Sample Category Title

UK Manufacturing Production Experiences 0.1% Fall In February

'It is clear that industry does not have the momentum required to offset the consumer-led slowdown in the services sector this year.' - Samuel Tombs, Pantheon Macroeconomics

In February, British total production experienced a 0.7% decrease compared to the previous month, the Office for National Statistics reported on Friday. The revealed figures did not justify experts' forecasts, as they expected to see a 0.3% increase. The decline was registered in all four major sectors. Nevertheless, the largest drop occurred in the electricity and gas industry, where downfall reached 3.4%. It was attributable to lower electricity generation and gas supply amid unusually high temperatures. Another major fall happened in the pharmaceutical, chemical products and crude petroleum industries, where growth plunged 4.4%, 2.1% and 2.6%, accordingly. In contrast, the largest gains were posted by the textiles and electrical equipment industries, where production increased 3.0% and 2.3%, respectively. However, it was not enough to offset the overall negative output of the manufacturing sector, which lost 0.1%, due to the erratic performance of pharmaceutical industry. Nevertheless, on a yearly basis, total production advanced 2.8% in February. Three out of four major sectors showed positive results. Yet, the largest contribution was made by the manufacturing sector, which posted a 3.3% increase, following a gain of 2.6% in the previous month.

US Job Creation Slows In March While Jobless Rate Drops To Lowest Since May 2007

'If today's decline in the unemployment rate doesn't reverse itself they may be compelled not only to hike but also to signal a faster pace of future tightening.' - Michael Feroli, JPMorgan

US private companies created less positions than expected last month; however, a fall in the jobless rate suggested that the labour market remained on a strong footing. The Labour Department reported on Friday that nonfarm payrolls rose 98,000 in March, compared to the previous month's downwardly revised gain of 219,000. Meanwhile, analysts expected the economy to add 174,000 new jobs during the reported period. According to economists, nonfarm employments was hit by the weather-related effects of the big storm that hit the Northeast and Midwest. Meanwhile, the unemployment rate fell to 4.5%, the lowest since May 2007, from 4.7% in February, while analysts anticipated an unchanged reading. In order to keep up with growth in the US working age population, the economy needs to create at least 75,000 jobs each month. Job growth averaged 178,000 per month in the Q1 of 2017, suggesting that an expected 1.0% GDP rise for the Q1 could be temporary. Average hourly earnings advanced 0.2% in March, after climbing 0.3% in the prior month. Back in March, the Fed raised rates for the first time this year and promised two more hikes in 2017. With the economy expected to bounce back in the second quarter, analysts pegged June for the next rate hike.

Canadian Economy Adds 19,400 Jobs Last Month

'While we share doubts about the sustainability of the recent pick-up in economic growth, the recent strength in employment will make it harder for the Bank of Canada to defend its dovishness on the economy and the need to keep interest rates low in the near future.' - David Madani, Capital Economics

Canadian companies created more than expected jobs last month, while the unemployment rate advanced as more people continued to enter or re-enter the labor market, official figures revealed on Friday. Statistics Canada reported that Canadian employers added 19,400 jobs to the economy in March, following the preceding month's gain of 15,300, surpassing analysts' expectations for a 5,700 increase and marking the fourth consecutive monthly gain. However, the Bank of Canada is expected to keep its monetary policy unchanged at its meeting this week. The Bank of Canada Governor Stephen Poloz said earlier that the Canadian economy had a lot of room for improvement and policymakers should bear in mind potential downside risks. The data also showed that 18,400 full-time jobs and 1,000 part-time jobs were added to the economy last month. In the meantime, the jobless rate climbed to 6.7% from 6.6% registered in February, meeting analysts' expectations. Even though March's report turned out better than expected, hourly salaries of permanent employees advanced just 0.9% compared to the same period a year ago. The largest downward pressure on wages was seen in Alberta, as it remained on the path to recovery from the May 2016 wildfires.

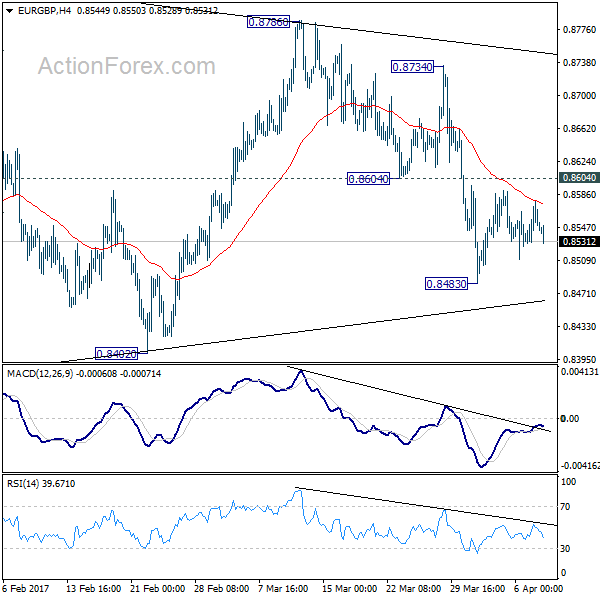

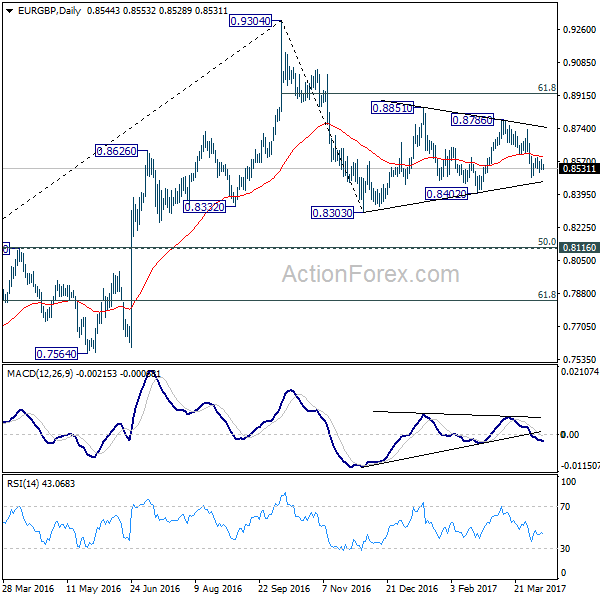

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8529; (P) 0.8554; (R1) 0.8582; More...

Intraday bias in EUR/GBP remains neutral for the moment. Overall outlook is unchanged. Fall from 0.8786 could be developing into the third leg of the whole corrective pattern from 0.9304. And hence, deeper decline is expected ahead. On the downside, break of 0.8483 will turn bias to the downside for 0.8402 support first. Decisive break there should confirm our bearish view and target 0.8303 and below. As fall from 0.9304 is viewed as a corrective move, we'd expect strong support at 0.8116/20 cluster support to contain downside and bring rebound. On the upside, above 0.8604 minor resistance will delay the bearish case. That is, one more recovery will be seen to complete a five wave triangle pattern fro 0.8303 before completion.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is likely ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Rise from 0.6935 (2015 low) will resume at a later stage to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

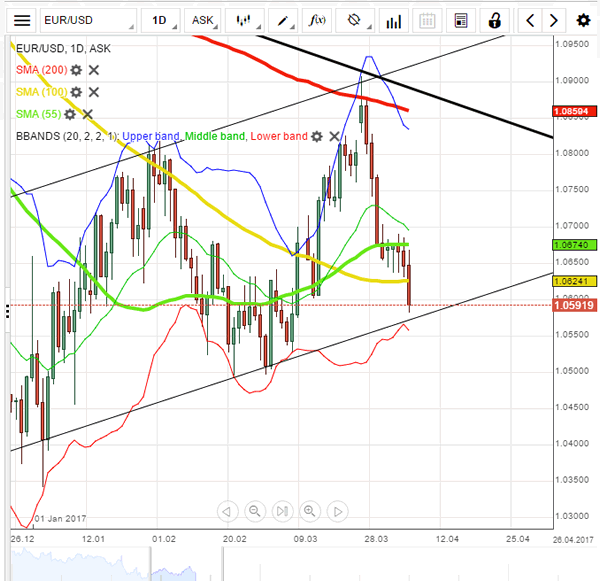

EUR/USD: Falls Below 1.06 Mark

'The dollar extended its rebound from session lows after New York Federal Reserve President William Dudley commented on the pace of interest-rate increases.' – Lananh Nguyen and Dennis Pettit, Bloomberg

Pair's Outlook

On Monday morning the common European currency fluctuated rather flat against the US Dollar below the 1.06 level. It could be observed that the fall of the currency exchange rate is likely going to extend itself into a fourth consecutive trading session. The reason for that is the fact that the closest support to the currency exchange rate was a cluster near the 1.0550 mark, where the lower Bollinger band, weekly S1 and a long term trend line are located at. It can be expected that the pair reaches this cluster first, before rebounding.

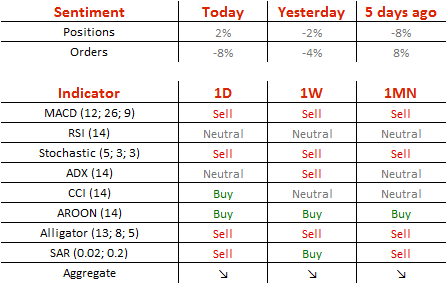

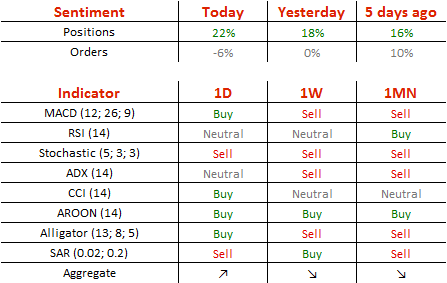

Traders' Sentiment

SWFX traders still remain almost neutral, as 51% of open positions are long on Monday. Meanwhile, 54% of trader set up orders are to sell the Euro.

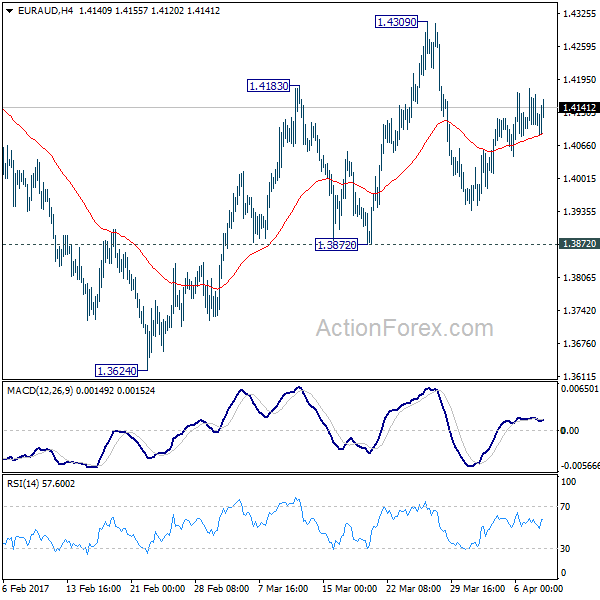

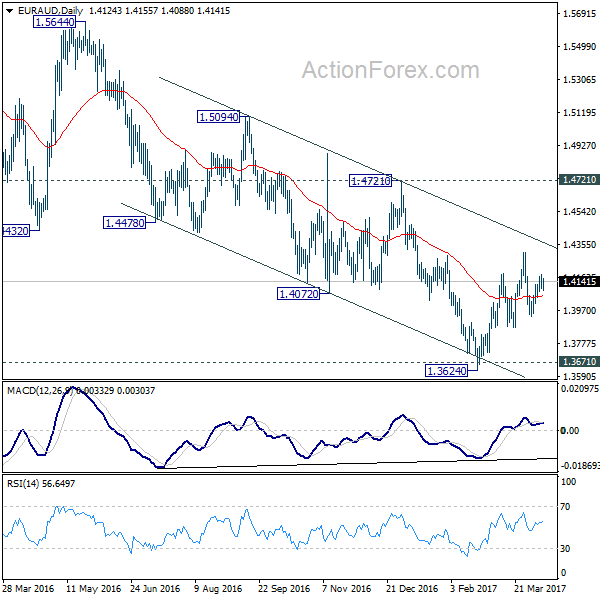

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4079; (P) 1.4128; (R1) 1.4160; More...

Intraday bias in EUR/AUD remains neutral for the moment. As it is still holding above 1.3872 support, we're mildly favoring the case of trend reversal after defending key support level at 1.3671. On the upside, break of 1.4309 will extend the rebound from 1.3624 to 1.4721 key resistance level next. Decisive break of 1.4721 should confirm larger trend reversal. However, firm break of 1.3872 support will dampen our bullish view. In such case, intraday bias will be turned back to the downside for 1.3624 low instead.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after testing 1.3671 key support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

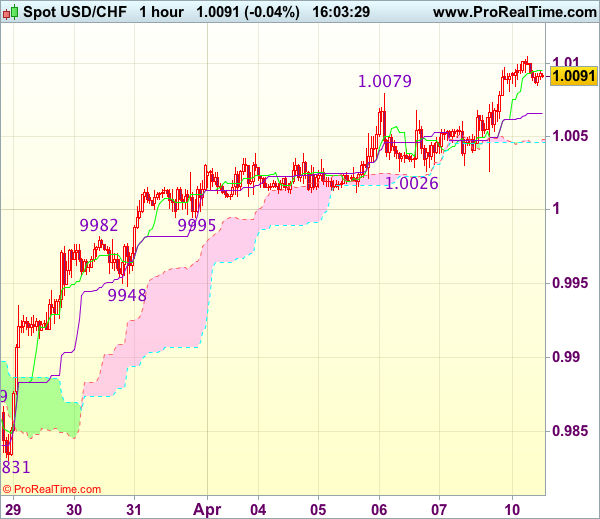

Trade Idea : USD/CHF – Buy at 1.0030

USD/CHF - 1.0097

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0095

Kijun-Sen level : 1.0066

Ichimoku cloud top : 1.0048

Ichimoku cloud bottom : 1.0046

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0030, Target: 1.0130, Stop: 0.9995

Position : -

Target : -

Stop : -

The greenback has maintained a firm undertone after Friday’s rally, adding credence to our bullish view that recent upmove from 0.9813 is still in progress and upside bias remains for this move to extend further gain to previous resistance at 1.0109, then towards 1.0140-45, however, loss of upward momentum should prevent sharp move beyond another previous resistance at 1.0171, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as support at 1.0026 should limit downside. Below minor support at 0.9995 would defer and suggest top is possibly formed, risk correction to 0.9960 but support at 0.9948 should hold from here.

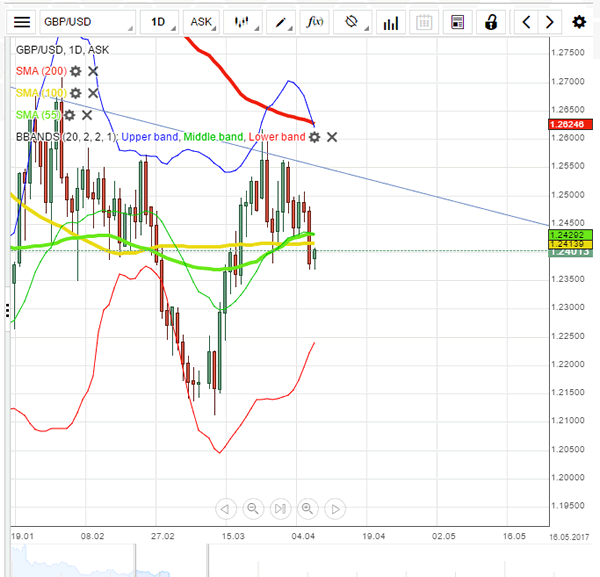

GBP/USD: Takes A Breath After Friday’s Plunge

'There are still geopolitical concerns, such as the Syrian situation, in the background, and there are no fresh incentives or reasons to buy the dollar.' – Sony Financial Holdings (based on Reuters)

Pair's Outlook

A rather unexpected development occurred on Friday, being that the British Pound fell under sharp selling pressure, while the Greenback soared across the board. The US NFP data sharply disappointed, but an upbeat reading of the unemployment rate, as well as a surge in US Treasury bond yields, were the catalysts. As a result, the Cable slumped back under 1.24, breaching the tough support cluster, which somewhat confirms the six-month down-trend. Technical studies insist the GBP/USD pair is to undergo a bullish correction today, but downside risks remain high, with the nearest support located only at 1.2310, namely the weekly S1.

Traders' Sentiment

Today 61% of traders hold long positions (previously 59%), whereas 53% of all pending orders are to sell the Pound, up from 50% on Friday.

Trade Idea : GBP/USD – Sell at 1.2450

GBP/USD - 1.2401

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2387

Kijun-Sen level : 1.2418

Ichimoku cloud top : 1.2469

Ichimoku cloud bottom : 1.2465

Original strategy :

Sell at 1.2450, Target: 1.2350, Stop: 1.2485

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2450, Target: 1.2350, Stop: 1.2485

Position : -

Target : -

Stop : -

As the British pound found good support around 1.2365-66 and has recovered, suggesting consolidation above this level would be seen an above the Kijun-Sen (now at 1.2418) would bring recovery towards 1.2450-55 before prospect of another decline, below said support at 1.2365-66 would extend recent decline from 1.2616 to 1.2350, then towards 1.2325-30 but near term oversold condition should limit downside and reckon 1.2300 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as 1.2450-60 should limit upside. Above the upper Kumo (now at 1.2469) would defer and suggest low is formed instead, risk test of resistance at 1.2506 first, break there would confirm, then a stronger rebound to 1.2525-30 would follow.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0674; (P) 1.0690; (R1) 1.0703; More...

Intraday bias is neutral in EUR/CHF remains neutral as it's staying in range above 1.0668 temporary low. The bearish outlook remains unchanged. That is, rebound from 1.0629 has completed at 1.0823. And the larger decline from 1.1198 is likely still in progress. On the downside, below 1.0668 will target 1.0620/29 key support zone. Decisive break there will resume whole fall from 1.1198 and target next long term fibonacci level at 1.0485. Nonetheless, break of 1.0734 will suggest that pull back from 1.0823 is completed and turn bias back to the upside for this resistance.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Current development suggests that it's not completed yet. Sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485. In any case, break of 1.0823 resistance is needed to be the first indication of reversal. Otherwise, deeper fall is still expected even in case of recovery.