Sample Category Title

Pound: “We Did Not Mean to Vote for Brexit”

Friday June 9: Five things the markets are talking about

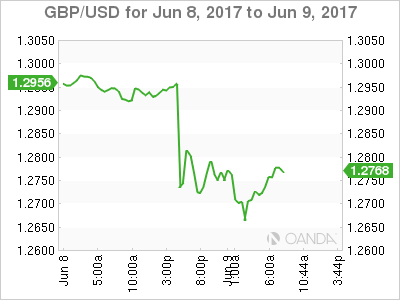

It's little surprise to see sterling tumble, as much as -2.4%, after a disastrous night for the PM Theresa May's Conservatives party, who with an electoral swing, lost her parliament majority with a hung House of Commons.

The key concern driving U.K asset prices, aside from market liquidity issues, is how this election will impact Britain's ongoing divorce with the European Union, which Prime Minister Theresa May had already begun three-months ago.

The Conservatives, as the party with most seats (316), will have first shot at trying to form a new government either as a formal coalition with another party or by relying on other parties to help vote through its policies.

If they can't build a majority large enough to govern, the Labour Party (261) would get a chance to form a government.

What's left is that the market again faces more political uncertainty and with Comey's testimony in Washington yesterday, it's on both sides of the Atlantic.

Note: This morning's press conference - PM May said she will not step down as PM and is in talks with senior party colleagues about how to form a new government.

For more political intrigue it's now onto French where voters go to the polls this weekend as part of a two-step process for parliamentary elections. The outcome will decide how much control President Macron will have to enact his legislative agenda.

1. Global stocks mixed results

In Japan, the Nikkei 225 stock average rallied +0.5%, supported by the index heavyweight SoftBank who rallied +7.4% to the highest in 17-years after agreeing to buy Boston Dynamics from Google parent Alphabet Inc. The broader Topix index rose +0.1%.

In Hong Kong, the Hang Seng fell -0.2%, the Hang Seng China Enterprises Index lost -0.6% and the Shanghai Composite added +0.3% - data overnight showed China's producer price gains moderated following further easing in commodity prices.

Elsewhere, South Korea's Kospi index climbed +0.8% and Singapore's Straits Times Index added +0.5%.

In Europe, indices are trading higher across the board, but off the earlier session highs with outperformance in the FTSE 100 benefiting from -2% slide in the pound (£1.2720).

In the U.S, stocks are set to open in the 'black.'

Indices: Stoxx50 +0.5% at 3580, FTSE +0.7% at 7499, DAX +0.5% at 12775, CAC-40 +0.6% at 5294 IBEX-35 +0.2% at 10975, FTSE MIB +0.6% at 21165, SMI +0.3% at 8839, S&P 500 Futures +0.2%

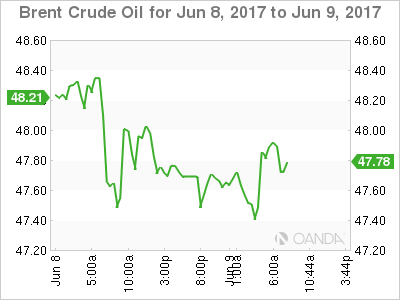

2. Oil prices resume slide as supply glut prevails

Global oil prices have resumed their downtrend ahead of the U.S open following steep falls this week, pressured by widespread evidence of a fuel glut despite efforts led by OPEC to tighten the market.

Brent crude is down -20c at +$47.66 a barrel, around -12% below its opening level on May 25, when an OPEC promise to restrict production was extended into 2018. U.S. light crude (WTI) is down -20c at +$45.44.

Not helping the supply glut is U.S supplies and production rates. U.S data this week showed a surprise +3.3m barrel build in commercial crude oil stocks to +513.2m. Inventories of refined products were also up, despite the start of the peak-demand summer driving season.

Note: U.S. refined oil product inventories are now back above 2016 levels and well above their five-year range.

Technically, the world is awash with crude and more production is coming. Libya's 270k-bpd Sharara oilfield has reopened after a workers' protest and should return to normal production by next week.

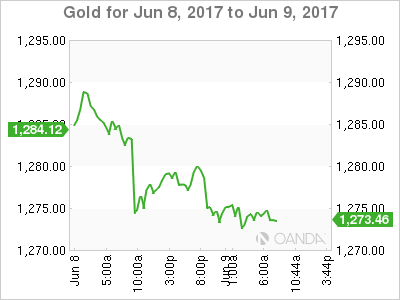

In early trade, gold (-0.4% to +$1,274.95) has fallen for a third day as the USD firmed after the U.K national election results left no single party with a majority.

3. Yields back up

Yesterday, the ECB kept its monetary policy unchanged, but changed its forward guidance by removing its easing bias regarding policy rates. German 10-year Bund yields are flat at +0.25%.

French 10-year yields have fallen -1bps ahead of this weekend's parliamentary election.

In the U.K, despite the political uncertainty, asset prices moves remain very well contained. U.K 10-years Gilts U.K. gilt yields rose +2 bps to +1.06%, after climbing +3 bps yesterday. The inconclusive U.K general election results will make it almost certain that the Bank of England (BoE) will keep monetary policy ultra-loose to support growth.

The focus now switches to next week's Fed decision (June13-14). For many, the big question is if the Fed does hike next week is whether it would leave the door ajar for further monetary tightening in the months to come. The yield on 10-year Treasury notes has rallied +1 bps to +2.20%.

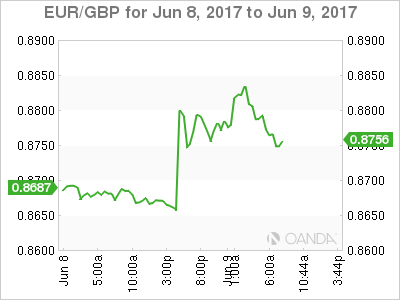

4. Pound plummets on political woes

It's little surprise that the focus in FX overnight was the pound and the U.K election results.

Sterling began the European session testing its two-month lows atop or £1.2635 on the possibility that PM May would not be able to acquire a solid majority. It has since recovered to trade back above £1.2741 on fundamental support - U.K showed industrial production weaker than forecast in April, but the trade deficit narrower more than expected.

Sterling remains down close to -2% compared with just before exit polls were released late Thursday.

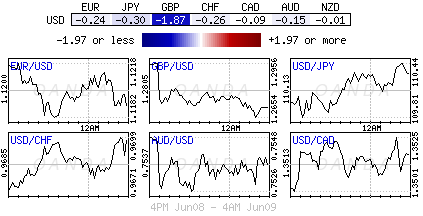

The 'big' dollar remains slightly firmer against other major pairs in relatively quiet trading with focus on the Fed rate decision next week. The EUR (€1.1179) is a tad softer after yesterday's ECB meeting and quarterly staff projections.

The yen (¥110.38) has not responded to any safe-haven demand after the PM May's disastrous election.

5. Germany's trade surplus steadies in April

Data this morning showed that Germany's adjusted trade surplus was unchanged in April, after exports and imports picked up further compared with the previous month.

Total exports of goods increased for the fourth consecutive month to a record of €106.3B in April. Goods imports rose by +1.2% to €86.6B (record).

This resulted in a stable trade surplus of €19.8B - the market was expecting €20B.

Note: German exports have picked up notably since the start of the year, led by stronger demand from China and India.

Elliott Wave Analysis: USD Index Undergoing A Recovery

USD Index is making a rally from the lows, specifically from the 96.48 level where we labeled end of wave 5. Current impulsive sequnce can be the first sign of a low in place and a suggestion that more gains may follow. At the moment we see first wave A/1 in motion, which can be trading in final stages. Once wave A or 1 unfolds, a new three wave correction into wave B or 2 may follow. Support for the upcoming correction can be around 96.88/97.12 region.

USD Index, 1H

UK Election Results In Further Questions Than Answers

The eyes of the world are on the United Kingdom once again following another unexpected outcome to an election vote.

Has recent history repeated itself once again? It certainly feels that way after it appears that market expectations were once again left on the wrong side of the trade when it comes to a UK vote, with the UK election concluding in a hung parliament. This wasn’t what anyone really wanted or expected as traders themselves watch the Pound slip 300 points against the Dollar, with losses in the British Sterling now seeing the currency diving all the way from 1.2950 to marginally below 1.2635 at the time of writing.

Before we dissect into the nitty gritty details around the behavior of the Pound there are a couple of other market-related questions on spectator’s minds, for example why has the FTSE 100 climbed higher at European open despite all of this uncertainty? This is most likely due to the Pound weakness and the inverse correlation that has seen Pound losses encourage FTSE gains over the past year. Another question that has left some puzzled is why has the financial market fluctuations been so restricted towards the Pound, and not seen in other asset classes like demand for safe-havens? It appears that investors are treating the UK election as an independent Brexit/Britain issue, which is something that will lead to more concern for the UK and its economy than impacts elsewhere on the financial markets.

Moving back to the Pound, another question on the mind of traders is why is the currency not moving further south? With all the uncertainty in mind, the next direction for the Pound should be lower and I personally still think that 1.25 is the possible eventual target for sellers should the selling momentum continue. The outcome to the UK election has been the opposite to what traders priced into the markets with the expectation of a landslide victory for Theresa May not occurring, which is why the Pound is looking at risk to retracing all gains made since the announcement of the snap election.

Some even expected the Pound to plunge all the way towards 1.20 against the Dollar in the event of a hung parliament and while the market might not have moved as much as expected with the door of uncertainty for the UK open even wider following this result, what this means away from any valuations in the financial markets is that the worst potential outcome has been realized with official Brexit negotiations scheduled to begin in less than a fortnight. It was widely perceived that the major motive for Theresa May to announce a snap election was to have a stronger hand in the Brexit negotiations, but her playing card has not turned out as she had hoped and now the UK is embracing even more uncertainty just days away from a collision course with the European Union.

Where does the market head from here? The risks look heavily tilted towards further downside pressure. What investors could be waiting for is some clues on what could possibly be happening next, before determining what direction the Pound should really be heading in next.

Although this outcome has come as an unexpected surprise for most, what we can confidently say at this stage is that the UK is going to encounter further political instability and this represents a wide contrast from the United Kingdom of the past, something that has clearly changed since the EU referendum and looks set to continue.

DAX Posts Gains As ECB Drops Rate Guidance, Upgrades Growth Forecast

The DAX index has posted modest gains in the Friday session. The index is up 0.49% and is currently at 12,770.50 points. On the release front, there is just one event on the schedule. Germany's trade surplus improved to EUR 19.8 billion, but this fell short of the forecast of EUR 20.3 billion.

The ECB played it cautious at the June policy meeting. The central bank maintained the benchmark rate at 0.00%, and made no changes to its quantitative easing scheme (QE) of EUR 60 billion/month. However, there was an unexpected development, as the ECB removed its guidance on rate cuts, saying that rates could remain at current levels for an extended period. Effectively, the ECB has closed the door on lowering rates into negative territory, although the bank could change its stance if economic conditions in the euro-area deteriorate. On a brighter note, the ECB revised upwards its growth forecasts for the eurozone – from 1.8% to 1.9% in 2017, and from 1.7% to 1.8% in 2018. Analysts also noted a shift in language, as Draghi characterized risks to the economy as “broadly balanced”, compared to previous warnings that risks were “tilted to the downside”. However, low inflation levels remain a serious concern, and the ECB acknowledged this, lowering its inflation forecast. The ECB is now predicting inflation in 2017 at 1.5% in 2017 and 1.3% in 2018. Back in March, the forecast stood at 1.7% in 2017 and 1.6% in 2018. The ECB is not expected to revisit its monetary policy until the September meeting. Drahgi and his colleagues appear in no rush to tighten monetary policy, but at the same time, policymakers carefully chose less dovish language in the rate statement, in order to relieve pressure from Germany, which has been outspoken in demanding tighter monetary policy.

There was plenty of excitement in Washington on Thursday, as former FBI director James Comey testified before the Senate Intelligence Committee on Thursday, The TV ratings were high, but Comey did not deliver any bombshells while on the stand. Comey stated that he was not specifically asked by President Trump to close an investigation into Trump's alleged ties with Moscow, so it is unlikely that his testimony will be the “smoking gun” that leads to charges of obstruction of justice against Trump. Still, Comey's testimony raised troubling questions about Trump's conduct, and will only complicate matters for the beleaguered Trump administration. Investors are growing more skeptical that Trump, who seems to be spending most of his time in damage control mode, will be able to deliver on key promises, and may come to view the president as a lame duck, just months into his presidency.

What Next For GBP After May’s Humiliating Defeat?

It's been quite a memorable night in the UK where once again an election has come and gone and results have come as quite a surprise to both voters and the markets, alike.

Only a month ago, with Theresa May's poll lead at around 20 points, it appeared that the election was going to be a landslide leading to questions about the future of Jeremy Corbyn as Labour leader. One month on and the reality is that the Conservative campaign is being labelled a shambles, it's on course to lose its majority and Corbyn is being praised for a quite remarkable comeback.

U.K. Parliament is Hung, Drawn and Quartered

While Labour voters may be celebrating, the markets are not in such a bright mood. A hung parliament – as looks very likely now – could be devastating for the preparation of Brexit negotiations which is due to begin in little over a week. A hung parliament was the worst outcome for the markets and yet, under the circumstances the response has been fairly mild. While the reason for this will only become apparent in the coming hours or days, the prospect of a coalition with the DUP or SNP which would take them above the threshold may be what markets are banking on.

Should that fail to materialise, then the moves which we've already seen overnight in the pound may get much worse. The drop in GBPUSD after the exit polls was very significant but even then, it remains slightly above the level that it was trading at prior to May calling the election back in April. Clearly there is no panic yet but should coalition talks fail and the prospect of another election prevail, I struggle to see it maintaining these levels and it would seriously harm the UK's position in Brexit talks and create huge uncertainty.

While the election may remain the focus as we see out the week, UK data will also attract some attention throughout the morning. Manufacturing and industrial production figures, along with trade balance data and an estimate of GDP for the three months to the end of May from NIESR will all be released.

Euro Dips As ECB Lowers Inflation Forecast

The euro has recorded slight losses in the Friday session. In the European trade, EUR/USD is trading at 1.1170. In economic news, there are no major events in the eurozone or the US. Germany’s trade surplus improved to EUR 19.8 billion, but this fell short of the forecast of EUR 20.3 billion.

As expected, the ECB kept the benchmark rate pegged at 0.00%, and made no changes to its asset-purchase plan (QE) of EUR 60 billion/month. However, the central bank did surprise the markets by removing its guidance on rate cuts, saying that rates could remain at current levels for an extended period. Previous rate statements had said that interest rates could go lower, so the markets may take the rate statement as a message that the ECB has taken a step closer to winding up its stimulus program. At the same time, the ECB lowered its inflation forecast, acknowledging that inflation levels remain below the ECB’s target of 2.0%. The ECB is now predicting inflation in 2017 at 1.5% in 2017 and 1.3% in 2018. Back in March, the forecast stood at 1.7% in 2017 and 1.6% in 2018. The rate statement made no reference to the QE scheme, which winds up in December. On a brighter note, the ECB revised upwards its growth forecasts for the eurozone – from 1.8% to 1.9% in 2017, and from 1.7% to 1.8% in 2018. Analysts also noted a shift in language, as Draghi characterized risks to the economy as “broadly balanced”, compared to previous warnings that risks were “tilted to the downside”. Drahgi and his ECB colleagues appear in no rush to tighten monetary policy, but at the same time used less dovish language in the rate statement, in order to relieve pressure from Germany, which has been outspoken in demanding tighter monetary policy.

In Washington, former FBI director James Comey is currently testified before the Senate Intelligence Committee on Thursday, The TV ratings were high, but Comey did not deliver any bombshells while on the stand. Comey stated that he was not specifically asked by President Trump to close an investigation into Trump’s alleged ties with Moscow, so it is unlikely that his testimony will be the “smoking gun” that leads to charges of obstruction of justice against Trump. Still, Comey’s testimony raised troubling questions about Trump’s conduct, and will only complicate matters for the beleaguered Trump administration. Investors are growing more skeptical that Trump, who seems to be spending most of his time in damage control mode, will be able to deliver on key promises, and may come to view the president as a lame duck, just months into his presidency. This kind of sentiment could boost the euro against the dollar.

Technical Outlook: Oil Price Remains Under Strong Pressure, Consolidation To Precede Fresh Weakness

Oil remains under strong pressure on evidence of oil oversupply that offset OPEC efforts to support oil prices by extending output cut for additional nine months. Long red daily candle that was left on last Wednesday's strong fall, continues to heavily weigh on market. Friday's action is entrenched within narrow consolidation range above fresh one-month low at $45.19, posted on Thursday. Firm bearish setup of daily studies maintains strong bearish pressure, with close below cracked Fibo 76.4% support at $45.68 required to confirm bearish resumption which may extend towards key short-term support at $43.74 (05 May spike low). Oil is also on track for the third straight strong bearish weekly close which confirms strong bearish stance. Bears may take a breather on consolidative/corrective action signaled by oversold slow stochastic on daily chart, however, no firmer signals so far, as indicator continues to move south.

Res: 45.91, 46.16, 46.89, 47.62

Sup: 45.19, 44.81, 44.17, 43.74

Sterling Nosedives On Hung Parliament Outcome

The UK election ended with an upset, as Theresa May and the Conservatives failed to secure a majority in the House of Commons. The UK is now faced with a hung parliament, meaning that even though the Tories are still the largest party, they have to either rule with a minority or form a coalition with another party to be able to govern effectively. The pound plunged on the news, as this implies increased instability within Parliament and likely makes the Brexit negotiating process much more difficult, at least for the UK.

GBP/JPY collapsed as soon as the first exit poll showed that the Conservatives were unlikely to gain majority. The pair fell below the support (now turned into resistance) of 141.90 (R2) and managed to dip below Wednesday's low of 140.70 (R1). The tumble was stopped at 139.60 (S1) and then, the rate rebounded somewhat. The price structure on the 4-hour chart still suggests a short-term downtrend, while the election dip confirmed a forthcoming lower low. We think that the pound could remain under pressure in coming days, at least until there is a clear plan about what happens next. We expect the bears to take the reins again soon and aim for another test near 139.60 (S1). A dip below that level could aim for our next support of 138.90 (S2).

Moving forward, we expect the pound's forthcoming direction to be dictated by how the election outcome will impact the Brexit process and whether this increases the likelihood for a softer negotiating approach. Signs that the divorce may end up “softer” than what was anticipated up to now could lead to a notable rebound in GBP, we think. The questions in our mind are: Will Theresa May resign? If she does, will the new Conservative leader have a different (and potentially softer) view on Brexit? What if the Labour Party manages to establish a coalition of many parties and challenge the Tories? We expect the answers to these questions to play a critical role in how sterling behaves in the following days.

ECB: Less dovish guidance, but no tapering in sight

Yesterday, the ECB kept its policy unchanged. The most striking change in the accompanying statement was the removal of the easing bias that rates can be lowered further. Policymakers now expect rates to remain at current levels moving forward. Draghi's press conference was eventful as well. The euro dipped initially, after he announced that even though the Bank upgraded its GDP forecasts until 2019, the inflation forecasts for the same period had been revised lower.

These downgrades likely poured cold water on expectations that QE tapering may be on the horizon. With inflation expected at 1.3% yoy in 2018, there is no rush for the ECB to consider scaling back its asset purchases. The common currency rebounded a few minutes later, after Draghi said the Bank removed its easing bias on rates mainly because the risk of deflation has disappeared. The key takeaway we got from this meeting is that the ECB is becoming more confident that inflation will eventually converge to its target, but it is still premature to discuss QE tapering at this stage.

As for the euro, even though it may underperform for a bit more, we remain optimistic on its broader path. The ECB is slowly but surely shifting towards a more sanguine tone, implying it could remove further dovish aspects from its guidance in coming meetings, if economic data continue to evolve as, or better than, projected.

EUR/USD traded lower as the ECB was not as optimistic as the market may have expected heading into the gathering. The pair is currently trading between the 1.1160 (S1) support and the resistance of 1.1240 (R1), while it still trades above the uptrend line taken from the low of the 17th of April. This keeps the outlook positive and as such, we would treat yesterday's slide as a corrective setback. We expect the bulls to take charge again soon and perhaps aim for the 1.1300 (R2) territory. A break above that level would confirm a forthcoming higher high and is likely to pave the way for our next resistance hurdle of 1.1370 (R3).

Today's highlights:

During the European day, we get the UK industrial production and trade data, both for April. In Norway, CPIs for May are due out. The forecast is for both the headline and the core rates to have declined. Further slide in the core rate could increase the likelihood for further easing by the Norges Bank and thereby, extend NOK's latest losses.

In Canada, the unemployment rate to have ticked up in May following a notable drop in April, while the net change in employment is expected to have risen. We see the risks surrounding the unemployment rate forecast as skewed to the downside, considering that the Markit manufacturing PMI for the month reported one of the strongest rates of job creation in five-and-a-half years. A positive surprise could bring CAD under renewed buying interest.

GBP/JPY

Support: 139.60 (S1), 138.90 (S2), 138.15 (S3)

Resistance: 140.70 (R1), 141.90 (R2), 143.00 (R3)

EUR/USD

Support: 1.1160 (S1), 1.1110 (S2), 1.1075 (S3)

Resistance: 1.1240 (R1), 1.1300 (R2), 1.1370 (R3)

GBP Falls Off A Cliff As PM May Loses Her Bet

USD broadly higher after UK elections

The outcome of the UK general election was quite a surprise as the market was broadly anticipating a victory for the Conservatives. Investors had bet heavily that Theresa May would have been able to reinforce her party's support in the House of Commons. Clearly this is definitely not going to happen.

Against such a backdrop, the pound suffered a sell-off with GBP/USD falling as low as 1.2636, down roughly 2% from yesterday. In fact, with the exception of the New Zealand dollar, all G10 currencies moved in negative territory against the greenback. The dollar index rose 0.45% to 97.36 as the single currency slid 0.20%, the Japanese yen fell 0.30 and the Canadian dollar edged down 0.10%.

We maintain our view that the dollar has been oversold, especially after the ECB reiterated a dovish stance yesterday and the political jitters surrounding James Comey's FBI dismissal in the US seemed to be a non-event. We expect the USD to get some colour back as investors cut their bullish bet on the EUR and risk aversion is eased.

Switzerland: Safe haven pressures expected amid UK results

That was a surprising result in the UK, Theresa May has lost her bet and did not win a clear majority. Her plan fell apart. A few weeks ago, markets had expected a large Conservative victory. But over the last week, the trend was rather negative for May and Labour leader Jeremy Corbyn's result overcame expectations.

Now we wonder how this result will impact the Swiss franc in particular. What can be said is that there are more upside pressures on the Helvetic currency. Indeed, negotiations between the EU and the UK that should start next on June 19th promise to be tense.

This is especially because of tensions betweens the ‘hard' Brexiteers and the ‘soft' Brexiteers. European political uncertainties should prevail and no one could really say at the moment what the future UK exit package will look like. We anticipate in the medium-term more move towards the CHF.

GOLD Failed To Hold Above $1300, SILVER Lack Of Follow-Through, CRUDE OIL Continued Decline.

GOLD Failed to hold above $1300.

Gold is consolidating within uptrend channel. Hourly support is located at 1246 (18/05/2017 low). Stronger support is given at 1195 (10/03/2017 low). Expected to show renewed upside pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Lack of follow-through.

Silver declines. Closest support is given at 16.20 (04/05/2017 low). Strong support is given at 15.63 (20/12/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). Expected to push back towards 61.8% Fibonacci retracement around 17.75.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Continued decline.

Crude oil keeps on moving lower after the recent collapse from $52. Support is given at a distance 43.76 (05/05/2017 low). The technical structure suggests further weakness towards 43.76.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).