Sample Category Title

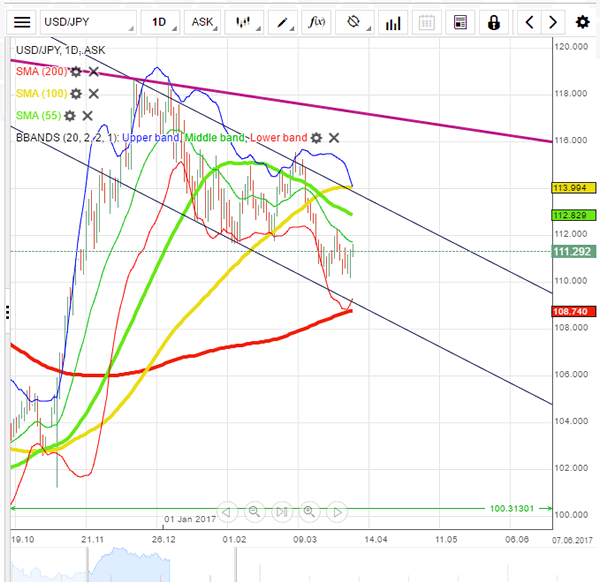

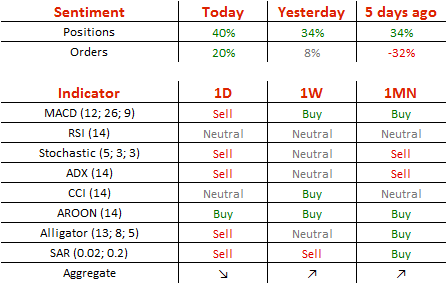

USD/JPY: Stabilises Above 111.00

'We believe the sluggish employment figures are largely attributable to weather-related noise and do not believe they will greatly dampen expectations of a Fed rate hike in June. Still, US indicators are likely to be patchy for now, sapping the momentum for those with a bullish USD/JPY view.' – Deutsche Bank (based on FXStreet)

Pair's Outlook

In spite of a poor US NFP reading, the Buck still managed to recover from its intraday low and close trade in the green zone against the Yen on Friday. The recovery reconfirmed the 110.50 level as a tough psychological support, which is likely to keep the USD/JPY pair afloat in case bears take over the market again. The weekly pivot point at 110.93 is now the closest support, but a bearish development is doubtful, even though technical indicators are giving corresponding signals. Meanwhile, a surge beyond 111.70 is also unlikely to occur, being that there are no market movers present and the 20-day SMA and the weekly R1 form relatively strong resistance around that area.

Traders' Sentiment

The Greenback appears to be overbought, as 70% of all open positions are long today, compared to 67% on Friday.

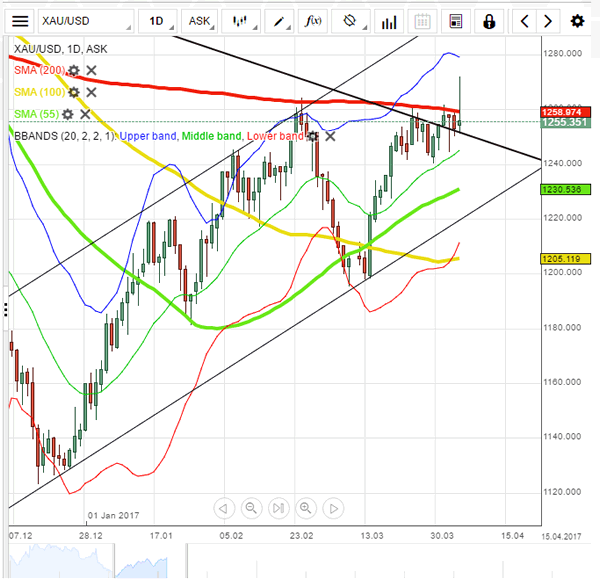

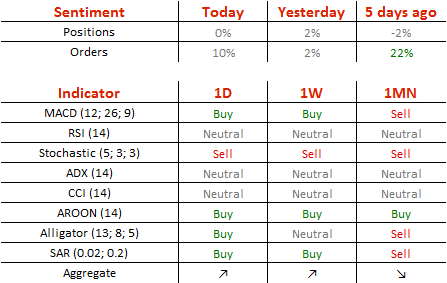

XAU/USD Retreats To Previous Levels

'I don't think it can have a further upside as even though the (U.S. interest) rate hike expectations have come down; the direction of hikes and monetary tightening are quite clear.' – Mark To, Wing Fung Financial Group (based on Reuters)

Pair's Outlook

The yellow metal's price has returned back to the levels just above the 1,250 mark. The jump witnessed on Friday receded, as the financial markets and the world calmed down after the US missile strikes in Syria. On Monday the bullion was squeezed in between the resistance of the 200-day SMA and the weekly PP, respectively, at 1,255.17 and 1,255.99 and the support, which is provided by the 50.00% Fibonacci retracement level at the 1,248.96 mark. Most likely markets will expect the today's speech of Janet Yellen regarding monetary policy before making further decisions.

Traders' Sentiment

Trader open positions are neutral in regard to the yellow metal's price. However, 55% of trader set up orders are to buy.

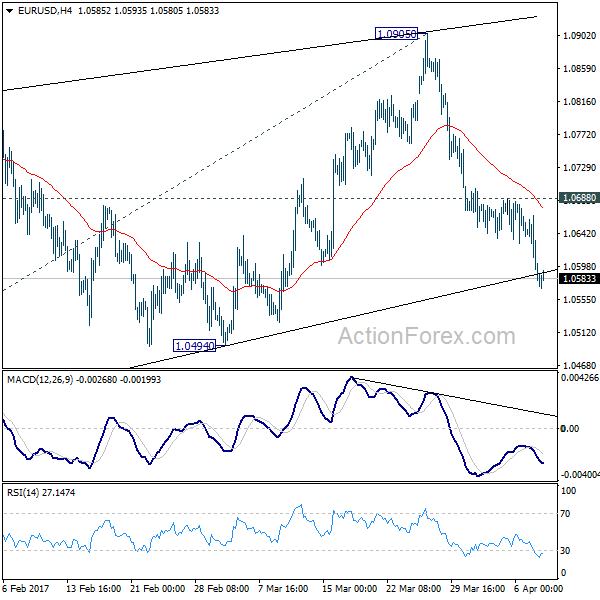

Trade Idea : EUR/USD – Sell at 1.0635

EUR/USD - 1.0583

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0582

Kijun-Sen level : 1.0619

Ichimoku cloud top : 1.0659

Ichimoku cloud bottom : 1.0651

Original strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

The single currency ran into renewed selling interest at 1.0667 on Friday (after NFP) and has dropped again, the breach o indicated support at 1.0600 adds credence to our bearish view that the decline from 1.0906 is still in progress and may extend further weakness towards 1.0550-55 (50% projection of 1.0906-1.0635 measuring from 1.0689), then 1.0525-30, however, near term oversold condition should prevent sharp fall below 1.0500, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0635 (previous support now resistance) should limit upside. Only a firm break above said resistance at 1.0667 would abort and suggest low is formed instead, risk a stronger rebound to 1.0689, then 1.0702.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0558; (P) 1.0611 (R1) 1.0642; More....

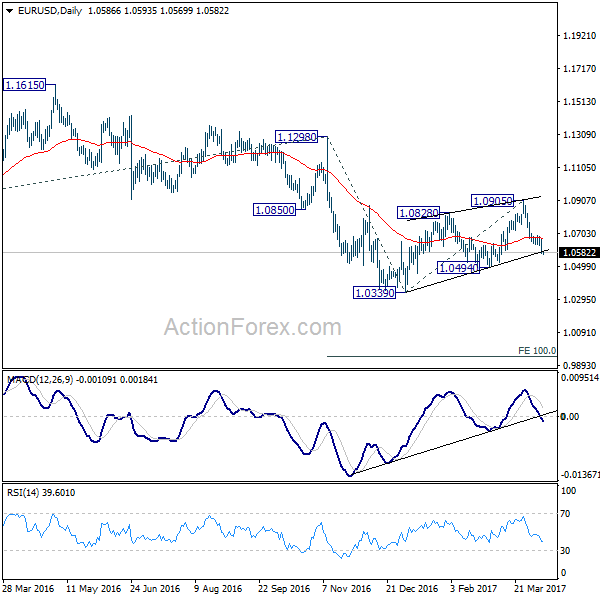

EUR/USD's fall from 1.0905 is still in progress and intraday bias stays on the downside. Corrective rise from 1.0339 is likely finished after being rejected by 55 week EMA. And, the larger down trend is ready to resume. Further fall should be seen to 1.0494 support first. Decisive break of 1.0494 support will confirm this bearish case and target 1.0339 low. Break of 1.0339 will confirm down trend resumption and target 100% projection of 1.1298 to 1.0339 from 1.0905 at 0.9946. On the upside, however, break of 1.0688 resistance will delay the bearish case and turn focus back to 1.0905 resistance instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

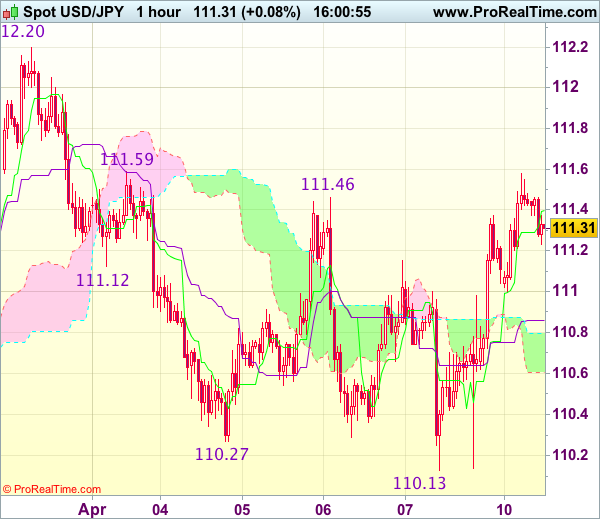

Trade Idea : USD/JPY – Buy at 110.90

USD/JPY - 111.28

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.40

Kijun-Sen level : 110.86

Ichimoku cloud top : 110.80

Ichimoku cloud bottom : 110.60

New strategy :

Buy at 110.90, Target: 111.90, Stop: 110.55

Position : -

Target : -

Stop : -

Although the greenback fell to as low as 110.13 late last week, as dollar has staged a strong rebound after holding above indicated support at 110.11, retaining our view that further consolidation above this level would be seen and mild upside bias is for test of 111.59 resistance, a break there would signal the fall from 112.20 has ended, then a stronger rebound to 111.90-00 would follow but said resistance at 112.20 should hold and choppy trading within 110.11-112.20 would continue.

In view of this, we are looking to buy dollar on dips but one should exit on such rebound. Below the lower Kumo (now at 110.60) would signal an intra-day top is formed instead, risk weakness to 110.40 but only break of said support at 110.11-13 would confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) but price should hold above 109.50-55 (100% projection of 112.20-110.27 measuring from 111.46).

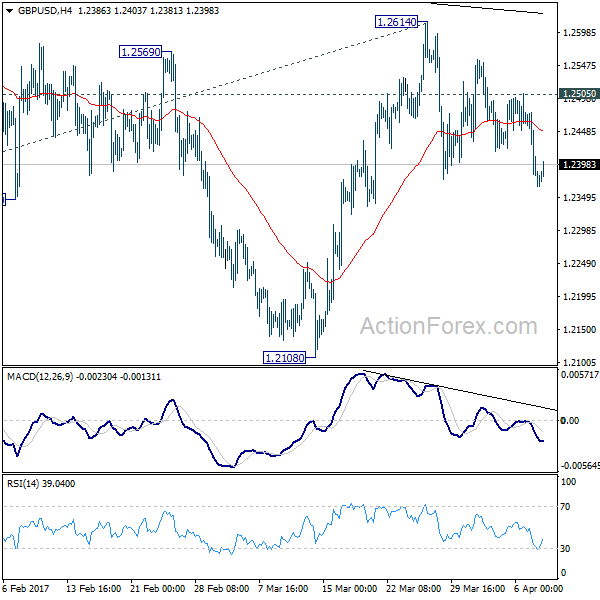

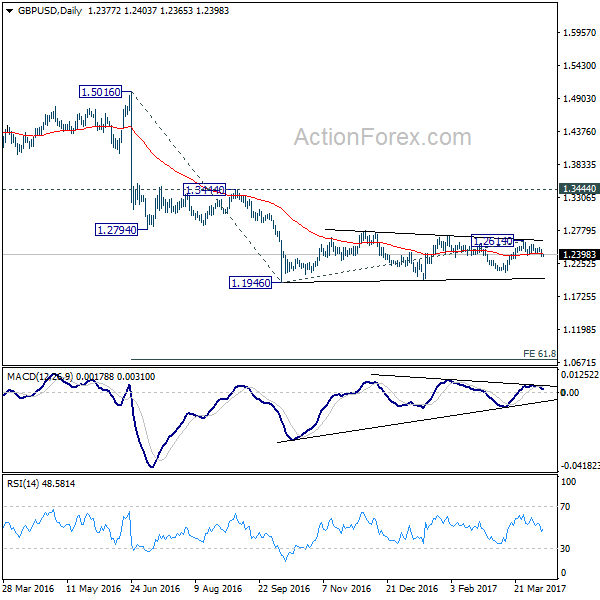

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2332; (P) 1.2404; (R1) 1.2445; More...

Intraday bias in GBP/USD remains on the downside for the moment. Rise from 1.2108 should have completed at 1.2614. And, the triangle pattern from 1.1946 could be finished with five waves to 1.2614 too. Deeper decline would be seen back to 1.2108 first. Decisive break there will argue that medium term down trend is resuming. In that case, GBP/USD should take out 1.1946/1986 support zone to 61.8% projection of 1.5016 to 1.1946 from 1.2614 at 1.0717. On the upside, however, break of 1.2505 resistance will invalidate this immediately bearish case. Then, it will turn bias back to the upside for 1.2614 resistance instead.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

US Non-Farm Payroll Disappoints, But The Rest Of The Report Is Solid

Nonfarm payrolls rose by only 98k in March, data showed on Friday, far below the consensus of 180k. February's print was revised lower to 219k from 235k previously. Nevertheless, the rest of the report was not as soft as the headline NFP print would suggest. The unemployment rate unexpectedly dropped to 4.5% from 4.7%, and for healthy reasons, considering that the labor force participation rate remained unchanged. Average hourly earnings were in line with the forecast of +0.2% mom, while last month's print was revised slightly higher to +0.3% mom.

USD/JPY dropped on the below-expectations NFP print, breaking below the 110.35 (S2) hurdle to find support a few pips above the 110.00 (S3) territory. However, the rate rebounded in the following minutes as market participants digested the entire report. The pair recovered its losses and surged further, to find resistance near the key obstacle of 111.60 (R1). A clear break above that key level could signal the return of the rate back within the sideways range between that hurdle and the 115.50 zone, which contained the price action from the 11th of January until the 22nd of March. Thus, if the bulls manage to overcome 111.60 (R1), we could experience further advances in coming days. The rate could initially challenge the 112.20 (R2) territory.

Overall, this report keeps the door wide open for another near-term rate hike by the Fed in our view, perhaps as early as at one of the summer meetings. Recent comments from Chair Yellen suggest that NFP numbers in the range of 75k – 125k are still consistent with further tightening in the labor market, while the drop in the unemployment rate has brought it in line with the Fed's target of full employment. Thus, we may well get some optimistic comments from FOMC officials regarding the strength of the labor market in the next days. The first of these remarks could come from Chair Yellen today. Any optimistic hints from the Fed chief regarding the US economy could enhance speculation regarding another near-term hike and thereby, bring USD under renewed buying interest.

EUR/USD declined in the aftermath of the employment data on Friday. The rate broke below two support (now turned into resistance) obstacles in a row and an upside support line taken from the low of the 3rd of January, before finding fresh buy orders near the 1.0570 (S1) level. In case we get some upbeat remarks from Chair Yellen today, we could see another test at the 1.0570 (S1) support. A clear break could set the stage for further declines towards the 1.0530 (S2) territory.

Today's highlights:

During the European day, we get Norway's CPI data for March. The forecast is for both the headline and the core rates to have ticked up. Something like that could diminish somewhat the likelihood for any further easing by the Norges Bank, which at its latest policy meeting shifted to a slightly more dovish tone, and thereby support NOK.

Besides Fed Chair Yellen, we have one more speaker on the agenda: ECB Vice President Vitor Constancio.

As for the rest of the week:

On Tuesday, we get CPI data for March from both the UK and Sweden. On Wednesday, all eyes will be on the Bank of Canada rate decision. The BoC is expected to stand pat. We see the case for the officials to keep the door wide open for a near-term rate cut if needed, despite the latest improvements in the profile for economic growth. In the UK, employment data for February are due out. On Thursday, we have a relatively quiet day, while on Friday, we get US CPI and retail sales data, all for March.

USD/JPY

Support: 111.00 (S1), 110.35 (S2), 110.00 (S3)

Resistance: 111.60 (R1), 112.20 (R2), 112.90 (R3)

EUR/USD

Support: 1.0570 (S1), 1.0530 (S2), 1.0500 (S3)

Resistance: 1.0600 (R1), 1.0640 (R2), 1.0700 (R3)

Market Update – Asian Session: USD Rallies As Trump-Xi Talks Viewed As Successful

Friday US Session Highlights

(US) MAR CHANGE IN NONFARM PAYROLLS: +98K V +180KE (lowest since May 2016)

(US) MAR UNEMPLOYMENT RATE: 4.5% V 4.7%E (lowest since April 2007); Underemployment Rate: 8.9% v 9.2% prior

(US) MAR AVERAGE HOURLY EARNINGS M/M: 0.2% V 0.2%E; Y/Y: 2.7% V 2.7%E; AVERAGE WEEKLY HOURS: 34.3 V 34.4E

(US) Feb Wholesale Inventories (Final) M/M: 0.4% V 0.4%E; wholesale Trade Sales M/M: +0.6% v -0.1% prior

Friday US markets on close: Dow flat, S&P500 -0.1%, Nasdaq flat

Best Sector in S&P500: Consumer Staples

Worst Sector in S&P500: Utilities

Biggest gainers: VMC +3.9%; INCY +3.4%; FMC +3.1%

Biggest losers: UA -3.2%; KMX -2.6%; CBT -2.3%

At the close: VIX 12.9 (+0.5pts); Treasuries: 2-yr 1.29% (+4bps), 10-yr 2.37% (+3bps), 30-yr 3.00% (+1bps)

Politics

(HU) About 60K marchers in Budapest protested PM Orban's targeting of Central European University - press

(US) KT McFarland has been asked to step down at deputy National Security Advisor to Pres Trump; Expected to be nominated as ambassador to Singapore - press

(US) Trump Chief Economic Advisor Gary Cohn: Not sure that Mnuchin’s Aug forecast will be reachable for tax reform - financial press

(US) Reminder: US Congress is on break for the next two weeks (starting April 10th), which leaves little time to pass spending bill and avoid a govt shutdown

Weekend US/EU Corporate Headlines

TSLA Said to be planning a factory in Guangdong, China - Southern Metropolis Daily

Key economic data:

(JP) JAPAN FEB BOP CURRENT ACCOUNT TOTAL: ¥2.81B V ¥2.51TE; ADJ CURRENT ACCOUNT TOTAL: ¥2.21T (multi-year high) V ¥1.79TE; TRADE BALANCE BOP BASIS: ¥1.08T V + ¥982BE

(AU) AUSTRALIA FEB HOME LOANS M/M: -0.5% V 0.0%E (biggest decline in 4 months)

Asia Session Notable Observations, Speakers and Press

Asian equity markets are mixed and US futures are higher on expectation of renewed risk appetite to start the new week. Investors are shrugging the miss in non-farm payrolls as a one-off due to weather impact and buying the recent dip. Nikkei225 is the best performer as USD/JPY hit a 1-week high above 111.50, while Australia miners have helped that index hit a 2-year high after positive broker commentary. In other FX majors, AUD/USD slid to January lows below 0.7480 and NZD/USD was at a 3-week low around 0.6920. Broad USD strength is derived from momentum on Friday as comments from Fed's typically more dovish voter Dudley are perceived to be increasingly more hawkish. Fed's Bullard also spoke in Australia, noting the underwhelming jobs report is in line with the view of 2% inflation and modest growth, urging a wait and see for Trump's fiscal policy combined with just one more rate hike by the Fed this year.

Geopolitical risk remains a hot topic in the wake of Syria strikes last week. Russian press has reported that communications in Syria have been disrupted after the US actions, while other reports noted new bombing on the rebel town that suffered the chemical attack. ISIS also waged an attack on a joint coalition forces base in the south of the country. Separately, US reports noted that a strike force led by US destroyer is approaching the Korean peninsula. State Sec Tillerson however said that a regime change is not the objective for North Korea

Florida meeting between China Pres Xi and US Pres Trump is viewed as a success. China has reportedly offered improved market access for US financial sector investments and beef exports in a move to avert a trade war, while Xi has extended Trump an invitation to visit Beijing in the near future. China State Media also said the meeting marks the start of a relationship based on cooperation and respect instead of conflict.

In notable economic data, Australia home loans saw their biggest m/m decline in 4 months, though most analysts are focusing on this week's employment data as a key driver for RBA bias going forward. Morgan Stanley however has already revised its prior view of a rate cut this year to expect neutral stance through 2017 on housing inflation concerns.

China

(CN) China's 21 listed property developers saw combined Q1 sales of CNY621.6B, +69% y/y - Chinese press

(CN) China NDRC: Will gradually reduce planned power output of existing coal fire power plants

(CN) China Premier Li Keqiang calling on cabinet to remain vigilant for risks related to bad assets, bond defaults, shadow banking and online finance - press

(CN) China State Information Center researcher Zhu Baoliang: Economic growth may stabilize at slower place in Q2 as the world economy remains sluggish and domestic auto, home sales cool - Chinese press

(CN) Goldman Sachs sees China Q1 GDP at 6.8% v 6.8% in Q4; 2017 GDP seen at 6.6% v "around 6.5%" official target - Chinese press

(CN) Chairman of China Securities Regulatory Commission (CSRC) urging listed companies in China to pay out more dividends - Chinese press

(CN) China State Media calls Trump/Xi meeting the start of a relationship based on cooperation and respect instead of conflict

Japan

(JP) Bank of Japan (BOJ) Amamiya: BOJ unrealized losses could be ¥24T if yield rises to 1%

(JP) Bank of Japan (BOJ) Gov Kuroda: Japan CPI to rise toward 2% target

(JP) IMF may raise Japan's 2017 GDP target above 1% from 0.8% in its upcoming World Economic Outlook report amid continued growth in exports - Japan press

Australia / New Zealand

(AU) Morgan Stanley: No longer expect RBA to cut rates this year; Expect rates to remain unchanged - Australian press

(AU) Moody's: Australia home prices forecast to rise 5.6% in 2017 before falling 0.6% in 2018 - press

(AU) CBA economist: RBA seems comfortable with inflation below target, but they would be sensitive to deterioration in the labor market - SMH

(AU) UBS: Rise in commodity prices may strengthen Australia's AAA rating - press

(NZ) Westpac: Recent rise in New Zealand inflation may not be sustainable - press

Korea

(US) Sen Markey (D-MA): Pres Trump should engage in direct negotiations with North Korea's Kim Jong Un as part of combined efforts with China - US press

(KR) US has ordered an aircraft carrier group to move closer to the Korean Peninsula in response to recent provocations from North Korea - US press

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.7%, Hang Seng flat, Shanghai Composite -0.3%, ASX200 +0.5%, Kospi -0.8%

Equity Futures: S&P500 +0.2%; Nasdaq +0.1%, Dax +0.3%, FTSE100 flat

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0570-1.0590; JPY 111.00-111.60; AUD 0.7480-0.7510; NZD 0.6920-0.6945; GBP 1.2365-1.2385

June Gold -0.2% at 1,255/oz; May Crude Oil +0.3% at $52.40/brl; May Copper -0.9% at $2.62/lb

(US) Weekly Baker Hughes US Rig Count: 839 v 824 w/w (+1.8%) (12th straight weekly rise)

ANZ: Oil market looks finely balanced; While US production is up, demand is also relatively strong - press

SPDR Gold Trust ETF daily holdings fall 0.3 tonnes to 836.5 tonnes

iShares Silver Trust ETF daily holdings fall to 9,862 tonnes from 10,208 tonnes prior; 6th straight decline, lowest since Mar 2016

(CN) PBOC SETS YUAN MID POINT AT 6.9042 V 6.8949 PRIOR; weakest Yuan setting since Mar 21st; 3rd straight weaker setting

(CN) PBoC skips open market operations for 11th straight session; drains net CNY10B

(AU) Australia MoF sells A$400M v A$400M indicated in 4.5% 2033 bonds; avg yield 3.008%; bid-to-cover 3.81x

(KR) South Korea MoF sells 5-yr Govt bonds at 1.915%

Asia equities / Notables / movers

Australia

Tabcorp (TAH) +0.9%; NSW wagering partnership

South32 (S22) +1.9%; Raised at CLSA

BHP (BHP) +1.0%; Raises at CLSA

Oz Minerals (OZL) +0.9%; exploration agreement

Worley Parsons (WOR) +4.0%; Block trade

Cimic (CIM) +1.1%; Leighton contract in India

Mesoblast (MSB) +8.2%; endpoint in phase 3 trial

Japan

Toshiba (6502) +6.3%; May sell TV business; Additional reports of Hon Hai intereest

Dentsu (4324) +2.8%; March sales

Hisamitsu Pharmaceutical (4530) -9.5%; FY16 results

Hong Kong

Skyworth Digital Holdings (751) -7.5%; Q1 guidance

Gemdale Properties (535) +1.8%; Mar sales

China Overseas Grand Oceans (81) +2.2%; Mar sales

Agile Group Holdings (3383) -2.7%; Mar sales

Greenland Hong Kong (337) -3.6%; Mar sales

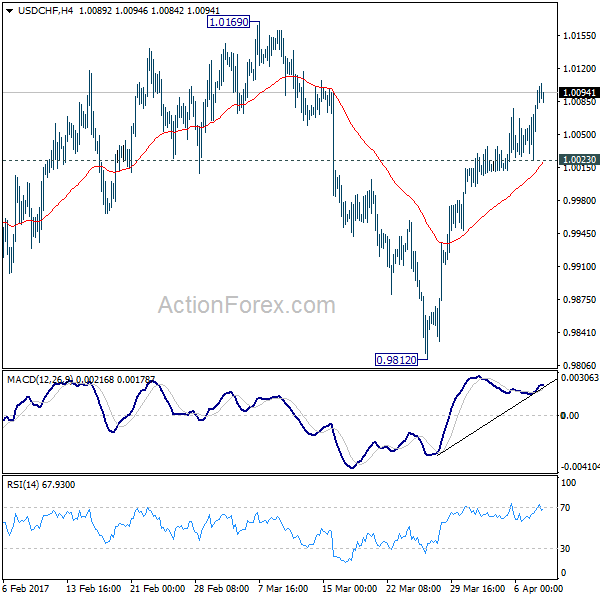

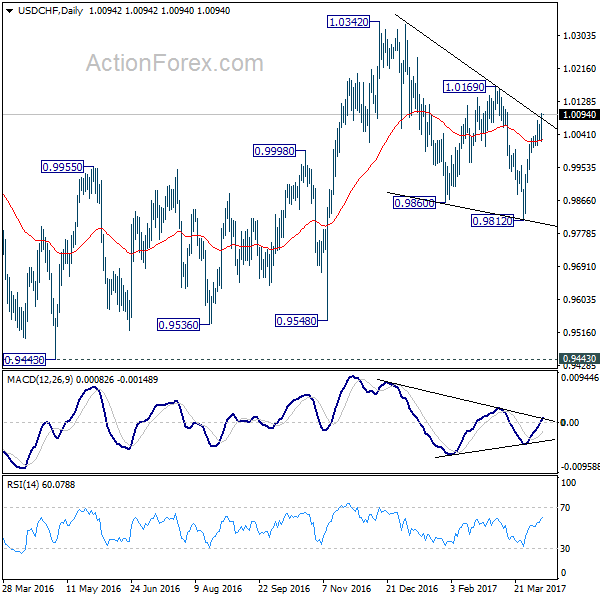

USD/CHF Daily Outlook

Daily Pivots: (S1) 1.0043; (P) 1.0069; (R1) 1.0117; More.....

USD/CHF's rise from 0.9812 continues today and intraday bias remains on the upside. Correction from 1.0342 has completed with three waves down to 0.9812. Further rise should be seen to 1.0169 resistance next. Decisive break there will confirm this bullish case and target 1.0342 key resistance next. On the downside, below 1.0023 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, we're still maintain that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the cross. However, the corrective nature of the fall from 1.0342 to 0.9812 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

APAC Update: Not A Manic Monday

Asia has had an orderly session today. U.S. Dollar strength continues from Friday and Asia stock are flat to small down.

U.S markets ignored a low-ball Non-Farm Payrolls on Friday, preferring to concentrate on yet another dip in the employment rate instead. An excellent round-up of the session and the week ahead from my colleague Alfonso can be found here. week-ahead

FX has traded sideways mostly with just the AUD suffering as we await Europe.

EUR/USD

Languishing at the bottom of its New York range after breaking support at 1.0627, the 100-day moving average, on Friday. This will become meaningful resistance now.

The price action had bought the 1.0495/1.0500 area back into view. The Euro will become increasingly sensitive to the politcial headlines from France now vis-a-vis the election. A break of 1.0500 will open up a further drop below 1.0400 from a charting perspective.

USD/JPY

The comeback king, perhaps as U.S. yields have firmed belatedly after the Fed discussed a balance sheet run-off last week. The moving of Carl Vinson carrier battle group to the vicinity of South Korea won't be helping either as geopolitical jitters from Friday continue to make themselves felt in that part of Asia.The range is still very well defined on the charts. Namely resistance at the 112.20 area with support at the 110.00 area. A daily close above or below respectively will tell us USD/JPY's next direction. I note bullish divergence between the daily stochastic and RSI with the price action of USD/JPY itself.

The range, however, is still very well defined on the charts. Namely resistance at the 112.20 area with support at the 110.00 area. A daily close above or below respectively will tell us USD/JPY's next direction. I note bullish divergence between the daily stochastic and RSI with the price action of USD/JPY itself.

AUD/USD

With Dahlian coal futures continuing to drop precipitously, copper flirting with support at its 100-day moving average and more negative reports on the Australian housing market, the AUD has found few friends today. The US/Australia 10-year rate spreads won't be helping either.

AUD cracked held support at 9490 on Friday, just, but trades under it at 7485 this afternoon. AUD has resistance at 7517 and 7556, it 100 and 200-day moving averages.

Below, the bottom of the daily Ichi moko cloud provides support at 7450. A break underneath here implies substantially lower levels lie ahead.

USD/CNH

President Xi's meeting with President Trump has passed without incident unsurprisingly. Perhaps except for Mr Trump telling Mr Xi he was bombing Syria over dinner. China has offered a few crumbs at the trade table, but as per Yen and Korean Won, its future is a USD story and a geopolitical one.

While we are mentioning Korea, Friday's Syria raids were clearly more than a passing message to both North Korea and China. When pondering whether an action is imminent in North Korea however, two things should come to readers minds, as I am sure they did to President Xi.

Seoul lies less than 60 kilometres from the North Korea border. Well within artillery and rocket range. North Korea has a lot of both.

Any strike against N.Korea would have to be completely overwhelming immediately due to point 1 above. This would require a lot more forces to be placed locally then one carrier battle group.

Back to USD/CNH, the price action is constructive on the charts. We have broken and held above the 100-day moving average at 6.8835 which becomes support. Behind this 6.8450 and 6.7900 are clearly denoted.

Resistance lies at 6.9300 and 6.9900 and as long as the USD continues to strengthen in general and yields rise, a slow grind higher seems to be the path of least resistance.

U.S. Bonds

The U.S. 2-year, 5-year and 10-year all had bearish outside reversal days on Friday, the 30-year narrowly dodging that bullet. That is, they made new highs, only to close lower than the previous day's lows. This implies higher yields i.e. lower prices from a charting perspective. A look at the 5 and 10-year charts tells the story.

US 5 Year.

5-years broke support at 118.13 on Friday having initially rallied through resistance at 118.50 to trade as high as 118.81. These all remain resistance.

The 5-year is flirting with its 100-day moving average at 117.98 with support at 117.83 behind this. A daily close under the latter implies a move to the 117.00 area.

US 10 Year

The outside reversal is clear to see. Breaking through resistance at 125.90 and onto 126.28, before falling to 125.20.

Support, like both the two and five years, lies just below at it's 100-day moving average at 124.84 and then the 124.75 level. A daily close below implies a move to and test of key support at 123.25.

Summary

Overall the USD is stronger although not markedly so against its g-10 compatriots. Nevertheless, some of the levels broken are significant, particularly in AUD and EUR. We realistically need to see still whether this is the start of a new move or a false dawn. The next couple of days should enlighten. More significant is the multiple bearish outside reversals on US Bonds as the market overcomes Friday's safe-haven run and finally starting absorbing the implications of a Federal Reserve balance sheet run-down. The 4th tightening in any other words.