Sample Category Title

Markets Weekly Outlook – Central Bank Focus as US Inflation Looms

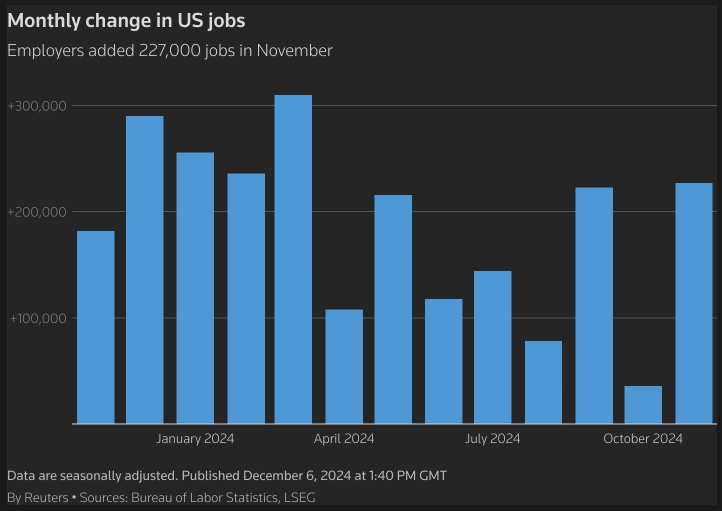

- US Jobs report all but confirms a December rate cut, with markets pricing in an 80% probability.

- Nasdaq nears 22,000 as US equities continue their strong performance, with the S&P 500 also hitting record highs.

- Global markets await US CPI and ECB decisions, with expectations of a 25 bps rate cut from the ECB.

- Focus for the week ahead includes US CPI, ECB decision, and Chinese inflation data.

Week in Review: Jobs Data All but Confirms a December Rate Cut

A week that saw a lot of choppy price action as markets awaited the US jobs report on Friday. A stellar jobs print of 227k and a slight uptick in the unemployment rate to 4.2% appear to have sealed a December rate cut.

Source: LSEG

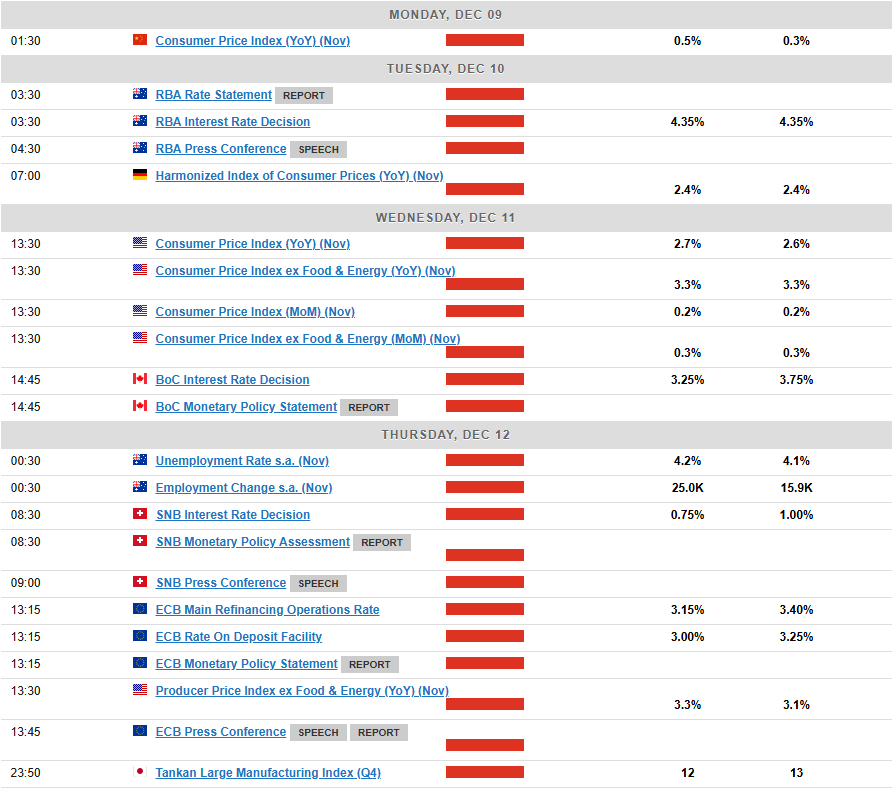

Barring any crazy inflation surprise in the week ahead, markets appear fairly certain that the Fed will deliver a 25 bps cut in December. Federal Reserve policymakers will enter a media blackout that kicks in on Saturday, in the run-up to the central bank’s Dec. 17-18 policy meeting.

US Equities have been the talk of the town once more, as Wall Street Indexes continued their impressive YTD performance. The S&P 500 and the Nasdaq hit intraday record highs on Friday while the Dow struggled following a drop in UnitedHealth shares.

The ‘Santa rally’ appears to be here with the S&P making its way above the 6100 handle and the Nasdaq eyeing consolidation above the 21500 handle. Following the day’s move the S&P and Nasdaq are on course for a third consecutive week of gains with the Dow on course for a minor setback.

Oil prices struggled this week despite OPEC + continuing their current production cut schedule into 2025. The Organization of the Petroleum Exporting Countries (OPEC)+, pushed back the start of oil output rises by three months until April and extended the full unwinding of cuts by a year until the end of 2026

Following a choppy week, Oil was trading down around 1% on Friday and on course to finish the week down around the same. Bank of America forecasts that increasing oil surpluses will drive the price of Brent to average $65 a barrel in 2025, while expecting oil demand growth to rebound to 1 million barrels per day (bpd) next year, the bank said in a note on Friday.

Gold remained rangebound for the majority of the week, as the precious metal coiled in a $40 range between 2612-2660. Not even Friday’s jobs data was enough to shake the precious metal into a breakout.

The DXY had a mixed week with a strong start and end to the week followed by a soft middle leaving the DXY on course for marginal gains of about 0.35%. This was reflected in the choppy price action by major pairs this week with the Euro and the GBP unable to hold onto gains against the Greenback.

The DXY will be worth monitoring given the US Dollar has a track record of poor performance in the Month of December. An uptick in US inflation however could aid the Dollar in its bid to reclaim the 107.00 handle next week.

The Week Ahead: US Jobs Data to Dominate

Asia Pacific Markets

The week ahead in the Asia Pacific region sees some key economic data releases and events.

In China, the big event next week is the annual Central Economic Work Conference. While it won’t focus on exact numerical targets (those are usually set during the Two Sessions), it will give clues about how policymakers are planning for next year. This could have an impact on emerging market currencies and currencies like the Australian Dollar as well.

The better question would be whether there’s any change in their approach to fiscal policy or monetary policy.

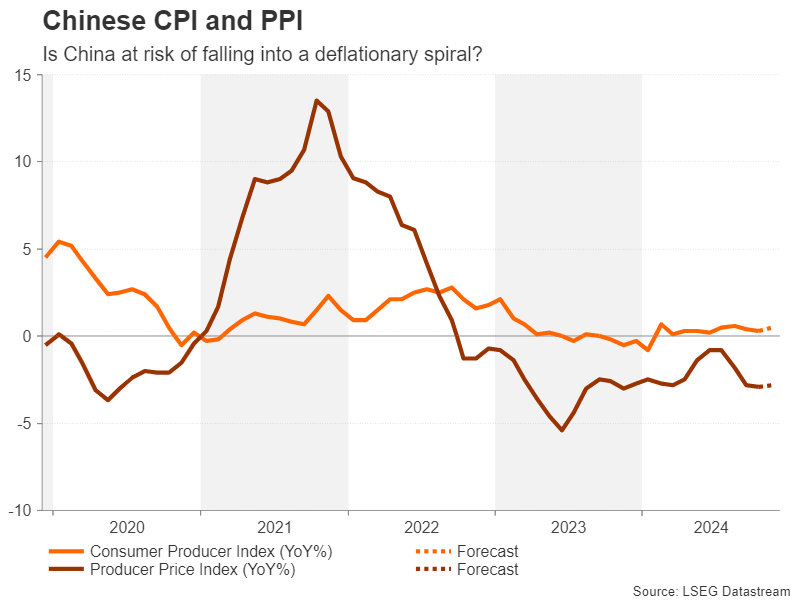

China will release its November inflation data on Tuesday and trade numbers on Wednesday. Inflation could very well rise to 0.6%, from the previous 0.3%. Imports are likely to stay weak due to low domestic demand, growing only around 1.2%.

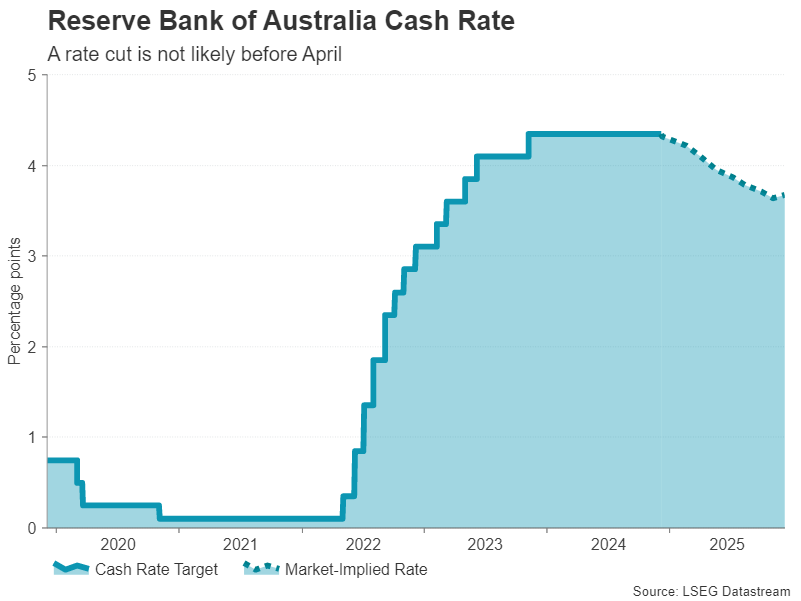

In Australia, the RBA is expected to keep rates on hold this week at 4.35%. The uptick in October core inflation coupled with stronger economic growth in the third quarter suggest the RBA isn’t in a hurry to lower rates.

In Japan, the Tankan Business Survey will be out this week. This comes as speculation continues to grow that the BoJ will deliver a rate hike of 25bps at its upcoming meeting. Something else to pay attention to may be the manufacturing sector, which may face challenges due to growing uncertainty around global trade policies, especially in the auto industry.

Europe + UK + US

In developed markets, the focus moves back to the US and CPI inflation data as speculation grows around a December rate cut.

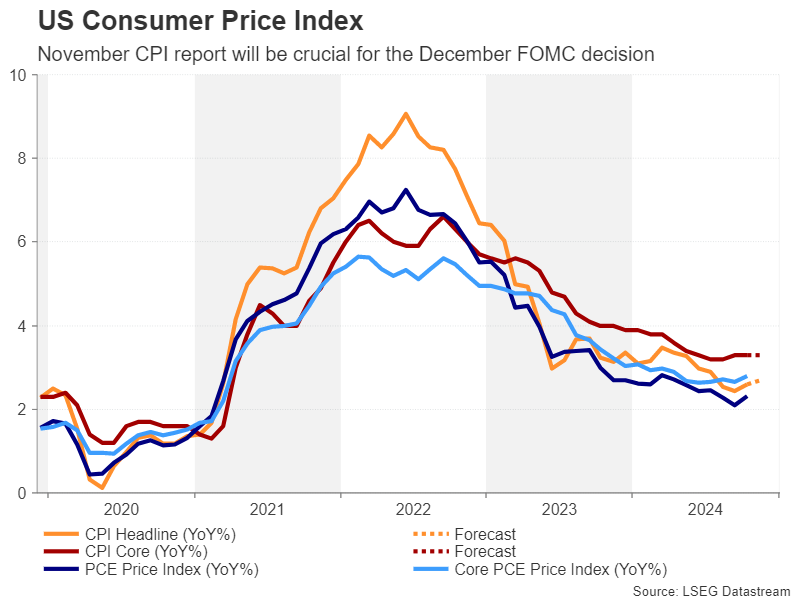

Core CPI is expected to rise by 0.3% month-on-month again, which could complicate the December decision for the Federal Reserve despite the probability of a rate cut lingering around the 80% mark.

Policymakers agree that policy remains restrictive and the sticking point seems to be over the pace of cuts. I do still think the idea of Trump assuming office will play in the minds of policymakers who will likely cut in December and take a pause in January.

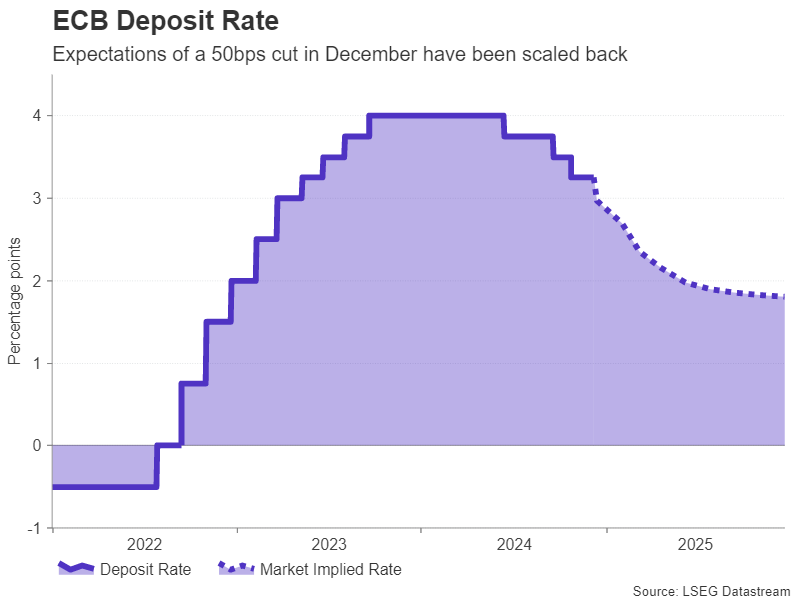

In Europe the ECB decision is due this week with any doubt around the size of a cut seemingly evaporated. A recent bout of data and comments from policymakers have seemingly ruled out the possibility of a 50 bps cut with 25 bps the most likely outcome.

To show they remain committed to managing rates effectively, the ECB is likely to signal that it plans to keep moving rates towards neutral levels and is open to lowering them further into easing territory if needed.

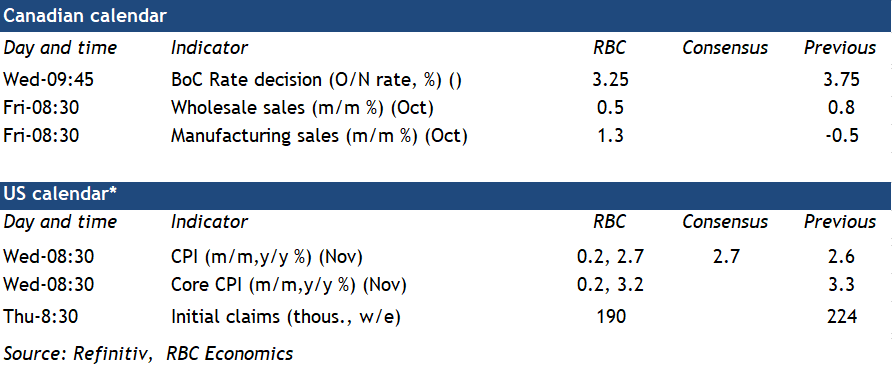

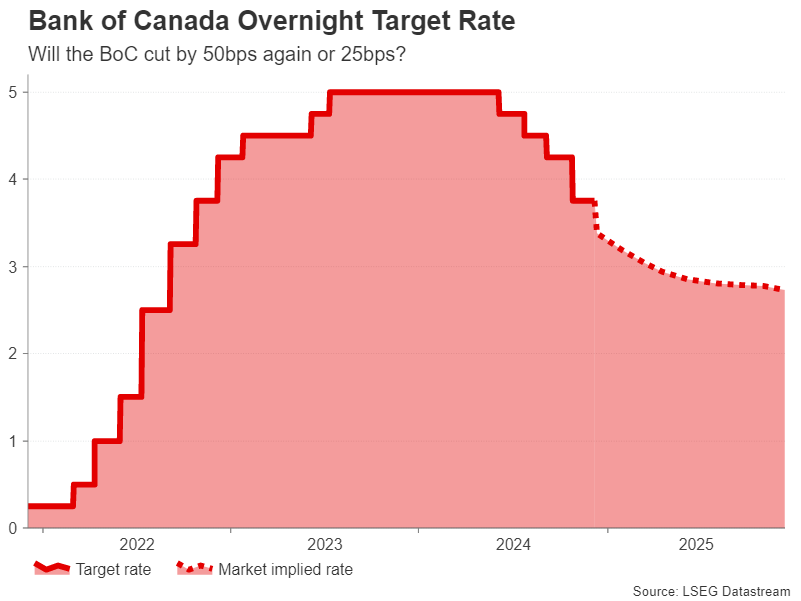

The Bank of Canada has lowered its policy rate by 125 basis points since June, and there’s a strong chance it will cut another 50 bps next week. This would bring the rate down to 3.25%, as the central bank tries to reach a neutral level quickly.

The cuts are needed as Canada struggles with slow economic growth and low inflation. There are other challenges as well while the looming threat of a Trump Presidency and tariffs when he takes office also weighs on the minds of BoC officials.

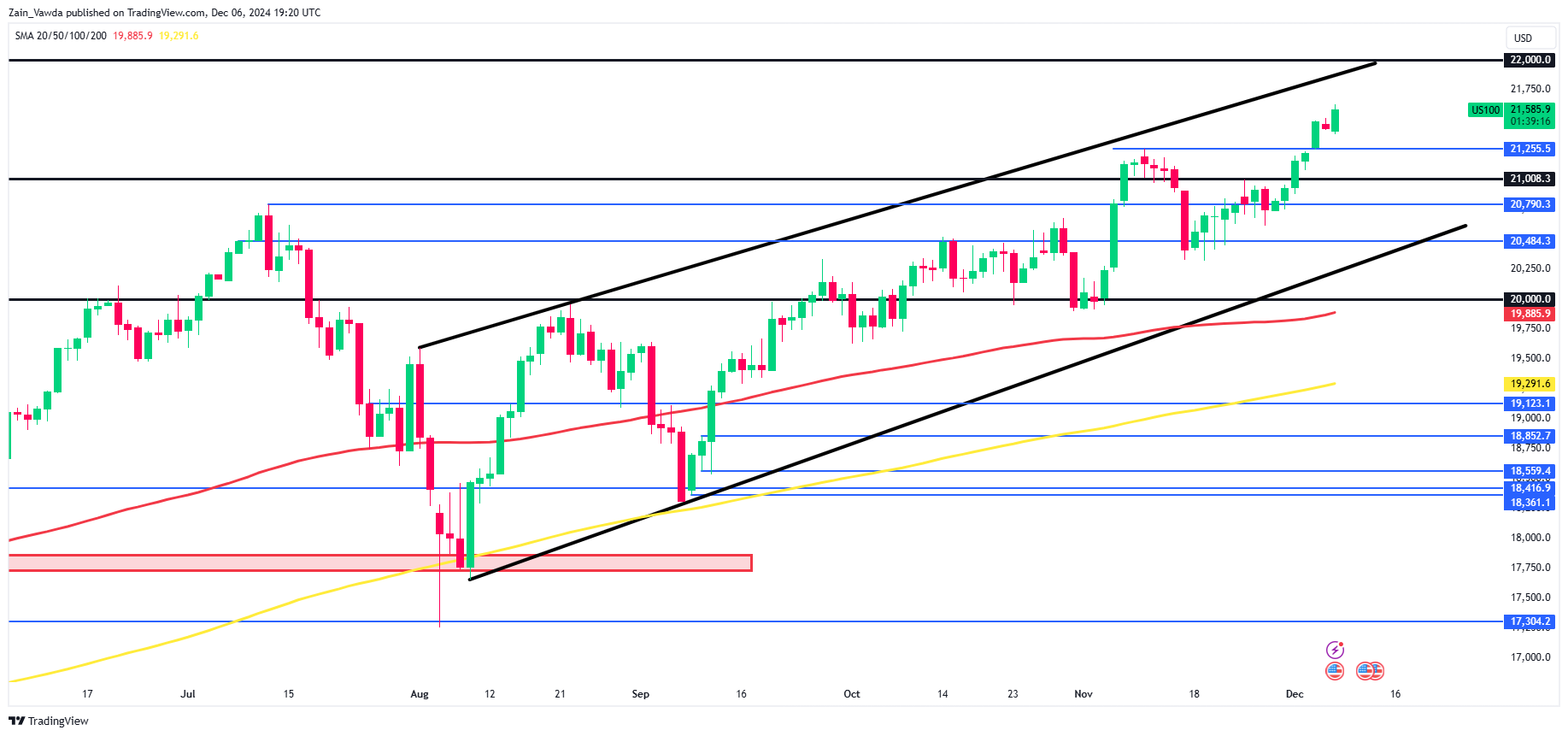

Chart of the Week

This week’s focus is now on the Nasdaq 100, following another stellar showing by US equities. The ‘santa rally they say’, looking good so far.

The Nasdaq 100 is now within 400 points of the 22000 handle following a strong end to the week as US jobs data seemed to confirm a December rate cut.

The Nasdaq is currently in a channel and the top of the channel is around the 22000 handle which would make that a key area of resistance. Before that level however the 21750 handle may also present challenge. The Nasdaq monthly open was around 20930 with the index already rising around 700 points this month.

Any pullback may be viewed as a potential opportunity for buyers to get involved. The historical performance of the index in December coupled with the current fundamentals suggest we may see more upside before the month comes to a close.

My bias remains bullish for the Nasdaq but getting involved now would pose the risk of a correction before the next leg to the upside.

Nasdaq 100 Daily Chart – December 6, 2024

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 21255

- 21000

- 20790

Resistance

- 21750

- 22000

- 22250

The Weekly Bottom Line: Data Clears the Path for the Rate Cut in December

Canadian Highlights

- The odds of a 50 basis-point rate cut rose to 80% as the unemployment rate ticked up to its highest level since January 2017 (excluding the pandemic).

- There are notable positives in the jobs report. Employment rose by more than twice the consensus forecast, and the employment rate held steady in October, breaking the recent trend of declines.

- With looming tariffs, fiscal spending is poised to rise in 2025. Together with the rebound in consumer spending and real estate, this argues for a more measured 25-basis point rate cut next week. The Bank may still opt for larger cuts if it prioritizes higher unemployment rate and broader economic weakness.

U.S. Highlights

- The embattled ISM Manufacturing Index showed improvement in November, but continued to point to contraction. In contrast to manufacturing, the services sector continued to expand in November, although the pace of growth slowed.

- As was widely expected, hiring rebounded in November, with payrolls adding 227,000 new jobs, as impact of the Boeing strike and hurricanes reversed. However, an uptick in the unemployment rate increased market confidence that a Fed rate cut is in the offing.

- Vehicle sales also posted a sizeable gain in November, reaching the highest level in over three years. It is possible that some of this strength in sales came from replacement demand related to hurricane activity.

Canada – Employment or Unemployment: That is the Question

This week on Bay Street, attention centered on bank earnings, which presented a balanced mix of misses and beats, resulting in modest movement. Investors had plenty to digest with today’s employment report. The unemployment rate climbed to 6.8% - its highest level since January 2017, excluding the pandemic. This nudged the odds of a 50 basis-point rate cut up to 80% (at the time of writing) from what was previously a near coin flip. Consequently, the 10-year bond yield dropped below 3.0% mark for the first time since October, while the S&P/TSX ended the week up 0.5%.

Yet focusing solely on the unemployment rate risks missing the full picture, as the increase was driven by a boost in labour force rather than job losses. There are plenty of bright spots in the overall picture. Employment rose by 51k – more than twice the consensus forecast. Full-time positions accounted for most of the gains, extending the momentum seen in recent months. Previously, employment growth trailed the expansion in the labour force, pushing the employment rate (the share of population that is employed) lower. This time, however, the employment rate held steady, rather than declining (Chart 1).

Taken together, these figures challenge the collective wisdom of the market. We think that today’s labour market data offers little justification for aggressive monetary easing. Moreover, average hourly wage growth of 4.1% year-on-year should still be too discomforting for the Bank of Canada. Strong wage growth without accompanying productivity gains fuels inflationary pressures, strengthening the case for a measured approach to rate cuts.

There are other reasons to tread carefully as 2025 approaches. President-elect Donald Trump’s renewed threats of tariffs loom large, potentially making trade dynamics a critical swing factor. In October, Canada’s merchandise trade balance recorded its eighth consecutive monthly deficit. Although exports rose for the first time in four months, modest import gains outpaced the improvement. Nonetheless, trade with the United States remained a bright spot. Despite declining, the value of exports to the U.S. exceeded the value of imports, contributing positively to Canada’s overall trade balance. This trend has played growing role on economic activity since the USMCA came into effect in mid-2020 (Chart 2).

This trade surplus with the U.S. is precisely what Trump opposes and demands stronger border security in exchange for Canada avoiding tariffs. As a result, any trade deal would likely entail increased spending on border security and defense. This would add to fiscal stimulus initiatives, such as tax holidays and direct payments.

Finally, recent rebounds in consumer and real estate activity argue for the Bank of Canada taking incremental steps to reduce restrictive monetary policy and avoiding steps that could exacerbate inflationary pressures. Still, policymakers may focus on the spike in the unemployment rate and the broader weakness in economic activity, opting to cut rates by another 50 basis points. The wait is almost over – attention now shifts to next Wednesday’s policy decision.

U.S. – Data Clears the Path for the Rate Cut in December

It’s not just the Christmas holidays that are fast approaching. The next Federal Reserve meeting is also just around a corner, and this week featured several important updates for signals on the health of the U.S. economy. This week’s results were broadly positive: contraction eased in manufacturing, activity continued to expand in the services sector, job growth rebounded in November, as did vehicle sales. Vehicle sales registered their highest level in over three years, although it is possible that some of this strength came from replacement demand related to hurricane activity.

The embattled ISM Manufacturing Index showed improvement in November, but still signaled that activity is contracting. Overall, the manufacturing sector has gained some momentum, with the new orders index rising for the third consecutive month, since the Fed began cutting interest rates. However, regulatory and trade policy cloud the outlook. In contrast to manufacturing, the services sector continued to expand in November, although the pace of growth slowed. Still, with 14 out of 18 industries reporting growth, the services sector appears to be in relatively good shape.

As expected, hiring rebounded in November, with payrolls adding 227k new jobs (Chart 1). Revisions also added 56k jobs to the gains seen in the prior two months. Smoothing through the recent volatility, job gains have averaged 173k over the past three-months, or only a modest step down from the 186K averaged over the prior twelve-month period. But this likely overstates the degree of “strength” in the job market. In the household survey, the unemployment rate backed up one tenth to 4.2%, after spending September and October at 4.1%.

Other indicators, such as the Job opening and labor turnover survey (JOLTS), similarly point to a labor market that has come into balance and is no longer a meaningful source of inflationary pressure. JOLTS data, released this week, showed that while job openings increased in October, the uptick was narrowly concentrated in professional and business services and leisure and hospitality. Meanwhile, both the quit rates and the hiring rate are below their pre-pandemic levels. This suggests that the employers are becoming more selective, while workers are less eager to leave job voluntarily. Indeed, with no significant premium for job switching (Chart 2) and given the low hiring rate, landing a new job may be challenging.

Comments from the latest Fed’s Beige book also reflected this trend, stating that “hiring activity was subdued as worker turnover remained low” and that “wage growth softened to a modest pace”. The Beige book, along with the payrolls and especially the next week’s inflation report will help to solidify the Fed’s stance on their next rate move later this month. The cooling labor market should give the policy makers confidence for another quarter point cut. However, with inflation showing some stickiness lately, and in the words of Jerome Powell this week, the Fed could “afford to be a little more cautious”. The market is pricing nearly 90% odds of a December cut, but the path for rate cuts in 2025 is less clear.

Bank of Canada to Cut Interest Rates Again by 50 Basis Points

We expect the Bank of Canada’s final policy decision of 2024 on Wednesday to be another 50 basis point interest rate cut—adding to a 50 bps cut in October and 125 bps in total cuts since June.

Canada’s economic backdrop has yet to crumble in a way that would cause the BoC to panic, but it is also clear that interest rates are higher than they need to be for inflation to hold at the central bank’s 2% target. Some interest rate-sensitive sectors of the economy (home resales, consumer spending on durables) showed signs of life in Q3, but overall gross domestic product growth is tracking below the BoC’s October forecast in the second half of the year and per person GDP declined for a sixth consecutive quarter in Q3.

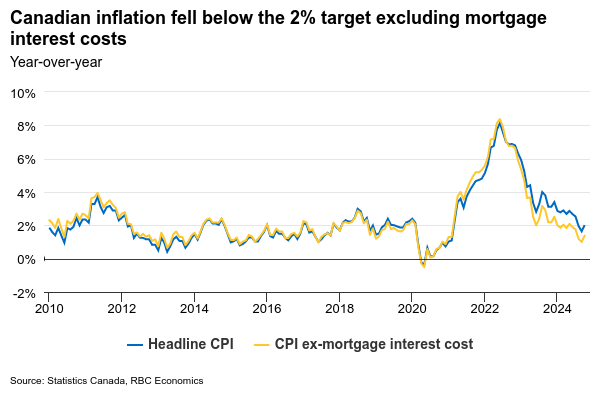

The unemployment rate—up by a full percentage point from a year ago—is flagging excess supply in labour markets and, excluding the impact of mortgage interest costs, (which are rising as a direct result of earlier interest rate increases) consumer price index growth has been essentially at or below the BoC’s 2% inflation target for all of 2024. It was 1.4% year-over-year in October.

And interest rates are still high— particularly when compared to that softening economic backdrop. The 50 bps cut we expect on Wednesday would still leave the overnight rate at the top end of the 2.25% to 3.25% range that the central bank views as “neutral,” well above the 1.75% peak in the decade ahead of the pandemic. In other words, additional interest rate cuts so far have been the equivalent of the BoC easing off the economy’s brakes rather than stepping on the gas. We continue to expect that additional interest rate cuts will be needed in the year ahead with the overnight rate ultimately falling below the BoC’s estimate of the neutral range at 2% in mid-2025.

Week ahead data watch

We expect U.S. headline inflation to tick up slightly from 2.6% year-over-year in October to 2.7%. Energy prices likely continued to decline on an annual basis but at a slower rate, pushing headline inflation higher. Food price growth was likely to edge lower again. Excluding volatile components (food and energy), we look for core inflation to hold steady at 3.3% for the third consecutive month.

Statistics Canada’s advance wholesale indicators suggest core wholesale sales likely rose by 0.5% in October, largely driven by higher motor vehicles, parts and accessories sales.

We look for manufacturing sales to grow by 1.3% in October, in line with StatsCan’s preliminary estimate. The growth was mainly supported by petroleum, coal products and transportation equipment subsectors.

Weekly Economic & Financial Commentary: The Song Remains the Same

Summary

United States: The Song Remains the Same

- Incoming economic data continue to illuminate pockets of stress in the U.S. economy. The unwinding of strikes and hurricane effects lifted nonfarm payrolls by 227K in November; however, job gains remain highly concentrated by industry. Openings also continue to trend lower through the month volatility. Meanwhile, tariff-related stress is beginning to form in both the manufacturing and services sectors.

- Next week: NFIB Small Business Optimism Index (Tue.), CPI (Wed.), Federal Budget Balance (Wed.)

International: Potpourri of Global Economic Events and Data

- Even though Thanksgiving has passed, market participants had their plates full this week with international political developments, economic events and data releases. Political uncertainty took hold amid headline-making developments in South Korea and France, while we also gained further insight into economic conditions in a variety of advanced and emerging economies.

- Next week: Bank of Canada (Wed.), Brazilian Central Bank (Wed.), European Central Bank (Thu.)

Interest Rate Watch: Hawk or Dove, Data-Dependency Name of the Game

- The Fed's blackout period—or two-week stretch ahead of its meeting where Fed officials do not make public policy comments—begins this Saturday. Recent comments suggest members believe the path for policy has grown more uncertain, though there remains broad support for a gradual data-dependent reduction in rates.

Topic of the Week: Bad Day for Barnier

- On Wednesday, the French government collapsed after its National Assembly voted to oust Prime Minister Michel Barnier. President Macron now faces the difficult decision of appointing another prime minister to navigate the fragmented Assembly and pass a budget bill for 2025.

ECB Preview: A Disputed 25bp Rate Cut

- Next week, the ECB is set to cut rates for the fourth time this year. Unlike the previous three cuts, the outcome of next week’s rate decision is not given as 1) the restrictive policy stance, 2) the deteriorating growth outlook, and 3) inflation at target has opened discussions of a 50bp cut. While a 50bp cut will certainly be discussed, we judge that the ECB will ultimately deliver a 25bp rate cut, and guide that they are open to any size of rate cuts at future meetings, subject to the incoming data. A 25bp cut next week will bring the ECB’s deposit rate to 3.0%. In the coming year, we expect a string of rate cuts, leading to a terminal rate of 1.5% being reached in September 2025.

- We expect a benign market reaction, even if Lagarde decides to twist guidance towards an increasing likelihood of a faster rate of normalisation.

Change guidance of policy restrictiveness

Since last year, the ECB has included a reference that it aims to keep monetary policy ‘sufficiently restrictive’ for as long as necessary. Following the disinflationary process that has gained traction through 2024, the updated staff projections next week are likely to forecast inflation on target from 2025 and onwards. Thus, whether monetary policy should stay restrictive is likely going to be debated. We believe that the slightly hawkish bias in the ECB’s communication is set to change as the need for a restrictive monetary policy stance in the Eurozone is no longer obvious. But the camps inside the GC are obviously divided. In a recent interview the ECB’s Schnabel said that in her view the restrictive part of the monetary policy stance is already fading. At the same time, we see the dovish camp, for example Villeroy, saying that there ‘won’t be any reasons’ for policy to remain restrictive.

A 25 or a 50bp rate cut? It is not the most important question

With activity indicators looking bleak heading into 2025, the case for a 50bp rate cut has strengthened, as the starting-point for financial conditions is restrictive based on most measures. However, given the ECB’s sole inflation mandate, and the ‘political’ aspect of having a gradual rate cutting cycle, we believe it will favour a 25bp rate cut.

However, whether the ECB will deliver a 25bp rate cut or 50bp rate cut in December is not that important in isolation, as the communication around it will be key as well. There seem to be diverging views on how to cut the cake. Most recently, Schnabel’s interview clearly suggested that she would opt for a 25bp rate cut, as would Vujcic, while others such as Lane, Villeroy and Centeno are more open to discussing a 50bp rate cut.

That said, rather than focusing on the rate cut next week, we should focus on where the policy rate will end in this cutting cycle, albeit we do not expect any verbal guidance on this. Markets may though interpret a 50bp cut as a signal of a lower terminal rate – and that may even be a signal that the ECB wants to send.

But as we do assume the ECB does not want a hawkish reaction from markets, leading to tighter financial conditions, we expect it to opt for a dovish 25bp cut, focusing on the communication on a potential jumbo cut.

Macro data since the October meeting has mainly given ammunition to the doves

Since the October meeting, the momentum in underlying inflation has fallen further and growth indicators have weakened. The composite PMI indicator declined sharply to 48.3 in November mainly driven by the service sector, which is now also in contractionary territory. Data indicates that the eurozone’s two largest economies, Germany and France, are likely to contract in Q4 while Spain should drive aggregate euro area growth together with Portugal and Greece. The deteriorating growth indicators combined with rising political uncertainty since the October meeting have mainly given ammunition to the dovish members of the ECB. However, the hawks’ last battalion, namely the labour market, continues to show resistance with the unemployment rate remaining at a record low of 6.3% in October and the national account data showing increased employment in Q3.

Underlying inflation has eased further

While headline inflation has increased from the three-year low in September, mainly reflecting base effects, the underlying momentum has continued to ease. The average month-on-month increase in seasonally adjusted core inflation has been 0.14% in the past three months, which is well in line with 2% annualised inflation. Importantly, the lower momentum in underlying inflation has been driven by service inflation where momentum is also quickly approaching the 2% target, according to the ECB’s own seasonally adjusted data. Hence, inflation developments have clearly also supported the doves in the ECB. For the hawks, an argument for a cautious cutting approach is wage growth that remains elevated given the tight labour market. Negotiated wage growth increased to 5.4% y/y in Q3, albeit largely driven by one-off payments, and has averaged 4.6% so far this year, compared to 4.4% in 2023.

Staff projections to show lower growth and inflation

We expect the ECB staff to take note of the recent easing in the momentum of underlying inflation and incorporate this into a lower forecast for core inflation next year relative to the forecast in September. We expect core inflation to be revised down to 2.2% y/y in 2025 (from 2.1%) and headline inflation to 2.1% y/y (from 2.2%). Oil futures were 6% lower at the cut-off date for the staff projections compared to December, but gas and electricity futures were higher, so we expect only a marginal reduction in the headline forecast. We expect the growth forecast to be revised down in 2025 to 1.1% y/y from 1.3% y/y due to the continued struggles in the manufacturing sector combined with cautious consumers and a weak German economy. In contrast to the ECB’s previous projections, consumers continue to have an elevated savings rate, which prevents consumption from picking up in the near term. The new staff projections will also include an additional year, albeit we do not attach significant weight to those projections given their embedded uncertainties.

Limited FX market reaction on 25bp rate cut

Speculation around a 50bp cut has diminished, with markets now largely positioned for a 25bp move, with only 27bp priced in. However, the post-decision communication will be crucial, given divisions within the Governing Council that could drive a range of market responses.

We view a dovish 25bp cut, where the ECB signals flexibility to adjust the size of future cuts, as the most likely scenario. Such an outcome would likely have a limited impact on EUR/USD, and with the probability of a jumbo cut still being priced in markets. However, should the ECB indicate a preference for continuing the easing cycle in 25bp increments, market pricing could shift, potentially triggering a hawkish response and a moderate EUR/USD rally, albeit given the meeting-by-meeting approach and thereby keeping full flexibility about future monetary policy decisions, we see that as a low probability outcome. By contrast, a 50bp cut – an outcome we believe is underappreciated despite weak euro area growth and inflation – would likely prompt significant EUR depreciation, with EUR/USD potentially dropping sharply.

Looking ahead, the Fed’s December meeting is likely to have a more decisive impact on EUR/USD’s near-term trajectory, with Friday’s US jobs report a critical input. While markets currently assign a decent probability to a Fed pause, we expect a 25bp cut. If this materialises, it should help contain further EUR/USD downside into year-end. Seasonal trends and our short-term valuation models support this view, as EUR/USD appears oversold after its sharp decline since October. We expect the pair to close the year at around 1.06.

From a strategic perspective, we maintain our bearish EUR/USD outlook, driven by the relatively stronger US growth narrative. Our 12M target remains 1.01, making parity a plausible level over the coming year. On the rates side, we note that the significant decline in rates over the past month has brought the spot level for long swap rates close to our 12- month forecast, thus offering a very limited declining profile from here, see more in Yield Outlook - Transatlantic decoupling but not for much longer, 28 November 2024. We do not expect a signal from the ECB to address the French spread widening to peers.

Weekly Focus – Cutting Cycle Continues

This week, we published our macroeconomic projections for the global economy and the Nordics. In the euro area, we expect growth to slowly increase during 2025, but the near-term outlook is weak. We expect some cooling in the US, but steady economic growth to continue despite fiscal and trade policy uncertainties. China continues to struggle with the heavy housing crisis, but stronger steps are taken to turn this around. New tariff clouds hang on the horizon, though and we have revised down our growth outlook.

In fixed income markets, France once again attracted attention after the parliament ousted PM Barnier. The political turmoil drove the OAT-Bund spread to new highs but later the move reversed. President Macron refused to step aside, and his first task will be to name a new PM. In a week where global yields largely traded sideways there was little French market contagion or South Korean for that matter, following the six hours of martial law, that did however plummet the Won.

In Europe, retail sales were a bit stronger than expected in October, which supports the outlook for more consumer driven growth going forward. The breakdown of the Q3 national accounts also revealed surprisingly strong domestic demand with solid investments and household consumption. Annual growth in compensation per employee was 4.4%, close to ECB projections, which supports the view of underlying inflation converging towards the 2% target.

In the US, weaker than expected ISM data blurred the picture of the service economy, which has largely looked strong recently. The jobs report was no big market mover but on the margin to the weak side. Close to 300,000 new jobs (including revisions) is strong but at odds with a much weaker employment picture in the household survey. Besides, it came along with a higher unemployment rate and a shrinking labour force, not exactly a sign of strength. It adds tailwinds to our call for back-to-back rate cuts at the upcoming FOMC meetings. This mix of solid euro area data and US data on the weak side contributed to some retraction in the recent month's move lower in EUR/USD.

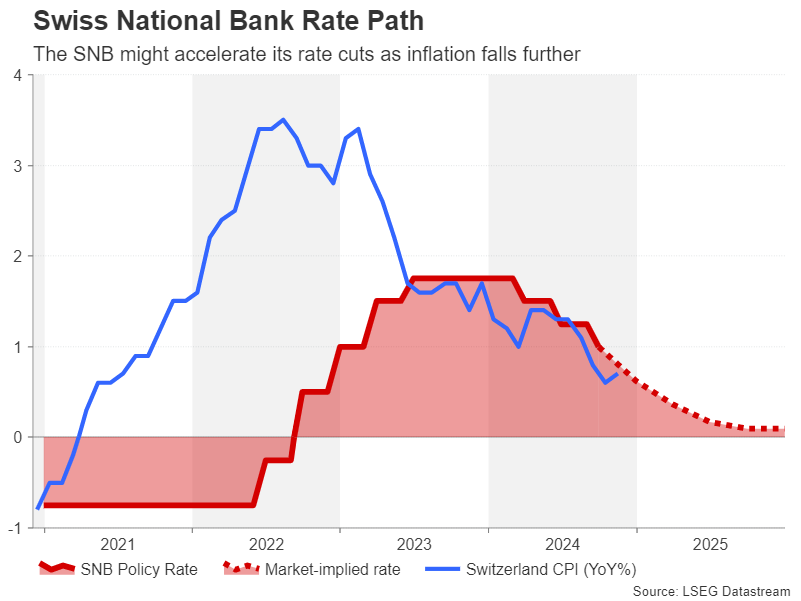

Next week, the ECB is set to cut rates for the fourth time this year. Weak data (besides this week) and inflation at target have opened for discussions on whether a 50bp cut is appropriate. We think it will certainly be discussed, but ECB will ultimately go for 25bp, and guide that they are open to bigger cuts later, subject to incoming data. We expect a similar cut from the SNB bringing the Swiss policy rate to just 0.75%.

In the US, the November CPI release will draw most attention. We expect core inflation has slowed down slightly, which would support our call for another rate cut from the Fed in December. In China, we will keep an eye on the Central Economic Work Conference, where the top leadership discusses and lays out economic priorities for the next year. Elsewhere in Asia, we will look out for the Tankan business survey; key input for the next Bank of Japan meeting, where we expect another rate hike.

Week Ahead – Central Bank Bonanza Begins, US CPI Eyed Too

- Last policy decisions of 2024 to shape market mood

- RBA, BoC, SNB and ECB are on the agenda

- US CPI report to be crucial too as Fed undecided

RBA to hold rates, but will it turn less hawkish?

The Reserve Bank of Australia will kick off the central bank bonanza next week, announcing its decision on Tuesday. Unlike its major peers, the RBA has not yet embarked on a rate-cutting cycle as policymakers remain wary about inflation despite the recent decline.

Governor Michelle Bullock said underlying inflation is still “too high” in recent remarks and doesn’t expect for it to return to target sustainably until 2026. Unless that outlook changes, the RBA isn’t about to ditch its ‘higher for longer’ stance anytime soon, and investors don’t see a rate cut before April 2025.

Even April was considered a bit optimistic prior to the GDP data that showed Australia’s economy grew by slightly less than forecast in the third quarter. The soft reading undermines Bullock’s claim about the level of excess demand in the economy. Monthly CPI was also weaker than expected in October, and further downside surprises could see the timing of the first rate reduction being brought forward again.

This may prompt Bullock and other board members to sound a little more upbeat about inflation as they keep rates at 4.35%. A dovish lean could push the Australian dollar below the four-month lows brushed on the back of the GDP print.

Aussie traders will also be keeping an eye on the November employment report due on Thursday, as well as CPI and PPI figures out of China on Monday, and November trade figures on Tuesday.

Whilst the Chinese data will be important in gauging the health of the world’s second largest economy, a bigger market mover might be any new announcement on stimulus, as political leaders meet next week to set out Beijing’s economic plan for 2025.

Will the BoC cut by 50 bps again?

In sharp contrast to the RBA, the Bank of Canada has been taking the lead in the global race to cut rates. The BoC has slashed rates four times this year, the last being a hefty 50 basis points. But investors are split if another double cut is likely in December.

Both headline and underlying measures of inflation ticked up in October, and the jobs market is rebounding after a soft patch. On the other hand, growth remains subdued and businesses are downbeat about the outlook, especially now that US president-elect Donald Trump is threatening tariffs of 25% on all Canadian imports.

Another consideration for the BoC is the widening yield spread with the US, as the Fed has not been as aggressive and may even go on pause soon. With the Canadian dollar already down more than 6% this year, policymakers may not want to risk lowering rates significantly below US ones.

Hence, Wednesday’s decision of whether to cut by 25 bps or 50 bps will likely be a very close call, and the risks to the loonie are symmetrical.

Dollar awaits CPI data as Fed meeting looms

The December policy decision is also proving to be a bit of a dilemma for the Federal Reserve. Judging by the latest rhetoric, most Fed officials appear to be in favour of a 25-bps reduction at the December 17-18 meeting but are not ready to commit just yet.

The CPI report for November out on Wednesday will be the last major piece of the jigsaw for policymakers ahead of the meeting, so a strong market reaction is almost guaranteed.

The headline rate of CPI is expected to edge up from 2.6% to 2.7% y/y, while core CPI is projected to stay unchanged at 3.3% y/y. Barring any upside surprises, the Fed will probably be inclined to lower rates and keep the January meeting as an option for pausing.

The producer price index will follow on Thursday.

The US dollar is consolidating after hitting two-year highs in November. Any unwelcome acceleration in the month-on-month rates could recharge the bulls to drive the dollar index to fresh highs.

SNB set for first cut under dovish new Chairman

The Swiss National Bank has trimmed rates three times since March when it became the first of the major central banks to ease policy. It’s widely expected to cut again in December, which will be new Chairman Martin Schlegel’s first decision since taking over from Thomas Jordan in October.

However, the size of the cut is less certain, and the choice between 25 bps or 50 bps was looking like a coin toss until the October CPI data came along. Switzerland’s annual CPI rate increased by 0.7%, falling short of the 0.8% expected. The odds for a 50-bps cut subsequently rose to more than 60%.

Dovish remarks by Schlegel have further boosted the chances for a larger reduction, after he repeatedly floated the idea of reintroducing negative interest rates if necessary.

Should the SNB opt for a 50-bps cut on Thursday, the Swiss franc could resume its downfall against the US dollar. However, if policymakers stick with a 25-bps increment, the franc could extend its latest recovery.

ECB unlikely to go big in December

Soon after the SNB announces its policy settings, the European Central Bank is expected to hit the headlines with its rate decision. A rate cut is almost certain, with economists predicting a 25-bps reduction. However, some investors think that a 50-bps cut is on the cards, although the odds have fallen in recent days to about 15%.

This has helped the euro to stabilize a little against the US dollar as ECB policymakers, including President Lagarde, have been careful not to pre-commit to a particular rate path amid a pickup in inflation in the euro area.

This has helped the euro to stabilize a little against the US dollar as ECB policymakers, including President Lagarde, have been careful not to pre-commit to a particular rate path amid a pickup in inflation in the euro area.

Nevertheless, a weak economy and renewed political uncertainty in both France and Germany have some traders betting that the ECB will have to be a lot more aggressive with its policy easing in the coming months.

However, it’s unlikely that the ECB will change its stance just yet and if it cuts rates by 25 bps as forecast on Thursday, the euro may not move much unless there is some unexpectedly dovish language by Lagarde in her post-meeting press briefing on Thursday that spurs a fresh selloff.

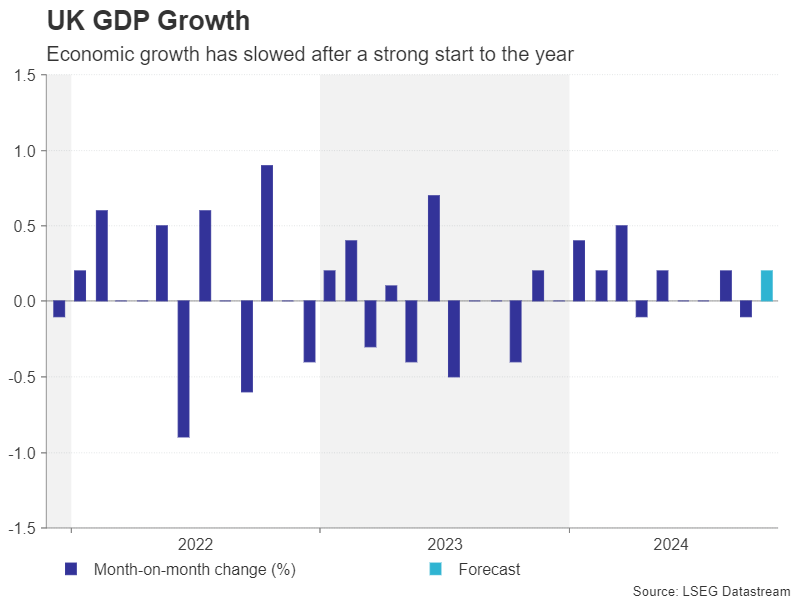

Pound rebounds ahead of UK data

Across the channel, the uncertainty over the UK economic outlook has also risen, mainly on the back of the Labour government’s budget. The tax and spend budget has been widely perceived as boosting inflation, limiting the scope for the Bank of England to cut interest rates. And whilst it does include measures that could lift growth, in the immediate term, the British economy appears to have stagnated.

GDP numbers for October will therefore be closely watched on Friday for signs that growth is coming out of the doldrums.

Although sterling has recouped a decent portion of its recent losses against the greenback, stronger-than-expected growth data could help it extend the gains.

Elsewhere, the yen might be sensitive to any revisions to Japan’s Q3 GDP print on Monday and any surprises in Friday’s quarterly Tankan business survey amid ongoing speculation about whether or not the Bank of Japan will hike rates at its December meeting.

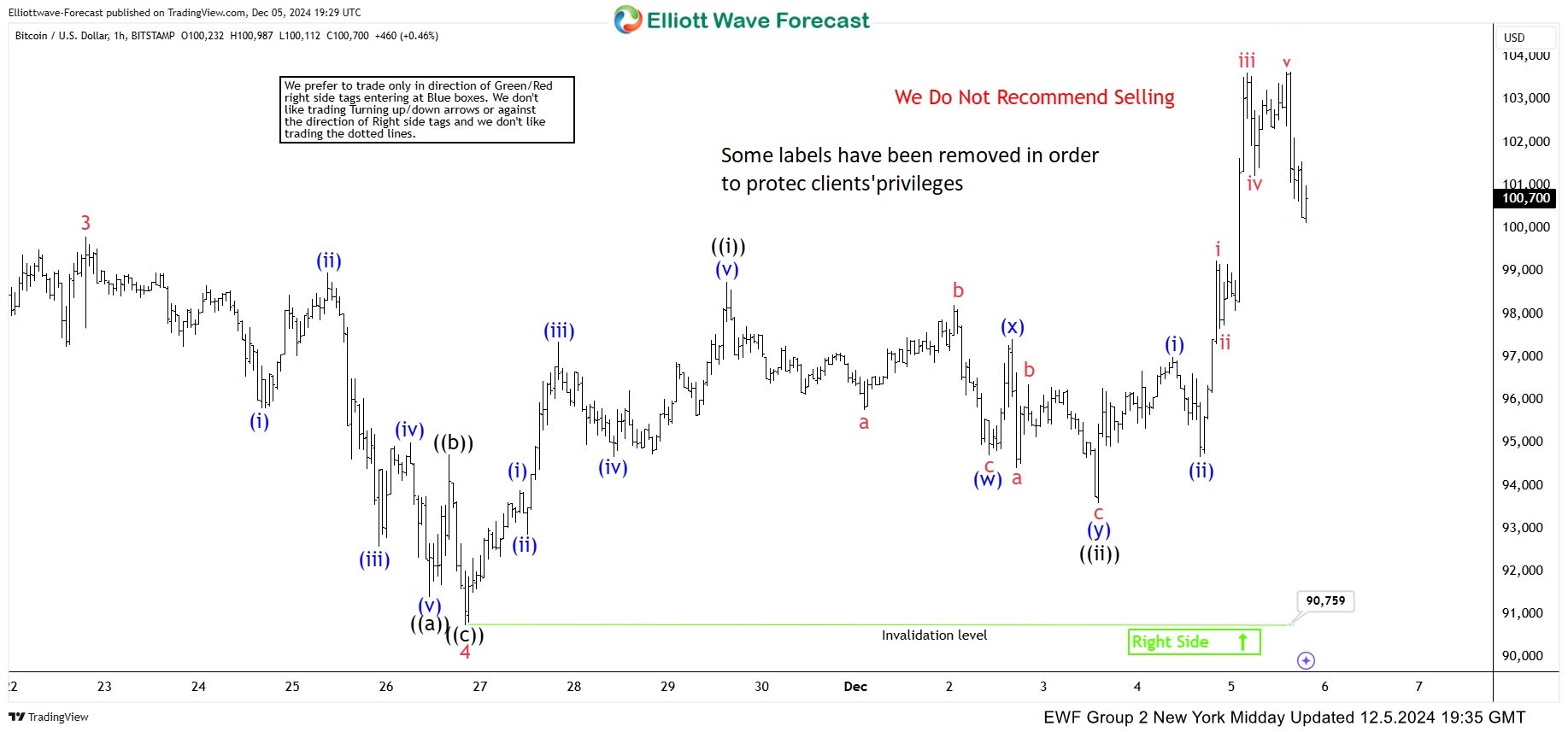

BTCUSD Made Rally Toward New All-Time Highs After Double Three Pattern

Hello fellow traders. In this technical article we’re going to take a look at the Elliott Wave charts charts of Bitcoin BTCUSD published in members area of the website. Our members know BTCUSD is showing impulsive bullish sequences in the cycle from the 50186 low. Recently, it made a clear three-wave correction. The pull back completed as Elliott Wave Double Three pattern and made rally toward new highs as expected. In this discussion, we’ll break down the Elliott Wave pattern and forecast.

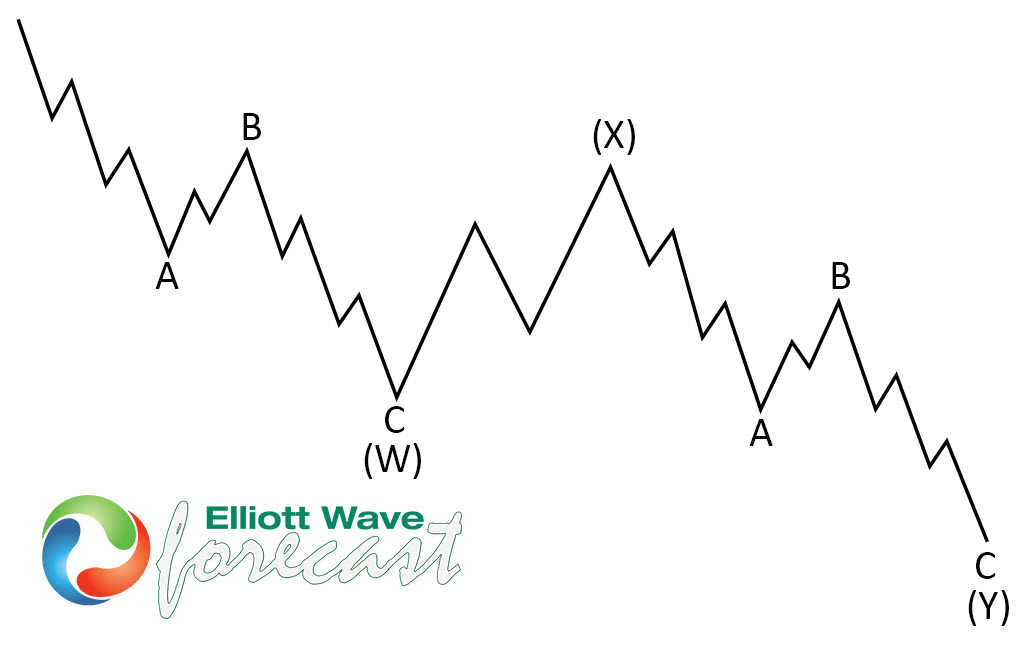

Elliott Wave Double Three Pattern

Double three is the common pattern in the market , also known as 7 swing structure. It’s a reliable pattern which is giving us good trading entries with clearly defined invalidation levels.

The picture below presents what Elliott Wave Double Three pattern looks like. It has (W),(X),(Y) labeling and 3,3,3 inner structure, which means all of these 3 legs are corrective sequences. Each (W) and (Y) are made of 3 swings , they’re having A,B,C structure in lower degree, or alternatively they can have W,X,Y labeling.

BTCUSD Elliott Wave 1 Hour Chart 12.03.2024

BTCUSD is giving us pull back against the 90818 low. The structure of this pullback is still incomplete at the moment, showing 5 swings down from the peak. The first leg, shows a clear 3-wave structure a,b,c red, followed by a 3-wave bounce in (x) blue. Wave (y) blue should also form a 3 waves pattern. We miss another swing down to complete clear 7 swings pattern in ((ii)) pull back. We advise against selling $BTCUSD and instead favor the long side. While the price stays above 4 red low: 90818, we expect to see further rally toward new highs.

BTCUSD Elliott Wave 1 Hour Chart 12.03.2024

Bitcoin found buyers as expected. The crypto completed Double Three pattern and reacted strongly. Eventually we got a break toward new highs. Now, intraday pull backs should ideally keep finding buyers as far as 90759 pivot holds.

Sunset Market Commentary

Markets

In the absence of important eco data and no new market moving political developments (in France or elsewhere), European market enjoyed a brief pauze after recent swings. European traders simply joined the countdown to the US payrolls which, alongside the November CPI data scheduled for next week, were supposed to provide last key input for the Fed December 18 policy meeting. After last months’ near-stagnation, mainly driven by hurricanes and strikes, US job growth rebounded by a close-to-expectations 227k. However, data from the previous two months also were upwardly revised by a net 56k. Goods producing sectors added 34k. Private services jobs grew 160k. Wage growth also was slightly stronger than expected with average hourly earnings at 0.4% M/M and 4.0% Y/Y. However evidence from the separate consumer survey was far less inspiring. With a 193k decline in the workforce, a 355k decline in employment, a rise in the unemployment rate from 4.1% to 4.2% and a decline in the participation rate from 62.6% to 62.5%.

Markets apparently focused more on the content of the consumer survey and see the rise in the unemployment rate as supporting the case for an additional 25 bps rate cut at the December meeting. US yields in a ‘logical’ steepening move decline between 6.5 bps (2-y) and 2.5 bps (30-y). Money markets raised the expectations for a 25 bps December Fed cut to almost 90%, from about 70% yesterday evening. German/EMU yields fell prey to modest spill-over effects from what happened in US and switched small gains for small losses. German yields currently decline between 3.0 bps (2-y) and 2.5 bps (10-y). EUR/USD briefly jumped well north of to the 1.06 (top near 1.0630) but were almost immediately undone with the pair currently again trading near unchanged levels (1.0585 area). The yen again outperforms with USD/JPY breaking further below the 150 mark (149.5). Equities apparently feel OK with the ‘confirmation’ that there is room for gradual further Fed easing. The S&P (+0.35%) is touching a new all-time record. The EuroStoxx 50 also enjoys the (relative political) calm, adding 0.45%.

News & Views

Hungary’s Orban has threatened vetoing the European Union’s next long-term budget if the European Commission does not distribute the some €20bn EU funds it is withholding over concerns related to the rule of law. The Hungarian president said that “the funds we don’t receive in 2025 and 2026 we’ll have to receive in 2027 and 2028” or he will torpedo the seven-year budget that outlines EU spending from 2028. Not having access to these resources was among the reasons for rating agency Moody’s to cut the outlook for Hungary’s credit rating last week. Hungary is marching towards parliamentary elections in 2026 and Orban’s party is trailing the pro-EU opposition party Tisza. Copy pasting the 2022 script with huge spending is given overstretched public finances a no-go. Sticking to the budget, Hungary’s AKK released its 2025 financing plan today. Gross bond issuance amounts to HUF 12.838bn. HUF 4123bn is needed to plug the cash deficit with the remaining part consisting of maturities (HUF 8043 bn) and switches and buybacks. Funding relies more heavily on the HUF institutional market next year, with HUF 3992 bn planned in HGB auction issuance. The AKK plans to issue HUF 200 bn in green bonds. It keeps the 30% upper bound on the share of FX debt for 2025. An international FX bond with a volume of up to €2.5bn is planned for the first half. This will include a €1bn green Eurobond and Chinese yuan-denominated panda bonds. The forint today again underperformed other regional currencies, probably on the ongoing rift between PM Orban and the EU.

Canadian employment grew 50.5k in November, double the 25k expected and picking up from the 14.5k in October. Employment gains were concentrated in full-time work (+54k). The bulk comes on the account of the public sector (45k), offsetting the meaning of the headline beat. The unemployment rate rose to the highest level since September 2021 (6.6%) though came together with an uptick in the participation rate to 65.1%. The employment rate steadied after falling for six months at 60.6%. The hourly wage rate missed the bar sharply, 3.9% vs 4.7% expected and down from 4.9%. The Canadian dollar loses ground against the US dollar, which just suffered a minor setback from the US Payrolls as well. USD/CAD trades around 1.409. The market-implied probability for a back-to-back 50 bps rate cut at the December 11 Bank of Canada meeting rose to 80% after the report.

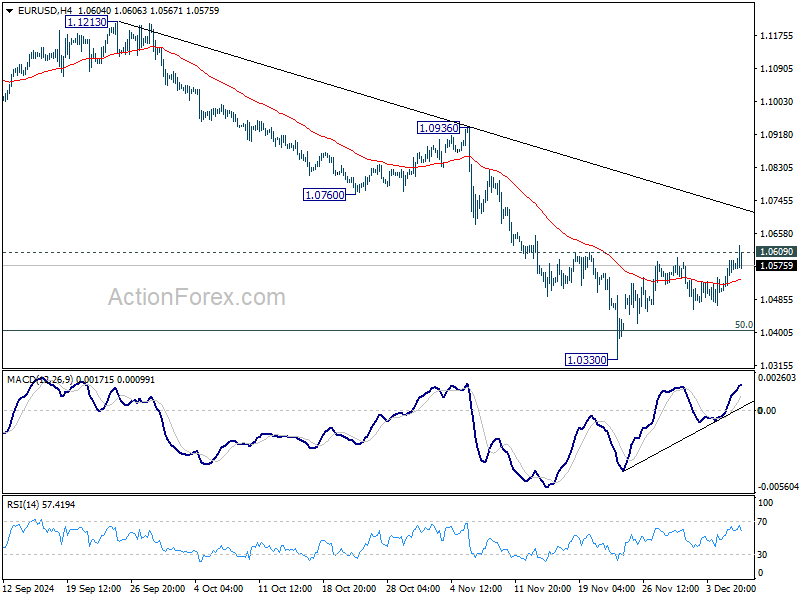

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0533; (P) 1.0562; (R1) 1.0615; More...

EUR/USD breached 1.0609 resistance briefly but quickly retreated. Intraday bias remains neutral first. On the upside, firm break of 1.0609 resistance will resume the rebound from 1.0330 to 55 D EMA (now at 1.0729). But strong resistance could be seen there to limit upside. On the downside, break of 1.0330 will resume the fall from 1.1213. Also, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.