Sample Category Title

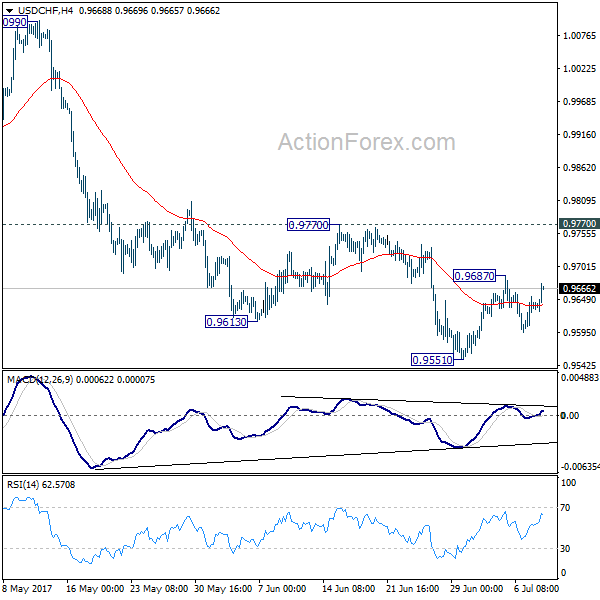

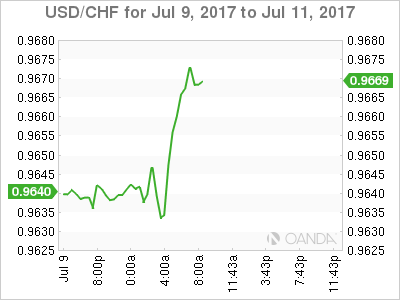

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9600; (P) 0.9627; (R1) 0.9663; More......

USD/CHF's consolidation from 0.9551 is still in progress and intraday bias remains neutral. In case of another rise, upside should be limited by 0.9770 resistance and bring fall resumption. Break of 0.9551 will extend the whole fall from 1.0342 and target 0.9443 key support level next. We'd expect strong support from there to bring rebound. Meanwhile, firm break of 0.9770 will indicate near term reversal, on bullish convergence condition in 4 hour MACD.

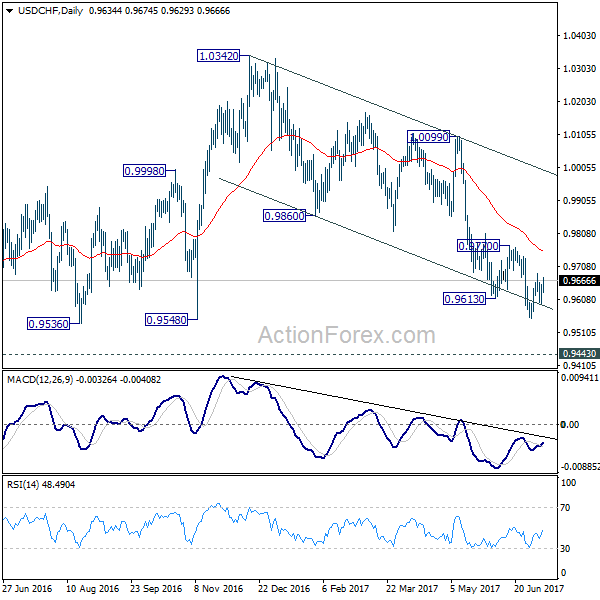

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

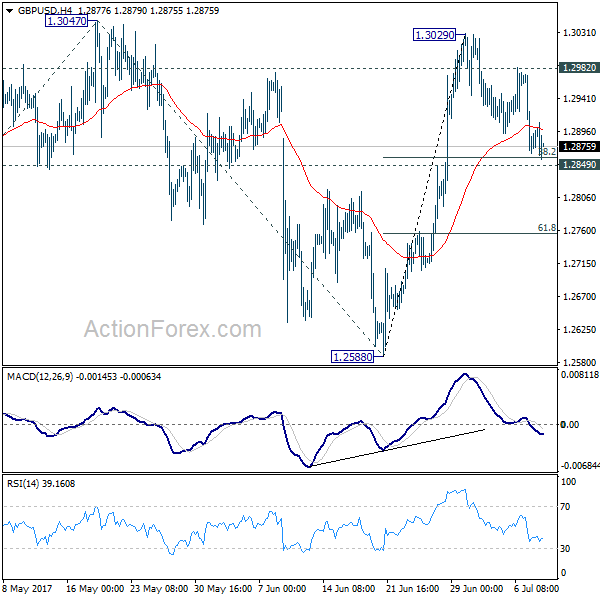

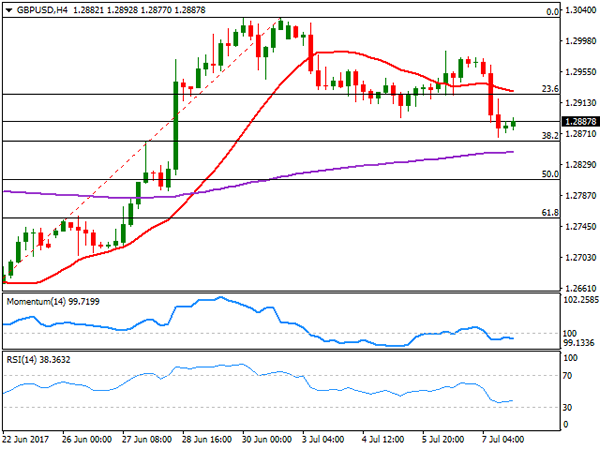

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2837; (P) 1.2905; (R1) 1.2945; More...

No change in GBP/USD's outlook as the correction from 1.3029 is still in progress. We'd continue to expect strong support from 1.2849 to contain downside and bring rise resumption. Above 1.2982 minor resistance should turn bias back to the upside for 1.3047 resistance. Break will target 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next. However, sustained break of 1.2849 will dampen our near term bullish view and turn focus back to 1.2588 support.

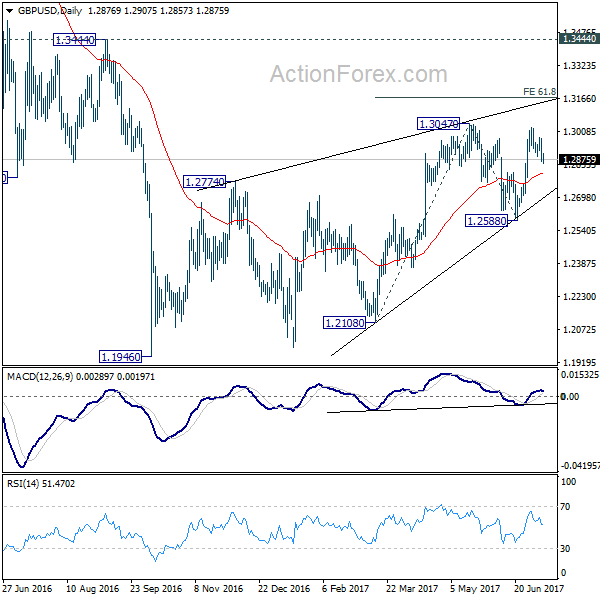

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

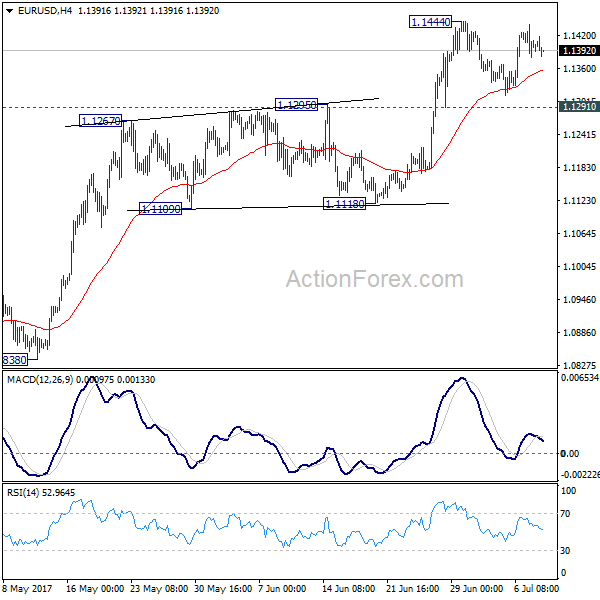

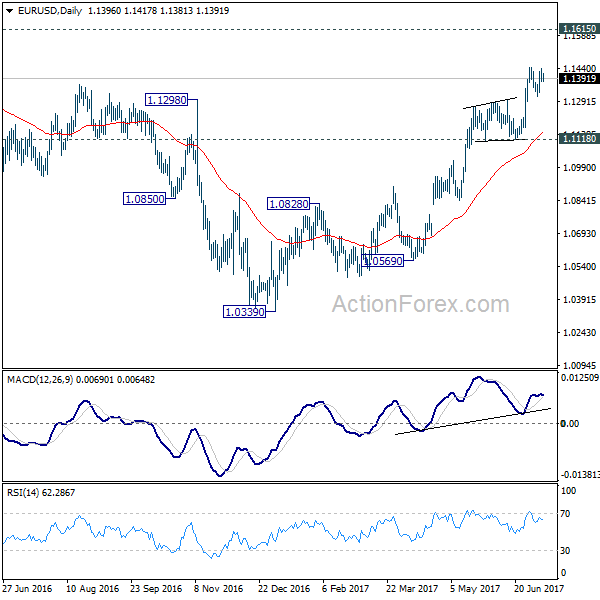

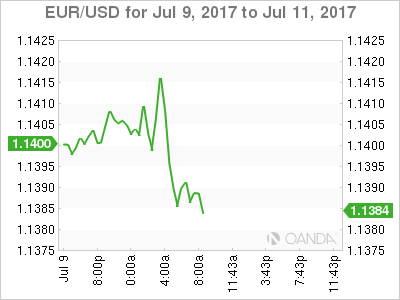

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1371; (P) 1.1405 (R1) 1.1431; More.....

EUR/USD continues to stay in range below 1.1444 and intraday bias remains neutral. Consolidation could extend but in case of another fall, downside should be contained by 1.1291 resistance turned support to bring rise resumption. Break of 1.1444 will extend the rally from 1.0339 low to 1.1615 resistance next. Meanwhile, break of 1.1291 will turn focus back to 1.1118 support instead.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1763). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Euro Firm as Sentix Stayed Closed to 10 Year High, Markets in Range Trading

The forex markets are generally staying in tight range today. Yen is attempting to extend recent down trend but momentum is relatively weak. In particular, USD/JPY is feeling a bit heavy ahead of 114.36 key medium term resistance level. Euro is firm as Sentix investor confidence stayed closed to 10 year high in July. But both Dollar and Sterling are mildly stronger and they pare some of last week's losses. Canadian Dollar is also in consolidation even though markets are expecting BoC to deliver a 25bps rate hike later in the week. In other markets, Gold dips to as low as 1204 and is held below 1210 handle so far. WTI crude oil is mildly lower at around 44.0.

Eurozone Sentix stayed closed to 10 year high

Eurozone Sentix investor confidence dropped 0.1 to 28.3 in July but beat expectation of 28.3. That's also close enough to the 10 year high at 28.4 made last month. Sentix noted in the statement that "in the last few days, the fears of investors before a change in interest rate policy in the euro area determined market activity." While investors' assessment rose for the seven straight month, expectations "cannot quite keep up". "The trend continues to be in the Eurozone, but the momentum should have reached a certain zenith." It also noted that the central bank policy index dropped to -26 as "it has been clear to investors that the ECB must leave its expansive course." But the inflation expectation index had an opposing trend and rose to -15.75. Sentix said that "it would not be a surprise if Mario Draghi at the next ECB meeting would rather warn investors not to be certain in their assessment of the speed of monetary policy, not the direction itself."

ECB Villeroy: Next fall is time to adapt the intensity of stimulus

ECB Governing Council member Francois Villeroy de Galhau said that it will be the central bank's decision "next fall" on "on adapting the intensity" of the monetary policy that "progress toward our inflation target and toward economic recovery." He used the phrase "adapt the intensity" a total of three times. That is seen by analysts as sign that ECB could pare back stimulus that would have least impact to tighten up financial conditions. Executive Board member Benoit Coeure also said last Friday that the central bank's decision to lower monthly bond purchase from EUR 80b to 60b is a guide for future policy adjustments. For now, markets generally expect ECB to announce a tapering plan in September that would bring down monthly asset purchase to zero in 2018.

BoJ offered another upbeat assessment on economy

In a BoJ quarterly report, the central bank upgraded the assessment on regional Japan. Six regional economies are described as "expanding moderately" or "moving toward a moderate expansion". That's seen as the most upbeat language since 2005. BoJ Governor Haruhiko Kuroda also said that "Japan's economy is expected to continue expanding moderately ahead." Nonetheless, Kuroda also remained cautious and reiterated the pledge to maintain ultra-loose monetary policy until the 2% inflation target is met. Released from Japan, machines orders dropped -3.6% mom in May versus expectation of 0.7% mom rise. Current account surplus narrowed to JPY 1.40T in May. Eco Watchers sentiment rose to 50 in June.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1371; (P) 1.1405 (R1) 1.1431; More.....

EUR/USD continues to stay in range below 1.1444 and intraday bias remains neutral. Consolidation could extend but in case of another fall, downside should be contained by 1.1291 resistance turned support to bring rise resumption. Break of 1.1444 will extend the rally from 1.0339 low to 1.1615 resistance next. Meanwhile, break of 1.1291 will turn focus back to 1.1118 support instead.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1763). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M May | -3.60% | 1.70% | -3.10% | |

| 23:50 | JPY | Current Account (JPY) May | 1.40T | 1.63T | 1.81T | |

| 1:30 | CNY | CPI Y/Y Jun | 1.50% | 1.60% | 1.50% | |

| 1:30 | CNY | PPI Y/Y Jun | 5.50% | 5.50% | 5.50% | |

| 5:00 | JPY | Eco Watchers Survey Current Jun | 50 | 49 | 48.6 | |

| 6:00 | EUR | German Trade Balance (EUR) May | 20.3B | 20.3B | 19.8B | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Jul | 28.3 | 28.1 | 28.4 | |

| 14:00 | USD | Labor Market Conditions Index Change Jun | 2.3 |

Dollar Firms While Oil Remains Under Pressure

It appears that equity markets have taken inspiration from the performance on Wall Street at the conclusion of last week, with Asian stocks trading broadly higher and European shares looking positive at the time of writing. The "Goldilocks" US jobs report seems to have acted as a catalyst to help risk sentiment, with the mixed nature of the June jobs report providing a platform of a support for the USD, while exciting equity bulls as strong job growth is a characteristic of a healthy economy, with the tepid wage growths suggesting a slower pace of monetary changes from the Federal Reserve.

With both the Asian and European markets marching into the new trading week on solid footing and investors appearing optimistic over the current outlook for the global economy, Wall Street could be in line to trade higher this afternoon

OPEC turns to Nigeria and Libya

It's quite remarkable how the supply cut exemptions from some OPEC members have come back to punish the cartel, as production in June climbed to the highest level so far in 2017. With the increasing output from Nigeria and Libya threatening to disrupt the efforts made by the rest of the group to rebalance the markets and not being something that was priced in, the price of oil could remain under pressure. There are reports circulating over the possibility that OPEC will request both Nigeria and Libya to cut production and while these might read as desperate, increased production from both nations was likely not factored into consideration when OPEC greed to extend its production cut. With the oversupply dynamics still weighing heavily on the mind of investors, the price of oil remains under pressure as oversupply remains the name of the game when it comes to price fluctuations

Dollar regains its footing

The Greenback stood tall during Monday's trading session as investors digested June's mixed employment report. While the impressive NFP headline number of 222k boosted sentiment towards the US economy and supported expectations of the Federal Reserve raising rates, the tepid wage growth fanned concerns over inflation lagging for prolonged periods. Although June's "Goldilocks" report may inspire Dollar bullish investors, the upside could still face headwinds as the lower inflation levels suggest a slower pace of monetary changes from the Federal Reserve. With the economic calendar fairly light today, price action may dictate where the Dollar Index trades with bulls eyeing 96.40.

Investors will be paying very close attention to Janet Yellen's testimony on Wednesday and Thursday for clues on when the central bank plans to unwind its balance sheet and raise US interest rates in the second half of 2017. It will be interesting to hear Yellen's thoughts on the latest jobs and inflation data and if she maintains her hawkish tone.

Commodity spotlight - Gold

Gold was under renewed selling pressure on Monday as the combination of Dollar strength and rising prospects of tighter global monetary policies punished the zero-yielding metal. With June's mixed jobs report supporting expectations of the Federal Reserve taking action this year, bears seem to be back. It will be interesting to see how prices react to the $1200 support and if buyers use this opportunity to propel the metal higher. From a technical standpoint, the yellow metal is coming under increasing selling pressure on the daily charts. The breakdown below $1214 may encourage a further decline towards $1200.

Will the Bank of Canada Pull the Trigger?

Monday July 10: Five things the markets are talking about

To date, rising interest rates continue to overshadow geopolitical developments and it's the Bank of Canada (BoC) turn this week to practice what G7 Central Banks have been preaching of late.

Over the past fortnight, markets have reassessed the outlook for tighter monetary policies from major central banks following a string of hawkish remarks.

Given the good economic news recently in Canada, Governor Poloz is expected to increase its policy interest rate by +25 bps points to +0.75% on Wednesday (10:00 am EDT). At the same time the Bank will publish its Monetary Policy Report with its current forecasts.

However, if they disappoint it will get very messy again for the loonie (C$1,2910) - over the last month, the CAD's painful rise has taken the 'bears' by surprise.

Note: The last time the BoC changed rates was two years ago when it lowered its policy rate by -25 bps.

Friday's solid U.S employment growth without inflation should keeps the Fed normalizing policy at a 'slow' pace, which is positive for equities, mixed for the dollar and yields.

Also on Wednesday, capital markets will look to the Fed's Janet Yellen's testimony before Congress for guidance on when the Fed could start reducing its balance sheet.

1. Stocks like employment reports

In Japan, stocks rallied to more than one-week highs overnight, following U.S equities after Friday's non-farm payroll (NFP) report supported the dollar outright against the yen (¥114.22). The Nikkei gained +0.8% while the broader Topix Index added +0.5%.

Down-under, Australia's S&P/ASX 200 Index gained +0.4%, while in Hong Kong, the Hang Seng Index rose +0.7%.

In mainland China, stock indexes were little changed as investors awaited fresh catalysts ahead of a plethora of data due next week.

Note: On July 17, China will release Q2 gross domestic product (GDP), along with June industrial output, retail sales and January-June fixed asset investment.

Overnight, markets shrugged off China's June inflation data, which met expectations and did little to alter the view that economic growth is cooling after a solid Q1 - June CPI rallied +1.5% y/y.

In Europe, markets have opened higher and continue to remain positive, as risk sentiment has improved over the weekend. Consumer discretionary sector lead the gains, while energy stocks again weigh on indexes.

U.S equities are set to open in the red (+0.1%).

Indices: Stoxx50 +0.4% at 3,475, FTSE +0.3% at 7,374, DAX +0.6% at 12,464, CAC-40 +0.2% at 5,158, IBEX-35 -0.3% at 10,460, FTSE MIB +0.6% at 21,147, SMI +0.7% at 8,944, S&P futures +0.1%

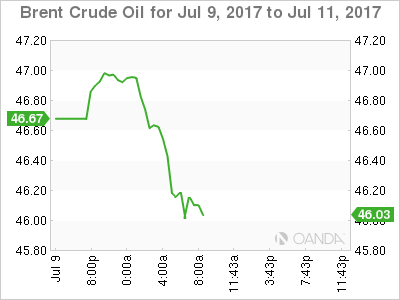

2. Oil edges up but market still under pressure

Last week, crude oil prices rolled over mid-week giving back half of gains seen since June 21.

Nevertheless, oil prices have recovered some losses overnight after its -3% fall Friday, but markets remain under pressure from high drilling activity in the U.S and ample supplies from OPEC.

Brent crude futures are at +$46.80 per barrel, up +9c or +0.2% percent from their Friday's close. U.S West Texas Intermediate (WTI) crude futures are at +$44.33 per barrel, up +10c c, or +0.2%.

The dynamics have not changed for oil; speculators are predominately booking some profits.

Note: Brent prices are -17% below their 2017 opening despite a deal OPEC to cut production from January.

On Friday Baker Hughes data showed that U.S energy firms added +7 oil drilling rigs last week, marking a 24th week of increases out of the last 25 and bringing the total count up to +763, the most since April 2015.

Note: U.S oil production has risen over +10% since mid-2016 to +9.34m bpd.

Gold is little changed overnight (-0.3% to +$1,207.88 an ounce) hovering atop of its four-month lows after stronger than expected U.S jobs data indicated that the Fed would maintain its stance on monetary tightening. On Friday, the yellow metal fell to its lowest print since March 15 and -2.3% on the week.

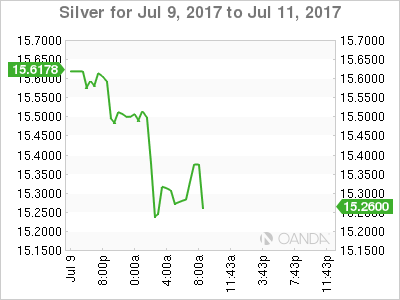

Silver fell about -6% last week to +$14.86 an ounce, its lowest in 15 months.

3. Global Yield curves getting steeper

Recent moves in the fixed income market are not for the faint hearted.

The U.S 10-year yield (+2.385%) has climbed nearly +25 bps from its 2017 low at the end of last month as investors brace for the possibility that the ECB will begins to withdraw its bond-buying stimulus.

With European economic data continuing to surpass expectations has resulted in the German 10-year Bund yield moving back above the psychological +0.5% level not seen since early last year.

Currently, U.S rates are tracking Euro yields higher, a move that appears justified by Friday's robust June jobs report.

Current consensus expects the 10-year yield to rise to +2.66% by year-end, +0.45% above where it was trading at the beginning of June.

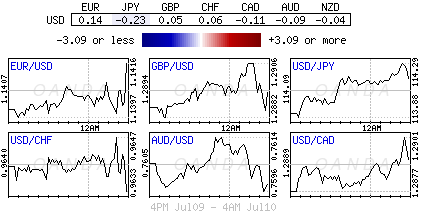

4. USD steady, EUR toppish, JPY weaker, Pound vulnerable

Over the last week, the EUR (€1.1383) has moved to a one-month high outright, while GBP (£1.2863, €0.8848) has suffered after U.K economic releases significantly lagged that of continental Europe's. The 'big' dollar has also rallied to the highest level since early May against the Yen (¥114.20) - supported by the BoJ's actions Friday who were forced to offer an unlimited amount of bids in its fixed-rate bond operation to stem the rise in JGB bond yields.

Where to from here? Further gains for EUR may be tough, there seems to be few near-term catalysts to build on this recent rally, while the recent weak U.K data makes an interest-rate rise by the BoE unlikely for now, leaving sterling vulnerable to further declines - especially against the dollar.

5. Swiss Sight Deposits Little Changed

The latest sight deposits data from the Swiss National Bank (SNB) suggests the bank largely refrained from intervening in currency markets last week, as the EUR (€1.0998) flirts with one-year highs against the franc.

Sight deposits - considered a proxy for intervention - were +578.7B CHF, little changed from the previous week.

DAX Edges Higher as Eurozone Investor Confidence Beats Estimate

The DAX index has edged higher in the Monday session, as the index is up 0.32% on the day. Currently, the DAX is at 12,437.00. On the release front, Germany's trade surplus widened to EUR 20.3 billion, matching the forecast. The Eurozone Sentix Investor Confidence edged up to 28.4, above the estimate of 28.1.

The new trading week has started with positive data. Germany's trade surplus climbed to EUR 20.3 billion in May, which was the second highest surplus this year. A boom in exports continues to lead to a favorable trade balance, and the manufacturing sector has also benefited from stronger global demand for German products. The German economy has also received a boost from strong domestic demand, and the labor market remains tight. The IMF has upgraded its forecast for the German growth to 1.8 percent in 2017, up from its estimate of 1.6 percent in April.

With the euro-area continuing to record stronger growth, the ECB is tiptoeing towards a tighter policy, as underscored by the ECB's June minutes. Policymakers discussed removing its "easing bias" at the June meeting, but ultimately decided not to make a move, since stronger economic conditions had not resulted in higher inflation. At the same time, minutes were cautious in tone, noting that "it was necessary to avoid signals that could trigger a premature tightening of financial conditions". ECB chief economist Peter Praet reiterated the bank's stance at a conference in Paris last week. Praet noted that eurozone economic growth is accelerating, but said that the ECB still needs to provide a "steady hand" in order to spur stubbornly low inflation levels. The ECB holds its next policy meeting on July 20. In June, the bank removed an easing bias towards lowering interest rates. However, policymakers may now be wary about sending more signals of tightening policy, so as to avoid another run on the euro, as was the case after Draghi's comments at the ECB forum. The ECB doesn't want the rate statement to shake up markets, so we could see an innocuous statement, to the effect that the economy is headed in the right direction, but QE will remain in place until inflation levels move higher.

Euro Inches Lower, German Trade Balance Matches Forecast

The euro has edged lower at the start of the week. Currently, the pair is trading slightly below the 1.14 level. It’s a quiet start to the week, with no major releases out of the eurozone or the US. On the release front, Germany’s trade deficit widened to EUR 20.3 billion, matching the forecast. The Eurozone Sentix Investor Confidence edged up to 28.4, above the estimate of 28.1.

US employment numbers were a mix on Friday, and EUR/USD didn’t show much interest. Nonfarm Payrolls rebounded in June, climbing to 222 thousand. This easily beat the estimate of 175 thousand. However, wage growth remained stuck at 0.2%, shy of the forecast of 0.3%. Wage growth has been soft in the first half of 2017, which has contributed to low inflation numbers.

The Fed has consistently said that it plans to raise interest rates for a third and final time in December. In June, Fed Chair Janet Yellen shrugged off inflation worries, saying that she expected inflation was mired at lows levels due to temporary factors. However, the markets don’t seem to be buying in, as the odds of a December hike have dropped to 47%, according to the CME Group. The US economy slowed down in the first quarter, and there are signs that Q2 will also be soft. Consumer spending, which comprises two-thirds of US economic growth, remains soft. Another sore point in the economy is inflation, which remains below the Fed’s target of 2%. If the economy doesn’t show signs of stronger growth and higher inflation, the Fed might change its tune about a December rate, which would likely send the US dollar lower.

With the eurozone economy showing broad improvement, the ECB is tiptoeing towards a tighter policy, as underscored by the ECB’s June minutes. Policymakers discussed removing its 'easing bias' at the June meeting, but ultimately decided not to make a move, since stronger economic conditions had not resulted in higher inflation. At the same time, minutes were cautious in tone, noting that 'it was necessary to avoid signals that could trigger a premature tightening of financial conditions'. ECB chief economist Peter Praet reiterated the bank’s stance at a conference in Paris last week. Praet noted that eurozone economic growth is accelerating, but said that the ECB still needs to provide a 'steady hand' in order to spur stubbornly low inflation levels. The ECB holds its next policy meeting on July 20. In June, the bank removed an easing bias towards lowering interest rates. However, policymakers may now be wary about sending more signals of tightening policy, so as to avoid another run on the euro, as was the case after Draghi’s comments at the ECB forum. The ECB doesn’t want the rate statement to shake up markets, so we could see an innocuous statement, to the effect that the economy is headed in the right direction, but QE will remain in place until inflation levels move higher.

Market Update – European Session: European Equities Continues Momentum Higher Following Strong US Payroll Report

Notes/Observations

European Equities trade higher seeing follow through from positive payrolls data out of the US on Friday

G20 Meeting over the weekend look to steps to reduce global overcapacity of steel

Overnight

Asia:

Japan govt cut its assessment of machinery orders for the first time since September 2016after May orders fell 3.6% m/m and only rose 0.6% y/y

PM Abe is looking to reshuffle his cabinet after according to Yomiuri poll Japan PM Abe approval rating fell to 36% from 49% in June (lowest reading since being in office)

China CPI falls slightly m/m, whilst PPI was in line with views

Cosco Shipping confirmed it will acquire Orient Overseas for HK$78.67/shr in a HK$49.2B deal.

Europe:

G20 Meeting in Hamburg over the weekend reiterated to fight protectionism and secure free trade. New elements include to agree by November steps to reduce global overcapacity of steel and in a first ever dissent: 19 members affirmed the Paris accord with the US (dissenter) saying it will help other countries "access and use fossil fuels more cleanly and efficiently.

German trade surplus rises in May following strong exports

EuroZone Sentix investor confidence dipped slightly from the prior month but came ahead of expectations

ECB 's Praet over the weekend noted Eurozone inflation will take a long time to rise back to target, with the reflation process being a long one.

Economic Data

(DE) GERMANY MAY CURRENT ACCOUNT: €17.3B V €15.4BE; TRADE BALANCE: €22.0B V €18.7BE

(FR) BANK OF FRANCE MAY BUSINESS SENTIMENT: 103 V 106E

(EU) EURO ZONE JULY SENTIX INVESTOR CONFIDENCE: 28.3 V 28.1E

(NO) NORWAY JUN CPI M/M: 0.4% V 0.2%E; Y/Y: 1.9% V 1.7%E

Fixed Income Issuance:

Non seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATU

Equities

Indices [Stoxx50 +0.4% at 3,475, FTSE +0.3% at 7,374, DAX +0.6% at 12,464, CAC-40 +0.2% at 5,158, IBEX-35 -0.3% at 10,460, FTSE MIB +0.6% at 21,147, SMI +0.7% at 8,944, S&P futures +0.1%]

Market Focal Points/Key Themes: European markets opened higher and continued to remain positive as trading progressed; exception was Spain, being dragged down by Almirall, reportedly Congress to look into Popular Bank case; risk sentiment improved after major risk events of the weekend are over; consumer discretionary sector lead gains; energy stocks weighed on by weakness in oil prices; potential merger of Chinese container companies impacted shipping and port companies, as analyst see deal supportive of shipping prices, but negative to port administrators

Equities

Consumer discretionary [Air France AF.FR +0.9% (traffic), Remy Cointreau RCO.FR -0.6% (analyst action)]

Consumer staples [CHR Hansen CHR.DK +0.6% (analyst action)]

Energy [Norsk Hydro NHY.NO +0.5% (acquisition)]

Healthcare [Almirall ALM.ES -25.4% (cuts outlook), Stada Arzneimittel SAZ.DE +1.4% (raised offer), Cellnovo CLNV.FR +2.1% (financing agreement)]

Industrials [Orkla ORK.NO +2.4% (divestment), Carillion CLLN.UK -32.1% (cuts outlook)]

Speakers

(UK) UK PM May's Deputy Green: Confident can get repeal bill through parliament

Currencies

GBPUSD resumes its downtrend after a spate of weaker data last week with the pair dropping to a 10 day low. Dealers not immediate support at 1.2860 with a break targets support at 1.2840-50.

EURUSD remains above 1.14, with option barriers noted at 1.14 and 1.1450. Trading remains in a holding pattern, EURJPY has pared early gains but remains above 130.10 with upside tarts at 130.29 followed by 130.71.

Fixed Income

Bund futures trade at 160.82 up 29 ticks as volumes spike after taking out Friday’s high of 160.73. Resistance lies near the 161.50 level followed by 162.10. A break of the 160.00 support level could see lows target 159.25 followed by 157.50.

Gilt futures trade at 125.25 higher by 11 ticks following the move with Bunds and Treasuries. The focus this week is on the syndication of 0.125% 2056 gilt linker on Tuesday. Price finds key support at the 124.42 support level. An acceleration lower could test the 122.88 region. Resistance remains the noted 126.00 region, followed by 126.72.

Monday’s liquidity report showed Friday’s excess liquidity rose to €1.6646T a gain of €0.6B from €1.664T prior. Use of the marginal lending facility fell to €148M from €187M prior.

Corporate issuance saw $5.75B issued last week in a shortened holiday week. Next week’s forecast is $15-20B

Looking Ahead

15:00 (US) May Consumer Credit: No est v $8.2B prior

16:00 (US) Weekly Crop Progress Report

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EUR/USD pair closed the week marginally lower around 1.1400, as the dollar got help from a mixed US employment report that anyway is not enough to change the ongoing negative sentiment towards the American currency, as poor wages' growth keeps casting doubts over Fed's ability to keep on raising rates. The ECB account of the latest policy meeting, on the other hand, gave the common currency a boost on Thursday, as policy makers discussed the possibility of dropping the pledge to expand their bond-purchase programme if necessary, with the market seeing that as a step forward in the tightening path. The central bank finally decide to maintain it, waiting for higher inflation.

As for US employment data released on Friday, the economy added 222,000 new jobs in June, surpassing expectations, although the unemployment rate ticked higher, to 4.4% from previous 4.3%, whilst wages grew below market's expectations, up just by 0.2% in the month. The upcoming week will be quite busy in the data front, with inflation in the US topping the list of market movers for the pair.

Technically, the daily chart shows that the pair topped around 1.1440 for a second consecutive week, whilst technical indicators have begun easing from oversold levels, but are far from confirming an upcoming reversal, moreover as the price remains well above all of its moving averages, which continue heading north. The short term picture is quite alike with indicators pulling back modestly within positive territory, but the price above bullish moving averages. Declines will remain corrective as long as buying interest defends the 1.1290 region, the neckline of the mentioned double top figure. To the upside, a long term resistance stands at 1.1460, with large stops probably gathering above it.

Support levels: 1.1380 1.1340 1.1290

Resistance levels: 1.1460 1.1490 1.1525

USD/JPY

The USD/JPY pair's advance extended to 114.17 last week, its highest since May 11th, with the pair up for a fourth consecutive week. Dollar gains were backed by surging yields worldwide, on fresh signals that central banks' are moving away from ease-oriented monetary policies. On Thursday, the German bund 10-year yield rose to its highest in 18 months, after the ECB unveiled that discussed removing the easing bias from their statement in their latest meeting. In the US, the 10-year note benchmark rose to 2.39%, its highest in two months. Over the weekend, news hit the wires that the BOJ will cut its inflation forecast, while maintaining the current stimulus in their upcoming meeting, according to "people familiar with the matter." The news can see the JPY regaining ground this Monday, particularly as demand for the USD remains limited. From a technical point of view, the daily chart shows that the positive stance persists, as the price has extended its advance beyond a bullish 200 DMA, although the 100 DMA keeps heading south below the largest. In the same chart, technical indicators head north near overbought levels. Shorter term, and according to the 4 hours chart, the technical outlook is also positive, with the RSI indicator consolidating near 64 and the Momentum heading higher, but below previous highs. The pair has a strong static resistance around 114.40, with a break above it signaling further gains ahead.

Support levels: 113.50 113.10 112.65

Resistance levels: 114.05 114.40 114.75

GBP/USD

The Pound edged lower against all of its major rivals on Friday, as worse-than-expected industrial and manufacturing production figures for May point to weaker growth of the UK economy, with the first down 0.1% and the second 0.2%, while construction output also fell in the month, and the trade balance's deficit widened more than expected, to £3.796B. The numbers cooled down expectations of a tighter monetary policy, resulting in the GBP/USD pair breaking below the 1.2900 level. US mixed employment data had little effect on the pair, but prevent it from recovering ground. The pair has an immediate support at 1.2860, the 38.2% retracement of the 1.2588/1.3029 rally from late June, with technical indicators heading lower within bearish territory, and the 20 DMA heading north below the mentioned Fibonacci support. Overall, the downward move remains corrective, albeit below the mentioned static support, the pair has room to extend its decline down towards 1.2750, the 61.8% retracement of the same rally. In the 4 hours chart, the scale leans towards the downside, as the 20 SMA gains bearish strength above the current level, while technical indicators hold within bearish territory, with limited directional strength.

Support levels: 1.2860 1.2820 1.2785

Resistance levels: 1.2925 1.2960 1.3000

GOLD

Gold prices fell further on Friday, with spot ending the week at $1,212.15, its lowest settlement in four months, following a mixed US employment report. A strong jobs' creation was balanced with poor wages' growth, not enough to deviate the Fed's from its tightening path, albeit uncertainty remains strong on the case. US inflation data, to be released this week, can shed some light over the matter and determinate gold's trend. Also, denting sentiment towards the commodity is the latest flip in central banks' stance, now inclined to tighten their monetary policies. The technical picture for the safe-haven is bearish according to the daily chart, with the price having extended its decline below the 200 DMA and indicators heading south near oversold readings. Shorter term, the 4 hours chart shows that a bearish 20 SMA keeps capping the upside, currently at 1,222.10, while the RSI indicator has managed to correct partially oversold readings, while the Momentum indicator lost upward strength well below its mid-line.

Support levels: 1,207.24 1,198.20 1,189.90

Resistance levels: 1,222.10 1,228.00 1,236.50

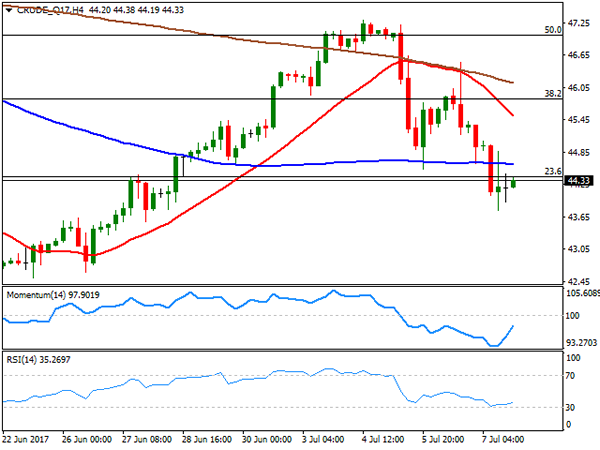

WTI CRUDE OIL

Crude oil prices closed the week in the red, with West Texas Intermediate futures down to $44.33 a barrel, shedding roughly 3% this past week, amid persistent fears of a global glut, and news that Russia is not willing to back further OPEC's output cuts. US government data released last Thursday showed that, despite crude oil stockpiles fell by 6.3 million, oil production rose on1.0% to 9.34 million barrels per day. Additionally, the Baker Hughes report released on Friday showed that the number of US active rigs drilling for oil rose by 7 to 763 last week. The daily chart for WTI shows that the price settled below its 20 SMA, and around the 23.6% retracement of its latest bearish run, after correcting half of the decline in the previous week, increasing chances of a downward extension. In the same chart, the Momentum indicator holds flat within positive territory, but the RSI indicator also supports a downward move by heading south around 41. In the 4 hours chart, the price settled below all of its moving averages, while technical indicators bounced from oversold levels, heading higher within positive territory, not enough to support a recovery.

Support levels: 43.70 43.10 42.60

Resistance levels: 44.80 45.50 46.10

DJIA

US indexes surged on Friday, ending the week with gains, helped the employment report released on Friday, indicating strong jobs' creation in June, and despite soft wages arise doubts over upcoming rate hikes. The Dow Jones Industrial Average added 94 points, to settle at 21,414.34, while the Nasdaq Composite gained 63 points, to 6,153.08. The S&P closed at 2,425.18, up 0.64%. Within the Dow, Goldman Sachs led decliners with a 0.62% loss, followed by General Electric that shed 0.61% and Chevron, this last hit by oil's decline. McDonald's led advancers, up 2.08%, followed by Nike that gained 1.43%. The daily chart for the DJIA shows that the index closed right around its 20 DMA, unable to recover above it, but far above the larger ones, whilst technical indicators turned higher within neutral territory. In the 4 hours chart, the advance was contained by the 20 and 100 SMAs, both converging around 21,420, whilst technical indicators recovered from oversold readings, but lost upward momentum below their mid-lines, limiting chances of a stronger advance in the short term.

Support levels: 21,366 21,305 21,278

Resistance levels: 21,420 21,459 21,515

FTSE100

The FTSE 100 found support in a weaker Pound last Friday, ending the day up 13 points or 0.19%, at 7,350.92. The mining sector edged lower on gold and silver weakness, with Fresnillo and Randgold Resources shedding over 1.0% each. EasyJet was the best performer, up 5.35%, followed by Centrica that added 2.87% on rumors of a takeover of the company. Royal mail led decliners, ending the day down 3.35%, while ITV shed 2.91%. The index remains biased lower according to technical readings, as in the daily chart, the recovery stalled below the 100 DMA while the 20 SMA extended its downward move above the largest. Indicators in the mentioned chart remain within negative territory with little directional strength. In the 4 hours chart, technical indicators have turned horizontal below their mid--lines, while the index settled a few points above a bullish 20 SMA, yet below the 100 and 200 SMAs, indicating limited buying interest.

Support levels: 7,327 7,294 7,256

Resistance levels: 7,372 7,424 7,452

DAX

European equities closed mostly lower on Friday, as persistent weakness in oil prices weighed, although the German DAX managed to close the day at 12,388.68, up by 7 points. Speculation that the easing monetary policy is getting closer to an end, undermined investors' confidence despite the economic recovery, indicating that stocks may remain under pressure this week. Within the German benchmark, ProSiebenSat.1 led decliners for a second consecutive session, down 1.29%, and followed by Commerzbank that shed 0.52%. RWE AG was the best performer, up 3.72%, followed by E.ON that added 2.55%. The index has held once again above a bullish 100 DMA in the daily chart, but remains nearby, and with technical indicators holding near oversold readings, which increase the risk of further declines ahead. In the 4 hours chart, the latest recovery was contained by a now flat 20 SMA, with the index holding around it, while technical indicators consolidate below their mid-lines, limiting chances of a steeper recovery. The index bottomed at 12,310 this past week, the level to break to confirm a new leg lower.

Support levels: 12,366 12,310 12,272

Resistance levels: 12,445 12,490 12,536