Sample Category Title

European Major PMI Manufacturing Data Beats Expectations to 6-Year Highs

Notes/Observations

- US healthcare vote back on; Trump said to have issued an ultimatum to leave Obamacare in place unless they pass new healthcare bill; political risk weighing on market participation

- Major European Manufacturing PMI extend further into expansion territory to multi-year highs

Overnight:

Asia:

- Japan Mar Preliminary Manufacturing PMI registers its 7th month of expansion (52.6 v 53.3 prior)

- BOJ chief Kuroda says "no reason" to withdraw stimulus now

Europe:-

- BOE Vlieghe stated that higher inflation did not mean any interest rate hike. Needed to see evidence of strong wage growth before considering voting for a rate rise

Americas:

- Fed's Kaplan (moderate, voter): 3 rate hike this year is reasonable baseline; could be faster or slow but not looking for a pause in hikes now

- Fed's Kashkari (dove, dissenting vote): - We're coming up short on our inflation mandate; Fed has powerful tools if inflation rises too fast

Energy:

- State Dept to approve Keystone pipeline permit Friday

Summary of Trump Healthcare Bill:

- Vote has been postponed to Friday morning (no set time)

- White House and GOP leadership said to have presented a 'final offer' on healthcare bill to the Freedom Caucus to either accept or reject. Freedom Caucus yet to give formal answer to this offer. White House reportedly offered to remove essential benefits from plans on the individual market

- Trump said to have issued an ultimatum to House Republicans that he will leave Obamacare in place unless they pass new healthcare bill - financial press

- White House: Freedom Caucus discussion was positive; does not say deal reached; moderate members will come to white house for talks; Trump has not asked house speaker Ryan to delay healthcare vote; ultimately expects to have votes to pass healthcare bill; confident the bill will pass in the morning

- President Trump: the healthcare bill vote is going to be very close; we have a chance

- Freedom Caucus Chair Meadows: still hopeful will get agreement on health care bill; Freedom Caucus has made reasonable requests. still not enough votes to pass health bill; plans to reach out to moderate Republicans in House to try to reach agreement; optimistic common ground will be found with enough Senators to pass a bill

- House Republican Leader McCarthy: there are not enough votes currently to pass healthcare bill; will start debate on house floor on healthcare bill on Friday morning

- White House spokesman Spicer: Trump is looking forward to a vote on the healthcare bill; have seen the numbers rising for 'yes' votes

Economic Data

- (NL) Netherlands Q4 Final GDP Q/Q: 0.6% v 0.5%e; Y/Y: 2.5% v 2.3%e

- (FR) France Q4 Final GDP Q/Q: 0.4% v 0.4%e; Y/Y: 1.1% v 1.2%e

- (FR) France Mar Preliminary Manufacturing PMI (beat): 53.4 v 52.4e (6th month of expansion), Services PMI: 58.5 v 56.1e, Composite PMI: 57.6 v 55.8e

- (CZ) Czech Mar Business Confidence: 13.1 v 15.2 prior; Consumer Confidence: 6.3 v 5.8 prior

- (DE) Germany Mar Preliminary Manufacturing PMI (beat): 58.3 v 56.5e (28th month of expansion and highest since Apr 2011), Services PMI: 55.6 v 54.5e, Composite PMI: 57.0 v 56.0e

- (EU) Euro Zone Mar Preliminary Manufacturing PMI (beat): 56.2 v 55.3e (45th month of expansion and highest since Apr 2011), Services PMI: 56.5 v 55.3e, Composite PMI: 56,7 v 55.8e

- (UK) Feb BBA Loans for House Purchase (miss): 42.6K v 44.9Ke

- Fixed Income Issuance:

- (ZA) South Africa sold total ZAR650M vs. ZAR650M indicated in I/L 2029, 2033 and 2050 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 09:20 GMT)

Indices [Stoxx50 -0.3% at 3,442, FTSE -0.1% at 7,336, DAX flat at 12,035, CAC-40 -0.3% at 5,017, IBEX-35 -0.4% at 10,288, FTSE MIB -0.2% at 20,134, SMI -0.2% at 8,613, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European equity indices are trading lower in the morning session as market participants remain jittery ahead of the highly anticipated vote on US President Trump's healthcare bill; Banking stocks generally lower across the board; shares of Allianz the laggard in the Eurostoxx after receiving an analyst downgrade; Commodity and mining stocks trading higher in the FTSE 100 as copper prices consolidate around intraday highs; Oil stocks lower as oil prices consolidate near intraday lows.

Upcoming notable scheduled US earnings (pre-market) include Finish Line, and REX American Resources.

Equities (as of 09:15 GMT)

- Consumer Discretionary: [IG Design IGR.UK +9.3% (trading update)]

- Financials: [Credit Suisse CSGN.CH +0.8% (revises Q4 Net loss, annual report), Allianz ALV.DE -1.4% (analyst downgrade)]

- Healthcare: [Biotest BIO.DE -8.8% (ImmunoGen has elected not to exercise its late stage co-development option for the US-Market with Biotest's antibody-drug conjugate (BT-062)), PureTech Health PRTC.UK +4.4% (Novartis licensing agreement)]

- Industrials: [FACC FACC.AT +0.1% (prelim FY16 results)]

- Technology: [Smiths Group SMIN.UK +3.9% (H1 results)]

Speakers

- ECB's Praet (Belgium, chief economist) reiterated view that Euro Area was doing better and that deflation risk was gone. Reiterated view that talks of exit from accommodative measures was premature as labor market had more slack than what jobs data showed. Italy's low growth showed acute structural problems and any return to ITL currency (Lira) for Italy would not solve the country's problem

- France Fin Min Sapin reiterated view that conditions were in place for budget deficit to GDP ratio to move below 3.0% in 2017

- Germany Fin Min Schauble reiterated view that pumping more money into Europe was the wrong message

- EU's Juncker reiterated view that UK Brexit bill will be around £50B

- EU's Dombrovskis reiterated EU Commission view that Italy needed to bring its debt level down; country needed to ensure 0.2% budget correction

- Italy Fin Min Padoan stated that its domestic economic and inflation situation was improving

- Sweden Central Bank (Riksbank) Business Survey: Industrial activity stronger than expected. Companies saw the coming six months economic activity would remain good, although there was some concern over political developments abroad

- Moody's affirmed New Zealand sovereign rating at AAA; outlook stable

Currencies

- FX price action and risk outlook hinging on President Trump looming healthcare vote. Political risk weighing on participation as time was running out to get votes for the Republican plan to repeal and replace "Obamacare"

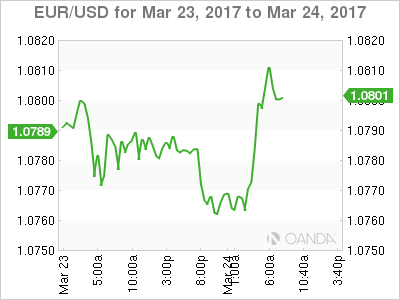

- EUR/USD was back above 1.08 level aided by the major European Manufacturing PMI as it extended further into expansion territory to multi-year highs

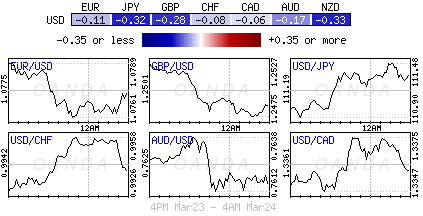

- GBP/USD was slightly lower in quiet trade hovering below the 1.25 level.

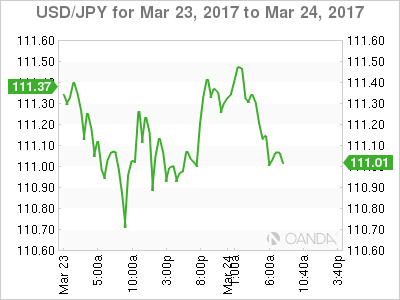

- USD/JPY moved off Thursday's low to stay above the 111 level in the session.

Fixed Income:

- Bund futures trade at 159.98 down 4 ticks retracing the bulk of the earlier losses with stronger preliminary PMI data out of Europe coming ahead of estimates with the highest reading recorded since April 2011. Resistance remains at 160.45 followed by 160.66. Support moves to 159.41 then contract low of 158.73.

- Gilt futures trade at 126.36 down 4 ticks, off the 126.05 session low, with weakness in Equities pushing futures higher during the session. Support moves to 125.80 followed by 125.47. Resistance moves to 126.85 then 127.35 followed by 127.89. Short Sterling futures trade flat to 1bp with Jun17Jun18 spread widening to 23/23.5Bp.

- Friday's liquidity report showed Thursday's excess liquidity rose to €1.336B a rise of €7B from €1.329T prior. Use of the marginal lending facility rise to €283M from €232M prior.

- Corporate issuance saw no deals priced with weekly issuance at $20.8B at the low end of analysts estimates.

For the week ending Mar 22nd Lipper US fund flows reported IG net inflows $5.2B bringing YTD inflows to €35.1B, High Yield Bonds saw inflows of $736M bringing YTD outflows to €5.69B.

Looking Ahead

- (US) House of Representatives vote on Healthcare Bill (no set time)

- 06:00 (EU) Daily Euribor Fixing

- 06:00 (FR) France Debt Agency (AFT) announces upcoming Bill/Oat auctions

- 06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to leave Key 7-Day Auction Rate unchanged at 10.00%

- 07:00 (UK) DMO to sell combined £2.0B in 1-month, 3-month and 6-month bills (£0.5B, £0.5B and £1.0B respectively)

- 07:30 (IS) Iceland cancels Bonds

- 07:30 (IN) India Weekly Forex Reserves

- 07:45 (US) Daily Libor Fixing

- 08:00 (CL) Chile Feb PPI M/M: No est v 0.9% prior

- 08:00 (US) Fed's Evans speaks at Community Development Event

- 08:00 Russia Central Bank (CBR) Gov Nabiullina to hold post rate decision press conference

- 08:30 (US) Feb Preliminary Durable Goods Orders: 1.3%e v 2.0% prior; Durables Ex-Transportation: 0.6%e v 0.0% prior; Capital Goods Orders (Non-defense ex aircraft): +0.5%e v -0.1% prior, Capital Goods Shipments (non-defense/ex-aircraft): +0.3%e v -0.4 prior; Ex-Defense: No est v 1.5% prior

- 08:30 (CA) Canada Feb CPI M/M: 0.2%e v 0.9% prior; Y/Y: 2.1%e v 2.1% prior; Consumer Price Index: No est v 129.5 prior

- 08:30 (CA) Canada Feb CPI Common Core Y/Y: No est v 1.3% prior; CPI Medium Core Y/Y: No est v 1.9% prior; CPI Trim Core Y/Y: No est v 1.7% prior

- 08:30 (US) Fed's Bullard to speak to Economic Club of Memphis

- 09:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond issuance

- 09:15 (UK) Baltic Dry Bulk Index

- 09:30 (BR) Brazil Feb Current Account: $0.0Be v -$5.1B prior; Foreign Direct Investment (FDI): $4.8Be v $11.5B prior

- 09:45 (US) Mar Preliminary Markit Manufacturing PMI: 54.7e 54.2 prior

- 10:00 (MX) Mexico Jan Retail Sales M/M: -0.6%e v -1.4% prior; Y/Y: 5.1%e v 9.0% prior

- 11:00 (EU) Potential European sovereign ratings after the close

- (CY) Cyprus Sovereign Debt to Be Rated by Moody's

- (DK) Denmark Sovereign Debt to be rated by Moody's

- (SA) Saudi Arabia Sovereign Debt to be rated by Moody's

- (LU) Luxembourg Sovereign Debt to be rated by DBRS

- 13:00 (FR) France Feb Net Change in Jobseekers: -10.0Ke v +0.8K prior; Total Jobseekers: 3.457Me v 3.468M prior

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 13:00 (IT) Pope Francis meets EU Leaders before Rome Summit

- 15:00 (CO) Colombia Jan Economic Activity Index Y/Y: 0.6%e v 1.0% prior

- 15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to cut Overnight Lending Rate by 25bps to 7.00%

All Eyes on Congress as Trump Issues Ultimatum

- Is Trump's ultimatum on healthcare win win for markets?

- Three Fed officials scheduled to appear as markets risk under-pricing rate hikes this year;

- Eurozone PMIs suggest ECBs difficulties turning to how to manage tightening cycle in two tier eurozone.

Financial markets are in wait and see mode on Friday although there is an underlying sense of optimism, after Donald Trump dug in his heals on the revised healthcare plan and declared Congress should accept the changes or live with Obamacare, paving the way for government to refocus its attention on tax reform.

With the vote looking very close right now, Trump has taken quite a big gamble because an inability to pass the new healthcare bill through a Republican controlled Congress when most are in agreement that Obamacare should be scrapped, will cast doubts on what other promises he will be unable to deliver on. That said, should the gamble pay off then in the short term it could reflect well on his ability to get things done, the only downside being that similar tactics may not be so effective in the future.

Still, as far as markets are concerned, the ultimatum that Trump has delivered should be good news. Trump has told lawmakers that a rejection of the plan will mean Obamacare stays in place and attention will turn to tax reform, one of the more stimulative policies that has driven the market rally since the election. While the sell-off earlier in the week suggested that an inability to get the healthcare plan passed will be bad for markets, this latest ultimatum should be win win for the markets, as either way it seems Trump is moving onto tax reform. The only risk now is that Trump suffers a backlash that could jeopardise his tax reform and fiscal stimulus plans.

With the vote expected later in the day or even over the weekend if we see further delays, there may be some hesitancy in the markets as this could strongly influence how they reopen next week. That said, there are other things to focus on today, with three Fed officials scheduled to speak including William Dudley, Charles Evans and James Bullard, the first two of which are both voting members on the FOMC this year. The Fed has struck a less hawkish tone since it raised interest rates last week which has triggered some profit taking on those positions that built up into the meeting. Ultimately, policy makers still appear to see two more rate hikes this year, something the markets are in danger of under-pricing after the correction over the last week. It will be interesting to see whether today's speakers continue to tread carefully when asked about the rate outlook.

It's been a relatively quiet morning in Europe so far although we are seeing the euro make some decent gains after PMI data suggested the regions recovery is gathering pace. Faster job growth, higher business activity and rising inflationary pressures - largely driven by higher commodity prices and weaker euro - are all positive signs for the region and will likely ask questions of the ECB later in the year. The ECB will reduce its monthly purchases as of next month in a move that it insisted is not tapering and yet, markets now appear to be expecting another reduction later this year, if not a rate hike. I still think the ECB needs to take a cautious approach here as the region continues to be split between those with a strong economy, low unemployment and inflationary pressures and those at the other end of the spectrum, with others somewhere in the middle. Managing the two or even three tier eurozone is going to be the next great challenge for the central bank. It seems that no matter what it does from here, there is going to be dissent.

Make or Break for Trump’s Reflation Trade

Friday March 24: Five things the markets are talking about

Markets remain in "wait and see mode" - Can Trump's self-proclaimed "infamous" negotiation skill push through his health care bill?

This bill is viewed as a potential bellwether for his ability to impose his economic and political agenda.

Thus far, delayed is better than defeat. Investors regard today's healthcare bill vote as "the" test for the Trump presidency. The GOP pulled the healthcare bill vote late yesterday afternoon to hold more meetings with the holdout Freedom Caucus. However, there is still lack of clarity in whether the White House has been able to appease the hard-right opponents with an amendment that does away with "essential benefits" clause while preserving the support of the moderates.

Net result, Trump's reflation trade has struggled this month as the administration remains far from delivering on pro-growth policies that boosted stocks and the dollar.

On the radar, more Fed officials are lined up for today, including Fed Bank of St. Louis President James Bullard, who will speak to the Economic Club of Memphis.

1. Japanese equities lead gains in Asia Pacific, Europe neutral

Despite losing -1.3% on the week, Japan's Nikkei has ended up +0.9% overnight and has moved decisively away from the previous session's two-month lows. The broader Topix index has also recovered some of this week's slide as the yen (¥111.18) halted its longest rally outright in six-year.

In Hong Kong, stocks have eked out marginal gains as investors wait for corporate earnings and today's U.S healthcare bill vote. The benchmark Hang Seng index added +0.1%.

In China, stocks have rallied for a second week as infrastructure spending has offset liquidity fears. The blue-chip CSI300 index rose +0.8%, while the Shanghai Composite Index added +0.6%.

In Europe, equity indices are trading lower as the market remains nervous ahead of U.S healthcare vote. Financials are leaning on Eurostoxx, while commodity and mining stocks are trading higher in the FTSE 100.

Overnight, U.S. stock futures have rallied (+0.2%) now that Republicans said the House was ready to vote on an amended health-care bill.

Indices: Stoxx50 -0.3% at 3,442, FTSE -0.1% at 7,336, DAX flat at 12,035, CAC-40 -0.3% at 5,017, IBEX-35 -0.4% at 10,288, FTSE MIB -0.2% at 20,134, SMI -0.2% at 8,613, S&P 500 Futures +0.2%

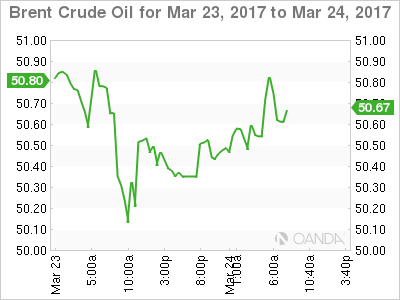

2. Saudi's cut oil supply to the U.S

Oil prices have edged a tad higher overnight, supported by a fall in Saudi exports to the U.S, however, the market remains under pressure from a supply glut.

Brent crude futures at +$50.69 per barrel are up +13c or +0.3% from yesterday's close. U.S. West Texas Intermediate (WTI) crude futures are up +18c, or +0.4%, at +$47.88 a barrel.

On the week, Brent is heading for a weekly fall of about -2%, while WTI is off -1.8%.

Support has come from the Saudi's who indicated that crude exports to the U.S would fall by around -300k bpd between February and March.

Note: Saudi exports are competing with U.S shale production, which is up about +9% in the past 18-months.

Currently, the market believes that OPEC needs to extend its production curbs beyond June or makes bigger cuts or oil prices are at risk of falling much further.

Note: Despite the OPEC-led cuts that began three months ago, Brent has fallen by over -13% now that other producers have stepped up and filled the gap.

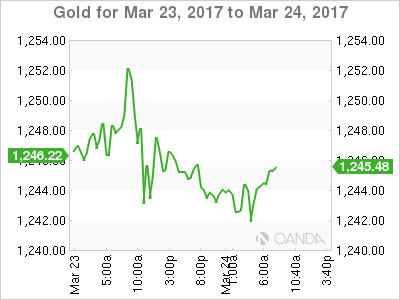

Gold prices have edged lower overnight (-0.2% at +$1,242.31 per ounce) on the back of a stronger dollar. Today's healthcare vote defeat will affect Trump's efforts to cut taxes and boost infrastructure and should drive more investors to gold as a safe haven.

3. Global yields need guidance

With market risk sentiment being somewhat fragile given the uncertainty on whether Trump can deliver on stimulus expectations has been supporting U.S treasuries and bunds prices this month.

In the U.S, 10-year yields rose above +2.6% earlier this month and reached a two-year high as investors anticipated the Fed would raise short-term interest rates. They did last week, but its signal of a "gradual" path of tightening policy has debt product better bid. U.S 10's are trading at +2.43%. German bunds are trading just above +0.5%.

In the U.K, yields on 10-year gilts have backed up +1 bps to +1.19% after data showed yesterday showed that U.K retail sales rose beating expectations.

Elsewhere, the Reserve Bank of New Zealand (RBNZ) held rates steady Wednesday (+1.75%) as expected and maintains a neutral policy stance. In its policy statement, officials expressed more concern over housing inflation while reiterating that the exchange rate should depreciate more to achieve balanced growth.

The yield on Aussie 10's are little changed at +2.75%.

4. Dollar waiting for vote outcome

Currently, FX price action and risk outlook continues to hinge on President Trump's healthcare bill vote this afternoon (no time set).

The EUR is trading back above the psychological € 1.0800 handle (€1.0810) supported by today's EU Manufacturing PMI print (see below) exceeding expectations and rallying further into expansion territory to new multi-year highs.

The pound is a tad lower (£1.2483) in quiet trading. Next week PM Theresa May is expected to begin divorce proceedings from the EU.

USD/Yen has moved off yesterday's lows to stay above the psychological ¥111.00 handle. It's the first day that the 'mighty' dollar has rallied in eight days.

5. Eurozone Composite PMI Highest in Six Years

Data this morning shows that the Eurozone grew at the fastest pace in six-years in Q1. The PMI for the eurozone's manufacturers and service providers rose to 56.7 in March from 56.0 in February.

With new orders also surging and businesses hiring additional workers at the fastest pace in a decade, the three monthly average rally may suggest a faster rate of expansion is likely to be sustained over coming months. There were also signs the pickup in activity is fueling inflationary pressures, with prices charged by businesses rising at the fastest rate in six years.

Data like this will have fixed income traders raising their expectations that the ECB should consider moderating its stimulus measures later this year. Market expectations were for a drop.

Spot Gold Eases from Fresh High

Spot Gold eases from fresh high at $1253 (the highest traded since 28Feb) after Thursday's close in red that signaled broader bulls might be running out of steam.

Overbought slow stochastic on daily chart is reversing lower and supports idea of extended correction.

Downside attempts remain limited for now and keep pivotal supports at $1239/37 (base of thick hourly cloud / broken Fibo 61.8% of $1263/$1195 descend) intact.

However, extended dips through $1239/37 should not exceed next strong support at $1229 (daily Kijun-sen / 10/20SMA bull-cross) to keep broader bulls from $1195 trough intact for eventual push towards targets at $1260/63 (200SMA / 27 Feb peak).

Res: 1246; 1253; 1258; 1260

Sup: 1241; 1239; 1237; 1229

Daily Technical Analysis

EURUSD

The EURUSD had another indecisive movement yesterday. The bias remains neutral in nearest term. Price is still trending higher in short term, moving above the EMA 200 and a trend line support as you can see on my H1 chart below but from a daily chart perspective 1.0830 – 1.0873 resistance area also remains well-respected and good place to sell with a tight stop loss. Key intraday support is seen around 1.0725 located around the EMA 200 and the trend line support. A clear break and daily/weekly close below that area would end the current short term bullish trend. On the upside, a clear break and daily/weekly close above 1.0873 would activate my bullish mode next week targeting 1.1000 region.

GBPUSD

The GBPUSD had a bullish momentum yesterday topped at 1.2531. Price is still moving confidently inside the bullish channel and above the EMA 200 as you can see on my H1 chart below. The bias remains bullish in nearest term testing 1.2570 – 1.2600 region. Immediate support is seen around 1.2475. A clear break below that area could lead price to neutral zone in nearest term testing 1.2420 but only a clear break back below the EMA 200 (1.2380) would interrupt the current bullish phase. Overall I remain neutral.

USDJPY

The USDJPY was indecisive yesterday but overall still able to maintain its bearish bias. The bias is bearish in nearest term testing 110.25/00 region. As you can see on my daily chart below, price slipped below 111.30 key support but still struggling around the daily EMA 200 located around 111.00. So from a longer term daily chart perspective we may need to wait until price convincingly close below 111.30/00 to expect a deeper movement to the downside. On the other hand, any sustained pullback above 111.30 could trigger further bullish pressure testing 111.80 or higher.

USDCHF

The USDCHF didn’t make significant movement yesterday. There are no changes in my technical outlook. The bias remains neutral in nearest term but price is still in a bearish phase after fell below the bullish channel as you can see on my H4 chart below targeting 0.9870 – 0.9800 support area. Immediate resistance is seen around 0.9975. A clear break above that area could trigger further bullish pullback testing 1.0015. Overall I remain neutral.

FTSE 100 – 55SMA Is Holding For Now But Upside Attempts Limited, Top Of Hourly Cloud Is Key

FTSE is struggling to break above two-day congestion despite today's opening higher, as near-term technicals are weak and overall sentiment ahead of start of Brexit negotiations remains negative.

The index is down around 1.5% for the week until now, with negative near-term outlook also driven by strong pound.

Pullback from fresh record high at 7444 was so far contained by 55SMA, with subsequent consolidation being unable to extend recovery and generate bullish signal for now.

Near-term price action is moving within thick hourly cloud (spanned between 7256 and 7297) and so far holding well below pivotal barriers at 7297 (hourly cloud top) and 7310 (Fibo 38.2% of 7444/7228 pullback), break of which is needed to generate stronger bullish signal.

Long red weekly candle also weighs on the price and maintains downside pressure.

Bearish scenario requires break below 7228 (55SMA / near-term base) for confirmation and extension towards next strong supports at 7184 (Fibo 61.8% of 7024/7444) and 7169 (top of ascending daily cloud).

Res: 7283, 7897, 7310, 7324

Sup: 7259, 7228, 7184, 7169

Gold Few Selling Pressures, Silver Increasing Demand, Crude Oil Heading Downwards.

Gold Few selling pressures.

Gold has risen sharply, nearly invalidating the bearish short-term outlook. The momentum seems back to bullish. Strong resistance is located at 1263 (27/02/2017 high). Hourly support can be found at 1224.10 (16/03/2017 low). Expected to show further strengthening.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

Silver Increasing demand.

Silver rose sharply Friday, invalidating the bearish outlook linked to the previous bearish pause. Correct pullback has failed to find seller indicating test of 17.56 resistance (16/03/2017 high). Strong support is given at 16.84 (27/01/2016 low).

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

Crude oil Heading downwards.

Crude oil's bearish pressures continues despite correct bounce due to a short-squeeze. The commodity had been unable to mount a serious challenge to resistance at 49.61 (08/12/2017 low) hourly support given at 47.09 (016/03/2017 low) Expected to see deeper selling pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/CHF Moving Sideways, EUR/JPY Continued Bearish Pressures, EUR/GBP Continued Weakness But…

EUR/CHF Moving sideways.

EUR/CHF's is moving up and down. The medium-term pattern suggests us to see continued bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/JPY Continued bearish pressures.

EUR/JPY rejection at 122.88 has triggered a correction. The pair is also very volatile. Hourly support at 120.55 (17/01/2017 low) has been broken. Another support at 120.02 (08/03/2017 low) has been broken. Resistance stands at 122.88 (13/03/0217 high). Expected to show continued weakness.

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Continued weakness but...

EUR/GBP is correcting lower. Yet there is the formation of a bullish flag which suggests reversal of current weakness targeting 0.9000. Key resistance is given at 0.8854 (15/01/2017 high) and other resistance can be found at 0.8787 (13/03/20167 high). Support is located at 0.8645( 05/02/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

USD/CHF Selling Pressures Decline, USD/CAD Holding Below 1.3400, AUD/USD Bouncing Lower.

USD/CHF Selling pressures decline.

USD/CHF is declining. Hourly support is given at 0.9862 (31/01/2017 low). Key resistance can be found at a distance at 1.0344 (15/12/2016 high). Expected to show continued weakness.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Holding below 1.3400.

USD/CAD is bouncing. However a break of resistance area around 1.3400 is needed to invalidate the current short term bearish technical structure. The road seems still wideopen for larger decline. Key support is given at 1.2969 (31/01/2017 low).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Bouncing lower.

AUD/USD has failed to test the key resistance at 0.7778 (08/11/2016 high). Hourly support at 0.7664 (16/03/2017 low) has been broken. Expected to see some short-term weakness towards resistance area around 0.7500.

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Trading Within Uptrend Channel, GBP/USD Pushing Higher, USD/JPY Consolidating.

EUR/USD Trading within uptrend channel.

EUR/USD keeps on pushing higher, even though the pair is now pausing around 1.0800. A break of the upside channel would signal persistent buying pressures. Key resistance is given at a distance 1.0874 (08/12/2017 high). Strong support can be found at 1.0493 (22/02/2017 low). The technical structure suggests deeper increase towards resistance at 1.0874.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Pushing higher.

GBP/USD now lies in a short-term uptrend channel. There are rooms for further strength. Hourly resistance is located at 1.2570 (24/02/2017 high). Hourly support is given at 1.2324 (03/17/2017 low). Expected to show continued strength.

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Consolidating.

USD/JPY has failed to break key resistance given at 115.62 (19/01/2016 high) confirming persistent selling pressures. The pair has broken strong support at 111.36 (28/11/2016 low). Hourly resistance can be located at 113.57 (16/03/2017 high).

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low)