Sample Category Title

UK & Canadian CPIs, Other Key Data in Focus

Next week's market movers

- In the UK, lots of key economic data are due out, among which inflation figures. However, with the recent BoE meeting now out of the way, we think that investors are likely to turn their attention primarily to developments surrounding the upcoming General election.

- In Canada, April's CPI rates may rebound following notable tumbles in March, but we doubt that this will lead to a material change in the BoC's dovish rhetoric.

- We also get key economic data from China, Australia, New Zealand, and Canada.

On Monday, during the Asian morning, we get China's retail sales, industrial production and fixed asset investment data, all for April. The forecast is for all of these indicators to have slowed in yearly terms. Indeed, both of the nation's official and Caixin manufacturing PMIs for the month showed that production continued to rise, albeit at a reduced pace, which supports the industrial output forecast. Meanwhile, the consensus for slowing retail sales is somewhat supported by the notable slowdown in imports during the month.

From New Zealand, we get retail sales for Q1. The forecast is for sales to have accelerated somewhat, in both quarterly and yearly terms. The case for another quarter of solid sales is supported by the New Zealand electronic card transactions indicator, a gauge of the nation's retail sales, which remained robust throughout the quarter. In addition, the continued increase in the nation's population growth due to strong net migration, supports further the forecast.

On Tuesday, the main event will probably be the release of the UK CPI data for April. The forecast is for both the headline and the core rates to have risen notably, something supported by the nation's services PMI for the month, which indicated that service firms raised their prices charged at the fastest pace since 2008. Indeed, in its latest Inflation Report, the Bank of England also anticipates inflation to have accelerated notably in April. In fact, the BoE forecasts suggest that the headline CPI rose to +2.7% yoy in April, while the market consensus currently anticipates a +2.6% yoy rise. As such, should inflation accelerate by less than what the BoE forecast, this would be yet another factor supporting the case for no action by the Bank in the foreseeable future. Considering that this is what is anticipated by financial markets as well, we think that sterling's forthcoming direction over the next weeks is likely to be decided primarily by news surrounding the upcoming General Election, rather than developments regarding monetary policy. In our view, incoming opinion polls that show the Conservatives maintaining or extending their current lead could support sterling as we approach the Election Day (June 8th).

On Wednesday, the UK employment data for March are coming out. In the absence of a forecast, we see the likelihood for the unemployment rate to have held steady, while average weekly earnings may have accelerated following three consecutive months of slowdowns. Our view is based on the UK services PMI for the month, which showed that the rate of job creation in the UK's largest sector was only marginal, and that firms reported stronger salary pressures. Accelerating nominal wages combined with the steady inflation rate for the month could turn real wage growth back to positive.

On Thursday, during the Asian morning, Australia's employment data for April are due out. The forecast is for the unemployment rate to have remained unchanged, and for the net change in employment to have remained in positive territory following a remarkable surge in March. The forecast for another month of employment gains is supported by the ANZ job ads indicator, which showed that job advertisements accelerated in April. This suggests that the labor market may have continued to tighten, something that could ease further some of the RBA's concerns regarding employment indicators.

From the UK, we will get retail sales data for April. Without a forecast available, we see the case for sales to have rebounded notably, following a bigger-than-expected plunge in March. Our view is based on the BRC retail sales monitor, which skyrocketed to +5.6% yoy in April from -1.0% yoy previously. In addition, the fact that the TR/IPSOS and the Gfk consumer sentiment indices both rose during the month, enhances the argument for a rebound in sales.

On Friday, we get Canada's CPI data for April, but no forecast is available yet. Our own view is that both the headline and the core CPI rates likely rebounded following notable tumbles in March. This view is consistent with the nation's Markit manufacturing PMI for April, which showed another robust increase in factory gate prices. A rebound in these rates would likely be an encouraging development for BoC officials, as it could confirm that the softness in March was only transitory. Nevertheless, we doubt that it will lead to a material change in the Bank's dovish bias. The BoC made it clear that it is going to maintain a cautious stance until uncertainties around trade clear up, something we don't see happening anytime soon given the recent tariffs from the US government

Do Not Get Carried Away By Oil’s Dead Cat Bounce

- Don't Be Scared & Stay Long EM Risk- Peter Rosenstreich

- Do Not Get Carried Away By Oil's Dead Cat Bounce - Arnaud Masset

- UK In Focus, BoE Keeps Its Rates Unchanged - Yann Quelenn

- USDHKD Heads for Intervention Threshold - Peter Rosenstreich

- Gold & Metal Miners

Economics - Don't Be Scared & Stay Long EM Risk

Much has been made of the historically low volatility seen across asset classes. Yet with key risk events over and lack of compelling drivers, low volatility environment is likely to remain. Of course there can always be a rogue iceberg that could derail the positive sentiment, but guessing on swan-like-trigger is unproductive. Investors should remain caution but hiding is not an investment strategy. Fears that refocusing on policy "normalizations" would damage risk appetite have not materialized as meaningfully shift is still months away. Still globally lose monetary policy environment has allowed markets to shrug of risk events such as Brexit, rising protectionism, geopolitical uncertainty etc. In addition, US President Trump destabilizing behavior has faded as an issue with most recent actions (firing of Comey) had a limited lasting market impact. And we don't expect that Feds shallow rate path to spark significantly higher rates or rotation out of risky assets. The Feds 14-June rate decision expected 25bp hike is already priced in. While EM economic growth data has further improved (as protectionist policy worries have declined) and subdued inflation indicate that more than a few EM Central Banks will cut rates this years. We see upside for EM growth outlook above 4.5%, so a bit of support from commodity prices will give EM another strong bound.

Judging by what only we can see there will be continued flow in EM carry trades as their risk metrics improve. Idiosyncratic risk such as North Korea, Mexico elections and China tightening is unlikely to snowball into a EM sell-off despite the large size of the current trade. Interestingly, the soft commodity prices have suspended investment into EM for some investors causing EM currencies to lag. We suspect there is still time to reload on high beta EM that also carry significant high carry such as TRY, RUB, IDR, MXN and BRL..

These currencies are most likely to benefit from the current low volatility environment. We especially like the EM Asia currencies as regional growth, despite credit tighten in China continue to improve. While news that US and China have agreed to a trade deal, while small in trading volume, suggest that a trade war or punitive currency policy is unlikely.

Crude Oil - Do Not Get Carried Away By Oil's Dead Cat Bounce

After falling as much as 20% in the second half of April, crude oil is making a comeback as the West Texas Intermediate bounced back at around $48 a barrel, up roughly 3% over the week. After the decision of OPEC and its allies to cut supply back in November last year, investors entered into a wait-and-see mode and took their time to assess the effectiveness of the OPEC decision. The market's enthusiasm was only short-lived but the WTI stabilised at between $48 and $55, during the first quarter, at least. It is quite clear that OPEC is always a trifle late. A few years ago the Cartel, realising that the US shale industry could jeopardise its dominant position in the oil business, tried to nip them in the bud by flooding the market with cheap oil. This move stopped any new investments in upstream exploration and killed the momentum of the US shale industry. However, the move came quite late as North America's frackers were already too efficient and were able to lower their break-even price well below $50 a barrel.

The problem now, is that OPEC countries are struggling with cheap oil prices, even though their breakeven prices are much lower (around $20 a barrel for Saudi Arabia, for example), as they need a higher price to balance their state budgets. To lift prices, OPEC trimmed production last year and members are currently discussing to extend the cut.

Unfortunately for OPEC and its allies, the US shale industry, which does not participate to the effort, is the primary beneficiary of those production cuts. Indeed, the higher the price, the higher the number of profitable US wells.

The number of US oil and gas rigs have been increasing steadily since May 2016 to reach 703 last week. In average, US drillers added 10 new rigs per week over the last 6 months.

Against a backdrop of supply glut and subdued demand, we believe that the recovery in oil prices is quite limited, especially given the current set-up. The Cartel will have to cut production more aggressively and for longer if it wants to lift prices substantially. Only in the latter case, may we see WTI above $55 a barrel, but again, the primary beneficiary will be the US shale industry. We do not rule out a recovery in crude oil prices in the short-term. However, we do not believe that a TWI above $55-60 is sustainable without significant improvement of the fundamentals.

Economics - UK In Focus, BoE Keeps Its Rates Unchanged

The Bank of England has decided to keep its interest rate unchanged at 0.25% against the backdrop of political uncertainties. Indeed, the 8th of June New General Election will take place, after Theresa May asked the Queen Elizabeth to dissolve the parliament. UK Prime Minister is attempting to gain a stronger majority before negotiations on the article 50 with the EU.

This is why the British central bank favoured the wait-and-see mode last Thursday. Political uncertainties regarding the 2-year negotiation period prevail. Anyway, the BoE has gained some time since last year as the UK economy had clearly benefited from pound devaluation after the Brexit vote. The inflation is now standing at 2.3% y/y. Yet the growth seems still a bit slow (0.3% for Q1 GDP). The unemployment rate keeps declining and is now standing at a 12-year low.

However, the UK is also facing some difficulties. The UK GDP missed forecasts and we may not see growth above the GDP forecasts within the next few years. Retail sales are falling at the fastest rate in seven years, yet, the UK economy is not collapsing as some had promised amid the Brexit campaigning. The UK is doing better than many western countries, which are still struggling with high unemployment rates, low growth and low inflation.

At this point, we do not believe that the BoE will provide any more hints regarding a possible tightening within the next few months. Inflation is getting stronger and this may be one opportunity to kill debt for the BoE. We recall that the debt-to-GDP ratio is 90% but however likely a rate hike of 25 basis point is, this would not make a significant impact on inflation and growth. Another point of concern now for the BoE is the level of real wages which are falling.

There is also one important thing to be said, the UK trade deficit is still very large despite the weaker pound. The trend is clearly negative and amounts for £3.6 billion. We believe that the overseas demand is falling for UK goods certainly on fears that the trade relations with the UK are unclear at the moment.

The future of trade relations are questioned a lot and this drives UK exports lower. The question is now to know whether there will be trade tariffs on importing product from the UK that would hit European business. This is the one reason why UK is facing a growing trade deficit. Replacement opportunities are now being searched for by foreign businesses. We know that long-term relations are always favoured but why would you import from the UK now if there is a threat that trade agreements in the future will ruin the profitability of your business by increasing costs.

Article 50 negotiations will obviously be key. Any positive development will provide a good traction for the UK economy and we must not forget that the UK has a certain number of bilateral agreements that existed before joining the EU. The uncertainties regarding the negotiations are sending the GBP lower. We believe the Sterling is largely undervalued and will strengthen when negotiations will unravel.

The election of Emmanuel Macron in France does not change much in our view even though he can be qualified as a hard Brexiter and he believes the UK has more to lose than the EU, which has the upper hand on the coming negotiations. He also said that the UK is now becoming a "US vassal state". Macron mentioned several times that he wants to make the UK exit harder as he does not want to provide the signal that it is easy to leave the EU.

FX Market - USDHKD Heads for Intervention Threshold

The long USD short HKD trade continues uninterrupted, clearly having no fears of preemptive official intervention at this point. USDHKD increased to 7.7891 in Asian trading well below the Hong Kong Monetary Authority's 7.85 upper band (7.75 to 7.85 convertibility range). HKMA has expressed commitment to the USD-linked exchange rate (expected to intervene at 7.8), yet the rapid HKD deprecations spawn questions about the sustainability of the peg. The widening US-HK interest rate differential makes borrowing cheap in HK and buying in US a tempting candidate for carry traders. Yet, Hong Kong's annual GDP growth is likely to have accelerated as 1Q GDP came in at 4.3% (above 3.7% exp). The read indicates that household spending and service exports remains solid. April PMI indicates that growth momentums will on a solid pace. From a fundamental standpoint Hong Kong is strong.

Concerns over Hong Kong's attempt to slow house price appreciations on tighter lending practices and increase in purchase tax has pushed Hibor (1-month Hibor 0.38 from 0.75 in Jan) below the US equivalent while high levels of interbank liquidy lower demand for HKD. In addition, China is also in the process of tightening financial conditions and expectations of gradual Fed interest rate increases and reduction in balance sheet are all generating excessive outflows. However, the hazard of waiting is that speculative short selling of HKD could complicate the HKMA objective and even threaten the stability of the banking system. Waiting could force the HKMA to intervene but possibly raise interest rates. Given the high level of leverage in Hong Kong households, a sharp increase in interest rates would pressure debt-holders and possibly constrict consumption (pressuring growth), a dangerous spiral. Currently given the manageable fundamental backdrop and the HKMA's massive $3.5 trillion reserves, we see no threat to the USD peg. Should we see USDHKD at 7.8 that would be a tempting short.

Themes Trading - Gold & Metal Miners

The sudden collapse in commodity prices in 2014 sent mining stocks into free fall. In the long term, however, precious metals - and gold in particular - are the perennial go-to sources of protection against inflation and economic downturns, something investors should be looking out for. The gold market is dynamic, and there are compelling reasons why gold producers could rally. Consumer demand remains solid, with around 2,500 tons of gold mined worldwide every year. Over the long haul, gold as a commodity has appreciated by more than 287% over the past 15 years; by comparison, the S&P 500 has gained less than 44% over the same period. In a period of central bank policy shifts, it is reasonable to envisage a rebound in metal prices - something mining stocks will benefit from. Gold miners are a good way to tap into the benefits of precious metals without paying storage costs.

Given the sharp debasement of precious metal over the last few weeks, a reversal is more than likely. Take advantage of the move.

Retail Sales Up in April, Revised Higher in March

Although April retail sales were below consensus, the March revision shows a stronger finish for the first quarter and a relatively modest start in the second quarter.

Retail Sales Improve in April

Retail sales increased a less than expected 0.4 percent in April, but March's retail sales were revised up from -0.2 percent to 0.1 percent, which will help to strengthen personal consumption expenditures (PCE) at the end of the first quarter and change the narrative at the beginning of the second quarter. Retail sales excluding automobile sales were also lower than expected, 0.3 percent versus 0.5 percent. However, they were also revised upward from a flat reading in March to a 0.3 percent increase. A very similar situation occurred with retail sales excluding automobile sales and gas, which increased 0.3 percent versus market expectations of a 0.4 percent increase. However, March sales were upped to 0.4 percent growth compared to an original increase of 0.1 percent.

The strongest sector in April was nonstore retailers, where sales increased 1.4 percent followed by sales at electronics and appliances stores, which increased 1.3 percent. Electronics and appliance store sales has been one of the weakest sectors of retail in the past year but has been very strong lately, increasing another 2.2 percent in February. Motor vehicle sales increased 0.7 percent and point to a recovery in automobile sales after a weak first quarter of the year.

On the housing market side of retail sales, the news was mixed, with building material and garden equipment and supplies dealer sales increasing a strong 1.2 percent but not enough to recover from the 1.7 percent decline in March. However, furniture and home furniture store sales were down 0.5 percent, perhaps a payback from a strong 1.5 increase in March.

Another sector that suffered a payback was clothing and clothing accessories store sales, which declined 0.5 percent after a strong 1.9 percent rise in March while general merchandise store sales continued their decline, this time dropping 0.5 percent. A positive development in this sector was a second consecutive increase in department stores sales, up 0.2 percent in April after a 0.1 percent in March. Still, the sector was down 3.7 percent versus April of last year.

Control Group Sales Shows Upward Revision for PCE in Q1

Perhaps the most important data point for this release was the upward revision to all the components of retail sales in March. This is especially true for control group sales, which was upwardly revised to 0.7 percent in March. For April, control group sales were up a less than expected 0.2 percent. That is, the upward revisions to March will help first quarter GDP growth but will likely lower the strength of PCE that we were expecting coming out of the gates in the second quarter of the year.

April CPI Inflation Rebound Keeps a June Rate Hike in Place

Confirming March's unexpected decline was "transitory," headline and core CPI inflation rebounded in April. A return closer to trend performance at the start of Q2 keeps the Fed on track for a June rate hike.

Food and Energy Prices Rise

Extending the theme we have witnessed this week with gains in both headline and core measures of import and producer prices, consumer inflation, as measured by the Consumer Price Index (CPI), also revealed a rebounding performance during the month of April. Admittedly a lower than expected rebound, headline CPI increased 0.2 percent in April from the 0.3 percent decline in March. Energy prices, which tend to be a significant factor in the monthly headline performance, rose 1.1 percent on the month, as all three major components - gasoline, natural gas and electricity - increased. Crude oil prices have fallen substantially in recent weeks and will likely influence next month's headline CPI performance.

Consumer food prices extended its recent rising streak to four months, but underlying details were on the soft side. The index for food at home prices rose 0.2 percent, but was largely driven by an outsized gain in fruits and vegetables (2.2 percent). Four of the five major grocery store food components fell on the month. Food prices away from home edged up 0.2 percent in April and are up a modest 2.3 percent pace over the past year.

Excluding food and energy, consumer prices increased a modest 0.1 percent in April following the unusual March decline of -0.1 percent. Shelter costs, which were a contributing factor to March's core CPI decline, returned to trend, up 0.3 percent. An outsized increase in tobacco, 4.2 percent, also underpinned the core. Outside of those two components, however, the core inflation environment remains soft. Medical care, communication (including wireless services), new & used cars and trucks, and apparel declined for the second month. The three-month annualized rate of core CPI has fallen from a recent high of 3.0 percent to a low of 0.6 percent - pointing towards further moderation in the year-over-year rate in the coming months (middle chart).

Economic Backdrop Still Supports June Rate Hike

The key question heading into today's CPI report was whether the unexpected decline in March consumer inflation was "transitory" as the Fed and consensus believed, or the start of a new concerning trend. While April's performance did rebound, the soft underlying performance is unlikely to quench concerns several Fed officials have expressed over the likelihood of reaching the Fed's 2.0 percent target. That said, the labor market remains strong and communication from most Fed officials remains resolute that they remain focused on their tightening monetary policy path. While the April CPI performance was weaker than we had projected, our overall economic growth outlook remains in place and we do not think the recent soft inflation prints will deter Fed officials from raising rates at the June meeting.

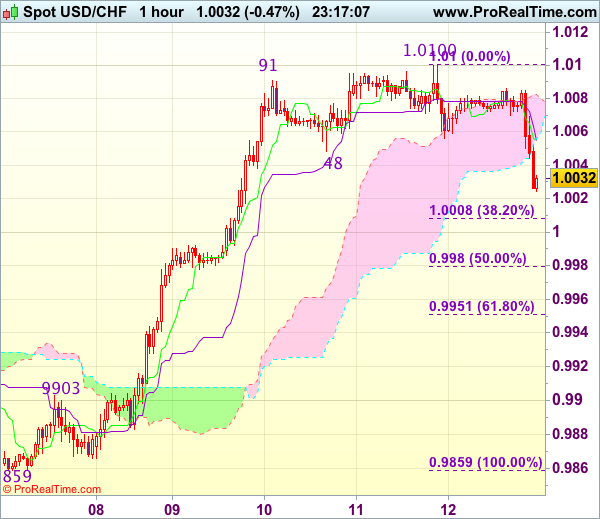

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 1.0020

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0047

Kijun-Sen level : 1.0047

Ichimoku cloud top : 1.0083

Ichimoku cloud bottom : 1.0056

Original strategy :

Buy at 1.0015, Target: 1.0115, Stop: 0.9980

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Current selloff has dampened our bullishness and suggests top has been formed at .1.0100, hence consolidation with downside bias is seen for retracement of recent rise towards 0.9980 (50% Fibonacci retracement of 0.9859-1.0100), break there would add credence to this view, bring further fall to 0.9950-55 (61.8% Fibonacci retracement) but price should stay well above previous resistance at 0.9903, bring rebound next week.

In view of this, would be prudent to stand aside in the meantime. Above 1.0045-50 would bring recovery to 1.0080-85, however, price should falter below strong resistance at 1.0100-8 and bring further consolidation later.

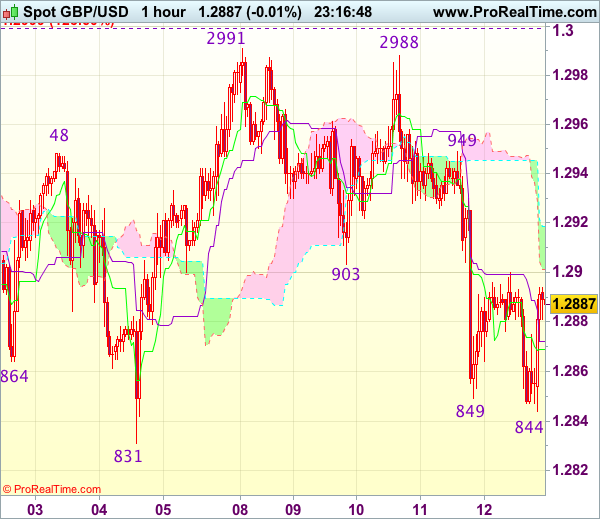

Trade Idea Wrap-up: GBP/USD – Hold short entered at 1.2900

GBP/USD - 1.2874

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2869

Kijun-Sen level : 1.2872

Ichimoku cloud top : 1.2919

Ichimoku cloud bottom : 1.2901

Original strategy :

Sold at 1.2900, Target: 1.2800, Stop: 1.2935

Position : - Short at 1.2900

Target : - 1.2800

Stop : - 1.2935

New strategy :

Hold short entered at 1.2900, Target: 1.2800, Stop: 1.2935

Position : - Short at 1.2900

Target : - 1.2800

Stop : - 1.2935

Although cable has rebounded after marginal fall to 1.2844 and consolidation above this level would be seen, still reckon upside would be limited to resistance at 1.2903 (previous support) and bring another decline, below said support would add credence to our bearish view that top is formed at 1.2991 earlier and bring test of 1.2831 support, break there would provide confirmation and extend the fall from 1.2991 top to 1.2805 and later towards 1.2770 but reckon previous support at 1.2757 would hold from here.

In view of this, we are holding on to our short position entered at 1.2900. Above 1.2925-30 would risk test of 1.2950-60 but break there is needed to signal low is formed, bring another bounce towards 1.2988-91 resistance but break of 1.2999-00 (1.236 times projection of 1.2109-1.2616 measuring from 1.2365 and psychological resistance) is needed to revive bullishness.

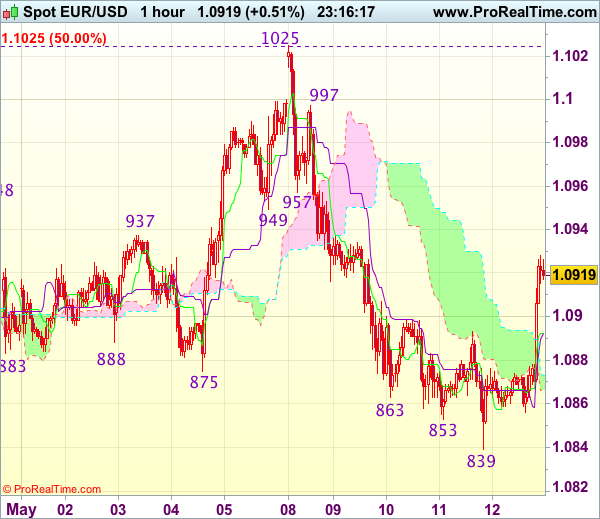

Trade Idea Wrap-up: EUR/USD – Sell at 1.0980

EUR/USD - 1.0921

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0892

Kijun-Sen level : 1.0892

Ichimoku cloud top : 1.0873

Ichimoku cloud bottom : 1.0866

Original strategy :

Sell at 1.0955, Target: 1.0840, Stop: 1.0990

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0980, Target: 1.0860, Stop: 1.1015

Position : -

Target : -

Stop : -

Current rebound in US morning suggests first leg of decline from 1.1025 top has ended at 1.0839 and near term upside risk is seen for this rebound to extend gain to 1.0950-55, however, if our view that top has been formed at 1.1025 is correct, upside would be limited to 1.0980 and resistance at 1.0997 should hold, bring another decline later. Below 1.0880 would bring weakness to 1.0855-60 but break of support at 1.0839 is needed to confirm and extend fall to 1.0821, then 1.0795-00 later.

In view of this, we are still looking to sell euro but at a higher level as 1.0997 resistance should limit upside. Only break of said resistance at 1.1025 would abort and signal early upmove has resumed instead, bring further gain to 1.1050-55 and later 1.1075-80 before prospect of another retreat.

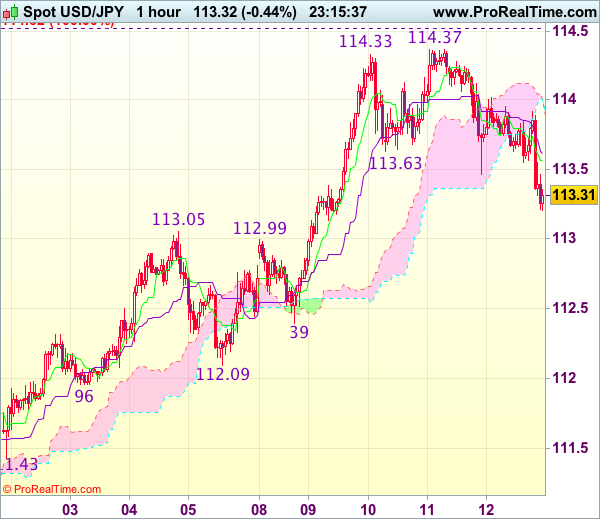

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 113.31

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.56

Kijun-Sen level : 113.61

Ichimoku cloud top : 114.01

Ichimoku cloud bottom : 114.00

Original strategy :

Buy at 113.15, Target: 114.25, Stop: 112.80

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Current selloff in NY morning on dollar’s broad-based weakness suggests a temporary top has been formed at 114.37 yesterday and consolidation below this level is seen with mild downside bias for test of previous resistance at 112.99-05 (now support), break there would add credence to this view, bring retracement of recent upmove to 112.70-75, however, reckon support at 112.39 would limit downside and price should stay above support at 112.09, bring rebound next week.

In view of this, would be prudent to stand aside in the meantime. Above the Kijun-Sen (now at 113.61) would bring recovery to 114.00, however, price should falter below said resistance at 114.37, bring another retreat later. Only break of 114.37 would revive bullishness and extend recent upmove to 114.50-55 (100% projection of 108.13-111.78 measuring from 110.87) and possibly 114.75-80 but price should falter below 115.00.

Trade Idea: EUR/GBP – Stand aside

EUR/GBP - 0.8473

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the single currency has rebounded again today, suggesting further consolidation above this week’s low at 0.8384 would take place and gain to 0.8509 resistance cannot be ruled out, however, as outlook remains consolidative, reckon upside would be limited to resistance at 0.8531 and bring further choppy trading. Only a break of said resistance at 0.8531 would add credence to our view that a temporary low has been formed at 0.8312 last month and extend the rebound from there for retracement of recent decline to 0.8550

On the downside, expect pullback to be limited to 0.8425-30 and 0.8400 should hold, bring another rebound later. Below said support at 0.8384 would extend weakness to support at 0.8351 but break there is needed to signal the rebound from 0.8312 low has ended at 0.8531 and bring further fall towards this support at 0.8312 which is likely to hold from here. As near term outlook is still mixed, would be prudent to stand aside for now.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

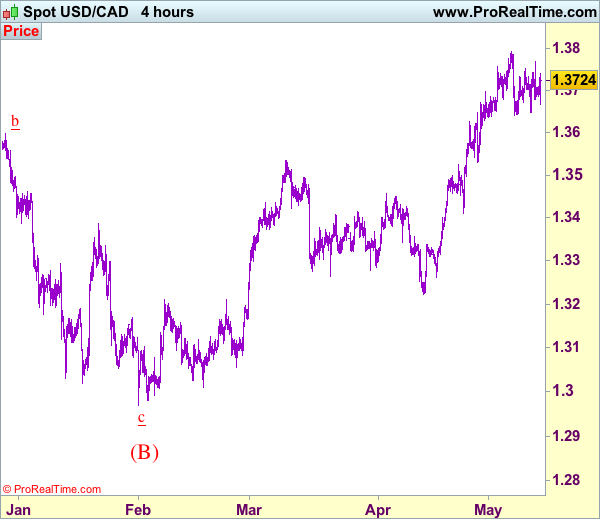

Trade Idea: USD/CAD – Buy at 1.3570

USD/CAD - 1.3725

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Buy at 1.3570, Target: 1.3770, Stop: 1.3510

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3570, Target: 1.3770, Stop: 1.3510

Position: -

Target: -

Stop:-

The greenback has remained confined within near term established range and further sideways trading below last week’s high at 1.3794 would take place, below 1.3640-45 would bring correction to 1.3600, however, reckon downside would be limited to 1.3570 and bring another rise later, only break of said resistance at 1.3794 would confirm recent upmove has resumed and extend further gain to 1.3840-50 but overbought condition should prevent sharp move beyond 1.3890-00 and price should falter below 1.3950.

In view of this, would not chase this rise here and would be prudent to buy again on pullback as 1.3570 should limit downside and bring another rise later. Below 1.3530 would abort and suggest a temporary top is formed, bring retracement of recent upmove to 1.3500 and later towards 1.3450-60 but support at 1.3411 should remain intact, bring another upmove later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.