Sample Category Title

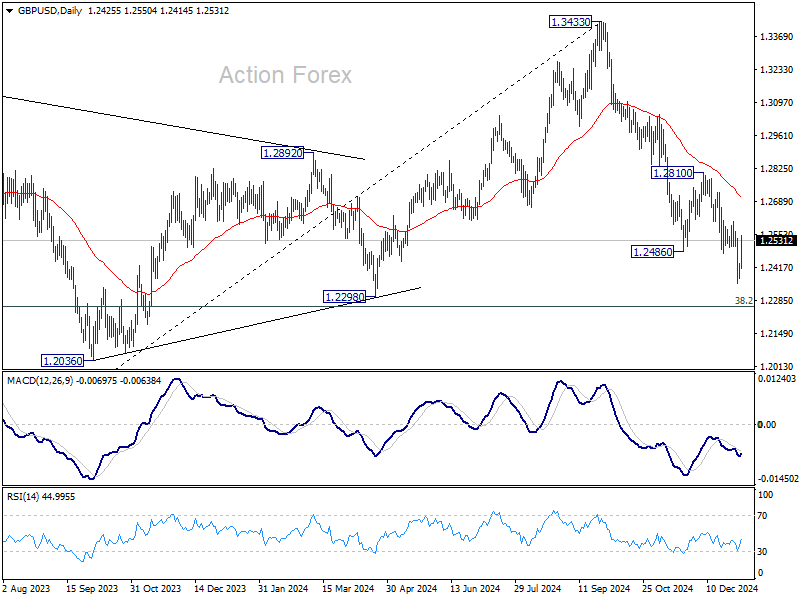

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2369; (P) 1.2402; (R1) 1.2453; More...

While GBP/USD rebounded strongly today, upside is capped below 1.2606 resistance and intraday bias remains neutral. Another fall remains in favor. Break of 1.2352 will resume the fall from 1.3433 to 1.2256/98 cluster support zone. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 1.2606 will confirm short term bottoming, and turn bias back to the upside to 55 D EMA (now at 1.2708).

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.

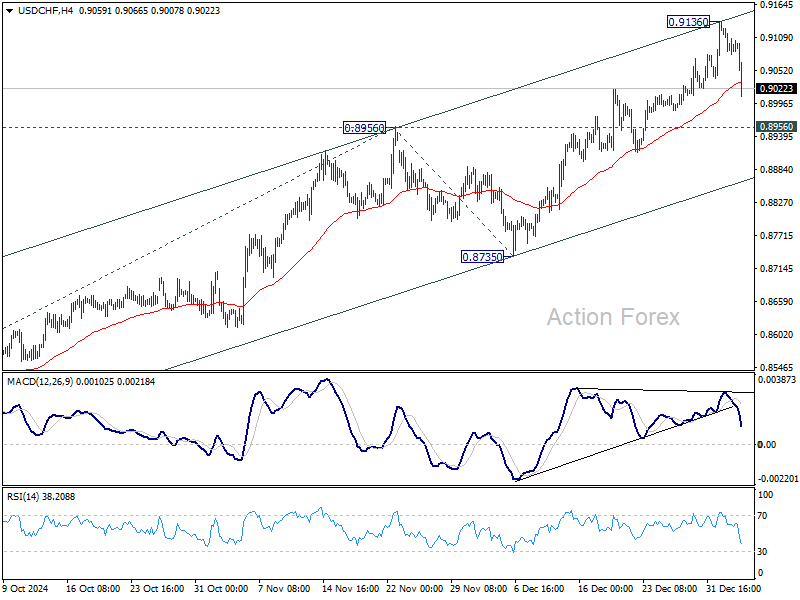

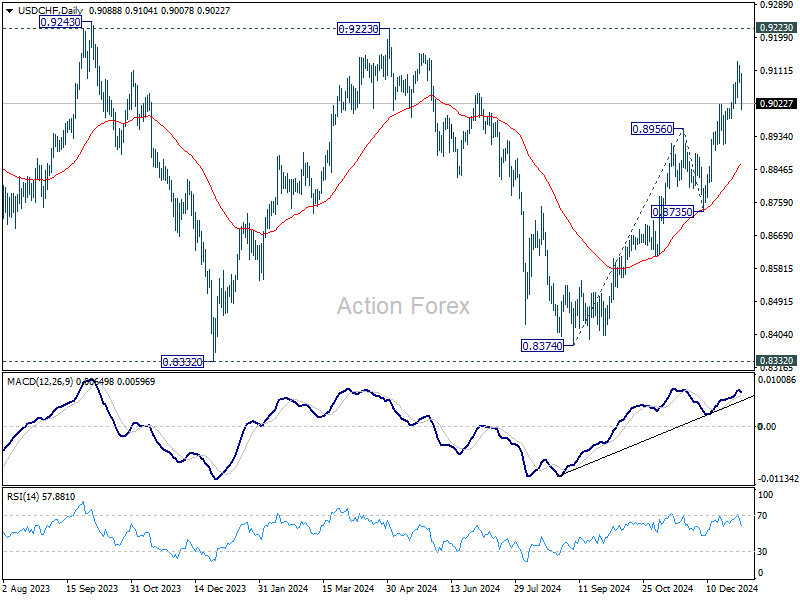

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9066; (P) 0.9098; (R1) 0.9117; More…

USD/CHF's is staying well above 0.8956 resistance turned support despite today's dip and intraday bias stays neutral. Outlook will remain bullish as long as 0.8956 resistance turned support holds. Above 0.9136 will resume the rally from 0.8374 to 0.9223 key resistance next. However, firm break of 0.8956 will turn bias back to the downside for 55 D EMA (now at 0.8861).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.

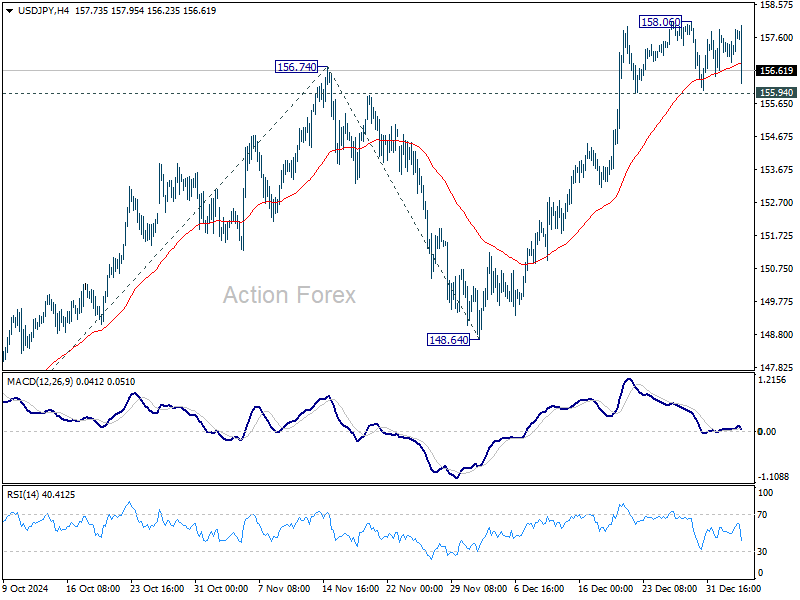

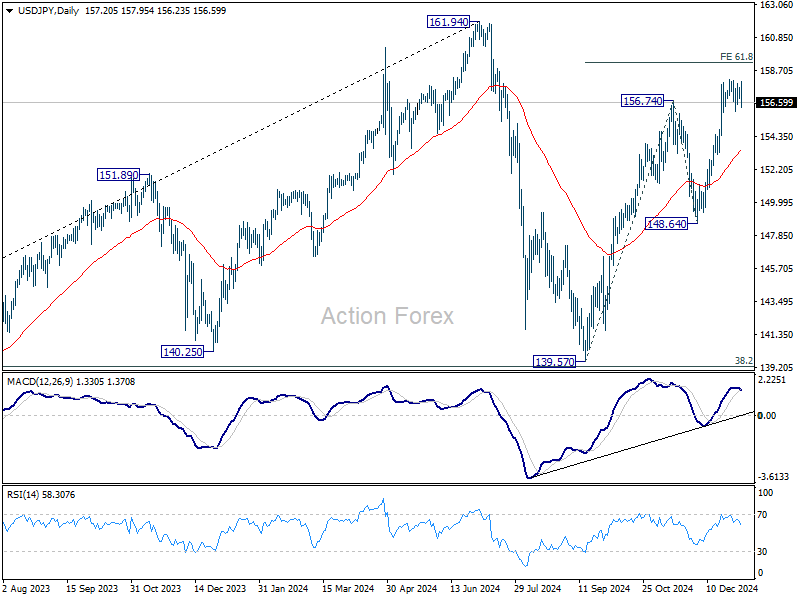

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.92; (P) 157.24; (R1) 157.62; More...

USD/JPY is still staying in range of 155.94/158.06 despite today's dip, and intraday bias remains neutral. Further rally is expected as long as 155.94 support holds. On the upside, break of 158.06 will resume the rally from 139.57 to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25. Firm break there will target 161.94 high. However, break of 155.94 will turn bias to the downside, for deeper pull back to 55 D EMA (now at 153.50).

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

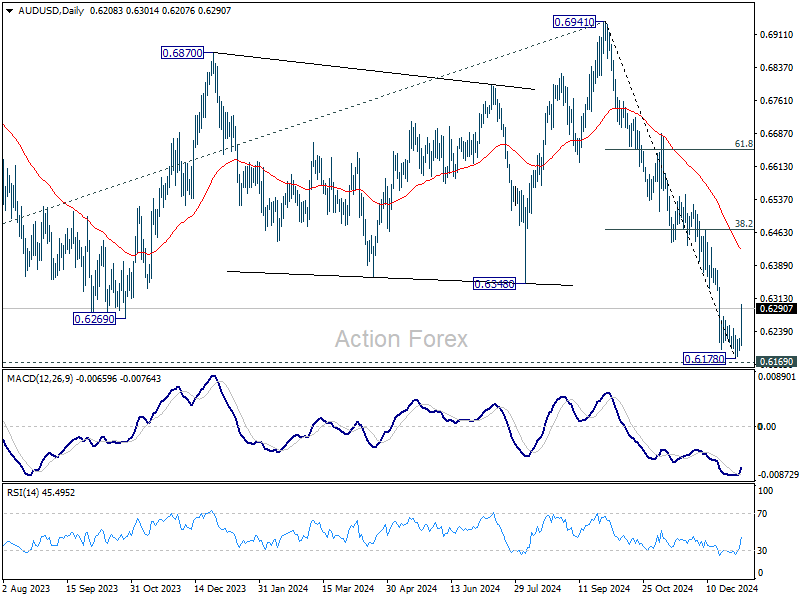

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6196; (P) 0.6210; (R1) 0.6232; More...

AUD/USD's extended rebound and break of 0.6273 resistance suggests short term bottoming at 0.6178, on bullish convergence condition in 4H MACD, and just ahead of 0.6169 key support. Intraday bias is back on the upside for 55 D EMA (now at 0.6245). But near term outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6178 at 0.6469. For now, more consolidation is in favor in the near term as long as 0.6178 holds, in case of retreat.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006, and could have completed at 0.6941 already. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.

Dollar Falls as Trump Considers Sector-Specific Tariffs Over Blanket Approach

Dollar weakened significantly, while stock futures rebounded, amid reports suggesting that the incoming Trump administration may scale back its plans for sweeping tariffs. According to The Washington Post, discussions among President-elect Donald Trump’s aides now lean toward imposing tariffs only on critical sectors tied to national or economic security, rather than blanket levies on all imports.

This approach marks a departure from the broader tariff policy championed during the campaign, reflecting political considerations around goods integral to daily life—such as food and consumer electronics—that could spark backlash if subject to hefty duties. In this scenario, the administration aims focus on reshuffling supply chains in areas like defense, medical equipment, and energy production back to US soil.

While the specifics are still under discussion, the move signals a more calculated approach to trade policy that could reduce market fears of widespread disruptions in global trade.

Quick update (14:40 GMT): Dollar pared back losses after Trump denied the report. On Truth Social, he said: "The story in the Washington Post, quoting so-called anonymous sources, which don't exist, incorrectly states that my tariff policy will be pared back. That is wrong. The Washington Post knows it's wrong. It's just another example of Fake News."

Separately, former Fed Chair Ben Bernanke, speaking at the American Economic Association conference, provided additional insight on the inflation implications of such measures, remarking that “Trump policies, whatever their merits on public finance grounds, probably will be modest in terms of their effect on the inflation rate.”

Bernanke admitted the difficulty of forecasting the tariffs’ full impact given uncertainties over whether they might be temporary bargaining chips or long-term measures, but he does not expect a “radical shift” in the inflation outlook.

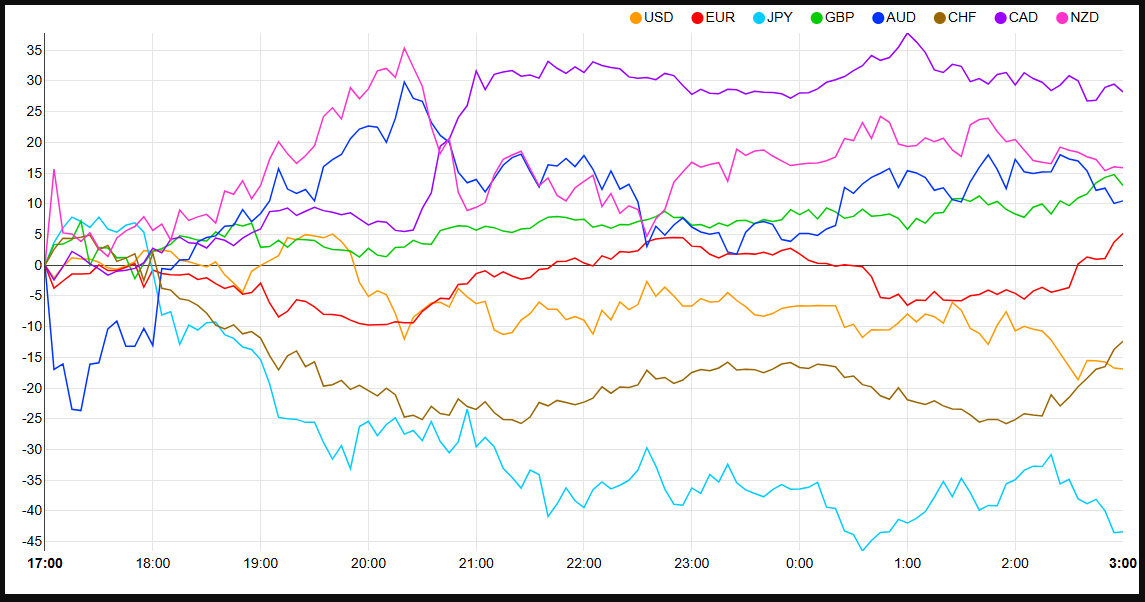

Commodity currencies rallied on the news, with the Australian and New Zealand Dollars posting the day’s biggest gains so far, while Canadian Dollar also strengthened. Meanwhile, Euro and Pound firmed up too, leaving the Swiss Franc under pressure as investors rotated out of haven assets. Risk-on sentiment also weighed on Yen and Dollar, as traders recalibrated views on US trade policies.

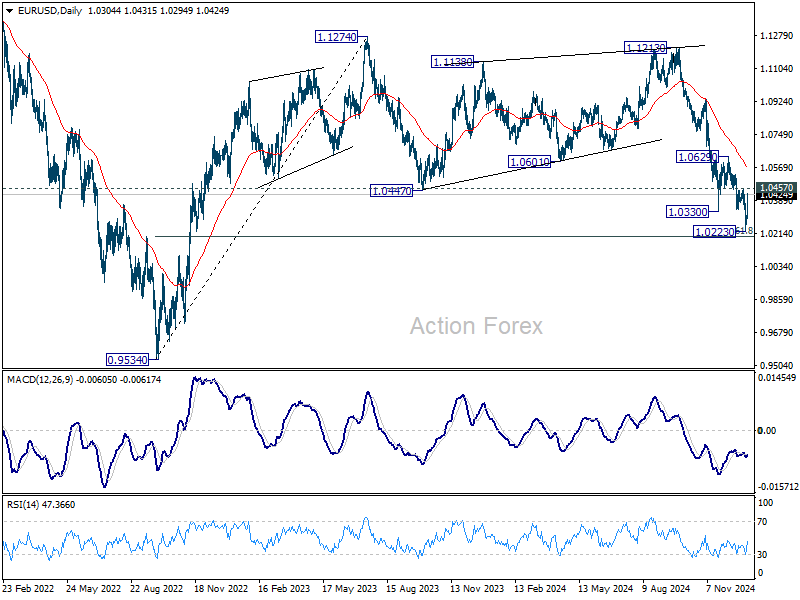

Technically, firm break of 1.0457 resistance in EUR/USD will confirm short term bottoming at 1.0223, just ahead of 61.8 retracement of 0.9534 to 1.1274 at 1.0199. Stronger rebound would then be seen towards 55 D EMA (now at 1.0574). But decisive break of 1.0629 resistance is needed to confirm near term bullish trend reversal. And that would depend on what exactly Trump's trade policies are, which might only be known after his inauguration on January 20.

In Europe, at the time of writing, FTSE is up 0.11%. DAX is up 0.93%. CAC is up 1.50%. UK 10-year yield is up 0.003 at 4.599. Germany 10-year yield is up 0.031 at 2.459. Earlier in Asia, Nikkei fell -1.47%. Hong Kong HSI fell -0.36%. China Shanghai SSE fell -0.14%. Singapore Strait Times rose 0.53%. Japan 10-year JGB yield rose 0.0359 to 1.129.

Eurozone Sentix investor confidence hits 14-month low, room for ECB support rapid diminishing

Eurozone Sentix Investor Confidence edged down from -17.5 to -17.7 in January, meeting expectations while marking the lowest level since November 2023. Current Situation Index fell from -28.5 to -29.5, its weakest reading since October 2022. Meanwhile, Expectations Index improved marginally from -5.8 to -5.0 but remained in negative territory.

Sentix highlighted Germany's economic struggles as a major drag on the Eurozone, with its overall index at -33.3. German Current Situation Index held steady at -50.8, underscoring a deep recessionary environment, while expectations fell to -13.8. Political uncertainty in Germany, exacerbated by electoral challenges, compounds the economic woes, adding to the region's fragility.

Sentix also warned that the broader Eurozone economy is at risk of falling "even deeper into crisis." Inflation concerns persist, with the thematic inflation index dropping from -12 to -15.25. This trend further constrains ECB, which limited room for additional rate cuts is "rapidly diminishing". Governments are also contending with high deficits as they attempt to stimulate growth.

Eurozone PMI services finalized at 51.6, resilient sector with persistent inflation pressures

Eurozone PMI Services for December was finalized at 51.6, an improvement from November's 49.5, signaling a return to growth after a brief contraction.

Meanwhile, PMI Composite edged higher to 49.6, up from November's 48.3, though still indicating a slight contraction in overall activity. Among individual countries, Spain stood out with a 21-month high at 56.8, while Germany and France posted modest improvements to 48.0 and 47.5, respectively.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that "services inflation remains elevated," driven by rising wages and higher costs being passed on to customers. These dynamics reinforce the expectation that ECB will take a cautious approach to monetary policy.

"Small interest rate cuts in the first quarter of 2025" appear likely as the central bank balances inflation concerns with sluggish economic growth.

Encouragingly, the services sector displayed resilience, with incoming business stabilizing and the decline in order backlogs slowing. Service providers, less exposed to the potential impacts of US tariffs than manufacturers, remain a crucial buffer against the region’s industrial slowdown.

However, the foundation for a robust services-led recovery in 2025 remains tenuous, with structural challenges such as high costs and fragile demand persisting.

UK PMI services finalized at 51.1, optimism hits multi-year low

UK PMI Services for December was finalized at 51.1, slightly up from November's 50.8, marking the fourteenth consecutive month of expansion. However, growth was marginal, with the index's quarterly average at its lowest in a year. PMI Composite slipped to 50.4, down from 50.5, its weakest reading since October 2023.

Tim Moore, Economics Director at S&P Global Market Intelligence, noted a "near-stalling" of new business inflows due to falling business and consumer confidence. Respondents cited concerns over "domestic economic prospects" for 2025 and lingering post-Budget uncertainty as major factors curbing growth momentum.

Cost pressures intensified, with input price inflation hitting an eight-month high. Service providers responded by raising prices at a rate well above pre-pandemic levels, further straining demand.

Nearly one in four firms reported payroll reductions, marking the steepest non-pandemic-related job shedding in over 15 years as subdued demand and rising employment costs forced businesses to delay hiring or reduce staff.

BoJ Ueda stresses caution on policy adjustments

BoJ Governor Kazuo Ueda reiterated the cautious stance on monetary policy adjustments at a Japanese Bankers Association event today. He emphasized that any interest rate hikes would depend on sustained improvements in economic and price conditions.

“Our stance is that we will raise the policy interest rate to adjust the degree of monetary easing if economic and price conditions keep improving,” Ueda stated.

However, he highlighted the need for vigilance regarding various risks, signaling that the timing of such adjustments would be carefully assessed. The governor also expressed his hopes for balanced growth in wages and prices in the coming year.

Japan's PMI services finalized at 50.9, optimism eases

Japan's service sector showed slight improvement in December, with final PMI Services index rising to 50.9 from 50.5 in November, indicating marginal growth. PMI Composite also increased to 50.5 from 50.1, reflecting modest stabilization in the broader economy.

Usamah Bhatti, Economist at S&P Global Market Intelligence, noted, "December data revealed sustained rises in both business activity and new business," with new orders growing at the fastest pace in four months. Employment in the service sector rose for the fifteenth consecutive month, signaling steady labor market gains. Despite these improvements, business optimism softened slightly.

The overall economic expansion was underpinned by softer contraction in manufacturing output and ongoing growth in the service sector. New orders across sectors expanded at their fastest rate since August, supported by the completion of outstanding work, particularly in manufacturing. However, optimism regarding future output declined, falling below the 2024 average.

China's services sector gains momentum, but Composite PMI signals broader economic strain

China’s services sector gained pace in December, with Caixin PMI Services rising to 52.2 from 51.5 in November, marking its highest level since May. However, the overall economic picture remains mixed as PMI Composite slipped to 51.4, its lowest since September. This divergence highlights that faster services growth was insufficient to offset the slowdown in manufacturing output expansion.

Wang Zhe, Senior Economist at Caixin Insight Group, remarked, “Prominent downward pressures remain, with tepid domestic demand and mounting unfavorable external factors.”

He added that sluggish employment and squeezed profit margins are weighing on market optimism. Declines in some gauges from the manufacturing PMI survey indicate that more time is needed to evaluate the consistency and effectiveness of recent policy stimulus.

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6196; (P) 0.6210; (R1) 0.6232; More...

AUD/USD's extended rebound and break of 0.6273 resistance suggests short term bottoming at 0.6178, on bullish convergence condition in 4H MACD, and just ahead of 0.6169 key support. Intraday bias is back on the upside for 55 D EMA (now at 0.6245). But near term outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6178 at 0.6469. For now, more consolidation is in favor in the near term as long as 0.6178 holds, in case of retreat.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006, and could have completed at 0.6941 already. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.

CAD Rises on Trudeau’s Possible Resignation

The Canadian dollar is up almost 1% against its US counterpart, 1.4310, in early Monday trading, following reports that Canadian Prime Minister Justin Trudeau may announce his resignation on January 6th after nine years at the helm. Markets are taking the news positively, as it suggests that the country’s new leader could boost growth with new economic measures.

Often, markets fall on news of a change of government due to the uncertainty premium. However, it seems that this time, too much negativity was built into the Canadian Dollar price, resulting in a lack of fresh sellers.

Technically, the USDCAD formed a double top as it approached the 1.4450 level, a typical pivot pattern that is reinforced by the divergence between the price momentum and the RSI indicator, indicating that the upward momentum has run out.

The current sharp decline could be the beginning of a reversal, something the markets have been reluctant to do in recent weeks. Next, it is worth considering potential downside targets. The first such target looks to be the 1.42 area, which is the correction level of 76.4% of the growth amplitude from September to the December peak.

A classic pullback to 61.8% would take the price to 1.4060. History also suggests that a decline from the extremes around 1.45 could be the start of a long-term trend that takes USDCAD to 1.2000.

Euro Surges Close to 1%, German CPI Looms

The euro has started the week with sharp gains. In the European session, EUR/USD is currently trading at 1.0403, up 0.91% on the day.

German CPI expected to rise to 2.4%

Germany’s economy may not be in great shape. but inflation has been moving higher and the trend is expected to continue when December CPI is released later today. Inflation rose from 2% to 2.2% in November, its highest level in four months, and is expected to hit 2.4% in December. Service inflation is at 4% and core CPI at 3%, which indicates the battle to contain inflation isn’t over.

Once the locomotive of Europe, Germany’s economy has faltered badly and has slowed the eurozone’s recovery. Germany’s once mighty auto industry has been hurt by weaker Chinese demand due to the slowdown in the the world’s second-largest economy. As well, China has gained a larger share of the global automotive market, at the expense of German auto exports. Unsurprisingly, Germany’s manufacturing sector is stuck in contraction territory.

Germany’s services sector moved back into expansion mode in December, as the Services PMI rose to a revised 51.3, up from 49.3 in November. The eurozone Services PMI improved to a revised 51.6, up from 49.5 in November. Spain continues to impress with its economic data, as the Services PMI climbed to 57.3, up from 53.1 in November. This marked a sixteenth straight month of expansion and was the highest level of growth since April 2023.

The US releases Final Services PMI later today. The market estimate for December stands at 58.5, compared to 56.1 in November. This points to strong business activity, which has been the linchpin of the US economy.

EUR/USD Technical

- EUR/USD has pushed above resistance at 1.0331. Above, there is resistance at 1.0436 and 1.0564

- There is support at 1.0203 and 1.0098

DXY and EUR/USD: Outlook and Technical Analysis

- The US Dollar Index (DXY) starts the week lower as market participants reposition ahead of a data-heavy week.

- EUR/USD recovers but will German inflation derail the rally?

- The DXY is at a key confluence; a break of the trendline could lead to a downside correction, while a bounce could open up the possibility of fresh highs.

The US Dollar Index (DXY) has started the week on the back foot as the Index flirts with a key level. It would appear market participants are repositioning ahead of a data heavy week that ends with the NFP jobs report on Friday.

Another reason that has been cited is that the Dollar could reconnect with the slight deterioration in its rate advantage over the holiday period. The holidays saw US Yields remain steady while rates in Germany, the Eurozone benchmark ticked higher.

Currency Strength Chart: Strongest – CAD, NZD, GBP, AUD, EUR, CHF, USD, JPY – Weakest

Source: FinancialJuice

EUR/USD Rises To Mid 1.03’s, German Inflation Data Ahead

EUR/USD has continued its recovery following the holiday period selloff which saw the pair fall to 1.02225. Parity for EUR/USD in 2025 cannot be ruled out yet as policy divergence remains a real possibility.

The only upside for market participants is that such a drop may present an enticing opportunity. Historically any moe toward parity or dips below have proved short-lived with significant buying pressure emerging. Will history repeat itself once more?

Looking at the immediate risks for EUR/USD, and German inflation data is due later in the day. German inflation is forecast to rise to 2.4% on a yearly basis in December from 2.2% in November.

A stronger print could help push EUR/USD toward the 1.0400 handle but I do not expect such a move to last. EUR/USD still faces significant bearish pressure and with a slew of data ahead this week, an early week correction followed by a selloff later in the week cannot be ruled out.

Technical Analysis

EUR/USD

EUR/USD has found some momentum following Friday’s bullish inside bar candle close.

On the daily timeframe, the trend remains bearish without a daily candle close above the 1.04300 handle.

Until such a break occurs, the possibility of fresh lows remains high. There is however the possibility of a break above the 1.0430 which could push EUR/USD toward the long term descending trendline and key resistance around the 1.0500 handle.

This could in theory provide a better risk to reward opportunity for potential shorts, however at this point the daily chart would have noted a change in character with the swing high at 1.04300 having been broken. This would make such a play counter-trend in nature and increase the risk of EUR/USD rising even further.

Interesting week ahead for EUR/USD with the DXY likely to be central to any development for the pair.

EUR/USD Daily Chart, January 6, 2025

Source:TradingView.com

Support

- 1.0293

- 1.0222

- 1.0000

Resistance

- 1.0430

- 1.0500

- 1.0535

US Dollar Index (DXY)

The US Dollar index daily chart is intriguing to say the least. The selloff this morning has brought the index into a key confluence that could help determine price action in the coming days.

The index has come within a whisker of the ascending trendline on the daily timeframe as it bounced off support at 108.64 this morning.

The next move will be key as a break of the trendline could lead to a short-term downside correction for the index toward 108.00 or potentially 107.00.

A bounce off the support level and a move higher could open up the possibility of fresh highs above the 110.00 handle.

The narrative around the US Dollar is one of strength. Recent comments by Fed policymakers touting rising inflation as a concern may lead to a pivot toward price pressures once more. Such a move could keep the USD supported in the medium term.

The Expectations around the Trump Presidency may also factor in as the January 21 inauguration nears.

The inauguration however does present two potential paths for the USD index. First one would be continued USD weakness before buying pressure returns just ahead of the Trump inauguration as market participants attempt to get the dollar on the ‘cheap’.

The second possibility is that we see a strong US Dollar right up until the inauguration. Thai move does however leave the USD vulnerable to selling pressure post election should President Trump not deliver on key campaign promises.

US Dollar Index (DXY) Daily Chart, January 6, 2025

Source:TradingView.com

Support

- 108.64

- 108.00

- 107.60

Resistance

- 109.00

- 109.52

- 110.00

Brent Crude Oil Hits 2.5-Month High in Early 2025

The XBR/USD chart shows a strong rally in Brent crude oil prices on January 2–3, breaking above $76.20 for the first time since mid-October.

According to Reuters, this surge was driven by:

- Economic stimulus measures in China, including wage increases for public servants and a significant boost in funding through treasury bonds.

- Forecasts of a colder winter in the US and Europe, potentially increasing demand for oil products.

According to technical analysis of the XBR/USD chart, the price broke out of a consolidation pattern (highlighted in blue) that had confined it in late 2024.

However, signs of waning bullish momentum are emerging:

- At point B, the price only slightly surpassed the previous high at point A before reversing downward, indicating buyer weakness.

- A bearish divergence is forming between the RSI indicator and points A and B.

These signals suggest that Brent crude oil prices could be vulnerable to a correction, potentially targeting the lower blue trendline as a support level.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Bitcoin on the Verge of $100,000 Again

Market Picture

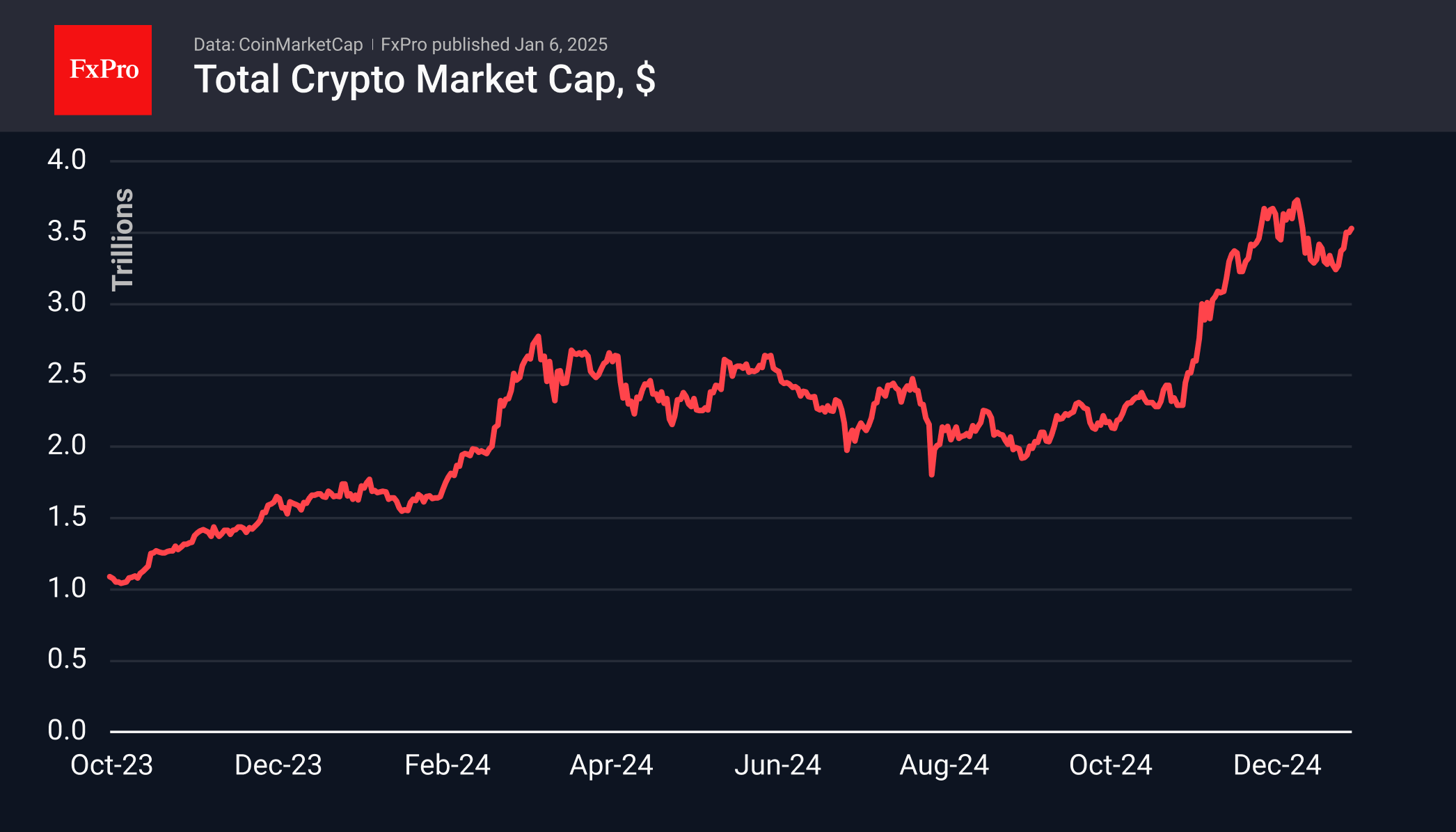

The crypto market capitalisation has surpassed $3.5 trillion, the highest since 19 December. Short-term growth in the market is being replaced by periods of consolidation. The market seems to be probing the ground beneath its feet and moving gently upwards. The sentiment index of 76 (extreme greed) indicates a period of active buying, leaving plenty of room for growth.

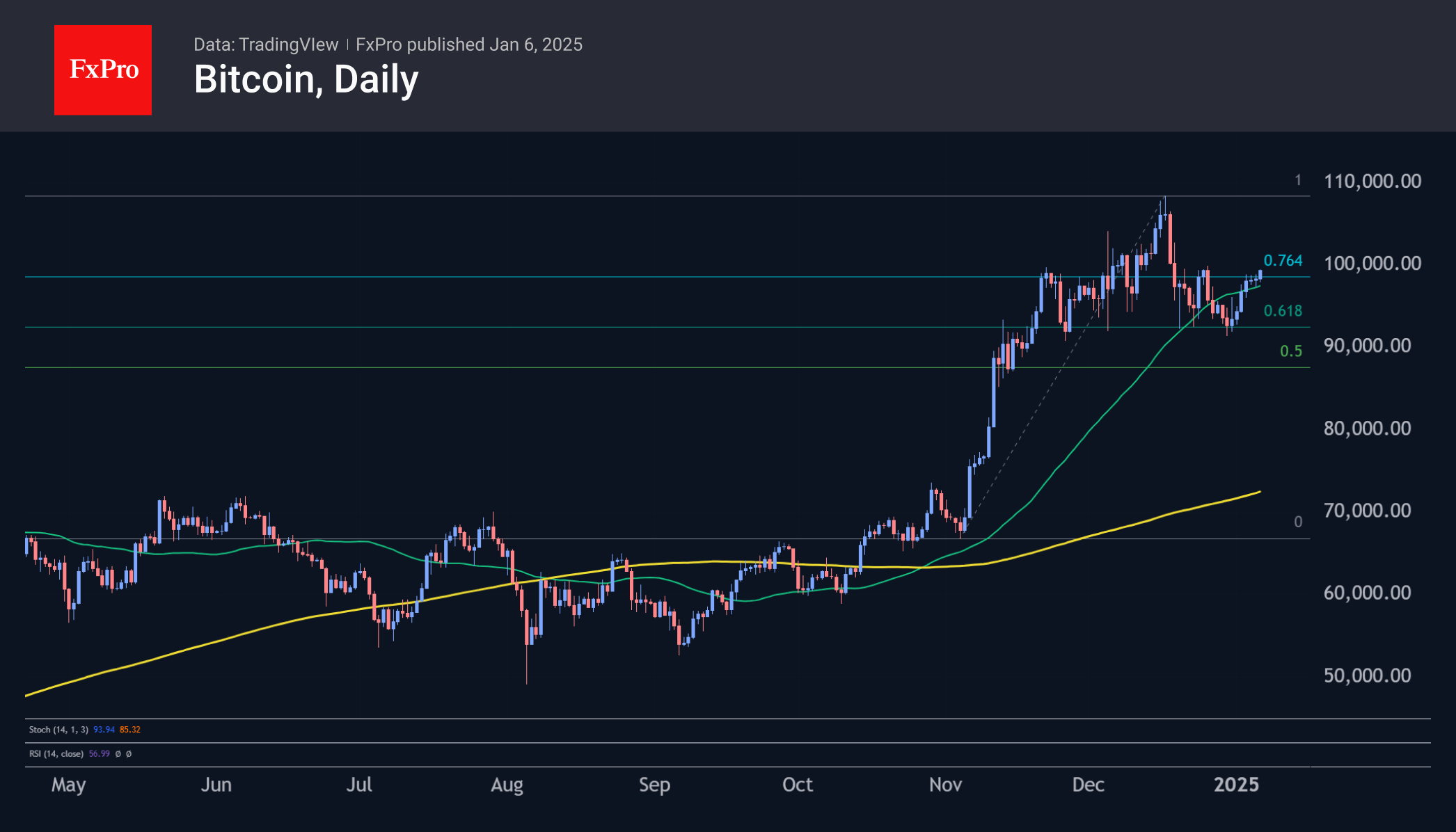

Bitcoin rose for the seventh day in a row and has already passed the $99,000 mark, a level it has traded above for less than two weeks.

So far, the technical picture looks like a classic correction completion with a resumption of the growth of 61.8% of the rally since the beginning of November. This scenario will be confirmed if the historical highs of around $109,000 are confidently breached. At the same time, we expect Bitcoin’s growth to accelerate after the $100,000 mark.

News Background

According to SoSoValue, net inflows into spot Bitcoin ETFs in the US were $908.1 million on Friday, 3 January, with net inflows of $245 million for the week after outflows of $387.5 million earlier. Spot Ethereum-ETFs saw net outflows of $38.2 million for the week, breaking a 5-week positive trend.

MicroStrategy is looking to raise an additional $2bn by selling shares to buy more of the first cryptocurrency. The final decision on the expansion of the BTC investment programme will be made at the shareholder meeting in the first quarter of 2025.

JPMorgan said the share of gold and Bitcoin in investors’ portfolios is expanding. In the long term, the strategy of capital protection against inflation and depreciation of fiat currencies will remain.

Solana developers have created quantum-resistant storage on the blockchain. Solana Winternitz Vault is available as an optional solution and is not yet applicable to the entire blockchain.

Chinese authorities will extend Forex rules to crypto transactions. China’s State Administration of Foreign Exchange (SAFE) has listed cryptocurrency transactions as risky transactions and requires financial organisations to monitor all transactions.

Bitcoin has turned 16 years old. The anonymous creator of Bitcoin, Satoshi Nakamoto, launched the network for the first cryptocurrency on 3 January 2009. At that time, the first block in the BTC network, the so-called genesis block, was created. On 9 February 2011, Bitcoin equalled the value of the US dollar for the first time.