Sample Category Title

Eco Data 7/15/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machinery Orders M/M May | -12.40% | -4.20% | 8.70% | |

| 02:00 | CNY | Industrial Production Y/Y Jun | 5.30% | 4.70% | 4.50% | |

| 02:00 | CNY | Retail Sales Y/Y Jun | 1.00% | -0.10% | -0.60% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | -5.70% | -4.90% | -4.10% | |

| 02:00 | CNY | GDP Q/Q Q2 | 0.90% | 0.90% | 1.30% | |

| 02:00 | CNY | GDP Y/Y Q2 | 4.30% | 4.50% | 5.00% | |

| 04:30 | JPY | Tertiary Industry Index M/M May | 1.10% | 0.40% | 1.30% | 0.80% |

| 09:00 | EUR | Eurozone Industrial Production M/M May | -0.20% | 0.30% | 0.10% | 0.30% |

| 12:30 | CAD | Manufacturing Sales M/M May | 1.30% | 1.10% | 4.20% | |

| 12:30 | CAD | Wholesale Sales M/M May | 0.00% | -0.70% | 0.60% | |

| 12:30 | USD | Empire State Manufacturing Jul | 15.6 | 9.3 | 5.7 | |

| 12:30 | USD | PPI M/M Jun | -0.30% | 0.20% | 1.10% | 0.60% |

| 12:30 | USD | PPI Y/Y Jun | 5.50% | 6.20% | 6.50% | 6.00% |

| 13:45 | CAD | BoC Interest Rate Decision | 2.25% | 2.25% | 2.25% | |

| 14:30 | CAD | BoC Press Conference | ||||

| 14:30 | USD | Crude Oil Inventories (Jul 10) | -1.7M | -1.8M | 3.0M | |

| 18:00 | USD | Fed's Beige Book |

| 23:50 | JPY |

| Machinery Orders M/M May | |

| Actual | -12.40% |

| Consensus | -4.20% |

| Previous | 8.70% |

| 02:00 | CNY |

| Industrial Production Y/Y Jun | |

| Actual | 5.30% |

| Consensus | 4.70% |

| Previous | 4.50% |

| 02:00 | CNY |

| Retail Sales Y/Y Jun | |

| Actual | 1.00% |

| Consensus | -0.10% |

| Previous | -0.60% |

| 02:00 | CNY |

| Fixed Asset Investment YTD Y/Y Jun | |

| Actual | -5.70% |

| Consensus | -4.90% |

| Previous | -4.10% |

| 02:00 | CNY |

| GDP Q/Q Q2 | |

| Actual | 0.90% |

| Consensus | 0.90% |

| Previous | 1.30% |

| 02:00 | CNY |

| GDP Y/Y Q2 | |

| Actual | 4.30% |

| Consensus | 4.50% |

| Previous | 5.00% |

| 04:30 | JPY |

| Tertiary Industry Index M/M May | |

| Actual | 1.10% |

| Consensus | 0.40% |

| Previous | 1.30% |

| Revised | 0.80% |

| 09:00 | EUR |

| Eurozone Industrial Production M/M May | |

| Actual | -0.20% |

| Consensus | 0.30% |

| Previous | 0.10% |

| Revised | 0.30% |

| 12:30 | CAD |

| Manufacturing Sales M/M May | |

| Actual | 1.30% |

| Consensus | 1.10% |

| Previous | 4.20% |

| 12:30 | CAD |

| Wholesale Sales M/M May | |

| Actual | 0.00% |

| Consensus | -0.70% |

| Previous | 0.60% |

| 12:30 | USD |

| Empire State Manufacturing Jul | |

| Actual | 15.6 |

| Consensus | 9.3 |

| Previous | 5.7 |

| 12:30 | USD |

| PPI M/M Jun | |

| Actual | -0.30% |

| Consensus | 0.20% |

| Previous | 1.10% |

| Revised | 0.60% |

| 12:30 | USD |

| PPI Y/Y Jun | |

| Actual | 5.50% |

| Consensus | 6.20% |

| Previous | 6.50% |

| Revised | 6.00% |

| 13:45 | CAD |

| BoC Interest Rate Decision | |

| Actual | 2.25% |

| Consensus | 2.25% |

| Previous | 2.25% |

| 14:30 | CAD |

| BoC Press Conference | |

| Actual | |

| Consensus | |

| Previous | |

| 14:30 | USD |

| Crude Oil Inventories (Jul 10) | |

| Actual | -1.7M |

| Consensus | -1.8M |

| Previous | 3.0M |

| 18:00 | USD |

| Fed's Beige Book | |

| Actual | |

| Consensus | |

| Previous | |

Fed’s Warsh: ‘No Tolerance’ for High Inflation, but Avoids Policy Signals

Federal Reserve Chair Kevin Warsh reiterated his commitment to restoring price stability in his first semiannual testimony before Congress, but stopped well short of offering any clues on the near-term interest rate outlook. Speaking just hours after June CPI came in much softer than expected, Warsh repeated that the Fed's "number one objective is to get monetary policy right" and pledged that "if we get policy right — and we will — the inflation surge of the last five years will be a thing of the past." The testimony reinforced his long-term policy philosophy rather than altering market expectations, with investors finding little to challenge the softer inflation narrative established earlier in the day.

Warsh maintained a firm stance on inflation throughout his prepared remarks. He stressed that policymakers have "no tolerance for persistently elevated inflation" and share "a resolute commitment to restoring price stability." At the same time, he avoided endorsing recent speculation about another near-term rate hike despite renewed geopolitical tensions and higher oil prices. Instead, he argued that while "monthly price fluctuations are inevitable — especially in an unsettled world," inflation over longer horizons is "determined largely by monetary policy." The combination of softer CPI and Warsh's refusal to signal a policy path leaves the Federal Reserve with greater flexibility to assess whether the latest rise in energy prices develops into broader inflation.

Beyond the immediate policy outlook, Warsh continued to outline what he described as "a new chapter at the Federal Reserve." He again criticized the central bank's 2020 average inflation targeting framework, calling it "a mistake" that sought "a little more inflation and end[ed] up with a lot more." He also highlighted accelerating business investment, particularly in artificial intelligence, describing it as "the most striking feature" of today's economy and suggesting that what is now known as AI investment "will soon be called just investment." Overall, the testimony was notable less for new policy signals than for confirming Warsh's preference to avoid forward guidance while emphasizing credibility, institutional reform and a disciplined commitment to defeating inflation.

Sunset Market Commentary

Markets

Oil captured most of the market attention in the run-up to the US June CPI and Fed chair Warsh's semiannual testimony before Congress. The NACHO trade pushed Brent towards an intraday high of $87.55, the most since mid-June. At a current price of +/- $86, one barrel is trading at an important technical and symbolical level, ie. the April-low that followed after US president Trump backtracked from Iran's total obliteration to announce the first ceasefire. With the most recent one bombed to smithereens and the US blockade reimposed, oil prices can be expected to gravitate back to levels between $90 and $110. If Trump is serious about collecting a 20% security-servicing fee on cargo that passes through the Hormuz Strait, prices may in theory be even higher. Other energy commodities rally in lockstep with gas prices testing the highest levels since early April (Dutch TTF) and European gasoline and diesel (affected additionally by the Ukraine-stricken Russian refineries) prices adding multiple percentage points as well. US bonds took a hit already yesterday and are licking their wounds today with yields more or less steadying going into the CPI release. German and UK bonds immediately gapped lower at the open with the latter underperforming. Germany's 2-yr yield fell just short of June's two-year high and traded 6.5 bps higher on the day. Longer maturities added between 1 and 2.5 bps. It's a relative outperformance of the long end though since those yields are already trading close to 15-year highs. UK rates added 3-4.5 bps across the curve. The US dollar failed to capitalize on the risk averse market environment. It is losing out modestly against all G10 peers.

US CPI missed the bar with headline inflation dropping by 0.4% m/m to 3.5% y/y (from 4.2%). A key reason, though, may soon prove temporary: energy prices slumped 5.7% m/m, led by the likes of gasoline (-9.7% m/m). That said, core inflation also printed lower than expected, with prices stagnating on a monthly basis and 2.6% higher y/y (from 2.9%). Both headline and core services inflation was flat while the likes of shelter (0.1% m/m), used cars (-0.2%), medical care (-0.1%) and apparel (-0.6%, a tariff gauge) amongst others weighed on the index too. The underlying gauge gained in importance after Fed Waller's earlier comments. Printing higher than 0.2% m/m would have created a significant risk for near-term (ie. July) tightening. Markets are now paring the odds from +/- 40% to just 14% currently while still assuming at least one move at a later meeting this year. US rates yanked up to 10 bps lower at the front end while dropping 2-5.5 bps in the 10-30 yr bucket. That capped some of the yield increases on other core bonds too. Stocks bounced and the dollar extended losses. EUR/USD rises towards 1.145 and DXY falls towards 100.7. Moves remain technically insignificant. The US CPI is a gift for Warsh. A hot print would have increased the heat at today's grilling before Congress with questions that press him into a timing for a rate hike. Now, he can be more close-mouthed and strike the same hawkish but little-telling chord he had done so far. His prepared remarks reveal nothing about his preference on rates either. Warsh doubled down on his earlier message to restore price stability by saying the Fed has no tolerance for persistently elevated inflation. He'll repeat that the Fed will get policy right without explaining what it actually means. Warsh called the economy resilient and growing at a solid pace while considering the labour market broadly stable.

News & Views

The small business economic trends index of the US National Federation of Independent Businesses for June rose more than expected to 97.4 from 95.3 in May, the best levels since February and nearing the LT average of 98. The rise was primarily driven by expectations for better business conditions and higher real sales expectations. The uncertainty index decreased from 91 to a still above-average of 89. The net percentage of firms expecting a better economy improved from 3% to 13%. Labour market indicators were mixed. 32% of small business owners reported job openings they could not fill in June, up 3 points from May, but still the lowest since May 2020. 21% (+ 3 pts) of business owners cited inflation as their single most important business problem, the highest reading since October 2024. The net percent of owners raising selling prices rose 2% to a net 38%, the fourth consecutive month that actual price increases have risen, marking the highest level since January 2023. A net 32% plan to increase prices in the next three months, down 2% from May's highest reading since July 2022. As the survey was conducted during June, it evidently doesn't capture the recent rebound in oil prices.

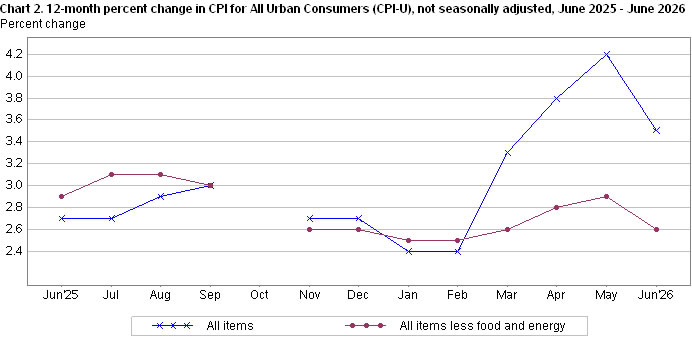

US: Inflation Cools More Than Expected in June on Broad-Based Softness

- The Consumer Price Index (CPI) fell 0.4% month-on-month (m/m) in June – the largest one-month decline since April 2020 and larger than consensus expectations. On a twelve-month basis, CPI stepped down to 3.5% (from 4.2% in May).

- The 5.7% m/m drop in energy costs was the main driver of the decline in CPI in June. Food prices rose 0.2% m/m and are up 3.0% on a twelve-month basis.

- Excluding food and energy, core prices were unchanged in June, also below expectations for a 0.2% m/m gain. On a twelve-month basis, core prices were up 2.6% —down from 2.9% in May and the slowest pace since before the U.S. -Iran conflict.

- Core goods prices fell 0.1% m/m for the second consecutive month. Prices fell for apparel (-0.6% m/m), medical goods (-0.2% m/m) and used vehicles (-0.2% m/m). On a twelve-month basis, core goods prices are up 0.8%, the slowest pace since June 2025.

- The bigger surprise was core services prices, which were flat on the month but are still up 3.2% y/y. Shelter costs rose just 0.1% m/m after a string of hotter readings. Vehicle insurance (-2.0% m/m), communication (-1.5% m/m) and medical care (-0.1% m/m) all contributed to the softness in services.

Key Implications

- Headline inflation took a larger step in the right direction in June than expected, and it wasn't all due to the monthly drop in global crude oil prices. The cooler core reading was also welcome, though we would be cautious about extrapolating one month of data, especially since crude has retraced much of its June drop.

- The next FOMC meeting is in a couple of weeks, and the June inflation data should help to quiet some of the more hawkish voices. The 2-Year Treasury yield is down about six basis points since the release, and market pricing for Fed hikes this year has also eased. Markets are also likely to key off Chair Warsh's testimony before the House Financial Services Committee at 10:00 a.m. today.

US: Small Business Optimism Rebounds in June as Growth Expectations Improve

- The NFIB's Small Business Optimism Index rose 2.1 points to 97.4 in June, moving closer to its 52-year average of 98.0. The Uncertainty Index fell 2 points to 89, although it remains elevated relative to historical norms, underscoring that the improvement in sentiment has not fully translated into a more predictable operating environment.

- Seven of the ten Optimism Index components improved during the month. The largest gains came from expectations for better business conditions, which rose 10 points to 13%, and expectations for higher real sales volumes, which increased 8 points to 9%. Hiring plans, job openings, and inventory assessments also improved, while planned capital outlays rose to 20%, the highest reading of the year. Offsetting these gains were weaker earnings trends, reduced plans to build inventories, and slightly more pessimistic views on future credit conditions.

- Labor market indicators recovered modestly following May's weakness. The share of firms reporting hard-to-fill job openings rose 3 points to 32%, while the net share planning to increase employment climbed 2 points to 11%. However, labour quality remains a constraint: 51% of firms hiring or trying to hire reported few or no qualified applicants, the highest share since September 2024, and 19% cited labour quality or availability as their single most important problem. Despite the improvement, hiring activity remains relatively subdued compared to levels seen through much of last year.

- Inflation pressures remain a key concern for small businesses. The net share of firms raising average selling prices increased 2 points to 38%, the highest reading since early 2023 and the fourth consecutive monthly increase. Inflation was cited as the most important business problem by 21% of owners, up 3 points from May. Encouragingly, the share of firms planning to raise prices over the next three months declined slightly to 32%, suggesting some easing in forward-looking price pressure.

Key Implications

- June's report points to a meaningful improvement in small business sentiment, driven largely by stronger expectations for business conditions and sales. The rebound suggests that concerns about the economic outlook have eased somewhat, supported by lower energy costs and a decline in uncertainty. However, optimism remains below its long-run average and firms continue to report caution around hiring and investment decisions, even as capital spending intentions improved from very weak levels.

- Despite the stronger headline reading, underlying conditions remain mixed. Labor demand improved but remains moderate, earnings trends deteriorated further, and inflation has re-emerged as the top business concern. The labour backdrop also looks more supply-constrained than demand-driven, with firms reporting fewer qualified applicants even as compensation pressures cooled. While softer price-setting intentions offer some hope that inflation pressures may ease over coming months, elevated borrowing costs and persistent cost pressures are likely to remain headwinds for small business activity through the second half of the year.

Soft CPI Overpowers Oil Shock as Dollar Retreats and Fed Gets Breathing Room

Dollar fell broadly in early trading after June CPI delivered a much larger-than-expected downside surprise, shifting market attention away from escalating geopolitical risks and back toward a more benign inflation outlook. Headline CPI fell -0.4% on the month while core CPI was unchanged, both undershooting expectations and challenging the aggressive repricing toward additional Federal Reserve tightening that had gathered pace over the past week. The softer inflation data also reduced the immediate significance of Fed Chair Kevin Warsh's first semiannual congressional testimony, giving policymakers greater flexibility to remain patient despite renewed strength in oil prices.

The inflation report arrived against a dramatically different geopolitical backdrop. Brent crude climbed above $87 after fighting between the United States and Iran intensified again. Iran launched ballistic missiles at a US air base in Jordan, while US forces carried out another extended wave of strikes against Iranian targets as both sides continued battling for control of the Strait of Hormuz. The renewed hostilities have further undermined confidence that last month's memorandum of understanding guaranteeing shipping through the Strait will evolve into a lasting peace agreement, keeping energy markets on edge and reinforcing concerns that higher oil prices could eventually feed back into global inflation.

Yet markets drew a distinction between today's inflation and tomorrow's inflation risks. June's CPI reflected the earlier decline in energy prices, with the energy component recording its largest monthly fall since April 2020, while shelter inflation slowed to its weakest monthly increase since January 2021. Those developments suggested underlying price pressures continued to moderate before the latest rebound in crude prices. Although the renewed surge in oil still poses an upside risk to future inflation, investors concluded the Fed now has more time to assess whether higher energy costs become embedded in broader price pressures before responding with additional tightening.

That shift substantially lowers the stakes surrounding Warsh's congressional appearance. Having repeatedly argued against providing explicit forward guidance, the new Fed Chair now has greater room to maintain that communication strategy. Rather than facing pressure to signal an imminent rate increase following Governor Christopher Waller's hawkish remarks on Monday, Warsh can point to softer inflation while emphasizing that policy will continue to depend on incoming data. Unless lawmakers force a more explicit discussion of future rate moves, the testimony is increasingly likely to produce few meaningful policy surprises.

Currency markets reflected the improved risk backdrop despite escalating tensions in the Middle East. For the week so far, New Zealand Dollar remained the strongest performer after hawkish comments from RBNZ Chief Economist Paul Conway reinforced expectations of additional policy tightening. Canadian Dollar benefited from higher oil prices, while Euro also traded firmly. By contrast, Dollar joined Yen and Swiss Franc among the week's weakest performers, suggesting investors were responding more to easing Fed expectations than to geopolitical headlines. Sterling and Australian Dollar traded in the middle of the performance rankings as markets balanced softer US inflation against persistent uncertainty over the global energy outlook.

US CPI Misses Forecasts at 3.5%, Core Inflation at 2.6%

US inflation slowed much more than expected in June, with headline CPI falling -0.4% on the month and core CPI unexpectedly flat. The sharp decline was driven by a 5.7% drop in energy prices, the largest monthly fall since April 2020, while shelter inflation also recorded its smallest monthly increase since January 2021. The softer data challenge recent Fed tightening expectations ahead of Fed Chair Kevin Warsh's congressional testimony. Read More.

AUD/NZD Tests Double Top Breakdown as RBNZ's Conway Revives Faster Tightening Bets

Paul Conway's latest speech suggests the RBNZ's inflation assumptions are already being challenged by the rebound in oil prices. He warned that New Zealand businesses now pass through higher costs more readily and are less likely to cut prices when costs ease, increasing the risk that temporary supply shocks become persistent inflation requiring a firmer monetary policy response. Read More.

Gold Slides as Oil Surges and Fed Hike Bets Build, Leaving $4,000 Increasingly Vulnerable

Gold extended its decline as Brent crude briefly climbed above $85 and markets sharply increased expectations for another Federal Reserve rate hike following hawkish remarks from Governor Christopher Waller. With traders awaiting US CPI and Fed Chair Kevin Warsh's congressional testimony, the psychologically important $4,000 level is looking increasingly vulnerable. A decisive break would shift focus to 3942.23, with the broader bearish trend targeting 3606.49. Read More.

Australia NAB Business Confidence Rebounds to -5 as Inflation Pressures Ease

Australia's NAB Business Survey showed business confidence rebounding sharply in June as fears over the Middle East conflict and energy prices eased. At the same time, purchase cost growth, final product price inflation and retail prices all moderated, suggesting the earlier oil shock had a smaller impact on inflation than feared. Read More.

Australia Westpac Consumer Sentiment Rebounds to 83.9, but Pessimism Still Runs Deep

Australia's Westpac–Melbourne Institute Consumer Sentiment Index rose 4.1% to 83.9 in July after the RBA paused its tightening cycle, easing fears of rapid further rate hikes. However, confidence remains among the weakest in the survey's 50-year history, while persistent inflation keeps attention firmly on the June quarter CPI report ahead of the RBA's August meeting. Read More.

NZIER QSBO Signals Improving Confidence but Sticky Inflation Risks

New Zealand's latest NZIER Quarterly Survey of Business Opinion showed confidence improving sharply in the June quarter as fuel prices eased, with a net 12% of firms expecting better economic conditions. However, hiring and investment intentions remained weak, while more than half of businesses reported rising costs and a growing number passed those increases on to customers, highlighting persistent inflation pressures for the RBNZ. Read More.

China Trade Data Crushes Forecasts as Exports and Imports Accelerate in June

China's trade growth accelerated sharply in June, with exports rising 27.0% and imports climbing 36.0%, both well above expectations. Semiconductor exports more than doubled to USD 38B, while stronger shipments to the US, ASEAN and the EU underscored resilient global demand. The main weak spot was crude oil imports, which fell -41% from a year earlier. Read More.

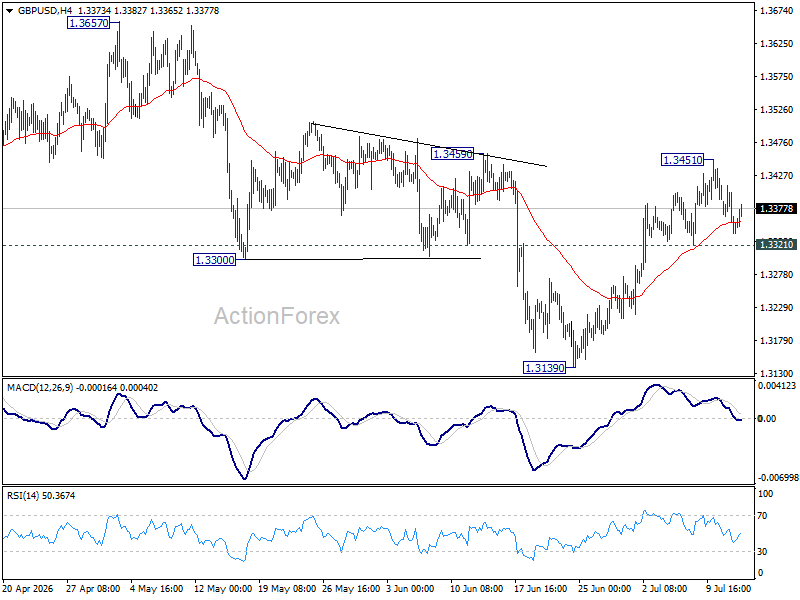

GBP/USD Daily Outlook

Intraday bias in GBP/USD stays neutral for consolidations below 1.3451. On the upside, firm break of 1.3459 will argue that whole correction from 1.3867 has completed, and target 1.3657 resistance for confirmation. On the downside, break of 1.3451 will turn bias back to the downside for 1.3139 support instead.

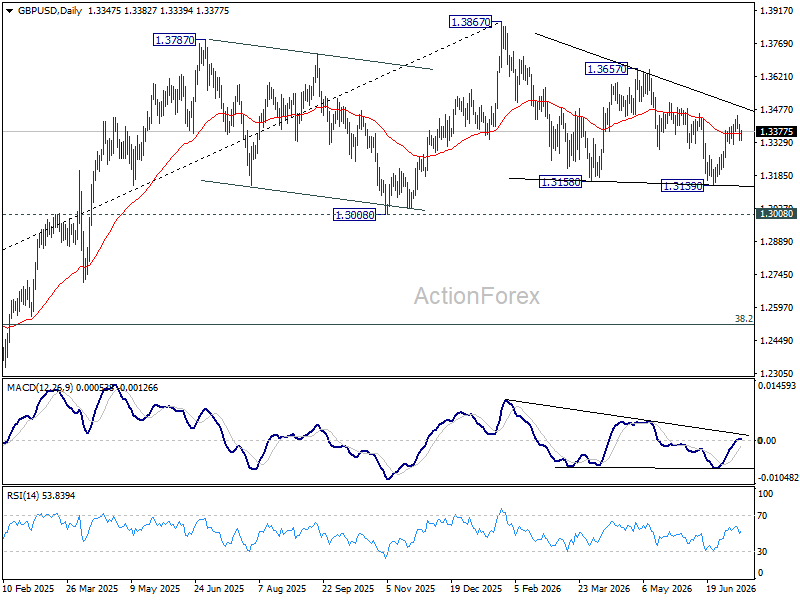

In the bigger picture, price actions from 1.3867 are a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

US CPI Misses Forecasts at 3.5%, Core Inflation at 2.6%

US inflation slowed much more than expected in June, offering the first meaningful challenge to the recent surge in Federal Reserve tightening expectations. Headline CPI fell -0.4% mom, slowing from 0.5% mom in May, while the annual rate eased from 4.2% yoy to 3.5% yoy. Core CPI was unchanged on the month, bringing the annual core rate down from 2.9% yoy to 2.6% yoy. Both headline and core inflation undershot market expectations, suggesting the recent inflation spike may have been more concentrated in energy than previously feared.

The sharp improvement was driven overwhelmingly by energy prices. The energy index fell -5.7% mom after posting consecutive monthly increases of 10.9%, 3.8% and 3.9% over the previous three months, marking the largest monthly decline since April 2020. That more than offset continued increases in shelter and food prices.

Shelter inflation slowed further, rising just 0.1% mom, the smallest monthly increase since January 2021, while food prices increased a modest 0.2% mom. Together, the data suggest underlying inflation pressures continued to moderate once the temporary energy shock began to unwind, despite energy prices still standing 15.7% above their level a year earlier.

Attention now shifts to Fed Chair Kevin Warsh's congressional testimony, where investors will look for clues on whether policymakers view the softer inflation report as sufficient to temper recent rate-hike expectations or continue emphasizing the inflation risks posed by the renewed surge in oil prices.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| CPI (MoM) | -0.4% | -0.1% | 0.5% |

| CPI (YoY) | 3.5% | 3.8% | 4.2% |

| Core CPI (MoM) | 0.0% | 0.2% | 0.2% |

| Core CPI (YoY) | 2.6% | 2.8% | 2.9% |

| Energy Index (MoM) | -5.7% | — | 3.9% |

| Energy Index (YoY) | 15.7% | — | — |

| Food Index (MoM) | 0.2% | — | — |

| Food Index (YoY) | 3.0% | — | — |

| Shelter Index (MoM) | 0.1% | — | — |

| Shelter Index (YoY) | 3.3% | — | — |

Market Takeaways

- Both headline and core CPI undershot expectations, providing the first meaningful downside surprise in several months.

- The sharp fall in energy prices was the dominant driver, with the largest monthly decline in the energy index since April 2020.

- Shelter inflation continued to moderate, posting its smallest monthly increase since January 2021, while core CPI was flat.

- The report suggests inflation pressures were less broad-based than recent hawkish Fed rhetoric implied.

- The data challenge recent market repricing toward additional Fed tightening, although renewed oil price gains could reverse some of June's disinflation in coming months.

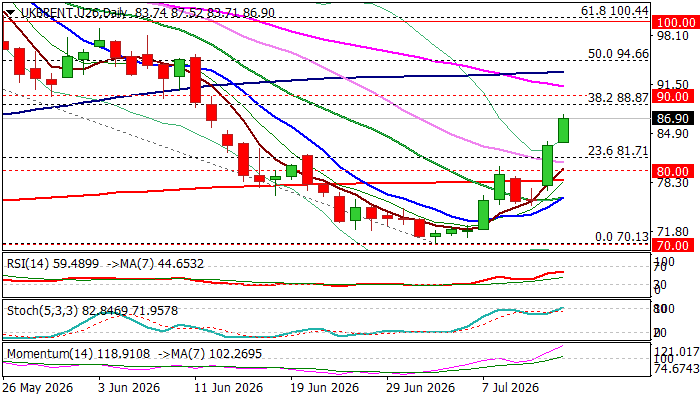

Brent Oil Hit One Month High as Situation in the Middle East Escalates Further

Brent price rallies for the second consecutive day on intensifying hostilities between the US and Iran that resulted in closure of strategic Strait of Hormuz and fueled fears about prolonged supply disruptions that may send fresh shockwaves towards already weakened western economies.

Oil price hit new highs of over one month on Tuesday and so far does not show signs of fatigue, as worsening geopolitical situation continues fueling bulls.

Technical picture on daily chart has also significantly improved as positive momentum strengthens, the price broke and closed above 200DMA ($78.53) and psychological $80 barrier on Monday, with Tuesday’s extension higher pressuring net pivotal barriers at $88.87 (Fibo38.2% of $119.18/$70.13) and psychological $90.

Formation of 5/200DMA golden cross and 10/20DMA bull-cross reinforces near-term structure, as bulls look for break above $88.87/$90 triggers to open way for further advance and validate reversal pattern.

Partial profit taking after strong rally cannot be ruled out in coming session and bulls are likely to face increased headwinds on approach to $90 zone, though dips, under current environment, should be shallow and mark positioning for further advance.

Potential corrective actions should be contained above $82.00 zone to provide better levels for re-entering bullish market.

Res: 88.00; 88.87; 90.00; 91.30

Sup: 85.80; 84.10; 83.70; 82.80

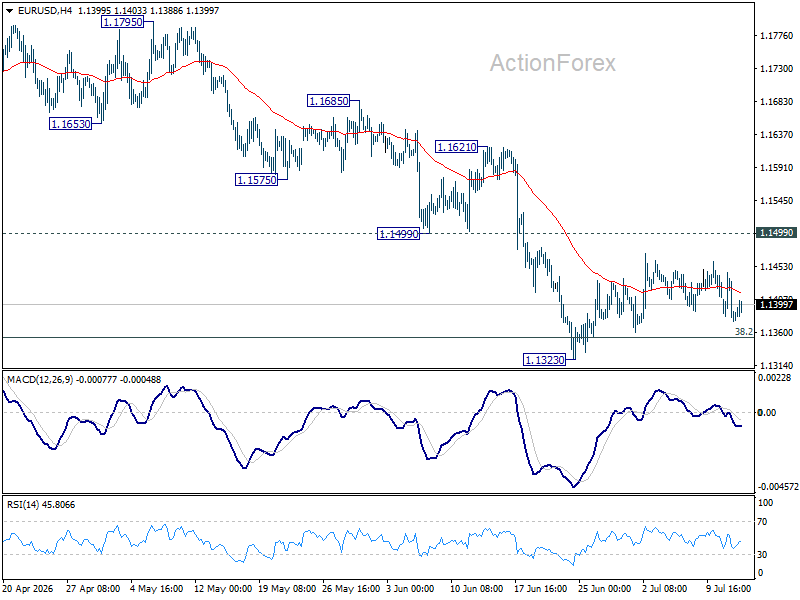

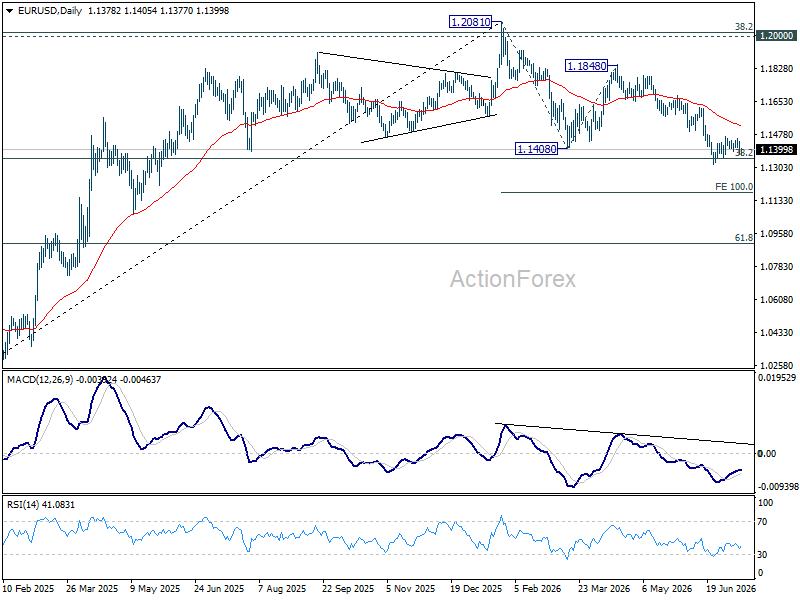

EUR/USD Daily Outlook

EUR/USD is still bounded in consolidations above 1.1323 and intraday bias stays neutral. With 1.1499 support turned resistance intact, further decline is expected. On the downside, break of 1.1323 will resume the fall from 1.2081 to 100% projection of 1.2081 to 1.1408 from 1.1848 at 1.1175. However, decisive break of 1.1499 will turn bias back to the upside for 1.1621 resistance.

In the bigger picture, focus is back on 38.2% retracement of 1.0176 to 1.2081 at 1.1353. Decisive break there will revive the case of medium term bearish trend reversal after rejection by 1.2 key cluster resistance level. Further fall should be seen to 61.8% retracement at 1.0904. Nevertheless, strong rebound from 1.1353, followed by break of 1.1621 resistance, will retain medium term bullishness.

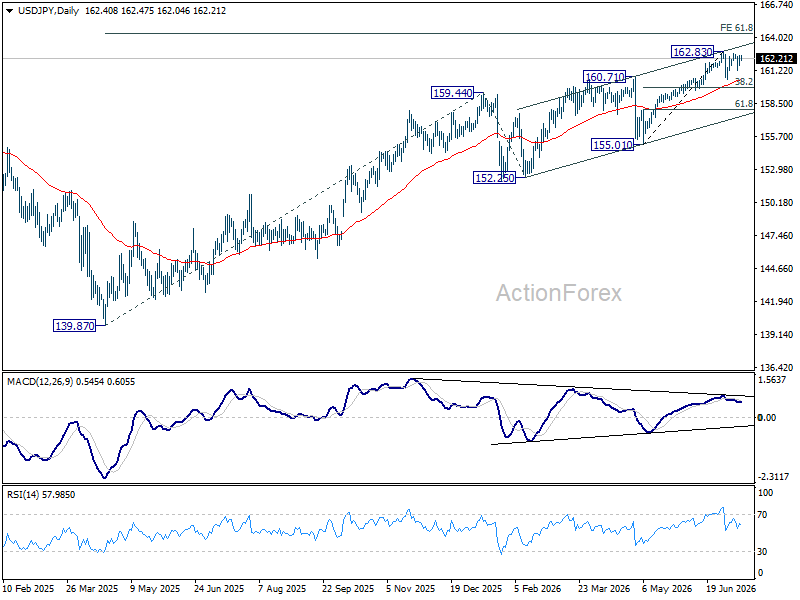

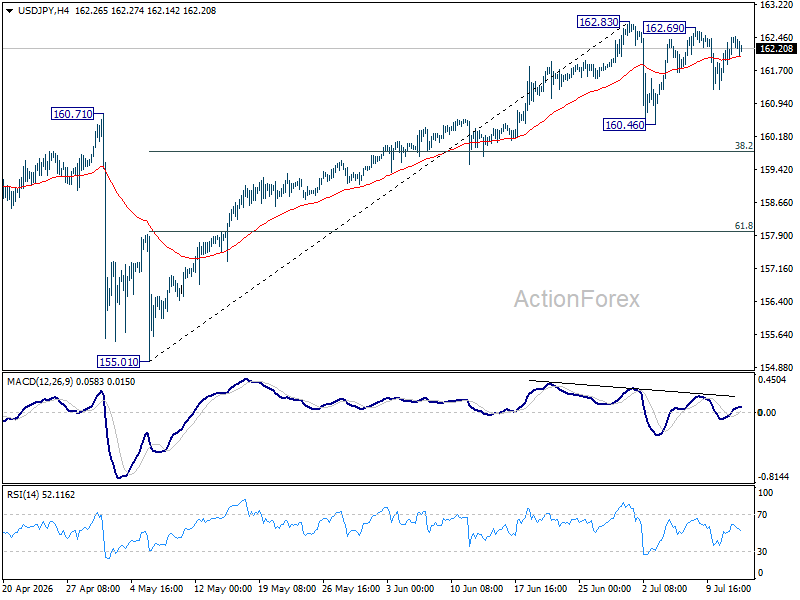

USD/JPY Daily Outlook

Intraday bias in USD/JPY remains neutral as consolidations continue below 162.84. In case of another fall, downside should be contained by 38.2% retracement of 155.01 to 162.83 at 159.84. On the upside, firm break of 162.83 will resume larger up trend.

In the bigger picture, rise from 139.87 (2025 low) is seen as another rising leg of the long term up trend. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. For now, outlook will remain bullish as long as 155.01 support holds, even in case of deep pullback.