Sample Category Title

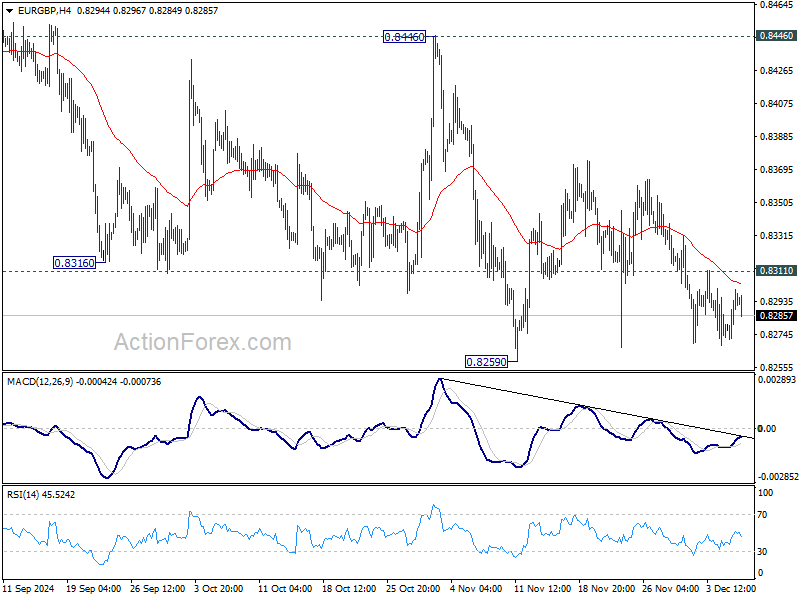

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8274; (P) 0.8287; (R1) 0.8311; More...

EUR/GBP is still bounded in range trading above 0.8259 support and intraday bias stays neutral. On the downside, decisive break of 0.8259 will resume larger down trend to 0.8201 key support. On the upside, break of 0.8311 minor resistance will turn bias back to the upside for recovery. But still, outlook will stay bearish as long a 0.8446 resistance holds, and downside breakout is expected at a later stage.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

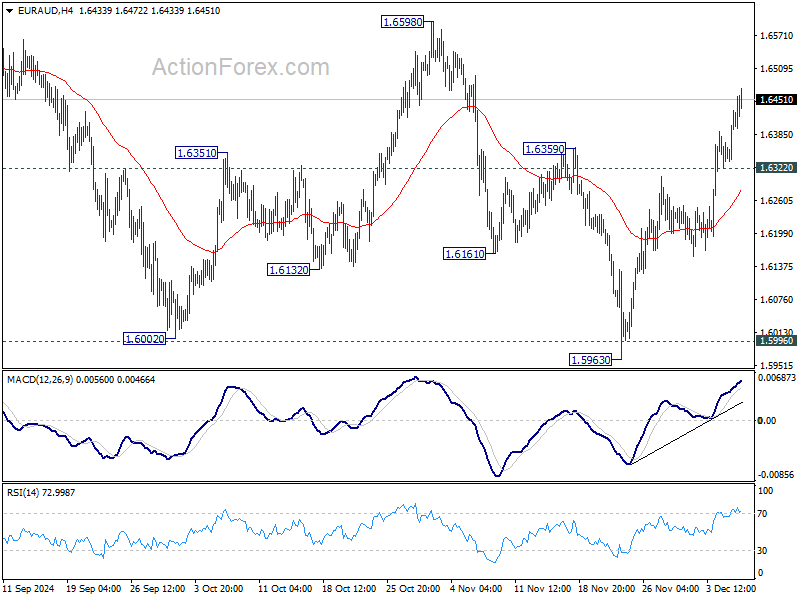

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6351; (P) 1.6392; (R1) 1.6448; More...

Intraday bias in EUR/AUD remains on the upside for the moment. Fall from 1.7180 could have completed at 1.5963, after defending 1.5996 key support. Further rise should be seen to 1.6598 resistance first. Firm break there will strengthen this bullish case and target a retest on 1.7180 high. Nevertheless, break of 1.6156 support will turn bias back to the downside for 1.5996 again.

In the bigger picture, immediate focus is now on 1.5996 key support level. Sustained break there will argue that whole up trend from 1.4281 (2022 low) is already reversing. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction. Nevertheless, strong rebound from current level, followed by break of 1.6359 resistance, will keep medium term outlook neutral at worst.

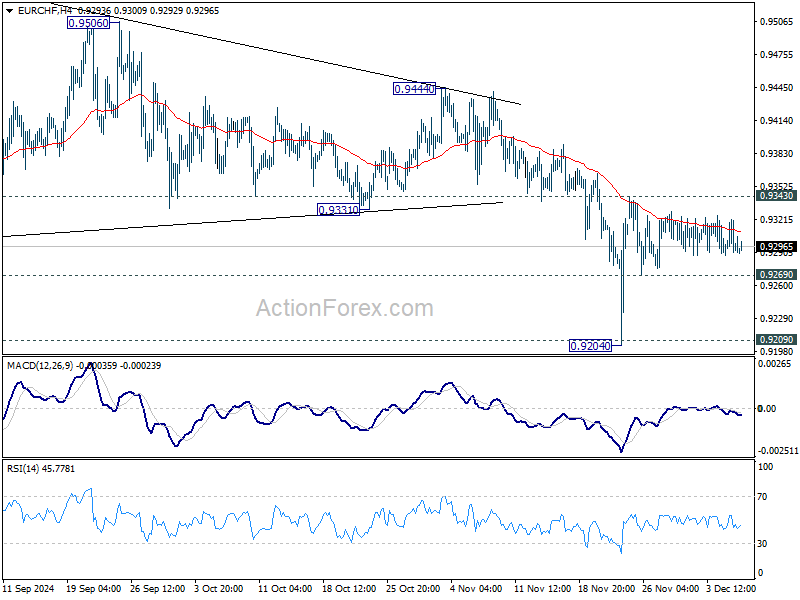

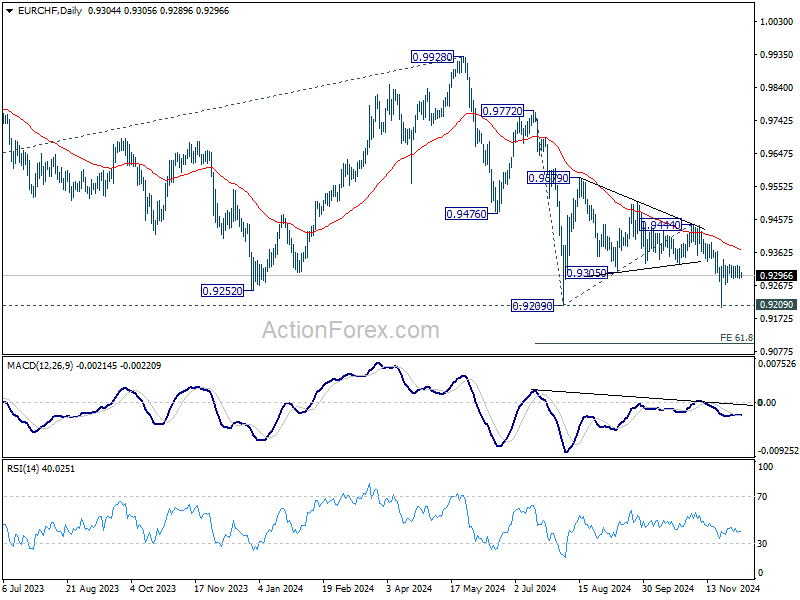

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9286; (P) 0.9305; (R1) 0.9319; More....

EUR/CHF is still bounded in sideway trading and intraday bias stays neutral. Further decline is in favor with 0.9343 resistance intact. On the downside, below 0.9269 minor support will bring retest of 0.9204/9 support zone. Decisive break there will confirm larger down trend resumption. Nevertheless, firm break of 0.9343 will now be a sign of near term bullish reversal, and target 0.9444 resistance for confirmation.

In the bigger picture, outlook will now stay bearish as long as 0.9444 resistance holds. Decisive break of 0.9209 low will resumed long term down trend to 61.8% projection of 0.9772 to 0.9209 from 0.9444 at 0.9096 next.

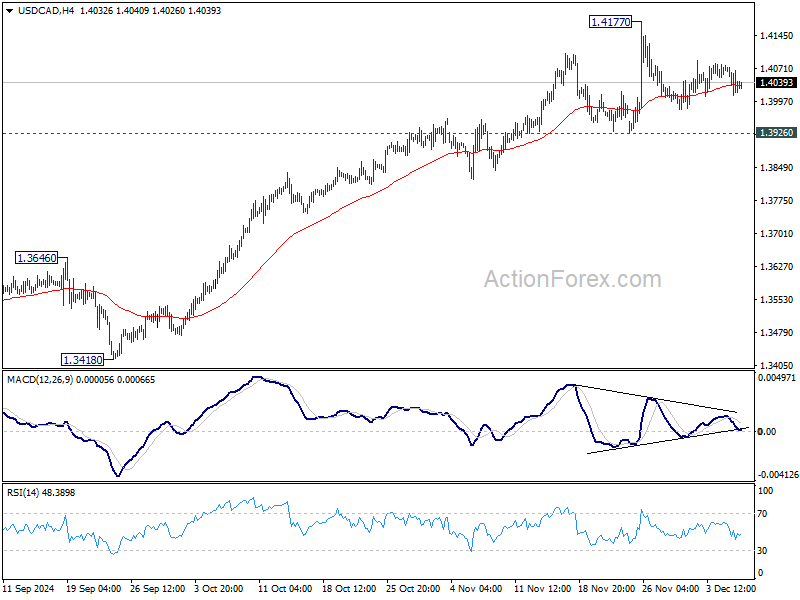

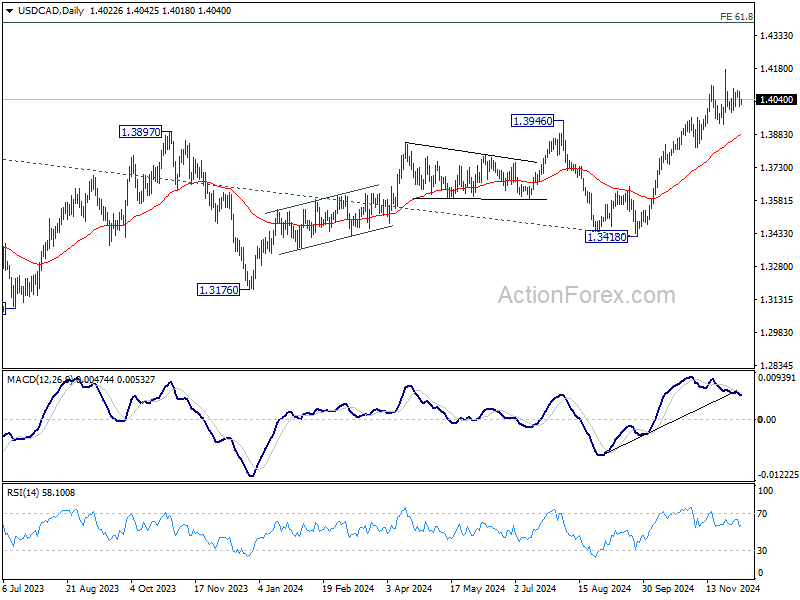

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3996; (P) 1.4039; (R1) 1.4068; More...

No change in USD/CAD's outlook as consolidation continues below 1.4177. Intraday bias remains neutral and further rally is expected with 1.3930 support intact. On the upside, firm break of 1.4177 will resume larger up trend towards 1.4391 projection level. However, break of 1.3926 will turn bias to the downside for deeper pullback to 55 D EMA (now at 1.3879).

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

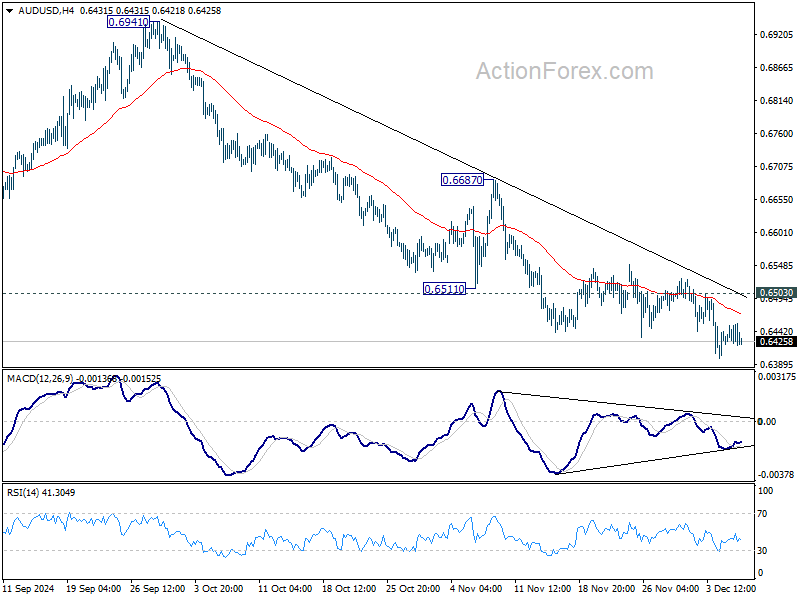

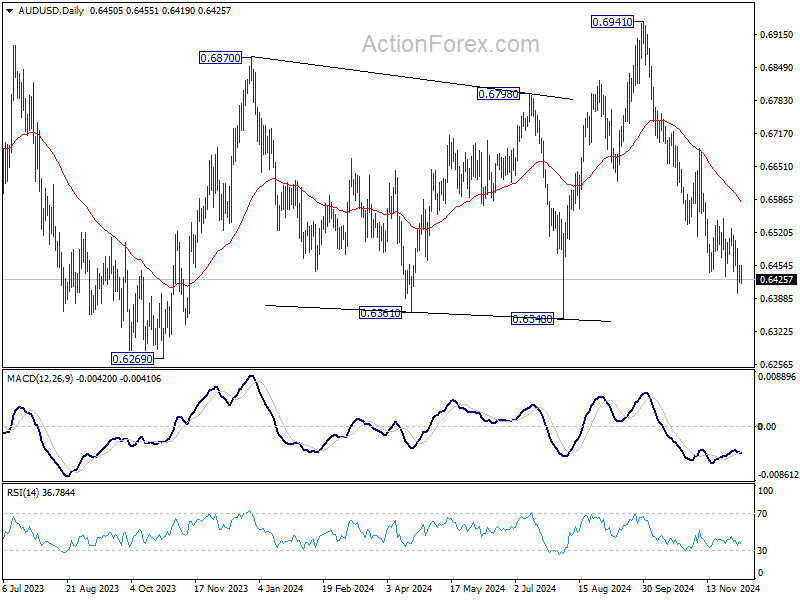

AUD/USD Daily Report

Daily Pivots: (S1) 0.6432; (P) 0.6443; (R1) 0.6465; More...

AUD/USD's fall from 0.6941 is still in progress and intraday bias stays on the downside for 0.6348 support. Break there will target 0.6269 low next. Considering bullish convergence condition in 4H MACD, break of 0.6503 resistance will indicate short term bottoming, and turn bias to the upside for rebound to 55 D MA (now at 0.6580).

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

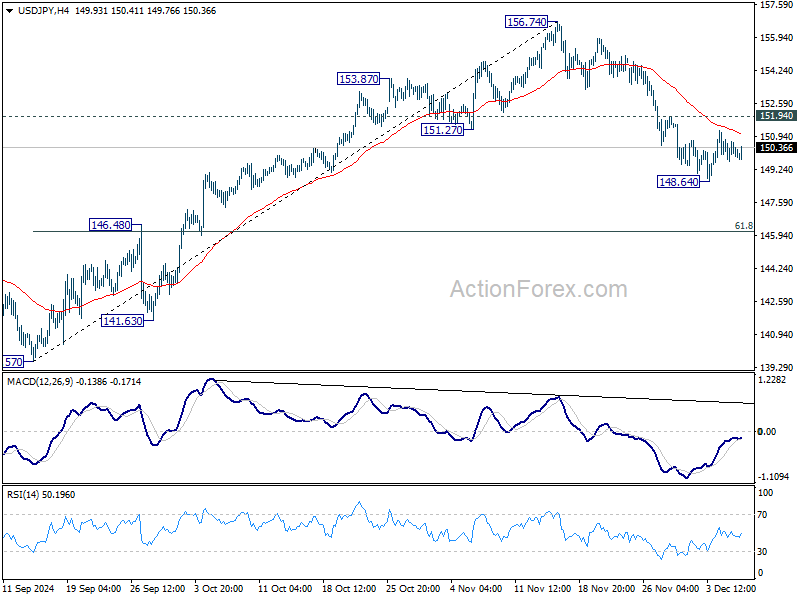

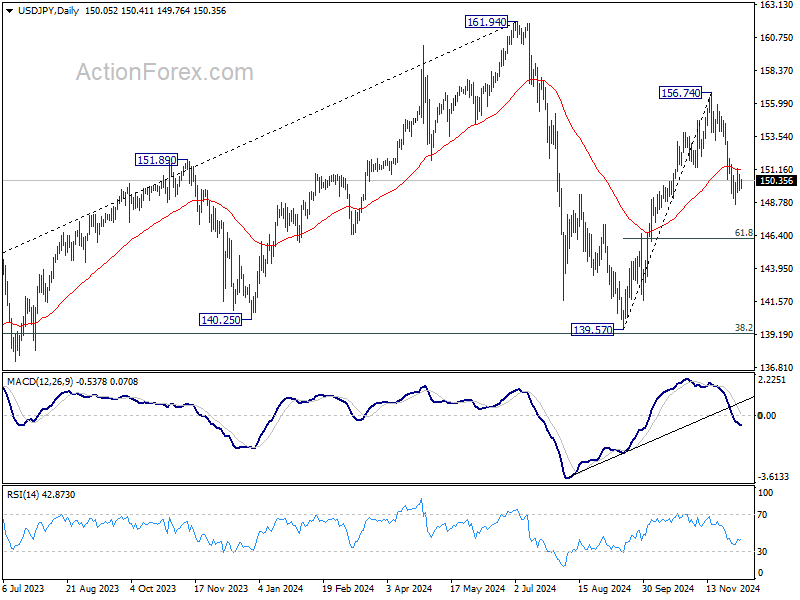

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.59; (P) 150.18; (R1) 150.71; More...

USD/JPY is still bounded in consolidation above 148.64 and intraday bias stays neutral. On the downside, break of 148.64 will strengthen the case that rise from 139.57 has already completed at 156.754. Deeper fall should then be seen to 61.8% retracement of 139.57 to 156.74 at 146.12 next. Nevertheless, firm break of 151.94 resistance will revive near term bullishness and bring retest of 156.74 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

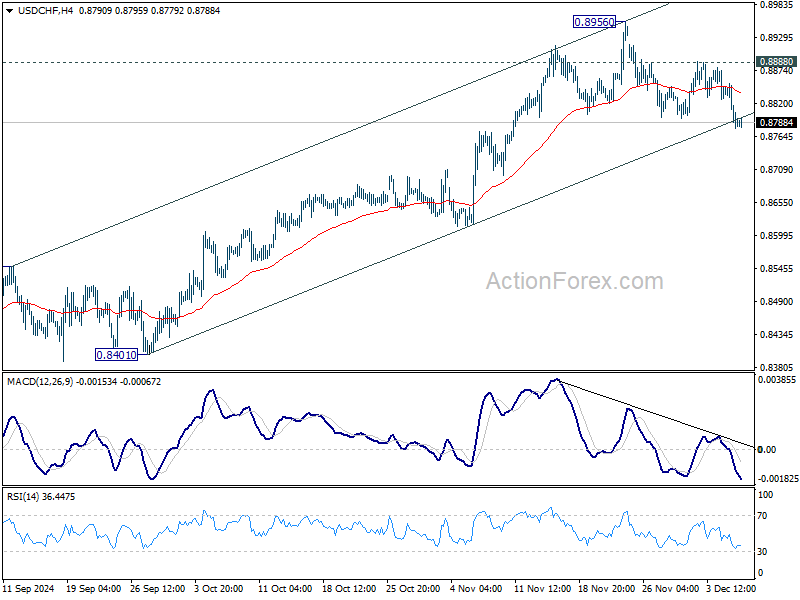

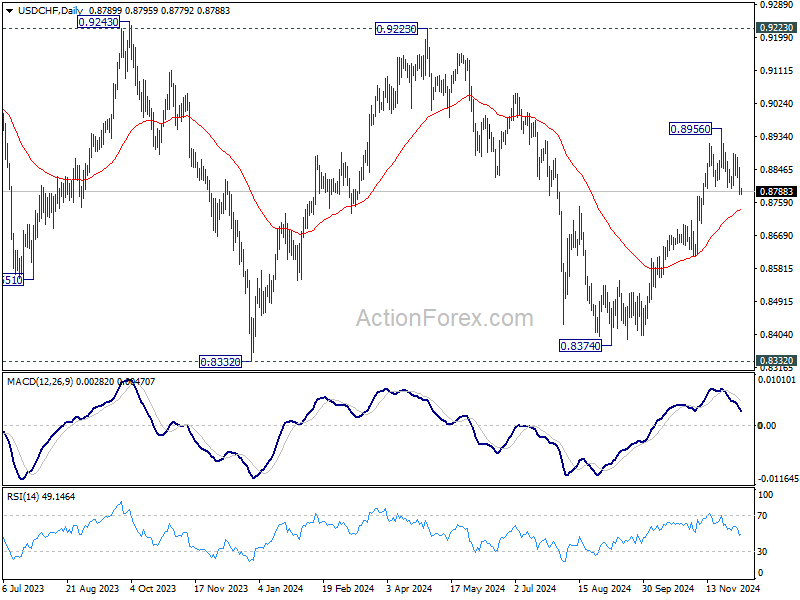

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8758; (P) 0.8806; (R1) 0.8832; More…

USD/CHF' fall from 0.8956 resumed and the break of 0.8800 support suggests that deeper decline is underway. Intraday bias is back on the downside for 55 D EMA (now at 0.8738). Strong support could be seen there to bring rebound. Break of 0.8888 will bring retest of 0.8956 first. Nevertheless, sustained break of 55 D EMA will indicate near term bearish reversal.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

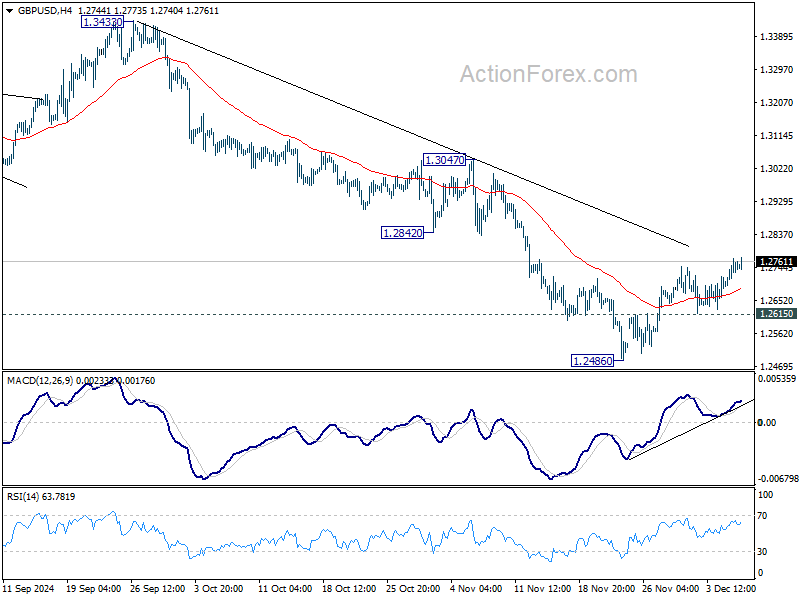

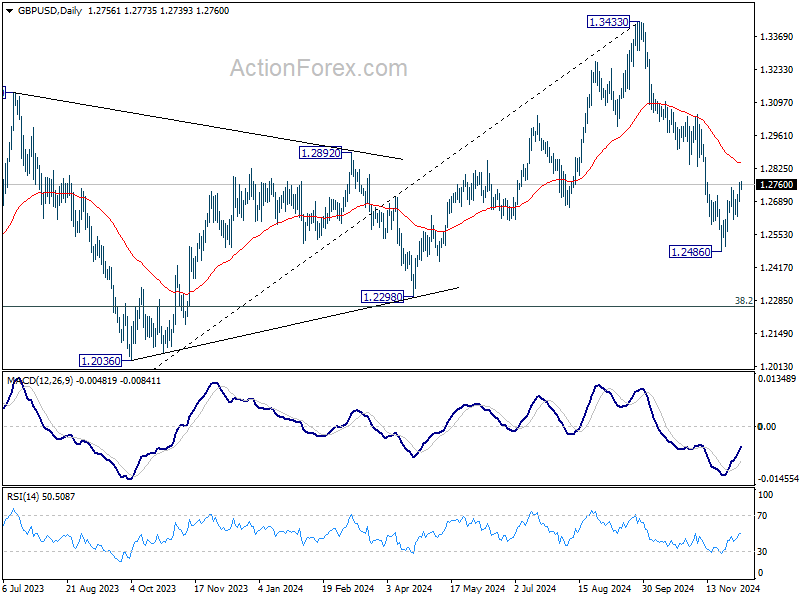

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2712; (P) 1.2742; (R1) 1.2790; More...

Intraday bias in GBP/USD remains on the upside at this point. Rebound from 1.2486 would target 55 D EMA (now at 1.2849). Strong resistance is expected there to limit upside, and bring resumption of whole fall from 1.3433. On the downside, below 1.2615 minor support will bring retest of 1.2486 low first. However, sustained break of 55 D EMA will argue that the near term trend has reversed, and targets 1.3047 resistance for confirmation.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2849) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

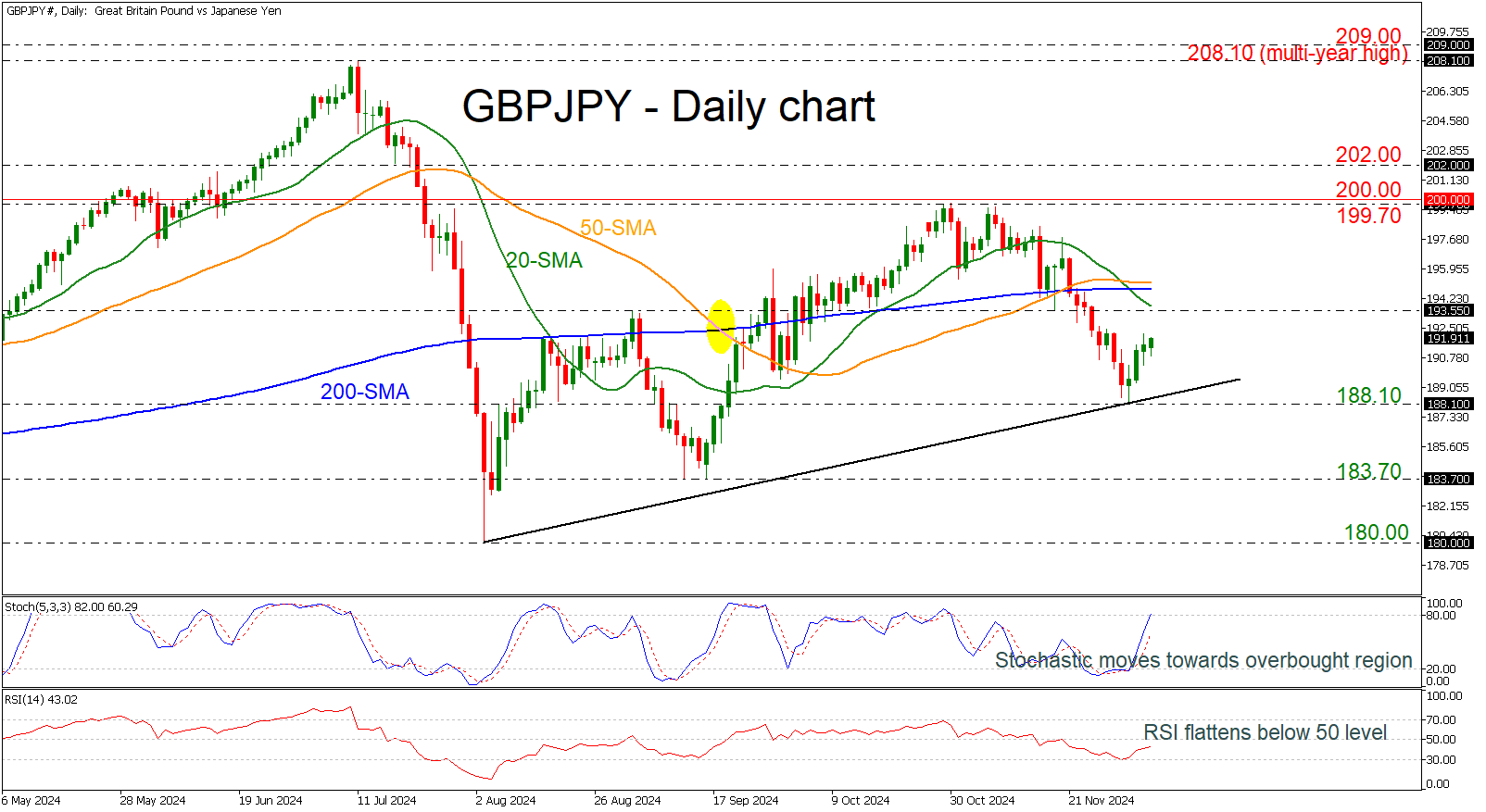

GBPJPY Looks Ready to Challenge 192.00

- GBPJPY bounces off uptrend line

- Stochastic and RSI head higher

GBPJPY has been moving higher over the last few days after the rebound from the support level around 188.00 and is currently trading near 192.00. This upward movement suggests a potential shift in market sentiment, with buyers stepping in to push prices higher.

The stochastic oscillator is heading toward the overbought area with strong momentum so far, while the RSI is trying to boost its positive sentiment below the neutral threshold of 50.

If the price continues the upside move, then it may find immediate resistance at the 193.55 level, which stands near the 20-day simple moving average (SMA). Slightly higher, the 200- and 50-day SMAs around 195.00 could pose a significant obstacle before the price moves towards the crucial 199.70 level.

Alternatively, a bearish wave could potentially lead traders to engage in another battle with the short-term uptrend line at 188.90, which is located ahead of the 188.10 barricade. Below that, the bearish structure may pause at the 183.70 support.

Overall, the technical indicators suggest that GBPJPY could continue its upward trajectory in the short term, especially if it breaks above the resistance level at 195.00. However, traders should remain cautious and watch for any signs of reversal.

Gold Prices Dip but Remain Supported by Fed Rate Cut Expectations

Gold prices dipped below 2,620.00 USD per troy ounce on Friday, marking a second consecutive session of decline. The value of the precious metal continues to be influenced by developments in US economic indicators and expectations surrounding the Federal Reserve's monetary policy.

Investor attention is particularly focused on the upcoming November US labour market data, poised to provide further insights into the Federal Reserve's monetary policy directions. Recent statistics indicating an increase in unemployment claims suggest potential cooling in the employment sector. This data arrives just ahead of the highly anticipated nonfarm payrolls report, which is crucial for gauging the health of the US labour market.

The probability of a Fed interest rate cut in December currently stands at 70%, with expectations of a 25-basis-point reduction. Such a cut would likely benefit Gold, as lower interest rates decrease the opportunity cost of holding non-yielding assets like Gold.

On the demand side, despite a decline in interest in jewellery, China's investment in Gold remains robust, according to World Bank data, providing fundamental support to Gold prices.

Technical analysis of XAU/USD

H4 chart: Gold has experienced a growth wave, peaking at 2,666.35, followed by a correction down to 2,616.60. A new growth impulse towards 2,663.00 is underway, and we anticipate the formation of a consolidation range around this level. If the price breaks upward, it may continue its ascent towards 2,714.00. The MACD indicator supports this bullish outlook, with its signal line hovering near zero and pointing upwards.

H1 chart: the XAU/USD has completed a growth impulse to 2,640.00 and is likely to form a narrow consolidation range around this level. An upward breakout would suggest the continuation of the growth impulse to 2,663.00, potentially extending to 2,666.00. This scenario is corroborated by the Stochastic oscillator, with its signal line currently above 50 and trending upwards towards 80, indicating strong upward momentum.