Sample Category Title

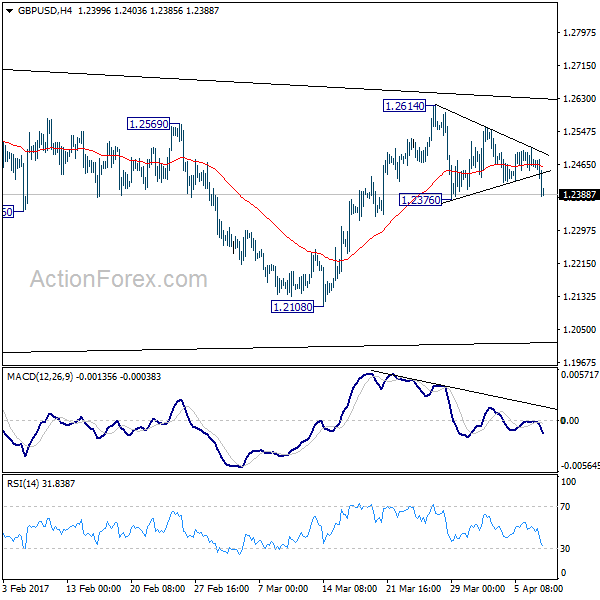

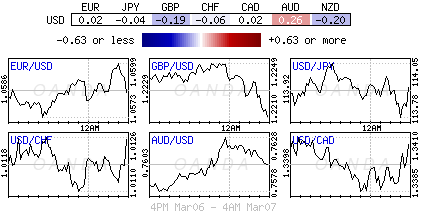

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2444; (P) 1.2474; (R1) 1.2499; More...

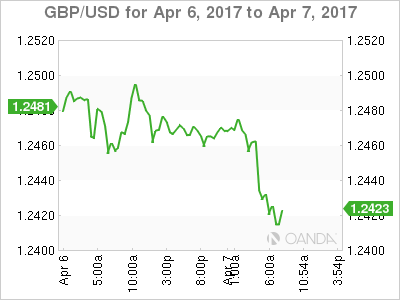

GBP/USD's sharp fall in early US session argues that fall from 1.2614 is possibly resuming. Intraday bias is cautiously on the downside for 1.2376. Break will confirm and target 1.2108 support level. Overall, price actions from 1.1946 are viewed as a consolidation pattern. Decisive break of 1.2108 will be an early sign of larger down trend resumption. On the upside, break of 1.2614 will extend the rise from 1.2108. But upside should be limited by 1.2705/2774 resistance zone to bring larger down trend resumption eventually.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

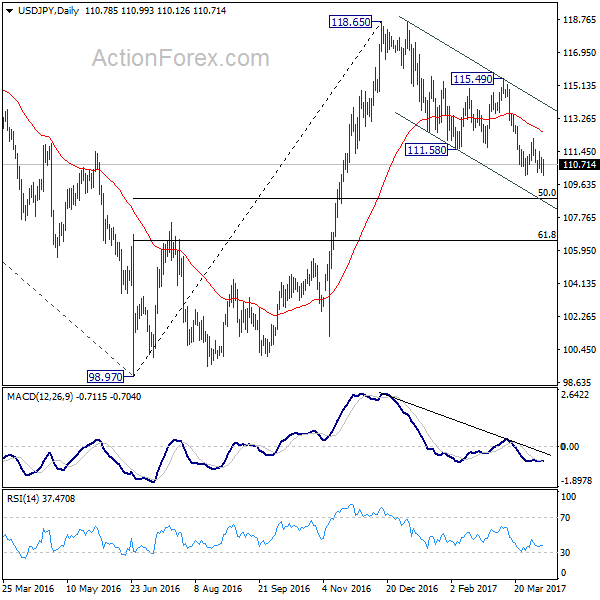

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.34; (P) 110.74; (R1) 111.19; More....

USD/JPY is still bounded in range above 110.10 and intraday bias remains neutral. More consolidation could still be seen. But, break of 112.19 resistance is needed to indicate short term reversal. Otherwise, outlook will stay bearish for another fall. Break of 110.10 will extend the whole decline from m 118.65 and target 50% retracement of 98.97 to 118.65 at 108.81. On the upside, however, break of 112.19 resistance will indicate short term reversal and turn bias back to the upside for 115.49 resistance.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.16) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

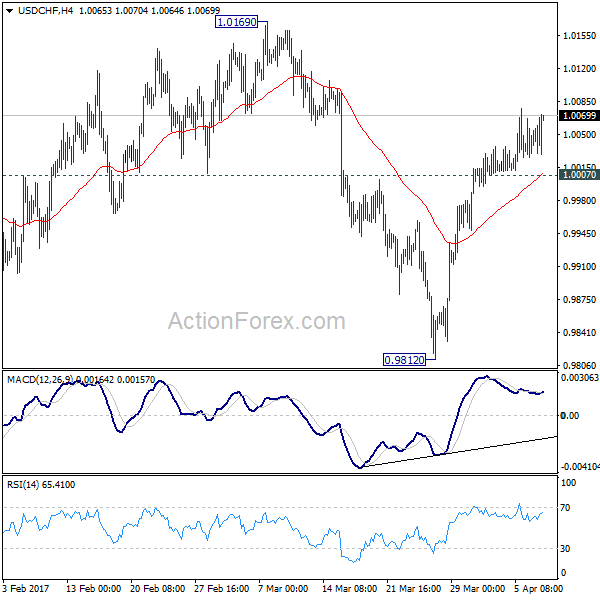

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0028; (P) 1.0047; (R1) 1.0069; More.....

USD/CHF's rally from 0.9812 is still in progress with 1.0007 minor support intact and further rise should be seen. We mentioned before that corrective decline fall from 1.0342 should have finished with three waves down to 0.9812 already. Rise from 0.9812 is expected to taken 1.0169 resistance next. Break of 1.0169 should confirm this bullish case and target a test on 1.0342 high. On the downside, below 1.0007 will bring deeper correction, possibly back to 0.9812 low.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

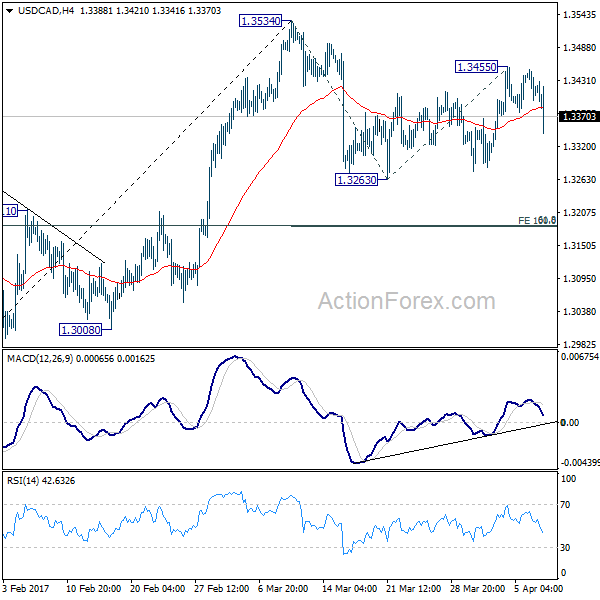

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3390; (P) 1.3420; (R1) 1.3442; More....

USD/CAD's sharp fall and break of 1.3373 minor support suggests that recovery from 1.3263 has completed with three waves up to 1.3455. The corrective structure in turns indicates that decline from 1.3534 is resuming. Intraday bias is turned back to the downside for 1.3263 support and below. Fall from 1.3534 is still viewed as a correction for the moment. Hence, we'd expect strong support from 1.3184 cluster level (61.8% retracement of 1.2968 to 1.3534 at 1.3184, 100% projection of 1.3534 to 1.3263 from 1.3455 at 1.3814 too) to contain downside and bring rebound. On the upside, break of 1.3455 will turn bias back to the upside for 1.3534 resistance.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 will argue that the third leg has already started and should at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Non-Farm Payroll Grew Only 98k, USD/CAD Dives but Not a Disaster for Dollar Yet

US non-farm payroll report comes in much weaker than expected. Only 98k jobs were created in March, around half of expectations of 177k only. Prior month's figure was also revised down from 235k to 219k. Unemployment rate dropped 0.2% to 4.5%, hitting the lowest level in nearly 10 years. Average hourly earnings posted 0.2% mom rise in March, below expectation of 0.3%. Released from Canada, employment rose 19.4k in March versus expectation of 5.7k. Unemployment rate rose to 6.7%. Notable weakness is seen in USD/CAD after the releases, as Canadian dollar is additionally supported by surge in oil price. Some buying is seen in the Japanese yen, on risk aversion and possibly on expectation of fall in treasury yields too. Meanwhile, dollar is so far steady against European majors.

US launched military strike in Syria, Russia Condemned, China Xi Overshadowed

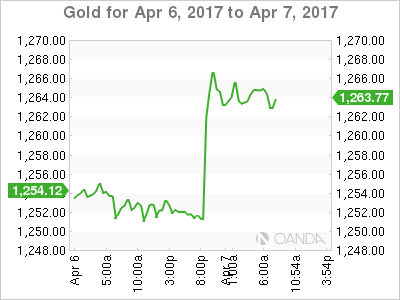

Gold and WTI Crude oil jump today on news that US launched military strike on the airfield in Syria in response to the government's use of chemical weapons on civilians. Stocks, however, are relatively steady with just mild safe haven flows. Russian President Vladimir Putin condemned the US strike as "act of aggression against a sovereign state". Meanwhile, Putin suspended the 2015 memorandum of understanding on air operation. And, Putin's spokesman said that the risk on confrontation between US and Russia as "significantly increased". Also, Putin ordered additional measures to strengthen Syria's air defenses to protect the "most sensitive" infrastructure assets of the country. The development overshadows the meeting between Trump and Chinese President Xi Jinping.

BoE Carney: Brexit negotiations a litmus test for responsible financial globalization

BoE Governor Mark Carney said today that "how Brexit negotiations conclude will be a litmus test for responsible financial globalization." And, the EU and UK are "ideally positioned to create an effective system of deference to each other's comparable regulatory outcomes, supported by commitments to common minimum standards and open supervisory cooperation." Meanwhile, Carney also said that " level of planning is uneven across firms" regarding Brexit. And, "plans may not be being sufficiently tested against the most adverse potential outcomes - for example, if there is no withdrawal or trade agreement in place when the UK exits from the EU."

Release from UK, industrial production dropped -0.8% rose 2.8% yoy in February, versus expectation of 0.2% mom, 3.7% yoy. Manufacturing production dropped -0.1% mom, rose 3.3% yoy, versus expectation of 0.3% mom, 3.9% yoy. Construction output dropped -1.7% mom in February. Trade deficit widened to GBP -12.5b in February. NIESR GDP estimate rose 0.5% in March.

ECB Praet: Premature to discuss reduction of asset purchases

ECB chief economist Peter Praet said in a TV interview that it's "premature" to discuss further reduction of asset purchases. He warned earlier this week that "if investors start perceiving that the path of the policy rate is subject to upward uncertainty ... long-term interest rates will be pushed higher and asset purchases will become less effective." ECB President Mario Draghi also said that there was no "sufficient evidence to materially alter our assessment of the inflation outlook". Therefore, "reassessment of the current monetary policy stance is not warranted at this stage." And those include "interest rates, asset purchases and forward guidance."

Also released from Europe, German industrial production rose 2.2% mom in February, trade surplus widened to EUR 2.1b in February. Swiss unemployment rate was unchanged at 3.3% in March. Swiss foreign currency reserves rose to CHF 683.0b in March.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3390; (P) 1.3420; (R1) 1.3442; More....

USD/CAD's sharp fall and break of 1.3373 minor support suggests that recovery from 1.3263 has completed with three waves up to 1.3455. The corrective structure in turns indicates that decline from 1.3534 is resuming. Intraday bias is turned back to the downside for 1.3263 support and below. Fall from 1.3534 is still viewed as a correction for the moment. Hence, we'd expect strong support from 1.3184 cluster level (61.8% retracement of 1.2968 to 1.3534 at 1.3184, 100% projection of 1.3534 to 1.3263 from 1.3455 at 1.3814 too) to contain downside and bring rebound. On the upside, break of 1.3455 will turn bias back to the upside for 1.3534 resistance.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 will argue that the third leg has already started and should at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | JPY | Labor Cash Earnings Y/Y Feb | 0.40% | 0.50% | 0.50% | 0.30% |

| 05:00 | JPY | Leading Index Feb P | 104.4 | 104.6 | 104.9 | |

| 05:45 | CHF | Unemployment Rate Mar | 3.30% | 3.30% | 3.30% | |

| 06:00 | EUR | German Industrial Production M/M Feb | 2.20% | -0.20% | 2.80% | 2.20% |

| 06:00 | EUR | German Trade Balance (EUR) Feb | 21.0B | 19.4B | 18.5B | |

| 07:00 | CHF | Foreign Currency Reserves Mar | 683.0B | 674.0B | 668.2B | |

| 08:30 | GBP | Industrial Production M/M Feb | -0.70% | 0.20% | -0.40% | |

| 08:30 | GBP | Industrial Production Y/Y Feb | 2.80% | 3.70% | 3.20% | |

| 08:30 | GBP | Manufacturing Production M/M Feb | -0.10% | 0.30% | -0.90% | |

| 08:30 | GBP | Manufacturing Production Y/Y Feb | 3.30% | 3.90% | 2.70% | |

| 08:30 | GBP | Construction Output M/M Feb | -1.70% | 0.00% | -0.40% | |

| 08:30 | GBP | Visible Trade Balance (GBP) Feb | -12.5B | -10.9B | -10.8B | |

| 12:00 | GBP | NIESR GDP Estimate Mar | 0.50% | 0.60% | 0.60% | |

| 12:30 | CAD | Net Change in Employment Mar | 19.4K | 5.7k | 15.3k | |

| 12:30 | CAD | Unemployment Rate Mar | 6.70% | 6.70% | 6.60% | |

| 12:30 | USD | Change in Non-farm Payrolls Mar | 98K | 177k | 235k | 219K |

| 12:30 | USD | Unemployment Rate Mar | 4.50% | 4.70% | 4.70% | |

| 12:30 | USD | Average Hourly Earnings M/M Mar | 0.20% | 0.30% | 0.20% | 0.30% |

| 14:00 | CAD | Ivey PMI Mar | 56.3 | 55 |

Non-Farm Payroll First, Middle East Second

Friday April 7: Five things the markets are talking about

Momentum in the U.S labor market was strong going into last month, however bad weather during non-farm payroll's (NFP) mid-March sample week pose the risk of weather-related delays in hiring.

Market consensus is looking for a headline print atop of +180k mark, which would be a very healthy rate of monthly growth, but off the Jan and Feb pace of +235k. A weaker print will have the market revising U.S Q1 GDP expectations.

Note: Advance indicators this week are mixed. Tuesday's ADP did not see any weakness for Mar., but instead recorded a solid gain (+263k vs. +184k), extending both Jan and Feb's trend. In contrast, the employment-index of the ISM non-manufacturing report Wed. points to a slowdown in hiring. Yesterday's U.S weekly jobless claims posted the largest drop in two years (+234k vs. +251k).

The U.S unemployment rate is expected to hold steady atop of its nine-year low of +4.7%.

Investors are also watching developments from the summit in Florida between Trump and Chinese President Xi Jinping.

Note: Expect the market to remain very nervous after Trump's missile attack on Syria last night – the capital market move, since dissipated, triggered an instant reaction across everything from stocks to commodities and currencies.

The attack caused a knee-jerk shift into safe-havens, although the impact was moderate as it is being interpreted as a "one-off" proportionate response.

1. No surprise, global equities mixed response to Syria missile attack

Japan's Nikkei (+0.4%) share average edged up in choppy trade overnight, but gains were limited as the U.S missile strike on Syria curbed investors' risk appetite. The broader Topix index climbed +0.7%.

In China, the Shanghai Composite Index rose +0.2%, and completed a +2% gain for the holiday-shortened week. In Hong Kong, the Hang Seng dropped -0.4%, while Singapore's Straits Times Index fell -0.3%.

In Europe, equity indices are trading lower amid geopolitical tensions. Banking stocks are leaning on Eurostoxx 600, while the FTSE 100 is slightly outperforming as oil stocks trade higher in line with Brent and WTI contracts.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.5% at 3,474, FTSE -0.1% at 7,294, DAX -0.6% at 12,161, CAC-40 -0.4% at 5,102, IBEX-35 -0.7% at 10,442, FTSE MIB -0.3% at 20,238, SMI -0.5% at 8,598, S&P 500 Futures -0.1%

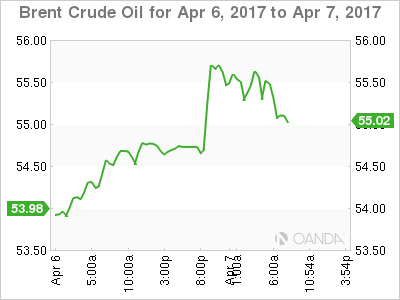

2. Oil jumps in knee-jerk reaction to Syria

Oil futures surged more than +2% to a one-month high overnight after the U.S launched its missile attack on a Syrian airbase. However, prices have since retreated a tad as there seemed no immediate threat to supplies.

Ahead of the attack, Brent crude futures were trading atop of +$55.62 then jumped to +$56.08 per barrel and up +1.3% from yesterday's close. U.S West Texas Intermediate (WTI) crude futures also climbed by more than +2%, to a high of +$52.94 a barrel, before receding to +$52.46, up +1.45%.

Note: Although Syria has limited oil production; its location in the Middle East and alliances with big oil producers raises concerns about spreading conflict that could disrupt crude shipments. Both Russia and Iran, staunch allies of Syria, condemned the attacks.

However, in oil supply fundamentals, markets remain oversupplied, even with efforts led by the OPEC to cut supplies to support global prices.

Gold rose more than +1% overnight to hit a five-month high as investors sought safe-haven assets. The yellow metal is trading at +$1,263.53 per ounce. The markets see higher prices in the short-term, at least until there is some clarity around Syria and if the "one-off" airstrike develops into something more.

3. Safe haven flows dominate bond prices

Bonds were amongst the biggest gainers across the various asset classes following the first Middle East military strike by the Trump administration.

Core European government bonds opened higher amid the broad flight-to-quality move after the Syria strikes. However, these early gains have since faded. Currently, 10-year Bund yields are trading lower by -2 bps to +0.24%.

Note: In typical risk-off fashion, Euro core bonds outperformed, while Italian and Spanish 10-year yields were little changed.

U.S. Treasury yields dropped to their lowest level in over four-months at +2.29% in risk averse trading, yields have since found support with 10's trading atop of +2.32% ahead of non-farm payrolls (NFP).

4. Safe haven trade dominates currency proceedings

Geopolitical has been able to keep market risk appetite sidelined, however, its boosted safe-haven assets after U.S launched numerous missile strikes on a Syrian airbase deemed responsible for recent chemical attack on civilians.

USD/JPY tested the lower end of the psychological ¥110 level on the initial reports of the U.S missile attack, but has since stabilized back to this week's mid-¥110 area (¥110.60). Another go to currency of choice during stress, the CHF ($1.0054) is little changed from its opening level in Asia.

The pound (£1.2425, down -0.3%) is softer after Feb Industrial Production and Trade data (see below) came in worse then expectations.

5. U.K Industrial Production and Trade data miss expectations

U.K. manufacturing output was weaker than expected in February, falling by -0.1% from January compared to a forecast rise of +0.3%. The year-to-year rise was also weaker, at +3.3% as against a +3.8% expected.

There was a larger fall in industrial production over the month as a warmer-than-usual Feb. reduced demand for electricity. Output was down +0.7% from Jan. as against a forecast drop of -0.1%.

Note: January's figures for both manufacturing and industrial production were slightly revised, but still recorded month-to-month decline – it's been a weak start to 2017.

Other data showed that U.K.'s deficit widened in Feb, although that was largely due to imports of big-ticket items. The U.K imported £12.5B more than it exported.

Canadian Dollar Edges Lower Ahead Of Canadian, US Job Data

USD/CAD is almost unchanged in the Friday session, as the pair trades slightly above the 1.34 line. On the release front, job numbers are in the spotlight on both sides of the border. Canada releases Employment Change and the unemployment rate, while the US releases three key events – Nonfarm Payrolls, Average Hourly Earnings and the unemployment rate.

Weak oil prices in the first quarter of 2017 have weighed on the Canadian dollar, which has been unable to make any inroads against its US counterpart. US crude continues to trade just above the $50 level, as the tug-of-war between OPEC and the US producers continues. The glut of oil worldwide remains as higher US production has offset OPEC cuts. US Crude Inventories continue to show surpluses, most of which have been higher than the forecast. This was the case again last week, with US crude inventories posting a strong gain of 1.6 million, surprising the markets which had forecast a decline. The indicator has posted 12 surpluses in the last 13 weeks, which has helped keep a lid on higher oil prices throughout 2017.

There were no surprises from the Federal Reserve policy minutes, which were released on Wednesday. The minutes had a slightly hawkish tone, as policymakers noted upside risk to the US economy. However, policymakers remain divided on whether inflation will rise to the Fed target of 2.0% percent. The minutes also stated FOMC members were in favor of taking steps to trim the $4.5 trillion balance sheet, which has ballooned since the Fed implemented its aggressive quantitative easing program back in 2008. However, the Fed is unlikely to make any moves in this front till later in the year, as President Trump’s fiscal policy remains a big question mark. So what’s next for the Federal Reserve? According to the CME’s Fed Watch, the odds of a rate hike at the May meeting are just 5 percent, while the likelihood of a rate hike in June stand at 63 percent. . Fed policymakers appear divided on how many more times the Fed will press the rate trigger. Last week, FOMC member Eric Rosengren called for three more hikes, saying the Fed should raise rates in June, September and December. Rosengren said that employment and inflation levels were close to the Fed’s targets, and that three additional hikes were needed in order to prevent the US economy from overheating. However, a majority of FOMC members are in favor of just two more hikes this year.

The Dollar, Yen, Swiss Franc and Gold Jump as Tension Rises in Middle East

- 'The global financial system is moving from fragility to resistance' says Mark Carney

- The Dollar, Yen, Swiss Franc and gold jump as tension rises in Middle East

- Market looks towards the Non-Farm Payroll later today

In the UK, Mark Carney's speech at 10:00 BST was billed as a top tier announcement, although what he was actually speaking about was not confirmed before the speech. Carney's announcement was watched eagerly for any snippet of monetary policy speak, which can have a profound effect on the strength of Sterling. Carney discussed the security and responsibilities of the financial system in the UK and said that "the global financial system is moving from fragility to resistance" and highlighted the UK's role as a key international financial centre.

However, he pointed out risks that need to be addressed globally, of not working together with other countries' financial systems and the risks that poses to liquidity and funding; and the risks to the UK's financial system, due to its complexity and size. He discussed the need for resilience and risk management in light of Brexit. Carney also emphasised the importance of Brexit globally by saying, "How the Brexit negotiations conclude will be a litmus test for responsible financial globalisation" and speaking positively about the UK's strong position in the negotiations. He was keen to point out the opportunities for increased trade and globalisation that this presents.

The outcomes of this morning's speech provided a boost for the Pound, which bodes well for this afternoon's release of the National Institute of Economic and Social Research (NIESR) Gross Domestic Product (GDP) Estimate for the UK, with it expected at 0.6% - anything wide of the mark could result in volatility for the Pound, but this morning's discussions may just have given Sterling the helping hand it needed.

Traders will be looking for safe havens this morning with tensions in the Middle East ratcheting up as the US bombed an airfield in Syria overnight. The airbase allegedly responsible for launching the chemical weapons attack earlier this week. The US administration have stated that there can be no future in Syria for Mr Assad and this will now complicate relationships between themselves and Russia. The Dollar, Yen, Swiss Franc and gold have gained on the news.

The main event today in the US today will be US non-farm payrolls at 13:30 BST and with the week's precursor ADP figure overshooting the mark, positive things are expected for today. How much of this is already priced in is hard to tell.

Markets are expecting a rise of 180,000 and although as mentioned, the private report was better than expected. Building activity has picked up and the housing market has been largely buoyant, this could translate into a better than expected payroll report sparking further strength in the Dollar.

Spring Jokes

When do monkeys fall from the sky?

During Ape-ril showers!

Can February March?

No, but April May!

What flowers grow on faces?

Tulips (Two-lips)!

Why is everyone so tired on April 1?

Because they've just finished a long, 31 day March!

Technical Outlook: FTSE Is Back Above Daily Cloud As Pound Weakens

FTSE managed to recover and emerge above daily cloud (cloud top lies at 7241), following spikes lower that penetrated deeply into cloud, yesterday and today.

Repeated strong downside rejections are seen as bullish signal, as cloud is still acting as support.

Fresh strength was also boosted by weakness of the pound that is probing below key supports and threatening of further easing.

The upside extension cracked daily Tenkan-sen barrier (7252) that further improves near-term picture.

Near-term studies are in bullish/neutral mode while dailies give mixed signals but expected to remain bullishly aligned while the price is holding above the cloud.

We look for close above daily cloud for firmer bullish signals.

Alternative scenario requires return into daily cloud to generate negative signal and re-focus recent lows at 7195/79.

Res: 7259, 7269, 7281, 7287

Sup: 7252, 7241, 7223, 7195

EUR/GBP Edges Up Post Soft UK Data And Carney’s Speech

EUR/GBP downtrend was held above the significant support line at 0.8500, after hitting a 5-week low of 0.8485 on March 31.

EUR/GBP bulls failed to gain the near-term major resistance level at 0.8600 on April 5, as the pressure at the level is heavy.

The bulls have regained momentum since this morning, as a result of a weakening Sterling caused by underperforming UK industrial and manufacturing data (Feb) and the Bank of England President Carney's statement.

Carney made a speech after the release of the data. He stated that the Brexit negotiation would influence bank regulations and cooperation. The transition period poses a risk to the stability of financial system.

On the 4-hourly chart, the price is heading from the lower band to the middle band by the Bollinger Band indicator, suggesting the bullish momentum is strengthening.

The resistance level is at 0.8565, followed by 0.8580 and 0.8600.

The support line is at 0.8530, followed by 0.8510 and 0.8500.