Sample Category Title

Eurozone retail sales fall -0.5%Q mom in Oct, EU down -0.3% mom

Eurozone retail sales volume declined by -0.5% mom in October, underperforming expectations of a -0.4% mom contraction. Breaking down the data, sales for food, drinks, and tobacco edged up 0.1% mom, while non-food products (excluding automotive fuel) slumped -0.9% mom, and automotive fuel sales in specialized stores dropped -0.3% mom.

Across the broader European Union, retail sales volume fell by -0.3% mom. Among member states, the sharpest monthly declines were seen in Belgium (-1.7%), Germany (-1.4%), and Denmark and Cyprus (both -1.1%). Conversely, Luxembourg led with a strong 2.4% increase, followed by Poland at 2.2% and Lithuania at 1.5%.

GBP/USD Continues its Rally: Third Day of Buying

The GBP/USD pair has risen to 1.2711, marking the third day of sustained buyer activity. This upward movement comes from comments from Bank of England Governor Andrew Bailey, who hinted at potential interest rate cuts in 2025 if the consumer price index (CPI) continues its downward trajectory.

In a recent interview, Governor Bailey discussed the possibility of a decisive easing in monetary policy, suggesting a total reduction of 100 basis points in 2025, which could bring the interest rate down to as low as 3.75% per annum. While this outlook is seen as positive, investors are currently more focused on the short term, with expectations set for the BoE's rate to remain unchanged in December 2024. Any substantial rate adjustments are anticipated to be implemented next year.

Governor Bailey also noted that UK inflation is declining more rapidly than anticipated, with current consumer prices nearly 1% below previous forecasts. This contrasts with official statistics, which recorded a CPI rise from 1.7% in September to 2.3% in October, suggesting that inflation pressures are not fully alleviated yet.

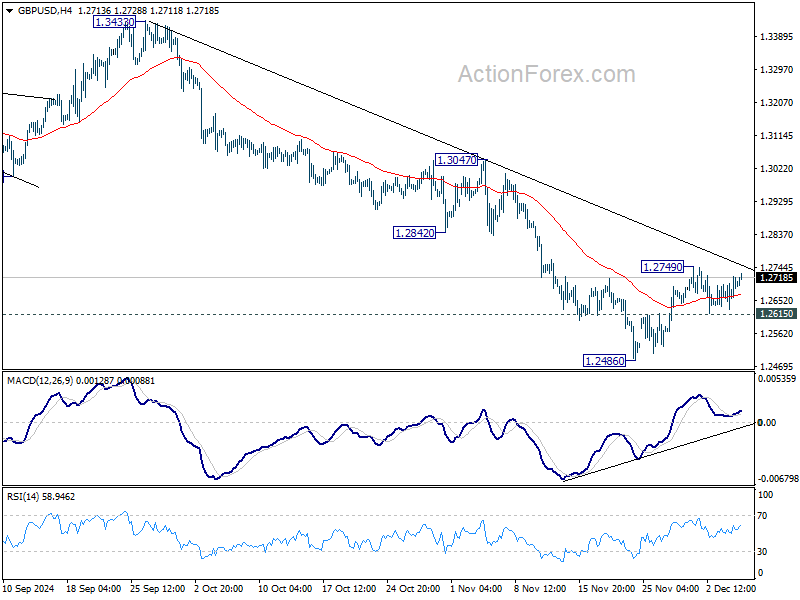

Technical analysis of GBP/USD

H4 chart: the GBP/USD is currently on an upward trend, targeting 1.2767. Once this level is reached, a retracement to 1.2628 is expected, testing it from above before potentially initiating another growth phase towards 1.2815, with prospects of extending to 1.2960. The MACD indicator supports this bullish scenario, with its signal line positioned above zero and trending upwards.

H1 chart: the pair has found support at 1.2628 and is building a growth structure towards 1.2767. Once achieving this level, a corrective phase to 1.2628 may ensue. This analysis is supported by the Stochastic oscillator, which shows the signal line moving upwards from above 50 towards 80, indicating continued upward momentum in the near term.

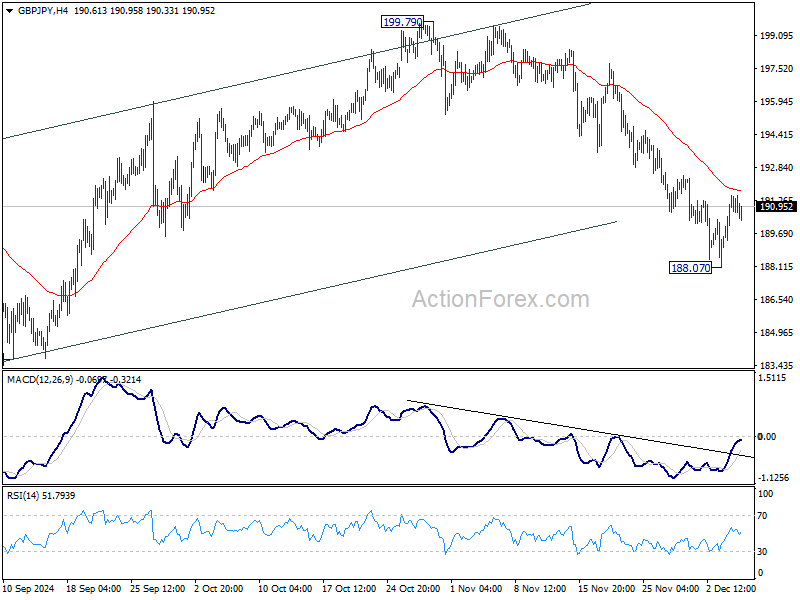

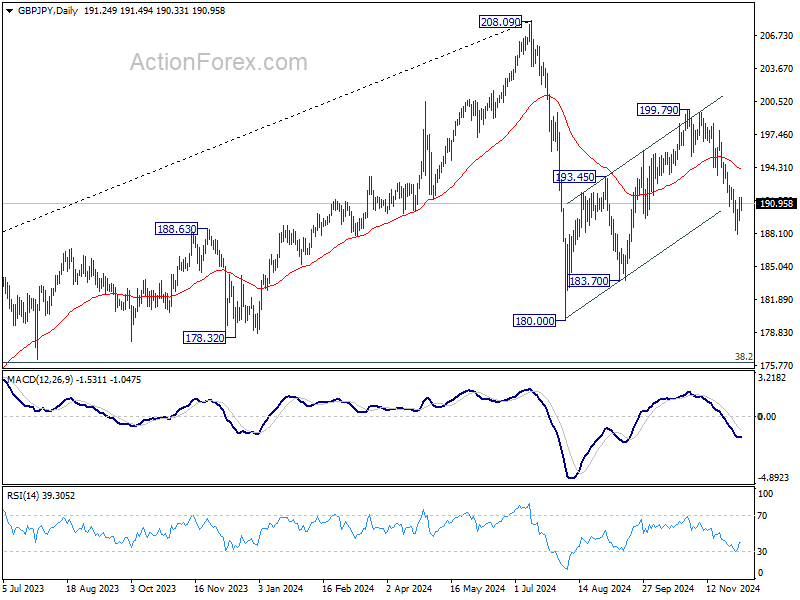

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.91; (P) 190.72; (R1) 192.08; More...

Intraday bias in GBP/JPY remains neutral for consolidations above 188.07 temporary low. Further decline is expected as long as 55 D EMA (now at 194.25) holds. On the downside, below 188.07 temporary low will resume the fall from 199.79 to 183.70 support. Firm break there will argue that whole decline from 208.09 is resuming, and target a test on 180.00 low next.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

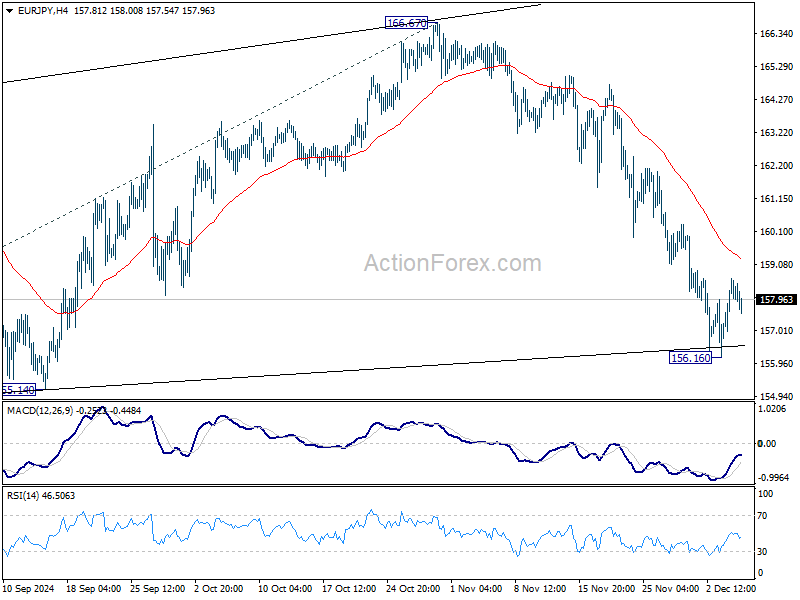

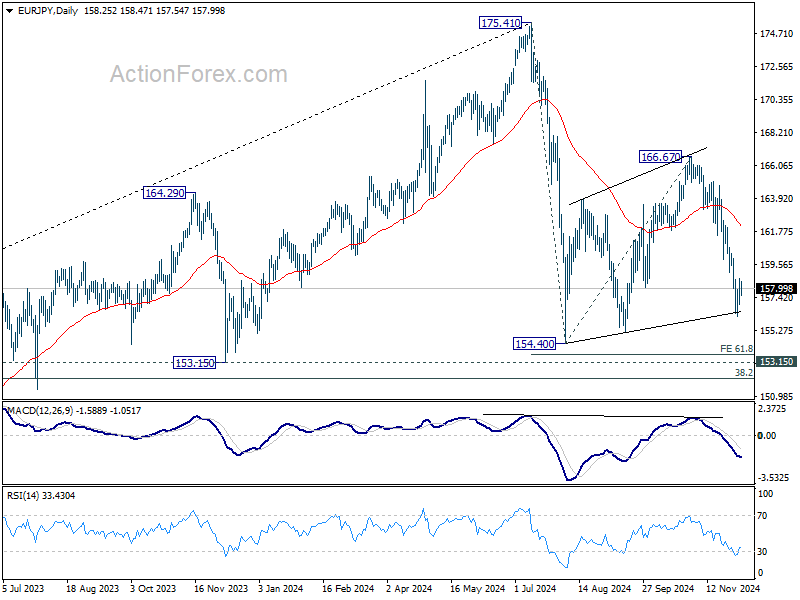

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.31; (P) 157.99; (R1) 158.99; More....

Intraday bias in EUR/JPY remains neutral for consolidations above 156.16 temporary low. Further decline is expected as long as 55 D EMA (now at 162.08) holds. On the downside, below 156.16 temporary low will resume the fall from 166.67 to 155.14 support first. Firm break there will raise the chance that whole decline from 175.41 is resuming, and target 154.40 low next.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

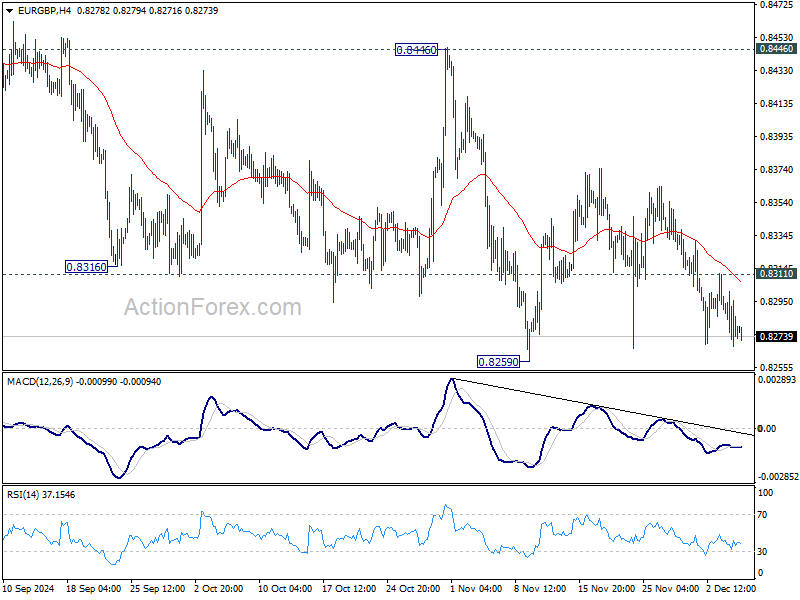

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8263; (P) 0.8282; (R1) 0.8296; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside, decisive break of 0.8259 will resume larger down trend to 0.8201 key support. On the upside, break of 0.8311 minor resistance will turn bias back to the upside for recovery. But still, outlook will stay bearish as long a 0.8446 resistance holds, and downside breakout is expected at a later stage.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

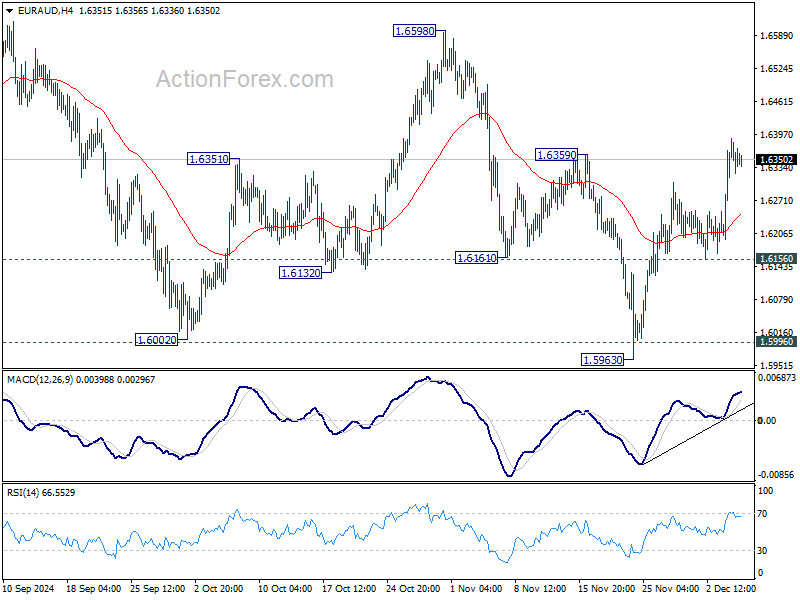

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6231; (P) 1.6312; (R1) 1.6426; More...

The break of 1.6359 resistance in EUR/AUD is tentatively taken as a the first sign of near term bullish reversal. Intraday bias now mildly on the upside for 1.6598 resistance. Firm break there will confirm successful defense of 1.5996 support and bring further rally. Nevertheless, break of 1.6156 support will turn bias back to the downside for 1.5996 again.

In the bigger picture, immediate focus is now on 1.5996 key support level. Sustained break there will argue that whole up trend from 1.4281 (2022 low) is already reversing. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction. Nevertheless, strong rebound from current level, followed by break of 1.6359 resistance, will keep medium term outlook neutral at worst.

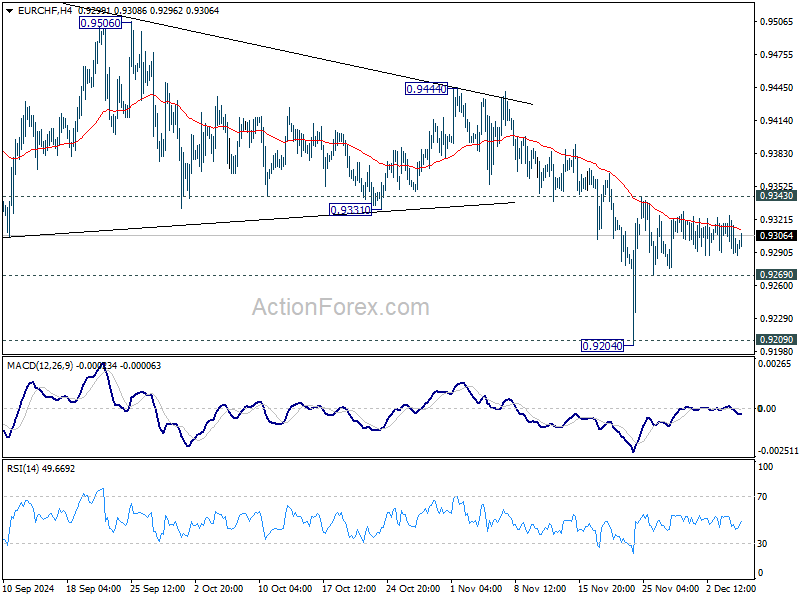

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9282; (P) 0.9304; (R1) 0.9318; More....

Intraday bias in EUR/CHF stays neutral for the moment. Further decline is in favor with 0.9343 resistance intact. On the downside, below 0.9269 minor support will bring retest of 0.9204/9 support zone. Decisive break there will confirm larger down trend resumption. Nevertheless, firm break of 0.9343 will now be a sign of near term bullish reversal, and target 0.9444 resistance for confirmation.

In the bigger picture, outlook will now stay bearish as long as 0.9444 resistance holds. Decisive break of 0.9209 low will resumed long term down trend to 61.8% projection of 0.9772 to 0.9209 from 0.9444 at 0.9096 next.

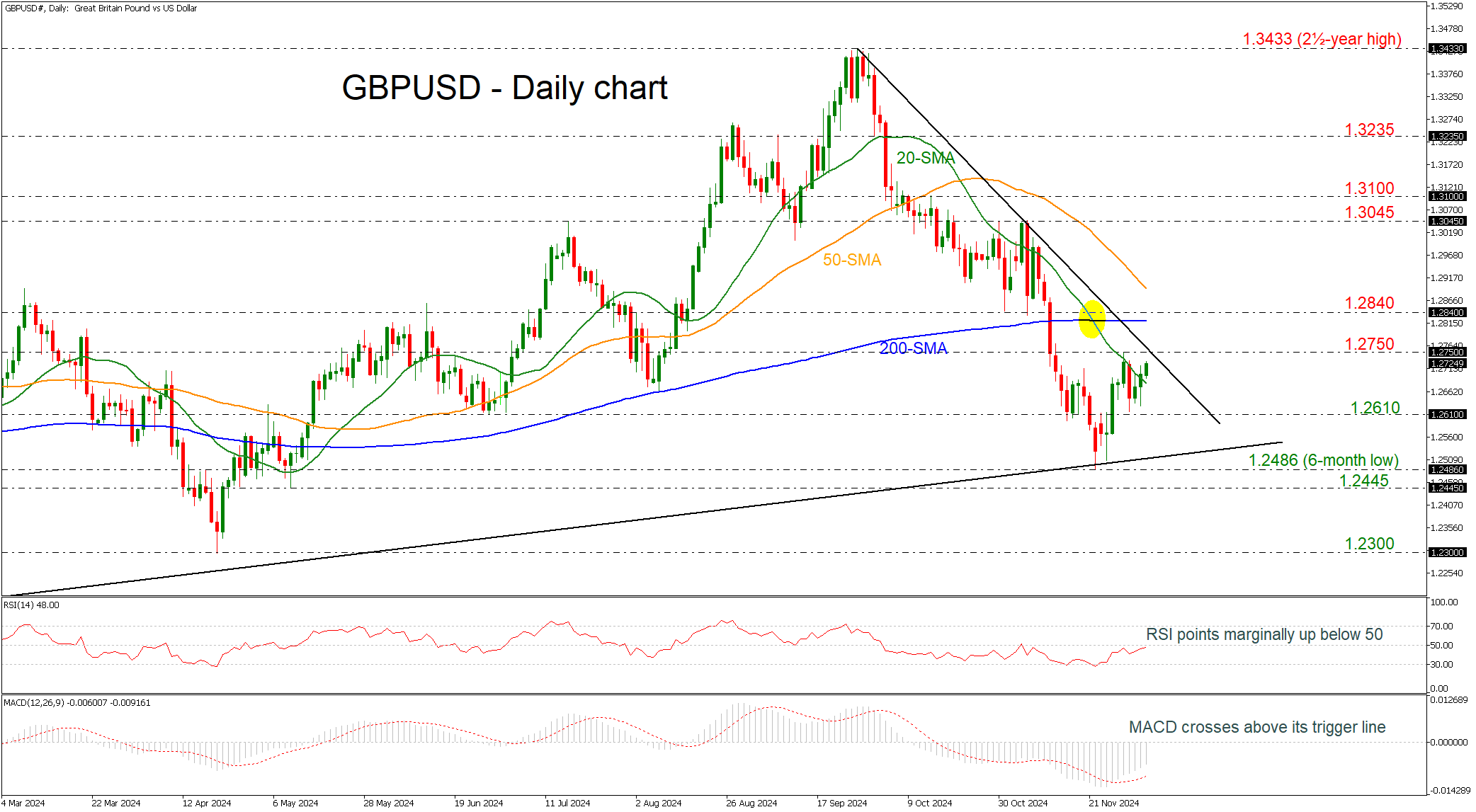

GBPUSD Shows Signs of Positive Momentum

- GBPUSD in bullish correction in short-term

- RSI and MACD head north

GBPUSD has been in a rising correction mode over the last couple of weeks after the bounce off the six-month low of 1.2486. The pair may revisit the 1.2750 barrier, which is holding near the short-term downtrend line. If the market successfully breaks this area, it may face a significant challenge at the flat 200-day simple moving average (SMA) at 1.2820, before encountering the 1.2840 resistance and the 50-day SMA around 1.2900.

However, if the price retreats below the 1.2610 support, then it may challenge the long-term ascending trend line at 1.2530 and the six-month bottom of 1.2486. Slightly lower, the 1.2445 support may pause the decline but the 1.2300 round number may be the next key turning point in the market.

According to technical oscillators, the RSI is ready to cross above the 50 level, and the MACD is strengthening its positive momentum above its trigger line. Both are indicating further increases in the market.

Overall, GBPUSD has shown a bullish tendency over the last one-and-a-half-year and any climbs beyond the 200-day SMA would also shift the short-term negative bias to a positive one.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0474; (P) 1.0509; (R1) 1.0546; More...

Intraday bias in EUR/USD stays neutral at this point. Outlook remains bearish with 1.0609 resistance intact. On the downside, break of 1.0330 will resume the fall from 1.1213. Also, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication. Nevertheless, firm break of 1.0609 will turn bias back to the upside for 1.0760 support turned resistance first.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

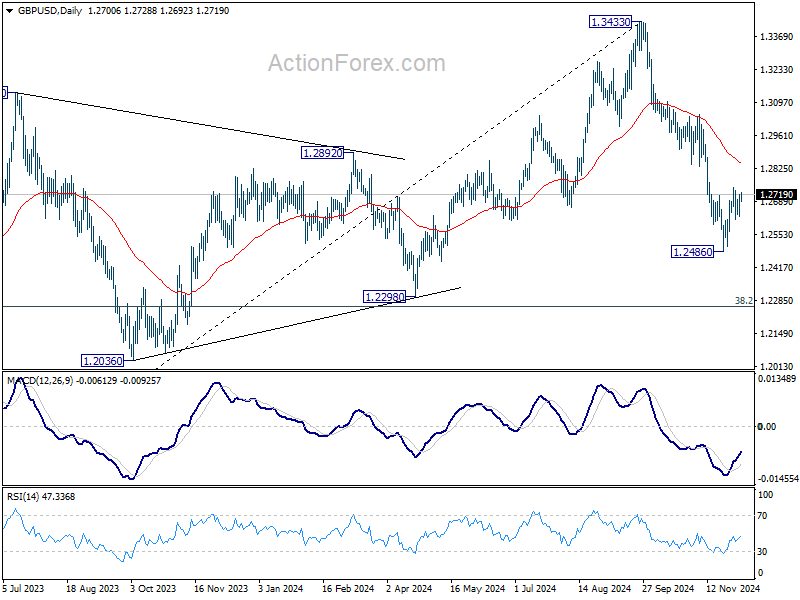

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2646; (P) 1.2684; (R1) 1.2737; More...

Intraday bias in GBP/USD remains neutral for the moment. Recovery from 2.2486 could extend through 1.2749. But outlook will stay bearish as long as 55 D EMA (now at 1.2853) holds. Below 1.2615 minor support will turn intraday bias back to the downside for retesting 1.2486. Break there will resume whole fall from 1.3433.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2867) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.