Sample Category Title

Australian Dollar Lower after Retail Sales Disappointment, Japanese Yen Soft after Tankan Survey

The forex markets opened the week relatively quietly with the exception of Australian Dollar. Aussie dives broadly after weak retail sales data and stays weak ahead of RBA rate decision. Meanwhile, Yen follows as the second weakest as Tankan survey showed less than expected improvements in sentiments. On the other hand, Euro is paring some of last week's loss. Focus will turn to French elections in April. Dollar is trading mixed ahead of a string of important economic data. That starts with ISM manufacturing today, ISM services on Wednesday and non-farm payroll on Friday. Fed will also release March FOMC meeting minutes this week.

Japan Tankan showed insufficient improvements

Japan Tankan large manufacturers index rose to 12 in Q1, up from 10 but missed expectation of 14. Large manufacturers outlook rose to 11, up from 8, but missed expectation of 13. Non-manufacturing index rose to 20, up from 18 and beat expectation of 19. Non-manufacturing outlook was unchanged at 16, missed expectation of 19. Large all industry capex rose 0.6%, beat expectation of -0.3% fall. The set of data showed that improvements in business condition in large manufacturers was not as much as anticipated. Some economists noted that the Tankan result point to 2% GDP growth in last quarter. While growth would remain solid, momentum could be starting to slow. And it's still unlikely for BoJ to meet 2% inflation target within time frame, considering that Tokyo CPI dropped more than expected by -0.4% yoy in March.

Aussie dives after weak retail sales

Australian dollar tumbles sharply today after weaker than expected retail sales. Sales dropped -0.1% mom in February versus expectation of 0.3% rise. Apparels was the biggest drag in sales, posting -2.5% mom fall. Meanwhile, sales of household goods dropped -0.4%. Executive director of the Australian Retailers Association noted that "discretionary spend" is showing impact in the data. Also from Australia TD securities inflation expectation rose 0.1% mom in March. Building approvals jumped 8.3% mom in February.

RBA rate decision is a main focus tomorrow and the central bank is widely expected to keep interest rate unchanged at 1.50%. There is little prospect of a rate cut this year as housing markets heat up again in recent months. Little new information would be given from this week's meeting as RBA would wait for the set of Q1 data to be released later before adjusting economic outlook. But for the moment, some notable weakness is seen in Aussie broadly.

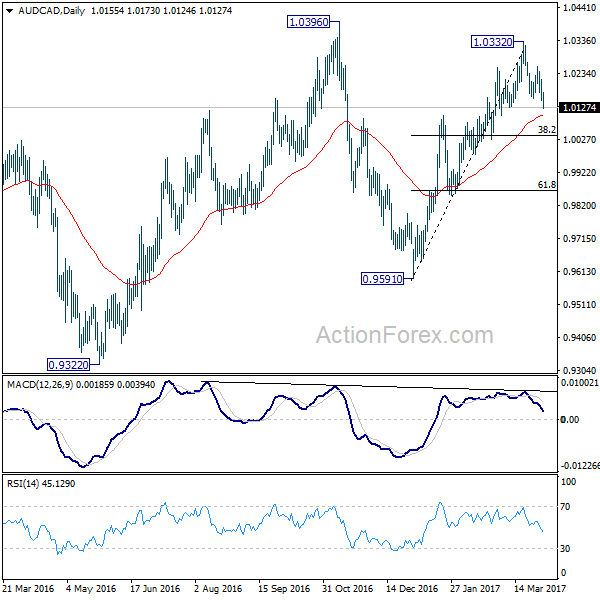

AUD/CAD's sharp decline today confirms resumption of fall from 1.0332 short term top. The development also suggests that rise from 0.9591 is completed already. Deeper fall should be seen back to 38.2% retracement of 0.9591 to 1.0332 at 1.0049 in near term. And the fall could extend to 61.8% retracement at 0.9874 and below. But overall, the cross is bounded in long term consolidation pattern start at 1.0784 (2012 high). And it stayed in range between 0.9148/1.0784 for more than five years. We're not seeing any clear long term trend yet.

PMI data the highlights today

PMI data will be the main focus today. Swiss will release retail sales and SVME PMI. Eurozone will release PPI, unemployment rate and PMI manufacturing final. UK will release PMI manufacturing. US will release ISM manufacturing and construction spending. Looking ahead, a number of important economic data will be released from US, including non-farm payroll. Fed will also release March FOMC minutes. However, it should be noted that based on recent Fedspeaks, two more hikes remains the base case in most policymakers' mind. Improvements in economic data could trigger speculation of one more hike. But the re-establishment of trend would likely depend on US president Donald Trump's economic policies. Here are some highlights for the week ahead:

- Tuesday: Australia trade balance; UK construction PMI; Eurozone retail sales; Canada trade balance; US trade balance, factory orders

- Wednesday: Eurozone services PMI final; UK services PMI; US ADP employment, ISM services, FOMC minutes

- Thursday: Japan consumer confidence; Germany factory orders; Swiss CPI; Eurozone retail PMI, ECB meeting accounts; US jobless claims; Canada building permits

- Friday: Japan labor cash earnings; leading indicator; Swiss unemployment, foreign currency reserves; German industrial production, trade balance; UK industrial and manufacturing production, trade balance; Canada employment, Ivey PMI; US non-farm payroll

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.02; (P) 111.60; (R1) 111.98; More....

Intraday bias in USD/JPY remains neutral for the moment. On the upside, break of 112.19 temporary will turn bias back to the upside for 115.49 resistance. Decisive break there should confirm completion of the correction from 118.65. In that case, further rise should be seen to 118.65 and above to resume the rally from 98.97. On the downside, though, below 110.99 minor support will turn bias back to the downside for 110.10 and break will extend the corrective fall from 118.65.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.16) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturers Index Q1 | 12 | 14 | 10 | |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q1 | 11 | 13 | 8 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q1 | 20 | 19 | 18 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q1 | 16 | 19 | 16 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q1 | 0.60% | -0.30% | 5.50% | |

| 23:50 | JPY | Tankan Small Mfg Index Q1 | 5 | 3 | 1 | |

| 23:50 | JPY | Tankan Small Mfg Outlook Q1 | 0 | 1 | -4 | |

| 23:50 | JPY | Tankan Small Non-Mfg Index Q1 | 4 | 2 | 2 | |

| 23:50 | JPY | Tankan Small Non-Mfg Outlook Q1 | -1 | -1 | -2 | |

| 0:30 | JPY | PMI Manufacturing Mar F | 52.4 | 52.6 | 52.6 | |

| 1:00 | AUD | TD Securities Inflation M/M Mar | 0.10% | -0.30% | ||

| 1:30 | AUD | Retail Sales M/M Feb | -0.10% | 0.30% | 0.40% | |

| 1:30 | AUD | Building Approvals M/M Feb | 8.30% | -1.50% | 1.80% | |

| 7:15 | CHF | Retail Sales (Real) Y/Y Feb | -0.80% | -1.40% | ||

| 7:30 | CHF | SVME PMI Mar | 58 | 57.8 | ||

| 7:45 | EUR | Italy Manufacturing PMI Mar | 55.1 | 55 | ||

| 7:50 | EUR | France Manufacturing PMI Mar F | 53.4 | 53.4 | ||

| 7:55 | EUR | Germany Manufacturing PMI Mar F | 58.3 | 58.3 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Mar F | 56.2 | 56.2 | ||

| 8:30 | GBP | PMI Manufacturing Mar | 55 | 54.6 | ||

| 9:00 | EUR | Eurozone PPI M/M Feb | 0.10% | 0.70% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Feb | 4.30% | 3.50% | ||

| 9:00 | EUR | Eurozone Unemployment Rate Feb | 9.50% | 9.60% | ||

| 14:00 | USD | ISM Manufacturing Mar | 57.1 | 57.7 | ||

| 14:00 | USD | ISM Prices Paid Mar | 66 | 68 | ||

| 14:00 | USD | Construction Spending M/M Feb | 1.00% | -1.00% |

GBP/USD: UK’s Economic Growth Confirmed At 0.7% In The Final Three Months Of 2016

For the 24 hours to 23:00 GMT, the GBP rose 0.42% against the USD and closed at 1.2527 on Friday, after the final gross domestic product (GDP) in the UK advanced 0.7% on a quarterly basis in 4Q 2016, at par with market expectations and confirming the initial estimate. In the prior quarter, the nation's GDP had risen 0.6%.

On the contrary, the nation's seasonally adjusted house prices registered an unexpected drop of 0.3% on a monthly basis in March, dropping for the first time since June 2015 and pointing to a slowdown in the nation's property market as the country prepares to leave the European Union. House prices had advanced 0.6% in the previous month, whereas market participants anticipated for an advance of 0.3%.

In the Asian session, at GMT0300, the pair is trading at 1.2540, with the GBP trading 0.1% higher against the USD from Friday's close.

The pair is expected to find support at 1.2462, and a fall through could take it to the next support level of 1.2385. The pair is expected to find its first resistance at 1.2586, and a rise through could take it to the next resistance level of 1.2633.

Trading trends in the Pound today is expected to be determined by the release of UK's Markit manufacturing PMI for March, set to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

USD/JPY: Japan’s Nikkei Manufacturing Index Revised Lower In March

For the 24 hours to 23:00 GMT, the USD declined 0.42% against the JPY and closed at 111.32 on Friday.

In the Asian session, at GMT0300, the pair is trading at 111.32, with the USD trading flat against the JPY from Friday's close.

Early morning data indicated that Japan's final Nikkei manufacturing PMI eased to a level of 52.4 in March, although remained in the expansion territory, compared to a level of 53.3 in the prior month. The preliminary figures had indicated a fall to 52.6. Moreover, the nation's Tankan large manufacturing index registered a less-than-expected rise to a level of 12.0 in the first quarter of 2017, compared to a reading of 10.0 in the prior quarter. Further, the nation's non-manufacturing index rose more-than-anticipated to a level of 20.0 in 1Q 2017, compared to a level of 18.0 in the previous quarter. Also, the nation's Tankan large manufacturing outlook index advanced to a level of 11.0 in 1Q 2017, compared to a reading of 8.0 in the previous quarter, while the outlook for non-manufacturing index remained steady at a level of 16.0 in 1Q 2017.

The pair is expected to find support at 110.88, and a fall through could take it to the next support level of 110.45. The pair is expected to find its first resistance at 111.97, and a rise through could take it to the next resistance level of 112.63.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

USD/CHF: Swiss Franc Trading Flat, Ahead Of Switzerland’s Real Retail Sales Data

For the 24 hours to 23:00 GMT, the USD rose 0.08% against the CHF and closed at 1.0012 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.0012, with the USD trading flat against the CHF from Friday's close.

The pair is expected to find support at 0.9993, and a fall through could take it to the next support level of 0.9974. The pair is expected to find its first resistance at 1.0030, and a rise through could take it to the next resistance level of 1.0048.

Moving ahead, traders will closely monitor Switzerland's real retail sales for February and the SVME–PMI for March, slated to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

USD/CAD: Canada’s Economic Growth Accelerated In January

For the 24 hours to 23:00 GMT, the USD declined 0.29% against the CAD and closed at 1.3296 on Friday.

The Canadian Dollar gained ground, after data showed that Canada's gross domestic product (GDP) jumped 0.6% on a monthly basis in January, driven by robust activity in manufacturing sector. In the previous month, the GDP had climbed 0.3%.

In the Asian session, at GMT0300, the pair is trading at 1.3315, with the USD trading 0.14% higher against the CAD from Friday's close.

The pair is expected to find support at 1.3275, and a fall through could take it to the next support level of 1.3235. The pair is expected to find its first resistance at 1.3361, and a rise through could take it to the next resistance level of 1.3407.

Ahead in the day, traders will keep a close watch on Canada's RBC manufacturing PMI for March and the Bank of Canada's business outlook survey report.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Daily Technical Analysis

EURUSD

The EURUSD had a bearish momentum last week bottomed at 1.0651 after formed a 'shooting star' formation on daily chart following a false break above 1.0873 key resistance. The bias is bearish in nearest term testing 1.0600 region. Immediate resistance is seen around 1.0700. A clear break above that area could lead price to neutral zone in nearest term testing 1.0750 but price is still in a valid short-term bearish trend and as long as stay below 1.0750 any upside pullback should be seen as a good opportunity to sell. On the downside, a clear break and daily close below 1.0600 would expose 1.0500 region. Overall I remain neutral.

GBPUSD

The GBPUSD attempted to push lower last week bottomed at 1.2375 but whipsawed to the upside and closed higher at 1.2553. As you can see on my H1 chart below price is moving back above the H1 EMA 200 and inside a bullish channel suggests a short-term bullish view. The bias is bullish in nearest term testing 1.2615 region. Immediate support is seen around 1.2520/00. A clear break below that area could lead price to neutral zone in nearest term testing 1.2450 area. Overall I remain neutral.

USDJPY

The USDJPY was indecisive last week. The 'hammer' bullish reversal signal remains valid although we haven’t seen a convincing and strong/consistent movement above 111.30 key level area so far. The bias is neutral in nearest term. Immediate support is seen around 111.00. A clear break below that area could trigger further bearish pressure testing 110.70/50 area but key support remains at 110.10. Immediate resistance is seen around 111.60. A clear break above that area could trigger further bullish pressure testing 112.00 or higher.

USDCHF

The USDCHF attempted to push lower last week bottomed at 0.9813 but whipsawed to the upside and closed higher at 1.0023. The bias is bullish in nearest term testing 1.0060. A clear break and daily close above that area would expose 1.0120 region. Immediate support is seen around 0.9990. A clear break below that area could lead price to neutral zone in nearest term testing 0.9950 area. Overall I remain neutral.

Market Morning Briefing

STOCKS

Overall all stocks are mixed. Dow, Shanghai, Nikkei and Nifty looks bullish while Dax could face immediate resistance.

Dow (20663.22, -0.31%) is trying hard to rise from levels near 20400 levels and could slowly inch up towards 21200 in the near term. There is some more room on the upside for the near term. A re-test of 20500-20400 levels could also be a possibility during the week.

Dax (12312.87, +0.46%) has been moving up, much in line with our expectation and could test immediate resistance near 12400 from where a short dip towards 12220 is possible.

Nikkei (18977.37, +0.36%) fell sharply on Friday on a fall in Dollar-Yen from levels near 112.20 but the support on Nikkei above 18600 may hold giving another bounce to the price index in the coming sessions towards 19200 and higher.

Shanghai (3222.51, +0.38%) bounced back from just above the daily trend-support. While that holds, we could target for a rise towards 3250 and higher in the near term.

Nifty (9173.75) looks strongly bullish for the near to medium term. A rise towards 9200-9280 is on the cards for the coming sessions.

COMMODITIES

Gold (1246) and Silver (18.23) are going nowhere as they keep trading in the narrow range of 1237-1263 and 17.94-18.50 respectively, which may continue for the rest of the week. Global cues are in favor of gold and silver as a break below 99.70 for Dollar Index (100.26) could be resulted in good gains for bullion. We have been expecting 1237 for gold and 17.90 for silver to hold for the current week and gradual buying at lower levels can’t be ruled as buyers are taking every dip as a further opportunity for buying.

Copper (2.65) is trading within a range of 2.55-2.70 with no directional bias. Only above 2.70, higher resistances of 2.80 can come into consideration. In the medium term 2.55-57 are going to be a strong support now but a close below that could open up 2.49 levels.

Brent (52.83) and WTI (50.56) both are trading within their narrow ranges of 52-53.5 and 50.30-51.70. Considering the short term overbought state, we may see some profit taking at higher levels. The trend is still bearish in the near to medium term time frame and a close below their supports could open up 50 for Brent and 48.36 for WTI as well.

Gold WTI ratio (24.69) may find support at current levels and could bounce back towards 26-27 levels.

FOREX

A pause day for all the currencies. This rest phase may go on for another 1-2 sessions.

Dollar Index (100.40) has made a high at 100.60, very close to our initial target of 100.70 but the strength at the higher levels hint at further rally towards 101.00 in the coming days.

Euro (1.0678) has found interim support near 1.0650 for now but failure to rise and sustain above 1.0700 levels may push it down once again towards 1.0580.

Dollar-Yen (111.36) has been rejected exactly from our interim resistance of 112.15 but as long as it trades above 110.90-75, the chances of seeing 112.80 and 113.40 can’t be ruled out.

Pound (1.2544) continues trading in the range of 1.2350-1.2600 just as expected and no change in this range bound price action is seen for the next few sessions.

Aussie (0.7612) has been trading in the narrow range of 0.7600-0.7675 for the last 7-8 sessions but it is standing at crossroads now. Either an immediate bounce from 0.7600 levels is seen or the decline extends to 0.7530-00. Wait and watch.

Dollar Rupee (64.85) is trading absolutely flat in the NDF market this morning. Our target of 64.80 has been met but the chances of seeing 64.60 still on the cards. Immediate resistance comes at 64.95-65.00. It remains to be seen if 64.80-60 holds as expected or not.

INTEREST RATES

The UK yields are all mixed. The 5Yr (0.55%) has some room on the downside and could possibly test 0.50% while the 10YR (1.13%) and the 20Yr (1.64%) are testing near term supports and could bounce back immediately from current levels.

The German 10-2Yr (1.078%) has fallen sharply from resistance near 1.31% and has paused for now. But there could be some more fall towards 1% in the near term. The German yields by themselves are also falling and could continue to fall in the near term.

The Japan 5yr (-0.11%) is heading towards resistance just above current Levels and if that holds, it could come off in the near term towards -0.15%. the 10YR (0.07%) and the 30YR (0.84%) are also heading towards resistance and may come off in the near term.

The US 10-5Yr (0.47%) is rising and may head towards 0.48-0.49% in the coming sessions. The yields by themselves may rise from support levels in the near term.

GOLD – Loses Upside Steam, Vulnerable

GOLD - The commodity faces downside pressure after rejecting higher prices the past week. On the downside, support comes in at the 1,240.00 level where a break will turn attention to the 1,230.00 level. Further down, a cut through here will open the door for a move lower towards the 1,220.00 level. Below here if seen could trigger further downside pressure targeting the 1,210.00 level. Conversely, resistance resides at the 1,260.00 level where a break will aim at the 1,270.00 level. A turn above there will expose the 1,280.00 level. Further out, resistance stands at the 1,290.00 level. All in all, GOLD looks to strengthen further but with caution.

Some Monday Morning Aussie!

For me, with price still at resistance, at some stage this week we're definitely going to see the Aussie Dollar come into play to wanted to feature the charts to kick off the week.

Now we've spoken about these particular Aussie resistance levels on the blog before but added this obvious trend line that price is creeping along.

AUD/USD Daily:

But first up, the daily is all about the horizontal resistance zone. Touch after touch after touch and still price flirts. Make of that what you will.

You're either a trader that believes so long as we're under the level then it's a sell. Or you're looking to buy as each touch potentially weakens the resistance level.

AUD/USD 4 Hourly:

Zooming into the 4 hourly chart, this short term trend line support level can definitely be used to help make the decision.

Which way is it for you?

EURUSD: Bearish, Threatens Further Weakness

EURUSD: With the pair closing lower the past week, it now looks to weaken further as we enter a new week. Resistance comes in at 1.0700 level with a cut through here opening the door for more upside towards the 1.0750 level. Further up, resistance lies at the 1.0800 level where a break will expose the 1.0850 level. Its weekly RSI is bearish and pointing lower suggesting further weakness. Conversely, support lies at the 1.0600 level where a violation will aim at the 1.0550 level. A break of here will aim at the 1.0500 level. All in all, EURUSD faces further bear threats.