Sample Category Title

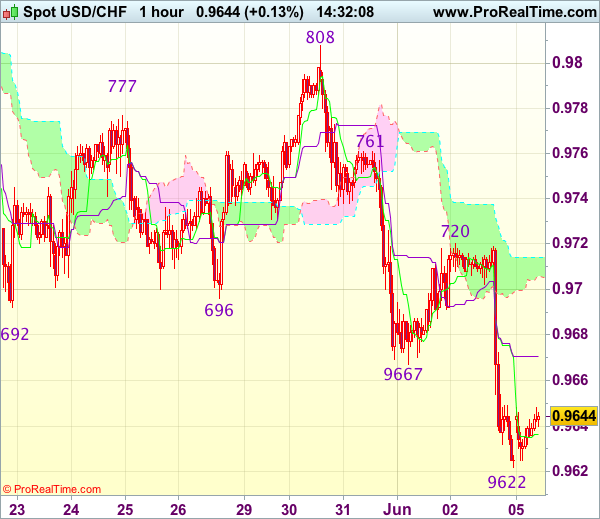

Trade Idea : USD/CHF – Sell at 0.9685

USD/CHF - 0.9636

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9637

Kijun-Sen level : 0.9671

Ichimoku cloud top : 0.9714

Ichimoku cloud bottom : 0.9706

Original strategy :

Sell at 0.9685, Target: 0.9585, Stop: 0.9720

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9685, Target: 0.9585, Stop: 0.9720

Position : -

Target : -

Stop : -

Dollar’s recovery after marginal fall to 0.9622 suggests minor consolidation would be seen and corrective bounce to the Kijun-Sen (now at 0.9671) cannot be ruled out, however, reckon upside would be limited to 0.9685-90 and bring another decline later, below said support at 0.9622 would extend recent decline to 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808) but oversold condition should limit downside to 0.9570 and price should stay well above support at 0.9550, bring rebound later.

In view of this, we are looking to sell dollar on recovery as 0.9685-90 should limit upside. Only break of resistance at 0.9720 would abort and signal a temporary low is formed instead, bring a stronger rebound to 0.9750 and then 0.9770 but price should falter below resistance at 0.9808.

Market Update – Asian Session: China Services PMI Soothes Soft Manufacturing Data

Asia Mid-Session Market Update: China Services PMI soothes soft manufacturing data; World Bank maintains global outlook; Oil rallies on Saudi Arabia-Qatar row

Friday US Session Highlights

(US) MAY UNEMPLOYMENT RATE: 4.3% V 4.4%E (lowest since May 2001)

(US) MAY CHANGE IN NONFARM PAYROLLS: +138K V +182KE; (birth/death adjustment +230)

(US) MAY AVERAGE HOURLY EARNINGS M/M: 0.2% V 0.2%E; Y/Y: 2.5% V 2.6%E; AVERAGE WEEKLY HOURS: 34.4 V 34.4E

(US) White House econ adviser Cohn: not worried about slowing job growth; we must create a better US jobs market

(US) Atlanta Fed cuts Q2 GDP to 3.4% from 4.0% on 6/1

Weekend corporate activity

HLF: Cuts Q2 guidance $0.75-0.95 v $1.00e (prior $0.88-1.08); Volume -8% to -4% y/y (prior -5% to -1%); Cuts FY17 $4.10-4.50 v $4.50e (prior $4.25-4.65); Volume -1% to +2% y/y (prior 2-5%)

P: Verizon may be interested in making a $100M investment in Pandora if it fails to reach sale to SiriusXM this week - NY Post

Politics

(RU) Russia President Putin denies knowledge of any attempts to set up back-channel discussions with Trump administration officials - US press

(US) White House not planning to give Congress a detailed tax reform draft until the August recess - Politico

(JP) Survey from Japan national broadcaster TBS saw PM Abe's cabinet approval rating fall 8.9 to 54.4%; lowest in over a year - press

(MX) MXN rallies from 18.82 to 18.72 on projections of a narrow win for ruling party in Mexico's key governor race - press

(UK) Survation/Mail poll on Parliamentary elections: Support for UK Conservatives at 40% (-6 ppt); Labour at 39% (+5 ppt)

Key economic data:

(CN) CHINA MAY CAIXIN PMI SERVICES: 52.8 V 51.5 PRIOR (4 month high); COMPOSITE: 51.5 V 51.2 PRIOR

(HK) HONG KONG MAY COMPOSITE PMI: 50.5 V 51.1 PRIOR (2nd straight expansion)

(AU) AUSTRALIA Q1 COMPANY OPERATING PROFIT Q/Q: 6.0% (4th straight quarter of increase) V 5.0%E; INVENTORIES Q/Q: 1.2% V 0.5%E

(AU) AUSTRALIA MAY ANZ JOB ADVERTISEMENTS M/M: 0.4% V 1.5% PRIOR (3rd straight increase)

(AU) AUSTRALIA MAY MELBOURNE INSTITUTE INFLATION M/M: 0.0% (3-month low) V 0.5% PRIOR; Y/Y: 2.8% V 2.6% PRIOR

(AU) AUSTRALIA MAY AIG PERF OF SERVICES INDEX: 51.5 V 53.0 PRIOR (3rd consecutive expansion. 3-month low

(SG) SINGAPORE MAY PMI COMPOSITE: 51.4 V 52.6 PRIOR

Asia Session Notable Observations

Asian indices slide despite the gains on Wall St as investors digest mixed US employment data on Friday. Outlook for June hike remains above 90%, though the case for 3 hikes total in 2017 stands more damaged by slow wage growth.

GBP down slightly in the wake of another terror attack in London that left 7 people dead; UK polls ahead of June 8th elections also continue to tighten.

China May Caixin Services PMI hits a 4-month high and Composite rises slightly. Among Services components, expansion in new orders was the most marked in the year-to-date, employment continued to increase but at slower pace, and input price inflation picked up from 6-month lows.

China Shenhua (China's largest coal miner) speculated to merge with GD Power Development; Both halted on A-shares.

World Bank maintained 2017 global GDP growth forecast at 2.7% and 2018 at 2.9%; WB also cut US by 0.1pt, Affirmed China at 6.5%, and raised EU and Japan by 0.2pts and 0.6pts respectively, citing recovery in industrial and a pick-up in global trade.

Oil rises nearly 1.5% on Saudi-Qatar spat. Saudi Arabia, Bahrain, and Egypt reportedly cut diplomatic relations after leaked tape where Qatari Emir Tamim bin Hamad al-Thani criticized Gulf rhetoric against Iran. Qatar also alleged to have provided assistance to terrorist organizations.

Speakers and Press

China

(CN) China Securities Regulatory Commission (CSRC) rejected IPO application from 9 out of 64 companies in May - Chinese press

(CN) China Securities Regulatory Commission (CSRC) announced new rules to curb disorderly stock sales

(CN) China Securities Regulatory Commission (CSRC) announced new rules to curb disorderly stock sales

(CN) China to accelerate approvals for green car subsidies, approving ~300 more green energy vehicle models to receive subsidies - Chinese press

(CN) China plans to continue its restructuring of SOEs in the coal power and steel sectors – Chinese Press

Japan

(JP) BoJ approx doubles ETF holdings in 1 year to ¥15.9T v ¥8.83T y/y - Nikkei

Australia/New Zealand

(AU) Australia's Queensland has commissioned an energy security taskforce to ensure state’s power system is secure during peak demand over 2017-18 and 2018-19 summers

Asian Equity Indices/Futures (00:30ET)

Nikkei flat, Hang Seng -0.3%, Shanghai -0.5%, ASX200 -0.7%, Kospi +0.1%

Equity Futures: S&P500 -0.1%; Nasdaq -0.1%, Dax closed, FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1265-1.1285; JPY 110.30-110.65; AUD 0.7420-0.7460; NZD 0.7115-0.7145; GBP 1.2855-1.2875

June Gold +0.3% at 1,284/oz; July Crude Oil +1.3% at $48.26/brl; July Copper -0.5% at $2.56/lb

SPDR Gold Trust ETF daily holdings rise 3.5 tonnes to at 851 tonnes; first rise since May 22nd

iShares Silver Trust ETF daily holdings fall to 10,601 tonnes from 10,605 tonnes prior; 3rd straight decline

(SA) Saudi Arabia, Bahrain, and Egypt said to have cut diplomatic relations with Qatar after leaked tape where Qatari Emir Tamim bin Hamad al-Thani criticized Gulf rhetoric against Iran; July WTI crude oil rises 1.5% above $48.35/brl

(US) Weekly Baker Hughes US Rig Count: 916 v 908 w/w (+0.9%) (20th straight weekly rise)

(CN) PBOC SETS YUAN MID POINT AT 6.7935 V 6.8070 PRIOR; 4th straight firmer Yuan fix; Strongest Yuan fix since Nov 10th

(CN) PBOC to inject combined CNY70B v CNY50B prior

(AU) Australia Finance Ministry (AOFM) sells A$400M in 3.25% 2029 bonds; avg yield 2.5171%; bid-to-cover 4.16x

(KR) South Korea sells 3-yr Govt bonds; avg yield 1.65%

Asia equities/Notables / movers

Australia

Fortescue (FMG) +0.3%; CEO: China steel demand remains strong

Tatts (TTS) -0.7%; ACCC not satisfied Tabcorp/Tatts merger is in best interest of public - AFR

Sirtex (SRX) -2.3%; Presents Phase 3 data from SIRVENIB study

Hong Kong

China Gas Holdings (384) +2.4%; Guides FY17

Guangzhou R&F Properties (2777) +0.5%; May sales

China Vanke (2202) -0.7%; May sales

IPE Group Limited (929) -1.5%; Guides Jan-Apr

Japan

Eisai (4523) +1.9%; Further Study of Combination of Eisai's Lenvatinib and Merck's Pembrolizumab in Previously Treated Patients with Metastatic Endometrial Cancer Supported by Interim Analysis of Ongoing Phase1b/2 Trial

ANA (9202) +0.3%; ANA and JAL to cut international route fuel surcharges by 50% in Aug - Japanese Press

Toshiba (6502) -0.6%; Foxconn Chairman: We have backing from Apple and Amazon in bid for Toshiba's memory chip unit - Nikkei

Trade Idea : GBP/USD – Stand aside

GBP/USD - 1.2871

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2870

Kijun-Sen level : 1.2875

Ichimoku cloud top : 1.2875

Ichimoku cloud bottom : 1.2845

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As sterling has remained confined within recent established range, retaining our view that further consolidation below indicated resistance at 1.2921 would be seen and weakness to 1.2845-46 (current level of the lower Kumo and Friday’s low) cannot be ruled out, however, break of 1.2830 support is needed to signal the rebound from 1.2769 has ended, bring further fall to 1.2800 but said support at 1.2769 should remain intact.

On the upside, above 1.2905 would bring another test of 1.2921-26 (resistance and previous support), however, break there is needed to signal low has been formed at 1.2769, bring further gain to 1.2940-45 (61.8% Fibonacci retracement of 1.3048-1.2769) and later towards 1.2970 but overbought condition should cap upside below 1.3000. As near term outlook is mixed, would be prudent to stand aside for now.

Trade Idea : EUR/USD – Hold long entered at 1.1205

EUR/USD - 1.1263

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1273

Kijun-Sen level : 1.1245

Ichimoku cloud top : 1.1221

Ichimoku cloud bottom : 1.1211

Original strategy :

Bought at 1.1205, Target: 1.1305, Stop: 1.1225

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1225

New strategy :

Hold long entered at 1.1205, Target: 1.1305, Stop: 1.1235

Position : - Long at 1.1205

Target : - 1.1305

Stop : - 1.1235

As euro has eased after marginal rise to 1.1285, suggesting minor consolidation below this level would be seen, however, reckon the Kijun-Sen (now at 1.1245) would hold and bring another rise later, above said resistance at 1.1285 would extend recent upmove to another previous chart resistance at 1.1300, break there would encourage for headway to 1.1340-45 but overbought condition should limit upside to chart point at 1.1366.

In view of this, we are holding on to our long position entered at 1.1205. Only below support at 1.1202 would abort and signal top is formed instead, risk weakness towards indicated support at 1.1164, once this level is penetrated, this would signal recent upmove has ended, bring further fall to 1.1130-40 first.

Trade Idea : USD/JPY – Sell at 111.00

USD/JPY - 110.58

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 110.52

Kijun-Sen level : 110.99

Ichimoku cloud top : 111.41

Ichimoku cloud bottom : 111.10

New strategy :

Sell at 111.00, Target: 110.00, Stop: 111.35

Position : -

Target : -

Stop : -

As the greenback has recovered after marginal fall to 110.31, suggesting consolidation above this level would be seen and corrective bounce to 110.80 cannot be ruled out, however, reckon the Kijun-Sen (now at 110.99) would limit upside and bring another decline later, below said support at 110.31 would extend recent decline to previous support at 110.24 but break there is needed to provide confirmation that early selloff from 114.37 top has resumed for weakness to 109.90-00 first.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 111.00 should limit upside. Only above the upper Kumo (now at 111.41) would abort and signal low is formed, bring another bounce towards Friday’s high of 111.71.

UK General Election And James Comey Due To Testify To The Senate

Market movers today

We face an important week in terms of the economic data calendar. Not least, Thursday will bring a key session with the ECB meeting, the UK general election and James Comey due to testify to the senate.

In the US, the final figures for PMI services for May and core capital goods orders for April are due out today. Services PMI increased to 54.0 in May, according to the preliminary numbers, whereas core capital goods orders were flat in April. This matches our view that progress is still being made in the services sector, but the manufacturing sector may be taking a breather for now. Today also brings ISM non-manufacturing for May, which has reached very high levels recently and may have run a bit ahead of itself.

In the UK, the PMI services index for May are due out today, which we estimate fell to 54.3 from 55.8. Focus will otherwise be on the polls as we approach Election Day on Thursday.

There are no significant market movers in Scandinavia today. The Danish and Norwegian markets are closed for Whit Monday today and that the Swedish market has half a day ahead of National day tomorrow.

Selected market news

In the US, Friday's nonfarm payrolls report did not live up to market expectations or even our own below-consensus estimates. With a disappointing headline print of 138,000 and negative revisions, it sent 3M average job growth to just 121,000 – the lowest level since 2012. The unemployment rate did drop 0.1pp but it was driven by a shrinking labour force. Irrespectively, at 2.5% y/y, wage growth seems to have lost momentum in recent months despite the lower unemployment rate.

For the Fed, subdued wage growth, low inflation and falling inflation expectations should be a concern amid weaker real data recently. However, while most of the latest FOMC speeches acknowledges this, they still indicate a forthcoming summer hike, which is probably why markets are still pricing in close to a 100% probability of a hike in June or July despite the disappointing non-farm payrolls report. Meanwhile, on release the USD index (i.e. DXY) fell to the lowest level since before the US presidential election. We think it is too early to position for a sustainable move higher in EUR/USD.

In the Middle East, Saudia Arabia, Bahrain, the UAE and Egypt have formed an alliance to block ties with Qatar. The alliance blames Qatar for supporting ‘terrorist groups aimed to destabilize the region'. The oil price has risen somewhat on the increased tension.

Danmarks Nationalbank (DN) FX reserve and central bank balance sheet numbers for May were broadly unchanged to those from April. Hence, DN did not need to intervene ahead of the second round of the French election as EUR/DKK traded close to 7.44 for most of the month. The next focus for the DKK market will be this week's meeting of the ECB, where the market will look for changes to the ECB's forward guidance (not our main scenario, see Fixed Income Markets on page 2). We forecast EUR/DKK at 7.4400 in 3-12M and for DN to keep its key policy rate unchanged at -0.65% on 12M.

Australia’s Services Sector Growth Slowed In May

For the 24 hours to 23:00 GMT, the AUD rose 0.81% against the USD and closed at 0.7441 on Friday.

LME Copper prices declined 1.37% or $77.0/MT to $5559.5/MT. Aluminium prices declined 0.70% or $13.5/MT to $1916.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7454, with the AUD trading 0.17% higher from Friday's close.

Overnight data showed that the AiG performance of services index fell to 51.5 in May in Australia, from a level of 53.0 reported in the last month.

Elsewhere, in China, Australia's largest trading partner, the Caixin services PMI rose to a level of 52.8 in May from 51.5 recorded in the previous month, its fastest pace of expansion in four months, amid an increase in new orders.

The pair is expected to find support at 0.7400, and a fall through could take it to the next support level of 0.7345. The pair is expected to find its first resistance at 0.7483, and a rise through could take it to the next resistance level of 0.7511.

Moving forward, investors will closely await the outcome of the Reserve Bank of Australia's monetary policy meeting, scheduled to take place tomorrow.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s PPI Remained Unchanged In April

For the 24 hours to 23:00 GMT, the EUR rose 0.59% against the USD and closed at 1.1283 on Friday.

On Friday, macroeconomic data showed that the producer price index (PPI) in the Euro-zone remained flat on a monthly basis In April, less than market expectations for a rise of 0.2%. In the prior month, the PPI had registered a drop of 0.3%. On the other hand, producer prices gained 4.3% year-over-year in April across the region, faster than the 3.9% rise in March. Analysts had expected a 4.5% increase for the month.

Meanwhile, Greece's economy expanded by 0.4% in the first quarter of 2017 compared with the fourth quarter of last year, revising upwards a previous preliminary estimate provided in May that showed a 0.1% fall. Following the release of positive GDP growth data, the Greek government urged for a clear solution regarding the debt load issue at the upcoming EuroGroup meeting on 15 June.

The greenback traded lower against its counterparts following the release of the weaker than expected US jobs report. Non-farm payrolls in the nation rose less than expected by 138.0k in May, after climbing by a downwardly revised 174.0k jobs in the previous month, thus raising concerns about the health of the US economic growth and the pace of the Federal Reserve's (Fed) plans to raise interest rates this year. Markets had anticipated an increase of 182.0k jobs. However, the nation's unemployment rate dropped to 4.3%, its lowest level since 2001. Meanwhile, the US average earnings rose 2.5% in May from the previous year, which was below market expectations of 2.6% gain but matched the 2.5% rate in April.

Further, the US trade deficit widened more than expected to $47.6 billion in April, compared to a revised trade deficit of $45.3 billion in the previous month. Market anticipation was for the nation to post a trade deficit of $46.1 billion.

Moreover, Philadelphia Fed Bank President Patrick Harker reiterated his support for two more interest rate hikes this year, stating that the US inflation remains on track to meet the Fed's 2.0% target. However, he commented that the biggest risk to the US economy is the uncertainty over Donald Trump's economic policies.

In the Asian session, at GMT0300, the pair is trading at 1.1273, with the EUR trading 0.09% lower from Friday's close.

The pair is expected to find support at 1.1224, and a fall through could take it to the next support level of 1.1174. The pair is expected to find its first resistance at 1.1304, and a rise through could take it to the next resistance level of 1.1334.

Going ahead, investors will focus on the Euro-zone's final services and composite PMIs, both for May, scheduled to release later in the day. Moreover, the US ISM non-manufacturing PMI and Markit services PMI data, both for the month of May, along with durable goods orders and US factory orders data for April, will be closely watched by traders.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

UK’s Construction Sector Activity Unexpectedly Rose To A 17-Month High Level In May

For the 24 hours to 23:00 GMT, the GBP marginally declined against the USD and closed at 1.2881 on Friday.

On Friday, data showed that the UK construction PMI unexpectedly climbed to a level of 56.0 in in May, expanding at its fastest rate in 17 months, as low interest rate and strong labour markets underpinned residential building activity. Market had expected the index to fall to 52.6, after it registered a level of 53.1 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2864, with the GBP trading 0.13% lower from Friday's close.

The pair is expected to find support at 1.2839, and a fall through could take it to the next support level of 1.2813. The pair is expected to find its first resistance at 1.2897, and a rise through could take it to the next resistance level of 1.2929.

Ahead in the day, Britain's services sector activity data for May, would be closely assessed by market participants for further direction in the local currency.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japan’s Services Sector Expanded At Its Fastest Pace In Almost 2 Years In May

For the 24 hours to 23:00 GMT, the USD declined 0.89% against the JPY and closed at 110.40 on Friday.

On Friday, data showed that Japan's consumer confidence index rose to 43.6 in May, compared to a reading of 43.2 reported in the previous month.

In the Asian session, at GMT0300, the pair is trading at 110.55, with the USD trading 0.14% higher from Friday's close.

Overnight data indicated that Japan's services PMI rose to a level of 53.0 in May from a reading of 52.2 recorded in the prior month, boosted by a sharp increase in new work, thereby providing further evidence that demand in the world's third-largest economy is picking up.

The pair is expected to find support at 110, and a fall through could take it to the next support level of 109.46. The pair is expected to find its first resistance at 111.40, and a rise through could take it to the next resistance level of 112.26.

With no additional economic data in Japan today, investors will now assess global macroeconomic events.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.