Sample Category Title

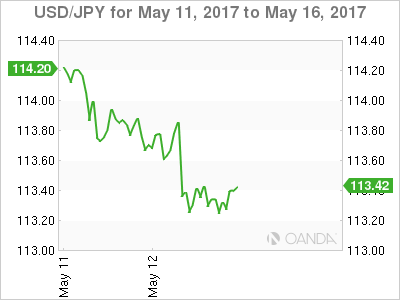

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.03; (P) 113.49; (R1) 113.78; More...

Intraday bias in USD/JPY remains neutral as consolidation from 114.36 continues. In case of deeper decline, downside should be contained by 112.08 cluster support (38.2% retracement of 108.12 to 114.36 at 111.97) and bring rally resumption. We're holding on to the view that corrective fall from 118.65 is completed with three wave down to 108.12. Above 114.36 will target 115.49 resistance first. Break there should resume whole rise from 98.97 to 125.85 high.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

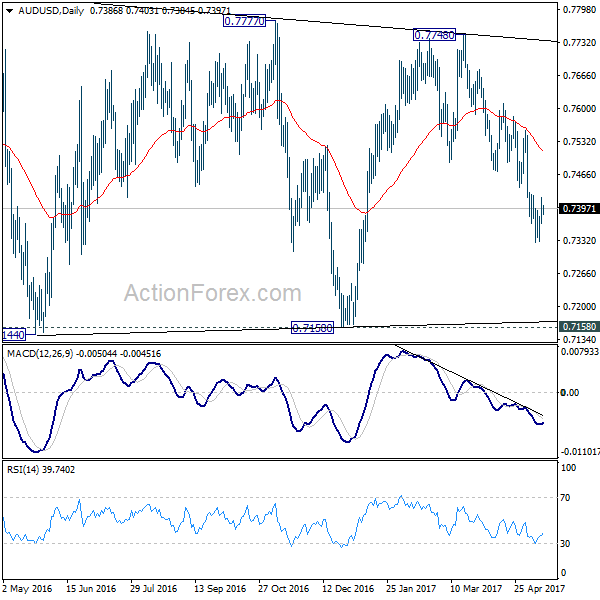

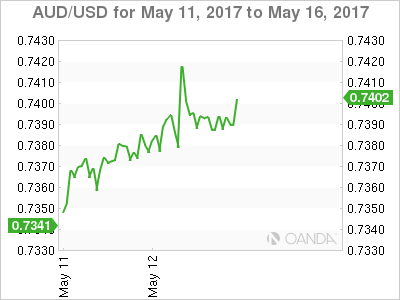

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7359; (P) 0.7390; (R1) 0.7416; More...

Intraday bias in AUD/USD remains neutral as the consolidation from 0.7382 continues. Upside of recovery should be limited below 0.7555 resistance to bring another fall. Below 0.7382 will target 0.7144/7158 support zone. However, there is no clear sign of larger down trend resumption yet. Hence we'll be cautious on strong support from 0.7144/58 to contain downside and bring rebound. On the upside, firm break of 0.7555 will argue that fall from 0.7748 is completed and turn bias back to the upside.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8115) and above.

Forex Markets Steady With Mild Strength in New Zealand Dollar and Canadian Dollar

The forex markets open the week rather steadily. New Zealand Dollar trades mildly higher after better than expected retail sales data. Canadian Dollar is also lifted mildly by rebound in oil price, which sees WTI back at 48.60, comparing to this month's low at 43.76. The Japanese Yen shows little reaction to another missile launch by North Korea while markets await the result of an emergency UN security meeting. Euro also shows little reaction to German CDU's win in an important state election. Meanwhile, UK is stepping up its rhetoric ahead of the Brexit negotiation. The focus of the week, though, will be on data from UK, Eurozone, Canada and Australia.

North Korea fired another missile test, UNSC to hold emergency meeting

In Asia, North Korea said today that it had successfully conducted a newly development mid-to-long range missile test over the weekend. The official KCNA news agency said that "the test-fire aimed at verifying the tactical and technological specifications of the newly developed ballistic rocket capable of carrying a large-size heavy nuclear warhead." Meanwhile, the Pacific Command of US military said that the type of missile fired was "not consistent with an intercontinental ballistic missile." The US and Japan called for an emergency meeting of the United Nations Security Council on North Korea. The meeting will be held Tuesday afternoon.

CDU won election in the most populous state in Germany

In Germany, Chancellor Angela Merkel's Christian Democratic Union had an important victory in elections in the state of North Rhine-Westphalia yesterday. The CDU is projected to get 33% of votes. Social Democratic Party came second with 31.4%. Meanwhile, the populist Alternative for Germany got 7.4% percent in their first run for NRW parliament. NRW is the most populous state in Germany and it's seen as a important indicator for the results in September's national election. Merkel and CDU are seen as given a strong start to their campaign for September.

Brexit Minister Davis: EU format of negotiation "illogical"

In UK, Brexit Minister David Davis criticized that the EU's format of negotiation is "illogical". He referred to the sequence of talks on dealing with citizen's rights, border between Northern Ireland and the Republic of Ireland and then a financial settlement. And, after completing that, the discussions on future relationships could start. He especially pointed out that without knowing UK's general border policy, free trade agreements, there is no way to handle the border of Irelands. Davis also blasted that "the simple truth is that we are leaving, we are going to be outside the reach of the European court."

China data indicates slower Q2

The batch of data released from China today is generally weaker than expected. Retail sales rose 10.7% yoy in April, down from prior month's 10.9% yoy and missed consensus of 10.8% yoy. Fixed asset investment rose 8.9% yoy, down from prior 9.2% and missed consensus of 9.1%. Industrial production rose 6.5% yoy, down from prior 7.6% yoy and missed expectation of 7.0% yoy. The set of data is in-line with recent PMIs, which showed loss of momentum in Q2 after a solid Q1.

Also released in Asian session, Japan domestic CGPI rose 2.1% yoy in April. Australia home loans dropped -0.5% in March. New Zealand retail sales rose 1.2% qoq in Q1. Swiss PPI, US Empire State manufacturing and NAHB housing index will be featured later in the day.

For the week ahead...

A number of economic data will be released from UK including CPI, employment and retail sales. Headline CPI is expected to jump further to 2.6% yoy in April. Currently, it's generally expected that BoE won't act before conclusion of the Brexit negotiation. But the markets would also be keen to see how the inflation numbers turn to to be and how they would stretch MPC member's tolerance. Meanwhile, Eurozone GDP, German ZEW will also be watched. In Asian pacific, RBA minutes and Australia employment, Japan GDP will be the highlight. Meanwhile, in North American, the main focus will be Canada CPI and retail sales.

Here are some highlights for the week ahead:

- Tuesday: RBA minutes; Japan tertiary industry index; Italy GDP; UK CPI, PPI; Eurozone GDP, trade balance; German ZEW; US housing starts and building permits, industrial production

- Wednesday: New Zealand PPI; Australia wage price index; UK employment; Eurozone CPI final; Canada manufacturing sales

- Thursday: Japan GDP; Australia employment; UK retail sales; US jobless claims, Philly Fed survey

- Friday: German PPI; Eurozone current account; Canada CPI, retail sales

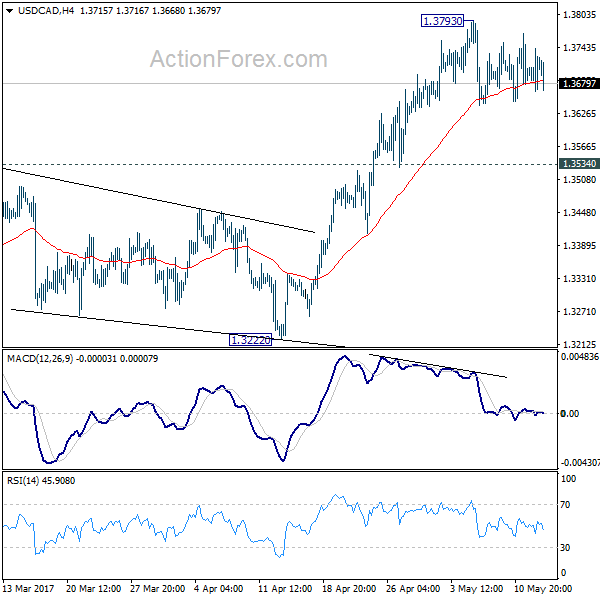

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3668; (P) 1.3705; (R1) 1.3745; More....

USD/CAD dips mildly today but it's staying in tight range below 1.3793. Intraday bias remains neutral for the moment. Outlook is unchanged that choppy rise from 1.2460 is seen as a corrective move. Hence, in case of another rally, we'd expect upside to be limited by 1.3838 fibonacci level to bring reversal. Meanwhile, break of 1.3534 resistance turned support will suggest that rise from 1.2968 has completed. In such case, intraday bias will be turned back to the downside for medium term channel (now at 1.3176).

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and would end at around 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Ex Inflation Q/Q Q1 | 1.20% | 0.90% | 0.60% | 0.70% |

| 23:50 | JPY | Domestic Corporate Goods Price Index Y/Y Apr | 2.10% | 1.80% | 1.40% | |

| 1:30 | AUD | Home Loans Mar | -0.50% | 0.00% | -0.50% | -0.80% |

| 2:00 | CNY | Retail Sales Y/Y Apr | 10.70% | 10.80% | 10.90% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Apr | 8.90% | 9.10% | 9.20% | |

| 2:00 | CNY | Industrial Production Y/Y Apr | 6.50% | 7.00% | 7.60% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Apr P | 22.80% | |||

| 7:15 | CHF | Producer & Import Prices M/M Apr | 0.00% | 0.10% | ||

| 7:15 | CHF | Producer & Import Prices Y/Y Apr | 1.00% | 1.30% | ||

| 12:30 | USD | Empire State Manufacturing Index May | 7.5 | 5.2 | ||

| 14:00 | USD | NAHB Housing Market Index May | 68 | 68 | ||

| 20:00 | USD | Net Long-term TIC Flows Mar | 68.3B | 53.4B |

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3668; (P) 1.3705; (R1) 1.3745; More....

USD/CAD dips mildly today but it's staying in tight range below 1.3793. Intraday bias remains neutral for the moment. Outlook is unchanged that choppy rise from 1.2460 is seen as a corrective move. Hence, in case of another rally, we'd expect upside to be limited by 1.3838 fibonacci level to bring reversal. Meanwhile, break of 1.3534 resistance turned support will suggest that rise from 1.2968 has completed. In such case, intraday bias will be turned back to the downside for medium term channel (now at 1.3176).

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and would end at around 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should indicate the start of the third leg while further break of 1.2968 should confirm. Nonetheless, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Market Morning Briefing: Slightly Worse Than Expected US Retail Sales And Inflation Data Has Weakened Dollar

STOCKS

Dow (20896.61,-0.11%) continues to remain in a sideways consolidation within 20780-20980 region as mentioned least week. Immediate support near 20780 is expected to hold in the near term. Only in case of a break below 20780, we may expect a fall towards 20600-20400 levels.

Dax (12770.41,+0.47%) is just above support near 12690 and while that holds, we could see a bounce back towards 12800 and higher in the near term. Near term looks bullish while above 12690.

Shanghai (3088.62, +0.17%) tested 3020 last week before bouncing back sharply from there. It is trying to inch up towards 3130-3170 levels which could be tested in the near term before a sharp fall is seen.

19610-20010 is the immediate region of trade for Nikkei (19842.15, -0.21%) in the near term. Only a break out on either side of the range could give a clear directional view for the medium term.

Nifty (9400.90, -0.23%) came off from levels below our resistance zone of 9460-9500 and while that holds, we could expect a correction towards 9270 in the coming sessions before a bounce back towards 9400. .

COMMODITIES

Muted price action has been seen in Gold (1229) as the same traded within the 1220-31 region last week. If the rise continues we may possibly see a test of 1255-65 levels in this week. A failure to break above 1265 could keep the price range-bound in the 1220-1265 regions. A Close below 1220 could open up 1186 levels as well.

Similar kind of trading pattern has been seen in silver (16.49) also. The scrip is highly oversold in near term chart, thus a possibility of a rise towards 16.80-95 levels can’t be ruled out.

Copper (2.53) is hovering around its crucial resistance of 2.53-55 and if these levels break then we might see a bounce towards 2.60 regions in very short term time period. We will remain bearish on copper while t is trading below 2.67-72 levels in the medium term time frame.

Sideways consolidation in the broader ranges of 49.50-51.50 for Brent and 46.80-49.30 for WTI continues as expected. Holding above the interim resistances of 51.50 in Brent and 49.30 in WTI implies strength in oil prices in the extreme short term. Still, the bulls will be assured of strength of Brent (51.40) and WTI (48.25) only when a firm closing above 53 and 51 are made by both Brent and WTI respectively.

FOREX

Slightly worse than expected US Retail Sales and Inflation data has weakened Dollar. It may take another couple of sessions to clear up if it is only a correction or a complete reversal.

Dollar Index (99.22) has lost the bullish momentum with a break below 99.25 it remains to be seen if a recovery emerges from 99.00-98.85 or not. Trend neutral in the range of 99.00-100.00 and a clear break from this range is required to get a directional move.

Similar loss of bullish momentum is visible in Dollar Yen (113.34) too, though it is still trading above the near term support of 113.10. The price action here may determine if another bounce towards 115.00-50 will come or not. Prefer to wait for a session and watch.

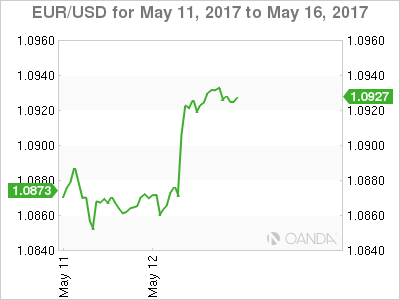

It has been a day of very sharp gains for Euro (1.0931) last Friday but for sustained strength, it needs a clear break above 1.0940-50. Otherwise a turnaround to the downside can’t be ruled out. With EURJPY (123.86) also stalling around an intermediate resistance around 124.20-50, it would be prudent to watch the price action of Euro at the current levels before taking a firm directional call.

Pound (1.2892) bounced back from the previous week’s low near 1.2825 and kept the trend still up in line with expectations. It has been moving sideways roughly in the range of 1.2800-1.3000 which may take a few more sessions before resolving.

Aussie (0.7395) tested the upper end of the range of 0.7325-0.7425 but the sharp rejection from there implied persistent weakness. As discussed last week, a resumption of the major downtrend may be expected this week for the target/support of 0.7300-0.7290 from where a significant recovery may be expected.

Dollar Rupee (64.30) ended the week in an indecisive manner as it closed with no specific directional clue. The narrow range of 64.25-45 is the neutral zone as a break above 64.45 will denote strength and a break below 64.25 may provide fresh downside momentum. It must be noted that the Indian CPI for April has come at 2.99% against 3.81% in March.US April CPI has just come at 2.99% which brings the inflation differential down to 0.79% only, making Rupee depreciation more difficult.

INTEREST RATES

The Japan yields have come off a bit from near term channel resistance as mentioned last week. The 5Yr (-0.13%), 10Yr (0.04%) and the 30Yr (0.83%) are down from -0.12%, 0.05% and 0.84% respectively and may come off in the near term. Immediate movement could be on the downside.

The UK yields continue to fall as expected. The 5yr (0.50%) could head towards 0.40% while the 10Yr (1.09%) and the 20YR (1.66%) could head towards 1% and 1.5% respectively.

The German-US 2yr (-1.98%) is rising again but is trading within very narrow region of -1.95% and -2% and a break on either side would indicate the further direction in Euro. The German-US 10yr (-1.93%) is headed higher and could rise towards -1.90% in the next few sessions.

USDCHF – Upside Pressure Remains Valid On Bull Threats

USDCHF - With the pair retaining its upside pressure by closing higher the past week, more strength is likely. On the downside, support lies at the 0.9950 level. A turn below here will open the door for more weakness towards the 0.9900 level and then the 0.9850 level. On the upside, resistance resides at the 1.0050 level where a break will clear the way for more strength to occur towards the 1.0100 level. Further out, resistance comes in at the 1.0150 level. Its weekly RSI is bullish and pointing higher suggesting further upside. All in all, USDCHF faces further recovery risk in the new week.

EURUSD – Retains Upside Bias On Recovery

EURUSD - With the pair retaining its short term uptrend, more strength is envisaged. Resistance comes in at 1.1000 level with a cut through here opening the door for more upside towards the 1.1050 level. Further up, resistance lies at the 1.1100 level where a break will expose the 1.1150 level. Conversely, support lies at the 1.0900 level where a violation will aim at the 1.0850 level. A break of here will aim at the 1.0800 level. Its weekly RSI is bullish and pointing higher suggesting further strength. All in all, EURUSD faces further bull threats.

GOLD – Hesitates, Closes Higher

GOLD - The commodity halted its weakness to close higher the past week. On the downside, support comes in at the 1,220.00 level where a break will turn attention to the 1,210.00 level. Further down, a cut through here will open the door for a move lower towards the 1,200.00 level. Below here if seen could trigger further downside pressure targeting the 1,190.00 level. Conversely, resistance resides at the 1,230.00 level where a break will aim at the 1,240.00 level. A turn above there will expose the 1,250.00 level. Further out, resistance stands at the 1,260.00 level. All in all, GOLD looks to weaken further but with caution.

AUD/JPY Stepping Down Between Support/Resistance Levels

After AUD/JPY resistance held back in February, we've seen a pullback in the pair worth another look.

The following excerpt is taken from from the previous AUD/JPY feature which I've linked to in the previous paragraph:

Here is the zone once again. It doesn't really get much clearer that this:

AUD/JPY Daily:

As you can see quite clearly, higher time frame resistance held and price subsequently dropped.

Keep that one in mind and now compare that above chart to the following updated daily chart, showing where we're at now:

AUD/JPY Daily:

This is where you can see that price has now pulled back to retest previous short term support, this time as resistance. An opportunity to look for a continuation if you're still in, and a chance to get short if you missed the first entry.

Zooming into the hourly chart, you can see a further intraday pullback into previous support turned resistance:

AUD/JPY Hourly:

Depending on how aggressive you are a trader, there are a few levels here that you could use to manage your risk and position sizing around.

How are you looking to trade the Aussie?

Should We Look Past The US Q1 Soft Patch?

Should we look past the US Q1 soft patch?

Friday was another disheartening day for US economic data and has left dollar bulls in doubt entering this week. Focus shifts to pivotal European economic releases, as the lack of tier one US economic announcements this week, will leave US investors lamenting on Friday's weaker retail sales and disappointing consumer price index prints. Given the recent trend of deteriorating US data, set against a backdrop of other G-10 economies that have surveyed data print above expectations, if this bias persists it may bode poorly for the US dollar's performance this week.

We can sugar-coat Friday's retail sales data, which rebounded from two sluggish months and was mitigated by a three-tenth upward revision to March. But the cold, hard fact is that the figures grew just 0.4%; badly missing market expectations of 0.6%, which did little to convince investors that a recent run of weak US economic performance was reversing. While confidence was extremely elevated for a high rebound after a poor print in March, the dollar may have got off easy this time, as the Fed had already warned the market that they would look through the Q1 US economic soft patch, so why shouldn't traders? If the deterioration in tier one US economic data continues, I think it will be time for a reality check, as both the market tonality, along with Fed policy expectations, could yaw significantly.

While the CPI missed the Fed's 2% mandate level, the print itself is unlikely to alter June rate hike expectations. A miss on both Retail sales and CPI is concerning and resulted in a modest repricing for hike odds to just over 70% in June and only a 50%.But US labour markets remain robust and parsing the recent Fed speak; there is little slack left in labour markets, so the FOMC will likely remain unwavering on it's tighter policy path.

Australian Dollar

Trying to extract juice from the Aussie dollar trade has been little more than an exercise in futility of late. Thwarted on the downside by commodity price basing, and struggling to stage any meaningful topside momentum due to lingering concerns over China's 'Moneyball' reduction. Fleshing out convincing signals amongst a myriad of global and domestic narratives has traders increasingly frustrated.

Friday's jump above .7400 after Friday weak US data was faded, suggesting focus remains on the emphatically weak Australian consumption data and uncertainty over the commodity landscape.

The base metal view is mixed: copper higher, while iron ore regained a foothold above USD 60 per tonne after there was a 3% drop in China iron ore futures on Friday. But momentum remains clouded as a weaker US dollar on Friday failed to excite commodity investors, suggesting that tighter monetary conditions in China are taking a bite out of demand. Parsing President's Xi's recent comments, regulators are committed to weed out excess leverage throughout the economy and commodities could continue to struggle near term as China deleverages.

The market has opened flat to Friday's close, as dealers await a round of fresh economic data from China which could steady the Aussie dollar market. This morning's China retail sales, industrial production and fixed asset investment will garner some attention after a recent soft patch in Mainland's economic data.

In the meantime, in the absence of any spark, look for dealers to go through their daily ritual of selling rallies above .74 and buying dips too.73

Japanese Yen

Dollar-Yen ground lower on the data, as dollar bulls were chop blocked by a slide in US Treasuries, which triggered stop loss orders at 113.50 on the way to a low of 113.20 before recovering. The bullish bond tone was then further aided by Chicago Fed Charles Evans, who said he thought 'downside risks [for inflation] still predominate.'

In a show of defiance, North Korea conducted a ballistic missile on the weekend, which has had little impact on risk so far as it was not the intercontinental variety, but there remains a very cautious mood in first markets eerily reminiscent of April trade.

We could see USDJPY struggle this week in the absence of any tier one US economic data to ignite the dollar bulls, as dealers shift their focus to Japan's preliminary GDP data to be released on Thursday, as an acceleration in economic activity would suggest a higher probability for the BOJ to consider tapering.

Euro

The EURUSD has surged on weaker US data and aided by an ECB source cited by Der Spiegel who stated that starting in July, the ECB would prepare markets for exit from ultra-loose policy; followed by starting in the fall to lay out plans for exit from QE. With political risk abating, the euro longs held steadfast above the critical support level last week, anticipating some ECB hint of policy convergence with the US.

Traders did take note of weekend elections held on Sunday in Germany's most densely populated North Rhine-Westphalia. Angela Merkel's conservative party scored a big victory, dealing a knockout blow to Martin Schulz's ambitions. With no election surprise, the EURO has held on to Friday gains.

In the meantime, I expect offers to remain substantial between a 1.0950-.75 level which was the top of the range before the French election run up.