Sample Category Title

EUR/CHF Weekly Outlook

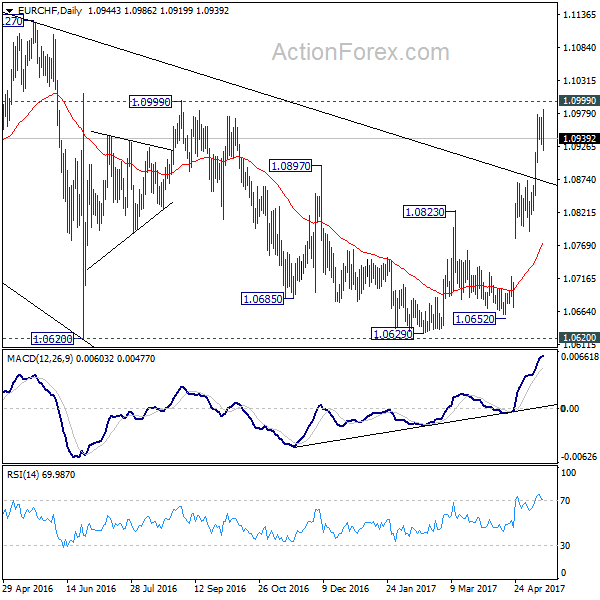

EUR/CHF's strong rally last week affirmed our view of trend reversal. That is, corrective pattern from 1.1198 has completed already after defending 1.0653 fibonacci level. Nonetheless, as the cross lost momentum ahead of 1.0999 resistance, we'd expect some more consolidation in near term before another rally.

Initial bias in EUR/CHF stays neutral this week for consolidation. Deeper pull back could be seen but downside is expected to be contained by 1.0791/0872 support zone to bring rise resumption. As noted before, the consolidative pattern from 1.1198 should be completed. Firm break of 1.0999 resistance will pave the way for a retest on 1.1198 high.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Current strong rebound is raising the chance that it's completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

Summary 5/15 – 5/19

Monday, May 15, 2017

[php_everywhere] [/php_everywhere]

Tuesday, May 16, 2017

[php_everywhere] [/php_everywhere]

Wednesday, May 17, 2017

[php_everywhere] [/php_everywhere]

Thursday, May 18, 2017

[php_everywhere] [/php_everywhere]

Friday, May 19, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary

U.S. Review

Mixed Signals on Inflation to Start Q2

- Survey data from businesses suggest that the labor market continues to tighten.

- Import and producer prices showed signs of acceleration this week, but another soft reading for the core CPI sends mixed signals to the Fed. On balance, the Fed remains positioned to hike rates in June while maintaining its slow and steady mentality.

- Retail sales were disappointing in April, but upward revisions to March's initial reading may indicate personal consumption growth was likely a bit stronger in Q1 than initially reported.

Mixed Signals on Inflation to Start Q2

The National Federation of Independent Business (NFIB) Small Business Optimism Index kicked off the week with a small decline of 0.2 points in April. The decline was led by a drop in expectations for improvement in the economy, which fell 8 points following the initial unsuccessful attempt to replace the Affordable Care Act. Despite the dip, confidence remains high, and the employment segments of the survey signaled even more pronounced labor market tightening. The share of respondents saying that it is hard to fill job openings edged up to 33 percent in April, the highest level since November 2000 (top chart). The share of business owners citing "finding qualified labor" as their most important problem is also trending near its previous high.

The Job Openings and Labor Turnover Survey (JOLTS) showed job openings rose slightly in March, ending the month at 5.7 million. With a relatively high share of employers struggling to fill positions, involuntary separations remain limited; the layoff & discharge rate is near an all-time low. The quit rate held steady at 2.1 percent in March, the level at which this measure has hovered for most of the past year. Although this marks an improvement from earlier in the cycle, wages have still failed to accelerate thus far in 2017. With the share of small businesses reporting jobs are hard to fill at a 17-year high, an acceleration in quits would bode well for a pick-up in wage growth later this year.

Inflation showed some continued signs of firming this week. Led by higher industrial supplies and fuel costs, import prices increased 0.5 percent in April. Excluding fuel, import prices increased 0.3 percent and are up 1.1 percent over the past year. Over the past three months, nonfuel import prices have risen at a 3.5 percent annualized clip, the fastest pace since 2011 (middle chart). Producer prices also surprised to the upside, rising 0.5 percent in April compared to expectations for a 0.2 percent increase. Excluding food, energy and trade services–our preferred measure of the PPI–prices jumped 0.7 percent, the largest increase in the three and a half year history of the series.

Consumer prices also rose in April, boosted by higher energy prices. However, the core CPI rose a smaller-than-expected 0.1 percent, bringing the year-ago pace of core inflation down to 1.9 percent. Core consumer price inflation has eased a bit to start 2017; the 1.9 percent year-ago reading was the first sub-two percent print since late 2015. The slowdown in core consumer prices is a bit puzzling given the price pressures further back in the pipeline. With lower energy prices likely to weigh on headline inflation in May, the Fed will have reason to maintain its slow and steady approach to tightening policy at its June meeting.

Retail sales rounded out the week this morning. Sales were disappointing in April, but upward revisions to March's initial reading suggest personal consumption growth may have been a bit stronger in Q1 than initially reported. The series is adjusted for the timing of Easter, however, and we may see a different story in the personal consumption data. Building materials, motor vehicles & parts and electronics outperformed, while clothing, furniture and food & beverage sales were soft.

U.S. Outlook

Housing Starts • Tuesday

Unseasonably mild winter weather during the first two months of the year helped get homebuilding off to a strong start in 2017. The relatively favorable building conditions allowed more construction activity to begin earlier this year, with housing starts through the first three months of the year up 8.1 percent from a year ago. Apartment construction accounted for a significant portion of the increase, as starts of five units or more are up 14.1 percent on a year-to-date basis. Single-family housing starts are up a more modest 5.9 percent over the same period.

We look for housing starts to recoup most of March's decline and rise to a 1.257 million-unit annual rate in April. While the mild winter weather likely pulled some building activity forward into the first quarter, we continue to expect housing starts to rise 7.3 percent this year, with virtually all of the growth coming from single-family construction.

Previous: 1,215K Wells Fargo: 1,257K Consensus: 1,260K

Industrial Production • Tuesday

Industrial production rose 0.5 percent in March, marking the second-largest increase in more than a year. However, the gain was almost entirely driven by a surge in utilities output, which reflected the return of more normal temperatures in March. Looking past the headline, manufacturing production declined 0.4 percent on the month, snapping a six-month string of gains. Notably, motor vehicle & parts output declined 3.0 percent as auto production pulled back. The weakness was not solely in autos, as declines were recorded across most durable and nondurable subsectors.

While the ISM manufacturing index edged another leg down April, the index remains at a still solid level that is consistent with our forecast. Looking to April, we expect a modest pickup in industrial production. While a breakout in activity seems unlikely in the nearterm, we expect manufacturing output expanded somewhat in April, and we look for a gain of 0.4 percent.

Previous: 0.5% Wells Fargo: 0.4% Consensus: 0.4%

Leading Economic Index • Thursday

The Leading Economic Index (LEI) continued to trend higher in March, increasing 0.4 percent. The gain marks the index's seventh-consecutive monthly increase. The improvement was relatively broad based as six of the LEI's eight components added to growth over the month. The interest rate spread component was the largest contributor in March, adding 0.19 percentage points to the headline. ISM new orders and the housing permits components were also strong on the month. Meanwhile, manufacturing hours worked and initial jobless claims were sources of weakness, subtracting 0.13 percentage points and 0.09 percentage points from the topline figure.

We expect the LEI to rise a modest 0.4 percent in April. The yield spread, manufacturing average weekly hours and initial unemployment claims components likely provided the largest contributions to the index's gain.

Previous: 0.4% Wells Fargo: 0.4% Consensus: 0.3%

Global Review

French Elections, Canadian Housing, and More

- By early this week financial markets were breathing a big sigh of relief with the results from the French elections, which produced a lopsided victory for the establishment (for lack of a better term) candidate, Emmanuel Macron, versus the extreme right candidate, Marine Le Pen.

- Canadian housing starts came down as expected to a still relatively strong 214,100 unit pace from a slightly downwardly revised 252,300 unit pace in March. March's increase in housing starts was the strongest print since early in 2012.

- Mexican industrial production remained flat in March.

Liberty, Equality, Fraternity

By early this week financial markets were breathing a big sigh of relief with the results from the French elections, which produced a lopsided victory for the establishment (for lack of a better term) candidate, Emmanuel Macron, versus the far right candidate, Marine Le Pen. Although polls before the election showed an almost uncontested election with Mr. Macron wining the contest almost unchallenged, many were concerned with the ability of polls to measure correctly, especially after several "surprises" during the last several years, i.e., Brexit and Trump.

Now, Mr. Macron will have to come up with a sound strategy to gain enough members in parliament during the June parliamentary elections as well as design a strategy to bring other parties to the table so he can form a governing coalition that can start delivering on his promises. And this is not going to be easy. Ms. Le Pen's rallying banners are not something that you can dismiss and if the political system tries to do so they do it at their own perils. Although Ms. Le Pen lost the election, the gain in votes was very important. In fact, voter participation during this presidential election was one of the lowest since the 1981. Interestingly enough, Ms. Le Pen almost doubled the number of voters compared to her father's, 10.6 million compared to 5.5 million in 2002, while Mr. Macron had only 20.7 million people voting for him versus 25.5 million who voted for Jacques Chirac in 2002 (read more on France's challenges on our Topic of the Week section).

Canadian Housing Starts Payback in April

In Canada, the country's housing market which has remained relatively strong, even as the economy downshifted due to the decline in oil prices over the last several years, saw some payback in April from the strong increase recorded in March. Housing starts came down as expected to a still relatively strong 214,100 unit pace from a slightly downwardly revised 252,300 unit pace in March. March's increase in housing starts was the strongest print since early in 2012. Housing starts in Canada are normally volatile but it seems that volatility has increased considerably since 2015 (middle graph). Meanwhile, building permits were down further in March, this time 5.8 percent compared to a decline of 2.8 percent in February while the new housing price index was up 0.2 percent after increasing 0.4 percent in February. This follows a downgrade on Canadian banks by Moody's investor services due to high household debt and concerns on high home prices.

Mexican Industrial Production Remains Flat in March

In Mexico, industrial production remained flat in March. Public utilities were up 0.5 while the mining sector improved 0.1 percent. However, manufacturing output was down 0.3 percent and construction output was down 0.2 percent. The year-over-year non-seasonally adjusted numbers looked much better, but those are not a good measure this time around because Easter occurred in March during 2016 and in April this year, which distorts the index and shows a stronger industrial sector than what it truly is.

Global Outlook

U.K. CPI • Tuesday

The U.K. will release CPI inflation for April this coming Tuesday. The consensus forecast looks for it to rise 0.4 percent on the month and 2.6 percent year over year. The CPI inflation rate in the U.K. stands at 2.3 percent and has trended upwards since early 2016. The sharp depreciation of the British pound following the Brexit referendum last June has seemed to have inflation implications.

While the rebound in energy prices has certainly helped support price pressures, core CPI, which strips out energy effects, has picked up too. April's core rate is expected to grow 2.2 percent in April, following 1.8 percent growth in March. The jump in prices has eroded growth in real income, which has, in turn, weighed on consumer spending. However, stagnation in average hourly earnings growth suggests that the core rate of inflation likely will not continue to shoot up.

Previous: 2.3% (Year-over-Year) Wells Fargo: 2.8% Consensus: 2.6%

Japan Q1 GDP • Wednesday

Japanese economic growth in Q1 is slated for release on Wednesday of next week. GDP is expected to expand 0.4 percent on a sequential rate and 1.8 percent at an annualized rate. This would be an improvement from the 0.3 percent quarter-over-quarter rate and 1.2 percent annualized rate in Q4 2016. Economic growth appears to be strengthening to begin 2017 as a result of a relatively weak yen and strong global demand, which help the Japan's vital export sector. Exports in March rose 12.0 percent, the fasted pace in over two years, coming at the heels of 11.3 percent growth in February.

Japan's Tankan index for large manufacturers in Q1 jumped to its highest level since Q4 2015. Moreover, the Bank of Japan's accommodative monetary policy seems to be supporting economic activity. We expect the Japanese economy to expand 1.2 percent in 2017, in-line with the consensus expectation.

Previous: 1.2% (Annualized) Wells Fargo: 2.3% Consensus: 1.8%

Canada CPI • Friday

Canadian CPI inflation for April is set to be released next Friday. Inflation cooled to 1.6 percent in March from 2.0 percent in February, year over year. March's rate landed below the midpoint of the Bank of Canada's (BoC) target range of 1 percent to 3 percent. On a sequential basis, prices actually declined 0.2 percent in March from a month earlier – a slight moderation from February's 0.3 percent slide. Canada's economy has been gaining momentum to begin 2017, helped by a rebounding energy sector that is enjoying higher oil prices. This, in turn, should put upward pressure on prices. We expect CPI inflation to average 2.3 percent in 2017 and 1.9 percent in 2018.

The BoC held its target rate for the overnight rate steady at 0.5 percent, expressing guarded optimism in its statement. In its April monetary report, the BoC revised its inflation expectations upward to 1.9 percent in 2017 and 2.0 percent in 2018.

Previous: 1.6% (Year-over-Year) Wells Fargo: 1.3% Consensus: 1.8%

Point of View

Interest Rate Watch

Elections and Market Economics.

Elections impact market expectations and certainly have altered prices thereby creating a political premium to markets independent of economic fundamentals. The challenge for investors is that political actions do alter market prices independent of any economic actions such that the fundamental values are obscured—at least for a short time.

Over the last year there have been interesting moves in the benchmark bond rates (top graph) and the euro/dollar spot rate (middle graph) that reflect expectations and the interaction of financial markets on a global scale.

Benchmark Bonds: A Political Barometer

In the top graph, the pattern of ten-year yields corroborates the politics/market pricing interaction. With the election of Donald Trump, the ten-year US-German and US-French spread widened out as expectations for economic policy actions and thereby more rapid economic growth took center stage. However, since the inauguration yield differences have declined as the realization that policy initiatives will take time and are likely to be moderated in scale as the legislative process moves forward. Tax cuts and fiscal stimulus through infrastructure spending will take time. Reflect on the observations that President Reagan's tax program did not pass Congress until August of his first year. The anticipation of the FOMC's increase in the funds rate in March provided a short-term boost to the benchmark rate but did not alter the broader downtrend to a level just above the pre-election level.

Euro/Dollar Spot and Economic Expectations: Caught in the Political Vortex

As illustrated in the middle graph, the euro/dollar exchange rate also exhibited a sharp reaction, in the short run, to the election and anticipation of economic change. Moreover, like benchmark yields, the exchange rate has drifted back toward pre-election levels. Finally, the U.S. PMI index has moved up and now back down as policy expectations have adjusted.

Credit Market Insights

Positive Attitudes Toward Housing

Earlier this week, the Federal Reserve Bank of New York released the results of its 2017 SCE Housing Survey which sheds light on consumers' expectations, behaviors and experiences related to home buying. The survey showed that more home buyers are expecting home prices to increase on a oneand five-year outlook. Moreover, a growing share of households still views owning a home as a sound financial investment.

That said, consumers' expectations for an increase in future mortgage rates have also increased, rising to 5.6 percent from 5.2 percent in 2016. Furthermore, sixty-five percent of renters still view obtaining a mortgage as difficult, but thought credit access was becoming easier. That said, tightening credit standards and rising mortgage rates (though still low) could make it more difficult and expensive for some to purchase a home.

What is encouraging is that renters are optimistic about their home buying prospects with 55.2 percent of those surveyed indicating that they will own a home at some point in the future. In fact, first quarter data for household formations showed the share homeowners rising to its highest level since Q3-2006, signaling that an increasing number of households are choosing home owning over renting.

With attitudes toward home buying remaining positive and more renters looking to own, we expect housing starts to reach 1.26 million units in 2017 and 1.35 million in 2018.

Topic of the Week

Emmanuel in Élysée

On May 7th the people of France elected 39 year old Emmanuel Macron as the leader of France, decisively defeating far-right leader Marine Le Pen (top chart). Having never held elected office, questions have risen over whether he can live up to his lofty campaign promises, which include significant economic reform. In his acceptance speech, Macron acknowledged the divisions and doubts disturbing France, but made a pledge to defend all peoples of France and Europe, making note of the common destiny of the European continent. Macron's staunchly pro-Europe stance stands in direct contrast to the rhetoric of his opponent.

Macron's pro-market agenda includes cutting regulation and improving education to boost competitiveness. Macron wants to cut 120,000 public sector jobs and take further measures to stabilize public finances. Moreover, reducing the unemployment rate to seven percent, from its current 10.1 percent level, is an objective of his administration. Other potential reforms include reducing the corporate tax rate to 25 percent from its current 33.3 percent rate. A 50-billion-euro investment program targeting specific industries such as renewable energy and transportation was also floated on the campaign trail. However, his reformist agenda could be undermined if he is unable to secure a favorable result in the parliamentary elections in June. Picking up seats in these elections should aid his legislative goals.

Macron is inheriting a French economy that is failing to gain traction and one that does not seem likely to break out any time soon. French GDP expanded just 1.2 percent in 2016 and has averaged just 0.8 percent on an annual rate over the past 5 years. Recently released GDP data for Q1 suggest the economy also started off 2017 on weak footing. GDP growth was just 0.3 percent on a sequential basis, and was just 0.8 percent, year over year (bottom chart). Macron's economic goals will likely be challenged by the weak French economy. However, consumer sentiment in France is rising, a signal that Macron has the people of France's confidence.

The Weekly Bottom Line

HIGHLIGHTS OF THE WEEK

United States

- Markets started the week off on a good note on French presidential election results and fairly constructive earnings and economic data. The S&P500 flirted with record highs, and the VIX fell to its lowest level in more than two decades.

- Sentiment soured later in the week as soft inflation data overshadowed a relatively robust retail spending report, with sales up 0.4% atop of an upwardly revised March gain. Total CPI inflation decelerated from 2.3% to 2.2% in April with the core measure slowing from 2.0% to 1.9% on the month.

- Expectations for a Fed rate hike as of June pared back slightly, but remained above 75% through this morning. Unless data continues to disappoint, we expect the Fed will raise rates next month, with another hike likely later on in the year.

Canada

- Canadian housing starts pulled back somewhat in April, but recent strength left the trend measure at 214k units, its fastest pace since late-2012.

- The Canadian dollar was down slightly on the week. The loonie has underperformed its peers so far this year, and speculative short interest has reached all-time highs, reflecting concerns around the health of Canadian housing and mortgage markets.

- At present, fears of a U.S.-style housing crisis appear overblown. The most likely scenario remains that headwinds to the market continue to intensify as we approach 2018, leading to a gradual cooling.

UNITED STATES - SOFT INFLATION DATA PARES JUNE HIKE EXPECTATIONS

Markets started the week off on a forward foot with rising confidence in the global economy, helped by last Friday's strong U.S. jobs report, further enhanced by the French presidential election results. The price investors demand to protect against volatility dropped, with the VIX falling early in the week, and touching its lowest level since 1993. U.S. equities were also supported by relatively strong earnings reports early in the week, with the S&P500 flirting with the 2,400 point level. Meanwhile a mild rebound in oil prices, following the bullish inventory report, shored up energy stocks since mid-week. The mood soured somewhat by the end of the week as a relatively good retail sales report was overshadowed by weak CPI data.

The election of Emmanuel Macron as President of France, the centrist candidate who ran on a platform of reform, was expected and largely priced in by markets. Still, it was a welcome development for global investors following the protectionist tilt in popular sentiment across many advanced economies over the past year. The result comes alongside some improvement in economic fortunes. This week, the European Union revised higher its Eurozone and U.K. growth outlook, with industrial production and employment growth in France coming in better than expected recently. But, while the new president has some political capital, he faces significant hurdles to enacting the much needed pro-growth reforms, with much riding on the results of the legislative assembly elections to take place in a month.

The U.S. data calendar was relatively light until Friday. The NFIB Index of Small Business Optimism held up well, while labor market strength was further confirmed by a strong job openings in March and a decline in both initial and continuing claims in early-May. Investors also had a number of Fed speeches to digest. Most of the speeches stuck to the script telegraphed by last week's FOMC policy statement, suggesting the Committee viewed the early-year weakness as transitory, and expected a firming in 'hard' economic data during the second quarter. Most Committee members continue to see a fair chance for two more hikes this year, and see the Fed beginning to wind down the balance sheet late this year or in early-2018.

The Fed's expectations were only partly confirmed by this morning's data. April's retail sales were shy of expectations, but nonetheless indicated more consumption momentum into the second quarter given the upward revisions to March spending figures. On the other hand, consumer price data matched expectations for 0.2% m/m as far as the headline print, but came in weaker after excluding food and energy prices with the core measure up a mere 0.1% m/m. After the unexpected decline in March, the softness in April, which saw the headline and core inflation measures slip to 2.2% and 1.9%, respectively, is likely to somewhat quiet those worried about the Fed falling behind the inflation curve.

While the soft CPI numbers may embolden a more dovish tilt within the FOMC, we believe that the strong April producer and import price data, which typically leads consumer prices, should help support the case for a rate hike. Moreover, while the soft CPI data has slightly pared back expectations for a move next month, markets continue to price in odds near 75%. Ultimately, unless the data continues to disappoint, we don't expect the Fed will pass on the opportunity to raise rates next month.

CANADA - HOUSING CONCERNS KEEP LOONIE WEAK

It was a light week for economic data in Canada, and accordingly, markets did not see any major moves. The S&P/TSX equity index was down slightly at the time of writing, despite some gains in crude oil prices as the week progressed. Equity markets at the moment appear more focused on events related to Canadian housing markets, including the downgrade of major Canadian banks by credit rating agency Moody's. Concordantly, the Canadian dollar remained volatile, and appeared likely to end the week down, continuing the theme of weak performance this year.

In the only major economic datapoint of the week, Canadian housing starts pulled back a bit in April, dropping back a notch to 214k units after a red-hot March print (252k). The pullback was relatively broad-based: the volatile multi-family segment saw a sizeable drop (-33k units), but so too did the more stable single family construction (-9k). Ultimately, the pace observed in April is likely more in line with underlying trends, but more near-term volatility in the figures is likely as builders in Ontario digest the recently announced 'Fair Housing Plan'. Aspects of the plan are positive for housing supply, such as an accelerated project approvals process. Conversely, changes around assignment sale rules may dent demand and crimp future supply.

Despite all indications pointing to robust GDP growth in the first quarter of 2017 and a steady expansion thereafter, sentiment towards Canada appears to have soured recently, reflected in a currency that has significantly underperformed its peers (Chart 1). The U.S. administration's remarks on NAFTA certainly haven't helped, but the more likely culprit appears to be perceived weaknesses in the financial system underpinning the housing market. The events surrounding Home Capital Group were a catalyst, with non-commercial (i.e. speculative) short interest in the Canadian dollar spiking following the announcement of further regulatory investigation. Indeed, since then, short interest has continued to climb, reaching an all-time high last week (Chart 2; this week's positioning data will be published later this afternoon).

Although housing markets are the key risk to the Canadian economy, fears of a U.S.-style housing crisis appear overblown. A string of macroprudential tightening measures in recent years may not have had much of a cooling effect, partly due to falling interest rates, but they have helped to reduce risks by improving underwriting standards. While reliable data on the 'shadow' mortgage market is scarce, growth appears to have outpaced the overall market in recent years. Still, such lending is a relatively new phenomenon, and its share of outstanding mortgages likely remains small.

Thus, while the risk of a correction cannot be dismissed, the more likely scenario is one of mounting headwinds. These would take the form of a gradual rise in borrowing costs, stretched affordability, the ongoing impact of past and recent cooling measures, and the potential reduction of credit availability from marginal lenders. Together these should serve to cool the hottest Canadian housing markets as we move into the latter half of the year and into 2018. Some frictions in this process are inevitable, but on balance we continue to expect a gradual, orderly deceleration of housing activity.

Week Ahead Dollar Looking to Regain Momentum

Political risk to dominate thin calendar of economic events

The US dollar will finish the week ending May 12 higher across the board against major pairs. Despite the dollar rally losing steam as softer economic data was released the U.S. Federal Reserve kept the June rate hike on the table boosting the greenback on a monetary policy divergence basis. The central banks of New Zealand and England issued statements this week and made it clear that there are no rate changes coming soon, unlike the US central bank. The miss in inflation and sales could only highlight a temporary problem as the May 7 U.S. non farm payrolls (NFP) added 211,000 jobs still points to a solid recovery.

The market is pricing in a 73.8 percent probability that when it meets on June 14 it will raise interest rates to a 100-125 basis points range. Weaker US data has brought it down from 83.1 percent yesterday but taking Fedspeak into consideration it remains a firm possibility. Federal Open Market Committee (FOMC) members have seen the number of speeches they deliver increase which better prepares the market for upcoming decisions. The FOMC meeting in March was a great example as Fed members warned investors that they were not pricing in an upcoming rate hike. The meeting in June become a test of trust. The Fed has been typically vague in their timing but is now dropping far more hints without resorting to outright guidance.

The week of May 15 to May 19 will feature little in the way of economic events. The market will focus on data out of the UK, with UK inflation to be released on Tuesday, May 16 at 4:30 am EDT and retail sales on Thursday, May 18 at 4:30 am EDT. The Bank of England (BoE) kept rates unchanged last week and the central bank issued a warning of the lack of wage growth as inflation is rising to a forecasted 2.8 percent in 2017. The BoE also reduced economic growth forecasts to 1.9 percent as the pound has been weaker ahead of Brexit.

The EUR/USD lost 0.601 in the last five days. The single currency is trading a 1.0932 after investors sold the EUR following the results of the second round of the French presidential election. The victory of Emmanuel Macron was correctly forecasted by pollsters and while the market breathed a sigh of relief it also took sold the EUR as it deemed the currency would not keep gaining ground.

Dovish comments from European Central Bank (ECB) president Mario Draghi kept the currency from appreciating versus the USD. In the other hand U.S. Federal Reserve members are keeping the June interest rate hike alive by talking about the need to act sooner rather than later and keep the hope of four rate hikes alive this year.

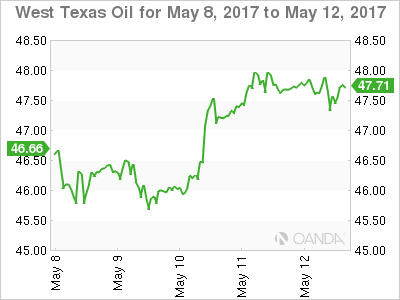

The price of crude gained 3.08 in the last week. West Texas is trading at $47.59 after a massive drawdown of weekly inventories in the US ended a string of losses for energy prices. The Organization of the Petroleum Exporting Countries (OPEC) has also been active with comments around the success of its production cut agreement and the high probability of an extension to be announced at the meeting with other major producers on May 25.

The Energy Information Administration (EIA) reported a 5.2 million barrels draw for the week ending May 5. Gasoline inventories fell by 200,000 which is feeling optimism ahead of the start of the US driving season. The drawdown in US energy stocks boosted the price of oil as it lined up with OPEC's release of data confirming their production limits, but the fact that there is low demand for energy and US producers, not bound by any agreement, are ramping up production to take advantage of current price levels will keep the price of crude volatile.

The USD/MXN lost 1.372 percent in the last five days. The currency pair is trading at 18.7523 after the political uncertainty in the US is removing downward pressure on the Mexican currency as the topic of trade and immigration is not top of the US political agenda until the turmoil in the White House can be resolved. Oil prices have also boosted the performance of the peso with lower inventories in the US driving crude prices higher. Mexico is part of the OPEC production cut and is expected to take part in the extension that will be announced on May 25.

The MXN was trading higher after the disappointing sales and inflation data out of the US on Friday morning. The Mexican peso went form being one of the worst performers during the US presidential elections and up to the inauguration of Donald Trump, only to quickly regain ground in 2017. Economic fundamentals have not changed much in that time frame, but political risk and risk aversion have dictated the price of the peso as it is used as proxy for other emerging market currencies.

Market events to watch this week:

Sunday, May 14

- 6:45 pm NZD Retail Sales q/q

- 10:00 pm CNY Industrial Production y/y

Monday, May 15

- 9:30 pm AUD Monetary Policy Meeting Minutes

Tuesday, May 16

- 4:30 am GBP CPI y/y

- 8:30 am USD Building Permits

- 6:45pm NZD PPI Input q/q

Wednesday, May 17

- 4:30 am GBP Average Earnings Index 3m/y

- 8:30 am CAD Manufacturing Sales m/m

- 10:30 am USD Crude Oil Inventories

- 9:30 pm AUD Employment Change

- 9:30 pm AUD Unemployment Rate

Thursday, May 18

- 4:30 am GBP Retail Sales m/m

- 8:30 am USD Unemployment Claims

Friday, May 19

- 8:30 am CAD CPI m/m

- 8:30 am CAD Core Retail Sales m/m

*All times EDT