Sample Category Title

Currencies: Dollar Maintains Most of Recent Gains Ahead of Key data

Headlines

European equity markets corrected lower today with the telecom sector underperforming. US stock markets opened around 0.25% in the red.

NY Fed Dudley said that the Fed will probably begin shrinking its balance sheet sometime later this year or in 2018 if economy stays on track. They will allow both MBS and Treasuries to run off. He added that there's no great urgency for the Fed to tighten aggressively though.

The BoE kept its policy unchanged with one member again voting in favour of an immediate rate hike. The BoE suggested interest rates could rise towards more normal levels over the next three years if Brexit negotiations go smoothly, but said it had been overoptimistic about economic performance for the first half of this year.

US shale oil output is growing at a faster than expected rate, keeping pressure on prices despite steep supply curbs from some of the world's biggest producers, Opec said in its monthly market report.

The European Commission revised upward its forecasts of euro zone economic growth this year and projected a lower unemployment rate, in new signs that the bloc's recovery is gathering pace. The 19-country currency bloc is expected to expand by 1.7% this year and 1.8% in 2018.

Banks' "unconstrained" ability to generate credit by pledging the same assets as collateral multiple times needs to be curbed or risks creating a new financial bubble, ECB vice president Constancio said. His remarks underscored the ECB's concerns about the prospect of a new boom in lending between financial firms

British industrial output shrank for a third month in a row in March (-0.5% M/M) underscoring how the impact of last year's Brexit vote has begun to weigh on the economy. The ONS also said Britain's trade deficit widened by more than expected, a further setback for hopes that sterling's fall would help rebalance the economy.

US weekly jobless claims stabilized around historical lows (236k) while markets expected a small setback to 245k. Continuing claims declined to a 28-yr low at 1918k. The bigger-than-forecast rebound in April producer prices indicates inflation pressures continue to build in the US economy and that March's decline was short-lived.

Rates

US Note future tests this week's low after strong data

Global core bonds continued to trade choppy. The Bund faced immediate selling pressure, but equity weakness came to the rescue and prevented losses. The EC only marginally upgraded its 2017 growth forecast, while keeping it unchanged in 2018 which avoid more ECB exit speculation. Heavyweight NY Fed governor Dudley suggested that the Fed will allow both MBS and US Treasuries to run-off, starting at the end of this year or the beginning of next. He added that there's no hurry to tighten policy though. His comments fell on deaf ears. US eco data, even if they were second-tier, managed to change the intraday tide. Weekly jobless claims remained near historically low levels while producer prices rose faster than forecast. US Treasuries recorded new intraday lows while German Bunds lost ground as well. Brent crude managed to hold above the key $50/barrel mark.

At the time of writing, the German yield curve bear steepens with yield 1 bp (2- yr) to 3.1 bps (30-yr) higher. Changes on the US yield curve range between +0.3 bps (10-yr) and +1.3 bps (30-yr). On intra-EMU bond markets, 10-yr yield spreads changes versus Germany range between -1 bps and +2 bps with Portugal (-3 bps) and Greece (-5 bps) outperforming.

The Italian debt agency tapped the on the run 3-yr BTP (€2.44B 0.35% Jun2020), 7-yr BTP (€2.25B 1.85% May2024), 30-yr BTP (€1.25B 2.7% Mar2047) and the off the run BTP (€1.25B 4.75% Sep2044). The combined amount sold (€7.19B) was near the upper end of the €5.5-7.25B target range. The auction bid cover was 1.51 which is rather strong for Italian standards. Tonight, the Treasury ends its refinancing operation with a $15B 30-yr Bond auction. Currently, the WI trades around 3.05%.

Currencies

Dollar maintains most of recent gains ahead of key data

Today, EUR/USD and USD/JPY initially drifted sideways. Both cross rates lost ground as equities finally fell prey to modest profit taking. The US eco data (PPI and claims) were better than expected. Core yields rose slightly, but were not able to trigger more USD gains. The focus for USD trading is on tomorrow's US CPI and retail sales. EUR/USD trades in the 1.0855/60 area. USD/JPY struggles not to fall below 114.

Overnight, most Asian equity indices gained ground with the Nikkei and the Korean indices at multi-month highs. Mainland China equities initially underperformed but staged a remarkable rebound towards the close. Until now the Chinese underperformance had little impact on other markets, but the issue deserves close monitory. USD/JPY (114.20) remained in risk-on modus, holding within reach of the recent highs. EUR/USD stabilized the 1.0865 area.

Early in Europe, there was again no clear directional momentum in European equities nor in EUR/USD and USD/JPY. The EU commission forecasts were revised only marginally higher and no market mover. At the onset of the US trading session, sentiment on risk gradually faltered. The correction weighed on EUR/JPY, EUR/USD and, to a lesser extent USD/JPY. The US PPI and jobless claims were stronger than expected and triggered some modest gains of the dollar against the euro. EUR/USD trades currently in the 1.0850/60 area. So, the price action in the cross rate was both due a pinch of risk-off and a small piece of USD strength. The US eco data also help to prevent a further USD/JPY decline. The pair stabilizes near 114. However, some further topping out might be on the cards if sentiment on risk would worsen more on China or for whatever other reason including simple profit taking.

Sterling ceding ground post-BoE decision.

Today, UK March production data and the trade balance were substantially weaker than expected. Sterling lost temporary ground upon their publication, but EUR/GBP drifted back to the low 0.84 area going into the BoE policy decision and inflation report. The Bank of England kept a balanced approach as it said that 'Monetary policy cannot prevent either the necessary real adjustment as the United Kingdom moves towards its new international trading arrangements or the weaker real income growth that is likely to accompany that adjustment over the next few years'. The Bank indicated that an earlier rate hike might be needed in case of a smooth Brexit,. However, what are the chances for this scenario? The moves in sterling remained modest, but the market apparently concluded that the BoE will give slightly more weight to supporting growth rather than fighting inflation. The vote was again 7-1 for an unchanged decision. There was no additional support for a rate hike, what some apparently expected. EUR/GBP trades currently in the 0.8445/50 area. Cable is drifting further away from the 1.30 resistance and trades currently in the 1.2860 area.

Inflation Pressures Remain Modest

The consumer price index (CPI) rose 0.2%m/m in April, as expected by markets. On a year-on-year basis inflation was 2.2%, a continued deceleration from its 2.8% peak in February.

It was necessities that took prices higher in April. Indices for shelter (+0.3%), energy (+1.1%), tobacco (+4.2%) and food (+0.2%) all rose on a monthly basis.

Leaning against these price increases, many categories saw falling prices, including apparel (-0.3%), education/communication (-0.3%), medical care (-0.2%), and new and used vehicles.

This tug of war between various categories left core inflation up a modest 0.1% (m/m) in April, after a surprising 0.1% drop in core prices in March. That leaves core inflation at 1.9% on a year-on-year basis, its slowest pace since October 2015.

The recent softening in core inflation is a result of continued deflation in core goods prices, down 0.6% year-on-year, and now a slowing in core services prices. Core services inflation had run as strong as 3.2% last fall, but has now decelerated to 2.7%.

Key Implications

April's CPI data provided some reassurance that there are still inflationary forces in the economy. However, the softening in recent months in core inflation may cause some concern for the Fed as it considers its next rate move. The Fed is very much in data dependent mode, and it will need to balance a red hot job market with an inflation picture that has a bit less oomph than it would like.

Overall, we expect the Fed to keep the faith on price pressures building down the line reflecting a strengthening economy. Price pressures in other measures, like the producer price index, showed heartier gains in April, and suggest higher inflation is on its way. So long as the economic data continues to cooperate over the next month, the Fed looks set to raise rates another quarter point in June.

Retail Sales Rebound in April, Strengthening Case for June Hike

Retail sales increased 0.4% in April according to the advance Census Bureau report. While this was slightly shy of expectations for a 0.6% rise, upward revisions to March sales - which are now reported to have grown by 0.1% instead of a 0.2% decline - more than made up for the miss.

Sales at motor vehicle & parts dealers (+0.7%) helped the headline, while gasoline station sales rose by a more muted 0.2%. Excluding autos and gas, retail sales were up 0.3% on the month, or slightly slower than the previous months' upwardly revised gain of 0.4% (previously reported as 0.1%).

Excluding gas, autos, building materials (+1.2%), and food services (+0.4%), the so-called 'control group' used in calculating GDP was up just 0.2% on the month. This was half the expected pace but comes atop of upward revision to 0.7% gain in the previous month. Gains in the control group were broad, with electronics (+1.3%), health and personal care (+0.8%) and sporting goods (+0.6%) showing strong gains together with the persistently outperforming e-commerce (+1.4%) . These were somewhat offset by 0.5% declines in the furniture, clothing, and general merchandise stores.

Key Implications

This was a healthy report all things considered. Despite the headline print falling shy of expectations, revisions to previous month's sales more than made up for miss. Together with the relatively muted price changes, the number suggests a fairly strong consumption profile at the start of the second quarter, with PCE likely to advance by nearly 3.5% during Q2.

Another encouraging element was the breadth of the gains themselves, with particular strength in building materials and discretionary spending categories. The former suggests that the healing housing market is spurring increasing renovation activity, which is a positive for residential investment. The latter indicates that consumers are spending on wants in addition to needs, and hints at the notion that strong job growth and rising wages are boosting confidence - something that we expect will continue supporting consumption.

The report is likely to further assuage fears that the weakness in the first quarter will spill over into the rest of the year. As such, it will likely strengthen the case for the Fed to raise rates next month despite the weaker-than-expected April CPI print released this morning. All in all, we expect the Fed will move in June, with another hike still likely during the second half of the year.

U.S. April Retail Sales Point to Stronger Q2 Consumer Spending

Highlights:

- April retail sales rose 0.4% to build on a 0.1% increase (previously reported as -0.2%) in March.

- Motor vehicle sales rose 0.8%, gasoline station sales inched up 0.2%, and building material store sales rose 1.2% after falling 1.7% in March.

- 'Control' (excluding motor vehicles, building materials and gasoline stations) sales rose 0.2% following a 0.7% jump in March.

Our Take:

The 0.4% gain in April retail sales was only slightly below expectations for a 0.6% increase and followed an upwardly revised March gain (now reported as up 0.1% versus the previous -0.2%). On balance, spending over the last two months is in line with the view that the slowing in Q1 real consumer spending growth, to just a 0.3% annualized pace, was more the result of 'normal' volatility in the data and a weather-related pull-back in utilities consumption than the beginning of a new weaker trend. Strong employment growth, rising wages and consumer confidence, and the still stimulative stance of monetary policy are all pointing to a solid household spending backdrop and the recent data remains in line with our forecast for a 2.8% increase in consumer expenditures in Q2 that we expect will support a 2.9% increase in GDP (following the surprisingly modest 0.7% Q1 gain.) Along with continued improvement in labour markets — the unemployment rate fell to a new cycle low of 4.4% in April — the data will provide reassurance to the Fed that the fundamental economic backdrop remains strong and, if anything, further increases the odds of another hike to the fed funds target range when monetary policymakers next meet in June.

US Inflation Rates Edged Down in April But Remained Near 2%

Highlights:

- The all items index rebounded by 0.2% in April but the year-over-year rate slipped to 2.2% from 2.4% in March.

- Higher energy prices (+9.3% from last year) continued to boost headline inflation.

- Consumer prices excluding food and energy rose by less than expected (+0.1%) following a 0.1% dip in March that was just the second monthly decline in decades.

- Rising shelter costs offset declines in a number of other core components in April.

- Year-over-year core inflation slipped to a 1½-year low of 1.9%.

- Prices for wireless telephone services declined again in April; a more substantial 7% drop in March shaved about 0.1 percentage point off of headline inflation.

Our Take:

Inflation has come off the boil in the last two months, though we don't see the latest data standing in the way of a June rate hike. Following last week's labour market report that showed a rebound in job growth and 4.4% unemployment rate, there seems to be a bit more urgency from Fed officials to continue removing accommodation. Whereas, a year ago, a slow start to the year led to a more cautious approach from the Fed, policymakers now seem more than willing to look through soft Q1 GDP. Inflation and wage data isn't yet signaling a sharp tightening in monetary policy is required, but with unemployment at a 16 -year low and inflation hovering around 2%, we expect the Fed will proceed with gradual rate hikes rather than risk falling behind the curve. We think a June rate hike is order, as well as further tightening over the second half of the year.

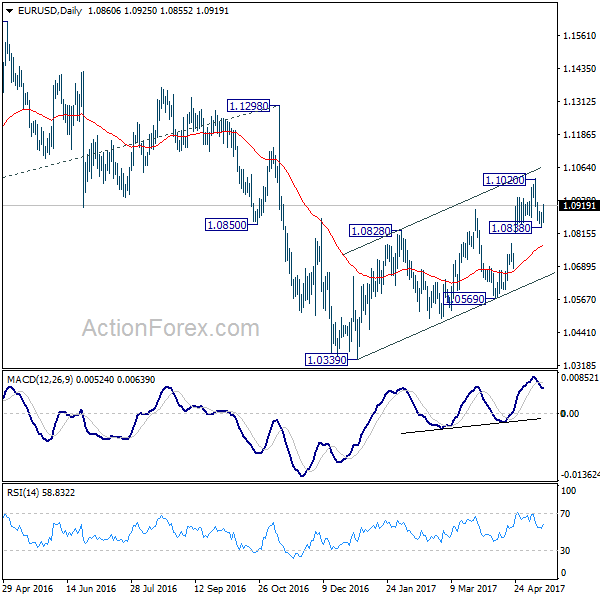

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0834; (P) 1.0864 (R1) 1.0889; More....

With a temporary low in place at 1.0838 in EUR/USD, intraday bias is turned neutral first. On the downside, below 1.0838 will target 55 day EMA first (now at 1.0760). As noted before, rise from 1.0339 is seen as a corrective move. Break of 55 day EMA will affirm the case that such correction is completed and bring deeper decline to 1.0569 for confirmation. However, above 1.1020 will extend such corrective rise instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.

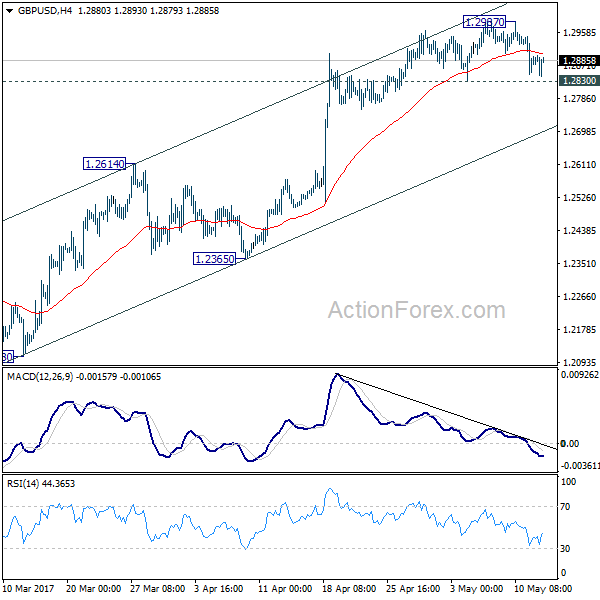

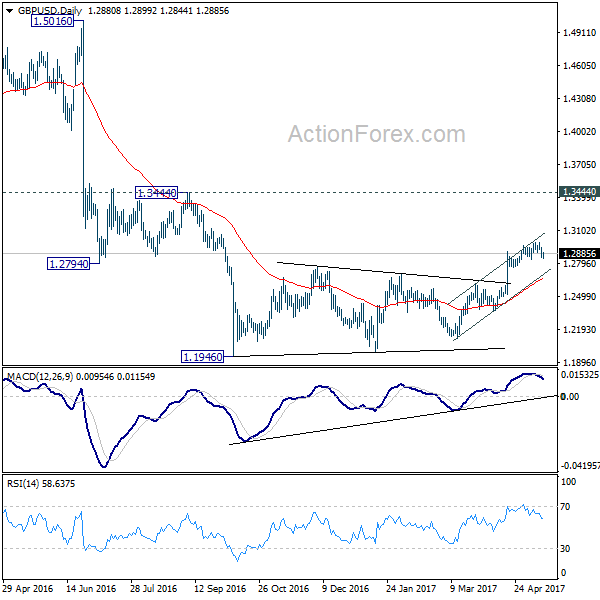

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2840; (P) 1.2894; (R1) 1.2940; More...

Intraday bias in GBP/USD remains neutral for the moment. Another rise cannot be ruled out, but upside momentum is clearly weak with bearish divergence condition in 4 hour MACD. Also, current rally is seen as part of the corrective pattern from 1.1946. Hence, even in case of another rally, we'll look for reverse signal above 1.2987. Meanwhile, break of 1.2830 support will indicate short term topping. In such case, intraday bias will be turned back to the downside for 1.2614 support.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

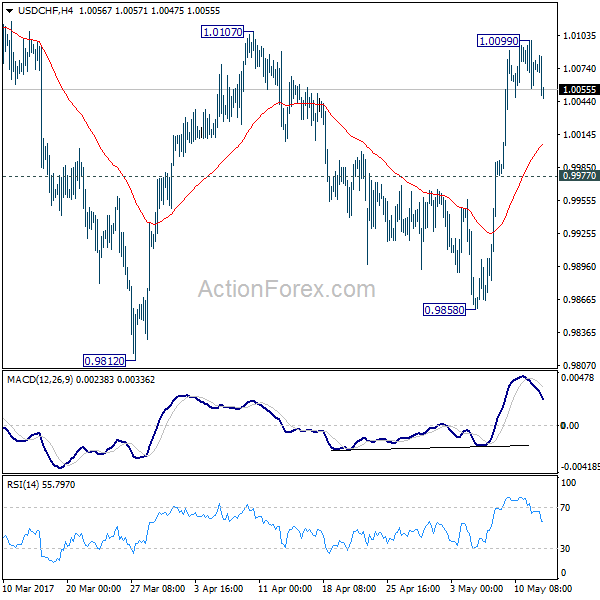

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0056; (P) 1.0077; (R1) 1.0099; More.....

Intraday bias in USD/CHF remains neutral as consolidation from 1.0099 temporary top extends lower. Deeper pull back could be seen. But downside is expected to be contained by 0.9977 and bring another rise. As noted before, correction from 1.0342 should have completed at 0.9812. Break of 1.0107 should pave the way to retest 1.0342 high.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.42; (P) 113.89; (R1) 114.33; More...

USD/JPY's retreat from 114.36 extends lower but it's staying above 112.08 support. Intraday bias remains neutral for more consolidation and outlook is unchanged. In case of deeper fall, downside should be contained by 112.08 support and bring another rally. Outlook remains unchanged that correction from 118.65 has completed with three waves down to 108.12. Above 114.36 will target 115.49 resistance first. Break will resume larger rally from 98.97 to 125.85 high.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Dollar Reverses after CPI and Retail Sales Disappointment, Set to End the Week Mixed

Dollar weakens broadly in early US session after disappointment from economic data. While the greenback is still trading at the strongest major currency for the week at the time of writing, it could end the week mixed. Headline CPI slowed to 2.2% yoy in April, down from 2.4% yoy, and missed expectation of 2.3% yoy. Core CPI slowed to 1.9% yoy, down from 2.0% yoy and missed expectation of 2.0% yoy. Headline retail sales rose 0.4%, below consensus of 0.6%. Ex-auto sales rose 0.2%, also below consensus of 0.5%. Elsewhere, Eurozone industrial production dropped -0.1% mom in March. German GDP rose 0.6% qoq in Q1. CPI was finalized at 2.0% yoy in April. Japan M2 rose 4.3% yoy in April, New Zealand business NZ manufacturing index dropped to 56.8 in April.

ECB Lane: Risks moving towards balance

ECB Governing Council member Philip Lane said that risks in the Eurozone economy are "still below balance but moving towards balance." And he emphasized the "need to see evidence that wage inflation is actually on its way to a level consistent with the target." And, the core is that how much of the "reasonably good data on output and unemployment" would "map into sustainable inflation". Regarding future monetary policy path, Lane said that "something has to happen in the rest of this year given there needs to be a plan in 2018."

BoJ official very cautious about an exit now

In Japan, BoJ Executive Director Masayoshi Amamiya said that there are "sufficient methods and tools" for stimulus exit. And, "it's possible to normalize monetary conditions while maintaining market stability". Board member Yutaka Harada urged the central bank to be "very careful" regarding stimulus exit. Hara said that "there might be a cost of delaying an exit. At the same time, there is a cost for an urgent exit". And emphasized that "we have to be very cautious about an exit now".

G7 FM to meet in Italy

G7 finance chiefs will start a two day meeting in Italy today. It's reported that Europe, Japan and Canada are seeking to get a clearer picture of US President Donald Trump's policies, through Treasury Secretary Steven Mnuchin. According to a Treasury spokesman, Mnuchin will brief G7 on the still evolving tax and regulatory reforms. However, trade and protectionism seem to be off the meeting's agenda. In addition, there will be a discussion of Greece's debt ahead of the May 22 meeting of Eurozone finance ministers,. with presence of representatives of ECB and IMF. IMF is believed to be pushing for debt relief measures for Greece which is objected by Eurozone governments for the time being.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.42; (P) 113.89; (R1) 114.33; More...

USD/JPY's retreat from 114.36 extends lower but it's staying above 112.08 support. Intraday bias remains neutral for more consolidation and outlook is unchanged. In case of deeper fall, downside should be contained by 112.08 support and bring another rally. Outlook remains unchanged that correction from 118.65 has completed with three waves down to 108.12. Above 114.36 will target 115.49 resistance first. Break will resume larger rally from 98.97 to 125.85 high.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ Manufacturing Index Apr | 56.8 | 57.8 | 58 | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Apr | 4.30% | 4.30% | 4.30% | 4.20% |

| 06:00 | EUR | German GDP Q/Q Q1 P | 0.60% | 0.60% | 0.40% | |

| 06:00 | EUR | German CPI M/M Apr F | 0.00% | 0.00% | 0.00% | |

| 06:00 | EUR | German CPI Y/Y Apr F | 2.00% | 2.00% | 2.00% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Mar | -0.10% | 0.30% | -0.30% | |

| 12:30 | USD | CPI M/M Apr | 0.20% | 0.20% | -0.30% | |

| 12:30 | USD | CPI Y/Y Apr | 2.20% | 2.30% | 2.40% | |

| 12:30 | USD | CPI Core M/M Apr | 0.10% | 0.20% | -0.10% | |

| 12:30 | USD | CPI Core Y/Y Apr | 1.90% | 2.00% | 2.00% | |

| 12:30 | USD | Advance Retail Sales Apr | 0.40% | 0.60% | -0.20% | |

| 12:30 | USD | Retail Sales Less Autos Apr | 0.20% | 0.50% | 0.00% | |

| 14:00 | USD | U. of Michigan Confidence May P | 97 | 97 | ||

| 14:00 | USD | Business Inventories Mar | 0.10% | 0.30% |