Sample Category Title

Summary 12/30 – 1/3

Monday, Dec 30, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Dec F | 49.5 | 49.5 |

| 08:00 | CHF | KOF Economic Barometer Dec | 101.1 | 101.8 |

| 14:45 | USD | Chicago PMI Dec | 42.8 | 40.2 |

| 15:00 | USD | Pending Home Sales M/M Nov | 0.70% | 2.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Dec F | |

| Forecast: 49.5 | Previous: 49.5 | ||

| 08:00 | CHF | KOF Economic Barometer Dec | |

| Forecast: 101.1 | Previous: 101.8 | ||

| 14:45 | USD | Chicago PMI Dec | |

| Forecast: 42.8 | Previous: 40.2 | ||

| 15:00 | USD | Pending Home Sales M/M Nov | |

| Forecast: 0.70% | Previous: 2.00% | ||

Tuesday, Dec 31, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | CNY | NBS Manufacturing PMI Dec | 50.3 | 50.3 |

| 01:30 | CNY | NBS Non-Manufacturing PMI Dec | 50.2 | 50 |

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Oct | 4.10% | 4.60% |

| 14:00 | USD | Housing Price Index M/M Oct | 0.50% | 0.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | CNY | NBS Manufacturing PMI Dec | |

| Forecast: 50.3 | Previous: 50.3 | ||

| 01:30 | CNY | NBS Non-Manufacturing PMI Dec | |

| Forecast: 50.2 | Previous: 50 | ||

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Oct | |

| Forecast: 4.10% | Previous: 4.60% | ||

| 14:00 | USD | Housing Price Index M/M Oct | |

| Forecast: 0.50% | Previous: 0.70% | ||

Wednesday, Jan 1 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| New Year Day |

| GMT | Ccy | Events | |

|---|---|---|---|

| New Year Day | |||

| Forecast: | Previous: | ||

Thursday, Jan 2, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:45 | CNY | Caixin Manufacturing PMI Dec | 51.6 | 51.5 |

| 08:30 | CHF | Manufacturing PMI Dec | 48.3 | 48.5 |

| 08:50 | EUR | France Manufacturing PMI Dec F | 41.9 | 41.9 |

| 08:55 | EUR | Germany Manufacturing PMI Dec F | 42.5 | 42.5 |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec F | 45.2 | 45.2 |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Nov | 3.50% | 3.40% |

| 09:30 | GBP | Manufacturing PMI Dec F | 47.3 | 47.3 |

| 13:30 | USD | Initial Jobless Claims (Dec 27) | 223K | 219K |

| 14:30 | CAD | Manufacturing PMI Dec | 51.9 | 52 |

| 14:45 | USD | S&P Global Manufacturing PMI Dec F | 48.3 | 48.3 |

| 15:00 | USD | Construction Spending M/M Nov | 0.30% | 0.40% |

| 16:00 | USD | Crude Oil Inventories |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:45 | CNY | Caixin Manufacturing PMI Dec | |

| Forecast: 51.6 | Previous: 51.5 | ||

| 08:30 | CHF | Manufacturing PMI Dec | |

| Forecast: 48.3 | Previous: 48.5 | ||

| 08:50 | EUR | France Manufacturing PMI Dec F | |

| Forecast: 41.9 | Previous: 41.9 | ||

| 08:55 | EUR | Germany Manufacturing PMI Dec F | |

| Forecast: 42.5 | Previous: 42.5 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Dec F | |

| Forecast: 45.2 | Previous: 45.2 | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Nov | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 09:30 | GBP | Manufacturing PMI Dec F | |

| Forecast: 47.3 | Previous: 47.3 | ||

| 13:30 | USD | Initial Jobless Claims (Dec 27) | |

| Forecast: 223K | Previous: 219K | ||

| 14:30 | CAD | Manufacturing PMI Dec | |

| Forecast: 51.9 | Previous: 52 | ||

| 14:45 | USD | S&P Global Manufacturing PMI Dec F | |

| Forecast: 48.3 | Previous: 48.3 | ||

| 15:00 | USD | Construction Spending M/M Nov | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 16:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: | ||

Friday, Jan 3, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 08:55 | EUR | Germany Unemployment Rate Dec | 6.20% | 6.10% |

| 08:55 | EUR | Germany Unemployment Change Dec | 15K | 7K |

| 09:30 | GBP | Mortgage Approvals Nov | 69K | 68K |

| 09:30 | GBP | M4 Money Supply M/M Nov | 0.10% | -0.10% |

| 15:00 | USD | ISM Manufacturing PMI Dec | 48.3 | 48.4 |

| 15:00 | USD | ISM Manufacturing Prices Paid Dec | 50.5 | 50.3 |

| 15:00 | USD | ISM Manufacturing Employment Index Dec | 48.1 | |

| 15:30 | USD | Natural Gas Storage | -93B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 08:55 | EUR | Germany Unemployment Rate Dec | |

| Forecast: 6.20% | Previous: 6.10% | ||

| 08:55 | EUR | Germany Unemployment Change Dec | |

| Forecast: 15K | Previous: 7K | ||

| 09:30 | GBP | Mortgage Approvals Nov | |

| Forecast: 69K | Previous: 68K | ||

| 09:30 | GBP | M4 Money Supply M/M Nov | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 15:00 | USD | ISM Manufacturing PMI Dec | |

| Forecast: 48.3 | Previous: 48.4 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Dec | |

| Forecast: 50.5 | Previous: 50.3 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Dec | |

| Forecast: | Previous: 48.1 | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -93B | ||

Markets Weekly Outlook – PMI Data and Increased Liquidity to Drive Markets

- US equities experience volatility amid tech and growth stock fluctuations, ending the Santa Rally week with marginal gains.

- Japanese Yen strengthens due to expected Bank of Japan policy changes, while US Dollar continues its advance.

- Key data releases next week include Chinese PMI data and US manufacturing PMI, with market focus on potential economic recovery signs in China and continued US resilience.

Week in Review: Wall Street Falters After Christmas Break

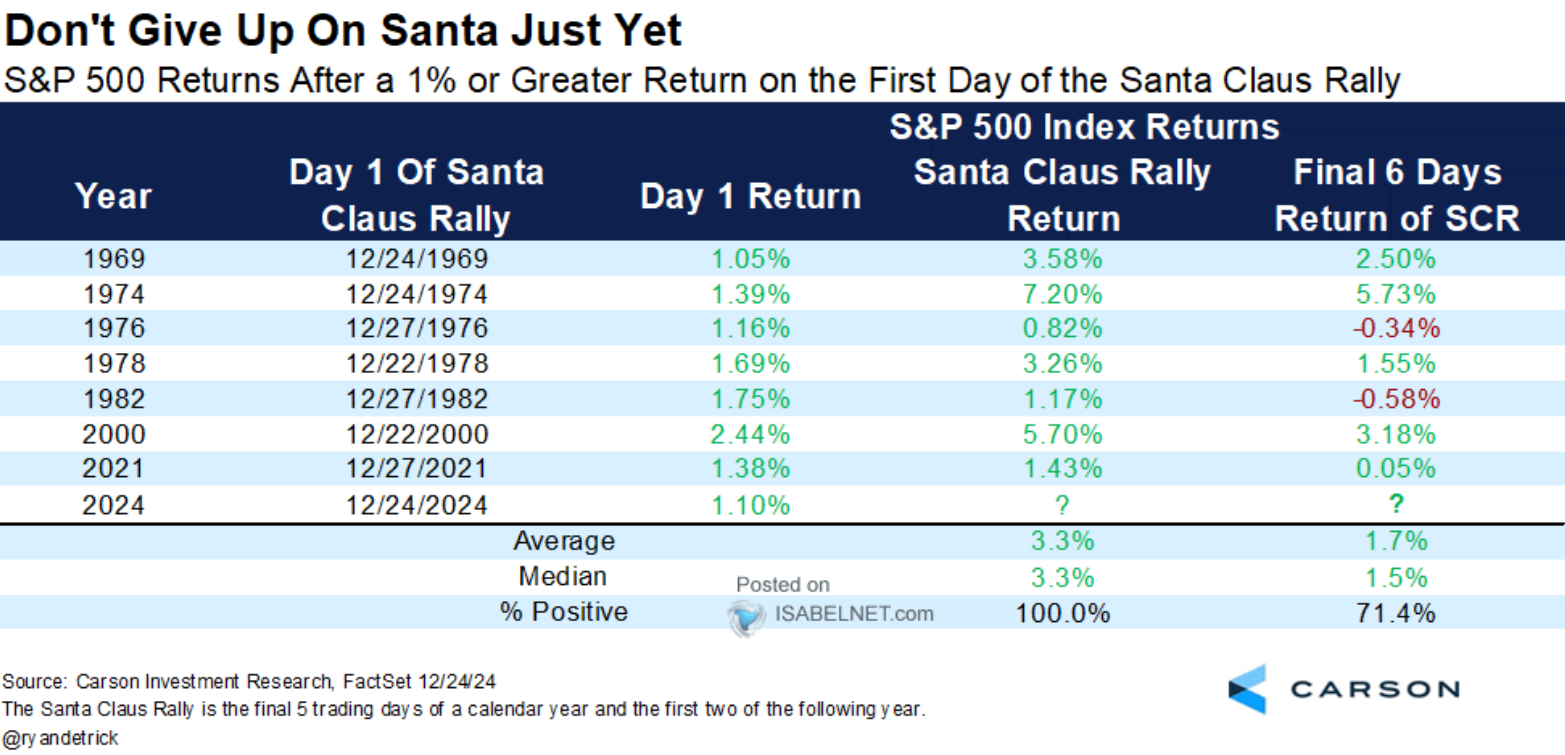

A strong week with a gain of 1.08% on the first day of the ‘Santa Rally’ (last trading day before Christmas). Bulls are excited! Since 1969, each time the S&P 500 has gained 1% or more on the first day of the Santa Claus Rally, it has been positive 100% of the time during the full rally period, with an average gain of 1.7%

Source: Carson Investment Research (click to enlarge)

Tech and growth stocks pulled Wall Street’s main indexes down on Friday, capping off a positive, shorter trading week known for usually being a strong time for markets.

Growth stocks sensitive to interest rates fell, with Nvidia dropping 3%, Tesla losing 3.8%, and Microsoft down 2%. Ten of the 11 major S&P sectors also dropped, with information technology and consumer discretionary seeing the biggest declines at around 2% and 1.9%, despite leading much of the market’s gains in 2024.

Will markets get the strong end to the Santa Clause rally ahead of January 1 next week?

The US Dollar Index (DXY) continued its advance this week and is on course for marginal gains. More importantly the Index is on course for a daily candle close above the 108.00 handle.

Despite the stronger US Dollar, EUR/USD and GBP/USD remained steady and held their ground with marginal losses to end the week.

The Japanese Yen bounced back from a five-month low against the dollar on Friday. This came after the Bank of Japan’s December meeting notes showed some policymakers becoming more confident about a possible rate hike soon. The central bank also reduced its monthly bond purchases which helped the Yen finish the week on a positive note.

Oil prices went up by about 1% on Friday and were on track for a weekly increase, despite light trading as the year-end approaches. The rise was supported by expectations of lower U.S. crude stockpiles and hopes for an economic recovery in China driven by stimulus measures.

Gold prices had a mixed week, edging higher for the majority of the trading week before dropping back closer to the 2600/oz mark to end the week. Gold continues to find support due to the growing list of uncertainties expected in 2025 while the stronger US Dollar is likely to cap the upside potential moving forward.

The Week Ahead: Data Remains Slow but Liquidity Likely to Return

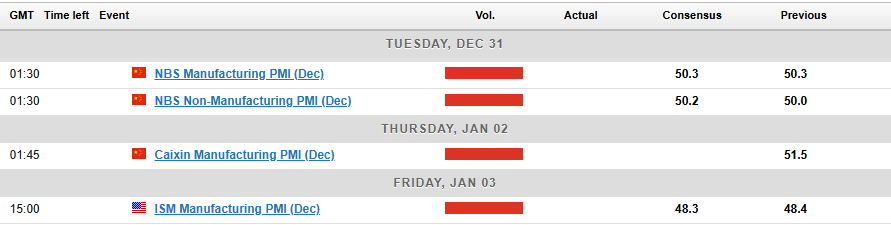

Asia Pacific Markets

The week ahead in the Asia Pacific region still remains light on the data front.

The highlight will be PMI data from China which could have ripple effects across various commodities. Manufacturing in China is key to global oil demand as well which adds further weight to the data release. Given the recent stimulus measures that have been put into effect by Chinese authorities, markets will be looking for signs of an improvement across the board in the coming weeks.

The NBS manufacturing PMI will be released on Tuesday while the Caixin manufacturing PMI will bring the week to a close on Thursday.

Europe + UK + US

In developed markets, it is a quiet week for Europe and the UK with the only high impact data release coming from the US.

The biggest data release from the US will be out on Friday with the manufacturing PMI data release. The US economy has remained resilient in 2024 with many expecting a blockbuster year under President Elect Donald Trump in 2025.

Chart of the Week

This week’s focus remains on US Equities and the S&P 500 in particular following its recovery and the start of the Santa Rally.

The S&P 500 looked set for a strong week heading into Friday, trading up around 3% for the week. However Friday’s tech and growth stock inspired selloff leaves the index with marginal gains for the week.

Given all the talk of the Santa Rally, the performance of the index on December 24 set the stage for a strong finish to the year. As we mentioned at the start of the article, Since 1969, each time the S&P 500 has gained 1% or more on the first day of the Santa Claus Rally, it has been positive 100% of the time during the full rally period.

With that in mind, the S&P 500 is now trading almost 1.7% lower than the December 24 high meaning the S&P could potentially rally around 1.7% before next Tuesday when the Santa Rally period ends. Will history repeat itself and the S&P 500 deliver?

Looking at the daily chart below, one can see that the overall bearish trend which began following the massive selloff on December 18 remains intact. The index needs a daily candle close above the swing high at 6072 to signal a shift to bullish structure.

There is also the possibility that the index could rise and test this week’s high on Monday or Tuesday next week before falling once more. In this way the index could maintain its historical Santa Rally performance while maintaining its current bearish trajectory, leaving the index open to further downside.

Given the optimism around the US economy with the Trump administration, the probability of a break higher remains strong. Thus despite the current technical picture one cannot overlook these key fundamental themes as well.

S&P 500 Daily Chart – December 27, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 5910

- 5871

- 5828

Resistance

- 6000

- 6030

- 6093

Week Ahead – Dollar Set to End 2024 on a High as Bulls Face Few Obstacles

- Another quiet holiday week looms for financial markets.

- Manufacturing PMIs, including the US ISM, are the only highlight.

- But rising US yields and sliding yen may spark New Year’s fireworks.

Manufacturing PMIs in the spotlight

The mid-week market closure in celebration of New Year’s Day across much of the world has left little space for any major data releases. S&P Global’s manufacturing PMIs and the equivalent ISM gauge are likely to be the only indicators capable of generating some significant market moves over the coming week.

However, any policy-related headlines about US President-elect Donald Trump could also spur volatility, while yen traders will probably be on intervention watch as the Japanese currency continues to bleed following the widening policy gap after the Fed and BoJ meetings.

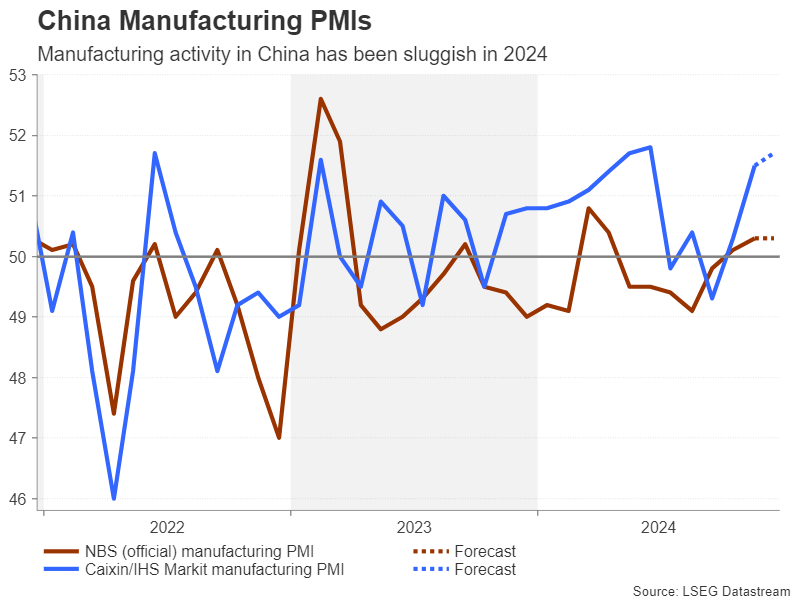

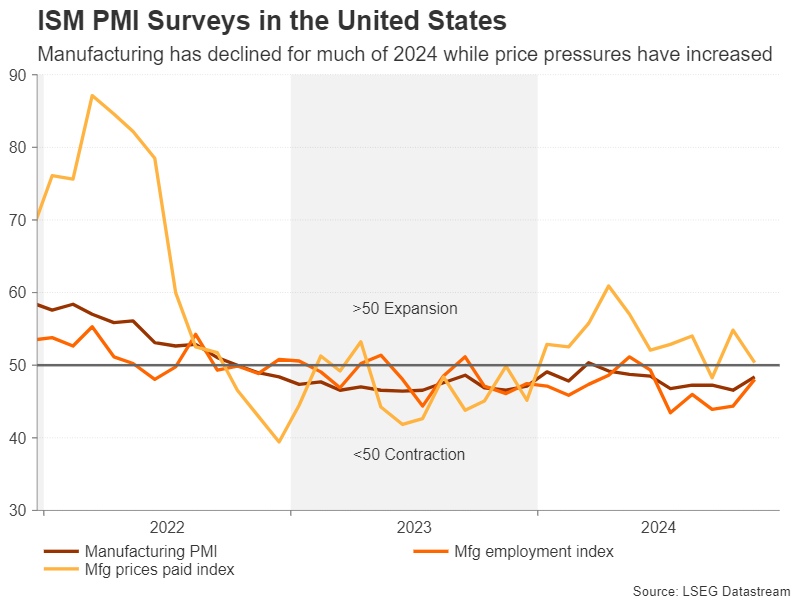

But first, it’s important to highlight that 2024 hasn’t been a great year for global manufacturers. Although most major economies enjoyed a modest rebound in manufacturing activity from the troughs of 2023, the recovery in most regions has been patchy at best, while in the Eurozone, it’s remained in contractionary territory for the entire year.

In China, there’s been some divergence between the official and S&P Global/Caixin manufacturing gauges. The government’s metric, which includes mainly large and state-owned enterprises, has barely managed to hold above 50, but the S&P Global/Caixin PMI has performed much better.

For December, they’re expected to rise modestly, maintaining their recent trend. Unless there’s a big upside surprise in either of them, the data is unlikely to provide much of a boost to regional stocks, but a negative surprise could dent sentiment.

Can ISM Mfg. PMI stop the Dollar’s advance?

In the United States, the manufacturing sector had a stronger first half but has been a drag on the rest of the economy in the second half. More worryingly, the disinflation process that started in 2022 ended at the start of 2024. However, the prices index now appears to be settling close to the 50-neutral level, suggesting that cost pressures are easing, which may help reduce the recent sharp layoffs in the sector.

In December, the ISM manufacturing PMI is forecast to have edged down from 48.4 to 48.3, with the prices index expected to pick up from 50.3 to 52.2. A weaker-than-expected reading for the latter could pressure the US dollar slightly, although in the absence of any crucial updates on the economy, investors will likely be tuning into Trump’s commentary.

Neither the Chicago PMI nor pending home sales due on Monday are anticipated to attract much attention. But Thursday’s weekly jobless claims could be a bigger driver if there’s an unexpected increase in those claiming unemployment benefits. Any data suggesting the Fed was overly cautious about inflation and too optimistic about the labour market could see the dollar’s latest bull run unravel.

Trump a risk for New Year’s volatility

With just a month to go to Trump’s inauguration, speculation is mounting about what policies he will prioritise in his first few months in office. The recent debacle with the spending bill when the government came close to shutting down suggests that not all Republicans are on board with Trump’s fiscal ideology. Meanwhile, Trump has already upped the ante when it comes to tariffs, threatening America’s allies – Canada, Mexico and the European Union – with higher levies.

Any developments on tariffs or fiscal policy during the holiday lull when trading volumes tend to be extremely thin could bring about some big spikes in Treasury yields, which would then have ripple effects in FX and equity markets.

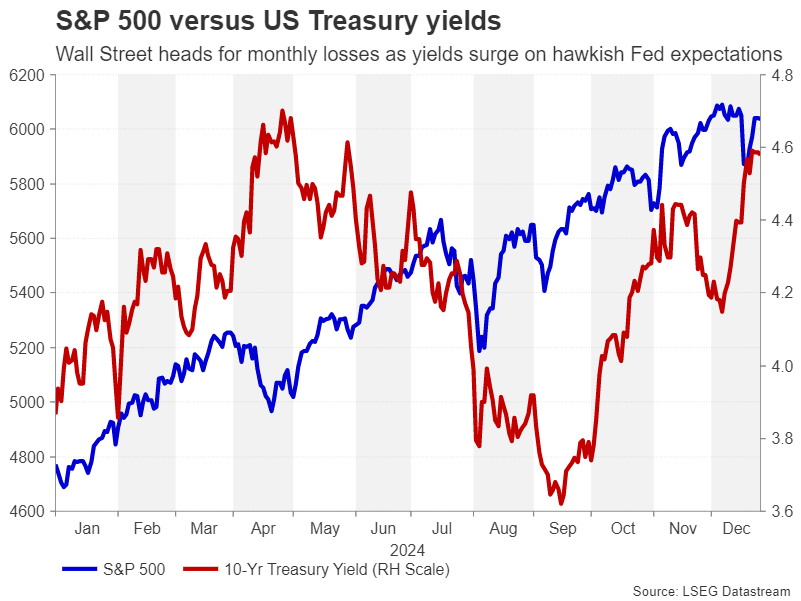

Can yields go even higher?

The benchmark 10-year yield has crossed above 4.60% and could soon surpass the 2024 high of just under 4.74%, while the dollar index is trading at more than two-year highs. This leaves the greenback vulnerable to a downside correction. But if both yields and the dollar continue to climb, it could force Japanese authorities to intervene to prop up the yen, which is down more than 5% in December.

Stocks on Wall Street could also suffer, although it’s mainly small-caps and non-tech stocks that seem to be struggling under the weight of higher yields. The tech-dominated Nasdaq 100 is even on track to end the month in positive territory, unlike the Dow Jones.

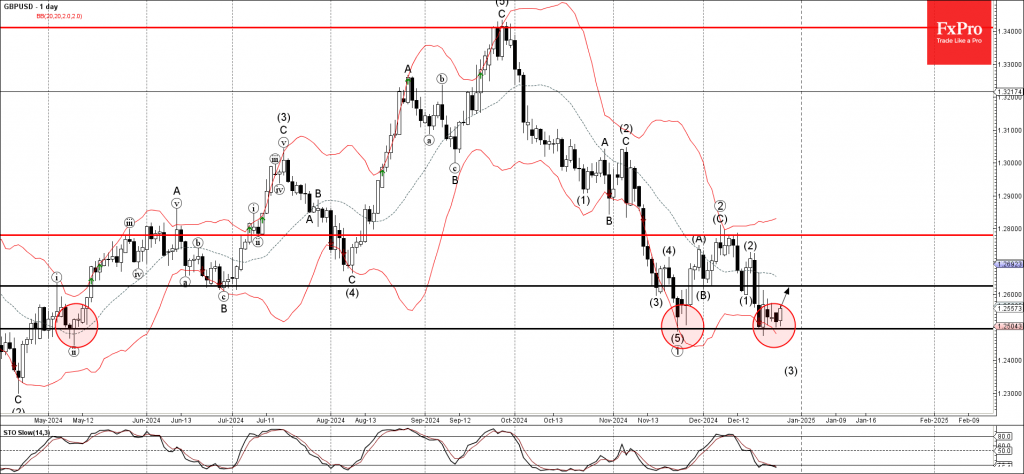

GBPUSD Wave Analysis

- GBPUSD reversed from support level 1.2495

- Likely to rise to resistance level 1.2625

GBPUSD currency pair recently reversed up from the pivotal support level 1.2495 (which has been steadily reversing the pair from May) intersecting with the lower daily Bollinger Band.

The upward reversal from the support level 1.2495 stopped the previous medium-term impulse wave (3).

Given the strength of the support level 1.2495 and the oversold reading on the daily Stochastic indicator, GBPUSD currency pair can be expected to rise to the next resistance level 1.2625 (former support from the end of November).

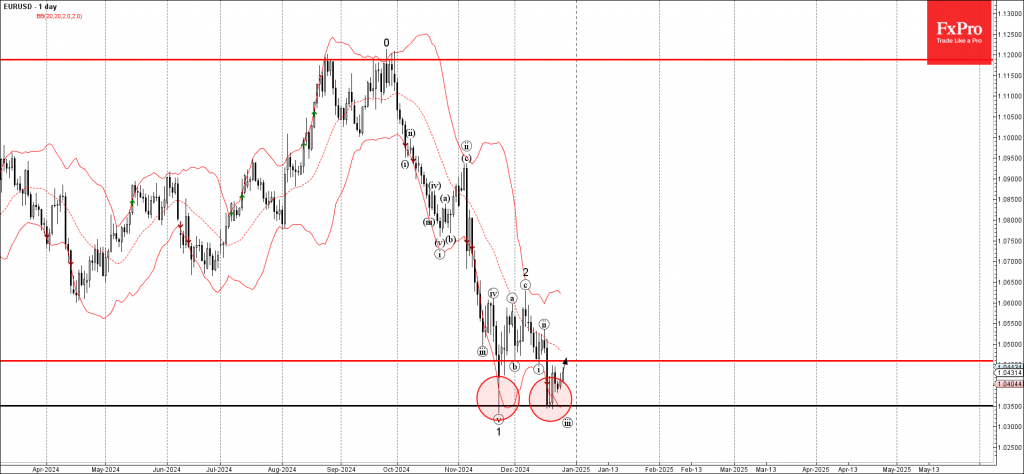

EURUSD Wave Analysis

- EURUSD reversed from powerful support level 1.0350

- Likely to rise to resistance level 1.0460

EURUSD currency pair recently reversed up with the daily Morning Star from the powerful support level 1.0350 (which stopped the previous sharp downward impulse wave 1 at the end of November).

The upward reversal from the support level 1.0350 started the active short-term correction iv.

Given the strength of the support level 1.0350 and the moderately bearish USD sentiment seen today, EURUSD currency pair can be expected to rise to the next resistance level 1.0460 (former support from the start of December).

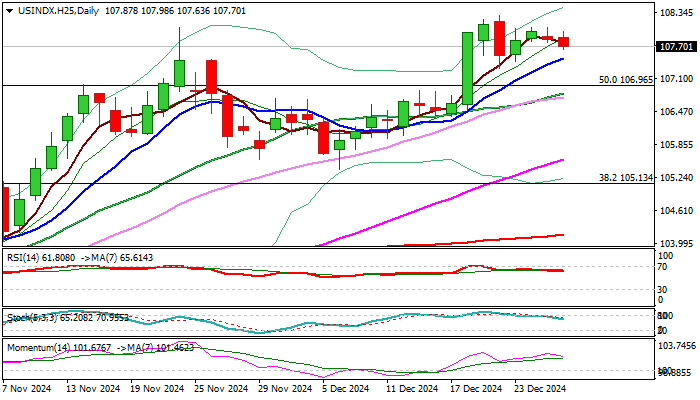

Dollar Index Outlook: Bulls Pause for Consolidation, Expected to Remain Intact While Above 107.00 Support

Near term action holds in extended consolidation under new multi-month high (108.28), as bulls took a breather in a quieted holiday trading.

Overall picture remains firmly bullish, with Dollar index being on track for the third consecutive monthly gain (over 7% advance in past three months).

The dollar index is also on track to register monthly close above the top of larger range (99.20/107.03) where the price was entrenched since December 2022.

The range top also marks 50% retracement of 114.72/99.20 correction (Sep 2022 / July 2023) and holding above this level will keep medium-term structure in firm bullish mode.

On the other hand, south turning daily indicators warn of possible correction or extended sideways trading, with solid supports at 107.47 (rising 10DMA) and 107.00 zone (former range tops) expected to hold dips and provide better levels to re-enter bullish market.

The dollar remains well supported by hawkish shift in Fed’s monetary policy outlook on still elevated inflation and expectations for more aggressive support to the economy from coming Trump’s administration, keeping in play prospects for stronger gains in coming months.

Next significant barriers lay at 108.80 (Fibo 61.8%) and 110.00 (psychological) violation of which to open way for full retracement of 114.72/99.20 corrective phase.

Res: 108.28; 108.80; 109.35; 110.00.

Sup: 107.47; 107.00; 106.73; 106.17.

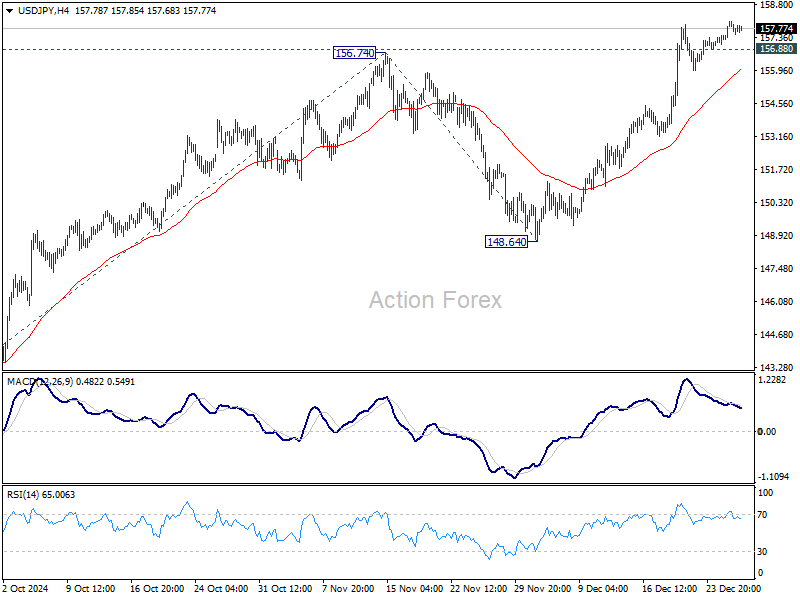

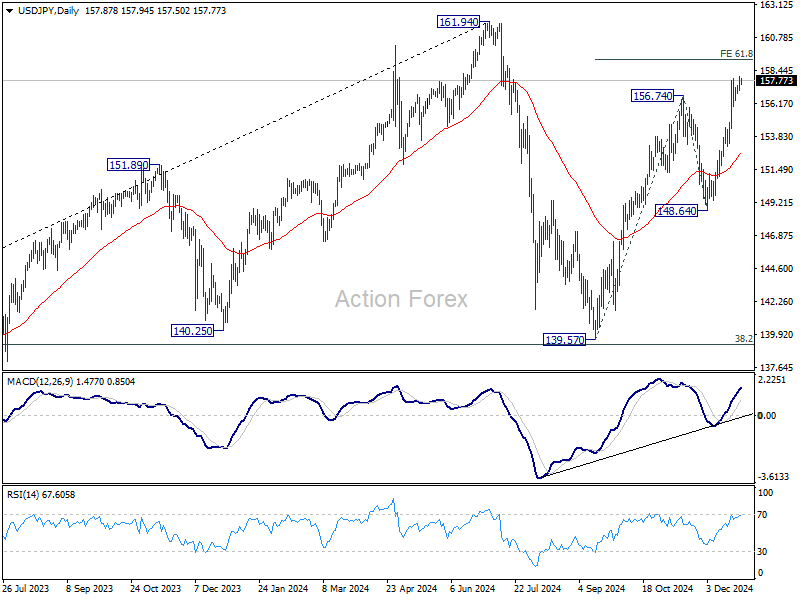

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.32; (P) 157.70; (R1) 158.42; More...

Intraday bias in USD/JPY stays mildly on the upside at this point. Rise from 139.57 is in progress for 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. Firm break there will pave the way back to 161.94 high. On the downside, though, below 156.88 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

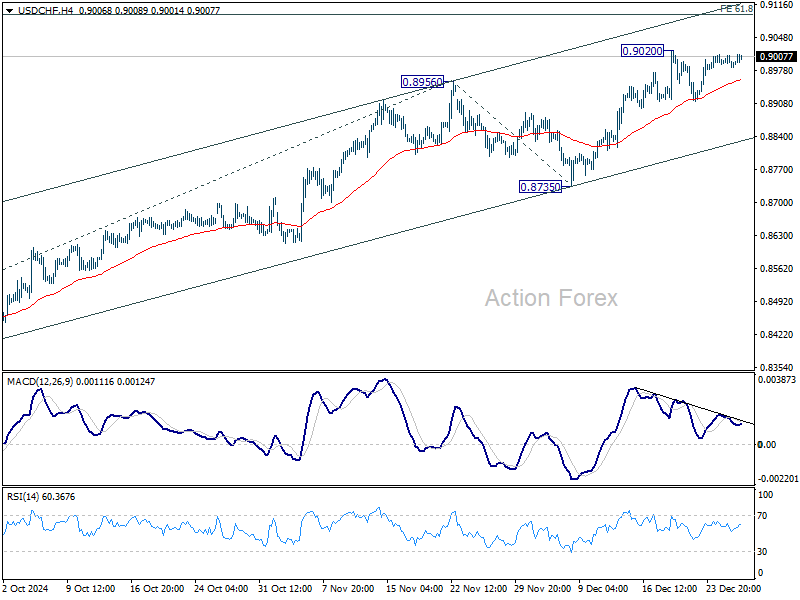

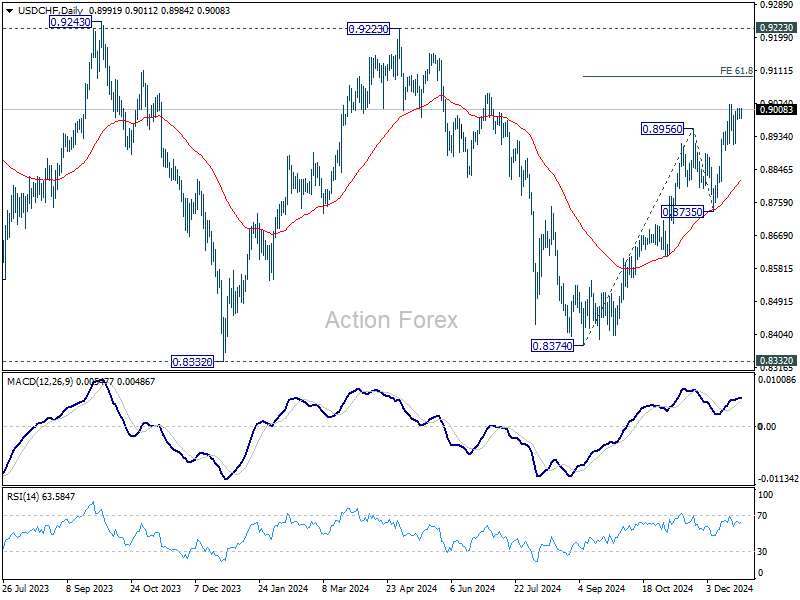

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8979; (P) 0.8994; (R1) 0.9004; More…

USD/CHF is staying in consolidations below 0.9020 and intraday bias remains neutral. While another pull back might be seen, downside should be contained above 0.8735 support to bring another rally. Above 0.9020 will resume the rise from 0.8374 and target 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

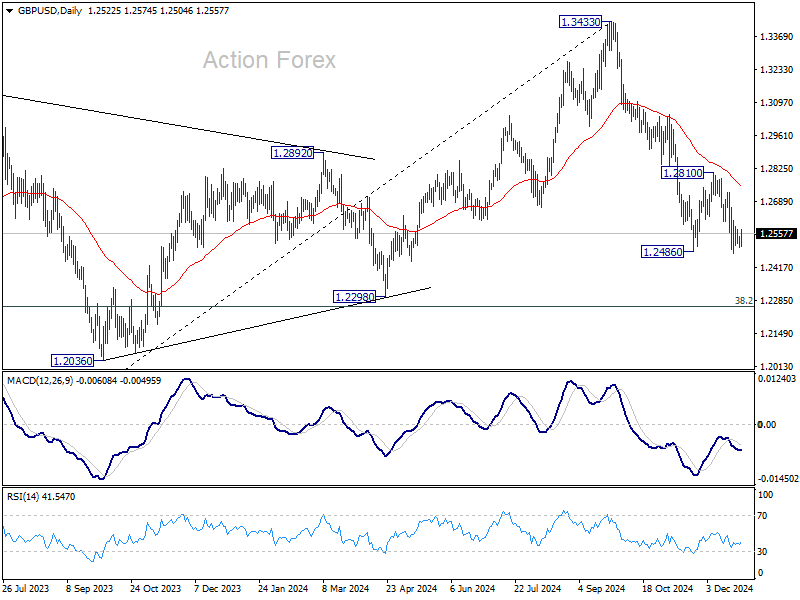

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2498; (P) 1.2530; (R1) 1.2559; More...

GBP/USD recovers mildly today but stays in range of 1.2474/2810. Intraday bias remains neutral for the moment. While another recovery cannot be ruled out, outlook will stay bearish as long as 1.2810 resistance holds. On the downside, break of 1.2474 will resume the fall from 1.3433 to 1.2298 cluster support zone.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.