Sample Category Title

Trump Becomes Gold’s Best Friend

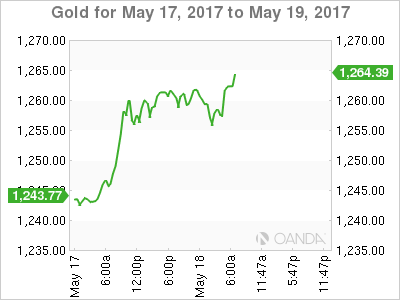

Gold swiftly regained its safe haven lustre on Wednesday after wave upon wave of uncertainty swirling around Donald Trump weathered risk sentiment. Concerns have skyrocketed over the current political turmoil in the United States obstructing Trump's efforts to implement his pro-growth policies, which simply punished the US Dollar. With expectations of an interest rate increase in June by the Federal Reserve slowly diminishing amid the soft economic data, Gold should find itself supported moving forward. Although uncertainty remains Gold's best friend, this spot could be temporarily replaced by Trump as his administration comes under increasing pressure. From a technical standpoint, Gold has staged a remarkable rebound on the daily charts and a break above $1260 should open a path towards $1275.

Is OPEC losing its grip?

Oil prices descended back into the abyss on Thursday as markets remained saturated despite OPEC's valiant efforts to cut production and support prices. Although US Crude oil inventories fell for a sixth-straight week, the decline was less than expected, which simply added to oversupply woes. Although investors previously displayed some optimism over Russia and Saudi Arabia agreeing that supply cuts should be extended until March 2018, this seems to have worn off. The OPEC vs US Shale saga feels like a fierce battle of attrition with the victor taking the spoils. While most remain optimistic over OPEC extending the production deal at the upcoming meeting on May 25, it becomes a question of how US Shale reacts and if pumping intensifies.

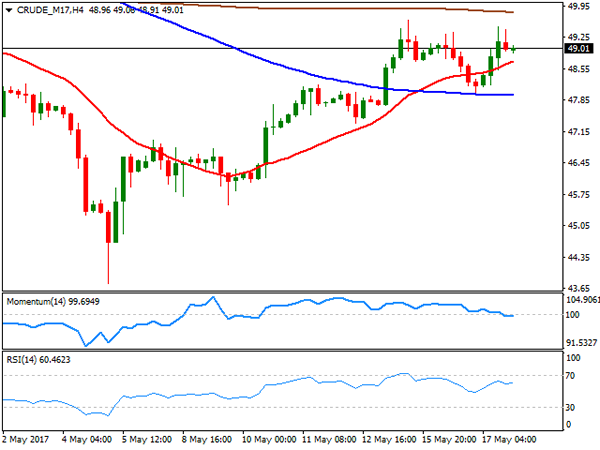

WTI Crude is under selling pressure on the daily charts. Repeated weakness and a daily close below $48 should encourage a depreciation towards $46.50.

Dollar pressured ahead of Unemployment Claims

The Greenback has received a thorough pummelling this week with prices sinking to levels not seen since November 2016 as the Trump uncertainty intensifies. Bears have exploited the fading optimism over the implementation of Trump's pro-growth policies by initiating repeated rounds of selling on the Greenback. While investors may direct their attention towards the unemployment report this afternoon, the Trump developments remain a dominant theme. If US unemployment claims disappoint and fall below expectations, the Dollar should be at risk of depreciating even lower.

Lame Duck Scenario Has Dollar On Defense

Investor bets that President Trump's policies would boost growth and inflation has been unwinding for months, but, those moves have intensified this week.

Global stocks, the mighty U.S dollar and government bond yields have been under pressure as investors pull back from their bets on the swift passage of the Trump administration's agenda.

Despite Trump continuing to hold the support of most Republicans, the market is becoming increasingly concerned that deeper cracks could emerge.

Since yesterday, the flight from risk assets has managed to send the VIX +30% higher, and trading a tad shy of +16, has filled the gap made into the French election.

It's not just the political anxiety, but combined with some softer U.S data of late – retail sales and inflation – is lowering the odds of a June rate hike.

1. Stocks take their cue from Wall Street

Equities in Asia followed the U.S lead, where the Dow and S&P 500 both sinking about -1.8% yesterday following reports that Trump tried to influence a federal probe.

In Japan, the Nikkei fell to a three-week low, falling -1.3%, as worries over Trump allegations offset a strong preliminary GDP for Q1 (+0.5%). The broader Topix saw similar pressure, falling -1.4%.

In Hong Kong, the Hang Seng Index fell -0.7% while the Hang Seng China Enterprises Index retreated -1.2%.

Down-under, the Australia's S&P/ASX 200 Index lost -0.8% despite a stronger Aussie employment change (+37.4k vs. +5k).

In Europe, ahead of the U.S open, regional indices trade modestly lower across the board with the FTSE 100 leading the decliners, basically shadowing U.S losses.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.8% at 3220, FTSE -1.2% at 7415, DAX -0.7% at 12539, CAC-40 -0.9% at 5268, IBEX-35 -1.3% at 10645, FTSE MIB -1.7% at 20915, SMI -0.9% at 8922, S&P 500 Futures -0.1%.

2. Oil down, as market stays well supplied, gold loses some shine

Oil prices are a tad lower on news that the market remains well supplied with crude despite efforts by OPEC to curb production and support prices.

Brent crude is down -17c at +$52.04 a barrel, while U.S light crude oil (WTI) is -16c lower at +$48.91.

Both benchmarks rose yesterday after news of a drawdown in U.S crude inventories and a dip in U.S output.

Note: The U.S. EIA said inventories fell -1.8m barrels in the week to May 12 to +520.8m barrels.

OPEC ministers meet in Vienna on May 25 to decide production policy for the next six-months. The market is expecting producers to prolong their agreement to limit production, perhaps by up to nine-months.

Heading into the U.S session, gold prices are a tad weaker (-0.2% at +$1,258.02 per ounce) after touching its two-week high overnight, mostly weighed down by profit taking.

The yellow metal rose about +2% yesterday, its biggest one-day percentage gain in 12-months.

3. U.S. Bond Yields Sink on Political Jitters

This week's safe haven demand has pushed down the yield on U.S 10's to trade well below the psychological +2.30% handle. Yesterday, the yield touched its lowest intraday level in four-week at +2.23%.

Currently the odds that the Fed will raise its benchmark rate next month are about +63%, based on the current effective fed funds rate. That's down from +83% before last Friday's retail sales and inflation reports.

The odds that the Fed moves in September are also on the decline. Fed fund futures are not pricing in a full hike until November.

Elsewhere, Australian benchmark yields fell -3 bps to +2.50%, while benchmark yields in France (+0.79%) and Germany (+0.32%) were little changed after dropping six basis points in yesterday's session.

4. Lame duck scenario has dollar on defense

The political mess that has engulfed the Trump Administration continues to pressure the ‘mighty' USD. Even market concerns about the momentum of the U.S economy is contributing to this week's downfall across the board.

Despite the dollar's small reprieve or consolidation (€1.1123, ¥110.46) heading into this morning's session, there is a potential that the USD could see further weakness if the market believes the situation could evolve into a possible “lame duck” environment.

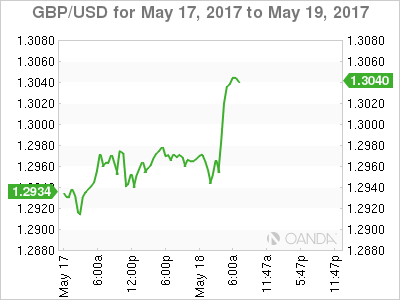

Better retail sales data from the U.K (see below) has helped push the pound (£1.3047) through the psychological £1.3000 handle for the first time in eight-months. To many, £1.3000 is the key pivot and now a lot of the structural shorts out there post-Brexit will be looking to wind back. Short-term sterling bulls are now targeting £1.3350/1.3400.

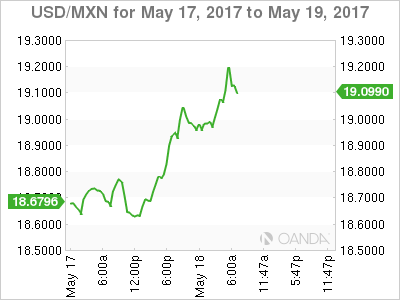

Elsewhere, MXN has fallen by over -2% overnight as a proxy for BRL as the Brazilian President gets embroiled in a corruption scandal.

5. UK Retail Sales Rebound in April

U.K data this morning sees retail sales rebounded last month – +2.3% m/m vs. +1.5% e – following a steep quarterly decline in Q1. The stronger print would suggest that the U.K economy has begun Q2 on a stronger footing.

Note: Compared with April last year, sales were +4.0% higher versus and expected +2.3% growth.

Accelerating inflation and low wage growth has weighed heavily on consumer spending in Q1, causing the whole economy to slow significantly.

Data this week showed U.K inflation hitting a three-year high of +2.7% in April, the third consecutive month of above-target price growth. The BoE expects inflation to peak at around +2.8% later this year, and gradually return to their +2% target afterwards.

Also in the U.K. today, the Conservative Party is expected to launch their election manifesto.

Risk Aversion Remains On Trump Concerns

- Europe playing catch up but US facing another tough session;

- Technical factors contributing to sell off, indices remain range-bound;

- UK retail sales rebound strongly in April sending GBPUSD above 1.30.

Risk aversion is rife once again in the markets on Thursday, with the brewing political storm surrounding President Donald Trump in the US largely being blamed for the moves.

Europe is partly playing catch up today, with indices deep in negative territory, but sentiment is far from improved, as seen by US futures which are pointing to another rough open. Prior to yesterday's open, major indices in the US were trading very close to their record highs, levels that have only been achieved on the belief that Trump will deliver on his tax reform and spending pledges. While I don't believe at this stage that these reports regarding Trump will jeopardise his agenda, markets must reflect the challenges he now faces which ultimately make it more difficult. At the very least, this distraction may delay the implementation of his plans which the markets won't like.

While the sell-off in risk markets is largely being attributed to the political circus in the US, I do think there's a technical element at play here as well. Prior to yesterday, the S&P had traded in a tighter range for the last few weeks between 2,380 and its highs, while the Dow had done similar between 20,800 and its highs. A break below these levels has likely triggered more selling which has contributed to the fear that we're currently seeing in the markets. As long as the S&P stays above 2,320 and the Dow above 20,400 - meaning both indices remain in their three month ranges – then I don't think there's anything to be concerned about. As long as this remains the case, it would suggest that what we're seeing is nothing more than consolidation while we await further progress on taxes and spending. A break below here may signal something more concerning.

It's not all bad news today, particularly for the UK which has already had a mixed bag of numbers this week. Yesterday we learned that while unemployment has fallen to its lowest level in more than 40 years, wages are falling in real terms thanks to subdued wage growth and higher inflation. Today we got the latest retail sales report which comes following the worst quarter of spending since 2010. Not only did we see a rebound in April but it would appear the nicer weather sent people to the shops in droves, with sales rising 2.3% from March – more than double what was expected – and 4% from a year ago. While these numbers will come as a relief, I don't think one good month in isolation is worth getting carried away with, not given the near-term outlook for real wage growth and the impact that often has on spending.

Still, the numbers did give a boost to the pound which has seen it break above 1.30 against the dollar for the first time since September last year. Should the pair hold above here today, it could signal significant further upside in the pair in the coming weeks and months. Of course, sterling is always going to be vulnerable to Brexit related news, but should we see a calm few months on this front and the data continue to perform relatively well, then we could see the pair trading back toward 1.35. Of course, this will also depend on how things develop in the US and whether the Fed follows through on rate hike plans, but there's certainly scope for upside in the pair which prior to this was pricing in a relatively dire scenario in the UK and quite the opposite across the pond.

The focus today is likely to remain on developments relating to Trump. On the data side we'll get jobless claims from the US, while ECB President Mario Draghi is due to speak, as is the Fed's Loretta Mester, a voter on the FOMC in 2018.

Technical Outlook: AUDUSD – Risk Of Recovery Stall In Play After Short-Lived Spike Above 0.7440 Pivot

The Aussie spiked above strong barrier at 0.7440 on Thursday after Australian unemployment fell to four-month low at 5.7% in April and 37.4K new jobs added that heavily beat forecast for 5.0K rise.

The pair rallied to fresh over two-week high at 0.7464 on solid data, but gains were so far short-lived and capped just under strong barrier provided by daily Kijun-sen line. Subsequent pullback below 0.7440 pivot put pressure on lower trigger at 0.7400 zone, signaling risk of reversal on break lower.

With overall bias being with bears and daily slow stochastic reversing from overbought zone, risk of recovery rally stall increases.

Yesterday's long-legged Doji signaled indecision, with today's action being so far in the same shape that would signal that recovery phase from 0.7327 low is running out of steam.

Firm break below 0.7400 pivot (reinforced by daily Tenkan-sen / 10SMA would generate stronger reversal signal.

Meantime, the pair may spend some time in extended consolidation between daily Tenkan-sen and Kijun-sen boundaries, before establishing in fresh direction.

Firm break above daily Kijun-sen pivot will be bullish.

Res: 0.7444, 0.7467, 0.7500, 0.7544

Sup: 0.7406, 0.7395, 0.7376, 0.7364

Daily Technical Analysis: AUD/USD Bullish Wicks Mark New Wave Of Buyers

The AUD has been rebounding of late, with stronger Employment numbers for the month and a reduction in the Unemployment Rate to 5.7% as it approaches full employment. Interestingly, the MI Inflation target is 4% for the next 12 months, which may signal rate hikes in the near future. USD weakness continues, and the USD Index looks destined a bit lower, with lower manufacturing numbers, but with all other indicators relatively stable, the concerns lie with whether Trump can now deliver on his Tax cut promises for the next boost to the US economy.

The AUD/USD is getting close to the POC zone (61.8, D L3, ATR,EMA89) within 0.7415-25. The interim bullish outlook is further supported by bullish wicks (blue highlight) that mark historical buyers. Now moment buyers could appear exactly there and the wicks are in confluence with the POC zone. We can also notice an ascending trend line. Target for the move is 0.7485 D H5 / W H5 confluence.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Market Update – European Session: UK Retail Sales Beat, More Allegations On Trump’s Russia Ties

Notes/Observations

Risk aversion simmering as dealers ponder whether Trump’s situation could evolve into a possible lame duck environment.

Brazil President on the ropes with calls for his resignation

UK Apr retail sales beats; GBP currency tests above 1,30 for 1st time since Sept

Overnight:

Asia:

Japan Q1 Preliminary GDP registers its 5th consecutive quarter of growth for the first time in over a decade (:Q/Q 0.5% v 0.5%e; Annualized GDP: 2.2% v 1.7%e)

BOJ Dep Gov Iwata: No decision on how the BoJ will exit their ultra-loose policy

China Apr Property Prices continue to cool amid a continuing crackdown on real estate speculation. ( M/M: rise in 58 of 70 cities vs. 62 prior

Australia Apr Employment Change rises for the 2nd straight month and outs in its best two-month performance since late 2015 (+37.4K v +5.0Ke); Unemployment rate at a 3-month low (5.7% v 5.9%e)

Europe:

EU plans to introduce stronger powers for securities regulator ESMA to boost capital market integration

Ireland PM Kenny confirms plan to resign; effective May 18th; successor to be appointed June 2nd

UK PM May will reportedly pledge to wipe out UK deficit by 2025; to allow for a borrowing increase to support economy during Brexit run-up

Americas:

Justice Dept names former FBI Director Mueller as special counsel to take over Russia probe

President Trump: Thorough investigation will confirm what we already know, there was no collusion between my campaign and any foreign entity

Brazil President Temer: Never asked for payments linked to former House Speaker Cunha

Economic Data

(NL) Netherlands Apr Unemployment Rate: 5.1% v 5.0%e

(FR) France Q1 ILO Unemployment Rate: 9.6% v 10.0%e; ILO Mainland Unemployment Rate: 9.3% v 9.6%e

(CN) China Apr Foreign Direct Investment (FDI) Y/Y: -4.3% v +6.7% prior

(TR) Turkey May Consumer Confidence Index: 72.8 v 70.8e

(ID) Indonesia Central Bank left its 7-Day Reverse Repo Rate unchanged at 4.75% (as expected)

(UK) Apr Retail Sales (Ex-auto/fuel) M/M: 2.0% v 1.0%e; Y/Y: 4.5% v 2.6%e

(UK) Apr Retail Sales M/M: 2.3% v 1.1%e; Y/Y: 4.0% v 2.1%e

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €4.77B vs. €4.0-5.0B indicated range in 2020, 2024, 2026 and 2027 Bonds

Sold €1.62B in 1.15% July 2020 SPGB, Avg yield -0.142% v +0.606% prior, bid to cover 1.44x v 2.24x prior

Sold €0.7B in 4.8% Jan 2024 SPGB; Avg Yield 0.777% v 1.157% prior; Bid-to-cover: 2.21x v 4.35x prior

Sold €1.26B in 5.90% 2026 SPGB; Avg Yield 1.370% v 1.043% prior; Bid-to-cover: 1.71x v 1.90x prior

Sold €1.19B in 1.5% Apr 2027 SPGB; Avg yield: 1.548% v 1.683% prior; Bid-to-cover: 1.43x v 1.55x prior

(FR) France Debt Agency (AFT) sold total €7.499B vs. €6.5-7.5B indicated range in 2020 and 2022 Oats

Sold €4.197B in 0.00% Feb 2020 Oat; Avg Yield: -0.45% v -0.32% prior; Bid-to-cover: 2.10x v 1.67x prior

Sold €3.302B in 0.00% May 2022 Oat; Avg yield: -0.12% v +0.09% prior; Bid-to-cover: 1.86x v 1.96x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.8% at 3220, FTSE -1.2% at 7415, DAX -0.7% at 12539, CAC-40 -0.9% at 5268, IBEX-35 -1.3% at 10645, FTSE MIB -1.7% at 20915, SMI -0.9% at 8922, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes

European indices trade modestly lower across the board with the FTSE MIB and FTSE 100 leading the decliners with concerns over President Trump said to weigh on markets. US Indices posted the worst decline since the US election yesterday, with futures continuing the down move eradicating overnight gains to trade down on the day. On the corporate front Royal Mail and Burberry posted better then expected results, Merck Kgaa shares are lower after Net profit fell for the year. Berendsen is the leading riser after an increased offer from Elis SA, with shares of Grammer down over 4% after its Chairman said order in take halved, due to dispute with Hastor family. Looking ahead to the US morning, notable earners include Alibaba, Retail giant Walmart as well as fashion retailer Ralph Lauren.

Equities

Consumer discretionary [ Burberry [BRBY.UK] +2.1% (Earnings), - Berendsen [BRSN.UK] +24%, ELIS [ELIS.FR] -5% (Increased takeover offer from ELIS), Grammer [GMM.DE] -4.7% (Order intake halves)]

Industrials: [Royal Mail [RMG.UK] +1.4% (Earnings)]

Financials: [Caixabank [CABK.ES] -2.4% (Reportedly will report Q2 loss)]

Technology: [Wirecard [WDI.DE] -3.7% (Earnings)]

Telecom: [Altice [ATC.NL] -2% (EU alleges breached EU rules by early implementation of PT Portugal acquisition), Iliad [ILD.FR] -2.2% (Earnings)]

Healthcare: [Merck [MRK.DE] -1.3% (Earnings)]

Speakers

ECB's Coeure (France): ECB guidance must stay in line with facts.At the moment, there were no grounds and no merit for changing the sequence. Future policy path is "not set in stone"; sequence of policy can be changed.

ECB's Weidmann (Germany): Governing Council to decide in Dec on market infrastructure steps

ECB's Jazbec (Slovenia): Too soon to announce any policy changes

ECB's Vasiliauskas (Lithuania): Policy makers not ready to unwind QE. Council should start reviewing its pledge for continued, ultra-easy policy if economic data confirmed the rebound in inflation is here to stay. Current guidance should be maintained; policy path should be predictable as possible. Did not see rate hikes before end of QE bond buying program

Brazil govt allies said to seek resignation of President Temer

Advisers to Donald Trump’s campaign had at least 18 calls and emails with Russian official during the last seven months of the 2016 presidential race (press reports). Six of the previously undisclosed contacts described to Reuters were phone calls between Kislyak and Trump advisers, including Flynn, Trump’s first national security adviser

Indonesia Central Bank Policy Statement Maintains neutral policy while monitoring inflation and likelihood of a Fed rate hike in June maintained its 2017 GDP growth between 5.0-5.4% range and inflation forecast between 3.0-5.0% (seen inside target). Saw exports and investments supporting growth. Reiterated view to stabilize IDR currency (Rupiah) to be in-line with fundamentals with inflows and sovereign rating to support IDR currency

Currencies

The political morass that has engulfed the Trump Administration has helped to weaken the USD in the past few sessions complemented by concerns about the momentum of the US economy following the recent disappointment data. Dealers note that the potential risk for further USD weakness could emerge if markets start to believe the situation could evolve into a possible lame duck environment. The European morning price action had the greenback consolidated some of its recent losses

Better retail sales data from the UK helped the GBP/USD pair move above 1.30 handle for its highest level since Sept

Fixed Income

Bund futures trade at 161.82 up 33 ticks, breaking above last week’s high of 160.99. Initial resistance comes from the 162.01 level followed by 163.68. A break of 160.01 support level could see lows target 159.01 followed by 157.50.

Gilt futures trade at 128.82 higher by 18 ticks, as risk-off rally continued after the cash close yesterday before fading overnight. Initial resistance comes from the 129.14 April 18th high. Price finds key support at the 127.51 support level. An acceleration lower could test the 126.80 region. Resistance remains the 129.51 level then 130.28 followed the August 2016 high of 132.80.

Thursday’s liquidity report showed Wednesday’s excess liquidity was unchanged at €1.6510T. Use of the marginal lending facility fell to €97M from €191M prior.

Corporate issuance saw over $1.35B come to market via 3 issues headlined by Martin Marietta Materials $600M, 2-part senior note offering and Entergy Louisiana LLC $450M 10-year secured note offering.

Looking Ahead

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

05:30 (UK) DMO to sell £2.75B in 1.75% 2019 Gilts

05:30 (PL) Poland to sell PLN3.0B in 2019, 2022, 2026 and 2027 bonds

05:50 (FR) France Debt Agency (AFT) to sell €1.5-2.0B in Inflation-lined 2028, 2030 and 2047 bonds (Oatei)

06:00 (RO) Romania to sell 2.25% 2020 Bonds

07:00 (BR) Brazil May IGP-M Inflation (2nd Preview): -0.8%e v -1.0% prior

07:30 (EU) ECB account of Monetary Policy Meeting (May Minutes)

08:00 (PL) Poland Apr Employment M/M: 0.1%e v 0.1% prior; Y/Y: 4.5%e v 4.5% prior

08:00 (PL) Poland Apr Average Gross Wages M/M: -1.7%e v +6.3% prior; Y/Y: 4.4%e v 5.2% prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) May Philadelphia Fed Business Outlook: 18.5e v 22.0 prior

08:30 (US) Initial Jobless Claims: 240Ke v 236K prior; Continuing Claims: 1.95Me v 1.918M prior

08:30 (CA) Canada Mar Int'l Securities Transactions: No est v C$38.8B prior

08:30 (CL) Chile Q1 GDP Q/Q: +0.2%e v -0.4% prior; Y/Y: 0.2%e v 0.5% prior

08:30 (CL) Chile Q1 Current Account Balance: -$0.8Be v -$0.7B prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (BE) ECB's Mersch (Luxembourg)

08:45 (DE) ECB’s Lautenschaeger (Germany) in Berlin

09:00 (RU) Russia Gold and Forex Reserve w/e May 12th: No est v $398.8B prior

10:00 (US) Apr Leading Index: 0.4%e v 0.4% prior

10:00 Treasury Sec Mnuchin testimony

10:30 (SE) Sweden Central Bank (Riksbank) Jochnick

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (CO) Colombia Mar Trade Balance: -$0.8Be v -$0.8B prior; Total Imports: $4.1Be v $3.7Be

11:00 (BR) Brazil to sell 2023 LFT

11:00 (BR) Brazil to sell 2018, 2019 and 2020 LTN Bills

12:30 (DE) German Chancellor Merkel on digital economy

13:00 (EU) ECB’s Draghi in Israel

13:00 (US) Treasuries to sell 10-Year TIPS Reopening

13:15 (US) Fed's Mester (hawkish, non-voter) speaks on Economy and Monetary Policy

14:00 (MX) Mexico Central Bank (Banxico) Interest Rate Decision: Expected to leave Overnight Rate unchanged at 6.50%

18:00 (CL) Chile Central Bank (BCCh) Interest Rate Decision: Expected to leave Overnight Rate Target unchanged at 2.75%

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

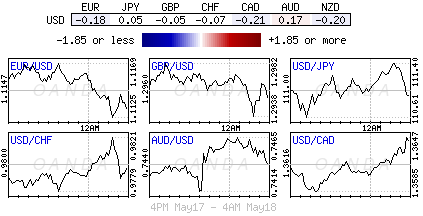

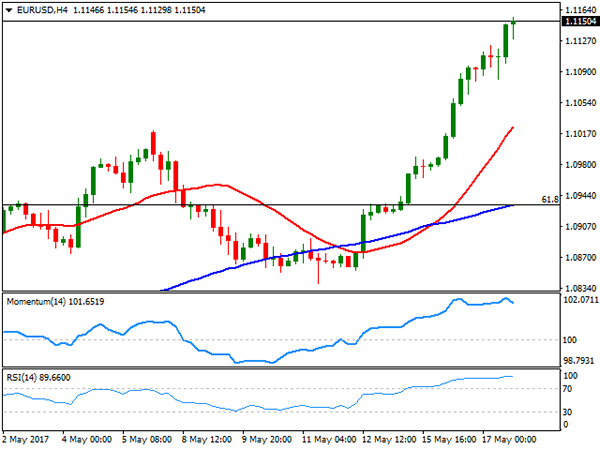

Risk aversion took its toll over the financial world this Wednesday, with US-related assets under heavy selling pressure amid Trump's latest scandals involving Russia. The American currency was threading water at the beginning of the day, but finally capitulated with Wall Street opening, with the Dow putting in a three-digit lost in the first minutes of trading. The EUR/USD pair corrected intraday down to 1.1081 before resuming its advance, reaching fresh yearly highs of 1.1149 during the American afternoon, holding nearby ahead of the daily close. Macroeconomic data had little to do with price action, as sentiment offset news. Nevertheless, once the dust settles the market will remember that European inflation remain at its highest ever since easing began in the region, rising at an annual pace of 1.9% in April. Monthly basis CPI was up by 0.4%, half the advance of March, but in line with market's expectations, lifting odds of sooner tapering in the EU.

The EUR/USD pair has now advanced straight for a fourth consecutive day, reaching overbought conditions in the daily chart, but with no signs that the ongoing advance has reached an interim top. In the 4 hours chart, technical indicators have eased modestly after reaching fresh extreme overbought readings, whilst the price stands far above bullish moving averages, also indicating that the rally may continue during the upcoming sessions. Wednesday's low at 1.1080 is the level where buyers will likely re-surge in the case of pullbacks, although the downward corrective move can extend down to 1.1000 without actually affecting the dominant bullish trend. Fresh highs will have bullish implications, with room then for an advance towards 1.1260.

Support levels: 1.1110 1.1080 1.1045

Resistance levels: 1.1160 1.1200 1.1260

USD/JPY

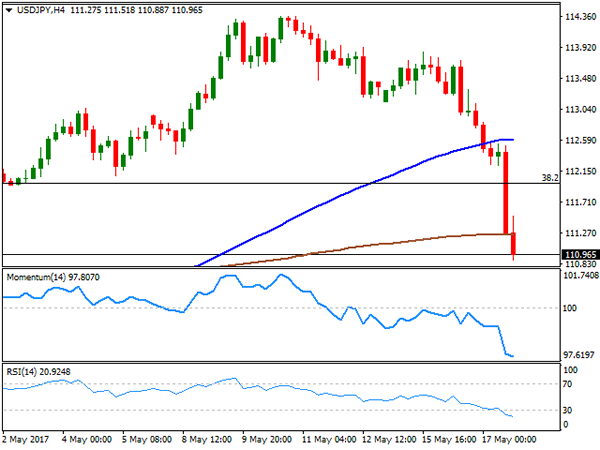

The USD/JPY pair shed whopping 200 pips this Wednesday, with the selling spiral accelerating early US session amid US political woes denting market's sentiment. Speculative interest rushed into safe-havens and away from the greenback on escalating concerns surrounding US President Trump's continuity, who is close to face an impeachment after new headlines saying that he pressed former FBI Director Comey to end an investigation on Michael Flynn, who was fired last February after it became known that he lied to Vice President Pence, on speaking with Russian Ambassador Kislyak about sanctions on Russia prior to Trump’s inauguration. The unstoppable decline in the pair persists into the Asian opening, despite extreme oversold conditions clear in intraday charts. Japan will release its Q1 preliminary GDP figures during the upcoming Asian session, but seems more likely that the pair will continue responding to risk sentiment. Technically, the 4 hours chart shows that the price has broken below its 100 and 200 SMAs, while technical indicators have barely decelerated within extreme oversold territory, with the RSI heading south around 20. The pair is at its lowest since late April, with an immediate support at 110.86, April's 26th low, with a break below it exposing 109.90, the 50% retracement of the November/December rally.

Support levels: 110.85 110.40 109.90

Resistance levels: 111.25 111.60 112.00

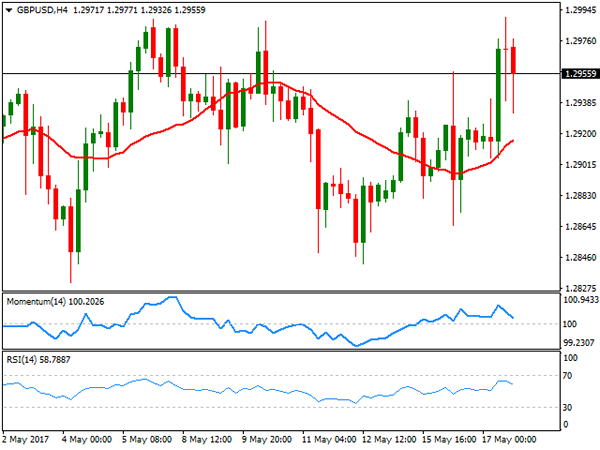

GBP/USD

Despite ending the day higher against its American rival, the British Pound was one of the few currencies that were unable to capitalize broad dollar's weakness. The GBP/USD pair peaked for the week at 1.2990, meeting once again strong selling interest just shy of the critical 1.3000 figure. In the data front, the UK released its latest employment figures which came in mixed. The unemployment rate fell to 4.6% in the three months to March, the lowest in over four decades, whilst the number of unemployed people fell by 53,000 to 1.54 million in the same period. Wages, however, increased by 2.1%, below market's expectations and lagging behind inflation for the first time in nearly three years. The UK will release its April retail sales this Thursday, expected to have increased by 1.0% in the month after March's 1.8% decline. From a technical point of view, and despite the inability of the pair to surpass the 1.3000 figure, the risk of a steeper decline is well limited by the absence of dollar's demand. Technically, the 4 hours chart presents a neutral stance, with the price above a modestly bullish 20 SMA, but with the Momentum indicator having pulled back to its mid-line, and the RSI indicator having turned lower, now around 58.

Support levels: 1.2900 1.2865 1.2830

Resistance levels: 1.2960 1.2995 1.3040

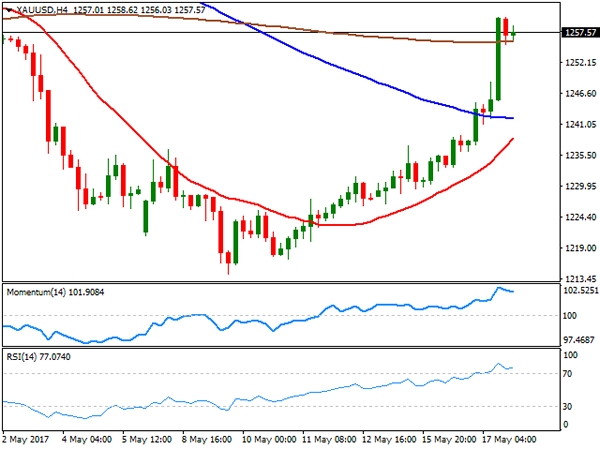

GOLD

Gold prices rallied to fresh May highs, with spot settling at $1,257.89 a troy ounce after flirting with 1,260.20 earlier in the day, as US political woes escalated to the point that US president Trump is near an impeachment, boosting demand for the safe-haven metal, as attention is now far from Central Bank's decisions. The commodity has broken above all of its moving averages in the daily chart that anyway remain flat, as the movement was quite abrupt, whilst technical indicators turned sharply higher, entering positive territory and suggesting a possible upward extension for the upcoming sessions, moreover if the political turmoil persist. In the shorter term, the 4 hours chart also favors additional gains, as technical indicators have barely pulled back within overbought territory before losing downward strength, whilst the price has settled above all of its moving averages, with the 20 SMA accelerating north, but still below the larger ones.

Support levels: 1,255.10 1,245.20 1,237.40

Resistance levels: 1,262.10 1,273.10 1,282.90

WTI CRUDE OIL

Crude oil prices recovered the ground lost on Tuesday, supported by better-than-expected market's news. West Texas Intermediate crude futures settled at $49.00 a barrel, after the EIA reported yet another decline in US crude inventories. Official figures showed that stockpiles fell by 1.8 million barrels in the week ended May 12th, the sixth consecutive weekly drop. Gasoline stockpiles also declined, by 400K barrels, while distillates fell by 1.9 million barrels. The US benchmark traded as high as 49.48 intraday, stalling its recovery below previous' weekly high of 49.64, as speculators are not fully convinced that this news will be enough to reduce the ongoing worldwide glut, neither latest OPEC comments pointing for a possible extension of their output cut deal until March 2018. Technically, the risk is however towards the upside, as in the daily chart, technical indicators have quickly turned north, still standing around their mid-lines, whilst an early decline met buying interest around a now horizontal 20 SMA, currently at 47.90. Shorter term, the 4 hours chart shows that indicators lack directional strength, with the Momentum stuck around 100, but the RSI aiming to regain the upside around 60 and the price holding above a bullish 20 SMA, all of which supports additional gains particularly on an advance beyond the mentioned weekly high.

Support levels: 48.70 47.90 47.20

Resistance levels: 49.65 50.20 50.80

DJIA

It was a bad day for equity traders, particularly for those in the US as the Dow Jones Industrial Average closed the day at 20,606.93, down by 372 points, while the Nasdaq Composite shed 2.57% or 158 points, to end at 6,011.24. The S&P fell by 43 points or 1.82%, to 2,357.03. It was the worst day for US indexes in this 2017, as the continuity of US President trump is close to be put on question, following the scaling scandals around inter-relationships with Russia. Within the Dow, financial-related equities suffered the most, with Goldman Sachs down 5.48% and JP Morgan shedding 4.04%. Only 5 members closed up, with UnitedHealth being the best performer with a measly 0.49% advance. The Dow fell to its lowest since April 21st, and holds near the mentioned close ahead of the Asian opening, with a strong bearish momentum in the daily chart supporting further declines for this Thursday, as technical indicators head sharply lower near oversold territory, whilst the index is currently aiming to break below its 100 DMA. In the 4 hours chart, technical indicators maintain their bearish momentum despite having entered oversold territory, whilst the index has broken below all of its moving averages.

Support levels: 20,602 20,557 20,503

Resistance levels: 20,688 20,732 20,797

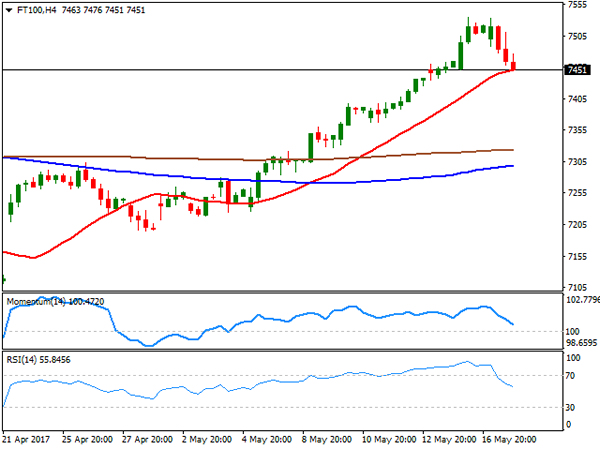

FTSE100

The FTSE 100 closed 18 points lower at 7,503.47, retreating from record highs on mounting risk aversion. Losses were limited as mining-related equities surged on gold demand, with Fresnillo being the top performer, adding 2.75% , and Randgold Resources up by 2.05%. Most members closed lower, with Ashtead Group being the worst performer by closing -3.82%, followed by CRH that shed 3.48%. The index fell further in after-hours trading heading into the Asian opening around 7,451. The Footsie trimmed most of its weekly gains, and the daily chart shows that technical indicators are pulling back sharply from overbought levels, supporting some additional declines. Still the index is holding far above bullish moving averages, keeping the longer term view far from bearish. In the short term and according to the 4 hours chart, the index is standing right around a bullish 20 SMA, whilst technical indicators present strong bearish slopes within positive territory, now approaching their mid-lines and in line with the longer term view.

Support levels: 7,435 7,402 7,363

Resistance levels: 7,476 7,500 7,533

DAX

The German DAX closed at 12,631.61, down by 170 points of 1.35%, with most European indexes falling by the most in nearly 9 months, on prospects the US president will be impeached for obstructing justice, on news indicating that he asked former FBI director Comey, before firing him, to drop the investigation on Michael Flynn. The scandals surrounding the Trump jeopardize his pro-growth agenda, forcing investors to unwind bets. Within the DAX just ThyssenKrupp managed to close in positive territory, adding 2.26%, whilst financials led the way lower, as Commerzbank shed 3.90% and Deutsche Bank 3.61%. The DAX fell further in after-hours trading, dragged lower by Wall Street's slump and currently around 12,540. The technical picture has turned bearish, as in the daily chart, the index is about to break below a bullish 20 SMA, whilst technical indicators have turned sharply lower, now pressuring their mid-lines. In the 4 hours chart, the decline accelerated below a now bearish 20 SMA, whilst technical indicators maintain their sharp bearish slopes near oversold territory.

Support levels: 12,534 12,485 12,440

Resistance levels: 12,593 12,629 12,666

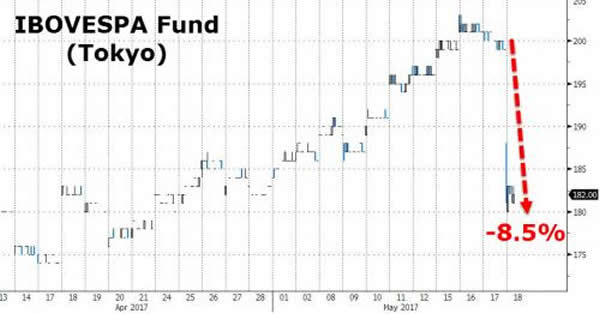

The Peso Gets Real In Asian Trading

Mexican Peso falls by over 2% in Asia as a proxy for the Brazilain Real as the Brazilian President gets embroiled in a corruption scandal.

It seems that Washington D.C. isn't the only centre of power to be enveloped in political scandals today, with President Michel Tenner apparently recorded endorsing bribes tosilence the now jailed former speaker, Eduardo Cunha, according to a story broken today by the O Globo newspaper. The tapes form part of a plea bargain arrangement by two of the owners of the world's largest meatpacker, BJS; itself engulfed in a corruption scandal for bribing officials, allegedly, to turn a blind eye to the export of tainted meat. President Tenner has only recently assumed the presidency, having got the job following the impeachment of his predecessor, Dilma Rousseff. You really couldn't make this up.

The story broke after North American markets had closed during the Asia morning. It has made those holding Brazilian assets or those wanting to short anything Brazilian's life a bit difficult. Brazil has a closed capital account, and the Real (BRL) is only able to be traded off-shore via the Non-Deliverable Forward market.

To put this in context to see just how seriously the street is taking these allegations, we need to look no further than the Next Funds Ibovespa Linked ETF which trades in Tokyo. It plunged 8.50% during the Tokyo trading day.

That leads us back to the Mexican Peso's two percent plus fall against the U.S. Dollar. As I said, there is basically no off-shore market for the Brazilain Real outside of North American trading hours. And like any emerging market, it can be a market you can't emerge from in an emergency. Traders have therefore reached for the nearest available currency that has some liquidity and can act as an approximate proxy for the Brazilian Real. Step forward the Mexican Peso.

It does seem rather unfair on Mexica, but I guess it is on the same continent is closer than Canada and has a free floating currency. The USD/MXN flew higher from 18.7650 to 19.1000 and is trading just below this level as we speak at 19.0750. The fact that it has remained at these levels could imply that there is a lot of somewhat desperate interest still out there looking to mitigate Brazilian risk.

In the process, today's USD/MXN rally has snapped a five-day cycle of MXN appreciation against the USD. The danger is of course that we could see a return to the mean, USD/MXN lower, once North American trading begins. Conversely, the USD/MXN rally could stay extended if liquidity does not appear in the U.S. session and interest remains one way. Investors may then also chose to buy the USD/South America NDF's of its neighbours instead.

Looking at the technical picture, USD/MXN has initial resistance at the day's highs of 19.1000. That is followed by the 26th of April high and also the 23.60% Fibonacci retracement at 19.29000. A break here, should it happen opens a move to the 19.6000/19.8000 region, the home of the 100 and 200-day moving averages.

Support is at the day's lows around 18.7650 followed by 18.6000. Long-term support rests at the 18.4000 level.

The Mexican Peso has assumed the role of the poor man's Real today following another alleged political scandal. It is perhaps a welcome break to be writing Sao Paolo instead of Washington D.C. As a proxy for the Real, the Peso maybe make back some of its losses once North America commences its day. However, should liquidity remain non-existent in the BRL, the Peso could remain under pressure along with its regional neighbours to the South as a proxy.

Euro Gains Ground As US Political Turmoil Intensifies

The euro has edged downwards in the Thursday session, after recording gains in the past three daily sessions. Currently, EUR/USD is trading at 1.1120. In the eurozone, there are no major economic events on the schedule. The president of the ECB, Mario Draghi, will speak at an event at the University of Tel Aviv. In the US, we'll get a look at unemployment claims and the Philly Fed Manufacturing Index.

The euro continues to gain ground, as EUR/USD has risen 1.7 percent this week and is currently trading at 6-month highs. The currency has received a boost from the growing political uncertainty which has gripped Washington. Facing relentless pressure from Democrats and some Republicans, the Justice Department has appointed a former FBI director as special counsel to investigate possible Russian involvement in the US presidential election as well as any connection between Trump and the Russians during the election campaign. On Tuesday, media reports surfaced that Trump asked former FBI director James Comey to end an investigation into ties between Russia and Trump's former security adviser, Michael Flynn. As if this wasn't enough of a headache for Trump's team, the president is under fire for passing classified intelligence to the Russian foreign minister. Trump initially denied the claim, but has since admitted that he did share intelligence with the Russians, arguing that he had acted within his rights. With the Trump administration frantically trying to douse political fires, investors are growing increasingly nervous that Trump's plans for a stimulus package and tax reform will stall, and these jitters have sent stock markets and the US dollar downwards.

The markets did a good job forecasting key consumer indicators in the eurozone. Final CPI for April matched the forecast with a strong gain of 1.9% in April, considerably higher than last month's gain of 1.5%. Eurozone inflation is closing in on the ECB's target of 2.0%, which could increase pressure on the ECB to consider tapering its ultra-loose monetary policy. There are voices in Germany and elsewhere in the euro-area which want Brussels to adopt a tighter monetary policy. On Tuesday, Eurozone Flash GDP for the first quarter was unrevised from the April forecast, posting a gain of 0.5% in the first quarter. The eurozone continues to show improved numbers in 2017, boosted in no small part by the German economy, which expanded 0.6% in the first quarter.

GOLD Medium-Term Bullish, SILVER Failed To Hold Above Fibonacci Retracement At 16.92, CRUDE OIL Monitoring The $50 Level.

GOLD Medium-term bullish.

Gold seems on its way back up. Hourly support is now located at 1195 (10/03/2017 low). Expected to show further upside pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Failed to hold above Fibonacci retracement at 16.92.

Silver is bouncing back. Strong support is given at 15.63 (20/12/2017 low). Closest support is given at 16.20 (04/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high).

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Monitoring the $50 level.

Crude oil continues to bounce on shortsqueeze move. Support is given at a distance 43.76 (05/05/2017 low). Demand is very strong and crude oil is set to be monitor again the $50 mark.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).