Sample Category Title

Canadian Labour Markets Leapt Forward in May

Canada added a healthy 54.5k net jobs in May. The previous month's drop in the labour force more than reversed (+78.4k in May), enough to move the unemployment rate a notch higher to 6.6%.

It was full-time work that led the gains, up 77k positions, while part-time employment fell 22.3k positions on net. Canada has added 185.1k net full-time positions so far this year, well ahead of the 27.9k net added at the same point in 2016.

It was largely the private sector leading the way, adding 59.4k net jobs, more than reversing April's declines. The public sector remained a net job creator as well (+9.2k).

Job creation was seen in both the goods-producing (+23.3k) and service-producing (+31.3k) sides of the economy. The goods side was largely a story of manufacturing (+25.3k) as the other major sectors turned in flat performances. Within services, professional services (+25.9k), transportation (+17.1k), trade (+15.2k), and health care (+15.1k) were the star performers. In contrast, finance, insurance, real estate and leasing saw a loss of 17.4k net positions, and a sizeable decline was also seen in information, cultural, and recreation (-15.8k).

Regionally, it was Ontario (+19.9k), Quebec (+14.9k), and B.C. (+12.3k) that led the gains. Job growth in the other provinces was effectively flat. Notably, a shrinking labour force in Quebec led the unemployment rate down to 6.0% (from 6.5%), while in Ontario, it was the opposite story, as rising participation swamped job gains, leading to a 0.7 p.p. climb in the unemployment rate, to 6.5% (reversing the previous month's declines)

Hours worked were up a modest 0.7% year-on-year (April: +1.1%), while the hourly wage rate gain 1.0% year-on-year, an improvement from the record slow pace recorded in the month prior.

Key Implications

This is a report with a lot to like in it. May recorded the biggest monthly net jobs gain since September of last year (and the best performance year-on-year since February of 2013), largely on gains in full-time work. Moreover, gains were spread across most sectors, with solid private sector hiring activity. Even the modest uptick in the unemployment rate is a welcome development as it reflected a labour market that drew Canadians back in. Indeed, among Canadians aged 15 to 64 years, the participation rate remains near all-time highs.

The soft spot in Canadian labour markets remains hours worked and wages. Growth in hours worked has improved in recent months, but remains somewhat soft, particularly given the healthy gains in full-time work. Similarly, wage growth may have recovered from last month's low, but at 1.1% year-on-year, remains soft by any measure.

The May jobs report provides further indication that the Canadian economy is likely to remain fairly robust in the second quarter. Wage growth may remain a soft spot for now, but the healthy labour market, including strong core participation rates, should continue the upward pressure in wages, and prices more generally. We remain of the view that the pieces are falling in place to allow the Bank of Canada to begin tightening monetary policy early next year.

CAC Yawns as ECB Remains Cautious, French Election Looms

The CAC index is showing little movement in the Friday session. Currently, the CAC is at 5275.00 points. On the release front, there are no major events on the schedule. French Industrial Production was soft, posting a decline of 0.5%. This was well short of the estimate of +0.3%.

There were no major moves from the ECB at the June policy meeting, as the central bank held course on interest rates and the quantitative easing program (QE). The central bank maintained the benchmark rate at 0.00%, and kept QE purchases at EUR 60 billion/month. However, the ECB did remove its guidance on rate cuts, saying that rates could remain at current levels for an extended period. Effectively, the ECB has closed the door on lowering rates into negative territory, barring a nosedive in economic conditions in the euro-area. As well, the ECB revised upwards its growth forecasts for the eurozone – from 1.8% to 1.9% in 2017, and from 1.7% to 1.8% in 2018. Analysts also noted a shift in language, as Draghi characterized risks to the economy as "broadly balanced", compared to previous warnings that risks were "tilted to the downside". However, low inflation levels remain a serious concern, and the ECB acknowledged this, lowering its inflation forecast. The ECB is now predicting inflation in 2017 at 1.5% in 2017 and 1.3% in 2018. Back in March, the forecast stood at 1.7% in 2017 and 1.6% in 2018. The ECB is not expected to revisit its monetary policy until the September meeting. Drahgi and his colleagues appear in no rush to tighten monetary policy, but at the same time, policymakers carefully chose less dovish language in the rate statement, in order to relieve pressure from Germany, which has been outspoken in demanding tighter monetary policy.

The stunning results in the British elections, which saw the Conservatives squander their majority, has overshadowed the upcoming French parliamentary elections. Unlike the election campaign across the Channel, the outcome is much less uncertain, as French President Emmanuel Macron is widely expected to cruise to victory. Opinion polls are showing that Macron's LREM party, which is barely one year old, has 30% of votes, with the conservative Republicans trailing at 22%. The polls, which were quite accurate in last month's presidential election, are predicting that Macron will win a convincing majority in parliament. Macron, a strong supporter of the European Union, is expected to implement pro-business reforms and streamline government. The young and charismatic Macron is expected to be a strong ally of German Chancellor Angela Merkel, who herself will face the voters in a September election.

Canadian Employment Surged 55k higher in May

Highlights:

- Employment jumped a much-stronger-than-expected 55k in May. Markets expected a 15k gain.

- Full-time employment was up 77k to more-than-offset a 22k drop in part-time.

- The unemployment rate inched up to 6.6% from 6.5% in April as labour force participation rose.

- Year-over-year wage growth for permanent employees remained modest but rose to 1.0% from the all-time low 0.5% in April

Our Take:

The jump in employment in May continued an unusually long streak of gains for a survey that is typically very volatile. The 55k surge in employment marked the 16th gain out of the last 18 months. Average growth over that period has been 21k. The unemployment rate ticked up to 6.6% from the cycle-low 6.5% in April but because of a jump in the labour force. The measure was still down 0.3 percentage points from a year ago and there is little evidence that factors like worker discouragement or involuntary part-time employment have been behind recent declines. The labour force participation rate is close to all-time highs when controlling for the aging of the population.

Wages remain the soft-spot although annual growth in permanent employee wages rose to 1.0% from the all-time low 0.5% increase in April. Other wage measures have, though, been somewhat stronger. Compensation-per-hour worked was up 2.5% year-over-year in the first quarter and wage growth in the alternative 'SEPH' labour force survey for Canada was 2.4% year-over-year in March.

Strengthening in labour markets and stronger recent GDP growth numbers increasingly argue that current ultra-low interest rates may no longer be needed to support the economy. We nonetheless, continue to expect slow wage growth, lack of upward pressure in consumer prices, and uncertainty about U.S. trade policy during the upcoming NAFTA renegotiation will keep the Bank of Canada cautious and don't expect a rate hike until the first half of 2018.

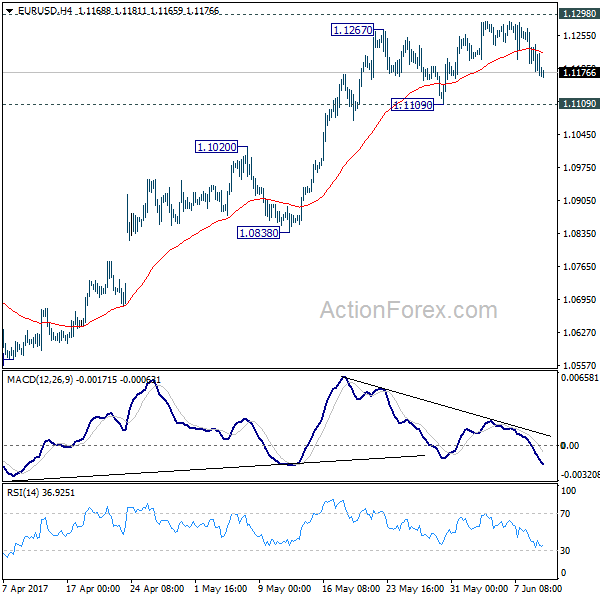

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1181; (P) 1.1225 (R1) 1.1256; More....

EUR/USD dips further in early US session but it's staying well above 1.1109 key near term resistance. Intraday bias remains neutral and further rally could be seen. Decisive break of 1.1298 will carry larger bullish implication and target 1.1615 resistance next. However, break of 1.1109 will indicate short term topping and rejection from 1.1298. In that case, intraday bias will be turned back to the downside for 1.0838 support first.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0888). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

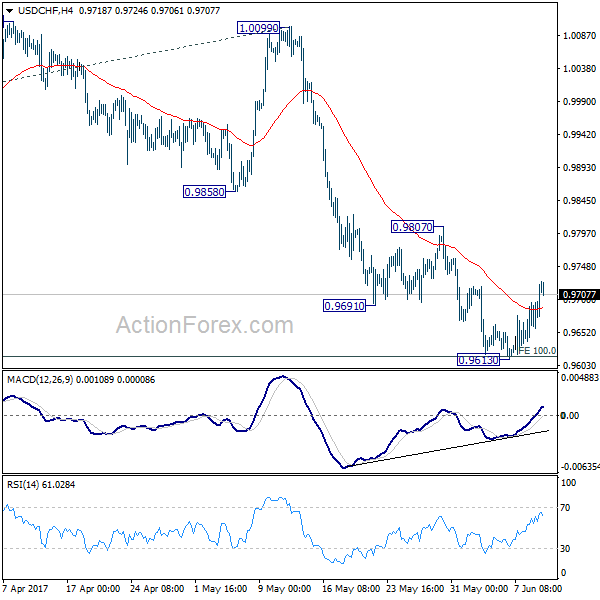

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9635; (P) 0.9666; (R1) 0.9703; More.....

USD/CHF's rebound from 0.9613 extends higher. But still, it's limited well below 0.9807 resistance. Near term outlook stays bearish and deeper fall is expected. When decline from 1.0342 resumes, we'd start to look for bottoming signal again as it approaches 0.9443 key support level. However, considering bullish convergence condition in 4 hour MACD, break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

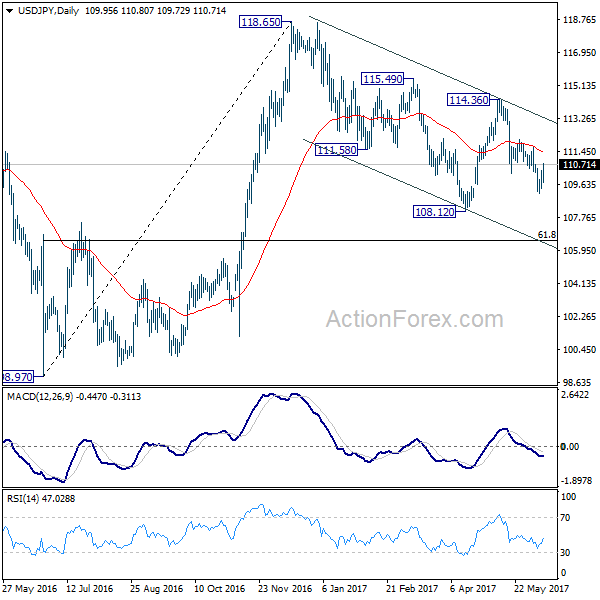

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.47; (P) 109.92; (R1) 110.48; More...

USD/JPY's rebound from 109.11 extends higher today. But still it's limited well below 111.70 resistance. Thus, near term outlook stays bearish and deeper decline is expected. Below 109.11 will target 108.12 low first. Break will extend whole decline from 118.65 to 61.8% retracement of 98.97 to 118.65 at 106.48. As such decline is seen as a correction, we'll looking for bottoming signal around 106.48. Meanwhile, break of 110.70 will suggest near term reversal and turn bias back to the upside for 114.36 resistance instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

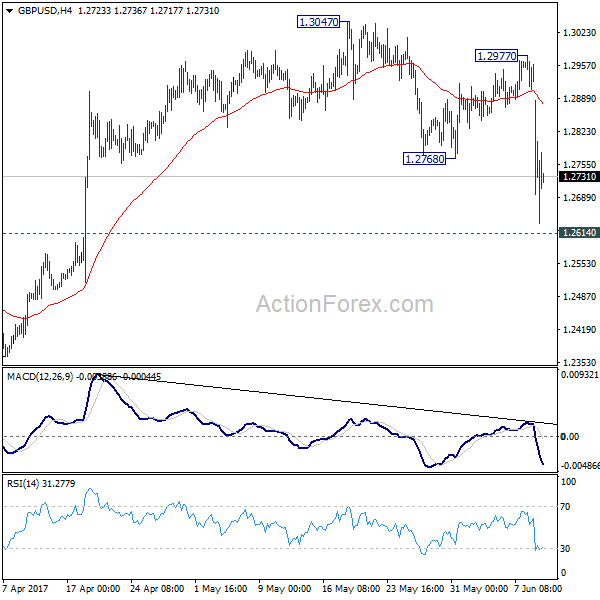

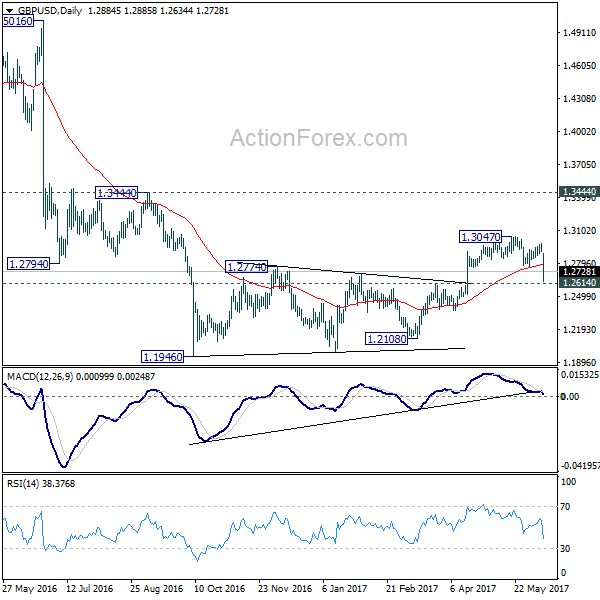

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2912; (P) 1.2944; (R1) 1.2982; More...

Intraday bias in GBP/USD remains on the downside as the decline from 1.3047 is still in progress for 1.2614 key support level. We're favoring the case that whole consolidation pattern from 1.1946 has completed at 1.3047 already. Decisive break of 1.2614 should confirm this bearish view. In such case, larger down trend should be resuming for a new low below 1.1946. On the upside, break of 1.2977 resistance is now needed to indicate completion of the fall from 1.3047. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

Sterling Stabilized as Conservatives Form Coalition with Democratic Unionist Party, CAD Jumps on Employment

Sterling stabilized a bit after the post UK election sharp fall. After suffering the election backslash and losing majority in the parliament, Prime Minister Theresa May visited the Queen at Buckingham Palace to get permission to form a new government. May emphasized that "what the country needs more than ever is certainty" and "now, let's get to work". The Conservatives is now expected to form coalition with Northern Ireland's Democratic Unionist Party. And both parties reached consensus to keep May in the position for now. But overall, May's political survival remains in question. And, there are five candidates identified who could fill the role of Prime Minister, including Boris Johnson, Philip Hammond and David Davis.

Released from UK today, trade deficit narrowed to GBP -10.4b in April. construction output dropped -1.6% mom in April. Industrial production rose 0.2% mom, dropped -0.8% yoy in April. Manufacturing production rose 0.2% mom, 0.0% yoy in April. NIESR GDP estimate rose 0.2% in May.

EU officials showed impatience regarding Brexit negotiation

EU official showed some impatience on the situation of Brexit negotiation after UK election. European Commission President Jean-Claude Juncker said that the can "open negotiations tomorrow morning at half-past nine." Therefore, they are "waiting for visitors coming from London". Juncker hoped that "we will not experience a further delay in the conclusion of this negotiation." EU President Donald Tusk said that "we don't know when Brexit talks start" but "we know when they must end". Hence "do your best to avoid a no as a result of no negotiation". Meanwhile, EU's Brexit negotiator Michel Barnier said that "Brexit negotiations should start when UK is ready; timetable and EU positions are clear."

Released from Eurozone, German trade surplus widened slightly to EUR 19.8b in April.

CAD lifted by job data

Some strength is seen in Canadian dollar in early US session on solid job data. The employment market grew 54.5k in May, well above expectation of 17.0k. Unemployment rate rose 0.1% to 6.6% in May. Nonetheless, the Loonie is standing on shaky ground as weakness in oil price persists. WTI dipped to as low as 45.27 earlier today before recovering to 45.70. Near term support at 43.76 is still what the WTI is targeting at. Also from Canada, capacity utilization rate rose to 83.3% in Q1.

Elsewhere, Japan M2 rose 3.9% yoy in May. China CPI accelerated to 1.5% yoy in May, PPI slowed to 5.5% yoy. Australia home loans dropped -1.9% in April.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2912; (P) 1.2944; (R1) 1.2982; More...

Intraday bias in GBP/USD remains on the downside as the decline from 1.3047 is still in progress for 1.2614 key support level. We're favoring the case that whole consolidation pattern from 1.1946 has completed at 1.3047 already. Decisive break of 1.2614 should confirm this bearish view. In such case, larger down trend should be resuming for a new low below 1.1946. On the upside, break of 1.2977 resistance is now needed to indicate completion of the fall from 1.3047. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. The rejection from 55 week EMA is maintaining bearishness in the pair. Also, at this point, as long as 1.3444 resistance holds, fall from 1.7190 is still expected to continue. Break of above mentioned 1.2614 support will affirm this bearish case.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y May | 3.90% | 4.30% | 4.30% | 4.00% |

| 01:30 | CNY | CPI Y/Y May | 1.50% | 1.50% | 1.20% | |

| 01:30 | CNY | PPI Y/Y May | 5.50% | 5.70% | 6.40% | |

| 01:30 | AUD | Home Loans Apr | -1.90% | -1.00% | -0.50% | |

| 04:30 | JPY | Tertiary Industry Index M/M Apr | 1.20% | 0.50% | -0.20% | -0.30% |

| 06:00 | EUR | German Trade Balance (EUR) Apr | 19.8B | 20.3B | 19.6B | |

| 08:30 | GBP | Industrial Production M/M Apr | 0.20% | 0.70% | -0.50% | |

| 08:30 | GBP | Industrial Production Y/Y Apr | -0.80% | -0.30% | 1.40% | |

| 08:30 | GBP | Manufacturing Production M/M Apr | 0.20% | 0.80% | -0.60% | |

| 08:30 | GBP | Manufacturing Production Y/Y Apr | 0.00% | 0.70% | 2.30% | |

| 08:30 | GBP | Construction Output M/M Apr | -1.60% | 0.40% | -0.70% | |

| 08:30 | GBP | Visible Trade Balance (GBP) Apr | -10.4B | -12.0B | -13.4B | |

| 12:00 | GBP | NIESR GDP Estimate May | 0.20% | 0.20% | ||

| 12:30 | CAD | Capacity Utilization Rate Q1 | 83.30% | 82.40% | 82.20% | |

| 12:30 | CAD | Net Change in Employment May | 54.5K | 17.0k | 3.2k | |

| 12:30 | CAD | Unemployment Rate May | 6.60% | 6.60% | 6.50% | |

| 14:00 | USD | Wholesale Inventories Apr F | -0.30% | -0.30% |

USD/JPY Important Resistance Could Reject the Price

The USD/JPY has spiked due to excessive USD buying negating the yen strength during risk off as seen yesterday. The pair is at important POC zone (D H4, order block, 50.0, trend line) 110.50-55. However if momentum persists the pair could spike further to the upside towards 110.70-85 POC2 (61.8, W H3, historical sellers). Watch for possible rejection within the POC zones although I personally favour the POC2 rejection due to possible Friday profit taking. The pair should drop to 109.65 if rejected.

PM May’s Gamble to Enlarge the Conservatives Majority Fails

Notes/Observations

- UK election results in a hung Parliament; PM May's gamble to enlarge the Conservatives majority fails

- Coalition with Northern Ireland's Democratic Unionist Party (DUP) could deliver the Conservatives the votes they need to pass legislation; DUP said to back PM May (no formal agreement in place)

Overnight

Asia:

- China May CPI in-line with expectations and at a 4-month high (Y/Y: 1.5% v 1.5%e)

- BOJ's Kuroda: Japan is no longer experiencing deflation; long way to go until Japan price stability target is achieved UK Results (646 seats of 650)

- Conservatives (Tories): 315 seats (-12)

- Labour: 261 seats (+29)

- SNP: 35 seats (-21)

- Liberal Democrats: 12 seats (+4)

- DUP: 10 seats (+2)

Election commentary

- PM May: will not step down as PM; in talks with senior party colleagues about how to form a new government; to visit Buckingham Palace later today - financial press

- Labour Party leader Corbyn (opposition): PM May has lost her mandate; I think that's enough for her to go

- Liberal Democrat spokesperson Campbell: It's very difficult to see how the Party could join a coalition

- Democratic Unionist Part (DUP) Donaldson: Would negotiate with the conservatives if they fail to achieve a majority adding that they have a lot of ground

- Democratic Unionist Part (DUP) member Foster: no-one wants to see a hard Brexit; we want a workable plan

- Democratic Unionist Part (DUP) said to consider a 'confidence and supply' arrangement to ensure Theresa May has support to keep her in government

- Labour Party Finance spokesperson McDonnell: Will not do a coalition deal; will put ourselves forward to form a minority govt

- Labour Shadow Chancellor John McDonnell: Labour will seek to form a minority government because the Conservative party is not "stable, If they do seek to do a coalition with the DUP... well, pardon the expression but someone used it during the campaign, it is a coalition of chaos

- Germany's DIW institute: UK election result has turned PM May into a "lame duck" and signals voters' rejection of her tough stance in the Brexit negotiations.

Americas:

- Former FBI Dir Comey testimony: Trump administration did not ask him to stop Russia election probe; Trump did not specifically order him to let Flynn probe go; took Trump's comment as a direction, but didn't obey it My common sense was that Trump was looking to get something in exchange for granting request to stay on the job

- President Trump's attorney: Comey hearing established that Trump was not being investigated for colluding or attempting to obstruct FBI investigation

Economic Data

- (NO) Norway May CPI M/M: 0.2% v 0.2%e; Y/Y: 2.1% v 2.1%e

- (NO) Norway May CPI Underlying M/M: 0.3% v 0.3%e; Y/Y: 1.6% v 1.6%e

- (DE) Germany Apr Current Account Balance: €15.1B v €24.5Be; Trade Balance: €18.1B v €23.0Be; Exports M/M: +0.9% v +0.3%e; Imports M/M: +1.2% v -0.5%e

- (DE) Germany Q1 Labor Costs Q/Q: No est v 1.5% prior; Y/Y: 2.5% v 2.9% prior

- - (FR) France Apr Industrial Production M/M: -0.5% v +0.2%e; Y/Y: 0.6% v 1.2%e

- (FR) France Apr Manufacturing Production M/M: -1.2% v -0.5%e; Y/Y: 1.1% v 1.8%e

- (CZ) Czech May CPI M/M: +0.2% v -0.1%e; Y/Y: 2.4% v 2.2%e

- (IT) Italy Q1 Unemployment Rate Q/Q: 11.6% v 11.6%e

- (UK) Apr Industrial Production M/M: 0.2% v 0.7%e; Y/Y: -0.8% v -0.3%e

- (UK) Apr Manufacturing Production M/M: 0.2% v 0.8%e; Y/Y: 0.0% v 0.7%

- (UK) Visible Trade Balance: -£10.8B v -£12.0Be; Total Trade Balance: -£2.1B v -£3.5Be; Trade Balance Non EU: -£2.1B v -£3.9B prior

- (UK) BoE/TNS May Inflation Next 12 Month: 2.8% v 2.9% prior

**Fixed Income Issuance:

- (IN) India sold INR150B vs. INR150B indicated in 2024, 2027, 2034 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

**Equities**

Indices [Stoxx50 +0.5% at 3580, FTSE +0.7% at 7499, DAX +0.5% at 12775, CAC-40 +0.6% at 5294 IBEX-35 +0.2% at 10975, FTSE MIB +0.6% at 21165, SMI +0.3% at 8839, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes European Indices trade higher across the board but off the earlier session highs with outperformance in the FTSE benefiting from a 200 pip plus fall in Sterling after a Hung Parliament in the UK Elections. In corporate news L'Oreal announced it was in seclusive talks with Natura in regards to BodyShop, whilst shares of Centrica trade higher after selling Canadian Business in which it will receive £240M. Air France maintains the positive news flow in Airlines after solid May metrics and RealDolmen trades sharply higher following strong Earnings.

Equities

- Consumer discretionary [Air France [AF.FR] +1.2% (May Metrics), John Menzies [MNZS] -1.8% (DX Group Investigation by the City of London Police), L'Oreal [OR.FR] +0.9% (Enters into exclusive discussions with Natura regarding sale of The Body Shop valued at €1.0B)]

- Industrials: [Airbus [AIR.FR] +1.6% (Media Day)]

- Financials: [Stanley Gibbons [SGI.UK] +15.6% (Confirms takeover approach)]

- Technology: [Realdomen [REA.BE] +5.9% (Earnings)

- Energy: [Centrica [CNA.UK] +1.7%(Partnership to sell Canadian E&P business to a consortium for C$722M in cash)]

Speakers

- PM May to go to Buckingham Palace with backing from Democratic Unionist Part (DUP) party to form govt. Conservatives and DUP will not have a formal coalition

- German Bundesbank raised its 2017 thru 2019 GDP growth forecasts. Raised 2017 GDP growth from 1.8% to 1.9%; 2018 GDP growth from 1.6% to 1.7% and 2019 GDP growth from 1.5% to 1.6%. It did cut its 2018 and 2019 inflation outlook. To just below the ECB target of around 2%.

- ECB's Weidmann (Germany) noted that a very healthy labor market situation, private consumption, together with general government demand and investment in housing in Germany would ensure an ongoing solid underlying pace

- Bank of France raised its 2017 thru 2019 GDP growth outlook. Raises 2017 GDP growth forecast from 1.3% to 1.4%; 2018 GDP from 1.4% to 1.6% and 2019 GDP from 1.4% to 1.6%

- ECB's Villeroy (France): noted that the French growth was lagging the Euro Zone. ECB remained active and was becoming more confident. ECB to remain predictable and saw no urgent need to change policy

- ECB's Nowotny (Austria) noted that ECB inflation forecasts had downside risks. Low inflation despite growth was a global issue. Did not rule out a fall in inflation in 2017 and 2018 if the Euro currency appreciated

- Labour Party leader Corbyn reiterated his call that PM May should resign. Brexit negotiations would have to go ahead without delay. Clear who won the election and was prepared to serve

- Moody's official Muehlbronner noted that was monitoring UK's process of forming new government

- Spain Catalan leader Puigdemont: To hold independence vote on Oct 1st with question will be "Do you want Catalonia to be an independent State within a Republican regime?"

- South Korea National Security Advisor: Do not look to change the agreement with US on the THAAD missile defense

Currencies

- FX market focus was on the GBP following the UK election results. GBP/USD began the session testing 7-week lows at 1.2635 before recovering and moving back above the 1.27 handle. The UK election results saw PM May lose her gamble with a hung Parliament and this increased uncertainty about the upcoming Brexit negotiations. Only one month ago the expectation was that the Conservatives would win big, and secure a landslide victory - The USD was slightly firmer against other major pairs in relatively quiet trading with focus on the Fed rate decision next week. The big question if the Fed does hike in June whether it would leave the door open for further monetary tightening in the months to come

- EUR/USD remained on soft footing after Thursday's ECB meeting and quarterly staff projections. The main focus was on inflation and the trimming of CPI during the ECB forecast horizon.

- The yen did not respond to any safe-have role despite the uncertainty of the UK election. USD/JPY higher by 0.4% and firmly above the 110 level for the time being.

Fixed Income

- Bund futures trade at 164.98 down 10 ticks after the ECB kept its monetary policy unchanged, but changed its forward guidance by removing its easing bias regarding policy rates. Resistance lies near the 165.70 level followed by 167.79. A break of the 162.65 support level could see lows target 159.96 followed by 157.50.

- Gilt futures trade at 129.08 higher by 25 ticks after the early general election resulted in a hung parliament. Gilts are in the middle of this week's trading range and continue to gravitate towards both the 129.00 handle and the 129.14 April 18th high. Price finds key support at the 128.48 support level. An acceleration lower could test the 127.43 region. Resistance remains the noted 129.00/129.14 region, then 129.75 followed by 130.28.

- Friday's liquidity report showed Thursday's deposits dropped rose to €614.9B from €608.4B prior. Use of the marginal lending facility fell to €143M from €257M prior.

- Corporate issuance saw $0.5B come to market via 1 issues headlined by Maxim Integrated Products senior unsecured note offering. This week's issuance is at $17.05B, lower than the analysts' issuance target to come in around $25B. For the week ending Jun 7th Lipper US fund flows reported IG funds net inflows $3.73B bringing YTD inflows to $61.69B, High yield funds reported outflows of $0.52B bringing YTD outflows to $4.90B.

Looking Ahead

- PM May post-election speech

- (MX) Mexico May Nominal Wages Y/Y: No est v 3.9% prior

- (PT) Portugal Debt Agency (IGCP) announces upcoming PGB auction for Jun 14th

- 05:30 (PL) Poland to sell Bonds

- 06:00 (UK) DMO to sell combined £3.0B in 1-month, 3-month and 6-month bills (£1.5B, £0.5B and £1.0B respectively)

- 06:00 (PT) Portugal Apr Trade Balance: No est v -€0.8B prior

- 06:45 (US) Daily Libor Fixing

- 07:00 (BR) Brazil Jun IGP-M Inflation (1st Preview): -0.4%e v -0.9% prior

- 07:00 (LT) ECB's Rimsevics

- 07:00 (CZ) Czech Central Bank comments on CPI data

- 07:30 (IN) India Weekly Forex Reserves

- 07:30 (UK) PM May at Buckingham palace

- 08:00 (UK) May NIESR GDP Estimate: No est v 0.2% prior

- 08:00 (BR) Brazil May IBGE Inflation IPCA M/M: 0.5%e v 0.1% prior; Y/Y: 3.8%e v 4.1% prior

- 08:15 (UK) Baltic Dry Bulk Index

- 08:30 CA) Canada May Net Change in Employment: +15.0Ke v +3.2K prior; Unemployment Rate: 6.6%e v 6.5% prior; Full Time Employment Change: No est v -31.2K; Part Time Employment Change: No est v +34.3K prior; Participation Rate: No est v 65.6% prior

- 08:30 (CA) Canada Q1 Capacity Utilization Rate: 83.5%e v 82.2% prior

- 09:00 (RU) Russia Apr Trade Balance: $8.7Be v $12.6B prior; Exports: $27.4Be v $31.3B prior; Imports: $18.7Be v $18.7B prior

- 09:00 (MX) Mexico Apr Industrial Production M/M: 0.3%e v 0.0% prior; Y/Y: -2.1%e v +3.4% prior; Manufacturing Production Y/Y: -1.0%e v +8.5 prior

- 10:00 (US) Apr Final Wholesale Inventories M/M: -0.3%e v -0.3% prelim; Wholesale Trade Sales M/M: 0.2%e v 0.0% prior

- 11:00 (EU) Potential sovereign rating after European close

- (CZ) Czech Sovereign Debt to be rated by Moody's - (IT) Italy Sovereign Debt to be rated by Moody's

- (PL) Poland Sovereign Debt to be rated by DBRS

- 12:00 (US) USDA World Agricultural Supply and Demand Estimates (WASDE) Crop Report

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 13:30 (DE) German Fin Min Schaeuble at CDU party event

- 14:00 (CO) Colombia Central Bank May Minutes