Sample Category Title

USD/JPY Faces Challenges as NFP Report Looms Large

Key Highlights

- USD/JPY is consolidating losses above the 148.65 support zone.

- A key bearish trend line is forming with resistance at 151.40 on the 4-hour chart.

- EUR/USD could recover if it clears the 1.0620 resistance zone.

- Bitcoin breached the milestone level of $100,000 and traded to a new all-time high.

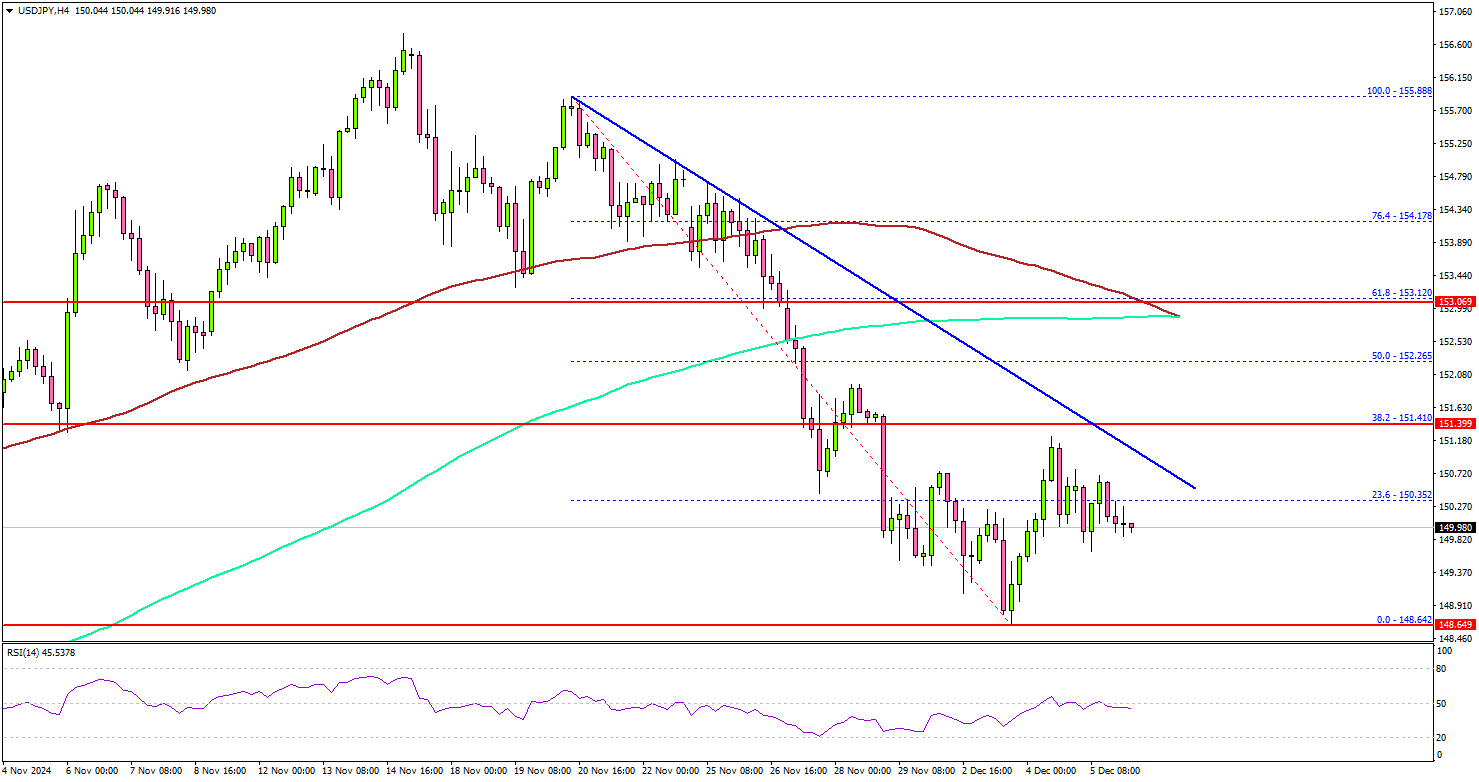

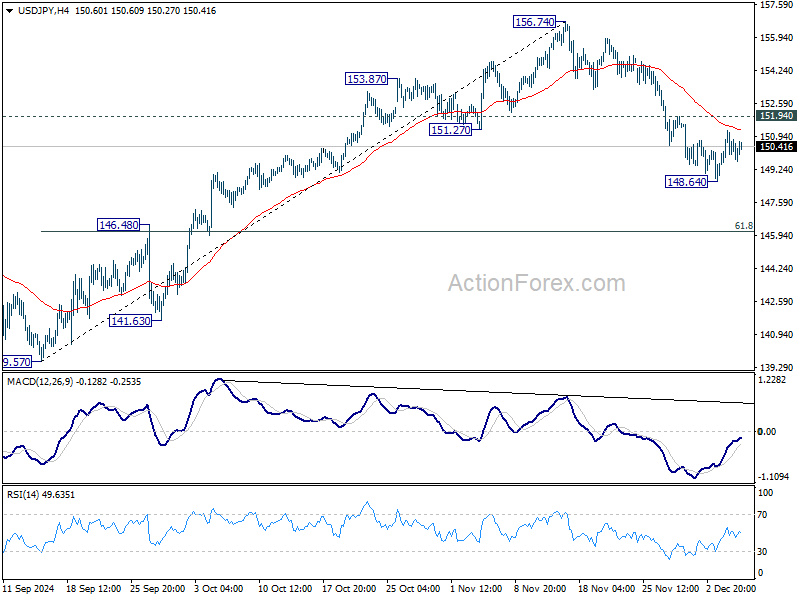

USD/JPY Technical Analysis

The US Dollar formed a base and recently started a recovery wave from 148.65 against the Japanese Yen. However, USD/JPY faces many hurdles as it approaches the US NFP report.

Looking at the 4-hour chart, the pair surpassed the 23.6% Fib retracement level of the downward move from the 155.88 swing high to the 148.64 low. The pair recovered above the 150.00 resistance level, but it faces many hurdles and remains well below the 100 simple moving average (red, 4-hour).

On the upside, the pair could face resistance near the 151.50 level. There is also a key bearish trend line forming with resistance at 151.40. The first major resistance is near the 152.20 level.

A close above the 152.50 level could set the tone for another increase. The next major resistance could be the 200 simple moving average (green, 4-hour) at 153.10, above which the price could climb higher toward the 154.00 resistance.

On the downside, immediate support sits near the 149.50 level. The next key support sits near the 148.65 level. Any more losses could send the pair toward the 146.50 level.

Looking at Bitcoin, the bulls pumped the price above the $100,000 resistance zone and the price traded to a new record high above $104,000 on TitanFX.

Upcoming Economic Events:

- Euro Zone Gross Domestic Product for Q3 2024 (QoQ) - Forecast 0.2%, versus 0.2% previous.

- Euro Zone Gross Domestic Product for Q3 2024 (YoY) - Forecast 0.9%, versus 0.9% previous.

- US nonfarm payrolls April 2024 – Forecast 200K, versus 12K previous.

- US Unemployment Rate for Nov 2024 - Forecast 4.2%, versus 4.1% previous.

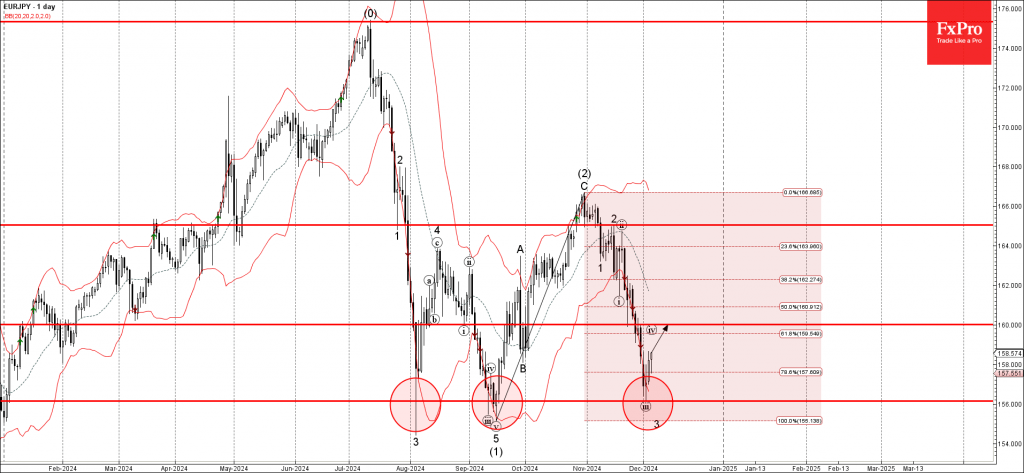

EURJPY Wave Analysis

- EURJPY reversed from key support level 156.00

- Likely to rise to resistance level 160.00

EURJPY currency pair recently reversed up from the key support level 156.00 (which has been reversing the pair from the start of August) standing close to the lower daily Bollinger Band.

The upward reversal from the support level 156.00 created the daily Japanese candlesticks reversal pattern Morning Star Doji.

Given the strength of the support level 156.00, EURJPY currency pair can be expected to rise toward the next resistance level 160.00 (target for the completion of the active wave iv).

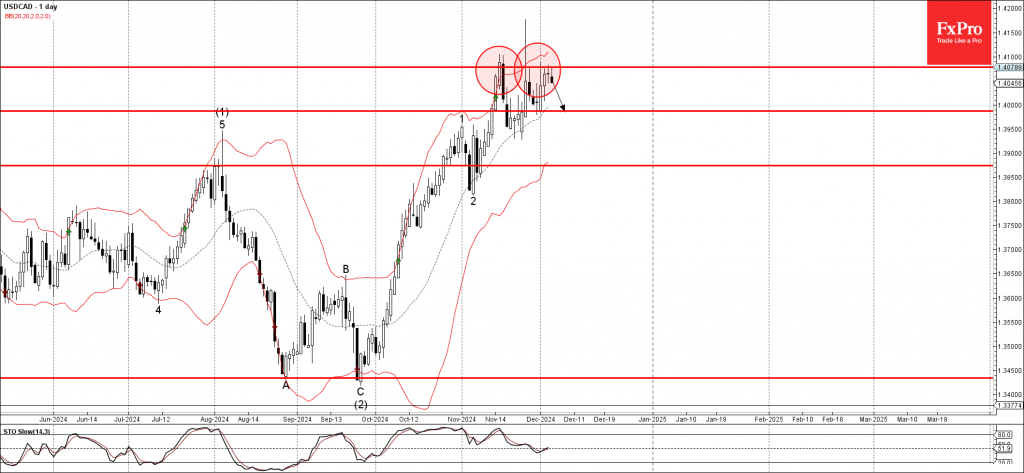

USDCAD Wave Analysis

- USDCAD reversed from pivotal resistance level 1.4080

- Likely to fall to support level 1.3990

USDCAD currency pair today reversed down from the pivotal resistance level 1.4080 (which has been reversing the pair from the start of November) standing near the upper daily Bollinger Band.

The latest downward reversal from resistance level 1.4080 is the 5th consecutive failed attempt to break above this level – which signals its strength.

USDCAD currency pair can be expected to fall toward the next support level 1.3990 (low of the previous minor correction from the end of last month).

November CPI Preview: Barely Budging

Summary

Stalling progress on the inflation fight should be evident in the November Consumer Price Index. We expect headline CPI to advance 0.25% over the month and 2.7% over the past year. The core index should similarly rise around 0.25%, which would keep the 12-month change stuck in the narrow range of 3.2%-3.3% for a sixth straight month. While some key sources of inflationary pressure, such as an overheated labor market, continue to dissipate, new headwinds to disinflation have emerged (e.g., the potential for tariffs and tax cuts) that make the final leg of inflation's journey back to the Fed's 2% target look increasingly difficult.

A Bump That Looks Increasingly Long

The stubborn picture of inflation that has emerged over the past few months is unlikely to be altered by the November CPI report. We look for headline inflation to advance 0.25%, which would mark a similar rise to October and push up the 12-month change in prices to 2.7%. After receiving some meaningful respite at the pump since the spring, gasoline prices headed a bit higher in November on a seasonally adjusted basis (+0.2% by our estimates). Meantime, the strength in the producer price index for finished consumer foods the past few months points to CPI food inflation remaining firm. After easing in October, we look for price growth for both food at home and away from home to partially rebound in November, resulting in total food inflation being up 2.2% year-over-year.

Excluding food and energy, inflation is likely to look similarly sticky. We expect the core index to also advance 0.25% in November. This would mark only marginal improvement compared to the past three months' average increase (0.29%) or the average for the year (0.27%) and leave the three-month annualized rate at 3.4%.

The two-month streak of price increases for core goods is likely to extend to three in another sign that goods deflation is subsiding. Used autos are likely to be the primary driver of another positive print for core goods in November, but remaining core goods prices were likely little changed as seasonal adjustment factors are increasingly positioned for holiday-season discounts to begin in November.

Services inflation should at least ease modestly relative to its recent trend. We estimate core services prices rose 0.32% compared to an average rise of 0.37% the past three months. Shelter prices should come in a little softer than October as the downward trend in owners' equivalent rent resumes. Lower jet fuel prices in recent months should also bring some relief to airline fares. We expect to see a pickup, however, in categories like motor vehicle insurance and communications due to some reversion to the recent trend, limiting the overall easing in services prices in November.

While inflation has proved stubborn the past few months, it is not as if there have been no signs of progress. The annual change in shelter inflation has slowed to 5.1% from 6.9% this time last year. With the November report, it should drop below 5% for the first time in two and a half years. Meantime, after bubbling up over the winter, the 12-month change in the CPI super core is back on the downswing. Goods prices are no longer falling as rapidly as they were a year ago, but the rate of price changes has at least returned to its pre-pandemic pace.

That said, the final leg of inflation’s journey back to the Fed’s target is looking tougher and tougher. Some key sources of inflationary pressure, most notably labor costs, continue to dissipate, helped by growing signs of a pickup in productivity growth. Yet new headwinds to disinflation have emerged, including the potential for higher tariffs and lower tax rates, which we have incorporated into our forecast. Overall, we expect the fight to get inflation back to the Fed’s 2% target when measured by the core PCE deflator to drag on through our 2026 forecast horizon, with negligible inroads made in the year ahead.

2025 International Economic Outlook

A New Horizon: The Economic Outlook in a New Leadership and Policy Era

Key Themes

- With Donald Trump elected as president with unified congressional support, economic policy in the United States is set to change rather dramatically. President Trump campaigned on making radical adjustments to U.S. trade policy, specifically reverting to tariffs as a means to balance trade deficits and extract concessions from key trading partners. While clarity on tariff policy is limited at this point, we feel comfortable assuming President-elect Trump will impose levies early in his term. To that point, underlying our 2025 global economic, central bank and FX forecasts is an assumption that President-elect Trump imposes a 5% tariff on all U.S. imports and a 30% tariff on all Chinese exports into the U.S. starting in H2-2025.

- Trump 2.0 tariffs are likely to disrupt, not upend, the U.S. economy. Economic expansion is still likely, albeit at a slower pace, while inflation could remain above the Fed's target as consumers at least partly bear the cost of tariffs. Overall disinflation and a less robust jobs market relative to a few years ago suggest the Federal Reserve is likely to continue lowering interest rates; however, resilient economic trends combined with somewhat firmer inflation should see the FOMC ease monetary policy more gradually going forward. Given our implicit tariff assumptions, we now believe the Federal Reserve will achieve a terminal target range for the fed funds rate of 3.50%-3.75%.

- Exposure to U.S. tariffs is likely to create diverging paths for economic growth for countries around the world. Emerging economies with strong trade linkages to the United States could see the most acute decelerations. China and Mexico are significantly exposed, and while China has offsetting policy mechanisms it can deploy, Mexico has limited monetary and fiscal space to respond to an external trade shock. Based on the growth, inflation and market reaction to tariffs, central banks could adjust monetary policy settings at different speeds, and in select cases, different directions. In particular, we expect the European Central Bank to ease quicker than previously envisaged, while institutions in the emerging markets could operate with more caution, or restart tightening cycles.

- Even following its post-election rally, we continue to believe the U.S. dollar can strengthen going forward. A less dovish Fed, more dovish major central banks internationally, trouble in China and uncertainty around U.S. economic policy should create an environment where the U.S. dollar performs particularly well. We believe those same dynamics will place significant depreciation pressure on emerging market currencies, with “high beta” currencies in Latin America and EMEA underperforming. Idiosyncratic factors can also contribute to particular underperformance from select developing currencies. We expect the euro to fall below parity relative to the U.S. dollar. Currencies associated with more closed economies—such as the Indian rupee—or linked to hawkish central banks—such as the Japanese yen and Australian dollar—can be more resilient in 2025.

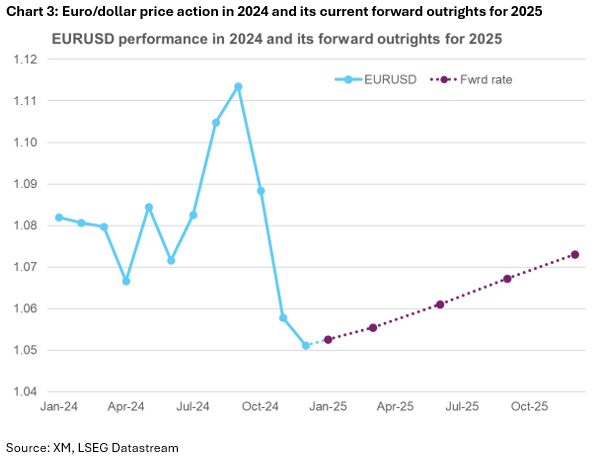

Year Ahead – Euro Might Finally Outperform the Pound in 2025

- Trump’s agenda and Fed to set the tone for 2025

- Eurozone politics, a dovish ECB and weak growth in the spotlight

- The UK is in better shape, but the budget could prove a major headwind

- Pound strength may persist in early 2025, the euro might find its moment later on

If the stars align, 2025 could be a dream year for the euro

It has been a year to forget for the euro area. Political crises in both France and Germany, continued weak growth - with Germany expected to contract for a second consecutive year - and an active conflict near its eastern borders have all impacted economic momentum. As a result, the euro weakened considerably against both the dollar and the pound.

Going into 2025, the outlook remains clouded. While the world adjusts to Trump’s second term and the Fed’s monetary policy stance, the euro area is leaderless. The new German Chancellor is expected to take office by mid-March, and French President Macron is under constant pressure following the June European election disaster.

Aggressive ECB easing to continue

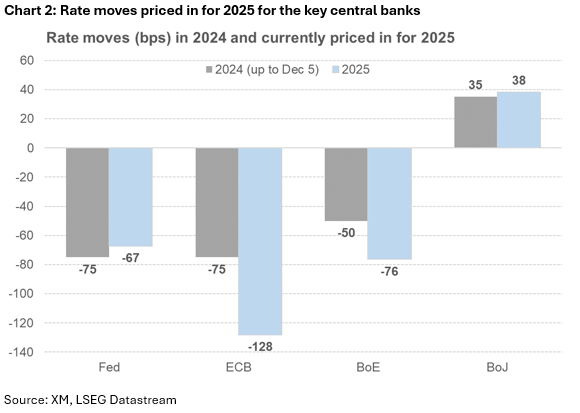

Meanwhile, the European Central Bank (ECB) is expected to further ease its monetary policy stance by around 130bps in 2025, thus decisively contributing to a potential growth pick up. However, the ECB cannot turn the current situation around on its own. Expansionary fiscal policy could be extremely effective at this stage, but, with the COVID pandemic in the rearview mirror, euro area governments have returned to a stricter fiscal doctrine, removing one of the key tailwinds of the economy.

Most market analysts are fairly pessimistic about the euro's performance in 2025. However, there is an avenue for a brighter performance in 2025 if the euro area manages to return to more respectable growth rates, boosted by consistent wage growth and increased consumer spending, outperforming both the US and UK.

Three external factors could determine euro’s performance

This scenario depends heavily on three factors: (a) Trump’s trade agenda, (b) the Ukraine-Russia conflict, and (c) China’s growth pickup. Should any of these factors prove unfavourable for the euro area, then the euro will most likely remain under pressure during 2025.

Having said that, should global economic performance prove below par in 2025, the ECB’s decisive stance and front-loading strategy could pay some dividends at a time when other major central banks also rush to support their economies, thus inadvertently weakening their currencies.

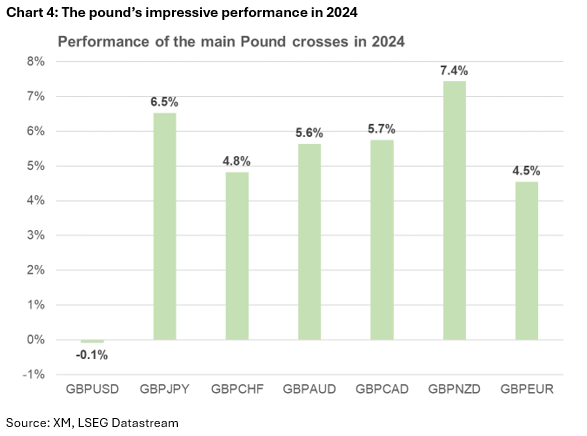

The pound’s good fortunes could reverse in the latter part of 2025

The pound exhibited solid strength during 2024, outperforming the euro for a second consecutive year and barely underperforming against the mighty dollar. The UK Labour party’s comfortable victory in the July 2024 general election and the measured dovish strategy by the Bank of England (BoE) contributed to the pound’s performance. However, both events could come back to haunt the pound during 2025.

While the world prepares for Trump’s second tenure in the White House, the UK is expected to escape relatively unscathed from the newly imposed trade tariffs. However, while the UK might be less affected from a potential deterioration in global trade due to its dominant services sector, the eurozone's anemic growth means the UK's economic outlook is not exactly rosy.

The UK budget remains a key unknown for 2025

Domestically, the impact of the 2025 budget is still uncertain. There are increasing concerns that the new tax measures, particularly the rise in employer’s national insurance, could prove counterproductive, hitting both employment and consumption, especially if the government insists on fully implementing these measures. However, there is a non-negligible possibility of amendments if PM Starmer succumbs to pressure from various industry groups, thus easing the overall impact. Meanwhile, the housing sector might be preparing for brighter days ahead, boosting consumer sentiment.

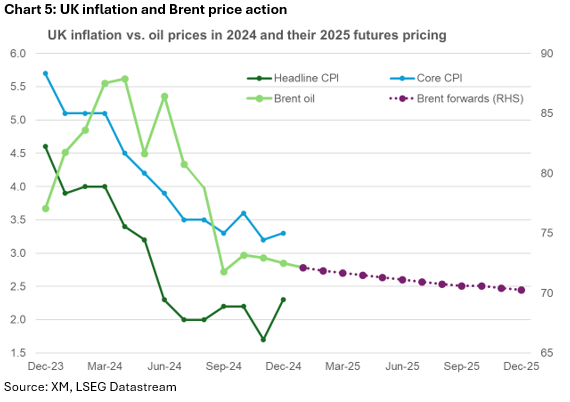

Amidst this environment, the BoE is forecast to continue supporting growth and consumer spending with further rate cuts. The market is currently pricing in 75bps of rate cuts, far less than the 130bps of easing expected by the ECB, which is surprising considering the BoE’s dovish pedigree. Having said that, another trade war could unsettle the BoE’s strategy, especially if core inflation fails to record a sizeable downward trend during 2025.

Pound’s strength could linger in early 2025

Putting everything together, the pound may experience a strong start to the year as the rest of the world scrambles to adjust to Trump’s “America First” agenda. However, this outperformance could moderate later in 2025 if the budget has a damaging effect on consumption, and the world divides into trading blocks, substantially hitting global growth momentum.

Sunset Market Commentary

Markets

Very few market-moving data in the US and EMU today. US markets are counting down to tomorrow’s US payrolls. This report, together with the US November CPI data (to be released on Dec 11), will provide concluding data evidence for the Dec 18 Fed policy meeting. US markets still only discount about 75% of a 25 bps cut, which we still see as the most likely scenario. Even so, US yields in technical trading add between 3.2 (2-y) and 1.5 bps (30-y) even as jobless claims printed slightly higher (worse) than expected (224k from 215k). German yields also add between 6.5 bps (5-y) and 2.0 bps (30-y). The rise gained some momentum on headlines from French RN Marine Le Pen as she said in an interview with Bloomberg that a budget was still possible if Macron and/or the next PM eases the stance on the debt path. This also triggered further intraday euro gains, with EUR/USD currently changing hands near 1.057. First short-term resistance is coming in at 1.0597/1.0610. EMU equities gain modestly (EuroStoxx50 + 0.5%). The S&P 500 is holding at record levels (little changed after open).

Sterling today is holding strong against the dollar (Cable 1.274) but meets resistance against the euro after recent rally (EUR/GBP 0.8785). The Monthly Decision Maker Panel survey of the Bank of England shows that UK CFO’s estimate year ahead own price inflation to be 3.7%, 0.2% higher compared to the previous survey. Expected year ahead wage growth was seen at 4.0% holding near its recent average. However, on a new question regarding the firms’ response to the increase in the employer National Insurance contribution announced in the budget, 54% of firms expects to raise prices and a similar group sees lower employment. 59% sees lower profit margins and 38% say they expects to pay lower wages than they otherwise would have done. This probably isn’t what the government wants to see, but also doesn’t make help the BoE to step up the pace of easing.

CE currencies (especially the forint and to a lesser extent the zloty) earlier this month face quite an uphill battle, but this week finally enjoyed some breathing space. This is partially due to the global market context, but domestic regional factors are also in play. On the global scene, the European risk-off eased at least temporarily. US interest rates are capped for now as the Fed will likely continue a process of gradual (25 bps) easing on Dec 18. A pause in the dollar rally also removed some pressure from regional currencies. At the same time, the Hungarian (MNB), Czech (CNB) and Polish central bank are in/heading to a pauze in their easing cycle. This for sure won’t be enough to shield local FX in a context of heightened risk-off, but helps in the current lower volatility intermezzo. At EUR/PLN 4.262, the zloty is closing in on the strongest levels against the euro since end September. At the press conference after yesterday’s NBP decision, governor Glapinski indicated that the debate on a rate cut might be delayed to October 2025, as Polish CPI might spike again in late 2025. The Czech koruna yesterday develop a similar pattern and today holds is gains (EUR/CZK 25.14). CNB governor Michl rather unambiguously closed the door for a December rate cut as wages continue to rise faster than expected. The forint end last week touched weakest levels since December 2022 (EUR/HUF 415 area) but currently also tries a (short-term?) reversal (EUR/HUF 411.9 currently).

News & Views

Swedish inflation accelerated slightly less than expected in November, by 0.3% M/M (from 0.2%) for the headline reading and by 0.5% M/M (from 0.4%) for the CPIF-gauge (using a fixed rate) preferred by the Swedish Riksbank. In annual terms, overall CPI stabilized at 1.6% with the CPIF measure rising from 1.5% to 1.9%, the highest level since May but remaining below the Swedish Riksbank 2% inflation target ever since. More detailed information and definitive figures will be available on December 12. Yesterday, a private survey by Prospera on behalf of the Riksbank showed consumer inflation expectations 1y, 2y and 5y ahead broadly unchanged compared with September: CPIF 1.7%-1.9%-2% from 1.7%-1.8%-2%. Inflation numbers won’t derail the central bank from implementing another rate cut at their final policy meeting of the year, albeit a smaller (25 bps) one than in November. The Swedish krone today rebounds off first technical resistance at EUR/SEK 11.49.

OPEC+ pushed back an increase in oil production planned for January by three months until the end of March. The full amount will be returned over a period of 18 months instead of the previously indicated 12 months. It’s the same gradual rollback of 2.2mn b/day of voluntary curbs which had already been delayed twice. Oil prices traded volatile but are unchanged in the end (Brent crude $72.5/b) given that the delay was broadly expected.

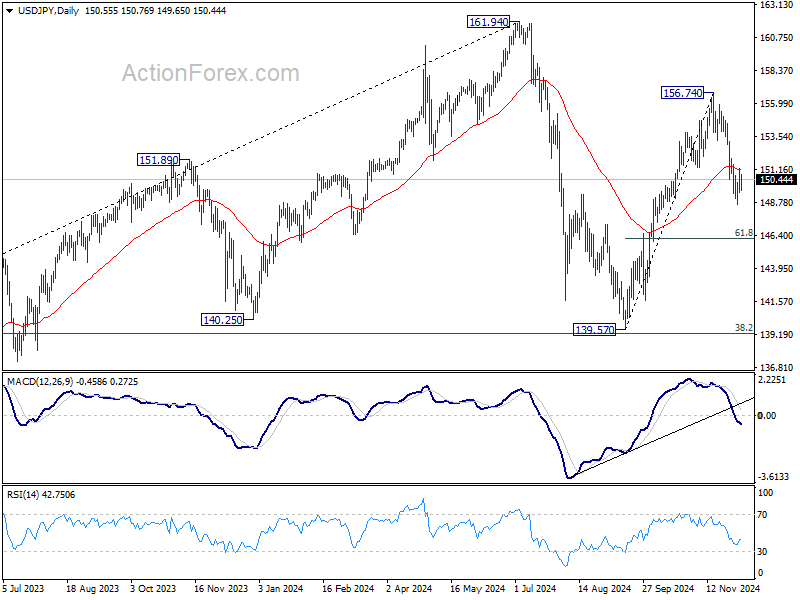

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.68; (P) 150.46; (R1) 151.39; More...

Intraday bias in USD/JPY remains neutral and more consolidations could be seen above 148.64. On the downside, break of 148.64 will strengthen the case that rise from 139.57 has already completed at 156.754. Deeper fall should then be seen to 61.8% retracement of 139.57 to 156.74 at 146.12 next. Nevertheless, firm break of 151.94 resistance will revive near term bullishness and bring retest of 156.74 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

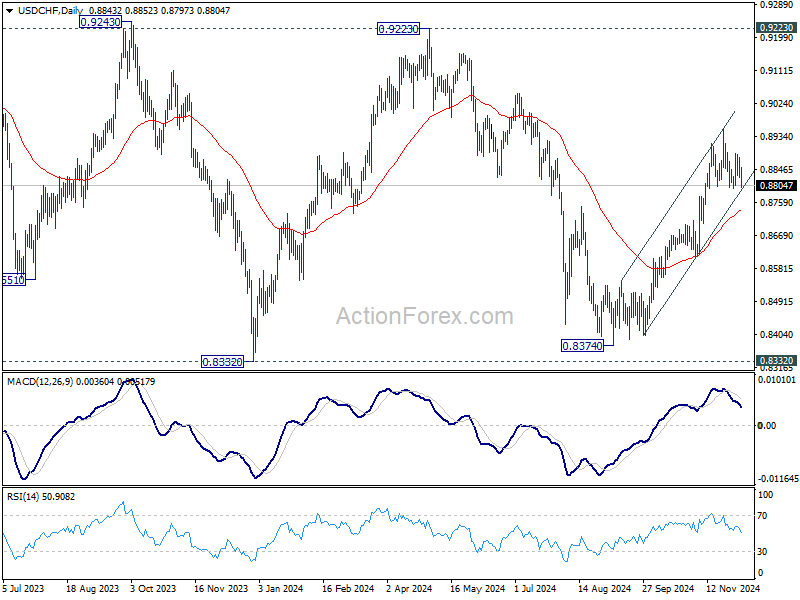

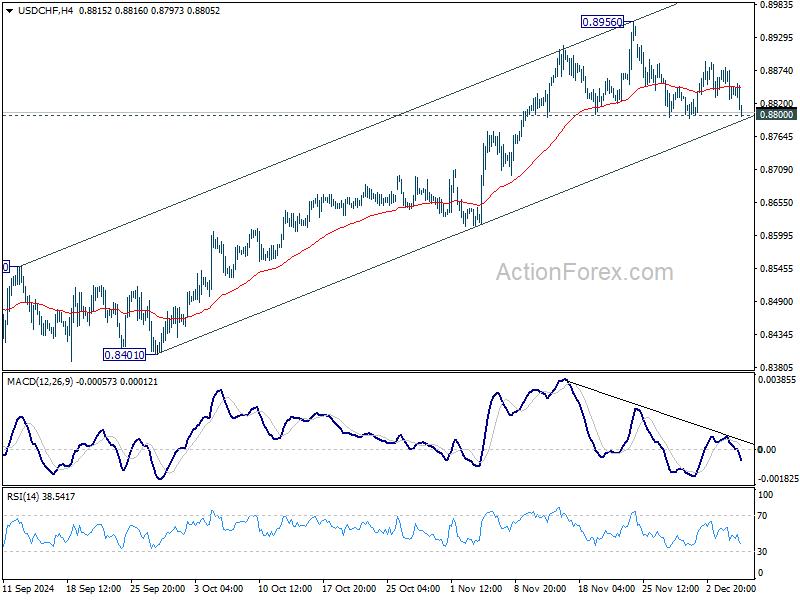

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8821; (P) 0.8851; (R1) 0.8874; More…

Immediate focus is now on 0.8800 support in USD/CHF with today's decline. Decisive break there will confirm short term topping at 08956. Intraday bias will be turned back to the downside for 55 D EMA (now at 0.8736). On the upside, break of 0.8956 will resume the rally from 0.8374, and target 0.9223 key resistance next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.