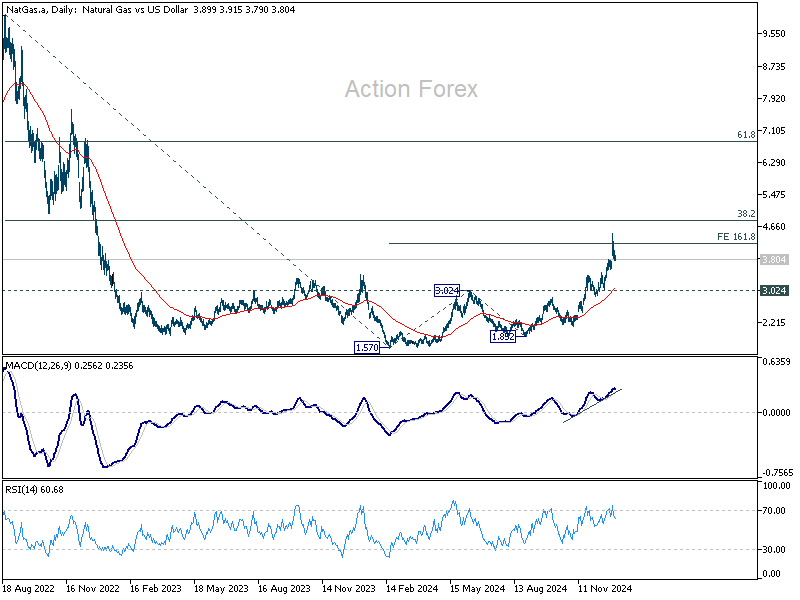

Europe’s economic outlook has been further clouded by an energy price surge. This week, Russian natural gas flows to the EU via Ukraine ceased after the expiration of a five-year transit agreement, forcing European nations to seek pricier LNG imports elsewhere. This development adds another layer of strain to energy-reliant economies like Germany, France, and the UK, worsening their already fragile terms of trade.

US natural gas futures reflected the energy market's unease, spiking to 4.474 earlier this week before retreating. Key resistance now stands at the 38.2% retracement of 10.03 to 1.570 at 4.870. Strong resistance is expected to cap further gains for now, setting the stage for medium-term range trading above 3.024 resistance turned support. However, decisive break above 4.870 could signal significant shifts in energy market dynamics, and could prompt panic rally towards 61.8% retracement at 6.798.

Trade tensions and diverging monetary policies are adding further pressure on European currencies. US president-elect Donald Trump has once again stoked fears of a trade war, tweeting today, "Tariffs will pay off our debt and MAKE AMERICA WEALTHY AGAIN!" This statement reinforces expectations of a more aggressive US trade agenda under his administration, which takes office on January 20. European economies, already struggling with stagnant growth, could face additional headwinds if punitive tariffs are imposed on exports to the US.

The monetary policy outlook for 2025 is also weighing on market sentiment. ECB is expected to proceed with steady rate cuts, totaling around 100 bps by the summer. BoE may also reduce rates by 60 basis points this year, with the possibility of deeper cuts of 100bps if economic conditions deteriorate further. In contrast, Fed is likely to adopt a more cautious easing path, with markets pricing in fewer than 50 basis points of cuts for the year. Yesterday’s US jobless claims report, which revealed an eight-month low in initial claims, highlighted the relative resilience of the US labor market. Upcoming ISM data and non-farm payroll data will be critical in solidifying these expectations for Fed’s policy path.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0203; (P) 1.0289; (R1) 1.0353; More...

Intraday bias in EUR/USD remains on the downside at this point, as fall from 1.1213 is in progress to 1.0199 fibonacci level. Decisive break there will solidify the case of larger bearish trend reversal. Next target will be 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. On the upside, above 1.0343 support turned resistance will turn intraday bias neutral first. But outlook will now stay bearish as long as 1.0629 resistance holds, in case of recovery.

In the bigger picture, current development suggests that rebound from 0.9534 (2022 low) has already completed at 1.1274 after rejection by 55 M EMA. Deeper fall should be seen to 61.8 retracement of 0.9534 to 1.1274 at 1.0199. Sustained trading below there will pave way back to 0.9534 low. This will now remain the favored case as long as 1.0629 resistance holds.

Riksbank Minutes Show Members Eyeing Rate Cut in January or March

In focus today

From the US, the ISM Manufacturing index for December is due for release. The latest PMI survey and hard industrial production data have pointed towards subdued output growth. In the evening, Richmond Fed's Barkin will be on the wires.

In yesterday's version, we incorrectly stated that we expect the Bank of Japan to hold rates unchanged at 0.25% at the January meeting. This was an error. We expect them to raise interest rates by 25 basis points to 0.50%. We apologise for any confusion this may have caused.

Early on Monday, China will release Caixin composite and service PMIs for December.

Economic and market news

What happened overnight

In China, a government official said that China will increase funding from ultra-long treasury bonds sharply to enhance business investments and consumption-boosting initiatives. The initiatives should finance subsidies for durable goods like cars, appliances and digital products like cell phones, tablets, computers, etc. In December Reuters reported that Chinese policy makers had agreed to issue 3tn CNY worth of these special treasury bonds in 2025. A separate FT scoop is making a reference to anonymous PBOC sources, saying this year the central bank will take steps towards a more orthodox monetary policy, prioritising rate-setting and moving away from loan growth -based targets. Last year, the PBOC clarified that it's main policy objective would be the seven-day repo rate, currently at 1.5%, which it is likely to cut further this year.

What happened yesterday

In Sweden, the minutes from the December Riksbank monetary policy meeting revealed that most Riksbank members are eyeing a cut in either January or March (Q1), rather than later during H1. On the exact timing, Jansson seemingly prefers January ahead of March and Bunge makes a similar comment. Breman said "beginning of 2025", while Thedéen and Seim seem to be on the more hawkish side, not specifying the exact timing but sticking to "H1 25". Our call is for the Riksbank to pause in January and cut in March (and June), but there is clear uncertainty about the exact timing and the minutes give some support to a January cut if anything. Current market pricing and the rate path suggesting a 50/50 distribution between January and March seem fair at this point.

In the euro area, manufacturing PMI for December was revised marginally downwards from 45.2 to 45.1 in the final release. In November it was 45.2. The final service PMIs will be released on Monday next week.

In the UK, manufacturing PMI fell to 47.0 in December from 48.0 in November. The figure was revised down from the preliminary print of 47.3.

FI: 2025's first trading day ended with virtually unchanged yields after a minor rally earlier in the day, thus 10y bunds ended 1bp higher at 2.37%. The rally in the morning seemed to be swap leg driven, dragging the Bund ASW spread briefly into negative territory albeit it ended the day at around 0.5bp. The turnaround in yields came after lower than expected US jobless claims. ECB's Lane speaks tonight.

FX: The broad USD continues to trade on a strong footing, significantly appreciating against both the EUR and GBP in yesterday's session, pushing EUR/USD down to 1.0250 and GBP/USD below 1.24. USD/JPY remains rangebound in the 157-158 range as uncertainty lingers around potential FX intervention and a possible January BoJ rate hike. In the Scandies, the NOK saw notable gains against the EUR, benefitting from a rising oil price, bringing EUR/NOK to around 11.70, while EUR/SEK remains steady near 11.45.

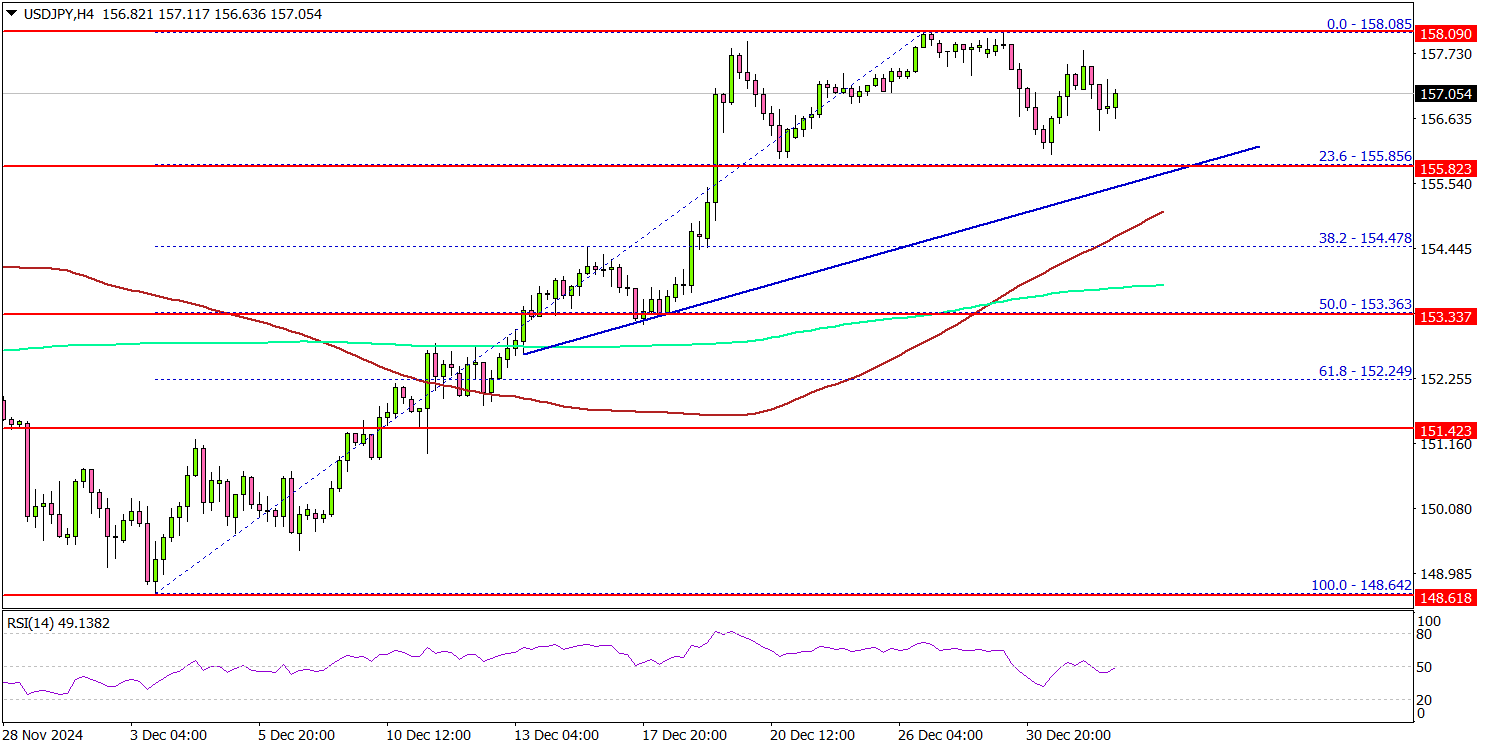

USD/JPY Settles After Rally: Can Bulls Push Higher?

Key Highlights

- USD/JPY started a fresh rally above the 154.50 resistance.

- A key bullish trend line is forming with support at 155.80 on the 4-hour chart.

- EUR/USD accelerated losses and traded below the 1.0340 support.

- GBP/USD also declined and traded below the 1.2475 support.

USD/JPY Technical Analysis

The US Dollar formed a base above the 152.00 level against the Japanese Yen. USD/JPY started a fresh surge above the 154.50 and 155.00 resistance levels.

Looking at the 4-hour chart, the pair settled above the 155.50 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair even climbed above the 157.50 level before the bears appeared.

A high was formed at 158.08 before there was a short-term downside correction. The price dipped below the 157.50 level. However, it remained stable above the 23.6% Fib retracement level of the upward move from the 148.64 swing high to the 158.08 high.

On the downside, immediate support sits near the 155.80 level and the trend line. The next key support sits near the 154.40 level. Any more losses could send the pair toward the 153.50 level or the 50% Fib retracement level of the upward move from the 148.64 swing high to the 158.08 high.

On the upside, the pair is facing hurdles near the 158.00 level. The first major resistance is near the 158.80 level. The next major resistance is near the 159.20 level.

A close above the 159.20 level could set the tone for another increase. In the stated case, the pair could rise toward the 162.00 resistance.

Looking at EUR/USD, the pair started another decline and traded below the 1.0340 support zone to move further into the red zone.

Upcoming Economic Events:

- US ISM Manufacturing Index for Dec 2024 – Forecast 48.3, versus 48.4 previous.

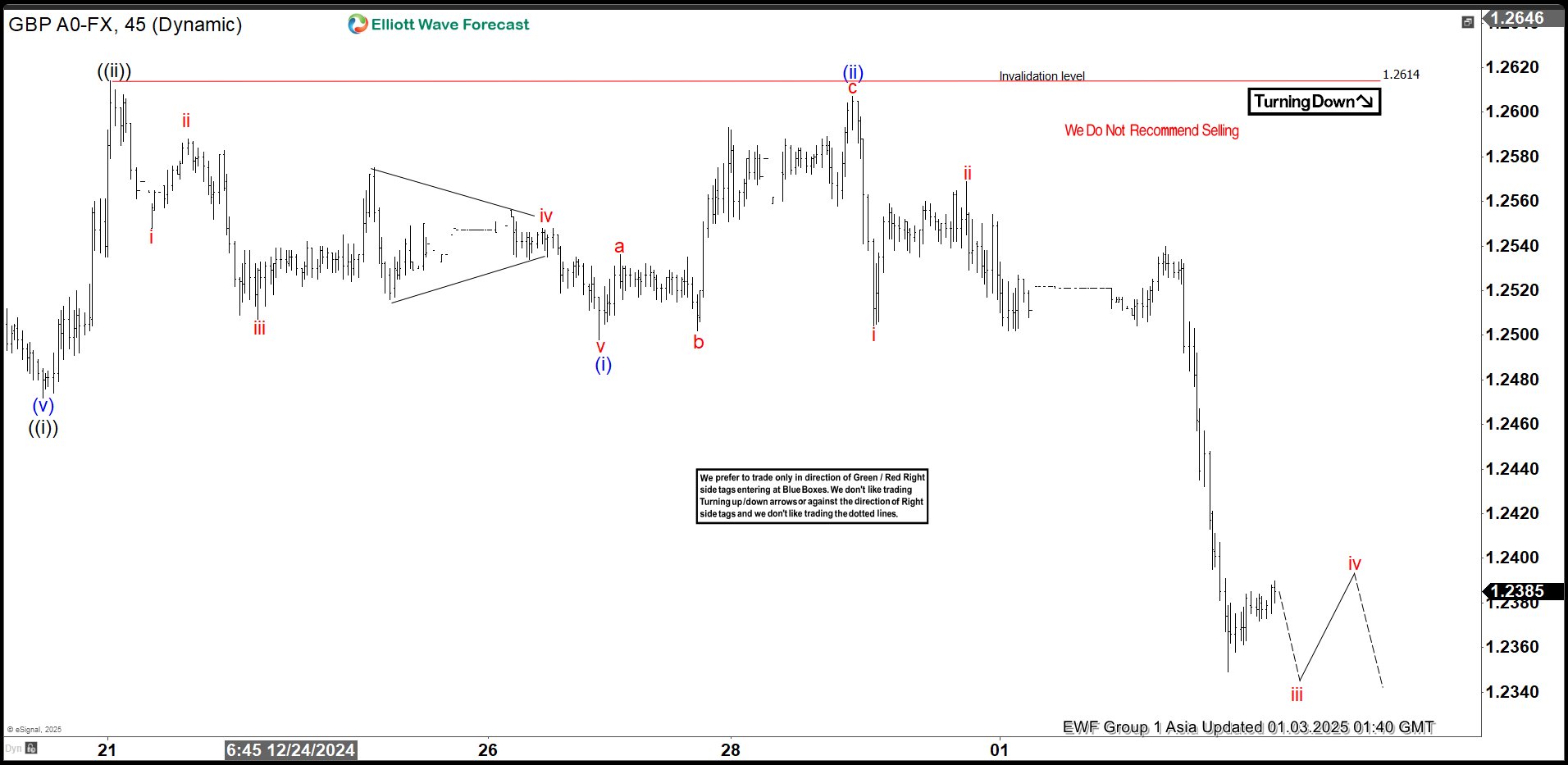

Elliott Wave View: GBPUSD Short Term Remains Bearish

Short Term Elliott Wave view in GBPUSD suggests decline from 12.6.2024 high is in progress as a 5 waves impulse. Down from 12.6.2024 high, wave ((i)) ended at 1.247 and wave ((ii)) rally ended at 1.261 as the 45 minutes chart below shows. Pair has turned lower in wave ((iii)) with internal subdivision as another impulse. Down from wave ((ii)), wave i ended at 1.2548 and rally in wave ii ended at 1.2588. Pair resumed lower in wave iii towards 1.2507. Wave iv rally ended at 1.2548 and wave v lower ended at 1.2498 which completed wave (i) in higher degree. Rally in wave (ii) ended at 1.2607 with internal subdivision as a zigzag.

Up from wave (i), wave a ended at 1.2536 and wave b ended at 1.2502. Wave c higher ended at 1.2607 which completed wave (ii). Pair has turned lower in wave (iii). Down from wave (ii), wave i ended at 1.2504 and wave ii ended at 1.2569. Expect pair to extend lower to end wave iii, then it should rally in wave iv before turning lower again. Near term, as far as pivot at 1.2614 high stays intact, expect rally to fail in 3, 7, or 11 swing for further downside.

GBPUSD 45 Minutes Elliott Wave Chart

GBPUSD Elliott Wave Chart

GBPUSD Elliott Wave Video

https://www.youtube.com/watch?v=ca1ewAKNZgs