Sample Category Title

Pound Remains Under Pressure Following BoE Growth Downgrade

If investors were looking for a reason to sell the Pound at its recent elevated levels, they found encouragement yesterday when the Bank of England (BoE) downgraded its growth forecast for the UK economy in 2017. Although a growth downgrade from 2% to 1.9% is hardly significantly material in the grand scheme of things, it has been used by traders as motivation to drag the Pound lower with the GBPUSD currently under pressure as trading concludes for the week.

The question to ask moving forward is which direction the Pound could take next. My personal opinion is that the BoE's negative views on inflation pressures should weigh on investor sentiment for a while. In addition, there is another major potential event risk for the Pound ahead with the General Election just a month away.

Just because Theresa May is seen as the most likely candidate to win the election next month, it doesn't mean that there won't be volatility in the Pound during the run up to the event. My view is also that investors have underpriced the risk of May not being victorious, meaning there could be some serious shuffling of positions if preliminary polls suggest that Theresa May does have a fight on her hands.

Another factor to consider in the future is how the prolonged Brexit negotiations with the European Union are likely to be, which is going to be quite a drag in the sand if I am honest with you. It shouldn't be misunderstood that the economic sentiment in Europe is gradually picking up decent momentum, and this could in fact provide the EU with some negotiating power when it comes to saying that it might be able to stand on its own feet with the United Kingdom as a fellow member.

Recent comments from Theresa May where she seemed to accuse the EU of influencing the upcoming elections are also not going to help secure the UK any leniency when it comes to a trade deal with Europe, if she ends up being the one to lead with negotiations that is.

EUR/USD Tests Support Ahead of US Retail Sales and CPI

EUR/USD has retraced around 1.15% post the second-round vote of the French presidential election.

The retracement was held above the support line at 1.0850 since yesterday.

On the 4-hourly chart, the 10 SMA is crossing over the 20 SMA, indicating the bearish momentum is waning.

The daily Stochastic Oscillator reading is below 20, suggesting a rebound.

However, if the support line at 1.0820 is broken, then we can expect an extended downtrend.

We will see the release of a set of crucial US data for April at 13:30 BST today; retail sales, retail sales excluding autos, CPI and core CPI. Please be aware that it will likely affect USD and USD crosses along with commodities.

With better-than-expected readings, it will likely weigh on EUR/USD, and tests supports.

With lower-than-expected readings, it will likely push EUR/USD up, and tests resistances.

The resistance level is at 1.0880, followed by 1.0900 and 1.0930.

The support line is at 1.0850, followed by 1.0835 and 1.0820.

The Correction on the “Black Gold” Market May Continue

Bears dominate on the oil market since April. I'd like to remind that earlier recommended selling oil to USD 50.00 and it has hit that mark. Futures for #CL have decreased by more that 16%. WTI has fount its support at 44.25 USD.

There was an abrupt turn of the quotes yesterday. Oil grew by more than 3% thanks to the support of the EIA. The US oil inventories have fallen by 5.247 million barrels during the previous week. Note, that the expectations were at the 1.786 million barrels mark. This decrease took place because of bad weather in the Gulf of Mexico.

Conclusions of the EIA Report:

- oil reserves: -5.247 million barrels;

- oil production: + 21 thousand barrels per day (=9.314 million)

- distillates stocks: -1.587 million barrels;

- gasoline stocks: -0.150 million barrels;

Everybody is waiting for the OPEC meeting at the moment to know about the outcome of the discussion of the production reduction. It will be help on May 25.

Trading recommendations:

Support levels: 47.00 USD, 44.25 USD

Resistance levels: 49.25 USD, 51.85 USD, 53.50 USD

Bulls dominate on the market now. The technical pattern shows a possibility of a correction. Here are the signals that indicate it:

1) the MACD indicator has reached the positive zone. It Is still rising now.

2) Bullish Engulfing, a strong reversal PA pattern, has emerged on the daily chart.

I'd recommend you buying oil after the price reaches the 48.15 USD local resistance level. 49.25 USD may be a goal for taking profit. I think that #CL may go to 50.00 and 51.50 USD marks in the medium term. These marks are the 61.8% and 78.6% correction levels. Use a trailing stop while working with this position.

USD/JPY Daily Confluence At Support

The USD/JPY is currently supported at POC zone 113.40-60 (Trend line, D L3, Order block, EMA89) and we might see a spike towards D L3 - 114.10. The pair is in uptrend on intraday (H1) and intra week (H4) charts. 1h or 4h candle close above 114.10 should provide additional strength in this pair, targeting 114.35 (ATR high) and 114.75 (D L5) if we see additional volatility. W H3 and ATR low should hold (113.15) if bulls want to remain in control. Bears would only have control below D L5 (112.90). If that happens during next days we might expect 112.15 as the target.

Pound Tumbles after BoE Downgrades its Inflation Forecasts

On its second "Super Thursday" of the year, the BoE kept its policy unchanged via a 7-1 vote, in line with the consensus. The lone dissenter was Forbes again, who voted for a hike, but considering that she is leaving the Committee in June, her dissent may have carried less importance for investors. There was speculation that we may have had another member, Saunders, dissenting this time. However, he preferred to stand pat, which may have come as a disappointment to those who were expecting a second vote for a rate increase. Turning to the Inflation Report, the BoE lowered its inflation projections for 2018 and 2019, which diminishes further the probability for a hike due to inflation overshooting in the foreseeable future. As a response to these, the pound tumbled.

The only point that appeared hawkish on a first glance was the final sentence of the minutes. The Bank noted that if the economy remains robust, policy could be tightened by a somewhat greater extent than the market yield curve currently implies. However, after digging into the Inflation Report, we noticed that both the market and the Bank have pushed back their expectations for a 25bps rate increase. The market just pushed it back further. According the market, such a move is fully priced in for Q4 2019, so even one quarter earlier is in line with the Bank's view, and is thus not as hawkish as it initially appears.

All these signals from the BoE confirm our view that the Bank is likely to remain on hold throughout this year, and even the next one if the data evolve more or less in line with expectations. As for the pound, we think that GBP traders are now likely to turn their attention back to developments surrounding the upcoming General Election. In our view, incoming opinion polls that show the Conservatives maintaining or extending their current lead could support sterling as we approach Election Day.

GBP/USD slid following the Bank's signals, falling below the (support now turned into resistance) barrier of 1.2900 (R1) to hit the key hurdle of 1.2850 (S1). Then the rate rebounded somewhat. The pair has been oscillating between that hurdle and the psychological zone of 1.3000 (R2) since the 27th of April, so given our proximity to the lower end of that range, we see the likelihood for further rebound in coming days. A break back above 1.2900 (R1) could confirm our view and is possible to set the stage for another test near the round figure of 1.3000 (R2).

Today's highlights:

During the European day, we get Germany's preliminary GDP data for Q1 and the forecast is for economic growth to have accelerated. We also get the nation's final CPI for April, as well as Eurozone's industrial production for March, though none of these indicators is usually a major market mover.

From the US, we get US CPI and retail sales data, all for April. Kicking off with the CPIs, the forecast is for the headline rate to have ticked down, and for the core rate to have remained unchanged. In case of an unchanged core print, we think that investors may focus primarily on retail sales, which come out at the same time. Both the headline and core retail sales rates are expected to have risen notably in monthly terms. Following two consecutive months of soft prints, we think that a rebound would be encouraging news for FOMC policymakers, who at their latest policy gathering noted they expect GDP growth to pick up speed in Q2. Strong retail sales could be a sign the US economy entered Q2 on a solid footing, and may thereby bring USD under renewed buying interest. We also get the nation's preliminary U of M consumer sentiment index for May.

USD/JPY traded lower yesterday after it hit again resistance at 114.35 (R1). Nevertheless, the setback was stopped by the short-term uptrend line drawn from the low of the 21st of April, near the 113.50 (S1) support area. Strong retail sales today may encourage the bulls to take advantage of yesterday's retreat and pull the trigger for another test at the 114.35 (R1) obstacle. If they manage to overcome it, they may set their sights on the next resistance of 114.90 (R2).

We have three speakers on the agenda: ECB Vice President Vitor Constancio, Chicago Fed President Charles Evans and Philadelphia Fed President Patrick Harker.

Will CPI And Consumer Data Signal A Q2 Rebound?

It's been a relatively flat start to trading on Friday but things should pick up as we approach the US session, with retail sales and inflation data due to be released, among others, and the Fed's Charles Evans scheduled to appear.

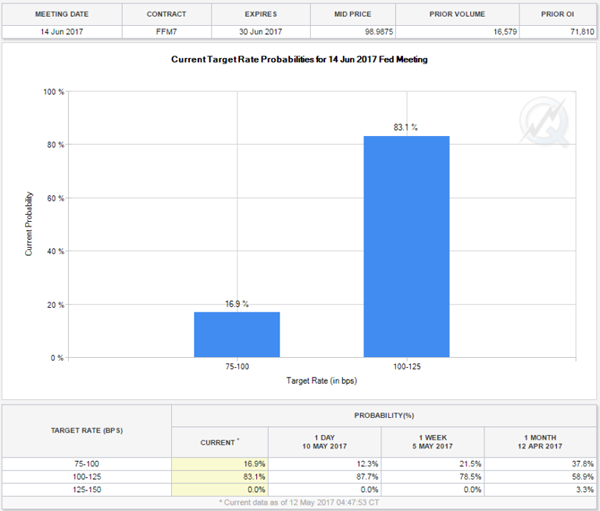

Will Investors Be So Confident on June Rate Hike if Data Doesn't Rebound?

With the Federal Reserve looking to raise interest rates twice more this year and markets eyeing June for the next hike – 83% priced in based on Fed Funds futures – today's inflation and consumer figures are going to be closely followed.

While CPI may not be the Fed's preferred measure of inflation, it will offer insight into whether inflationary pressures are building or the trend of the last couple of months is continuing. That may prove to be a concern for the Fed ahead of the June meeting.

CAC Quiet as French Nonfarm Payrolls Beats Estimate

We'll also get insight into the US consumer, a very important part of the economy, with the release of retail sales data for April and UoM consumer sentiment data for May being released. It's been a disappointing couple of months for the US consumer but we're expecting a rebound this month, with sales seen rising by 0.6%, while consumer sentiment is seen holding at 97, very close to its multi-year highs. The tendency of the US to slow in the first quarter – as noted by the Fed in its statement last week – appears to be once again responsible for the weakness in recent inflation and spending figures, today could offer some insight into whether we'll see a similar second quarter rebound this year.

Gold Follows Copper and Oil Higher

Will One of the Fed's Most Dovish Members Support Higher Rates?

Charles Evans speech later today could offer some insight into the June meeting, with him being among the more dovish voting members of the committee. Should he allude to a rate hike next month then it would suggest there's relatively little opposition and markets are relatively well positioned, although there is still some room for it to be increasingly priced in.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had another indecisive movement yesterday. Price slipped below 1.0850 but still closed above the key support as you can see on my H1 chart below. The bias is neutral in nearest term. 1.0850 area remains a good place to buy with a tight stop loss as a clear break below that area would expose the pre-gap level at 1.0730 and the trend line support. Immediate resistance is seen around 1.0900. A clear break above that area could trigger further bullish pressure testing 1.0950 area and keeps the bullish outlook intact. Overall I remain neutral.

GBPUSD

The GBPUSD had a bearish momentum yesterday bottomed at 1.2848 but closed a little bit higher at 1.2888. The triple top formation I told you about yesterday gave us a valid bearish signal. The bias is bearish in nearest term testing 1.2830. A clear break below that area would expose 1.2780 region which is a good place to buy with a tight stop loss. Immediate resistance is seen around 1.2915. A clear break above that area could lead price to neutral zone in nearest term testing 1.2950 or higher. Overall I remain bullish.

USDJPY

The USDJPY was corrected lower yesterday bottomed at 113.45 but closed a little bit higher at 113.85. The bias is neutral in nearest term. 113.60 area remains a good place to buy with a tight stop loss as a clear break below that area would expose 113.00 or lower. Overall price is still in a bullish trend, but need a clear break above 114.35 to continue the bullish scenario testing 115.00 or higher.

USDCHF

The USDCHF had another indecisive movement yesterday. The bias is neutral in nearest term but overall price is still in a bullish phase after broke above the trend line resistance as you can see on my H4 chart below targeting 1.0170 area. Immediate support remains around 1.0050. A clear break back below that area would interrupt the bullish scenario testing 1.0000 region. Overall I remain neutral.

CAC Quiet As French Nonfarm Payrolls Beats Estimate

The CAC continues to drift this week. In the Friday session, the index is at 5386.00 points. On the release front, euro area data was mixed. French Nonfarm Payrolls posted a gain of 0.3%, edging above the estimate of 0.2%. German Preliminary GDP climbed 0.6% in the first quarter, matching the forecast. However, Eurozone Industrial Production contracted 0.1%, marking its third decline in four months. The weak reading missed the estimate of +0.3%. It's a busy day in the US, with the release of key consumer spending and inflation reports.

Germany is the locomotive of the eurozone, and strong numbers in the largest economy in Europe has boosted eurozone growth. The forecast for German Preliminary GDP was on target, as the economy expanded 0.6% in the first quarter, compared to a 0.4% gain in Q4 of 2016. The upswing was broadly based in the economy, with strong consumer and state spending, and an upsurge in the construction and manufacturing sectors. Stronger global demand has boosted German exports, notably for automobiles and machinery. However, inflation continues to recede, as Final CPI dropped to 0.0%. This trend has also characterized inflation in the eurozone, which rose earlier in the year but has since retracted.

Anytime Mario Draghi is talking, the markets are all ears. The ECB president spoke about monetary policy before a Dutch parliamentary committee on Wednesday, but there was nothing new in his remarks. Draghi reiterated that the ECB continues to monitor growth and inflation levels, but has no plans at present to modify its monetary policy. Draghi said that that central bank would tighten its policy once the 'tail risks' of a drop in inflation receded and growth improved. Currently, the ECB is making monthly purchases of EUR 60 billion under its asset-purchase scheme, which is scheduled to expire in December. Inflation levels were higher in the first quarter, which led to calls for Draghi to tighten policy. However, the ECB was reluctant to make any moves during the French election campaign, and this aversion could continue, with Germany holding elections in September. The central bank appears satisfied with the status quo, and can be expected to hold course, unless eurozone growth and inflation levels climb sharply.

ECB Study Shows Eurozone Unemployment Higher than Official Data

President Donald Trump appears to have badly misjudged the ramifications in firing FBI director James Comey. The firing has set off a political firestorm in Washington, with Trump facing accusations of triggering a constitutional crisis and undermining the rule of law. Comey had been conducting an investigation into possible collusion between Trump and Russia during the presidential campaign, so predictably, Comey's dismissal has raised suspicions that Trump is trying to impede the investigation by firing Comey. The crisis could heat up further, with calls in Congress to appoint an independent investigator into Trump's connections with Russia. This latest political storm has yet to shake up the markets, but a prolonged crisis could paralyze Washington and delay Trump's agenda of tax reform and increased fiscal spending.

DAX Steady As German GDP Climbs 0.6%

The DAX index has had an uneventful week, and is showing limited movement in the Friday session. Currently, the DAX is trading at 12,717.25. On the release front, German Preliminary GDP gained 0.6%, matching the forecast. German Final CPI came in at a flat 0.0%, also matching the estimate. Eurozone Industrial Production contracted 0.1%, marking its third decline in four months. The weak reading missed the estimate of +0.3%. It's a busy day in the US, with CPI and Retail Sales reports for April.

German economy has posted solid numbers in recent months, and the forecast for Preliminary GDP was on the money, as the economy expanded 0.6% in the first quarter, compared to a 0.4 gain in Q4 of 2016. The upswing was broadly based in the economy, with strong consumer and state spending, and an upsurge in the construction and manufacturing sectors. Stronger global demand has boosted German exports, notably for automobiles and machinery. However, inflation continues to recede, as Final CPI dropped to 0.0%. This trend has also characterized inflation in the eurozone, which rose earlier in the year but has since retracted.

The eurozone economy received a passing grade on Thursday, as the European Commission released its Spring 2017 Economic Forecast. The report noted that the European economy is in its fifth year of recovery, and forecast eurozone GDP growth of 1.7% in 2017 and 1.8% in 2018. On the inflation front, the report stated that inflation had risen in recent months, but this was mainly due to an increase in oil prices. Still, inflation was expected to reach 1.6% in 2017 and 1.3% in 2018, compared to just 0.2% in 2016. Stronger growth has led to lower unemployment, and the report projected that eurozone unemployment rate would drop to 9.4% in 2017 and 8.9% in 2018. The report reiterated what ECB president Mario Draghi has long been saying, namely, that risks to the eurozone economy remain tilted to the downside. These risks include US economic and trade policy under President Trump, the banking sector in Europe and the UK's exit from the EU. This forecast is considerably more optimistic than the Winter 2017 forecast, as is apparent from the captions in the press releases for these two reports: The Winter forecast was entitled “Navigating through choppy waters”, while the caption for the Spring forecast reads “Steady growth ahead”.

ECB President Mario Draghi addressed a Dutch parliamentary committee on Wednesday, and reiterated that the ECB continues to monitor growth and inflation levels, but has no plans at present to modify its monetary policy. Draghi said that that central bank would tighten its policy once the “tail risks” of a drop in inflation receded and growth improved. Currently, the ECB is making monthly purchases of EUR 60 billion under its asset-purchase scheme, which is scheduled to expire in December. Inflation levels were higher in the first quarter, which led to calls for Draghi to tighten policy. However, the ECB was reluctant to make any moves during the French election campaign, and this aversion could continue, with Germany holding elections in September. Bottom line? We can expect the ECB to hold course, unless eurozone growth and inflation levels climb sharply.

President Donald Trump's firing of FBI director James Comey could have been viewed as yet another controversial move by the temperamental president , but the firing has set off a political firestorm in Washington. Trump has been accused of triggering a constitutional crisis and undermining the rule of law. Comey had been conducting an investigation into possible collusion between Trump and Russia during the presidential campaign, so predictably, Comey's dismissal has raised suspicions that Trump is trying to impede the investigation by firing Comey. The crisis could heat up further, with calls in Congress to appoint an independent investigator into Trump's connections with Russia. This latest political storm has yet to shake up the markets, but a prolonged crisis could paralyze Washington and delay Trump's agenda of tax reform and increased fiscal spending.

GOLD Short-Term Bearish, SILVER Short-Term Bounce At $16.00, CRUDE OIL Bullish Consolidation.

GOLD Short-term bearish.

Gold continues its decline after the yellow metal has faded near the hourly resistance at 1295 (18/04/2017 high). Hourly support is now located at 1195 (10/03/2017 low). The road is wide-open for further decline.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Short-term bounce at $16.00.

Silver's bearish pressures are still lively despite short-term consolidation. Strong support is given at 15.63 (20/12/2017 low). Closest support is given at 16.20 (04/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). Expected to see continued bearish pressures.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Bullish consolidation.

Crude oil is bouncing back on short-squeeze move. The commodity has bounced from a level below $48. Support is given at 43.76 (05/05/2017 low). Expected to see renewed bearish pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).