Sample Category Title

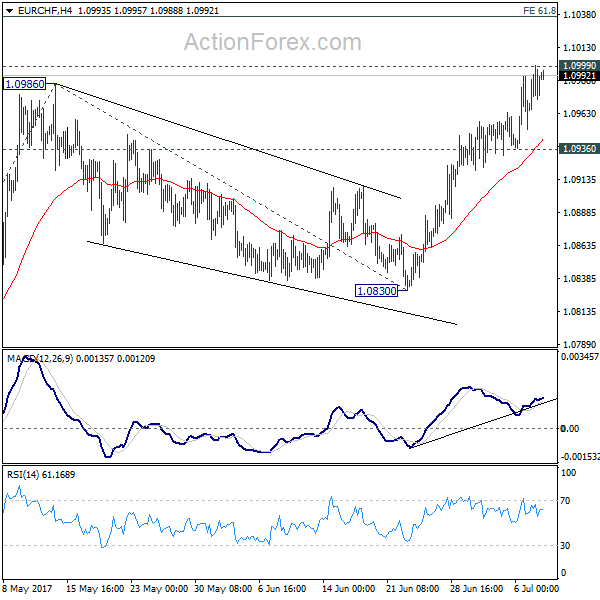

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0965; (P) 1.0982; (R1) 1.1004; More...

Intraday bias in EUR/CHF remains on the upside for the moment. Decisive break of 1.0999 medium resistance will target 61.8% projection of 1.0652 to 1.0986 from 1.0830 at 1.1036 next. On the downside, break of 1.0936 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0830 support holds.

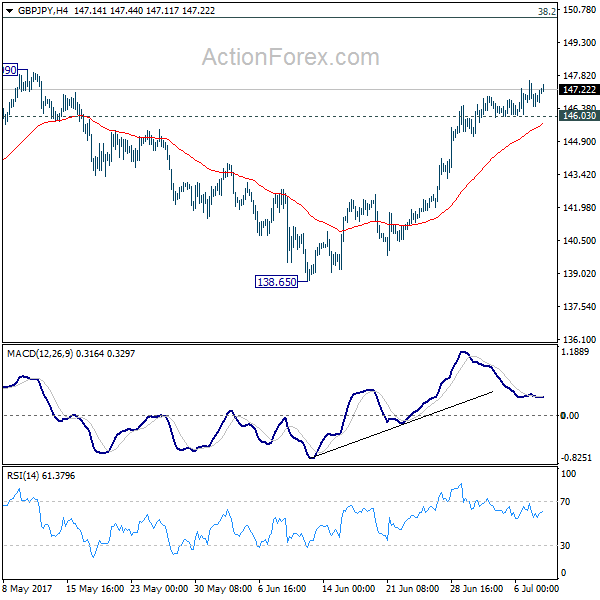

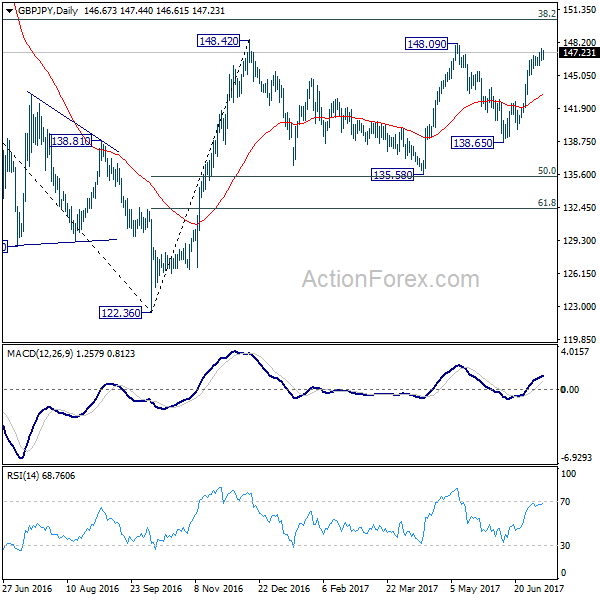

GBP/JPY Daily Outlook

Daily Pivots: (S1) 146.17; (P) 146.88; (R1) 147.40; More....

Upside momentum in GBP/JPY remains a bit weak. Still, with 146.03 minor support intact, further rise is expected for 148.09/42 resistance zone. Decisive break there will extend whole rally from 122.36 to long term fibonacci level at 150.43 next. Nonetheless, break of 146.03 minor support will indicate short term topping. In such case, bias will be turned back to the downside for pull back towards 55 day EMA (now at 143.30).

In the bigger picture, rise from medium term bottom at 122.36 is expected to continue to 38.2% retracement of 196.85 to 122.36 at 150.43. Decisive break there will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case the sideway pattern from 148.42 extends, we'd be looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.

Elliott Wave Analysis: USD Index Showing First Signs Of A Reversal, More Upside In View

USD Index is turning up from recent 95.45 lows where market might have accomplished a bigger impulsive drop down in wave C. That said, current bounce can be a new change in trend, maybe even part of a big impulsive rally, but as always we need to focus on minimum expectation which is a recovery up to the upper channel line, towards 96.70.

USD Index, 4H

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1404

The initial reaction after the test of 1.1445 led to a dip to 1.1380 support and there is an intraday risk of diving lower, for the final leg of the prolonged consolidation pattern. The outlook on the senior frames remains bullish, for 1.1550.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1445 | 1.1550 | 1.1380 | 1.1020 |

| 1.1550 | 1.1610 | 1.1290 | 1.0838 |

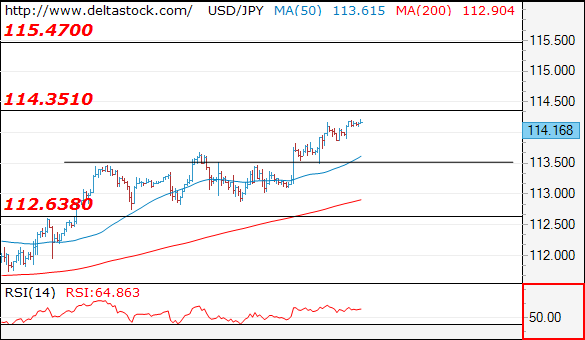

USD/JPY

Current level - 114.16

The bias is positive and my outlook is bullish, for a rise towards 115.40 area. Key support lies at 113.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 114.30 | 114.30 | 113.50 | 110.30 |

| 115.40 | 115.50 | 112.60 | 108.81 |

GBP/USD

Current level - 1.2904

The recent slide from 1.2980 led to a tight test at 1.2860 support and my outlook is already positive, for a renewal of the general uptrend towards 1.3050.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2980 | 1.3130 | 1.2860 | 1.2635 |

| 1.3130 | 1.3500 | 1.2790 | 1.2480 |

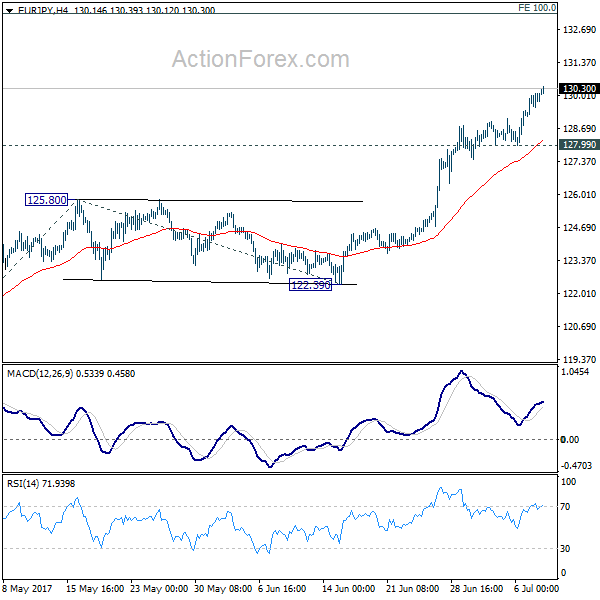

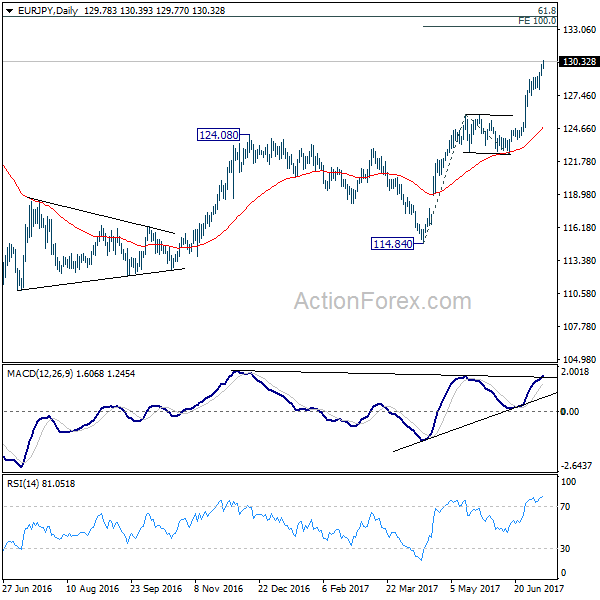

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.30; (P) 129.71; (R1) 130.25; More...

EUR/JPY rises further to as high as 130.39 so far and intraday bias remains on the upside for 100% projection of 114.84 to 125.80 from 122.39 at 133.35 next. On the downside, break of 127.99 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the break of 126.09 support turned resistance should have confirmed completion of down trend form 149.76 (2014 high), at 109.03 (2016 low). Current rise from 109.03 would now target 61.8% retracement of 149.76 to 109.03 at 134.20 and above. Medium term outlook will remain bullish as long as 122.39 support holds.

Yen Stays Weak in Quiet Start, G20 Shrugged

Yen stays weak in an otherwise quiet start to the week. G20 meeting didn't give impact to the markets. Global leaders pledge to continue to "fight protectionism including all unfair trade practices" and "recognize the role of legitimate trade defense instruments in this regard." While leaders have taken note of US's withdrawal from the climate accord, all but US "agree that the Paris Agreement" is irreversible. Regarding migration, G20 somewhat toughen up and said that "we emphasize the sovereign right of states to manage and control their borders and in this regard to establish policies in their own national interests and national security, as well as the importance that repatriation and reintegration of migrants who are not eligible to remain be safe and humane."

BoJ offered another upbeat assessment on economy

In a BoJ quarterly report, the central bank upgraded the assessment on regional Japan. Six regional economies are described as "expanding moderately" or "moving toward a moderate expansion". That's seen as the most upbeat language since 2005. BoJ Governor Haruhiko Kuroda also said that "Japan's economy is expected to continue expanding moderately ahead." Nonetheless, Kuroda also remained cautious and reiterated the pledge to maintain ultra-loose monetary policy until the 2% inflation target is met. Released from Japan, machines orders dropped -3.6% mom in May versus expectation of 0.7% mom rise. Current account surplus narrowed to JPY 1.40T in May. Eco Watchers sentiment rose to 50 in June.

ECB Villeroy: Next fall is time to adapt the intensity of stimulus

In Eurozone, ECB Governing Council member Francois Villeroy de Galhau said that it will be the central bank's decision "next fall" on "on adapting the intensity" of the monetary policy that "progress toward our inflation target and toward economic recovery." He used the phrase "adapt the intensity" a total of three times. That is seen by analysts as sign that ECB could pare back stimulus that would have least impact to tighten up financial conditions. Executive Board member Benoit Coeure also said last Friday that the central bank's decision to lower monthly bond purchase from EUR 80b to 60b is a guide for future policy adjustments. For now, markets generally expect ECB to announce a tapering plan in September that would bring down monthly asset purchase to zero in 2018.

Elsewhere

China PPI was unchanged at 1.5% yoy in June. PPI also unchanged at 5.5% yoy. German trade surplus widened slightly to EUR 20.3b in May. Eurozone Sentix investor confidence will be release in European session. US will release labor market conditions index. Looking ahead, the economic calendar is not particularly heavy this week. BoC rate decision is the main focus and recent developments are setting up for a 25bps rate hike to 0.75%. UK job data will be watched as recent disappointing data cooled some BoE hike expectations. US will release PPIU and CPI. But most attention will be on Fed chair Janet Yellen's testimony .

Here are some highlights for the week ahead:

- Tuesday: Australia NAB business confidence, home loans; Japan machine tools orders; Canada housing starts

- Wednesday: Japan tertiary industry index; UK employment; Eurozone industrial production; BoC rate decision

- Thursday: China trade balance; German CPI final; Swiss PPI; Canada housing starts; US PPI, jobless claims; Fed chair Yellen testimony

- Friday: Eurozone trade balance; US CPI, retail sales, industrial production, U of Michigan sentiment; business inventories

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.30; (P) 129.71; (R1) 130.25; More...

EUR/JPY rises further to as high as 130.39 so far and intraday bias remains on the upside for 100% projection of 114.84 to 125.80 from 122.39 at 133.35 next. On the downside, break of 127.99 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the break of 126.09 support turned resistance should have confirmed completion of down trend form 149.76 (2014 high), at 109.03 (2016 low). Current rise from 109.03 would now target 61.8% retracement of 149.76 to 109.03 at 134.20 and above. Medium term outlook will remain bullish as long as 122.39 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M May | -3.60% | 1.70% | -3.10% | |

| 23:50 | JPY | Current Account (JPY) May | 1.40T | 1.63T | 1.81T | |

| 1:30 | CNY | CPI Y/Y Jun | 1.50% | 1.60% | 1.50% | |

| 1:30 | CNY | PPI Y/Y Jun | 5.50% | 5.50% | 5.50% | |

| 5:00 | JPY | Eco Watchers Survey Current Jun | 50 | 49 | 48.6 | |

| 6:00 | EUR | German Trade Balance (EUR) May | 20.3B | 20.3B | 19.8B | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Jul | 28.1 | 28.4 | ||

| 14:00 | USD | Labor Market Conditions Index Change Jun | 2.3 |

US Dollar Trades Mixed On Payrolls Report

The US dollar closed on Friday with some modest gains following a broadly better than expected jobs report. Data from Labor department showed that payrolls increased 222,000 in the month of June. This was higher than the estimates of 173,000 that was forecast by economists. The unemployment rate inched higher to 4.4%, from 4.3% previously while average earnings remained steady at 2.5% on the year.

The greenback was mixed as the currency posted gains across the board, but the Canadian dollar managed to emerge on the top last Friday. This was followed by the Australian and the Kiwi dollars which posted gains.

Looking ahead, the economic calendar today is light. China's inflation figures released earlier in the day showed that consumer prices rose 1.5% on the month, missing estimates of 1.6% increase. China's producer prices index was also steady, rising 5.5%, same as the previous month.

The German trade balance figures and the Eurozone Sentix investor confidence will be the other data points that will be released later today.

EURUSD intraday analysis

EURUSD (1.1402): The EURUSD attempted to rally back to the $1.1400 handle last week. The positive gains on Thursday were partly erased by Friday's declines as EURUSD closed at 1.1403. In the short term, price action is likely to trade within a range ahead of key events this week that includes the semi-annual testimony to Congress by Fed Chair, Janet Yellen. The lower high formed in EURUSD on the 4-hour chart suggests that price action could be biased lower. Support is seen at 1.1357 followed by 1.1300. A breakdown below this level could see the common currency post further declines. However, if support is established at 1.1357 or 1.1300, then expect further gains with the currency pair likely to remain consolidating above this level.

GBPUSD intraday analysis

GBPUSD (1.2893): The British pound posted strong declines on Friday after price reversed near the resistance level of 1.2975 as expected. The declines came as the UK's industrial and manufacturing production data was weaker than expected. Industrial output fell 0.1% while manufacturing production declined 0.2% on the month. The GBPUSD fell to a 7-day low, closing on Friday at 1.2893. Price action is currently looking to retrace some of those declines but resistance at 1.2900 could likely cap the retracement. This will confirm a decline in GBPUSD towards 1.2800 where support is very likely to be tested.

USDJPY intraday analysis

USDJPY (114.14): The USDJPY continues its ascent with prices now seen trading near the 114.00 handle. The strong gains have managed to push USDJPY closed to testing the May 10th highs of 114.37. Establishing resistance here could see a short-term decline back to the lower support at 112.00. However, a breakout above 114.37 could keep the bullish momentum going. In the near term, watch for support at 113.36 which has already witnessed some strong consolidation.

GBPJPY Bullish In The Short- And Medium-Term, Eyes One-Month High

GBPJPY has advanced by nearly half a percent in today’s trading so far, eyeing Friday’s one-month high of 147.60.

The short-term momentum as depicted by the RSI is bullish. Specifically, the indicator is well above its 50 neutral-perceived level and currently maintains a positive slope. Notice though that at 69, it is close to the 70 overbought level.

If the price keeps advancing, resistance could be met around Friday’s high of 147.60. Further up, a potential psychological level, namely the 148.00 handle, combined with the seven-month high of 148.10 from May 10, might form an additional barrier to the upside.

Should the price decline, the area around the 146.00 handle, which is another potential psychological level that was of significance in the recent past, could provide support. Further declines would shift the focus to the area around the current level of the 50-day moving average (MA) at 143.96 for additional support.

Regarding the medium-term outlook, the pair recorded a bullish cross in January. This is a positive medium-term signal whose strength is supported by the price being above the 50- and 200-day MAs, as well as by both MAs currently being upward sloping. The divergence between the price and the two MAs could be a sign of an overextended rally though.

Overall, both the short- and medium-term are currently bullish.

EURUSD Consolidates Around 1.14, Maintains Bullish Trend

EURUSD is consolidating around the key psychological level at 1.1400. After hitting a 13-month high of 1.1445 on June 29, there was a slight pullback since the market reached overbought conditions, as was indicated by the RSI rising to 70.

Upside momentum has weakened and a neutral phase is expected in the near term. Any corrective move lower would likely find support at 1.1290. This is considered to be an important level since it was recently tested as both support and resistance. Further weakness below this level may see EURUSD slip towards 1.1108. A break from here would target 1.0822, which is where the 200-day moving average converges and was also a level previously tested as support and resistance.

Looking at the bigger picture, the uptrend that started from the January 3 low of 1.0340 to the June 29 high of 1.1445 is still intact. There are no signs of a reversal in the uptrend yet. The risk is to the upside based on the bullish market structure on the daily chart. There was a bullish crossover of the 50-day MA with the 200-day MA on May 23, while the 50-day MA is still rising. RSI remains in bullish territory above 50. All these technical signals highlight the bullish bias in the market.

A successful break above the 1.1445 high would open the way towards the key 1.1500 area with scope to target the May 3, 2016 peak of 1.1616. Such a move would strengthen the medium-term bullish bias.

Market Update – Asian Session: China CPI/PPI In Line And BOJ Affirms Policy Stance

Asia Summary

Markets take a risk on sentiment at the start of the week, seemingly unconcerned about the G20 who met over the weekend in Hamburg, Germany among heavy protesting. The Communique was fairly standard, reiterating to fight protectionism and secure free trade. New elements include to agree by November steps to reduce global overcapacity of steel and in afirst ever dissent: 19 members affirmed the Paris accord with the US (dissenter) saying it will help other countries "access and use fossil fuels more cleanly and efficiently."

Japan govt cut its assessment of machinery orders for the first time since September 2016 after May orders fell 3.6% m/m and only rose 0.6% y/y v the expected 7.6%. USD/JPY rose 0.1% to 113.99 after the data and later tested 114.20. The PBOC again skipped open market operations for the 12th consecutive day, while local press highlighted financial stability as a major topic for the National Financial Work Conference, which will start in mid-July. CPI and PPI were a non-event in the session.

Global shipping names rallied after Cosco Shipping (1919.HK) confirmed it will acquire Orient Overseas for HK$78.67/shr in a HK$49.2B deal. Maersk gave their support of the deal, saying consolidation would be good for the industry.

Key economic data

(CN) CHINA JUN CPI M/M: -0.2% V -0.1% PRIOR; Y/Y: 1.5% V 1.6%E

(CN) CHINA JUN PPI Y/Y: 5.5% V 5.5%E

(JP) JAPAN JUN BANK LENDING (INC TRUSTS) Y/Y: 3.3% V 3.2%E; BANK LENDING (EX-TRUSTS) Y/Y: 3.3% V 3.3%E

(JP) JAPAN MAY TOTAL CURRENT ACCOUNT: ¥1.65T V ¥1.79TE; ADJ TOTALCURRENT ACCOUNT: ¥1.40T V ¥1.63TE; TRADE BALANCE BOP BASIS: -¥115.1B V -¥45.0BE

(JP) JAPAN MAY MACHINE ORDERS M/M: -3.6% V 1.7%E; Y/Y: 0.6% V 7.6%E

(JP) Japan Jun Bankruptcies Y/Y: -7.5% v 19.5% prior

Speakers and Press

China

(CN) China Head of State Administration of Foreign Exchange (SAFE) Pan Gongsheng said no intention of devaluing yuan currency to boost its competitiveness – financial press

(CN) Overseas M&A expected to be major talking point at National Financial Work Conference in mid-July - SCMP

Japan

(JP) Bank of Japan (BOJ) Gov Kuroda: Economy is turning towards moderate expansion; BOJ will continue to adjust policy as needed

(JP) According to Yomiuri poll Japan PM Abe approval rating fell to 36% from 49% in June (lowest reading since being in office)

Australia/New Zealand

(AU) Australia Department of Industry, Science and Innovation: Iron ore will sink back below $50/ metric ton next year as global supply expands and demand moderates in China

(NZ) New Zealand Ministry of Business, Innovation and Employment: Find no evidence of China steel coil dumping

US

(US) Fed's Kashkari says large banks need to raise 'much more' equity - US financial press

Asian Equity Indices/Futures (00:30ET)

Nikkei +0.8%, Hang Seng 1.0%, Shanghai Composite -0.2%, ASX200 +0.5%, Kospi +0.3%

Equity Futures: S&P500 +0.2%; Nasdaq +0.4%, Dax +0.2%, FTSE100 +0.3%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1409-1.1390; JPY 114.20-113.89; AUD 0.7615-0.7596; NZD 0.7281-0.7265

Aug Gold +0.1% at 1,210/oz; Aug Crude Oil +-0.8% at $44.58/brl; Sept Copper +0.2% at $2.66/lb

(AU) Australia repurchases A$500M in Oct 2018 and March 2019 bonds

(CN) PBoC skips open market operations (12th straight session)

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.7964 V 6.7914 PRIOR

(KR) Bank of Korea (BOK) sells KRW1.20T v KRW1.2T offered in 1-yr monetary stabilization bonds; avg yield 1.46% v 1.47% prior

(KR) South Korea sells 5-year bonds at 1.985%

(JP) Japan 5-year JGB yield hits highest level since Jan 2016, near -0.03%

Asia equities notable movers

Australia

Bellamy's Australia, BAL.AU China suspends export licence of newly acquired canning facility

Ardent Leisure Group,AAD.AU Reports June theme park unit visitation -30.5% y/y, Rev A$4.4M, -35.3% y/y; +2.5%

88 Energy,88E.AU Gives update on Project Icewine, located onshore North Slope of Alaska; -25.5%

Japan

KDDI Corp, 9433.JP President comments on mobile price cuts: Says price cuts needed to compete with Mvnos; -3.1%

Hong Kong/China

316.HK China COSCO Shipping Holdings confirms to bid HK$49.2B ($6.3B) or HK$78.67/share in cash for Orient Overseas International (~31% premium); +24.2%

China Life, 2628.HK China Development said to seek to buy up to 25.3% of China Life - US financial press; +0.4%

US

MYCC To be acquired by Apollo Global Management for $17.12/shr cash (~31% premium); declares one time dividend of $0.13

PBR Federal Court of Appeals in New York partially grants appeal related to class action

WFC Court Grants Preliminary Approval of $142M Settlement in Wells Fargo Unauthorized Accounts Class Action

US market Friday Summary

US stock markets moved up after the June jobs report offered more of the same for investors and the Fed to ponder. Fears that the Fed might have made (or is about to make) a policy mistake should ease, but the data are likely to suggest to the Fed that there is no urgency about raising rates again soon. Job growth accelerated ahead of forecasts, but wage growth came up short of expectations once again. The unemployment rate ticked up along with the participation rate, indicating some slack likely still exists for the US labor market. The NASDAQ reversed course once again, adhering to the fickle nature of trade that has engulfed technology stocks in recent weeks. Along with the strength in technology, homebuilding stocks move higher along with healthcare and deep cyclical sectors. The energy complex moved lower along with crude oil prices.

US rates drifted higher, while the Treasury curve continued to steepen, and TIPS breakeven spreads came off, helped by the decline in oil prices. The US Dollar firmed almost across the board, with the exception being the Loonie. The Canadian Dollar surged after a Canada jobs report crushed expectations. The Yen remained under pressure after the BOJ offered to buy unlimited amount in fixed-rate bonds as part of their yield control operations. Gold prices dropped back towards the 1200 mark, hitting that level for the first time since March.