Sample Category Title

RBNZ Holds Benchmark Rate At Record Low Of 1.75%

'The RBNZ continues to see an outlook shaped by considerable uncertainty and is in no hurry to alter policy in either direction as a result. There is no change to our view. We continue to see the next move in the OCR being up, but not until mid-2018.' - Cameron Bagrie and Philip Borkin, ANZ Bank New Zealand

As markets expected, the Reserve Bank of New Zealand left its monetary policy unchanged at its March meeting on Wednesday amid high global uncertainties. The RBNZ Governor Graeme Wheeler said that policymakers would keep monetary policy loose for an extended period of time, as it might need to be adjusted in light of existing uncertainties coming mainly from the US and Europe. On Wednesday, the Monetary Policy Committee voted to hold the official cash rate at a record low of 1.75%, claiming that the current global situation was preventing inflation from reaching the Bank's target. Moreover, Wheeler said that the inflation rate would probably remain below 2% until 2019. However, some analysts suggest that inflation will reach 2% already this quarter and borrowing costs will start growing within a year. Wheeler noted that a 4% drop in the value of the Kiwi since February was 'encouraging' but added that further depreciation of it was necessary to 'achieve more balanced growth'. Back in the Q4 of 2016, New Zealand's economy expanded at a slower-than-expected pace, forcing the RNBZ to review its 2017 growth forecast. Thus, according to the Bank, annual economic growth is unlikely to rise above 3.5% this year.

GBP/USD Might Be Targeting 1.2550 Short Term

As we could see on previous Session Recap webinar, the GBP/USD perfectly rejected from POC and provided more than 120 possible pips. Another bullish sign that wee see today is Bullish SHS pattern ( Inverted Head and Shoulders) that might provide a continuation to the upside targeting 1.2550. However Retail Sales data might move the price today. On a worse than expected result the pair might drop to POC (Ema 89, ATR pivot, D L4) 1.2430-50 and then it might spike. On a better than expected data look for continuation above 1.2516 towards 1.2550 D H5/ W H4 confluence.

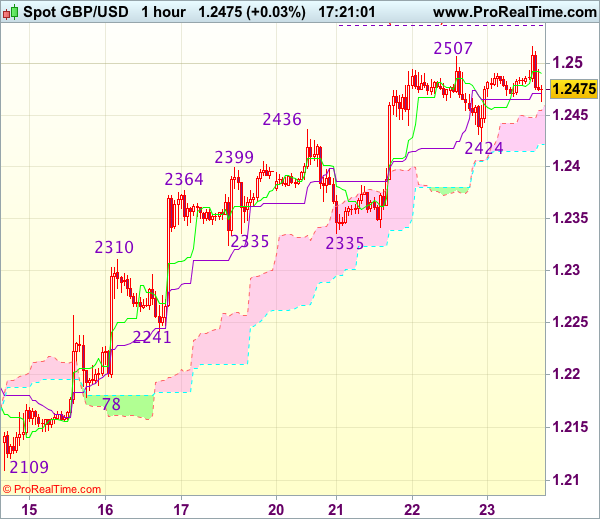

GBPUSD Hit New High Today, But Struggling Above Fibo Barrier At 1.2476, UK Data In Focus

Cable remains steady on Thursday and posted new high at 1.2514, signaling bullish continuation after Wednesday’s action ended in long-legged Doji and closed at important Fibo 61.8% barrier at 1.2476.

Technical studies are in firm bullish setup and supportive for further advance, as daily cloud contained yesterday’s dips and is going to widen in coming days, is continuing to underpin.

Focus remains at immediate targets at 1.2563/68 (Fibo 76.4% of 1.2704/1.2107 / 24 Feb high), however, close above 1.2476 is seen as initial requirement to maintain bullish bias.

Solid supports at 1.2412/04 (broken 100SMA / daily cloud top) need to contain extended dips to keep bulls intact and prevent deeper downticks.

Res: 1.2514, 1.2521, 1.2568, 1.2580

Sup: 1.2465, 1.2412, 1.2404, 1.2383

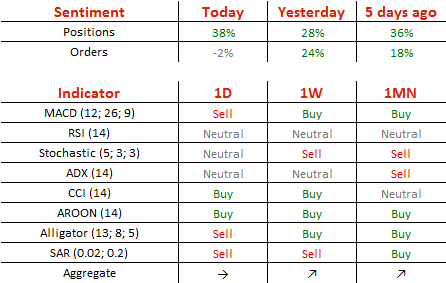

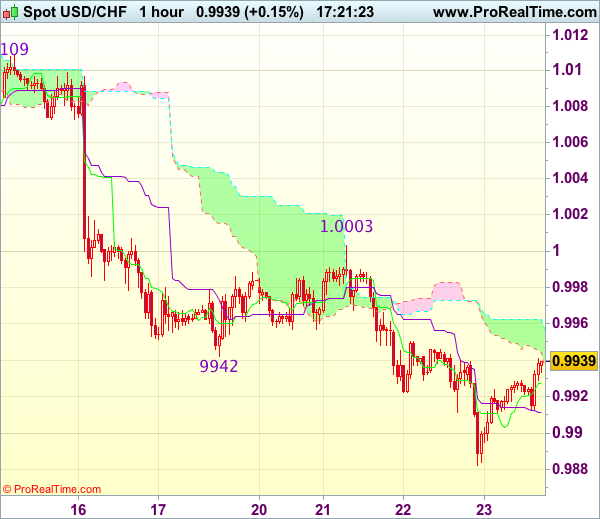

Trade Idea Update: USD/CHF – Sell at 1.0000

USD/CHF - 0.9935

Original strategy :

Sell at 1.0000, Target: 0.9900, Stop: 1.0035

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0000, Target: 0.9900, Stop: 1.0035

Position : -

Target : -

Stop : -

Dollar’s rebound after falling to 0.9882 yesterday suggests consolidation above this level would be seen and corrective bounce to 0.9945-50 cannot be ruled out, however, reckon upside would be limited to 0.9980 and renewed selling interest should emerge around 1.0003 resistance, bring another decline later. A break of said support at 0.9882 would add credence to our view that recent decline from 1.0171 is still in progress and may extend weakness to 0.9865-70 but loss of downward momentum should prevent sharp fall below 0.9850 and reckon 0.9825-30 would hold.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0000-05 should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

Trade Idea Update: GBP/USD – Buy at 1.2400

GBP/USD - 1.2472

Original strategy :

Buy at 1.2400, Target: 1.2520, Stop: 1.2365

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2400, Target: 1.2520, Stop: 1.2365

Position : -

Target : -

Stop : -

As cable has continued trading with a firm undertone, adding credence to our bullish view that recent upmove from 1.2109 is still in progress and may extend further gain to 1.2540-50 but loss of upward momentum would limit upside to previous chart resistance at 1.2570 and price should falter below 1.2600-10, risk from there has increased for a retreat to take place later.

In view of this, would not chase this move here and we are looking to buy cable on subsequent pullback as 1.2400 should limit downside. Below 1.2380-85 would defer and risk correction to 1.2350-55 but still reckon support at 1.2335 would remain intact, bring another rise later.

Trade Idea Update: EUR/USD – Buy at 1.0725

EUR/USD - 1.0781

Original strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

As the single currency retreated after rising to 1.0825 yesterday, suggesting minor consolidation below this level would be seen and pullback to 1.0750-60 cannot be ruled out, however, reckon support at 1.0719 would limit downside and bring another rise later, above indicated resistance at 1.0825-29 would extend further rise to 1.0850-60 but loss of near term upward momentum should prevent sharp move beyond 1.0880 and price should falter below 1.0900, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0719 support should limit downside and bring another rise later. Below 1.0690-00 would defer and suggest top is possibly formed, risk weakness to 1.0640 (previous resistance now support) but still reckon indicated support at 1.0600 would remain intact.

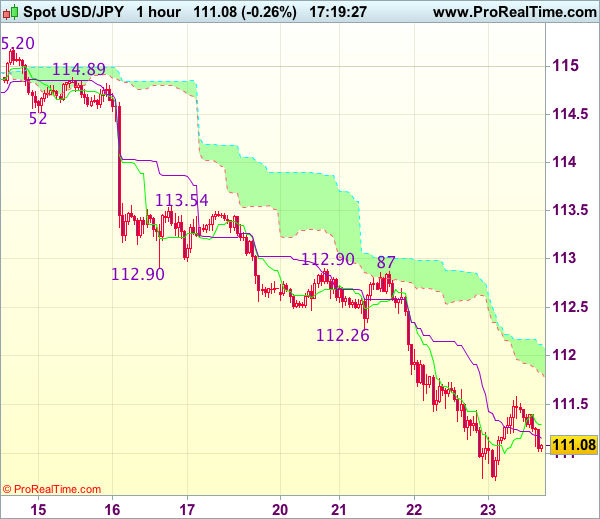

Trade Idea Update: USD/JPY – Sell at 112.00

USD/JPY - 111.12

Original strategy :

Sell at 112.00, Target: 110.80, Stop: 112.35

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.00, Target: 110.80, Stop: 112.35

Position : -

Target : -

Stop : -

As the greenback recovered after falling to 110.73, suggesting consolidation above this level would be seen and corrective bounce to 111.55-60 is likely, however, still reckon upside would be limited to 112.00-10 and bring another decline later, a break of said support at 110.73 would signal recent decline is still in progress and may extend further fall to 110.50 but near term oversold condition should prevent sharp fall below 110.20-25 and reckon 110.00 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as 112.00 should limit upside. Only above indicated previous support at 112.26 would abort and signal low is formed instead, bring a stronger rebound to 112,59 but resistance at 112,87-90 should cap upside.

EUR/USD Remains Below Weekly Resistance Level

'Current bullish rally is part of wave C, that may see more gains in sessions ahead, ideally towards the upper channel line.' – Gregor Horvat, Elliot Wave Financial Service (based on investing.com)

Pair's Outlook

On Thursday morning the common European currency against the Greenback remained below the combined resistance of the weekly R1 at 1.0814 level and the 38.20% Fibonacci retracement level at 1.0826. Although the resistance was holding, various clues were indicating that it will be broken sooner or later. In the case that unfolds, the currency exchange rate would surge to the next combined resistance cluster, which is located around the 1.0885 mark. The cluster consists of the weekly R2, 200-day SMA, the upper Bollinger band and an upper trend line of a medium term ascending channel pattern.

Traders' Sentiment

Traders remain bearish as 62% of open positions are short on Thursday. Meanwhile, 54% of trader set up orders are to sell the Euro.

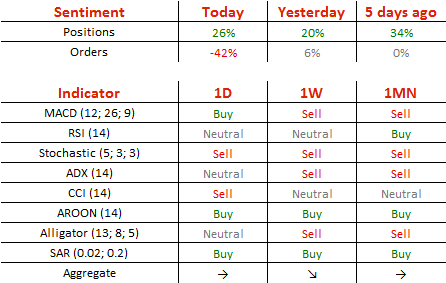

GBP/USD Takes Another Shot At Conquering 1.25

'In our view there are significant headline risks for GBP exchange rates over coming weeks and months.' – Commonwealth Bank of Australia (based on PoundSterlingLive)

Pair's Outlook

In spite of strong volatility, the Cable managed to remain relatively unchanged on Wednesday, retaining its position above the monthly PP. The Pound keeps taking advantage of the Buck's weakness due to lower US Treasury yields, therefore, another positive outcome and a surge beyond 1.25 is possible. The GBP/USD pair has only one solid resistance on its path, namely the cluster around 1.26, which could prevent the Sterling from reaching its target—the 23.60% Fibo at 1.2672. Nevertheless, today's bullish potential is likely to be very limited, as there are no strong market movers present. Meanwhile, technical studies are also unable to confirm the possibility of a positive outcome.

Traders' Sentiment

Today 63% of traders are long the Pound (previously 60%), but the share of sell orders is significantly higher, taking up 71% of the market.

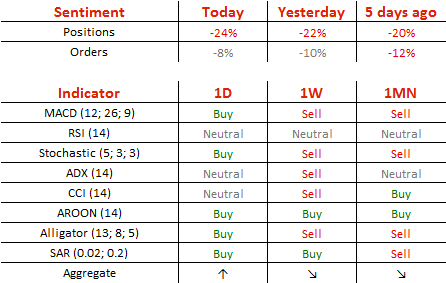

USD/JPY Attempts To Post Gains

'There is certainly a bit more bullishness in the yen over the last two weeks and we are seeing that continue.' – Silicon Valley Bank (based on Business Recorder)

Pair's Outlook

As was anticipated, the US Dollar weakened against the Japanese Yen for the seventh day in a row yesterday, but with losses slightly exceeding expectations. The given pair closed below the monthly S1, managing to retain its position above 111.00, where demand could now trigger a rebound. Technical indicators in the daily timeframe are unable to confirm this possibility, but the weekly ones are giving bullish signals. Although, technically, the Buck should now experience a bullish correction, we should not rule out the possibility of bears continuing to push the exchange rate lower, with the nearest significant support being only around 110.00.

Traders' Sentiment

There are 69% of all open positions being long today (previously 64%), while 51% of all pending orders are to sell the US Dollar.