Sample Category Title

Asian Market Update: Uncertainty Remains On US Healthcare Legislation As White House Calls The Vote For Friday

Uncertainty remains on US healthcare legislation as White House Calls the vote for Friday

US Session Highlights

(US) INITIAL JOBLESS CLAIMS: 258K V 240KE; CONTINUING CLAIMS: 2.00M V 2.04ME

BHP.AU Escondida Union spokesperson: no wage agreement reached last night; likely to revert to old contract; no more wage talks are scheduled - press

F Guides Q1 $0.30-0.35 v $0.45e - filing ahead of analyst event

(US) Rep Brady (R-TX): There is 95% agreement on healthcare bill as of this morning; there is still work to do to get the necessary votes

(US) Mar Kansas City Fed Manufacturing Activity: 20 v 14e

US markets on close: Dow flat, S&P500 -0.1%, Nasdaq -0.1%

Best Sector in S&P500: Real Estate

Worst Sector in S&P500: Healthcare

Biggest gainers: PVH +8.5%, TRIP +2.7%, CBT +2.7%, NKE +2.7%, AAL +2.6%

Biggest losers: FTR -8.1%, ACN -4.5%, CNC -4.0%, FDX -3.4%, HRB -2.5%

At the close: VIX 13.1 (+0.3 pts); Treasuries: 2-yr 1.28% (+2bps), 10-yr 2.42% (+2bps), 30-yr 3.03% (+2bps)

US movers afterhours

MU: Reports Q2 $0.90 v $0.81e, R$4.65B v $4.65Be; Guides Q3 $1.43-1.57 v $0.88e, R$5.2-5.6B v $4.65Be; +10.3% afterhours

SPWH: Reports Q4 $0.25 v $0.27e, R$221.4M v $229Me;Guides Q1 -$0.08 to -$0.06 v -$0.03e, R$150-155M v $160Me, SSS -11% to -9%; -6.6% afterhours

OXM: Reports Q4 $0.63 (adj) v $0.91e, R$261M v $267Me; -8.7% afterhours

GME: Reports Q4 $2.38 v $2.29e, R$3.05B v $3.12Be; Guides initial FY17 $3.10-3.40 v $3.72e, SSS -2% to +2%; -11.3% afterhours

Politics

(US) CNBC's Harwood: Freedom Caucus source sees "no way" the healthcare bill passes tomorrow morning

(US) CBO releases new scoring on amended GOP healthcare bill; shows less savings over next 10 years than March 13th estimate but will maintain same coverage losses

(US) White House chief strategist Bannon: Feel good about progress made in Congress negotiations - CNN

(US) Congressman Chris Collins (R-NY): Message from White House is that if healthcare legislation does not pass, it will move on to tax reform and keep Obamacare in place; Freedom Caucus attaching amendment that will keep 0.9% Medicare surcharge tax on high earners and repeal "essential benefits" requirements.

(US) House Speaker Ryan: We intend on passing the bill tomorrow (does not respond to whether he thinks GOP has the votes).

(US) House Minority leader Pelosi: Time to pull the plug on healthcare bill; Latest CBO score shows it is crueler to Medicaid recipients

Asia Key economic data:

(JP) JAPAN MAR PRELIMINARY PMI MANUFACTURING: 52.6 V 53.3 PRIOR (7th month of expansion)

(JP) Japan Jan Final Leading Index: 104.9 v 105.5 prelim; Coincident Index: 115.1 v 114.9 prelim

(NZ) NEW ZEALAND FEB TRADE BALANCE (NZ$): -18M V +180ME (8th month of deficit)

(KR) South Korea Mar Consumer Confidence: 96.7 v 94.4 prior

(SG) Singapore Feb Industrial Production M/M: -3.7% v +1.2%e; Y/Y: 12.6% v 10.0%e

Asia Session Notable Observations, Speakers and Press

Asian indices are mixed, tracking late-day caution in US markets as GOP leadership pulled the vote on US healthcare reform to hold more meetings with holdout Freedom Caucus. Late in the evening, White House announced it was ending the negotiations and scheduled the vote for Friday afternoon. There is still lack of clarity on whether Speaker Ryan and Pres Trump were able to appease the hard-right opponents with an amendment that does away with "essential benefits" clause while preserving the support of the moderates. White House has also reportedly threatened Congressional lawmakers that they would have to live with Obamacare if the bill does not pass, as it plans to shift its focus to tax reform.

Political risk continues to weigh on overall sentiment as investors second-guess market conviction of pro-business policies coming down the pike amid the apparent GOP infighting. Vix spiked up to close above 13 for the first time since early January after the healthcare vote was pulled, even though Treasuries were slightly lower across the curve. In FX, USD strengthened throughout the Asia session with risk-on USD/JPY lifting some 50pips off the lows above 111.40 once the talks on healthcare broke for the night. GBP/USD was also a notable mover to the downside, as BOE's Vlieghe suggested rates may not necessarily rise after the latest CPI data saw inflation hit above BOE target for the first time since Dec 2013, stating evidence of wage growth would be needed while attributing the CPI boost to GBP devaluation.

Also of note, BOJ Gov Kuroda deflected expectations of adjustment to long-term yield target, noting inflation recovery is still lacking strength and risks to economy and prices are still skewed to downside. Recall the latest BOJ policy statement was somewhat more optimistic on inflation achieving 2% objective in the medium term, and Kuroda said he would be prepared to discuss long-term rate target adjustment if inflation picks up. In Japan's economic data, March preliminary PMI remained in expansion for the 7th straight month at 52.6, down from 53.3 in Feb. New Export orders and Backlog both increased but at a slower pace, while Output Prices declined in a change of trend. Local economist said "latest PMI data again point to a Japanese manufacturing economy expanding at a decent clip and new order books remain in solid growth territory."

New Zealand trade numbers were a miss with 8th month of deficit against expected return to surplus. Exports missed consensus at 4.01B v 4.20Be, while Imports were in line around 4.0B. Shipments to China were strong, rising 6.3% y/y as exports to US declined again.

China

(CN) China Vice Premier Zhang: China long-term positive economic fundamentals unchanged

(CN) PBoC Beijing branch announces measures to control home risks; To tighten mortgage rules on some divorced couples

(CN) US financial press warns about risks to China banking liquidity on expected maturity of CNY1.53T in negotiable certificate of deposits (NCDs)

Japan

(JP) BOJ Gov Kuroda: Easing program has been working smoothly; Will discuss LT rate target if inflation picks up

Australia/New Zealand

(NZ) RBNZ: Feb new residential mortgage lending fell 14% to NZ$4.38B - press

Korea

(KR) South Korea Fin Min Yoo: North Korea appears all set for nuclear test - Korean press

Asian Equity Indices/Futures (01:00ET)

Nikkei +0.9%, Hang Seng -0.2%, Shanghai Composite -0.1%, ASX200 +0.8%, Kospi -0.2%

Equity Futures: S&P500 +0.3%; Nasdaq +0.3%; Dax +0.4%; FTSE100 +0.2%

FX ranges/Commodities/Fixed Income (01:00ET)

EUR 1.0760-1.0785; JPY 110.85-111.40; AUD 0.7610-0.7640; NZD 0.7000-0.7035

Apr Gold -0.3% at $1,244/oz; May Crude Oil +0.4% at $47.89/brl; May Copper -0.7% at $2.63/lb

(CN) PBoC skips open market operations for today's session v injecting CNY30B yesterday; PBoC drains net CNY30B this week v drained CNY120B prior

(CN) PBOC SETS YUAN MID POINT AT 6.8845 V 6.8856 PRIOR; 3rd straight stronger setting

(JP) Japan investors bought net ¥149B in foreign bonds v sold ¥696B in prior week; Foreign investors sold net ¥580B in Japan stocks v sold ¥723B in prior week

(AU) Australia MoF (AOFM) sells A$600M in 1.75% 2020 Bonds; avg yield: 2.0563%; bid-to-cover: 6.25x

Asia equities / Notables / movers by sector

Consumer discretionary: 1958.HK BAIC Motor Corp +1.7% (FY16 result); CKF.AU Collins Foods -8.8% (Deutsche Bank cuts rating); 3865.JP Hokuetsu Kishu Paper Co +3.9% (annual result speculation)

Financials: 2628.HK China Life Insurance -1.7% (annual result); NAB.AU National Australia Bank +1.3%, ANZ.AU ANZ Bank +2.0% (raises mortgage rate); 8354.JP Fukuoka Financial +4.5% (SMBC raises rating)

Industrials: DOW.AU Downer EDI -25.1% (trading resumes); 6324.JP Harmonic Drive Systems -1.3% (Okasan cuts rating)\

Technology: 6502.JP Toshiba Corporation +7.8% (govt plans full review of chip unit sale)

Materials: 2600.HK Aluminum Corporation of China -2.1%, 914.HK Anhui Conch Cement -3.0% (annual result); 2168.HK Yingde Gases -3.8% (profit warning); SYR.AU Syrah Resources +5.8% (maintains budget); FMG.AU Fortescue Metals -0.6% (to repay debt); EVN.AU Evolution Mining -4.0% (block trade)

Energy: 1165.HK Shunfeng Photovoltaic International -4.9% (FY16 guidance); 883.HK CNOOC +4.2% (annual result)

Utilities: 2380.HK China Power International -3.9% (annual result)

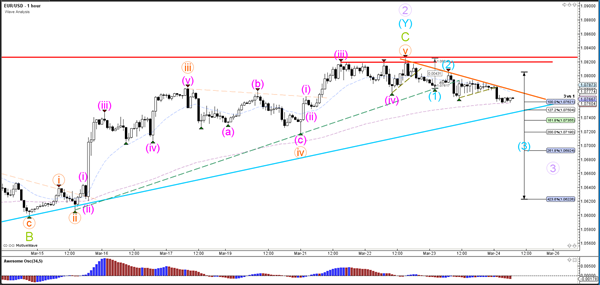

EUR/USD Breaks Rising Wedge And Approaches Channel Support

Currency pair EUR/USD

The EUR/USD broke below the rising wedge chart pattern (red/green) trend lines without breaking the resistance top (red), which means that the wave 2 (purple) has not been invalidated as yet. The EUR/USD is now testing the next support (blue) level which is part of a larger uptrend channel (blue/red lines).

The EUR/USD could be a in a bearish wave 3 (blue) if price manages to break below the support trend line (blue). A break above the resistance trend line (orange) could see price retest the resistance zone (red).

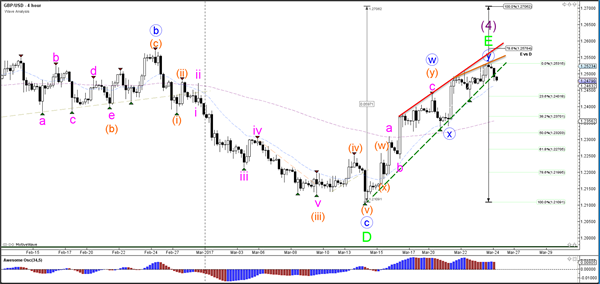

Currency pair GBP/USD

The GBP/USD is trying to break below the support trend line (dotted green). The bearish turn could complete the wave E (green) and start a bearish breakout. The wave E (green) could also become expanded (another WXY correction) which is why I am keeping an eye on the Fibonacci levels to see if price will bounce strongly at one of the Fibs.

The GBP/USD broke above resistance (dotted orange) and completed wave C (orange). Price in the meantime has broken below support (dotted green) and could be in a wave 3 (orange) aiming for the wave 3 vs 1 Fibonacci targets.

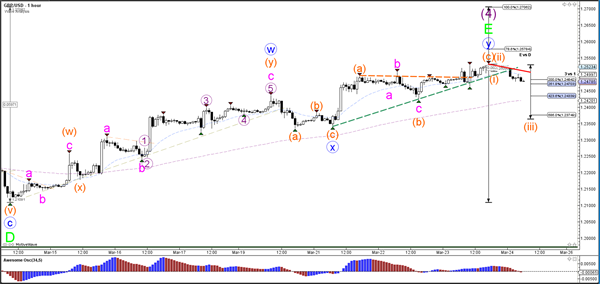

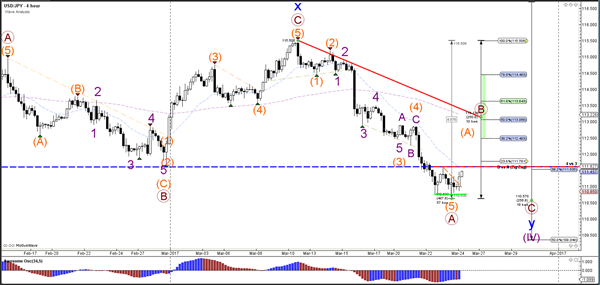

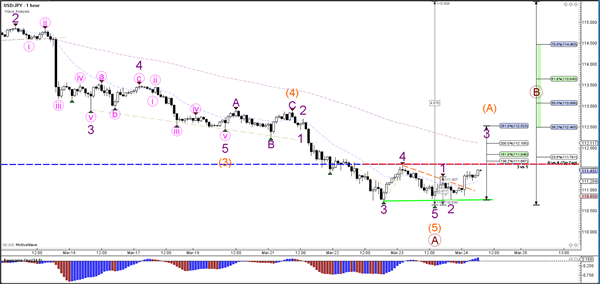

Currency pair USD/JPY

The USD/JPY completed a 5th wave (orange) within a larger bearish ABC zigzag (brown), which could take price down to the 50% Fibonacci retracement support level of wave 4 vs 3 (purple).

The USD/JPY managed to post a lower low to complete the expected waves 5 (orange/purple). In the meantime, price has broken above a resistance trend line (dotted orange) and is approaching the previous bottom which has now become a resistance level (dotted red). A break above that could see a wave 3 (purple) within wave A (orange).

US Stock Markets Fell Back Slightly

Market movers today

In the US, PMI manufacturing for March is due out today. Given that Markit PMI was significantly below the level suggested by ISM and Empire in February, one could be tempted to call for an increase in PMI manufacturing in March in order to close part of this gap. However, it is worth keeping in mind that manufacturing activity has been increasing since last summer, partly on the back of a recovery in the oil market. Without further increases in the oil price, the given level is probably as high as we are going to get. Also, there are signals of a deceleration in economic growth in Q2 this year, which should also cap growth in the manufacturing sector. Thus, we expect manufacturing PMI to stay around the current level. This continued improvement in manufacturing should also spill over into core capital goods orders for February, which is due out today as well. Both new orders and value of shipments bottomed out in mid-2016 and we expect them to move higher in coming months.

Today, PMI figures for the euro area are due out. Overall, we expect PMIs to remain strong as we saw rising Ifo expectations in February and a moderate increase in the ZEW expectations in March, which has been good at leading the PMI figures historically. However, it should be noted that economic expectations have risen after the good news from the PMIs and other economic surveys, making it less likely that we will see further upside surprises. This also reflects that data moves in cycles and that some moderation is likely after a period of strong data.

There are no market movers in Scandi today.

Selected market news

The announcement of the EUR233bn take-up on the fourth and final ECB TLTRO II had limited market impact.

US stock markets fell back slightly as yesterday's vote in the US House of Representatives on the American Health Care Act (Trumpcare), which is to replace Obamacare, was postponed.

New home sales in the US climbed to a seven-month high of 592,000 in February from 558,000 in January, which indicates a modest effect on the US residential real estate market from the recent increase in borrowing costs.

In the UK, retail sales figures were released yesterday. Although retail sales excluding fuels came out strong in February (+1.3% m/m), they have been weak in recent months. Looking at 3M/3M, retail sales have declined 1.25%. Overall, retail sales data supports our view that growth is slowing, as higher consumer prices hit real wage growth and hence private consumption.

AUD/USD: Aussie Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the AUD declined 0.55% against the USD and closed at 0.7627.

LME Copper prices declined 3.7% or $78.5/MT to $5790.5/MT. Aluminium prices rose 0.2% or $3.0/MT to $1913.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7614, with the AUD trading 0.17% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7592, and a fall through could take it to the next support level of 0.7569. The pair is expected to find its first resistance at 0.7652, and a rise through could take it to the next resistance level of 0.7689.

Looking ahead, traders would keep a close watch on Australia’s HIA new home sales and private sector credit data, both for February, slated to release next week.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

EUR/USD: Economic Recovery In The Euro-Zone Steadily Firming: ECB Economic Bulletin

For the 24 hours to 23:00 GMT, the EUR declined 0.12% against the USD and closed at 1.0780.

In economic news, the Euro-zone's flash consumer confidence index improved more-than-anticipated to a level of -5.0 in March, compared to a level of -6.2 in the previous month, while markets were expecting the index to rise to a level of -5.9.

Separately, the European Central Bank (ECB), in its economic bulletin report, stated that economic recovery in the Euro-zone continues to pick up pace and the recent incoming data point towards robust momentum in the first quarter.

Elsewhere, in Germany, the GfK consumer confidence index unexpectedly fell to a level 9.8 in April, defying market anticipations for it to remain steady at 10.0, as consumers remained concerned about the impact of rising inflation on their incomes.

The US dollar traded higher against most of its major currencies, after data indicated that new home sales in the US jumped 6.1% on a monthly basis, to a level of 592.0K in February, rising by the most since July 2016, suggesting that housing market recovery continued to gain momentum. New home sales registered a revised reading of 558.0K in the prior month, while investors had envisaged it to climb to a level of 564.0K. On the other hand, the nation's initial jobless claims unexpectedly rose to a level of 258.0K in the week ended 18 March, hitting its highest level in two months, compared to a revised reading of 243.0K in the prior week. Markets participants expected a fall to a level of 240.0K.

Meanwhile, the Federal Reserve Bank of San Francisco President, John Williams, stated that the economy is in a good place and added that he expects the central bank to raise interest rates three or four times this year.

In the Asian session, at GMT0400, the pair is trading at 1.0768, with the EUR trading 0.11% lower against the USD from yesterday's close.

The pair is expected to find support at 1.0750, and a fall through could take it to the next support level of 1.0732. The pair is expected to find its first resistance at 1.0795, and a rise through could take it to the next resistance level of 1.0822.

Moving ahead, investors will closely monitor the flash Markit manufacturing and services PMIs for March across the Euro-zone, slated to release in a few hours. Additionally, the US preliminary Markit manufacturing PMI for March and flash durable goods orders data for February, scheduled to release later today, will pique significant amount of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

GBP/USD: UK’s Retail Sales Sharply Rebounded In February

For the 24 hours to 23:00 GMT, the GBP rose 0.34% against the USD and closed at 1.2516, on upbeat British retail sales data.

Data revealed that Britain's retail sales rebounded more-than-anticipated by 1.4% on a monthly basis in February, soothing fears of weaker consumer spending as the nation prepares to leave the European Union. Market expectation was for retail sales to rise 0.4%, compared to a revised drop of 0.5% in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.2489, with the GBP trading 0.22% lower against the USD from yesterday's close.

The pair is expected to find support at 1.2455, and a fall through could take it to the next support level of 1.2422. The pair is expected to find its first resistance at 1.2526, and a rise through could take it to the next resistance level of 1.2564.

Going ahead, market participants will focus on UK's BBA mortgage applications for February, slated to release in a few hours.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

USD/JPY: Japan’s Flash Nikkei Manufacturing PMI Declined To A 3-Month Low Level In March

For the 24 hours to 23:00 GMT, the USD declined 0.24% against the JPY and closed at 111.02.

In the Asian session, at GMT0400, the pair is trading at 111.28, with the USD trading 0.23% higher against the USD from yesterday's close.

The Japanese Yen lost ground, after data indicated that Japan's preliminary Nikkei manufacturing PMI dropped to a level of 52.6 in March, expanding at its slowest pace in three months as growth in new orders and output slowed. The PMI had recorded a level of 53.3 in the previous month.

Early morning data showed that the nation's final leading economic index came in at 104.9 in January, while the preliminary figures had indicated a revised level of 104.8. Meanwhile, the nation's final coincident index dropped less than initially estimated to a level of 115.1 in January, after registering a revised reading of 115.5 in the prior month and compared to a fall to a level of 114.9 in the flash print.

The pair is expected to find support at 110.77, and a fall through could take it to the next support level of 110.26. The pair is expected to find its first resistance at 111.62, and a rise through could take it to the next resistance level of 111.96.

Looking ahead, investors would await Bank of Japan's summary of opinions report coupled with Japan's jobless rate, national consumer price index, flash industrial production, retail trade and large retailers' sales data, all slated to release next week.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

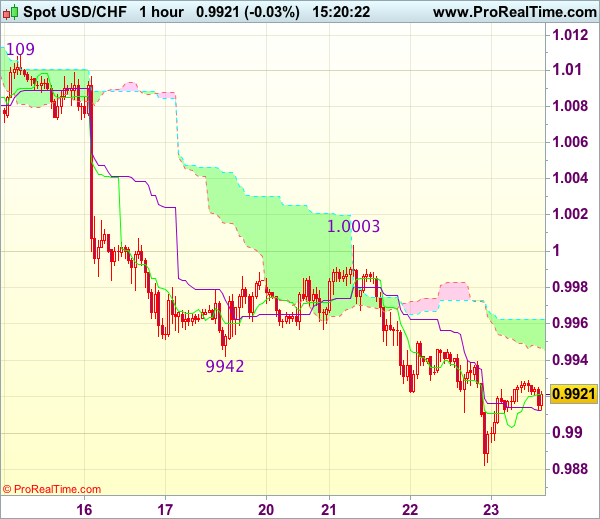

Trade Idea : USD/CHF – Sell at 1.0000

USD/CHF - 0.9954

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9944

Kijun-Sen level : 0.9936

Ichimoku cloud top : 0.9936

Ichimoku cloud bottom : 0.9917

Original strategy :

Sell at 1.0000, Target: 0.9900, Stop: 1.0035

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0000, Target: 0.9900, Stop: 1.0035

Position : -

Target : -

Stop : -

As the greenback has continued edging higher after rebounding from 0.9882, retaining our view that further consolidation above this week’s low at 0.9882 would be seen and recovery to 0.9980 cannot be ruled out, however, reckon upside would be limited to 0.9992 (38.2% Fibonacci retracement of 1.0171-0.9882) and resistance at 1.0003 should hold, bring retreat later. Below support at 0.9912 would suggest the rebound from 0.9882 has ended, bring another test of this level, break there would extend recent decline to 0.9850 but loss of downward momentum should prevent sharp fall below 0.9825-30.

In view of this, we are looking to sell dollar on further subsequent rebound as resistance at 1.0003 should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

USD/CHF: Swiss Franc Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.15% against the CHF and closed at 0.9932.

In the Asian session, at GMT0400, the pair is trading at 0.9954, with the USD trading 0.22% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9922, and a fall through could take it to the next support level of 0.9891. The pair is expected to find its first resistance at 0.9972, and a rise through could take it to the next resistance level of 0.9991.

Amid a lack of economic releases in Switzerland today, investors would direct their attention to Switzerland’s ZEW expectations survey, UBS consumption indicator, KOF spring economic forecast report, all set to release next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

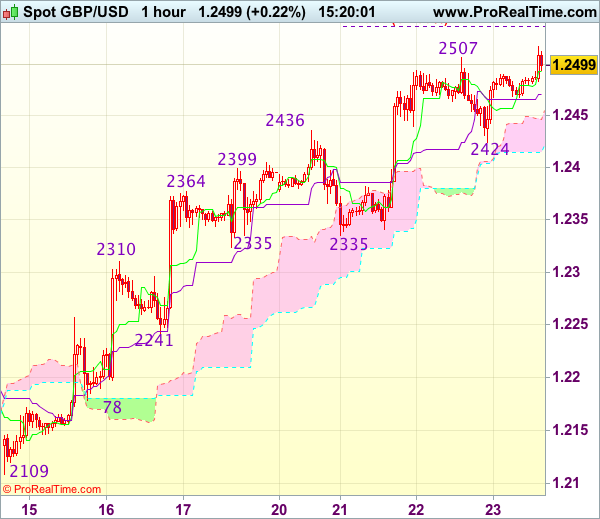

Trade Idea : GBP/USD – Stand aside

GBP/USD - 1.2477

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2499

Kijun-Sen level : 1.2497

Ichimoku cloud top : 1.2472

Ichimoku cloud bottom : 1.2424

Original strategy :

Buy at 1.2425, Target: 1.2540, Stop: 1.2390

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has retreated after marginal rise to 1.2531 yesterday, suggesting consolidation below this level would be seen and pullback to 1.2450, then towards support at 1.2424 cannot be ruled out, however, a break below latter level is needed to signal top is formed, bring retracement of recent upmove to 1.2400 and then towards 1.2370 but price should stay well above indicated strong support at 1.2335.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Above said resistance at 1.2531 would signal recent upmove from 1.2109 is still in progress and may extend further gain to 1.2550 but loss of upward momentum would limit upside to previous chart resistance at 1.2570 and price should falter below 1.2600-10, risk from there has increased for a retreat to take place later.